India Fintech Market Size, Share, Trends and Forecast by Deployment Mode, Technology, Application, End User, and Region, 2026-2034

India Fintech Market Size & Forecast 2026-2034

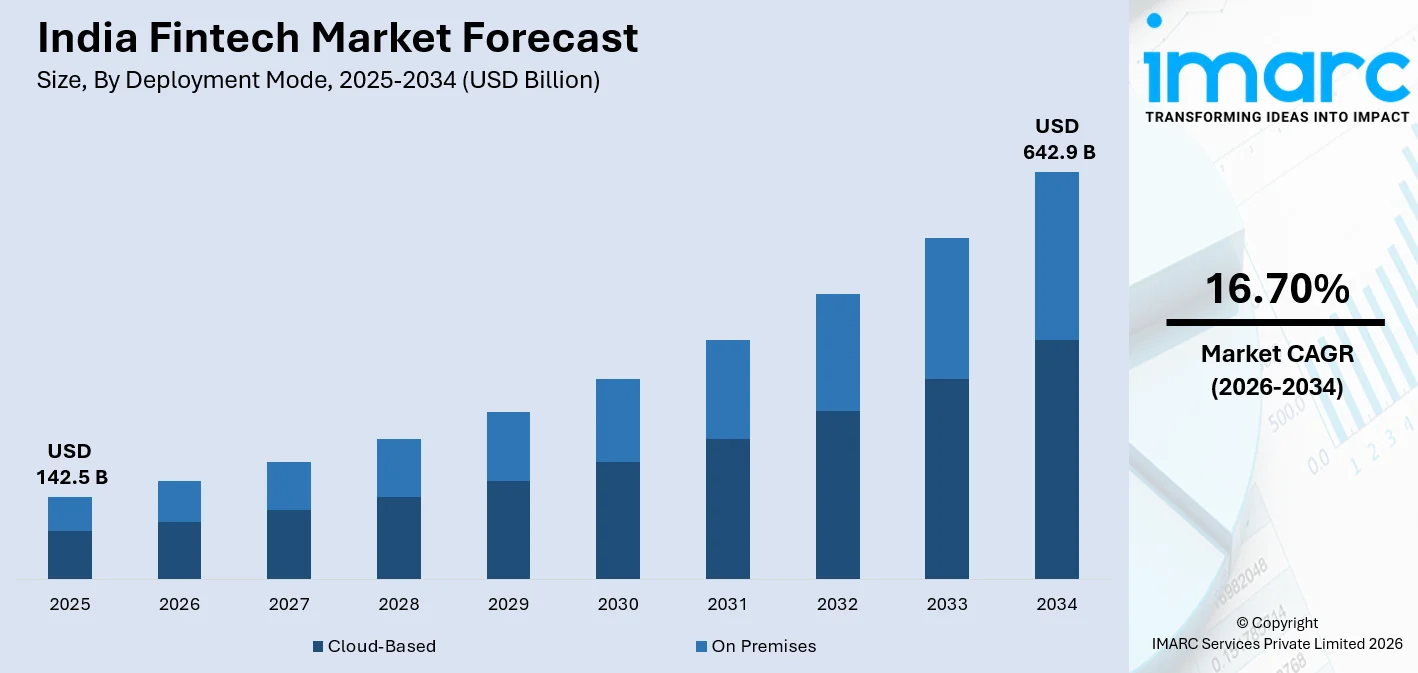

The India Fintech market size, valued at USD 142.5 Billion in 2025, is projected to reach USD 642.9 Billion by 2034, growing at a CAGR of 16.70% from 2026-2034. Multiple factors are driving this growth, including a decisive shift toward digital-first financial behavior, widespread access to affordable smartphones, and ongoing policy initiatives aimed at expanding financial services to underserved households and enterprises nationwide.

