India Flat Glass Market Size, Share, Trends and Forecast by Technology, Product Type, Raw Material, End Use, Type, End Use Industry, and Region, 2026-2034

India Flat Glass Market Summary:

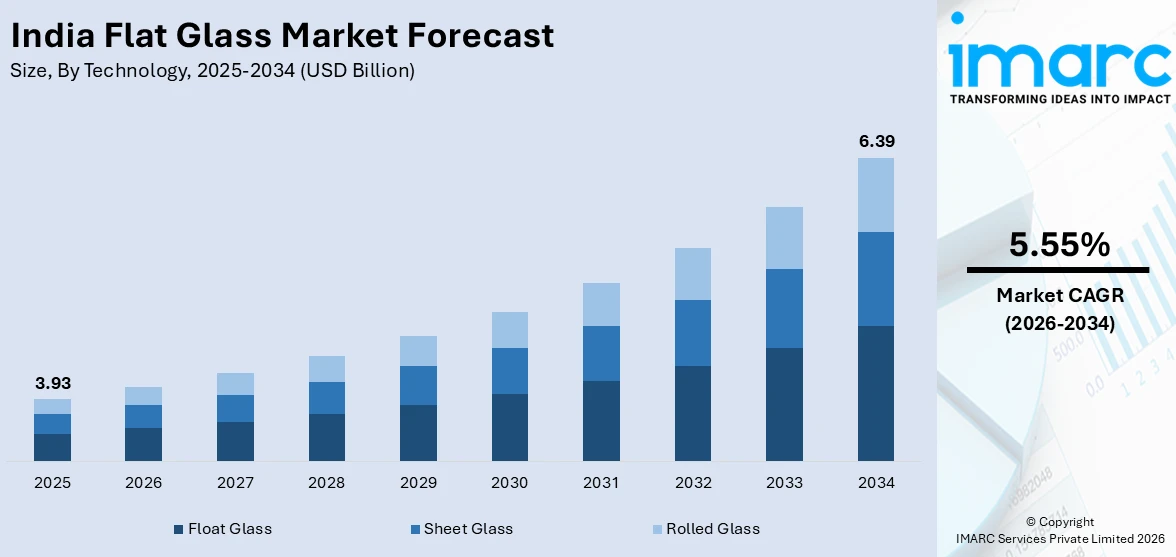

The India flat glass market size was valued at USD 3.93 Billion in 2025 and is projected to reach USD 6.39 Billion by 2034, growing at a compound annual growth rate of 5.55% from 2026-2034.

The market is driven by rapid urbanization, expanding construction activities, increasing automotive production, and rising demand for energy-efficient building materials across India. Growing adoption of solar energy applications and government infrastructure development initiatives further support demand. Advancements in glass processing technologies and the increasing preference for aesthetically appealing and sustainable architectural designs are also strengthening the India flat glass market share.

Key Takeaways and Insights:

- By Technology: Float glass dominates the market with a share of 56% in 2025, driven by its superior optical clarity, cost-effective mass production capabilities, and extensive applications across architectural glazing and automotive industries.

- By Product Type: Basic float glass leads the market with a share of 25% in 2025, owing to its widespread availability, affordability, and versatile applicability across residential and commercial construction projects.

- By Raw Material: Sand represents the largest segment with a market share of 40% in 2025, driven by being the primary silica source essential for glass manufacturing and its abundant domestic availability across major Indian states.

