India Food Service Market Size, Share, Trends and Forecast by Sector, Systems, Type of Restaurants, and Region, 2026-2034

India Food Service Market Size, Share, Trends & Forecast (2026-2034)

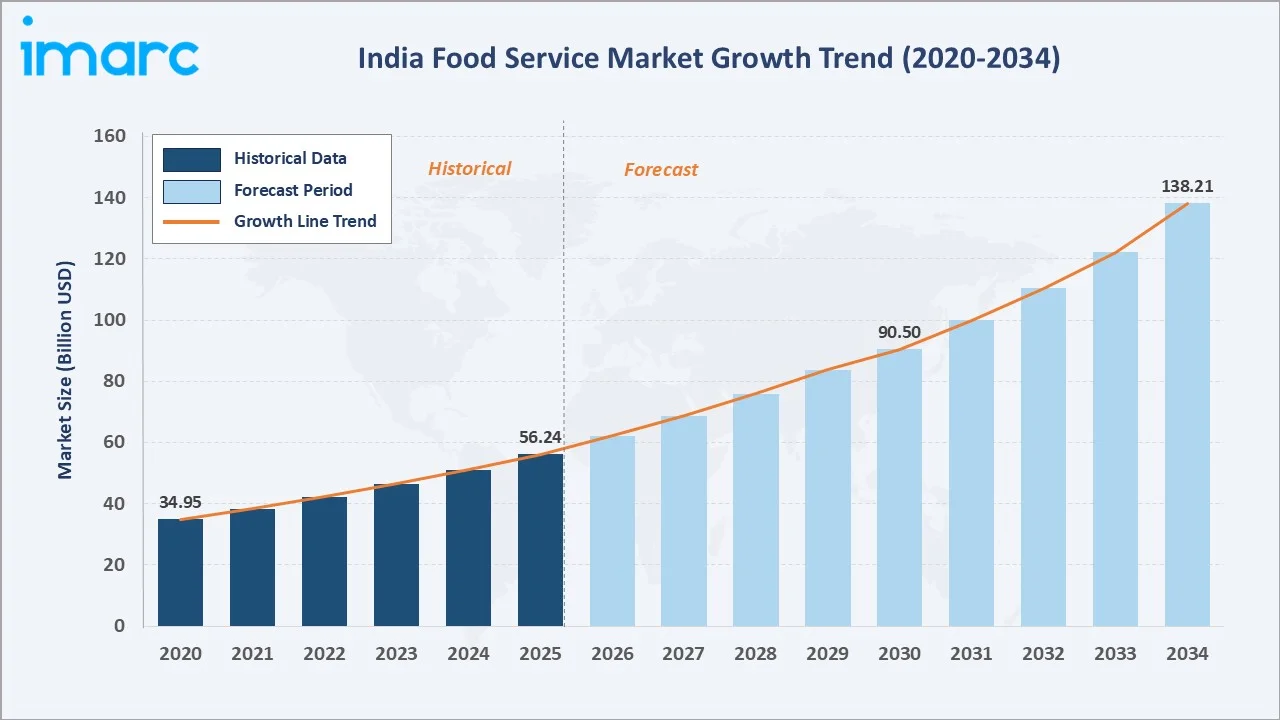

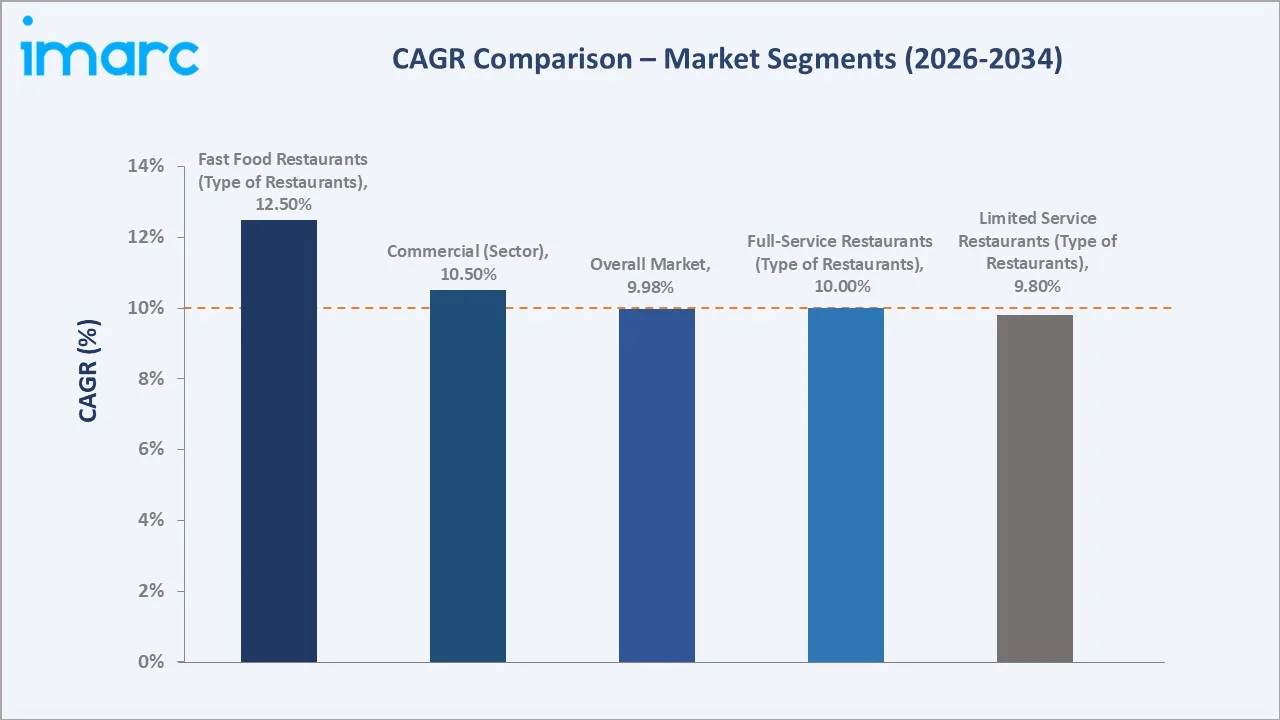

The India food service market reached USD 56.24 Billion in 2025 and is projected to reach USD 138.21 Billion by 2034, growing at a CAGR of 9.98% during 2026-2034. Rapid urbanization and the rise of nuclear families, increasing disposable income and dining-out culture, the explosive growth of online food delivery platforms, the aggressive expansion of quick-service restaurants (QSRs) and fast-casual dining chains into Tier-2 and Tier-3 cities, and the influence of global food trends are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 56.24 Billion |