In recent years, India has established itself as one of the world’s most significant fintech markets. This position is the result of rapid digital payment adoption, substantial venture capital investment, and expanding partnerships among banks, non-banking financial institutions, and technology companies. Central to this transformation is the Unified Payments Interface (UPI), a real-time payment infrastructure that has fundamentally changed how hundreds of millions of Indians conduct transactions. UPI processed over 185.8 billion transactions in FY2025 and accounted for over 83.4% of all digital retail payments nationally. Additionally, related segments such as digital lending, wealth technology, and embedded finance are expanding at an unexpectedly rapid pace. Collectively, these developments indicate a positive medium- to long-term outlook for India’s fintech sector.

To get more information on this market Request Sample

India Fintech Industry Analysis Key Insights

- Cloud-based dominates the deployment mode at 64.7% in 2025 - as financial institutions have come to rely on cloud environments to manage growing transaction loads, scale operations efficiently, and sustain a faster pace of digital product development.

- Application Programming Interfaces account for technology at 27.9% in 2025 - enabling secure, structured data exchange between banks, fintech providers, and third-party services forming the connective tissue that makes open banking ecosystems viable.

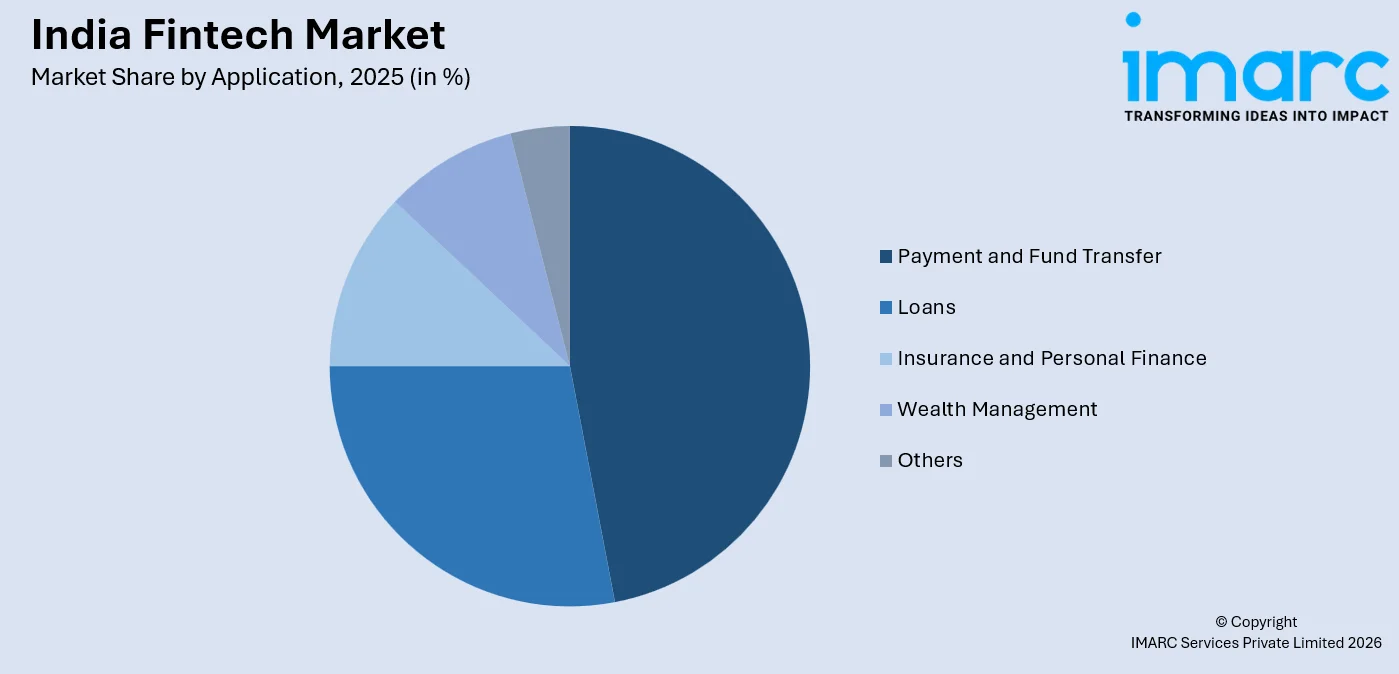

- Payment and fund transfer command 46.5% of application share in 2025 - Driven by the deep integration of digital payment channels particularly mobile wallets and UPI which have become indispensable fixtures in the daily financial lives of millions of consumers.

