India Flexible Packaging Market Size, Share, Trends and Forecast by Product Type, Raw Material, Printing Technology, Application, and Region, 2026-2034

India Flexible Packaging Market Size, Share, Trends & Forecast (2026-2034)

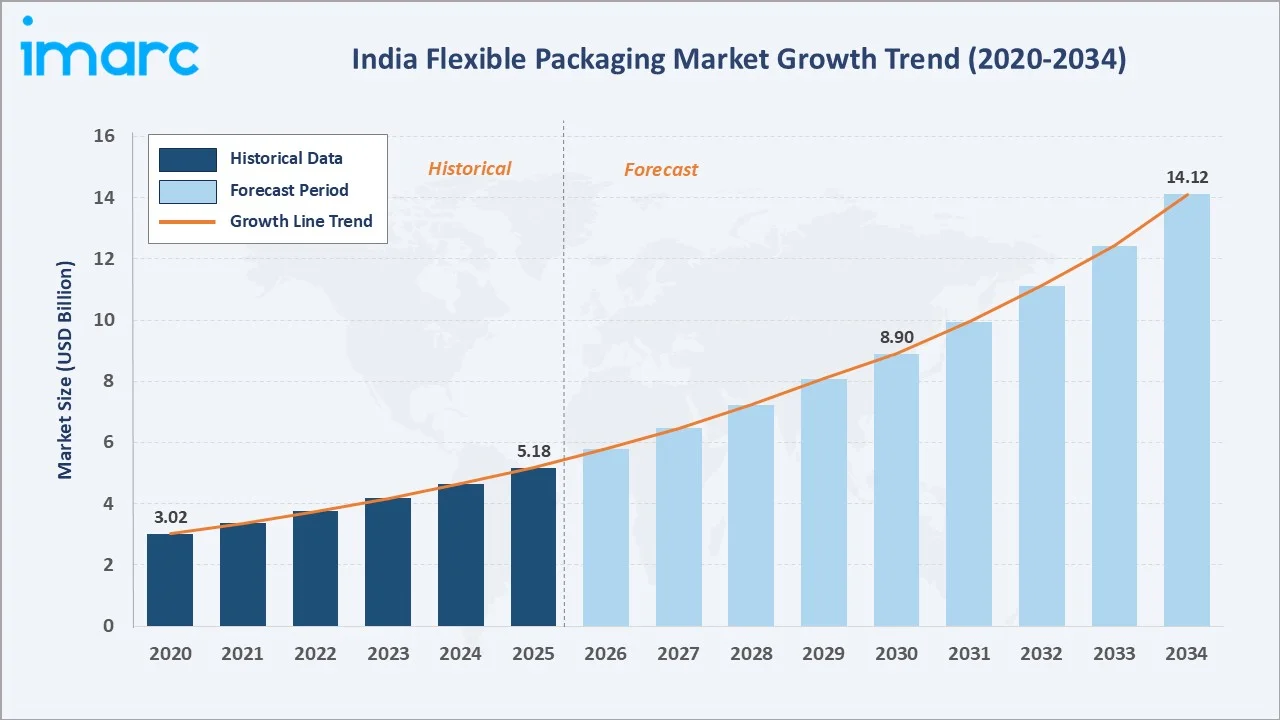

The India flexible packaging market reached USD 5.18 Billion in 2025 and is projected to reach USD 14.12 Billion by 2034, growing at a CAGR of 11.43% during 2026-2034. The market is driven by rapid e-commerce expansion, rising packaged food demand, and growing pharmaceutical sector requirements.