|

Forecast Market Size (2034) |

USD 138.21 Billion |

|

CAGR (2026-2034) |

9.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

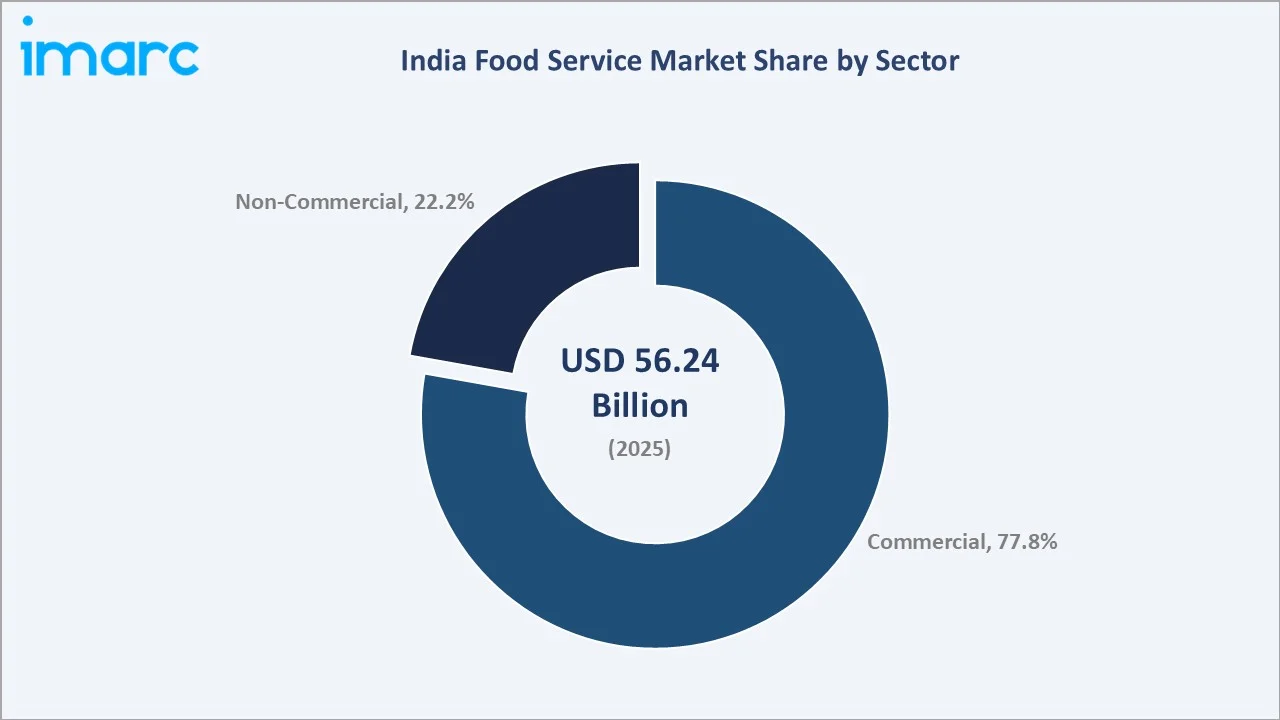

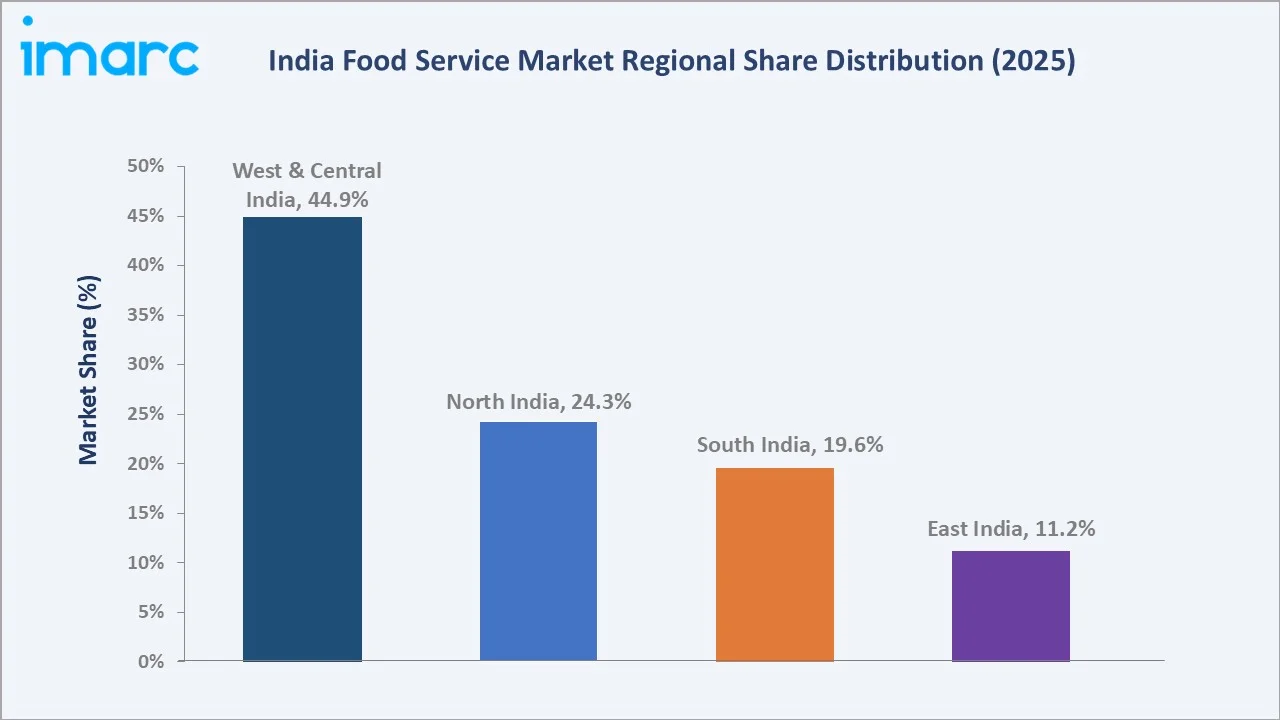

West and Central India leads regionally, holding a 44.9% market share in 2025, anchored by Mumbai’s concentration of premium full-service restaurants and Maharashtra’s established QSR infrastructure, along with Gujarat’s growing food-away-from-home culture. The commercial sector commands the dominant 77.8% share, reflecting the broad base of profit-oriented food service establishments including restaurants, cafes, hotels, and food courts that serve India’s rapidly expanding dining-out consumer base.

