India Fantasy Sports Market Size, Share, Trends and Forecast by Sports Type, Platform, Demographics, and Region, 2026-2034

India Fantasy Sports Market Size & Forecast 2026-2034

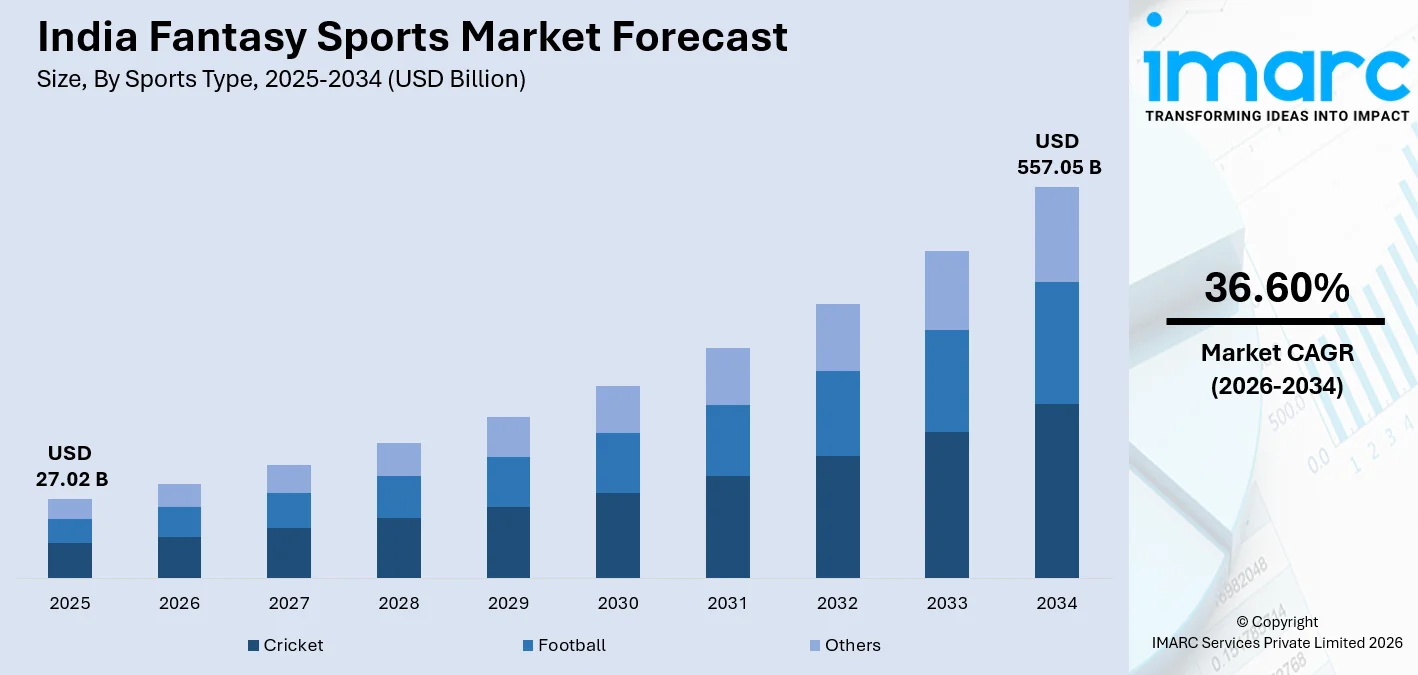

The India fantasy sports market size was valued at USD 27.02 Billion in 2025 and is projected to reach USD 557.05 Billion by 2034, growing at a compound annual growth rate of 36.60% from 2026-2034, driven by the widespread adoption of mobile internet, the cultural dominance of cricket, and a young, digitally fluent population actively engaged in competitive gaming. The Promotion and Regulation of Online Gaming Act, 2025, pivoted platforms toward free-to-play, esports, and social gaming formats, broadening audience reach. Formal recognition of esports as an official sport, multilingual content expansion, and strong venture capital inflows further reinforce the India fantasy sports market share.