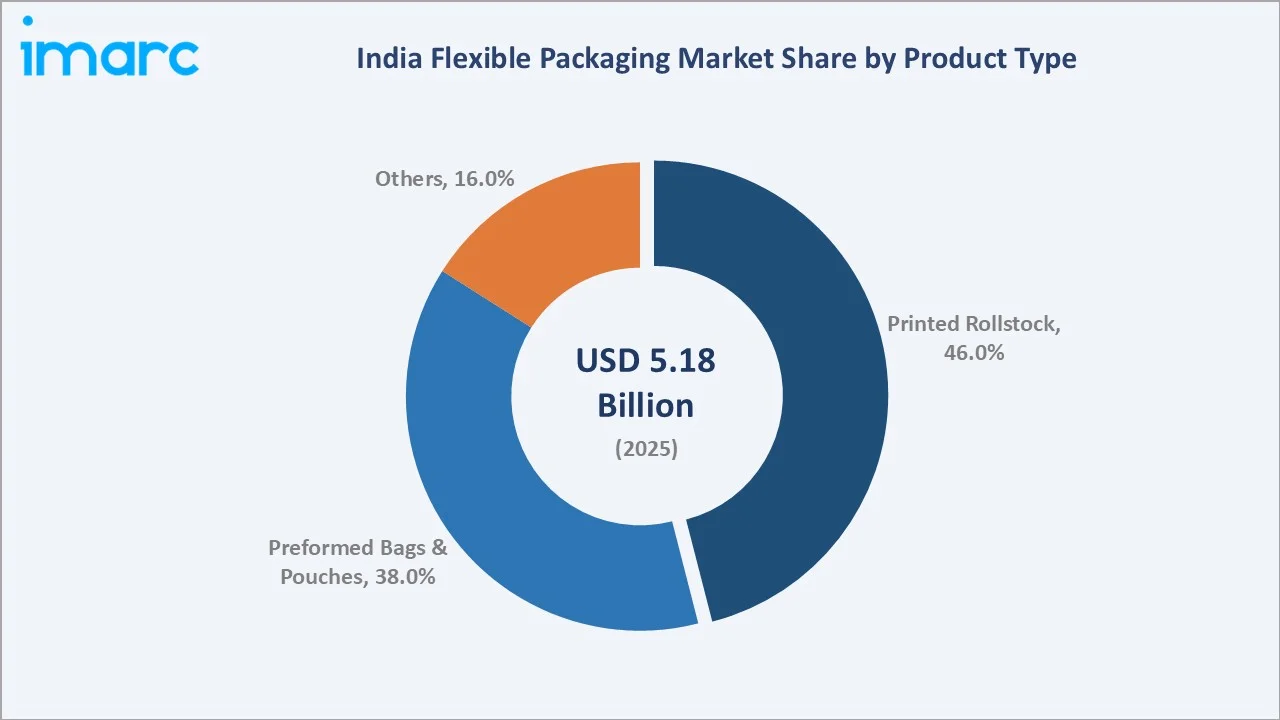

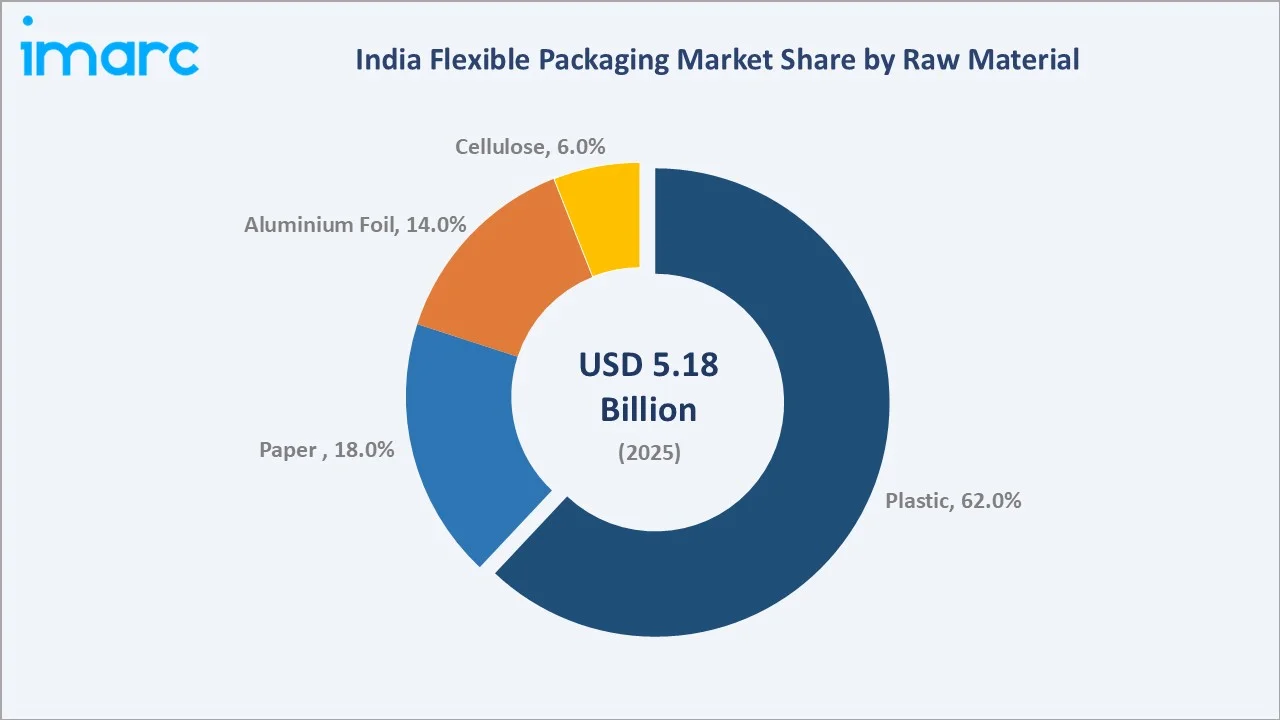

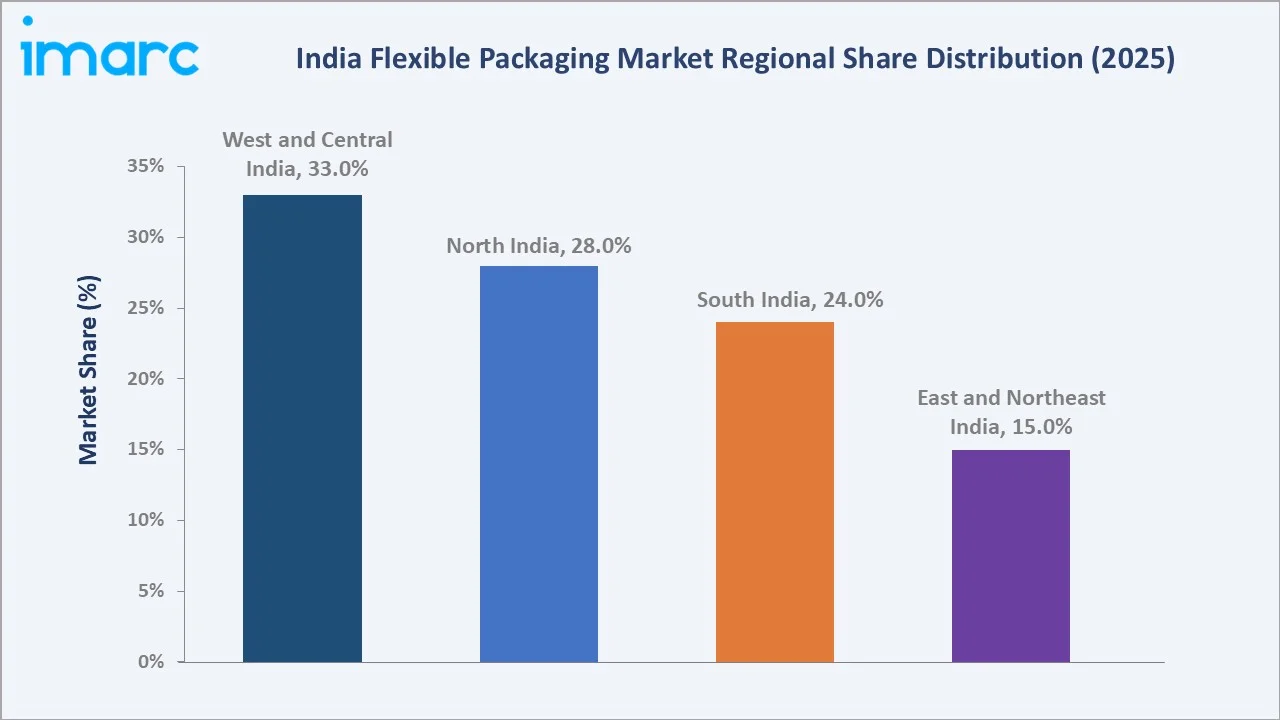

Printed rollstock dominates product type at 46.0%, plastic leads raw material at 62.0%, and West and Central India command the largest regional share at 33.0%, reflecting Maharashtra and Gujarat's concentrated FMCG and pharmaceutical manufacturing base.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.18 Billion |