To get more information on this market, Request Sample

India’s food service market is underpinned by three structural forces: urbanization driving the shift from home-cooked meals to out-of-home dining, the technology-enabled food delivery ecosystem creating a digital-first food service channel accessible to 900+ million smartphone users, and the QSR chains’ systematic penetration of India’s 700+ Tier-2 and Tier-3 cities with standardized menus and franchise models.

Executive Summary

The India food service market is experiencing robust, broad-based expansion driven by the convergence of urbanization, rising aspirational consumption, and the technology-led democratization of food discovery and delivery. The market was valued at USD 56.24 Billion in 2025 and is forecast to reach USD 138.21 Billion by 2034, growing at a CAGR of 9.98%. This trajectory is anchored by 600 million Indians expected to reside in urban areas by 2031, directly expanding the core food service consumer base.

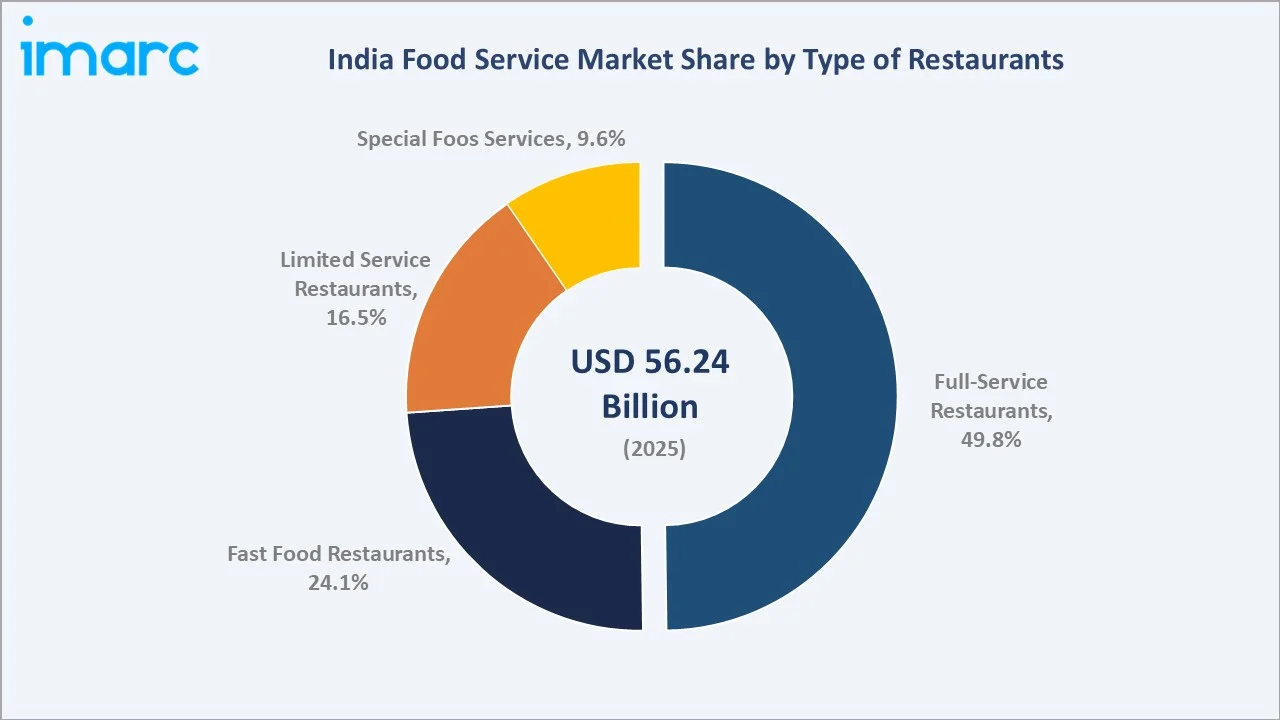

The commercial sector dominates with a 77.8% share, while full-service restaurants account for 49.8% of the restaurant type mix. West and Central India lead regionally at 44.9%. Key players including Jubilant Bhartia Group, Devyani International Limited, Westlife Foodworld, and Barbeque Nation Hospitality Ltd. shape the competitive landscape.

