India Fitness App Market Size, Share, Trends and Forecast by Type, Platform, Device, and Region, 2026-2034

India Fitness App Market Size, Share, Trends and Forecast (2026-2034

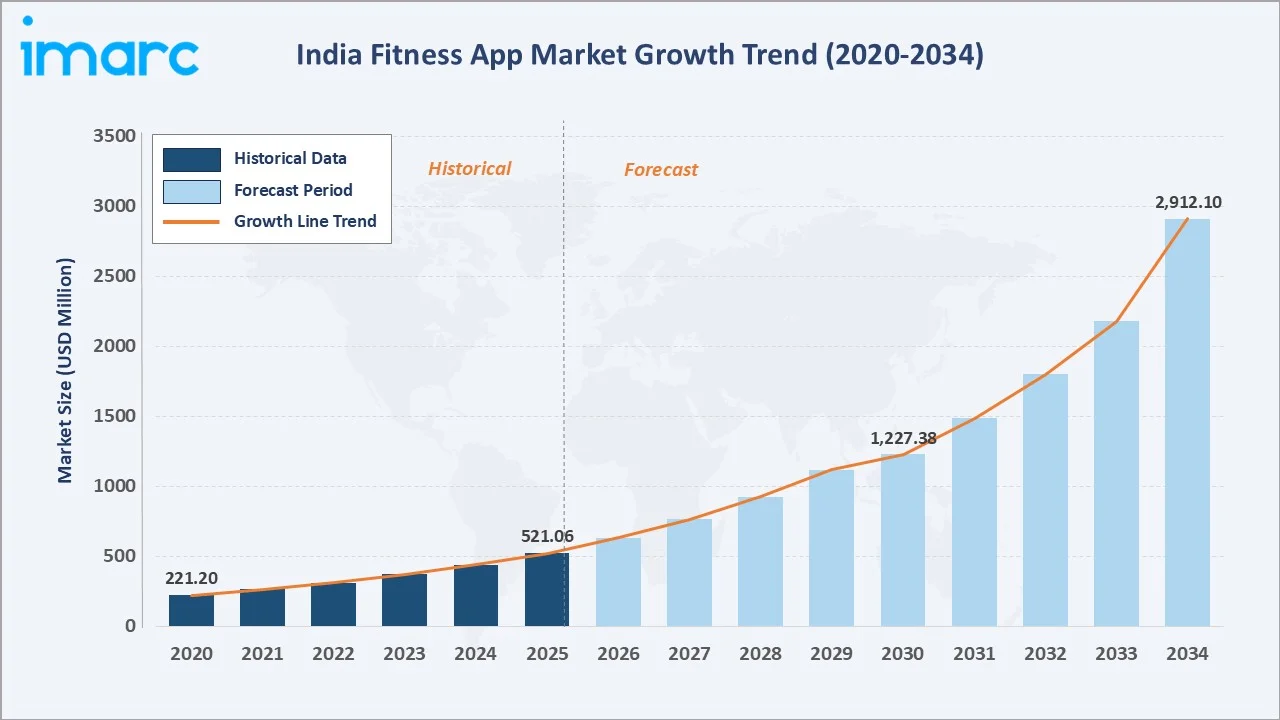

The India fitness app market size reached USD 521.06 Million in 2025 and is projected to reach USD 2,912.10 Million by 2034, exhibiting a CAGR of 18.69% during 2026-2034. Rising health consciousness among India's expanding urban population, rapid smartphone penetration exceeding 900 million active users, and growing demand for personalized digital wellness solutions are the primary forces driving India fitness app market growth.