|

Forecast Market Size (2034) |

USD 14.12 Billion |

|

CAGR (2026-2034) |

11.43% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Printed Rollstock (46.0%, 2025) |

|

Dominant Raw Material |

Plastic (62.0%, 2025) |

|

Leading Region |

West and Central India (33.0%, 2025) |

The India flexible packaging market expanded from USD 3.02 Billion in 2020 to USD 5.18 Billion in 2025, anchored at USD 8.90 Billion in 2030 and forecast to reach USD 14.12 Billion by 2034. Rising consumer incomes, packaged food penetration, and pharmaceutical sector expansion sustained the structural demand trajectory through the historical period.

To get more information on this market, Request Sample

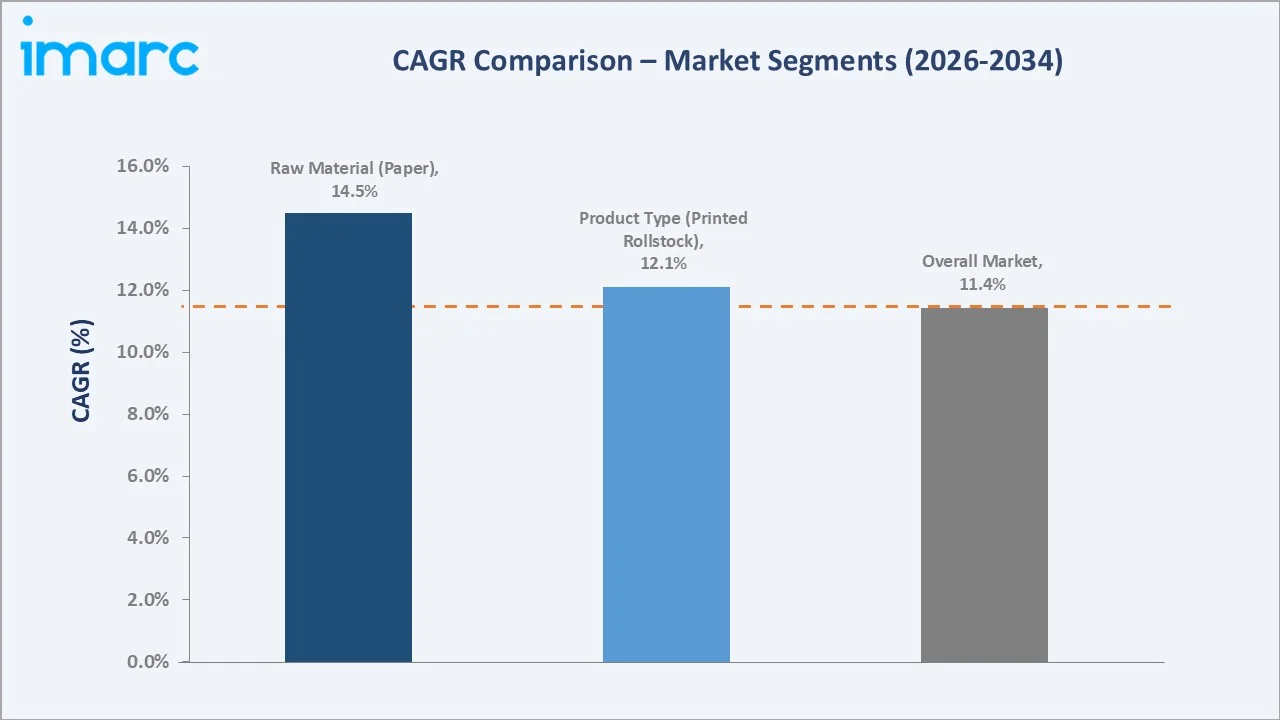

Printed rollstock grows at ~12.1% CAGR as mainstream FMCG and pharma packaging demand accelerates. Paper packaging grows fastest at ~14.5% CAGR as sustainability mandates drive converter investment in fibre-based flexible formats. West and Central India maintains the largest regional share through the forecast period.

Executive Summary

The India flexible packaging market reached USD 5.18 billion in 2025, representing one of India's highest-growth packaging segments, driven by the structural expansion of organised retail, food processing, pharmaceuticals, and e-commerce. The market is projected to reach USD 14.12 billion by 2034.

Printed rollstock at 46.0% dominates by capturing mainstream FMCG, food, and pharmaceutical flexible packaging. Plastic at 62.0% leads raw materials through superior barrier properties and cost efficiency.

West and Central India, at 33.0%, leads regionally through Maharashtra and Gujarat's dominant FMCG and pharmaceutical manufacturing concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Printed Rollstock – 46.0% share (2025) |

|

Dominant Raw Material |

Plastic – 62.0% market share (2025) |

|

Leading Region |

West and Central India – 33.0% market share (2025) |

|

Market Opportunity |

Sustainable mono-material pouches, pharma flexible pack, e-commerce mailers, high-barrier food packaging |

Key Analytical Observations Supporting The Above Data:

- Printed Rollstock at 46.0%: The printed rollstock segment dominates as it provides the optimal balance of print quality, converting efficiency, and cost for high-volume FMCG and pharmaceutical packaging. Widespread adoption across food, personal care, and pharma categories by major Indian and multinational brand owners further strengthens segment demand.

- Plastic at 62.0%: The plastic segment dominates due to superior barrier properties, lightweight nature, and versatility across all flexible packaging formats. Cost efficiency and compatibility with high-speed filling lines make plastic films the preferred raw material for food, pharmaceutical, and FMCG flexible packaging applications.