- Banking leads end user at 41.8% in 2025 - as banks increasingly look to fintech partners to modernize their digital infrastructure while raising the bar on what customers experience day to day.

- West and Central India leads regionally at 34.6% in 2025 - Driven anchored by the presence of Mumbai and Pune two cities that function as the country’s primary centers for financial capital, fintech innovation, and institutional activity.

India Fintech Market Trends and Dynamic 2026

Market Trends

Digital Payments Continue to Dominate the Fintech Ecosystem

UPI Digital payments continue to set the pace for everything else happening in India’s fintech space. UPI transaction volumes tell the story clearly: over 106 billion transactions were processed in just the first half of 2025. What is particularly noteworthy is not just the raw volume, but the growing share attributable to merchant payments a sign that digital financial tools are weaving themselves into the fabric of everyday commerce, whether at a neighborhood retailer, a cab booking, or a utility bill payment.

Artificial intelligence is transforming fintech platforms by strengthening fraud detection, automating customer service, and improving credit risk assessment

Financial institutions are increasingly adopting machine learning to enhance the precision and nuance of lending decisions, thereby extending credit to borrowers who may have been excluded under traditional frameworks. In addition to credit assessment, prominent applications of artificial intelligence in fintech include conversational payment interfaces and digital assistants, which are becoming genuinely useful tools rather than superficial features.

API-Driven Open Banking is Accelerating Innovation

Open banking is gradually removing barriers that previously restricted financial data to individual institutions. Through application programming interfaces (APIs), banks and authorized third-party providers are now able to exchange data securely and in real time. This architecture has enabled fintech companies to develop innovative services. Notable outcomes include digital lending platforms, embedded finance products, and personal finance management tools, many of which operate atop existing banking infrastructure without necessitating changes in customer banking behavior.

Fintech adoption is also expanding beyond metropolitan markets, reaching new segments and driving inclusive growth.

The geographic reach of fintech in India is expanding in ways that were not apparent a few years ago. Enhanced internet access, increased smartphone availability, and rising digital literacy are collectively integrating tier-2 and tier-3 cities into the fintech ecosystem. As digital payment infrastructure extends nationwide, these cities have shifted from being secondary considerations to becoming the primary growth frontier for fintech companies that have already established a presence in metropolitan areas.

- Vernacular and Voice First Interfaces: India’s linguistic diversity has long been one of the practical barriers to mass fintech adoption. Companies responding to this reality are introducing regional language support and voice-first interfaces that allow users to navigate financial services in the language they are most comfortable in a design shift that is meaningfully lowering the threshold for first-time users who have limited familiarity with English-language platforms.

- Embedded Finance and Super App Convergence: Another interesting aspect of the fintech ecosystem in India is the increasing trend of integrating finance into non-traditional channels. E-commerce websites and ride-hailing applications are now offering lending services, insurance products, and investing options as a part of their core offerings. However, these are not being done as after-thoughts; they are being done in a way that they are contextually relevant. This evolution is taking the fintech ecosystem in India to a point where the lines between the two are blurred.

- Regulatory Technology Adoption: Keeping up with India’s regulatory environment is a real operational challenge. The Reserve Bank of India’s guidelines on digital lending and data localization have evolved with some frequency, and fintech companies are responding by building out their regulatory technology capabilities not just to stay compliant in the present, but to manage compliance continuously as the rules continue to develop.

- Green and Sustainable Fintech Initiatives: A quieter but notable shift is underway in how Indian fintech companies are thinking about product design. ESG-linked lending products and sustainability-oriented investment instruments are beginning to appear on platforms that previously had no mandate to address environmental considerations. Government encouragement has played a role here but so has an evolving consumer sensibility around what it means to handle money responsibly.

Growth Drivers

Expansion of Real-Time Digital Payment Infrastructure

The numbers attached to India’s real-time payments infrastructure have become almost difficult to contextualize. In a single month of 2025, over 19.6 billion UPI transactions were recorded, with an aggregate value of ₹24.9 lakh crore. These are not just impressive statistics, they reflect how thoroughly digital payment behavior has permeated financial transactions across income levels, geographies, and merchant categories.