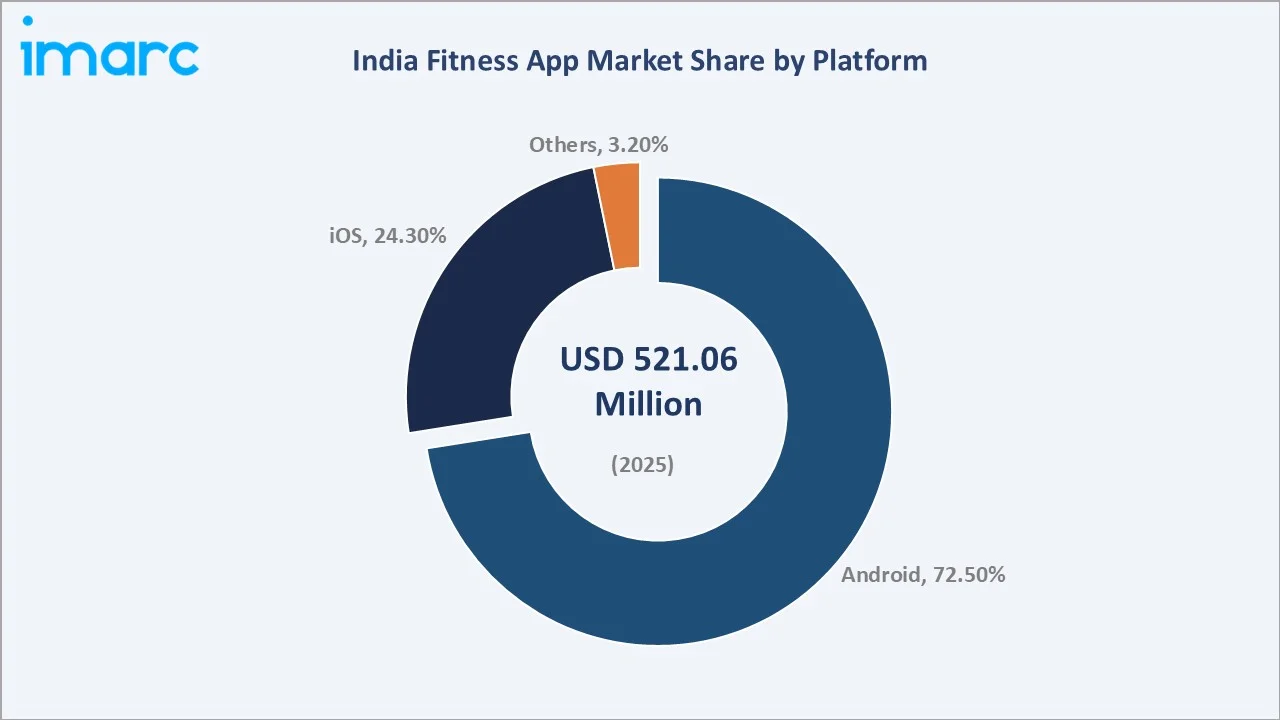

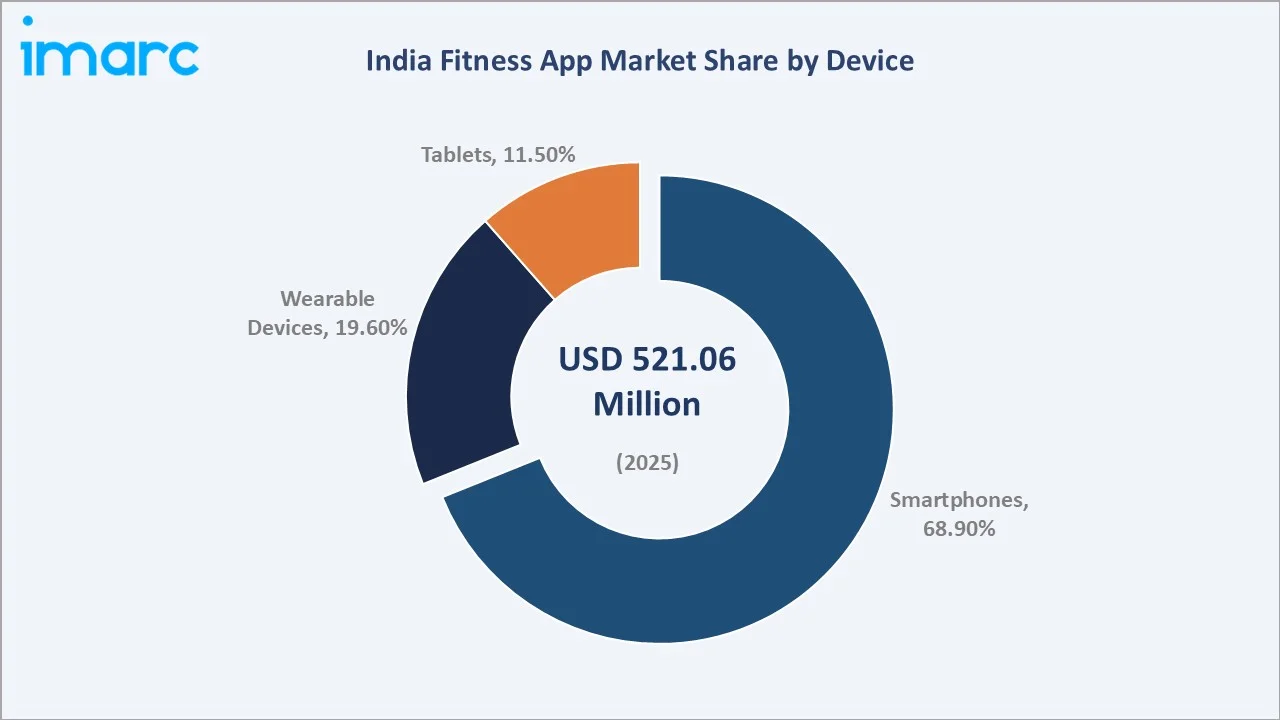

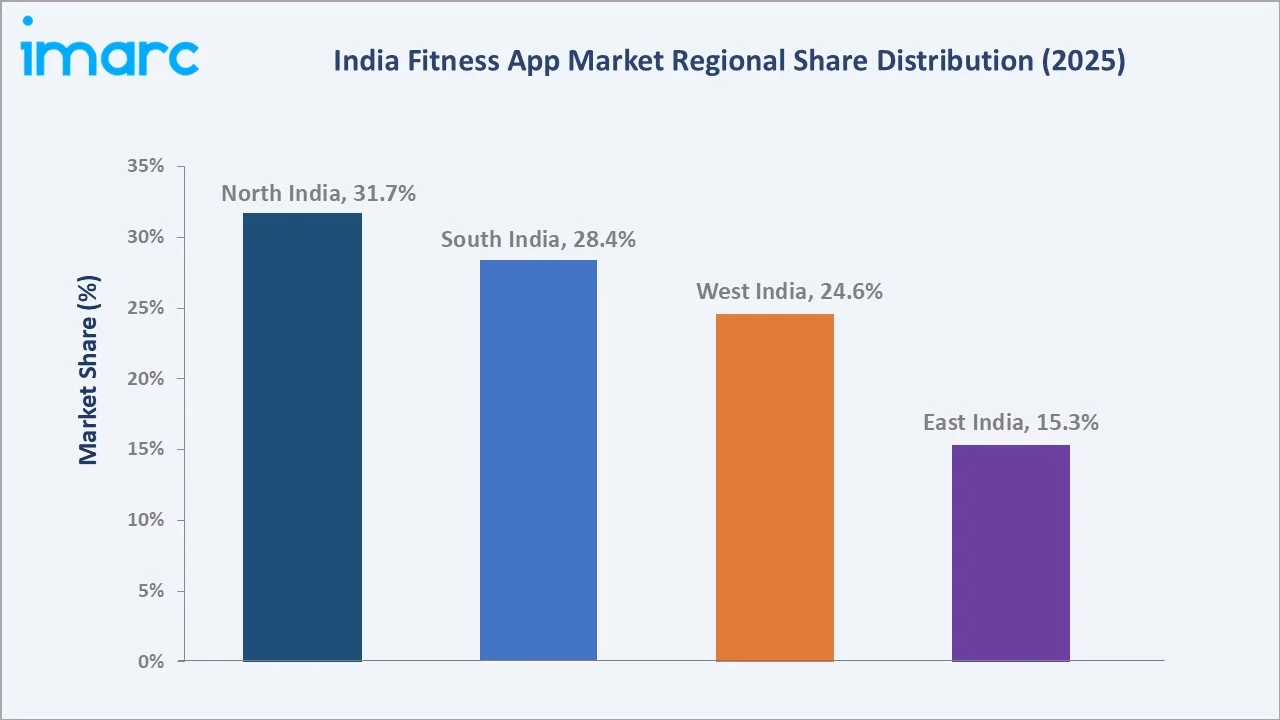

Android platform commands a dominant 72.5% share in 2025, while smartphones account for 68.9% of device-based usage, and North India leads regional adoption with a 31.7% market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 521.06 Million |

|

Forecast Market Size (2034) |

USD 2,912.10 Million |

|

CAGR (2026-2034) |

18.69% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Platform |

Android (72.5% share, 2025) |

|

Leading Device |

Smartphones (68.9% share, 2025) |

|

Largest Region |

North India (31.7% share, 2025) |

|

Second Region |

South India (28.4% share, 2025) |

To get more information on this market, Request Sample

The India fitness app market growth trajectory from 2020 through 2034, with historical expansion to USD 521.06 Million in 2025, reflects sustained digitalization-driven demand, while the forecast to USD 2,912.10 Million captures accelerating AI integration, wearable technology adoption, and urban health-consciousness-led demand across all four regions of India.