To get more information on this market Request Sample

India Fantasy Sports Industry Analysis — Key Insights

- Cricket commands the sports type share at 87.4% in 2025-its dominance anchored in IPL fandom and the format's structural compatibility with fantasy team-building mechanics.

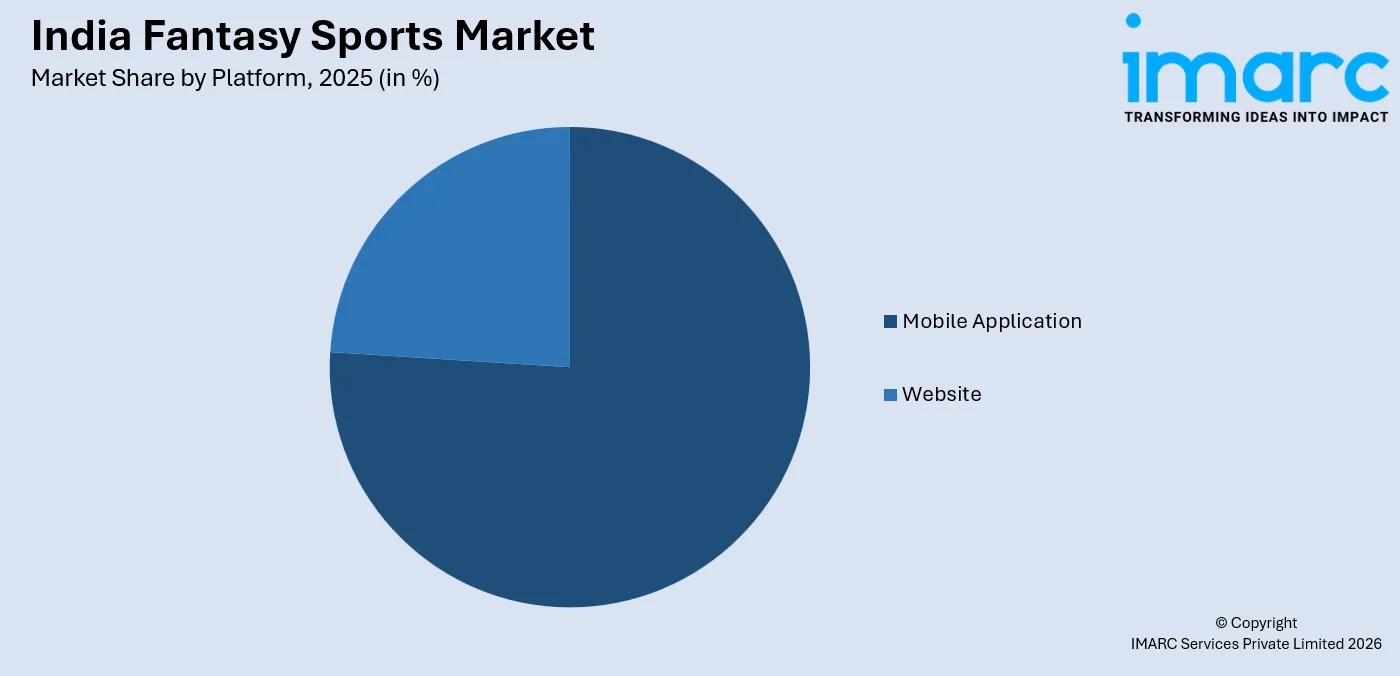

- Mobile application dominates platform at 76.2% in 2025- reflecting India's smartphone-first user behavior and seamless in-app experiences that drive daily engagement.

- 25-40 years leads demographics at 48.0% in 2025- combining digital fluency with higher disposable income and strategic-thinking engagement habits well-suited to fantasy sports.

- North India leads regionally at 37.4% in 2025-driven by deep cricket traditions, rapid urbanization, and high internet penetration in Delhi and Uttar Pradesh.