Financial Inclusion Initiatives Expanding the Consumer Base

Government programs spanning digital identity infrastructure, mobile banking access, and payment facilitation are steadily drawing millions of previously unbanked individuals into the formal financial system. For fintech companies, this is not merely a social narrative, it represents a concrete and expanding addressable market of customers who are entering the financial mainstream for the first time.

Strong Venture Capital Investment in Fintech Innovation

India is still receiving considerable cross-border venture capital investments in its digital financial services landscape, and this is a clear vote of confidence by global investors in the long-term structural drivers in the country’s financial services industry. Startups in payments, lending, and financial data analytics have collectively raised significant capital in recent periods, and the pace of innovation in these verticals is consistent. From a regulatory standpoint, the industry has been helped rather than hindered.

- Expansion of the Account Aggregator Framework: India’s Account Aggregator framework is a notable recent advancement in financial infrastructure. This consent-based system enables secure data sharing between institutions, giving customers greater control over their information and allowing providers to offer more tailored products.

- Growth of Digital Lending Platforms: Technology-enabled lending platforms are addressing a persistent gap in India’s financial system: extending credit to individuals and MSMEs without traditional credit histories or collateral. By leveraging alternative data and faster underwriting, these platforms are expanding access to formal credit for underserved segments.

- Emergence of Neobanks and Digital-Only Financial Platforms: Neobanks are redefining financial services by building their offerings around mobile platforms rather than adapting legacy branch infrastructure. These fully digital institutions provide comprehensive account management and services through efficient, technology-driven models, raising customer expectations for modern banking.

- Integration of Fintech Solutions within E-Commerce Ecosystems: E-commerce platforms are integrating fintech capabilities directly into the purchase process. Features such as buy-now-pay-later, digital wallets, and point-of-sale financing make transactions more accessible and convenient for a wider range of customers.

Market Restraints

Regulatory Complexity and Compliance Requirements: Operating within India’s regulatory environment is not straightforward. Compliance requirements shift with some regularity and navigating them demands meaningful legal and operational bandwidth. For well-capitalized incumbents this is manageable; for early-stage startups trying to scale quickly, the associated costs and complexity can be genuinely constraining.

Market Concentration in Digital Payment Platforms: The degree of concentration in India’s digital payments market warrants attention. When over 83% of UPI transactions flow through just two platforms, questions about competitive balance and long-term market health become difficult to set aside. How this dynamic evolves and whether regulatory intervention will be required to address it remains one of the more consequential open questions in the sector.

Cybersecurity and Data Protection Issues: As transaction volumes scale and more sensitive financial data moves through digital channels, the cybersecurity burden on fintech companies grows proportionally. Data protection is no longer a compliance checkbox it is foundational to customer trust, and any significant breach carries reputational consequences that can be difficult to recover from.

India Fintech Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Deployment Mode | Cloud-Based | 64.7% | 2025 |

| Technology | Application Programming Interface | 27.9% | 2025 |

| Application | Payment and Fund Transfer | 46.5% | 2025 |

| End User | Banking | 41.8% | 2025 |

| Region | West and Central India | 34.6% | 2025 |

Deployment Mode Insights

Cloud-Based – 64.7% market share (2025) | Leading Deployment Mode

Cloud infrastructure has become the operational backbone of choice for most fintech companies, and it is not difficult to see why. The ability to scale transaction processing capacity up or down in response to demand, combined with meaningful cost advantages over on-premises alternatives, makes cloud a natural fit for an industry that experiences highly variable load patterns. Beyond operational efficiency, cloud environments are also accelerating the product development cycle, allowing fintech firms to ship new financial services at a pace that on-premises infrastructure simply cannot match.

|

Segment Breakdown Cloud-Based (64.7%) · On Premises |

Technology Insights

Application Programming Interface – 27.9% market share (2025) | Leading Technology