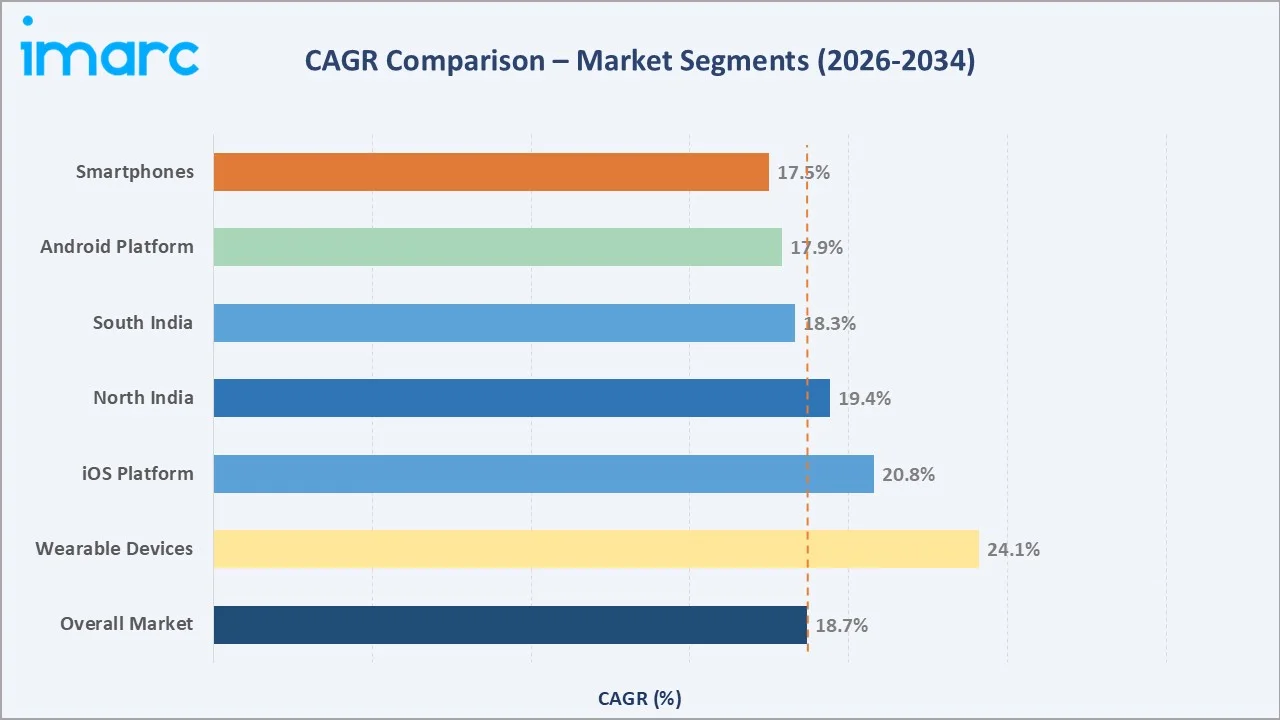

The CAGR trajectories across key platform, device, and regional sub-segments, with wearable devices at ~24.1% CAGR and iOS platform at ~20.8% CAGR, are the fastest-growing categories within the India fitness app industry analysis through 2034.

Executive Summary

The India fitness app market is on a sustained high-growth trajectory from USD 521.06 Million in 2025 to USD 2,912.10 Million by 2034. Fitness apps, as essential digital wellness tools deployed across smartphones, tablets, and wearable devices for workout tracking, nutrition monitoring, activity logging, and virtual coaching, benefit from the growing non-discretionary nature of health investment among India's expanding urban middle class and corporate workforce.

Android platform dominates at 72.5% in 2025, driven by India's predominantly Android-first smartphone ecosystem and the affordability of Android-compatible devices across tier-1, tier-2, and tier-3 cities. iOS platform (24.3%) commands premium positioning, attracting health-conscious, higher-income urban users investing in comprehensive Apple fitness ecosystems including Apple Watch integration.

Smartphones lead device adoption at 68.9% in 2025, while wearable devices (19.6%) represent the fastest-growing device segment with smartwatch penetration rapidly accelerating across India's expanding mid-income demographic.

North India commands the largest regional share at 31.7% in 2025, reflecting high smartphone penetration, strong gym culture, and urban health-consciousness concentrated in Delhi, Noida, Gurgaon, and Chandigarh.

Key Market Insights

|

Insight |

Data |

|

Leading Platform |

Android – 72.5% share (2025) |

|

Second Platform |

iOS – 24.3% share (2025) |

|

Leading Device |

Smartphones – 68.9% revenue share (2025) |

|

Fastest-Growing Device |

Wearable Devices – 19.6% share (2025) |

|

Leading Region |

North India – 31.7% revenue share (2025) |

|

Second Region |

South India – 28.4% revenue share (2025) |

|

Top Companies |

cult.fit (Curefit Healthcare Pvt Ltd), Healthifyme Wellness Private Limited, FITPASS, Squats Fitness Private Limited, Nike Inc., MyFitnessPal Inc., Google LLC (Fitbit), Samsung Electronics Co., Ltd., Strava Inc., Azumio Inc. |

Key Analytical Observations Expanding on the Above Data:

- Android's 72.5% share in 2025 dominates because India has the world's second-largest smartphone user base, overwhelmingly Android-driven. Budget-to-mid-range Android smartphones from Samsung, Xiaomi, Vivo, and Realme, place fitness app access within reach of the mass-market consumer, fueling app download volumes across tier-1 and tier-2 cities simultaneously and sustaining Android's structural market leadership through 2034.

- Smartphones' 68.9% device dominance reflects the convenience and ubiquity of smartphone-based fitness engagement. The vast majority of Indian fitness app users access workout tracking, calorie counting, and virtual coaching exclusively through mobile phones, with lightweight app UX optimized for 4G/5G connectivity and mobile-native interaction patterns designed for India's mobile-first digital consumption behavior.

- North India's 31.7% leadership is driven by concentrated corporate wellness demand in the Delhi-NCR technology and finance corridor, high gym culture penetration in Punjab and Haryana, and the rapid adoption of fitness subscription apps among India's working professional demographic aged 25–40 who prioritize health management as a lifestyle investment.