Key Market Insights

|

Insight |

Data |

|

Largest Sector |

Commercial – 77.8% share (2025) |

|

Fastest Growing Sector |

Commercial – ~10.5% CAGR (2026-2034) |

|

Largest Restaurant Type |

Full-Service Restaurants – 49.8% share (2025) |

|

Fastest Growing Restaurant Type |

Fast Food Restaurants – ~12.5% CAGR (2026-2034) |

|

Leading Region |

West and Central India – 44.9% share (2025) |

|

Top Companies |

Jubilant Bhartia Group, Devyani International Limited, Westlife Foodworld, Barbeque Nation Hospitality Ltd. |

Key Analytical Observations Supporting the Above Data:

- Commercial sector’s 77.8% share (2025) reflects the dominance of profit-oriented food service establishments across India’s urban landscape, encompassing standalone restaurants, QSR chains, hotel F&B, food courts in malls, and airport dining.

- Full-service restaurants’ 49.8% share (2025) reflects India’s strong cultural preference for leisurely dining experiences that combine food with social occasions, from neighborhood dhabas and mid-casual Indian restaurants to premium fine-dining establishments in metros.

- Fast food restaurants’ fastest-growth trajectory (~12.5% CAGR) is driven by QSR chains’ aggressive expansion, with Domino’s India added around 200 new stores during the first nine months of the FY 2025, including 75 stores in the third quarter alone, and the growing adoption of self-order kiosks, mobile apps, and delivery aggregator partnerships by McDonald’s, KFC, Burger King, and Subway.

- West and Central India’s 44.9% share (2025) reflects the region’s dominance as India’s largest food service market by revenue. Mumbai alone accounts for a disproportionate share of India’s premium restaurant revenue; Maharashtra and Gujarat’s dense urban clusters create the highest concentration of organized food service outlet density per capita in the country.

India Food Service Market Overview

Food service encompasses businesses concerned with preparing, serving, and delivering food items to consumers in settings outside their homes. The sector spans a broad continuum from street food and dhabas to five-star hotel restaurants, covering full-service sit-down establishments, quick-service and fast-casual restaurants, food courts, cloud kitchens, and institutional catering for healthcare, education, and corporate facilities.

Macroeconomic drivers include India’s per capita GDP expected to reach around US$3,000 in 2025-26, the rapid growth of India’s working woman population (World Bank Gender Data Portal stated Indian females labor force participation rate in 2025 stood at 32.4%) driving demand for convenient out-of-home meals, and the National Restaurant Association of India (NRAI) estimating the sector employs over 7.3 million workers directly, making food service India’s third-largest employer.