- West and Central India at 33.0%: The region leads through Maharashtra's dominant FMCG manufacturing base, Gujarat's pharmaceutical packaging cluster, and the concentration of major flexible packaging converters in Mumbai and Ahmedabad, creating India's highest flexible packaging demand density.

India Flexible Packaging Market Overview

The India flexible packaging market encompasses the design, manufacture, and supply of all flexible packaging materials and solutions used across food, beverages, pharmaceuticals, cosmetics, and consumer goods sectors. Flexible packaging includes plastic films, paper, aluminium foil, and cellulose materials formed into pouches, bags, rollstock, and sachets.

The ecosystem integrates raw material and film producers, printing and conversion equipment manufacturers, packaging converters, brand owners, and regulatory bodies. Macroeconomic drivers include India's rising middle class, urbanisation, organised retail expansion, e-commerce growth, and food safety and pharmaceutical packaging regulations.

Market Dynamics

To evaluate market opportunities, Request Sample

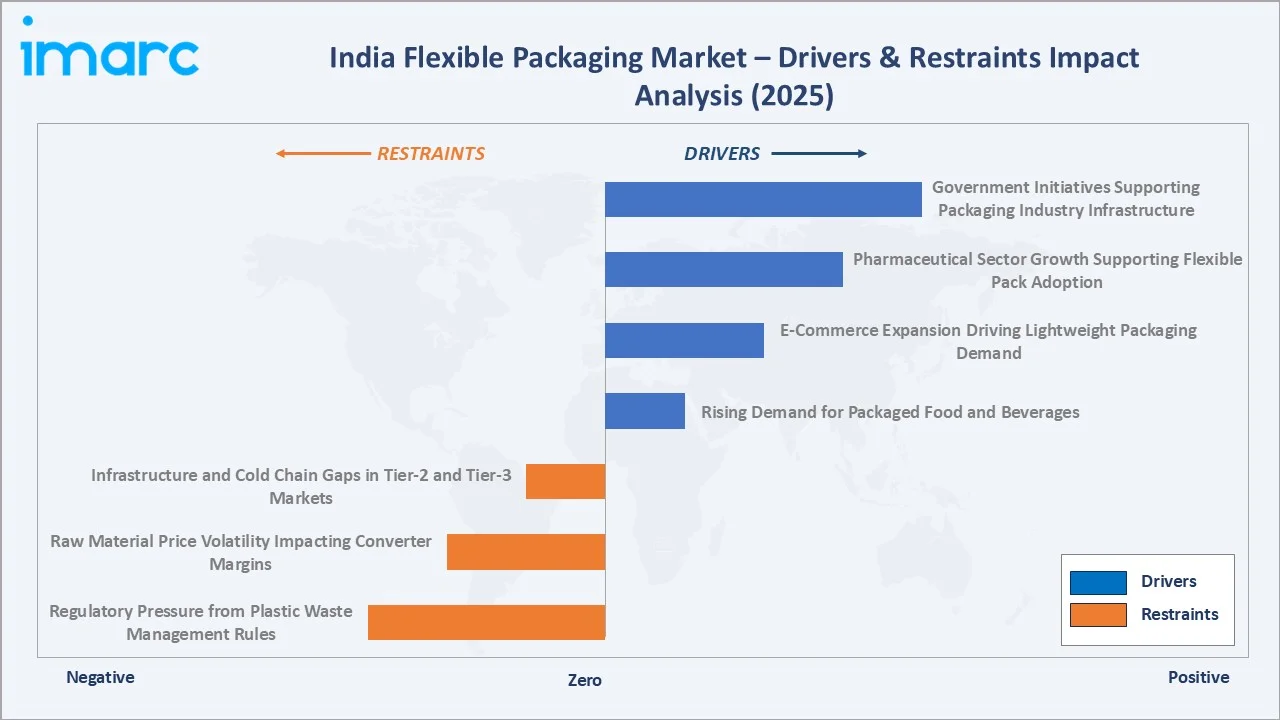

Market Drivers

- Rising Demand for Packaged Food and Beverages: India's expanding urban population and changing dietary habits are accelerating demand for packaged food and beverages. Flexible packaging extends shelf life and reduces transport damage. As organised retail and quick-commerce channels grow, FMCG companies are increasing the use of printed rollstock and preformed pouches, driving converter capacity investment.

- E-Commerce Expansion Driving Lightweight Packaging Demand: The rapid growth of e-commerce and quick-commerce logistics is creating strong demand for lightweight, durable, and protective flexible packaging. Online grocery and FMCG deliveries require tamper-evident, puncture-resistant, and brand-printed flexible solutions, particularly preformed pouches and rollstock formats.

- Pharmaceutical Sector Growth Supporting Flexible Pack Adoption: India's pharmaceutical industry, the world's third largest by volume, is expanding its use of high-barrier flexible packaging for drug sachets, blister packaging backing, and unit-dose pouches. Rising generic drug exports and domestic formulation production are increasing demand for aluminium foil laminates and plastic pharmaceutical flexible packaging.

- Government Initiatives Supporting Packaging Industry Infrastructure: PLI schemes for food processing, Make in India incentives for packaging manufacturers, and cold chain infrastructure investments are supporting flexible packaging industry expansion. Increased food processing investment directly drives demand for high-performance flexible primary packaging.

Market Restraints

- Regulatory Pressure from Plastic Waste Management Rules: India's Plastic Waste Management Rules and EPR mandates are creating compliance costs and formulation challenges for flexible packaging manufacturers. The requirement to transition toward recyclable mono-material structures and incorporate recycled content is increasing R&D expenditure and material costs for packaging converters.

- Raw Material Price Volatility Impacting Converter Margins: Flexible packaging converters face margin pressure from crude oil price volatility, which directly impacts plastic film, adhesive, and ink costs. Aluminium price fluctuations affect foil laminate economics. Input cost uncertainties compress converter profitability and limit capacity investment in smaller regional manufacturers.

- Infrastructure and Cold Chain Gaps in Tier-2 and Tier-3 Markets: Inadequate cold chain infrastructure in non-metro markets limits penetration of premium flexible packaging formats requiring temperature-controlled storage. Distribution inefficiencies in smaller cities reduce the value proposition of high-barrier flexible packaging, constraining market expansion beyond metropolitan centres.