- South India's 28.4% share reflects the concentrated tech-employee user base in Bengaluru, Hyderabad, and Chennai, where higher disposable incomes, international fitness app exposure, and wearable device penetration combine to create India's highest per-capita fitness app spending region and the strongest premium subscription conversion rates in the domestic market.

India Fitness App Market Overview

A fitness app is a mobile software application designed to support users in achieving health and wellness goals through features including workout tracking, virtual coaching, calorie and macro counting, activity and step monitoring, sleep quality analysis, and personalized nutrition planning. Product configurations range from specialized exercise and weight loss applications to comprehensive all-in-one digital wellness platforms integrating biometric data from wearable devices and connected health sensors.

The India fitness app ecosystem integrates global technology platforms, domestic health-tech startups, fitness content creators, certified trainers, device manufacturers including smartphone and wearable OEMs, telecom operators, health insurance companies, and corporate wellness program administrators. End-users span working professionals, college students, homemakers, senior citizens, and professional athletes across urban, semi-urban, and rural geographies throughout India.

Market Dynamics

To evaluate market opportunities, Request Sample

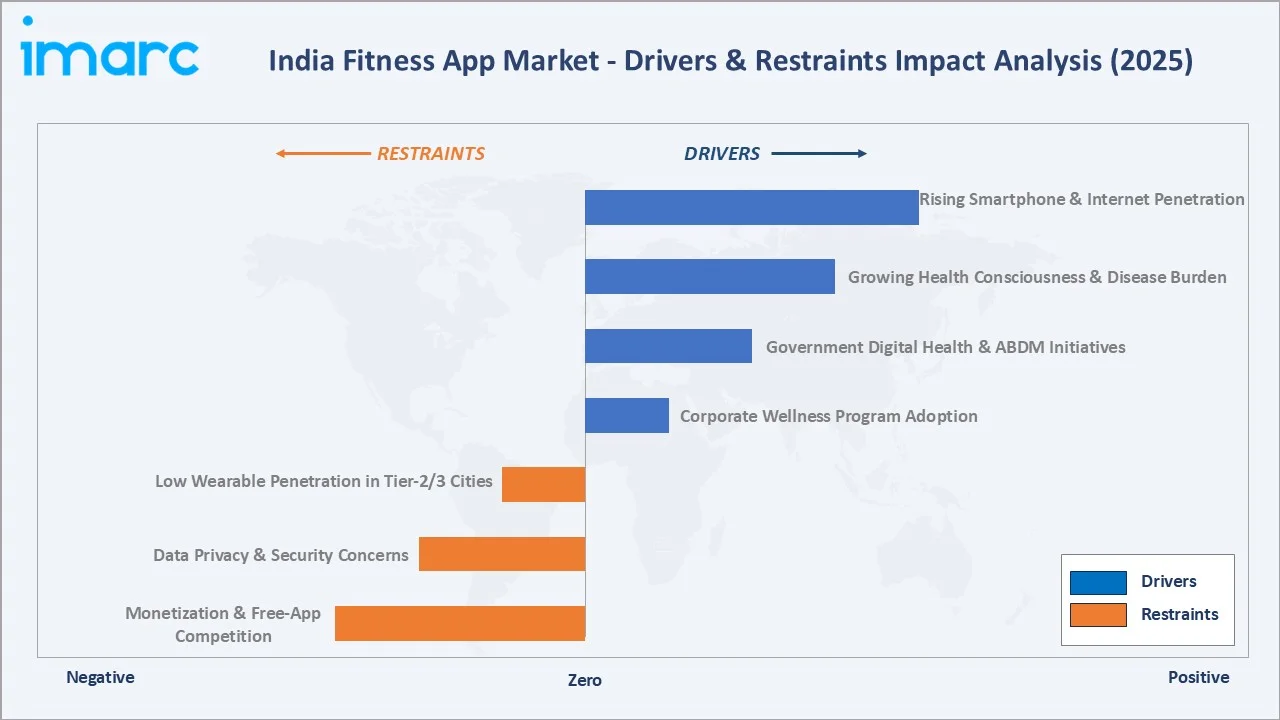

Market Drivers

- Rising Smartphone and Internet Penetration: India surpassed 900 million internet subscribers in 2024, supported by TRAI data, with average mobile data consumption of 17–19 GB per user per month driven by Reliance Jio's aggressive pricing strategy. This internet-connected smartphone universe is the fundamental enabler of fitness app consumption at scale. In January 2023, Jio Bharat announced that it will enable the existing 250 million feature phone users with internet-enabled phones, directly expanding the accessible audience for fitness app developers and monetization platforms across underserved geographies.

- Growing Health Consciousness and Lifestyle Disease Burden: The Indian Council of Medical Research (ICMR) reports that non-communicable diseases including diabetes, cardiovascular conditions, and obesity collectively account for over 60% of India's total disease burden. With the International Diabetes Federation estimating India at 77 million diabetic adults, the world's second-highest count, preventive health management through digital fitness tools is increasingly viewed as a necessity rather than a luxury by urban consumers, driving sustained subscription and engagement growth across all fitness app categories and user demographics.

- Government Digital Health and Ayushman Bharat Digital Mission Initiatives: India's Ayushman Bharat Digital Mission (ABDM), launched in 2021 and scaled through 2024, has created over 739 million Ayushman Bharat Health Accounts (ABHA IDs), establishing a verified digital health identity infrastructure. This government-endorsed digital health ecosystem is accelerating consumer comfort with digital wellness data management, creating a favorable environment for fitness app monetization, health data portability, and insurance-integrated wellness incentive programs.

Market Restraints

- Monetization Challenges and Free-App Competition: India's app market is intensely price-sensitive, with most active fitness app users relying on free-tier features. The prevalence of high-quality freemium offerings from Nike Training Club, Google Fit, and Samsung Health creates persistent barriers to paid subscription conversion, compressing average revenue per user (ARPU) and making it structurally difficult for smaller domestic players to achieve profitability at scale without differentiated premium content strategies or corporate wellness partnerships.

- Low Wearable Device Penetration in Tier-2 and Tier-3 Cities: Despite rapid smartphone adoption nationwide, wearable device penetration remains concentrated in India's top eight metropolitan areas. Smartwatch and fitness tracker ownership among fitness app users in cities below Mumbai, Delhi, Bengaluru, and Hyderabad is estimated below 12%, constraining the full functionality of wearable-integrated app features for a significant portion of the total addressable user base and limiting premium feature monetization potential outside metro markets.