APIs have quietly become one of the most important building blocks in India’s financial services infrastructure. By enabling secure, standardized data exchange between financial institutions and third-party developers, they have created conditions for an open, collaborative ecosystem in which fintech companies can build innovative products without needing to own or replicate the underlying infrastructure. What this means in practice is faster product development, more interoperable services, and a financial system that can evolve far more dynamically than the siloed architectures of the past allowed.

|

Segment Breakdown Application Programming Interface (27.9%) · Artificial Intelligence · Blockchain · Robotic Process Automation · Data Analytics · Others |

Application Insights

Access the comprehensive market breakdown Request Sample

Payment and Fund Transfer – 46.5% market share (2025) | Leading Application

It is perhaps unsurprising that payments and fund transfers command the largest share of the fintech market, given how fundamentally UPI has changed how people transact. The segment encompasses the full spectrum of digital payment systems enabling consumers and businesses to move money via mobile instantly, at any time, and at negligible cost. The normalization of real-time mobile payments has set a high bar for what users expect from every other financial interaction they have.

|

Segment Breakdown Payment and Fund Transfer (46.5%) · Loans · Insurance and Personal Finance · Wealth Management · Others |

End User Insights

Banking – 41.8% market share (2025) | Leading End User

Banks represent the largest institutional cohort deploying fintech solutions and for good reason. The imperative to modernize aging infrastructure, compete with digital-native challengers, and meet rising customer expectations around speed and personalization has made fintech partnership a strategic necessity rather than an optional enhancement. The result is a steady stream of collaborations that are reshaping what banking looks and feels like for end customers.

|

Segment Breakdown Banking (41.8%) · Insurance · Securities · Others |

Regional Insights

West and Central India – 34.6% market share (2025) | Leading Region

Mumbai and Pune occupy an outsized role in shaping India’s fintech landscape. Mumbai’s position as the country’s financial capital means that institutional relationships, regulatory conversations, and capital flows are uniquely concentrated here. Pune, for its part, has become a notable center for fintech products and engineering talent. Together, these cities account for a disproportionate share of startup activity, venture investment, and digital payment adoption factors that collectively explain West and Central India’s leading regional position.

|

Regional Breakdown West and Central India (34.6%) · North India · South India · East India |

North India

Delhi NCR provides the fulcrum of the fintech industry in the north of India, with the city’s regulatory proximity and consumer base driving the growth of the industry. The presence of the capital city, coupled with the concentration of government offices and public sector banks, has led to the development of a culture of fintech companies that are highly sensitive to regulatory, lending, and B2G payment-related opportunities. Noida and Gurugram have now established themselves as the operational base of the north Indian fintech industry, with a large percentage of back-office operations of fintech companies, NBFC-associated fintech companies, and credit technology companies targeting the underserved middle-income segment of India. The vast hinterlands of Uttar Pradesh and Rajasthan provide the potential for the growth of the fintech industry in the rural segment of the Indian market.

|

Metric

|

Details

|

|---|---|

|

Key States

|

B2G payments, lending infrastructure, NBFC-linked startups, credit-tech platforms, regulatory compliance solutions |

|

Major Growth Drivers

|

Delhi, Gurugram, Noida, Chandigarh, Jaipur, Lucknow |

|

Outlook

|

Digital credit penetration and rural payments expansion across Uttar Pradesh and Rajasthan |

South India

Bengaluru’s reputation as India’s technology hub makes the South Indian fintech market the most technologically advanced in the country. The city’s reputation as a hub for technology and entrepreneurship has created a disproportionate share of India’s fintech infrastructure, from payment systems and API banking platforms to regtech and embedded finance platforms. Chennai is a significant fintech and enterprise technology hub, and although Hyderabad is still in the process of building its fintech reputation, it is gaining traction as a hub for Insurtech and wealth management of fintech startups. The South Indian fintech market is the most innovative in terms of fintech products per capita and is the primary location of developer-centric fintech platforms, which are then replicated in the rest of the country.