Market Dynamics

To evaluate market opportunities, Request Sample

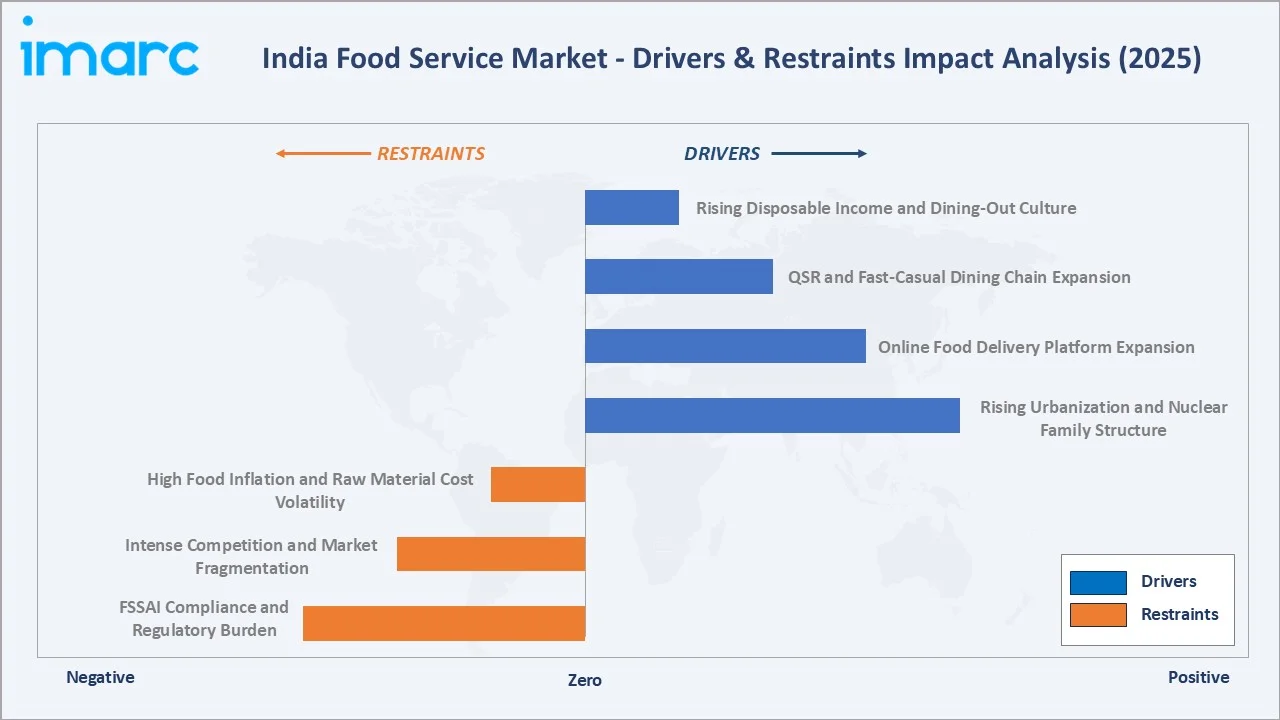

Market Drivers

- Rising Urbanization and Nuclear Family Structure: India’s urban population is projected to reach 600 million by 2031, creating an expanding base of consumers with hectic professional lifestyles, smaller households without dedicated cooks, and higher per-capita discretionary spending on food experiences.

- Online Food Delivery Platform Expansion: Zomato’s food delivery app recorded around 30.7 million users, while Swiggy’s all-in-one super app reported 24.7 million weekly active users. Cloud kitchens, delivery-only food production facilities with zero dine-in investment, have proliferated to 20,000 active cloud kitchens in Delhi alone, enabling brands to serve new geographies at lower capital costs than traditional restaurants.

- QSR and Fast-Casual Dining Chain Expansion: India’s organized QSR chains are systematically penetrating Tier-2 cities where real estate costs are 40–50% lower than metro equivalents and same-store sales growth outperforms metro performance. Westlife Foodworld plans to open around 45-50 McDonald’s outlets each year.

- Rising Disposable Income and Dining-Out Culture: India’s household disposable income growth, with the middle class rising at 6.3 percent per year, is driving increased food-away-from-home spending. Moreover, according to the YouGov Profiles survey, nearly three in four Gen Z consumers in India, or 73%, said they like trying new cuisines, highlighting a strong appetite for culinary discovery.

Market Restraints

- High Food Inflation and Raw Material Cost Volatility: Food inflation, measured by the Consumer Food Price Index (CFPI), remained under pressure during April-December FY25, mainly due to select food items such as vegetables and pulses. Together, vegetables and pulses carry a total weight of 8.42% in the CPI.

- Intense Competition and Market Fragmentation: Although the organized share of India’s food services industry is expanding, it currently accounts for only one-third, or 33%, of the total market. The dominance of the unorganized segment creates significant growth opportunities for branded and chain outlets to increase their penetration across India.

- FSSAI Compliance and Regulatory Burden: The Food Safety and Standards Authority of India (FSSAI) licensing requirements, mandatory food safety management systems (FSMS), hygiene rating compliance, and calorie labelling mandates for chain restaurants create significant operational compliance costs.

Market Opportunities

- Cloud Kitchen and Delivery-First Restaurant Models: Cloud kitchens enable food service brands to expand geographic reach with 60-70% less space than traditional restaurants. The cloud kitchen market in India is growing at 15–18% CAGR, driven by Rebel Foods, EatClub Brands, and FreshMenu.

- Premiumization of Indian Casual Dining: India’s premium casual and fine-dining segment is growing at 12–15% CAGR, driven by aspirational urban consumers seeking experiential dining with artisanal menus, craft beverages, and Instagram-worthy ambiance.

- Corporate and Institutional Catering Expansion: India’s corporate cafeteria and institutional catering segment is growing rapidly as organized office parks, IT campuses, hospitals, and educational institutions outsource food service management to professional catering companies.

Market Challenges

- High Real Estate Costs in Premium Urban Locations: A recent survey of high street retail locations in India showed that Delhi’s Khan Market commands the highest rentals, ranging from INR 1,000 to INR 1,500 per sq. ft. per month. Gurugram’s DLF Galleria followed, with monthly rents ranging from INR 800 to INR 1,200 per sq. ft.