Market Opportunities

- Wearable Device Integration and IoT Health Ecosystem Expansion: The rapid growth of affordable smartwatches from boAt, Noise, Fire-Boltt, and Amazfit, is expanding the wearable addressable market in India beyond premium Apple Watch and Garmin users. Various companies are creating a large installed base of wearable-connected users for fitness app developers to build deeper health tracking integrations, enabling richer data streams and premium feature justification for subscription upgrade conversations.

- Corporate Wellness Program Integration and B2B Revenue Streams: Large Indian IT companies and multinational corporations are adopting structured corporate wellness programs with fitness app subscriptions as a core employee benefit component. FITPASS, with its multi-gym access model, and HealthifyMe's B2B corporate health platform have signed enterprise contracts with companies creating a recurring B2B revenue stream with lower churn than consumer subscription models and expanding the total addressable enterprise wellness market substantially.

Market Challenges

- High User Churn and Engagement Retention Difficulties: The India fitness app market faces a structural 30-day user retention challenge. Seasonal engagement spikes around New Year resolutions and summer fitness campaigns are followed by rapid drop-offs, placing constant pressure on app developers to invest in gamification, social features, and personalized AI coaching to sustain long-term user engagement and reduce subscriber churn to economically viable levels.

- Regulatory Uncertainty for Digital Health Data Intersection: The convergence of fitness data with health insurance, diagnostic telemedicine, and pharmacotherapy creates evolving regulatory complexity for platform operators. IRDAI's 2024 guidelines on insurance-linked wellness programs, requiring actuarial validation of fitness app data for premium discounts, introduce meaningful compliance costs for smaller fitness app operators seeking to participate in India's growing health insurance integration market and wellness-linked financial product ecosystem.

Emerging Market Trends

1. AI-Driven Personalization and Adaptive Coaching Transforming User Engagement

AI-powered personalization is fundamentally transforming how Indian fitness app users engage with digital health platforms, shifting from generic workout libraries to real-time adaptive programs responsive to individual biometric inputs and behavioral patterns. HealthifyMe's proprietary AI nutrition coach "Ria" analyzed food log entries, enabling calorie recommendations tailored to Indian regional dietary patterns including South Indian meals, North Indian thalis, and Bengali cuisine, a localization depth unavailable from global fitness apps, directly driving subscription retention and differentiation in India's competitive fitness app landscape.

2. Wearable Device Integration Creating Unified Health Ecosystems

The convergence of fitness app platforms with India's rapidly expanding affordable wearables market is creating unified digital health ecosystems where step data, heart rate variability, SpO2 monitoring, and sleep quality scores flow seamlessly into personalized workout and nutrition recommendations. In October 2025, ODDS Fitness launched India's first AI-integrated platform simultaneously measuring physical performance, nutrition compliance, and mental wellness indicators through wearable data integration, representing a significant advancement toward holistic health tracking beyond conventional workout logging applications.

3. Vernacular Language Content Driving Tier-2 and Tier-3 City Adoption

Vernacular language fitness content is emerging as the primary driver of India fitness app market expansion beyond the English-speaking urban user base. Applications offering Hindi, Tamil, Telugu, Kannada, Bengali, and Marathi audio workout instructions, video coaching, and nutrition guidance are achieving disproportionate download growth in tier-2 and tier-3 cities.

4. Gamification and Social Fitness Features Enhancing Long-Term Retention

Gamification mechanics including fitness streaks, leaderboards, community challenges, achievement badges, and friend comparison dashboards are proving effective in extending India fitness app user engagement beyond the initial 30-day adoption window that represents the market's primary retention challenge.

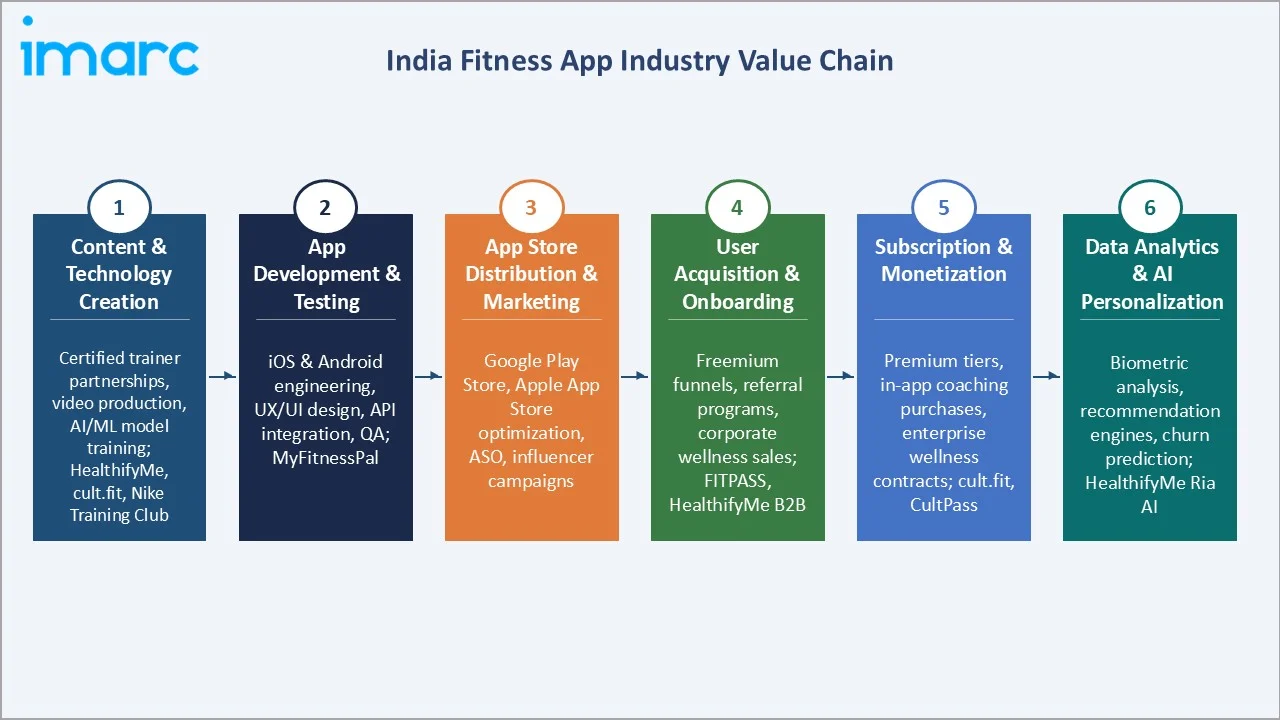

Industry Value Chain Analysis

The India fitness app value chain spans six stages from content and technology creation through data analytics and AI-driven personalization. Platform development and AI/ML engineering capture the highest value-add margins, while distribution through app stores and user acquisition through performance marketing generate the highest working capital requirements, favoring well-capitalized mid-to-large platform operators over early-stage single-feature applications competing in crowded download markets.