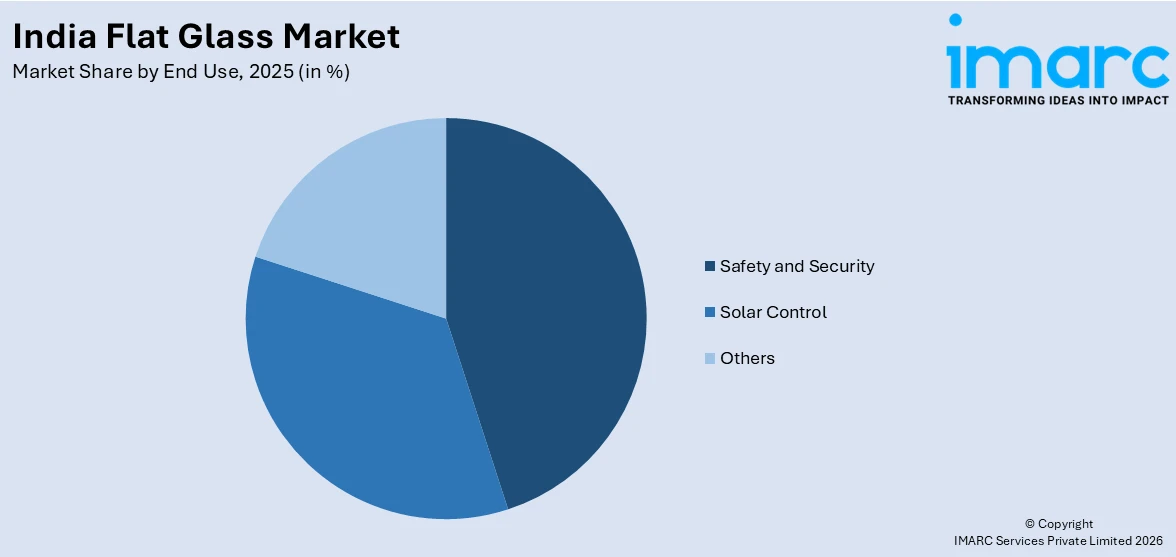

- By End Use: Safety and security dominate the market with a share of 39% in 2025, owing to increasing building safety regulations and growing demand for laminated and toughened glass in commercial buildings.

- By Type: Fabricated dominates the market with a share of 60% in 2025, driven by growing preference for processed and customized glass solutions offering enhanced thermal insulation and solar control functionalities.

- By End Use Industry: Construction represents the market with a share of 45% in 2025, owing to massive infrastructure development programs, rapid urbanization in tier-one and tier-two cities, and expanding residential housing projects.

- Key Players: The India flat glass market exhibits a moderately consolidated competitive landscape, with established domestic manufacturers and multinational corporations competing across product segments. Market participants differentiate through technological innovation, production capacity expansion, product portfolio diversification, and strategic distribution network development.

To get more information on this market Request Sample

The India flat glass market is experiencing robust growth, primarily fueled by the country's unprecedented construction boom and rapid urbanization across metropolitan and emerging cities. The expanding automotive manufacturing sector, supported by government policies promoting domestic production, is generating substantial demand for high-quality glazing solutions. In April 2025, Asahi India Glass Ltd partnered with INOX Air Products to commission India’s first green hydrogen facility for float glass manufacturing at its Soniyana plant in Rajasthan, marking a major step toward sustainable glass production and decarbonisation. Additionally, India's ambitious renewable energy targets are driving significant adoption of flat glass in solar panel manufacturing. The growing preference for energy-efficient and sustainable building materials, coupled with increasing consumer awareness about aesthetic architectural designs, is further augmenting demand. Rising disposable incomes and evolving lifestyle preferences are encouraging the use of premium glass products in residential and commercial applications.

India Flat Glass Market Trends:

Growing Adoption of Energy-Efficient and Smart Glass Solutions

The India flat glass market is witnessing a significant shift toward energy-efficient glazing solutions as architects and developers increasingly prioritize sustainable building designs. Smart glass technologies, including electrochromic and thermochromic variants, are gaining traction in premium commercial and residential projects. As per sources, Saint‑Gobain Glass India launched the production of India’s first low‑carbon glass with an estimated approximately 40 % reduction in carbon footprint compared to existing products, integrating it into its energy‑efficient glass portfolio to support decarbonised construction. These advanced glass solutions offer dynamic light and heat management capabilities, reducing dependence on artificial climate control systems. The integration of low-emissivity coatings with flat glass products is becoming standard practice in green-certified buildings, reflecting the broader industry movement toward environmentally responsible construction practices across Indian urban centers.