|

Metric

|

Details

|

|---|---|

|

Key States

|

API banking, payment rails, embedded finance, regtech, insurtech, wealth management platforms |

|

Major Growth Drivers

|

Bengaluru, Chennai, Hyderabad, Kochi, Coimbatore |

|

Outlook

|

Developer-first fintech product innovation; primary origin point for platforms adopted nationally |

East India

Kolkata’s reputation as a commercial and banking hub provides the basis for a fintech market in East India that is centered on trade finance and cooperative banking reform. Although the region is low in terms of the density of venture-backed startups, it is gaining traction as a fintech market with significant growth potential due to the sizeable population of the unbanked in West Bengal, Odisha, and the northeastern states. The state-backed digital infrastructure drive and the success of the Jan Dhan payment systems have created a strong foundation in the region. Bhubaneswar is slowly but surely emerging as a fintech and technology hub.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Financial inclusion, Jan Dhan-linked payments, microfinance digitization, Agri-fintech, cooperative banking reform |

|

Major Growth Drivers

|

Kolkata, Bhubaneswar, Patna, Guwahati, Ranchi |

|

Outlook

|

Emerging hub for microfinance digitisation and agri-fintech aligned with regional economic fabric |

Market Outlook 2026-2034

What is the future outlook of the India Fintech market?

The India fintech market is expected to maintain strong growth through 2034

The structural drivers underpinning India’s fintech growth are durable rather than cyclical, which gives the long-term outlook a degree of confidence that is worth noting. Payments, lending, insurance, and wealth management each carry meaningful headroom for further penetration, particularly as the market extends beyond its current urban core. Technological developments in artificial intelligence, blockchain, and embedded finance are expected to generate fresh innovation vectors over the coming years, while continued improvements in internet infrastructure and government financial inclusion initiatives should broaden the addressable base further still. On balance, India appears well-positioned to sustain its standing as one of the world’s leading fintech ecosystems through 2034 and beyond.

India Fintech Market - Leading Key Players

India’s fintech competitive landscape is unlike most markets it brings together established banks, global technology platforms, and a dense population of homegrown fintech startups, all competing and frequently collaborating within the same ecosystem. The result is an industry that moves quickly, where incumbents cannot afford complacency, and new entrants can achieve meaningful scale faster than in most other markets. India has earned its place among the world’s largest fintech ecosystems, and the combination of accelerating digital adoption and supportive policy infrastructure suggests that position is not under threat.

| Company | Leading Brands | Highlights |

|---|---|---|

| PhonePe (Walmart Inc.) | PhonePe UPI, PhonePe Financial Services, Digital Gold | PhonePe has built one of India’s most comprehensive digital financial platforms on a UPI foundation. Beyond peer-to-peer and merchant payments, the company has expanded into insurance distribution and investment products, making a credible push toward becoming a one-stop financial destination for its users. Strategic tie-ups with financial institutions and continued investment in its marketplace are central to how the company is positioning itself for the next phase of growth. |

| Google Pay (Alphabet Inc.) | Google Pay UPI | Google Pay has established itself as one of the most heavily used UPI platforms in the country, processing over 7.23 billion transactions in January 2026 alone equivalent to roughly a third of total UPI volume for the month. The application’s clean interface and deep integration with Google’s broader ecosystem have made it a preferred channel for both everyday peer-to-peer transfers and merchant payments across the country. |

| Paytm (One97 Communications Ltd.) | Paytm Wallet, Paytm Payments Bank, Digital Gold | Paytm has made a notable bet on the physical layer of digital payments through its Soundbox rollout a device that provides instant audio confirmation of incoming payments and has become a familiar presence at small merchants across the country. With over 13.7 million units deployed by September 2025, the company has embedded itself deeply into the everyday operational rhythm of a significant portion of India’s merchant base. |

| Razorpay | Razorpay Payment Gateway, RazorpayX | Razorpay occupies a distinctive position in India’s fintech landscape as the infrastructure layer on which a large number of businesses have built their payment and financial operations. Its gateway, business banking, and financial automation products serve a broad range of companies from early-stage startups to established enterprises. The company continues to push the boundaries of what payment infrastructure can do, with AI-driven capabilities becoming an increasingly prominent part of its product roadmap. |

Some of the competitive fields extend well beyond the largest platforms. Pine Labs Private Limited, BharatPe (Resilient Innovations Pvt. Ltd.), CRED (Dreamplug Technologies Pvt. Ltd.), MobiKwik (One MobiKwik Systems Ltd.), and Policybazaar (PB Fintech Limited) each hold meaningful positions within their respective segments and continue to shape how the broader market develops.