|

Stage |

Key Players / Examples |

|

Content & Technology Creation |

Certified trainer partnerships, video production, AI/ML model training; HealthifyMe, cult.fit, Nike Training Club |

|

App Development & Testing |

iOS and Android platform engineering, UX/UI design, API integration, quality assurance; MyFitnessPal |

|

App Store Distribution & Marketing |

Google Play Store and Apple App Store optimization, ASO, influencer campaigns |

|

User Acquisition & Onboarding |

Freemium conversion funnels, referral programs, corporate wellness sales; FITPASS, HealthifyMe B2B |

|

Subscription & Monetization |

Premium subscription tiers, in-app coaching purchases, B2B enterprise wellness contracts; cult.fit CultPass |

|

Data Analytics & AI Personalization |

Biometric data analysis, adaptive recommendation engines, churn prediction; HealthifyMe Ria AI |

Integrated fitness app platforms with proprietary AI coaching capabilities and captive content libraries, such as cult.fit combining gym network data, live-class engagement metrics, and nutrition tracking, achieve structurally lower user acquisition costs and higher lifetime values than single-feature apps competing purely on price in India's commoditized workout tracking segment. Vertical integration across content, technology, and monetization layers is the key competitive advantage for market leaders.

Technology Landscape in the India Fitness App Industry

AI and Machine Learning: Adaptive Coaching and Nutrition Intelligence

The dominant technology differentiation in premium India fitness apps is AI-driven personalization, where machine learning models trained on large longitudinal datasets of user workouts, biometric inputs, and nutrition logs generate adaptive coaching recommendations that improve in accuracy over time. Convolutional neural network-based pose estimation, integrated in apps like Fityoga and InsaneAI Fitness, provides real-time movement correction for yoga and strength training without physical trainer presence, democratizing professional coaching quality for India's mass-market fitness app consumers across metro and semi-urban geographies.

Wearable Integration and IoT Health Data Standards

Bluetooth Low Energy (BLE) and ANT+ protocol integration enables fitness apps to receive real-time heart rate, SpO2, step count, and GPS data from connected wearables including Apple Watch, Samsung Galaxy Watch, and India's mass-market boAt and Noise smartwatches. Google Health Connect and Apple HealthKit provide standardized interoperability layers enabling health data portability across fitness app ecosystems, reducing user lock-in and raising the minimum viable feature quality across the India fitness app platform landscape.

Cloud Computing and Real-Time Analytics Infrastructure

India's fitness app platforms predominantly operate on AWS, Google Cloud, and Microsoft Azure infrastructure for scalable backend processing of real-time biometric streams, video workout delivery, and personalized AI inference workloads. Edge computing integration, particularly for on-device AI inference on Apple's Neural Engine and Qualcomm's Hexagon DSP in Android flagship devices, is enabling real-time fitness coaching without cloud latency, improving the quality of live workout guidance and real-time form correction features for premium users demanding professional-grade digital training experiences.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type |

🔒 |

🔒 |

2025 |

| Platform | Android | 72.5% |

2025 |

| Device | Smartphones | 68.9% |

2025 |

| Region | North India | 31.7% |

2025 |

By Platform

To access detailed market analysis, Request Sample

Android commands a 72.5% majority share in 2025 owing to India's fundamentally Android-driven smartphone ecosystem. The cost-competitiveness of Android devices across the INR 5,000–30,000 price range, combined with Google Play Store's vast fitness app catalog and Android's openness to third-party health data integrations, makes it the default platform for India's mass-market fitness app users.

iOS platform, with 24.3% in 2025, growing at ~20.8% CAGR through 2034, is expanding as Apple's iPhone series achieves record India shipments of approximately 12 million units annually, supported by India-based manufacturing at the Foxconn and Tata Electronics plants in Tamil Nadu and Karnataka.

By Device

Smartphones account for 68.9% of India fitness app market revenue in 2025, reflecting the primacy of mobile-first fitness engagement across all user demographic segments. The lightweight, always-carried nature of smartphones enables passive activity tracking, calorie logging at mealtime, and on-demand workout access that tablet or desktop fitness platforms cannot replicate in terms of convenience and behavioral integration with daily routines.

Wearable devices, with 19.6% in 2025 and growing at ~24.1% CAGR, represent the fastest-growing device segment in the India fitness app market through 2034. Smartwatch-integrated heart rate monitoring, workout auto-detection, and SpO2 tracking drive deeper fitness app engagement, with wearable-connected user sessions averaging 40–60% longer than smartphone-only equivalents.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

31.7% |

Delhi-NCR corporate wellness demand; Punjab/Haryana gym culture; high smartphone penetration in Tier-1 cities |

|

South India |

28.4% |

Bengaluru IT hub; Hyderabad Cyberabad corridor; Chennai tech sector; highest per-capita fitness app spend |

|

West India |

24.6% |

Mumbai-Pune financial and tech ecosystem; cosmopolitan fitness culture; strong Apple/iOS user base |

|

East India |

15.3% |

Kolkata growing health consciousness; expanding 4G/5G in Odisha and Northeast; emerging fitness startup ecosystem |

North India's 31.7% market dominance in 2025 is driven by a structurally exceptional combination of corporate wellness investment, gym culture depth, and smartphone penetration concentrated in the Delhi-NCR megacluster. Corporate wellness programs mandated by Gurgaon's large MNC employer base—including Google India, Microsoft India, and Deloitte—drive institutional fitness app adoption beyond individual consumer subscriptions, creating a structurally recurring enterprise revenue layer.

South India, with 28.4% in 2025, is the highest per-capita revenue contributor within India's fitness app market. Bengaluru's 1.7 million IT workforce, characterized by above-average disposable incomes, international travel experience, and health-conscious work culture, generates disproportionate premium subscription adoption.