- Skilled Labor Shortage and High Attrition: India’s food service sector faces a chronic shortage of trained chefs, kitchen managers, and service staff, with annual attrition rates of 30–40% in many QSR and casual dining chains. The high training cost per employee combined with rapid turnover creates a persistent operational challenge that directly impacts service quality consistency and customer satisfaction scores.

Emerging Market Trends

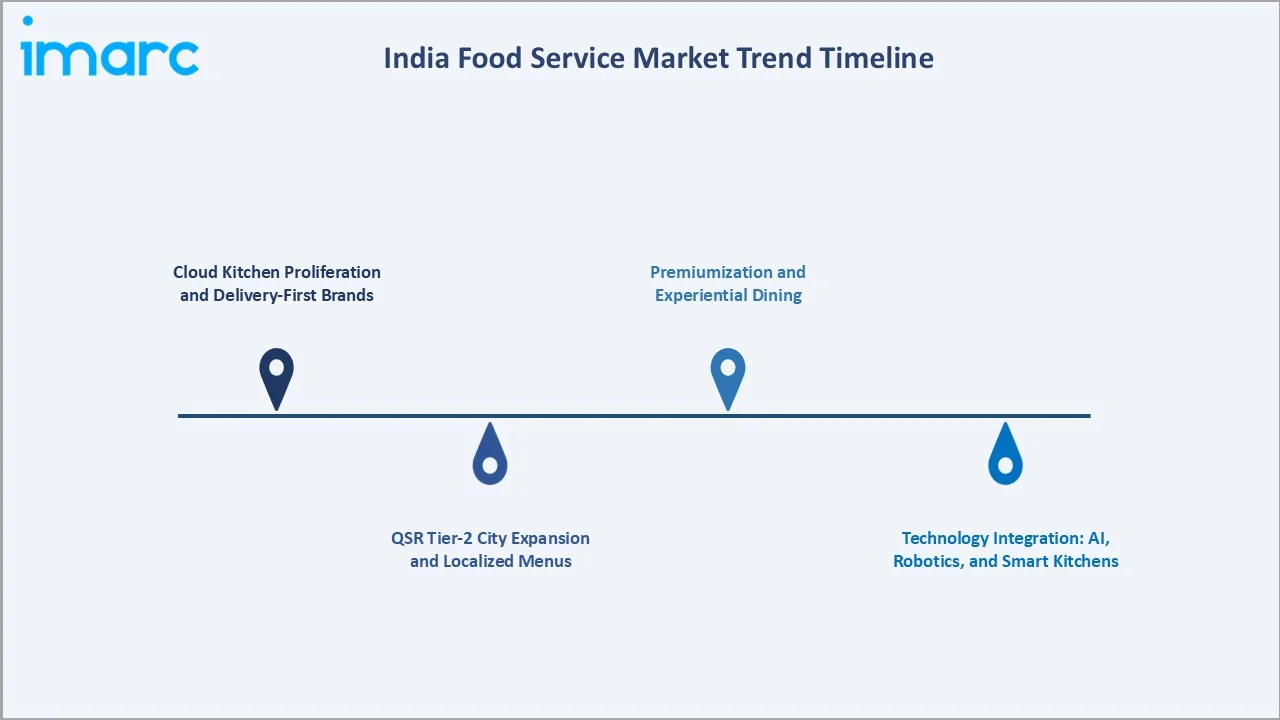

1. Cloud Kitchen Proliferation and Delivery-First Brands

Cloud kitchens have transformed India’s food service landscape by enabling brand proliferation at minimal capital cost. Rebel Foods, operating 450 cloud kitchen hubs across India in 2025, produces food for 12 brands (Faasos, Behrouz Biryani, Mandarin Oak, Sweet Truth) from single facilities. The model’s scalability and elimination of dine-in real estate costs position cloud kitchens as the structurally fastest-growing food service format through 2034.

2. QSR Tier-2 City Expansion and Localized Menus

The systematic penetration of India’s Tier-2 cities (Lucknow, Jaipur, Indore, Coimbatore, Visakhapatnam) by QSR chains represents the market’s most significant volume growth opportunity. Westlife Foodworld’s Masala Grill Veg for Gujarat and Chicken Chettinad for Tamil Nadu, achieving higher trial rates than standard menu items, exemplifies the localized menu adaptation strategy enabling QSR chains to achieve acceptance in culturally diverse regional markets.