Market Opportunities

- Sustainable Mono-Material Flexible Packaging Development: The transition toward recyclable mono-material polyethylene and polypropylene pouches creates significant growth opportunities for converters investing in high-barrier mono-material technology. As brand owners seek EPR-compliant solutions, manufacturers offering certified recyclable flexible packaging gain competitive advantage and premium pricing.

- High-Growth Pharmaceutical and Nutraceutical Flexible Packaging: Expanding domestic pharmaceutical production, growing nutraceutical consumption, and increasing diagnostic kit packaging requirements are creating high-value flexible packaging demand. Aluminium foil laminate pouches and high-barrier plastic sachets offer significantly higher margins than food-grade flexible packaging formats.

Market Challenges

- Multi-Layer Film Recyclability Complexity: Traditional multi-layer flexible packaging structures combining plastics, aluminium, and adhesives are difficult to recycle and face increasing regulatory scrutiny. Reformulating established multi-material laminates without sacrificing barrier performance requires significant technical investment, creating challenges for converters.

- Fragmented Converter Landscape Limiting Technology Investment: India's flexible packaging converter market includes numerous small and mid-sized regional players with limited capital for technology investment. This fragmentation constrains industry-wide adoption of advanced printing technologies, high-barrier coating capabilities, and sustainability-driven process innovation.

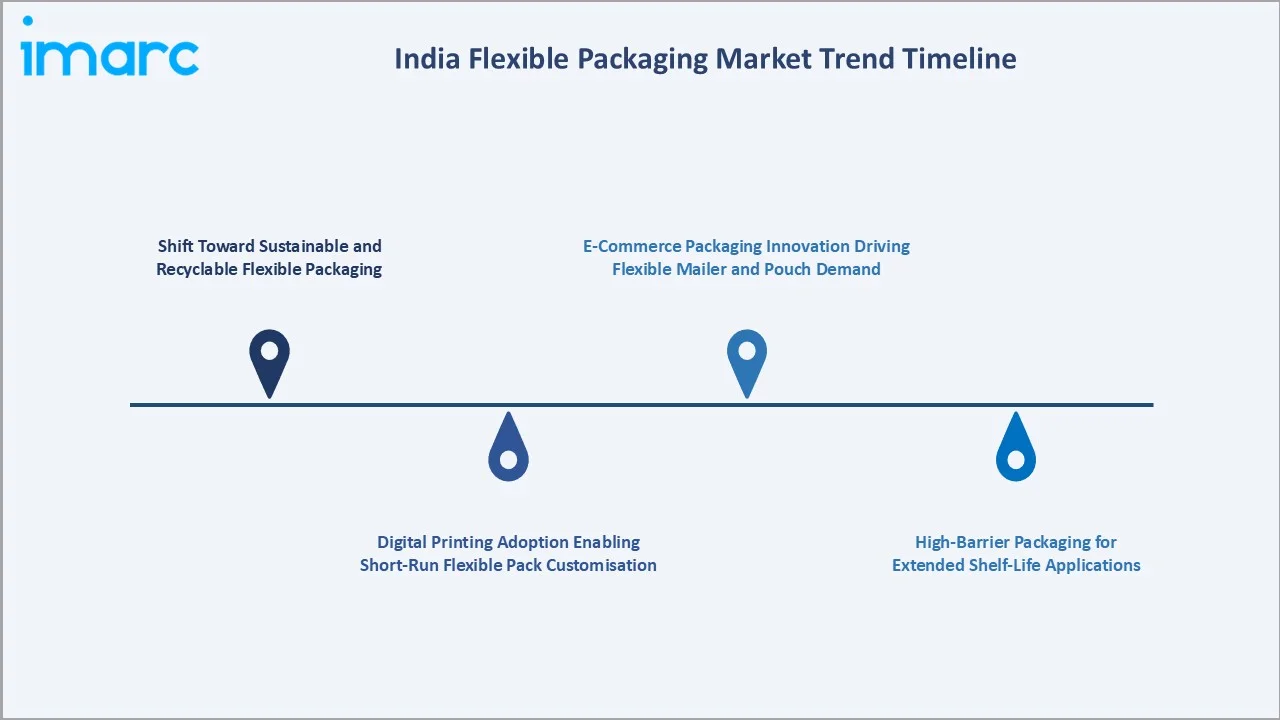

Emerging Market Trends

1. Shift Toward Sustainable and Recyclable Flexible Packaging Structures

Indian converters and brand owners are investing in recyclable mono-material polyethylene and polypropylene flexible packaging structures to comply with EPR mandates and respond to consumer sustainability awareness. Several leading FMCG companies are committed to 100% recyclable flexible packaging targets, accelerating converter investment in high-barrier mono-material film technology.

2. Digital Printing Adoption Enabling Short-Run Flexible Pack Customisation

Digital printing technology adoption by Indian flexible packaging converters is enabling cost-effective short-run production, faster time-to-market, and personalised packaging designs. This supports brand owners in executing seasonal campaigns, regional language packaging, and limited-edition flexible packaging formats without minimum order constraints.

3. High-Barrier Flexible Packaging for Extended Shelf-Life Applications

Rising demand for extended shelf-life food products across snacks, dairy, and ready-to-eat categories is driving investment in high-barrier flexible packaging films with superior oxygen and moisture transmission rates. Modified atmosphere packaging and vacuum packaging flexible formats are gaining adoption in organised retail and food export applications.

4. E-Commerce Packaging Innovation Driving Flexible Mailer and Pouch Demand

India's rapid e-commerce and quick-commerce growth is creating demand for flexible packaging formats specifically engineered for direct-to-consumer delivery, including tamper-evident mailer pouches, resealable flexible bags, and custom-printed e-commerce outer packaging. Flexible packaging converters are investing in e-commerce specific capabilities.