India Fantasy Sports Market Trends and Dynamic 2026

Market Trends

PROG Act and Free-to-Play Transformation Reshape Industry Architecture

The Promotion and Regulation of Online Gaming Act, signed into law in August, 2025, triggered the most significant structural disruption in India's fantasy sports history. Dream11, MPL, My11Circle, and Paytm First Games all suspended paid operations and pivoted to free-to-play formats. The sector's near-term revenue model fundamentally shifted toward advertising, sponsorship, and social engagement rather than contest entry fees, forcing platforms to innovate rapidly around non-monetary engagement loops.

AI-Driven Personalization and Data Analytics Become Competitive Differentiators

Artificial intelligence and real-time data analytics have become defining features of leading fantasy platforms, enabling personalized team recommendations, predictive player performance scores, and customized contest matchmaking at scale. In April 2025, Fantasy gaming brands, recognizing the power of AI-driven targeting, increased their IPL 2025 advertising spend by 50-60% compared to the last season. These platforms leveraged data analytics to reach sports-engaged audiences with precision during high-traffic cricket events, turning behavioral data into a key competitive asset for user acquisition and retention.

Esports Recognition Unlocks New Growth Pathways Beyond Real-Money Formats

India's formal recognition of esports as an official sport in 2025 marks a pivotal milestone for the fantasy sports adjacency. Esports included as a demonstration sport at the Khelo India Youth Games 2025, signaling government commitment to competitive gaming development. This unlocks avenues for institutional sponsorships, educational pathways, and structured league formats.

- Multi-Sport Integration: Platforms are expanding beyond cricket into kabaddi, football, and basketball, diversifying year-round engagement beyond IPL seasonality and reducing revenue concentration risk.

- Vernacular Content Expansion: Multilingual app interfaces and regional language content are widening market access to Tier 2 and Tier 3 cities, onboarding the next wave of first-time users.

- Creator-Led Community Gaming: Content creators and social media influencers are becoming primary retention engines, building community-first experiences that transcend individual tournament cycles and sustain off-season engagement.

Growth Drivers

Cricket Dominance and the IPL as the Primary Engagement Engine

Cricket's unrivaled status in Indian culture makes it the cornerstone of the fantasy sports market. The IPL serves as an annual catalyst for massive user acquisition and retention across platforms. Dream11, India's largest fantasy platform, hosted over 35 million daily active users during the IPL 2025 season, demonstrating cricket's unparalleled capacity to drive simultaneous, competitive engagement among tens of millions of fans across regions, age groups, and income levels.

Smartphone Proliferation and 5G-Enabled Real-Time Fantasy Experiences

India's digital infrastructure upgrade is enabling increasingly immersive fantasy sports experiences that were impossible on previous network generations. According to Nokia's Mobile Broadband Index (MBiT) 2025 Report, 87% of smartphones shipped in India during Q2 2025 are 5G-capable, enabling low-latency real-time fantasy gaming with instant score updates, AI recommendations, and live leaderboards. The rapid expansion of 5G across urban and semi-urban markets is compressing the technical gap between premium and mass-market user experiences.

Young, Sports-Passionate Demographics Create a Self-Renewing User Base

India's demographic structure is a powerful structural driver for the fantasy sports market. India had 591 million active gamers in FY24, with 23 million new users added that year alone, a growth rate that outpaces any other major gaming market globally. The country's vast base of sports-engaged youth, combined with rapidly rising digital fluency and growing disposable incomes among the working-age population, creates a continuously self-renewing addressable market.

- Esports Recognition as Official Sport: India's formal recognition of esports provides regulatory clarity and institutional support, unlocking new sponsorship, education, and competitive pathway opportunities for platforms.

- Rising Disposable Income: India's expanding middle class and growing employment among 25-40-year-olds increase discretionary spending on digital entertainment, directly benefiting fantasy sports engagement models.

- Digital Payments Ecosystem Maturity: UPI's widespread adoption and a growing digital-payment habit enable frictionless in-app transactions, supporting subscription, in-app purchase, and advertising revenue models across platforms.