Competitive Landscape

The India fitness app market is moderately fragmented, with global platform leaders including Nike, MyFitnessPal, and Google (Fitbit) coexisting alongside well-funded domestic champions including cult.fit and HealthifyMe. Competitive intensity is highest in the Android smartphone freemium segment, where user acquisition costs are rising and retention metrics are the primary differentiator of long-term market position.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Curefit Healthcare Pvt Ltd |

cult.fit App, CultPass, Mind.fit |

Leader |

Omnichannel fitness; gym + digital integration; India-first content |

|

HealthifyMe Wellness Private Limited |

HealthifyMe App |

Leader |

AI nutrition coaching; subscription SaaS; India dietary database depth |

|

FITPASS |

FITCOACH, FITFEAST |

Challenger |

Gym network aggregation; B2B corporate wellness; IRDAI integration |

|

Fittr |

Fittr App |

Challenger |

Community-driven transformation; coach marketplace; affordability focus |

|

Nike, Inc. |

Nike Training Club, Nike Run Club |

Leader |

Global premium brand; free content strategy; wearable integration |

|

MyFitnessPal, Inc. |

MyFitnessPal App |

Leader |

Calorie and macro tracking; food database depth; global platform scale |

|

Fitbit (Google LLC.) |

Fitbit App |

Leader |

Wearable device ecosystem; Android health data hub; AI health analytics |

|

Azumio, Inc. |

Glucose Buddy, Fitness Buddy, Sleep Time |

Emerging |

AI biometric health analytics; glucose and sleep intelligence platform |

Key players include Curefit Healthcare Pvt Ltd, HealthifyMe Wellness Private Limited, FITPASS, Fittr, Nike, Inc., MyFitnessPal, Inc., Fitbit (Google LLC.), Azumio, Inc., and others.

Key Company Profiles

Curefit Healthcare Pvt Ltd

Curefit Healthcare Pvt Ltd (cult.fit) is India's largest omnichannel fitness and wellness platform, headquartered in Bengaluru.

- Product Portfolio: The company offers cult.fit App, CultPass, and Mind.fit apps, among others.

- Recent Developments: In March 2026, Cult.fit raised around $50 million from Temasek as it prepares for a potential initial public offering, signaling renewed investor confidence in the company’s growth trajectory and improving financial performance. The funding values the fitness-tech platform at roughly $1.6 billion and comes as it works toward profitability, supported by strong revenue growth and a significant reduction in losses.

- Strategic Focus: cult.fit's strategy differentiates through its omnichannel model combining physical gym infrastructure with digital platform reach, enabling higher engagement and lower churn than pure-play digital competitors.

HealthifyMe Wellness Private Limited

HealthifyMe is India's leading AI-powered health and nutrition platform, headquartered in Bengaluru. The platform combines calorie and macro tracking with an AI nutrition coach called Ria, delivering personalization depth unavailable from global nutrition tracking competitors.

- Product Portfolio: HealthifyMe App with AI calorie tracking, macro analysis, and personalized meal planning.

- Recent Developments: In June 2023, HealthifyMe secured $30 million in a pre-Series D funding round led by global investors, reinforcing confidence in its growth strategy and technology-driven approach. The company plans to use this capital to strengthen its artificial intelligence capabilities, enhance its AI-powered coaching ecosystem, and invest in talent acquisition while accelerating international expansion. A key focus is the advancement of its AI-driven virtual nutritionist and platform features, enabling more personalized, data-driven health and fitness solutions at scale.

- Strategic Focus: HealthifyMe's strategy centers on AI personalization depth and Indian dietary accuracy as its primary competitive moats, building a subscription-first business with B2B corporate wellness contracts providing revenue predictability.

Fittr

Fittr is a community-driven fitness transformation platform headquartered in Pune. The platform built its differentiation on a peer coaching and community support model where transformation coaches, many of whom are Fittr users who achieved personal fitness goals, provide personalized plans and accountability support to paying members at accessible price points well below premium one-on-one coaching alternatives.

- Product Portfolio: Fittr App with AI-guided workout plans, nutrition tracking, and progress analytics.

- Recent Developments: In April 2020, Fittr, a Pune-based fitness technology platform, raised $2 million in a pre-Series A funding round led by Surge, the early-stage accelerator program of Sequoia Capital India, marking a key step in its growth journey. The company, which operates a community-driven digital fitness ecosystem, has built a large global user base while remaining profitable since inception, supported by a freemium model that offers personalized coaching and subscription-based services.

- Strategic Focus: Fittr's community and coach marketplace model creates network effects where user transformation success stories generate organic user acquisition through social sharing, reducing paid marketing dependence and supporting the platform's affordability positioning relative to premium corporate wellness products.

Fitbit (Google LLC.)

Google LLC, through its Fitbit acquisition completed in 2021. Google's combined fitness platform strategy integrates wearable hardware health tracking with Android operating system-level health data management, positioning Google as the central health data infrastructure provider for India's Android-dominant fitness app ecosystem.

- Product Portfolio: Fitbit App for Fitbit wearable users with step tracking, heart rate monitoring, sleep analysis, and workout detection; Google Fit for Android device health data aggregation, step counting, and third-party fitness app data consolidation; Google Health Connect for cross-app health data sharing on Android.

- Recent Developments: In August 2025, Google introduced an AI-powered personal health coach within its Fitbit ecosystem, signalling a shift toward more proactive and personalized digital health solutions. Built on its Gemini AI models, the coach leverages user data, such as activity levels, sleep patterns, and health metrics, to deliver tailored recommendations, adaptive workout plans, and real-time wellness guidance based on individual goals and daily routines.

- Strategic Focus: Google's fitness platform strategy focuses on establishing Android health data infrastructure dominance through Google Health Connect as the interoperability standard, while Fitbit hardware maintains premium wearable market presence in urban India.

Market Concentration Analysis

The India fitness app market is moderately fragmented at the national level, reflecting significant regional concentration among domestic champions in specific user segments, with no single company holding more than 15–20% of total India market revenue. The market is bifurcated between the Android freemium mass-market segment dominated by global platforms (Nike, Google, Samsung, MyFitnessPal) offering premium-quality free content, and the paid subscription segment where domestic leaders cult.fit and HealthifyMe hold stronger positions through India-specific content depth and AI personalization localization.

Consolidation dynamics at the segment level are more advanced than overall market fragmentation suggests. cult.fit's physical gym network and digital platform combination, through its 400+ city-center footprint, creates a structurally defensible moat in the omnichannel fitness segment unavailable to pure-play digital competitors. Global consolidation through strategic investment and partnerships is occurring primarily through telecom and insurance companies acquiring fitness app stakes as healthcare engagement enablers, Reliance Jio's health platform investments and IRDAI's wellness program frameworks are the primary consolidation catalysts shaping India's fitness app ownership landscape through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Wearable devices at ~24.1% CAGR through 2034 represent the highest-growth device segment, driven by India's affordable smartwatch ecosystem from boAt, Noise, and Fire-Boltt that is democratizing biometric health tracking across mid-income demographics. AI-powered coaching subscriptions integrating wearable biometric data with adaptive workout plans represent the fastest-growing premium revenue category, with HealthifyMe's Ria AI and cult.fit's AI coaching demonstrating successful subscription conversion rates among India's urban professional fitness demographic aged 25–40.