Expansion of Solar Energy Applications Driving Glass Demand

India's accelerating transition toward renewable energy sources is creating substantial opportunities for flat glass manufacturers specializing in photovoltaic module components. The government's commitment to expanding solar power generation capacity is stimulating unprecedented demand for specialized solar glass variants. In March 2025, Borosil Renewables announced a Rs 900 crore investment to boost its solar glass manufacturing capacity in Gujarat to 10 GW by 2026, underscoring industry efforts to scale domestic supply for solar applications. Manufacturers are investing in developing ultra-clear and anti-reflective glass products specifically designed to maximize solar energy conversion efficiency. This trend is encouraging the establishment of dedicated solar glass production facilities across key industrial corridors, fundamentally reshaping the product mix and strategic priorities of domestic flat glass producers.

Rising Demand for Lightweight Automotive Glazing Solutions

The automotive industry's evolving requirements are significantly influencing the India flat glass market landscape. Vehicle manufacturers are increasingly seeking lightweight yet durable glazing solutions that contribute to overall fuel efficiency improvements without compromising passenger safety or comfort. In June 2024, Asahi India Glass Ltd (AIS) reported robust demand for high‑value automotive glass products, including UV‑cut side window glasses and sunroof glass, and projected supplies of over 1.5 million sunroof glasses in FY 2025 to meet rising OEM requirements for advanced glazing features. The growing emphasis on panoramic sunroofs, heads-up display compatible windshields, and advanced driver assistance system integrated glass is transforming automotive glazing specifications.

Market Outlook 2026-2034:

The India flat glass market is poised for sustained revenue growth during the forecast period, supported by accelerating infrastructure development, expanding automotive production, and rising solar energy installations. Revenue generation is expected to be primarily driven by the construction sector's continued expansion across metropolitan and tier-two cities. Increasing investments in smart city projects, industrial corridors, and commercial real estate developments are anticipated to significantly boost flat glass consumption. The market revenue trajectory is further reinforced by technological advancements in glass processing and growing exports of value-added glass products. The market generated a revenue of USD 3.93 Billion in 2025 and is projected to reach a revenue of USD 6.39 Billion by 2034, growing at a compound annual growth rate of 5.55% from 2026-2034.

India Flat Glass Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Technology |

Float Glass |

56% |

|

Product Type |

Basic Float Glass |

25% |

|

Raw Material |

Sand |

40% |

|

End Use |

Safety and Security |

39% |

|

Type |

Fabricated |

60% |

|

End Use Industry |

Construction |

45% |

Technology Insights:

- Float Glass

- Sheet Glass

- Rolled Glass

Float glass dominates with a market share of 56% of the total India flat glass market in 2025.

Float glass technology dominates the India flat glass market, serving as the most widely adopted manufacturing method across the industry. This production process involves floating molten glass on a bed of molten tin, producing sheets with exceptional surface uniformity, optical clarity, and consistent thickness. The technology's ability to produce large volumes of high-quality flat glass at competitive costs makes it the preferred choice for manufacturers serving diverse end-use industries including construction, automotive, and electronics sectors across the Indian market.

The sustained dominance of float glass technology is attributable to continuous improvements in production efficiency and the expanding range of downstream applications. Indian manufacturers have invested significantly in modernizing their float glass production lines, incorporating advanced process controls and energy recovery systems. Technology serves as the essential foundation for producing value-added variants including toughened, laminated, coated, and insulated glass products, thereby reinforcing its central role in the broader flat glass value chain.

Product Type Insights:

- Basic Float Glass

- Toughened Glass

- Coated Glass

- Laminated Glass

- Insulated

- Extra Clear Glass

- Others

Basic float glass leads with a share of 25% of the total India flat glass market in 2025.