Market Restraints

Sudden Regulatory Shift and Compliance Uncertainty: The abrupt enactment of the Promotion and Regulation of Online Gaming Act has created an unpredictable operating environment, forcing platforms to overhaul business models without adequate transition time.

Risk of User Migration to Unregulated Platforms: Banning paid fantasy sports risks driving committed users toward offshore or black-market platforms that continue offering real-money contests without legal oversight. This undermines responsible platform development, creates asymmetric competitive pressure that compliant domestic operators cannot match, and potentially erodes the user base that would otherwise drive the transition to legitimate free-to-play and esports models.

Platform Monetization Viability in Free-to-Play Models: Transitioning from entry-fee-based revenue to advertising and sponsorship dependency introduces significant financial uncertainty for platform sustainability. Free-to-play models struggle to replicate the depth of engagement and willingness to spend that real-money contests historically generated, creating a structural revenue gap that not all operators will successfully bridge during the transition period.

India Fantasy Sports Market Segmentation Analysis

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Sports Type |

Cricket |

87.4% |

2025 |

|

Platform |

Mobile Application |

76.2% |

2025 |

|

Demographics |

25-40 Years |

48.0% |

2025 |

|

Region |

North India |

37.4% |

2025 |

Sports Type Insights

Cricket — 87.4% Market Share (2025) | Leading Sports Type

Cricket's structural advantages, multiple formats (T20, ODI, Test), a dense domestic calendar, and the global spectacle of the IPL make it uniquely suited to fantasy sports mechanics. Dream11 is known for its staggering user base of over 220 million, with cricket contests commanding the overwhelming majority of platform engagement. The sport's nuanced selection dynamics, including pitch reading, player form cycles, head-to-head matchups, and impact player rules, create an endlessly replenishable pool of strategic decisions that sustain user engagement year-round.

|

Segment Breakdown Cricket (87.4%) · Football · Others |

Platform Insights

Access the comprehensive market breakdown Request Sample

Mobile application — 76.2% Market Share (2025) | Leading Platform

India's mobile-first digital ecosystem has made the smartphone app the natural home for fantasy sports platforms. 5G data usage in India surged 93% year-on-year, reaching 29,094 petabytes in December 2025 from 15,082 petabytes in December 2024, an infrastructure leap enabling real-time score updates, seamless live leaderboards, and instant team editing features that define premium mobile fantasy experiences. The convergence of affordable 5G hardware with intuitive app design continues to broaden mobile fantasy sports participation across urban and semi-urban markets.

|

Segment Breakdown Mobile Application (76.2%) · Website |

Demographics Insights

25-40 years age group — 48.0% Market Share (2025) | Leading Demographics

This cohort combines analytical thinking with digital fluency and financial capacity to engage actively in contest-driven platforms. In FY24, India recorded 148 million users making in-game purchases, including 8 million new paying players, underscoring the monetization potential of this demographic. Working professionals aged 25-40 engage with fantasy sports as a second-screen experience during live matches, integrating cricket analysis, real-time decision-making, and social competition into their sports-watching habits.

|

Segment Breakdown 25-40 Years (48.0%) · Under 25 Years · Above 40 Years |

Regional Insights

North India — 37.4% Market Share (2025) | Leading Region

North India's dominance is anchored in a sporting culture where cricket occupies a quasi-religious status, particularly during IPL and Ranji Trophy seasons. The region encompasses India's highest-density urban internet corridors: Delhi-NCR holds one of the world's most engaged cricket fanbases, while Uttar Pradesh contributes the country's single largest state user base for digital gaming. According to TRAI, India's total wireless data subscribers reached 1018.59 million by December 2025 from 961.08 million in September 2025, with North India's dense urban hubs in Delhi, UP, and Punjab driving a disproportionately large share of mobile gaming and fantasy sports engagement nationally.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 37.4% |

| Key States | Delhi, Uttar Pradesh, Punjab, Haryana, Rajasthan |

| Key Growth Drivers | Cricket culture, urbanization, high internet penetration, youth population |

| Outlook | Continued market leadership |

|

Regional Breakdown North India (37.4%) · West and Central India · South India · East India |