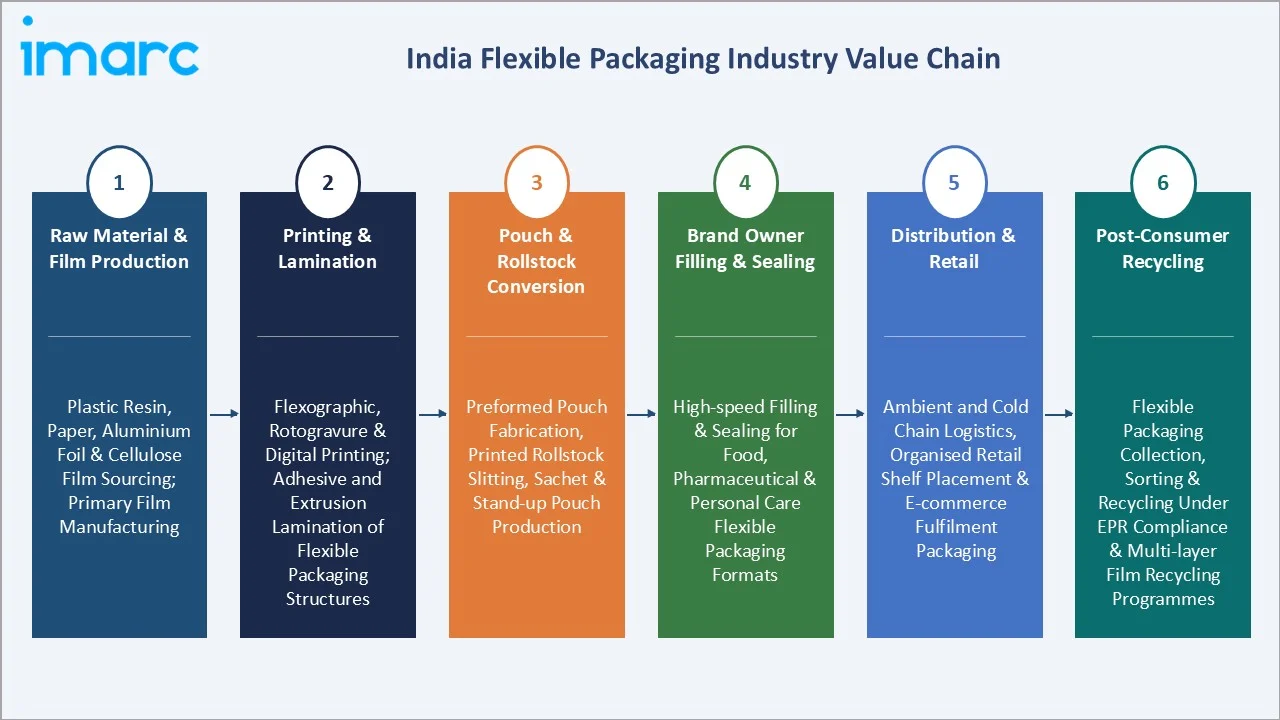

Industry Value Chain Analysis

The India flexible packaging value chain integrates raw material and film production, printing and lamination conversion, pouch and rollstock fabrication, brand owner filling and sealing, distribution and retail, and post-consumer recycling. The value chain is characterised by high integration between film producers and converters in Maharashtra and Gujarat.

|

Stage |

Key Activities |

|

Raw Material & Film Production |

Plastic resin, paper, aluminium foil, and cellulose film sourcing and primary film manufacturing |

|

Printing & Lamination |

Flexographic, rotogravure, and digital printing; adhesive and extrusion lamination of flexible packaging structures |

|

Pouch & Rollstock Conversion |

Preformed pouch fabrication, printed rollstock slitting, sachet, and stand-up pouch production |

|

Brand Owner Filling & Sealing |

High-speed filling and sealing operations for food, pharmaceutical, and personal care flexible packaging formats |

|

Distribution & Retail |

Ambient and cold chain logistics, organised retail shelf placement, and e-commerce fulfilment packaging |

|

Post-Consumer Recycling |

Flexible packaging collection, sorting, and recycling under EPR compliance and multi-layer film recycling programmes |

The raw material and film production tier is the value chain's most capital-intensive stage. The printing and lamination tier is experiencing the most rapid technology transition as digital printing progressively complements rotogravure and flexography for short-run and personalised packaging production.

Technology Landscape in the India Flexible Packaging Industry

Flexographic Printing Technology

Flexographic printing technology dominates India's flexible packaging printing landscape due to high-speed output, cost efficiency, and compatibility with a wide range of flexible substrates. Advances in UV-LED flexo printing are improving print quality and reducing energy consumption, with Indian converters upgrading flexo press capabilities to meet brand owner quality standards for food and pharmaceutical flexible packaging.

Rotogravure Printing Technology

Rotogravure printing offers superior print quality, colour consistency, and high-volume efficiency for premium flexible packaging. Indian converters serving multinational FMCG brands maintain rotogravure capabilities for large volume rollstock and pouch printing, particularly for food, personal care, and pharmaceutical flexible packaging, where colour accuracy and fine detail reproduction are critical.

High-Barrier Coating and Lamination Technology

Advanced barrier coating technologies, including PVDC, EVOH, and AlOx vacuum deposition, are enabling Indian manufacturers to produce high-performance flexible structures with required oxygen, moisture, and aroma barrier properties, improving recyclability and reducing dependence on aluminium foil lamination.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Printed Rollstock |

46.0% |

2025 |

|

Raw Material |

Plastic |

62.0% |

2025 |

|

Printing Technology |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

West and Central India |

33.0% |

2025 |

By Product Type

The printed rollstock segment leads at 46.0% in 2025, encompassing the mainstream FMCG, food, and pharmaceutical packaging market as the most versatile and cost-effective flexible packaging format for high-volume converting and filling operations.

To access detailed market analysis, Request Sample

Preformed bags and pouches at 38.0% reflect strong demand across stand-up pouches, zipper bags, and retort pouches for food, detergent, and personal care applications. Others at 16.0% includes lidding films, sachets, and specialty flexible formats for agricultural, industrial, and healthcare end uses.

By Raw Material

Plastic leads raw material at 62.0% through cost efficiency, superior barrier properties, lightweight nature, and versatility across all flexible packaging formats. Paper at 18.0% is the fastest-growing segment, driven by sustainability mandates and brand owner shifts toward fibre-based flexible packaging formats.