Basic float glass leads the product type segment in the India flat glass market, serving as the most widely consumed glass variant across multiple applications. Its affordability, widespread availability, and versatile applicability make it the foundation of the domestic glass industry. Basic float glass is extensively used in standard window glazing, interior partitions, mirrors, and general-purpose architectural applications where advanced performance characteristics are not mandatory, making it accessible to a broad spectrum of consumers and construction projects.

The product's leading position is sustained by the massive volume demand generated by India's residential construction sector and small-scale commercial projects. Basic float glass serves as the essential raw material for downstream processors who convert it into toughened, laminated, and coated glass products. The establishment of new production capacities by domestic manufacturers is improving regional availability and reducing dependence on imports, further strengthening the product's accessibility and competitive pricing across distribution channels.

Raw Material Insights:

- Sand

- Soda Ash

- Recycled Glass

- Dolomite

- Limestone

- Others

Sand exhibits a clear dominance with a 40% share of the total India flat glass market in 2025.

Sand represents the largest raw material segment in the India flat glass market, functioning as the primary source of silica, which constitutes the principal ingredient in glass manufacturing. High-quality silica sand with appropriate chemical composition and particle size is essential for producing flat glass with desired optical and physical properties. In September 2025, high‑quality silica sand from Shankargarh in Uttar Pradesh emerged as a key supplier to glass manufacturers, with approx. 22,000 tons shipped in June alone to meet increased demand from both vehicle and bottle glass producers nationwide.

The dominance of sand as the leading raw material is fundamentally linked to its irreplaceable role in the glass melting process, where it typically accounts for the highest proportion of the batch composition by weight. Manufacturers prioritize sourcing high-purity silica sand to ensure consistent product quality and minimize defects in the finished glass. Growing environmental regulations around sand mining are encouraging industry to explore sustainable sourcing practices and optimize batch compositions to improve resource efficiency.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Safety and Security

- Solar Control

- Others

Safety and security leads with a market share of 39% of the total India flat glass market in 2025.

The safety and security dominate the end-use classification in the India flat glass market, reflecting the growing emphasis on protective glazing applications across commercial, institutional, and residential buildings. This segment encompasses laminated glass, toughened glass, and other processed glass products designed to withstand impact, resist break-ins, and minimize injury risks from glass breakage. In 2025, Agarwal Toughened Glass India Ltd, a leading safety glass manufacturer known for laminated, double‑glazed, and insulated safety glass products, reported a more than doubled Profit After Tax for H2 FY25, underscoring surging demand for value‑added safety glazing solutions across infrastructure and commercial sectors in India.

The growing demand for safety and security glass applications is further reinforced by the expanding commercial real estate sector, where building regulations increasingly mandate the use of safety glazing in facades, storefronts, and public areas. Educational institutions, healthcare facilities, and government buildings represent significant demand centers for safety glass products. The automotive sector's requirement for laminated windshields and toughened side windows additionally contributes to this segment's prominent market position across the entire value chain.

Type Insights:

- Fabricated

- Non-Fabricated

Fabricated dominates with a market share of 60% of the total India flat glass market in 2025.

Fabricated dominates the segment in the India flat glass market, reflecting the industry's progressive shift toward processed and value-added glass products. Fabricated glass undergoes additional manufacturing processes such as tempering, laminating, coating, insulating, and other treatments that enhance its functional properties beyond those of basic unprocessed glass. The growing demand for glass products with specialized characteristics such as thermal insulation, solar control, acoustic dampening, and impact resistance is driving the sustained expansion of this segment.

The leading position of fabricated glass is supported by the increasing sophistication of building design requirements and evolving consumer expectations regarding glass performance. Architects and developers are specifying processed glass solutions that meet stringent energy efficiency standards, safety regulations, and aesthetic requirements for modern construction projects. The expanding network of domestic glass processing facilities is improving the availability and affordability of fabricated glass products, enabling broader market penetration across mainstream residential and industrial segments.

End Use Industry Insights:

- Construction

- Automotive

- Solar Energy

- Electronics

- Others

Construction leads with a share of 45% of the total India flat glass market in 2025.