West and Central India:

West and Central India represents a pivotal commercial hub for the India fantasy sports market, home to the corporate headquarters of leading platforms, including Dream Sports Group (Mumbai) and key technology centers. The region's urban centers, Mumbai, Pune, and Ahmedabad, combine high smartphone penetration with a large aspirational middle-class demographic actively engaged in sports entertainment.

|

Metric

|

Details

|

|---|---|

| Key States | Maharashtra, Gujarat, Madhya Pradesh, Goa |

| Key Growth Drivers | Corporate headquarters concentration, urban affluence, sports media partnerships |

| Outlook | Strong sustained growth driven by metro demand |

South India:

South India is a rapidly growing market for India fantasy sports, fueled by a highly educated technology workforce in Bengaluru, Hyderabad, and Chennai and a cricket culture deeply intertwined with the Chennai Super Kings and Sunrisers Hyderabad IPL franchises. The region has become an investment center for the broader gaming ecosystem: KRAFTON India invested over $200 million since 2021 in Indian digital content platforms, and Krafton acquired cricket game developer Nautilus Mobile for $14 million. This investment footprint is creating new talent pipelines and platform capabilities that increasingly benefit South India's fantasy sports audience.

|

Metric

|

Details

|

|---|---|

| Key States | Karnataka, Telangana, Tamil Nadu, Andhra Pradesh, Kerala |

| Key Growth Drivers | Tech workforce engagement, IPL franchise loyalty, esports investment |

| Outlook | High-growth region driven by digital adoption |

East India:

The region's cricket enthusiasm runs deep. Kolkata's Eden Gardens is one of the world's largest cricket stadiums, and the KKR franchise has cultivated a fanatical followership that translates directly into fantasy sports participation during IPL seasons. India's online gaming sector attracted approximately $3 billion in FDI, reflecting investor confidence that extends to the eastern market's expanding internet access, growing youth population, and increasing penetration of affordable 5G-capable smartphones across Odisha, Bihar, and the North-Eastern states.

|

Metric

|

Details

|

|---|---|

| Key States | West Bengal, Odisha, Bihar, Jharkhand, North-East states |

| Key Growth Drivers | Cricket culture, growing internet penetration, youth demographics |

| Outlook | High-potential emerging market |

Market Outlook (2026-2034)

What is the future outlook of the India Fantasy Sports market?

The India Fantasy Sports market is expected to sustain steady revenue growth through 2034.

The India fantasy sports market is expected to sustain extraordinary growth momentum through 2034, supported by continued smartphone and 5G network expansion, deepening cricket engagement, and a maturing esports ecosystem. India's Promotion and Regulation of Online Gaming Act, 2025, reset the commercial architecture, but the structural drivers remain compelling. Platforms pivoting toward free-to-play social gaming, AI-powered fan engagement, and esports content are well-positioned to capture a substantially larger and more diverse user base over the forecast horizon, reinforcing India's standing as the world's fastest-growing fantasy sports and digital gaming market.

India Fantasy Sports Market — Leading Key Players

The India fantasy sports market features a competitive landscape shaped by platform scale, sports rights partnerships, and the post-PROG Act pivot to free-to-play and esports formats. The ongoing regulatory recalibration continues to reshape competitive dynamics and investment flows across the sector.

| Company | Leading Brands | Highlights |

|---|---|---|

|

Dream Sports Group |

Dream11, FanCode, DreamSetGo | India's largest fantasy sports platform (250M+ users) and secured $150M investment in November 2025. |

|

BalleBaazi |

BalleBaazi fantasy sports app | Niche fantasy sports platform with a cricket-first focus, expanding into various games, known for innovative contest formats and regional language support. |

|

11 Wickets.com |

11Wickets fantasy platform | Cricket-focused fantasy platform with multi-format support, competing in the mid-tier fantasy segment. |

Some of the other key players in the market include MPL (Mobile Premier League), Vision11, Howzat, FanFight / A23, etc.