Aluminium foil at 14.0% serves pharmaceutical blister packaging, confectionery wrapping, and premium food packaging requiring absolute moisture and oxygen barrier performance. Cellulose at 6.0% is growing in sustainable packaging applications as regenerated cellulose films offer biodegradability advantages for food and tobacco packaging.

Regional Market Insights

|

Region |

Share (2025) |

Key Flexible Packaging Market Characteristics |

|

West and Central India |

33.0% |

Largest region driven by concentrated FMCG, pharmaceutical, and food processing manufacturing base |

|

North India |

28.0% |

Second-largest region supported by FMCG manufacturing, food processing, and pharmaceutical sector growth |

|

South India |

24.0% |

Growing region driven by food, pharmaceutical, and consumer goods flexible packaging demand |

|

East and Northeast India |

15.0% |

Emerging region with growing food processing investment and expanding FMCG distribution infrastructure |

West and Central India, at 33.0%, leads through its dominant FMCG manufacturing base, pharmaceutical packaging cluster, and concentration of major flexible packaging converters. North India, at 28.0%, reflects a large FMCG hub and growing pharmaceutical flexible packaging demand.

South India, at 24.0%, is driven by food and beverage, pharmaceutical, and packaging demand across its industrial base. East and Northeast India, at 15.0%, is the smallest but fastest-growing region, with expanding food processing investment and tea packaging demand creating new flexible packaging growth opportunities.

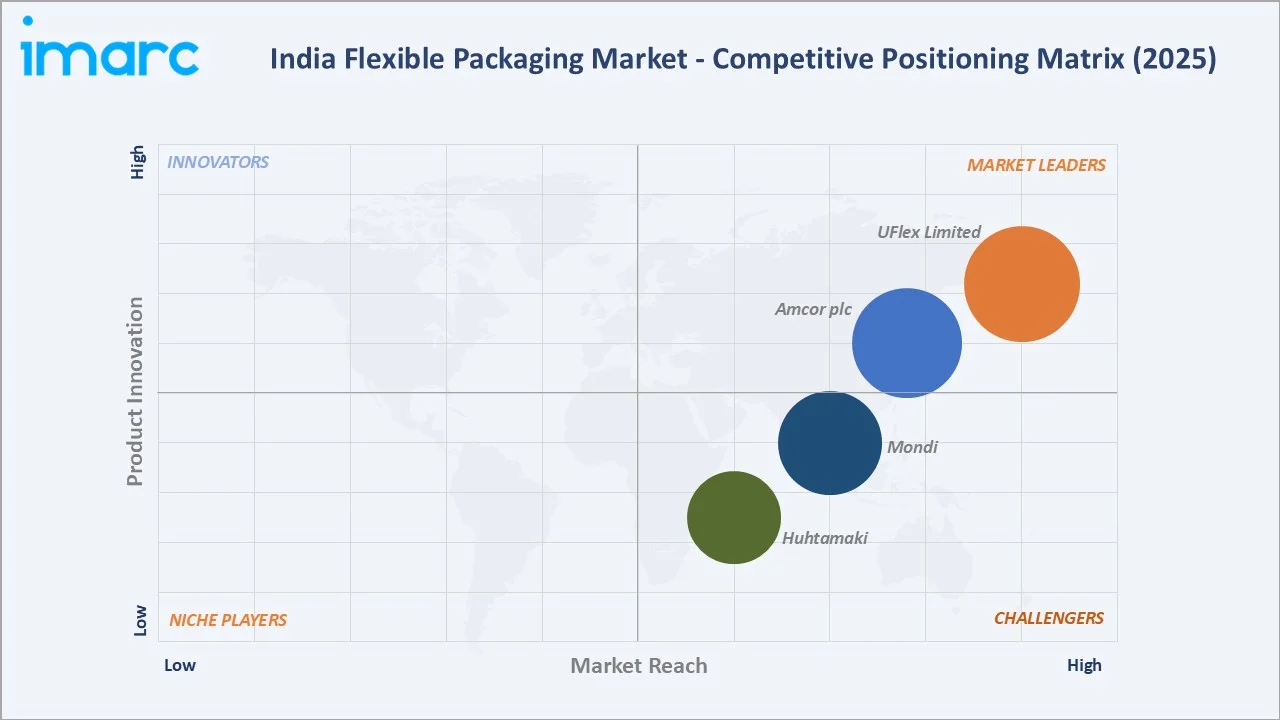

Competitive Landscape

The India flexible packaging market competitive landscape is moderately fragmented, with a mix of large domestic converters, multinational packaging majors, and numerous regional small and mid-size converters. Key competitive differentiators include printing technology capabilities, sustainability credentials, barrier film lamination, geographic reach, and customer service responsiveness to FMCG brand owner requirements.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

UFlex Limited |

Flexible packaging films, laminates, pouches, rollstock |

Market Leader |

India's largest flexible packaging company with integrated film production, printing, and pouch-making capabilities. |

|

Amcor plc |

Flexible packaging laminates, pouches, rollstock for food and pharma |

Market Leader |

Global leader with strong India presence through Phoenix Flexibles acquisition, serving multinational FMCG brands. |

|

Huhtamaki |

Flexible packaging films, laminates, and printed pouches |

Strong Challenger |

Operates in India as Huhtamaki India Limited, leading packaging converter serving major Indian food, beverage, and personal care brand owners. |

|

Mondi |

Kraft paper bags, flexible laminates, and sustainable packaging |

Challenger |

Investing in India operations with a focus on sustainable fibre-based flexible packaging for food and e-commerce. |

Key players include UFlex Limited, Amcor plc, Huhtamaki, Mondi, and others.

Key Company Profiles

UFlex Limited

UFlex Limited is India's largest flexible packaging company, headquartered in Noida, Uttar Pradesh, with an integrated manufacturing model covering polyester and nylon film production, printing, lamination, and pouch fabrication. UFlex operates globally with manufacturing facilities in India, the USA, Mexico, Poland, Egypt, Russia, and the UAE.

- Key Products: Flexible packaging films, laminates, pouches, rollstock

- Strategic Focus: Expanding sustainable and biodegradable flexible packaging portfolio, growing pharmaceutical packaging capabilities, and increasing recycled content in flexible film production to comply with India's EPR mandates.