Latest Development & News

- January 2026: PhonePe continued to demonstrate the scale of its market position by processing approximately 9.91 billion transactions during the month, a figure that represents approximately 45.7% of total UPI volume. Across the network, 21.7 billion transactions worth ₹28.33 lakh crore were processed, a data point that speaks to how thoroughly digital payments have become embedded in the financial lives of Indian consumers.

- March 2026: Cred CRED obtained formal authorization from the Reserve Bank of India to operate as a licensed payment aggregator a regulatory milestone that meaningfully expands what the platform can do commercially. With this approval, CRED can now ship onboard merchants directly and process transactions across a wider range of payment instruments. The scale at which it is already operating ₹8.5 trillion in payments facilitated for approximately 15 million users in FY2025 underscores how much it has grown beyond its origins as a credit card bill payment app.

India Fintech Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Deployment Modes Covered | On-Premises, Cloud-Based |

| Technologies Covered | Application Programming Interface, Artificial Intelligence, Blockchain, Robotic Process Automation, Data Analytics, Others |

| Applications Covered | Payment and Fund Transfer, Loans, Insurance and Personal Finance, Wealth Management, Others |

| End Users Covered | Banking, Insurance, Securities, Others |

| Regions Covered | North India, South India, West and Central India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India fintech market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India fintech market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India fintech industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Indian Fintech Market Report

India’s fintech market was valued at approximately USD 142.5 Billion as of 2025. Several factors have converged to drive this growth among them, the rapid expansion of digital payment adoption, a steady broadening of internet access, and substantial capital flowing into fintech ventures.

The market is projected to reach approximately USD 642.9 Billion by 2034, implying a compound annual growth rate of 16.70% over the 2026 to 2034 period. Continued innovation across digital payments, lending, and wealth technology is expected to be the primary engine of this expansion.

Cloud-based deployment leads the market, representing 64.7% of the market. The appeal is that practical cloud environments allow fintech companies to handle transaction volumes that fluctuate significantly, without the capital expense and rigidity of maintaining their own infrastructure.

Application Programming Interfaces constitute the leading technology segment, accounting for 27.9% of the market. APIs have become the plumbing that connects the various parts of the financial ecosystem allowing banks, fintechs, and third-party providers to exchange data and services in ways that were simply not feasible under older, more closed architectures.

Payment and fund transfer services hold the largest share of any application category, at 46.5% of the market. The growth of UPI in particular has been transformative it has normalized the expectation of instant, cost-free digital payments in a way that has pulled millions of consumers into digital financial services for the first time.

The banking sector leads all end-user segments, representing 41.8% of the market. Banks have increasingly recognized that building everything in-house is neither efficient nor fast enough to meet customer expectations, leading to a wave of fintech partnerships aimed at accelerating the quality and scope of their digital offerings.

The market features a broad and competitive field. The most prominent names include Paytm, PhonePe, Razorpay, Pine Labs, CRED, Policybazaar, Zerodha, BharatPe, Lendingkart, and MobiKwik, though the list of relevant players extends considerably further.

West and Central India commands 34.6% of the market. Much of this can be traced back to Mumbai and Pune cities where the concentration of financial institutions, venture capital, and fintech talent creates a self-reinforcing cluster effect that is difficult to replicate elsewhere.

The fintech market is being propelled by a combination of expanding digital payment infrastructure, rising smartphone penetration, purposeful government initiatives to deepen financial access, and the consistent flow of investment capital into fintech ventures.

The fintech market is navigating real headwinds: a regulatory environment that continues to evolve, a growing cybersecurity threat surface as digital transaction volumes rise, and competitive intensity that is increasing from both fintech challengers and established banks that are no longer standing still.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)