The construction represents the largest end-use industry segment in the India flat glass market, driven by the country's massive and ongoing infrastructure development programs. Rapid urbanization, expanding commercial real estate, growing residential housing demand, and large-scale government infrastructure initiatives are generating substantial and sustained demand for diverse flat glass products. Glass facades, curtain walls, windows, doors, partitions, skylights, and railings represent the primary consumption channels within the construction sector across the country.

The construction sector's dominance in flat glass consumption is further reinforced by evolving architectural trends that increasingly favor glass-intensive building designs for their aesthetic appeal, natural lighting benefits, and modern visual character. Smart city development projects, industrial corridor construction, metro rail expansion, and airport modernization programs are creating additional demand avenues for specialized glass products. The growing preference for green building certifications is also driving adoption of advanced glazing solutions including insulated and low-emissivity systems.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India represents a significant share in the India flat glass market, driven by extensive construction activities across major urban centers. The region benefits from robust infrastructure development programs, expanding residential and commercial real estate projects, and the presence of key industrial manufacturing hubs that generate sustained demand for diverse flat glass products across multiple end-use applications.

West and Central India hold a prominent position in the India flat glass market, supported by thriving construction and automotive manufacturing sectors. The region houses several major flat glass production facilities and benefits from well-established industrial corridors, strong commercial real estate growth, and proximity to key raw material sourcing locations driving consistent manufacturing output and market expansion.

South India contributes significantly to the India flat glass market, driven by rapid urbanization and expanding construction activities across key states. The region's growing information technology and commercial office infrastructure, thriving automotive manufacturing ecosystem, and increasing adoption of solar energy applications are collectively generating strong and sustained demand for diverse flat glass products and glazing solutions.

East India is an emerging contributor to the India flat glass market, supported by accelerating infrastructure development and urbanization across key states. The region benefits from expanding government-led construction initiatives, growing residential housing demand, and increasing industrial development activities that are gradually strengthening flat glass consumption and creating promising new market growth opportunities.

Market Dynamics:

Growth Drivers:

Why is the India Flat Glass Market Growing?

Rapid Urbanization and Expanding Construction Activities

India's accelerating urbanization is serving as a primary catalyst for the flat glass market, with millions of people migrating to cities annually, creating unprecedented demand for residential, commercial, and institutional construction. In March 2026, the Uttar Pradesh Real Estate Regulatory Authority approved 36 new real estate projects worth approximately Rs 8,778 crore, with nearly half concentrated in Gautam Budh Nagar (including Noida), reflecting strong construction momentum driven by infrastructure expansions and urban development. The government's ambitious infrastructure development programs, including smart city missions, affordable housing schemes, and industrial corridor projects, are generating massive requirements for flat glass products.

Growing Solar Energy Installations and Renewable Energy Targets

India's ambitious renewable energy targets are creating significant growth opportunities for the flat glass market, particularly in the solar energy segment. The government's commitment to substantially expanding solar power generation capacity is driving unprecedented demand for photovoltaic module glass, including ultra-clear and tempered glass variants specifically designed for solar applications. According to reports, India’s PLI scheme enabled approval of ~48.3 GW solar module manufacturing capacity across Gujarat, Tamil Nadu, Andhra Pradesh, and Odisha, boosting domestic production and supporting solar glass demand. The establishment of large-scale solar parks, rooftop solar programs, and floating solar installations across the country is generating consistent and growing requirements for specialized flat glass products, encouraging domestic manufacturers to expand dedicated production capacities.

Expanding Automotive Manufacturing and Vehicle

Production India's growing automotive industry is providing substantial impetus to the flat glass market, with increasing vehicle production volumes driving consistent demand for automotive glazing products. The country's emergence as a major automotive manufacturing hub for both domestic consumption and exports is stimulating investment in automotive-grade glass production capabilities. In 2025, India’s automobile exports rose by 19% to over 5.3 million vehicles in FY 2024‑25, buoyed by strong overseas demand for passenger vehicles, two‑wheelers, and commercial vehicles, reflecting heightened production and global competitiveness that underpins demand for advanced automotive glazing solutions. The evolving vehicle design landscape, characterized by larger windshields, panoramic sunroofs, and advanced glazing features, is increasing the glass content per vehicle and driving demand for sophisticated flat glass solutions catering to modern automotive design and safety requirements.