Emerging Markets

East India at an estimated ~17.5% CAGR is among the fastest-growing regional markets for India's fitness app industry through 2034. Odisha's expanding urban middle class, Jharkhand's improving digital infrastructure, and Kolkata's growing corporate wellness culture are creating new high-potential fitness app user cohorts. Tier-2 and tier-3 cities across all four regions—including Lucknow, Jaipur, Coimbatore, Nagpur, and Bhubaneswar—represent the market's next 100 million addressable users, requiring vernacular language content, offline functionality for variable internet connectivity, and affordable subscription tiers priced at INR 99–199 per month rather than premium urban price points of INR 499–999.

Venture & Investment Trends

Venture capital investment in India's fitness tech sector peaked at USD 387.9 million in 2021, with over 100 VCs having backed the sector. Despite a funding slowdown to approximately USD 7 million in 2025, strategic investment from insurance companies, telecom operators, and corporate wellness program aggregators is replacing VC capital as the dominant growth financing mechanism. IRDAI's wellness integration framework, enabling fitness app data to inform health insurance premium structures, is attracting insurance-sector capital into fitness platform equity and data partnerships. Chiratae Ventures, Blume Ventures, and Kalaari Capital remain the most active domestic investors, supporting companies including Fitbudd, AyuRythm, and Fittr in emerging niche fitness verticals including women's health, senior fitness, and mental wellness.

Future Market Outlook (2026-2034)

The India fitness app market is forecast to expand from USD 521.06 Million in 2025 to USD 2,912.10 Million by 2034 at a CAGR of 18.69%, adding approximately USD 2,391 Million in incremental annual market value over the forecast period. This sustained high-growth trajectory reflects the convergence of India's digital infrastructure expansion, rising health consciousness, and structural demographic advantages, with 650 million Indians below age 35 representing a fitness app consumer cohort at the peak of long-term health investment motivation, digital literacy, and disposable income growth.

Three technology forces will most significantly shape the India fitness app industry through 2034. AI personalization depth will transition from a premium differentiator to a table-stakes capability, compelling all market participants to invest in machine learning coaching infrastructure or exit to commoditized free-tier positioning.

Research Methodology

Primary Research

Primary research encompassed structured interviews with India fitness app industry stakeholders, including senior product managers at domestic fitness platforms, corporate wellness program procurement specialists, certified personal trainers and nutritionists active on digital coaching marketplaces, app store category managers, and health insurance product teams developing wellness-linked premium structures. Primary data validated market sizing, platform and device segment shares, regional demand estimates, and technology adoption timelines across tier-1, tier-2, and tier-3 Indian city categories.

Secondary Research

Key secondary sources include Telecom Regulatory Authority of India (TRAI) subscriber data, Indian Council of Medical Research (ICMR) non-communicable disease burden reports, Ministry of Health and Family Welfare digital health policy documentation, Ayushman Bharat Digital Mission (ABDM) enrollment statistics, Google Play Store and Apple App Store fitness category analytics, International Diabetes Federation Diabetes Atlas, IRDAI insurance wellness program regulatory circulars, and industry publications covering India's digital health, fitness technology, and consumer mobile application markets.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating smartphone penetration rates, internet subscriber growth trajectories, consumer health expenditure data, wearable device shipment forecasts, corporate wellness program adoption rates, and historical India fitness app market evolution patterns from 2020 through 2025. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty, regulatory evolution risk, and technology adoption pace variation across India's highly heterogeneous geographic and demographic user segments.

India Fitness App Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Exercise and Weight Loss, Diet and Nutrition, Activity Tracking, Others |

| Platforms Covered | Android, iOS, Others |

| Devices Covered | Smartphones, Tablets, Wearable Devices |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Curefit Healthcare Pvt Ltd, HealthifyMe Wellness Private Limited, FITPASS, Fittr, Nike, Inc., MyFitnessPal, Inc., Fitbit (Google LLC.), Azumio, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India fitness app market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India fitness app market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India fitness app industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Fitness App Market Report

The India fitness app market size reached USD 521.06 Million in 2025, reflecting sustained demand driven by rising smartphone penetration, increasing health consciousness among urban Indians, and growing adoption of AI-powered personalized fitness solutions across metro and semi-urban geographies.

The market is projected to reach USD 2,912.10 Million by 2034, growing at a CAGR of 18.69% during 2026-2034, driven by AI personalization advancement, wearable device ecosystem expansion, insurance-integrated wellness programs, and India's expanding digital health infrastructure through the Ayushman Bharat Digital Mission.

Android dominates with a 72.5% platform share in 2025, reflecting India's predominantly Android-driven smartphone ecosystem across urban and semi-urban geographies where budget-to-mid-range Android devices from Samsung, Xiaomi, Vivo, and Realme place fitness app access within reach of the mass-market consumer base.

Wearable devices represent the fastest-growing segment at ~24.1% CAGR through 2034, driven by India's booming affordable smartwatch market from domestic brands including boAt, Noise, and Fire-Boltt, which collectively shipped over 25 million units annually by FY 2023-24, democratizing biometric health tracking beyond premium device users.

North India commands the largest regional share at 31.7% in 2025, driven by Delhi-NCR corporate wellness demand, Punjab and Haryana gym culture, and high smartphone penetration among working professionals aged 25–40 in India's capital region and surrounding tier-1 cities.

The primary growth drivers include rising smartphone and internet penetration exceeding 850 million connected users, growing lifestyle disease burden driving preventive health investment, government Ayushman Bharat Digital Mission digital health infrastructure creation, AI-powered personalization improving user retention and engagement, and India's expanding corporate wellness program adoption among major IT and financial services employers.

Leading companies include Curefit Healthcare Pvt Ltd, HealthifyMe Wellness Private Limited, FITPASS, Fittr, Nike, Inc., MyFitnessPal, Inc., Fitbit (Google LLC.), Azumio, Inc., and others.

Key fitness app types in the India market include exercise and weight loss apps offering structured workout programs, diet and nutrition apps providing calorie tracking and meal planning, activity tracking apps monitoring steps and daily movement, and comprehensive wellness platforms integrating multiple fitness, nutrition, sleep, and mental wellness functions across a unified user experience.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)