Amcor plc

Amcor plc is a global leader in responsible packaging headquartered in Zürich, Switzerland, with a strong and growing India presence following its acquisition of Phoenix Flexibles, a Gujarat-based flexible packaging converter serving food, personal care, and home care markets.

- Key Products: Flexible packaging laminates, pouches, rollstock for food, pharma, and others.

- Recent Developments: In April 2025, Amcor completed its all-stock merger with Berry Global, strengthening its position as a global leader in consumer and healthcare packaging solutions. The combined company brings together expanded packaging capabilities, advanced material science expertise, and enhanced innovation resources, creating new growth opportunities.

- Strategic Focus: Expanding India manufacturing capacity, integrating Phoenix Flexibles into its global sustainability frameworks, and targeting Indian FMCG multinational client base with premium flexible packaging solutions.

Market Concentration Analysis

The India flexible packaging market is moderately fragmented, with the top 4-5 players collectively accounting for approximately 35-45% of organised sector revenue. The unorganised and regional converter segment represents a significant share of total market volume, particularly in commodity flexible packaging formats for local food and FMCG brands.

Market concentration is increasing as multinational packaging majors acquire regional converters, FMCG brand owners consolidate their flexible packaging supply base, and sustainability compliance requirements create barriers for smaller converters. The trend toward consolidated supply relationships is expected to continue through 2034 as quality and sustainability standards intensify.

Investment & Growth Opportunities

Highest Growth Segments

Pharmaceutical flexible packaging (~15% CAGR), sustainable mono-material pouches (~18% CAGR from smaller base), e-commerce mailer flexible packaging (~20% CAGR), printed rollstock for organised retail FMCG (~12.1% CAGR), and high-barrier food flexible packaging for extended shelf-life applications (~13% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Pharmaceutical and nutraceutical flexible packaging represents the India flexible packaging market's highest per-unit-value emerging opportunity, with aluminium foil laminate pharmaceutical pouches and high-barrier unit-dose sachets generating significantly higher margins than commodity food-grade flexible packaging, supported by India's expanding pharmaceutical export volumes.

Investment Themes

- Sustainable flexible packaging manufacturing investment to capture EPR-driven brand owner reformulation demand as India's Plastic Waste Management Rules require certified recyclability targets and minimum recycled content percentages through 2027, creating a structurally growing addressable market for certified sustainable flexible packaging converters.

- Pharmaceutical flexible packaging capacity expansion to serve India's growing API and formulation export industry, targeting the high-margin blister packaging foil, unit-dose sachet, and sterile flexible packaging formats for generic drug manufacturers supplying regulated export markets.

Future Market Outlook (2026-2034)

The India flexible packaging market is projected to grow from USD 5.18 Billion in 2025 to USD 14.12 Billion by 2034, delivering an 11.43% CAGR over the forecast period. The market's anchor value of USD 8.90 Billion in 2030 reflects an industry at its most transformative commercial inflection, with sustainable mono-material packaging gaining mainstream adoption and pharmaceutical flexible packaging scaling rapidly.

Three structural forces define India flexible packaging market growth through 2034. India's rising per-capita packaged food consumption creates a compounding demand cycle across FMCG, snack food, dairy, and ready-to-eat categories. The pharmaceutical sector's expanding export volumes create sustained demand for high-barrier flexible packaging. Sustainability-driven material reformulation creates a significant investment opportunity as converters invest in recyclable mono-material technologies.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including packaging converter senior management, FMCG brand packaging managers, pharmaceutical packaging procurement leads, retail category managers, and flexible packaging material suppliers across India's major manufacturing clusters.

Secondary Research

Secondary research encompassed company annual reports, India Plastic Waste Management Rules documentation, food packaging standards, flexible packaging industry association reports, organised retail and e-commerce growth data, and India pharmaceutical export data from PHARMEXCIL. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using end-use bottom-up model incorporating food packaging flexible film consumption by segment, pharmaceutical flexible packaging volume growth aligned to India pharma production data, FMCG and organised retail expansion forecasts, and converter capacity investment projections, adjusted for sustainability-driven material mix transition.

India Flexible Packaging Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Printed Rollstock, Preformed Bags and Pouches, Others |

| Raw Materials Covered | Plastic, Paper, Aluminium Foil, Cellulose |

| Printing Technologies Covered | Flexography, Rotogravure, Digital, Others |

| Applications Covered | Food and Beverages, Pharmaceuticals, Cosmetics, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | UFlex Limited, Amcor plc, Huhtamaki, Mondi, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India flexible packaging market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India flexible packaging market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India flexible packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Flexible Packaging Market Report

The India flexible packaging market reached USD 5.18 Billion in 2025, driven by printed rollstock at 46.0%, plastic raw material at 62.0%, and West and Central India leading at 33.0% regional share through the region's dominant FMCG and pharmaceutical manufacturing base.

The India flexible packaging market grows at 11.43% CAGR during 2026-2034, reaching USD 14.12 Billion by 2034, driven by packaged food demand expansion, pharmaceutical sector growth, e-commerce flexible packaging adoption, and sustainable packaging investment.

Printed rollstock leads at 46.0%, capturing mainstream FMCG, food, and pharmaceutical packaging as the most versatile format for high-volume converting and filling operations. Preformed bags and pouches at 38.0% are the second-largest segment.

Plastic leads at 62.0% through cost efficiency, superior barrier properties, and versatility. Paper at 18.0% is the fastest-growing segment driven by sustainability mandates. Aluminium foil at 14.0% serves pharmaceutical and premium food packaging applications.

West and Central India leads at 33.0% through its concentrated FMCG manufacturing, pharmaceutical cluster, and flexible packaging converter base. North India at 28.0% is the second-largest region.

Leading companies include UFlex Limited, Amcor plc, Huhtamaki, Mondi, and others.

The India flexible packaging market is projected to reach approximately USD 8.90 Billion by 2030, with sustainable mono-material flexible packaging gaining a significant share, pharmaceutical packaging growing rapidly, and e-commerce packaging creating new high-growth flexible format demand.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)