Latest Development & News

- February 2026: FanCode, a Dream Sports company, acquired the exclusive broadcast rights for the Indian Super League (ISL), marking a significant expansion into Indian football media and sports content distribution. The production of ISL matches will be handled by Kaleidoscope Production and Services (KPS Studios).

- April 2025, Karnataka introduced a comprehensive regulatory framework for the online real money gaming (RMG) sector. The policy featured a whitelist system to recognize and authorize legitimate operators. According to Storyboard18, the framework also includes age verification requirements, grievance redressal systems, and player support mechanisms as part of efforts to curb illegal betting and gambling platforms.

- February 2025: Times Internet launched Cricbuzz11, a new platform offering real-money fantasy cricket contests. The app allowed participants to create virtual teams and compete in contests during major cricket tournaments such as the Champions Trophy and Women's Premier League (WPL).

India Fantasy Sports Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sports Types Covered | Cricket, Football, Others |

| Platforms Covered | Website, Mobile Application |

| Demographics Covered | Under 25 Years, 25-40 Years, Above 40 Years |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Dream Sports Group, Mobile Premier League (MPL) (Galactus Funware Technology Private Limited), 11 Wickets.com (Ability Games Pvt. Ltd), BalleBaazi, MyTeam11, MyFab11, Paytm First Games Pvt. Ltd., Fantasy Power 11, Head Digital Works Pvt Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India fantasy sports market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India fantasy sports market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India fantasy sports industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Fantasy Sports Market Research Report and Industry Forecast Report

The India fantasy sports market size was valued at USD 27.02 Billion in 2025.

The India fantasy sports market is anticipated to reach a value of USD 557.05 Billion by 2034.

Cricket dominates the India fantasy sports market with a share of 87.4%, driven by its deep cultural roots and the structural alignment between cricket's multiple formats and fantasy sports mechanics.

Mobile application commands the India fantasy sports market with a share of 76.2%, reflecting India's smartphone-first digital behavior. The convenience of in-app team creation, real-time score tracking, and push notification-driven engagement makes mobile applications the dominant access point.

25-40 years segment commands the India fantasy sports market with a share of 48.0%, with fantasy sports as a second-screen experience during live matches, integrating cricket analysis, real-time decision-making, and social competition into their sports-watching habits.

North India currently leads the India fantasy sports market, accounting for a share of 37.4%. The region's dominance is driven by its deeply entrenched cricket culture, high internet penetration in urban centers such as Delhi-NCR, Uttar Pradesh's large youth gaming population, and the concentration of fantasy sports marketing and sponsorship activity targeting North India's sports-passionate demographic.

Some of the major players in the India fantasy sports market include Dream Sports Group (Dream11), 11 Wickets.com (Ability Games), and BalleBaazi, among others.

Key trends shaping the India fantasy sports market include the industry-wide pivot to free-to-play and esports formats following the 2025 regulatory overhaul, deep integration of AI and real-time data analytics into user experiences, the formal recognition of esports as an official sport in India, multi-sport platform diversification beyond cricket, and the expansion of vernacular content to broaden accessibility across Tier 2 and Tier 3 cities.

Growth in the India fantasy sports market is primarily driven by the unmatched cultural dominance of cricket and the annual IPL engagement cycle, rapid 5G network expansion enabling immersive real-time fantasy experiences, the formal recognition of esports as an official sport, and multilingual platform interfaces unlocking non-metro market segments previously underserved by English-only digital experiences.

The India fantasy sports market faces significant challenges, including regulatory uncertainty following the Promotion and Regulation of Online Gaming Act, 2025, which banned real-money gaming and forced abrupt business model transformations across platforms. Additional challenges include the risk of user migration to unregulated offshore platforms, the structural difficulty of replicating real-money contest monetization within free-to-play frameworks, investor sentiment uncertainty during the regulatory transition, and potential workforce disruption affecting approximately two lakh jobs across the erstwhile real-money gaming ecosystem.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)