Market Restraints:

What Challenges the India Flat Glass Market is Facing?

Volatile Raw Material Prices and Energy Costs

The India flat glass market faces significant headwinds from fluctuating prices of key raw materials, particularly soda ash and silica sand, along with rising energy costs for glass furnace operations. Natural gas and petroleum coke prices directly impact manufacturing economics, with energy representing a substantial portion of total production costs, creating uncertainty in pricing strategies and compressing profit margins for manufacturers.

Environmental Regulations and Compliance Burden

Increasingly stringent environmental regulations governing emissions, waste management, and resource utilization in glass manufacturing are imposing significant compliance costs on industry participants. Glass production is inherently energy-intensive, and regulatory requirements for emission control equipment, continuous monitoring systems, and cleaner fuel adoption necessitate substantial capital investments. Smaller manufacturers face disproportionate compliance burdens, potentially leading to operational challenges and requiring significant facility upgrades.

Import Competition and Pricing Pressures

The India flat glass market contends with competitive pressures from imported glass products, particularly from countries with established large-scale manufacturing infrastructure and lower production costs. Imported flat glass, especially in value-added categories, can undercut domestic pricing, creating challenges for local manufacturers investing in capacity expansion and technology upgradation. Persistent competitively priced imports continue exerting downward pressure on domestic margins.

Competitive Landscape:

The India flat glass market features a moderately consolidated competitive structure characterized by the presence of established domestic manufacturers alongside global industry participants operating through local subsidiaries and joint ventures. Market leaders leverage extensive production capacities, vertically integrated operations, and widespread distribution networks to maintain their competitive positions. The competitive landscape is shaped by ongoing investments in capacity expansion, technological modernization, and product portfolio diversification. Smaller regional players compete primarily in basic glass segments while larger participants increasingly focus on value-added and specialty glass products. Strategic collaborations, backward integration into raw material sourcing, and forward integration into glass processing represent key competitive strategies being pursued across the industry.

Recent Developments:

- In January 2025, Gold Plus Glass Industry Ltd, India’s second‑largest float glass producer, commissioned its new manufacturing facility in Karnataka, adding 584,000 metric tons per annum float glass and 109,500 tons per annum solar glass capacity. With this expansion, its total float glass output now exceeds one million tonnes annually, strengthening domestic supply for construction and solar use.

India Flat Glass Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Float Glass, Sheet Glass, Rolled Glass |

| Product Types Covered | Basic Float Glass, Toughened Glass, Coated Glass, Laminated Glass, Insulated, Extra Clear Glass, Others |

| Raw Materials Covered | Sand, Soda Ash, Recycled Glass, Dolomite, Limestone, Others |

| End Uses Covered | Safety and Security, Solar Control, Others |

| Types Covered | Fabricated, Non-Fabricated |

| End Use Industries Covered | Construction, Automotive, Solar Energy, Electronics, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Flat Glass Market Research Report and Industry Forecast Report

The India flat glass market size was valued at USD 3.93 Billion in 2025.

The India flat glass market is expected to grow at a compound annual growth rate of 5.55% from 2026-2034 to reach USD 6.39 Billion by 2034.

Float glass held the largest India flat glass market share, driven by its superior optical clarity, cost-effective production capabilities, and extensive applications across construction, automotive, and solar energy industries throughout the country.

Key factors driving the India flat glass market include rapid urbanization and expanding construction activities, growing solar energy installations, rising automotive production, increasing demand for energy-efficient building materials, and government infrastructure initiatives.

Major challenges include volatile raw material and energy costs, stringent environmental compliance requirements, import competition from established global producers, high capital intensity of manufacturing operations, supply chain constraints, and fluctuating demand patterns across key end-use industries including construction and automotive sectors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)