3. Technology Integration: AI, Robotics, and Smart Kitchens

In March 2025, Jubilant FoodWorks launched Elate, India’s first Android-based POS and order-taking system for the foodservice industry, integrating its D2C apps with in-store operations to improve ordering and customer experience. Robotic kitchen assistants for repetitive tasks (dough tossing, frying) and automated beverage dispensers are being piloted at scale by QSR chains to address labor shortages and reduce per-unit food preparation costs.

4. Premiumization and Experiential Dining

India’s affluent consumer segment is driving growth in experiential dining, chef’s tables, omakase experiences, regional cuisine revival, and themed dining concepts that command per-head spending of INR 2,000–8,000. In August 2025, Bayroute opened a new Middle-Eastern food service outlet in Ghatkopar, Mumbai, and Pizza Express opened at Oberoi Sky City Mall, reflecting the sustained appetite for premium international cuisine concepts in India’s top metro markets.

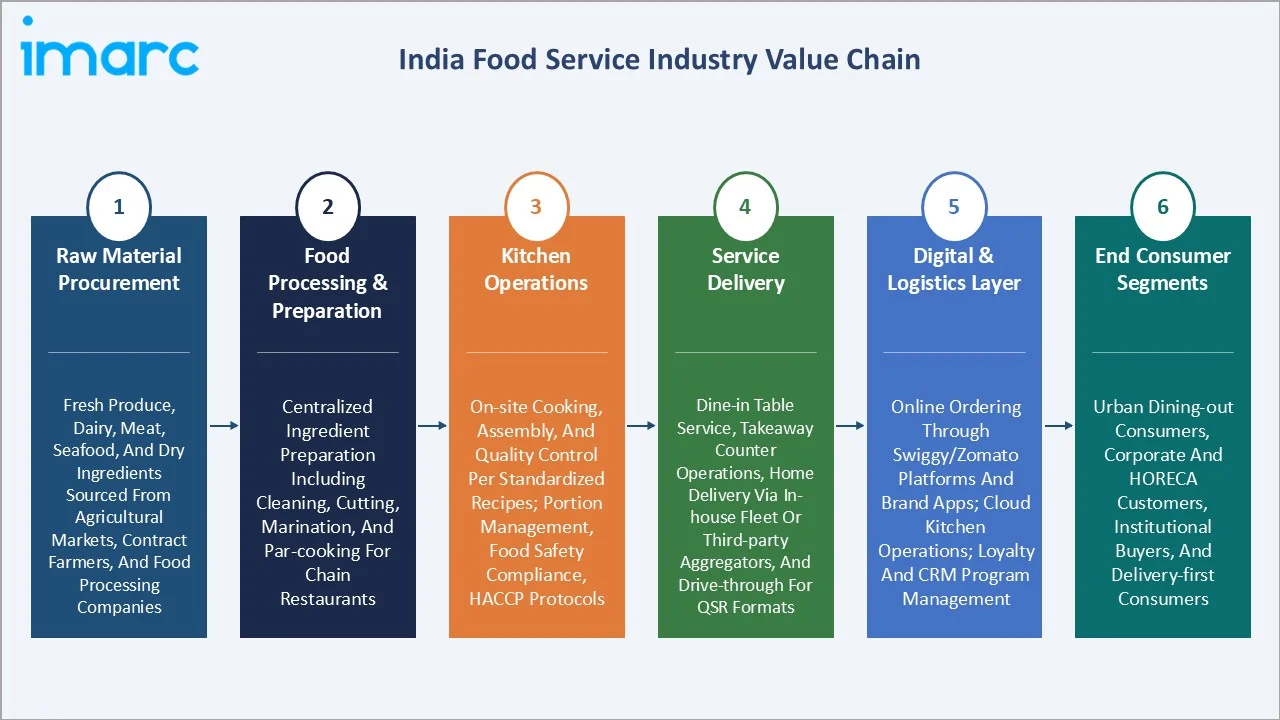

Industry Value Chain Analysis

The India food service value chain spans raw agricultural produce procurement through end-consumer meal delivery, with each stage subject to specific food safety, temperature control, and quality management requirements.

|

Stage |

Description |

|

Raw Material Procurement |

Fresh produce, dairy, meat, seafood, and dry ingredients sourced from agricultural markets, contract farmers, and food processing companies |

|

Food Processing & Preparation |

Centralized ingredient preparation including cleaning, cutting, marination, and par-cooking for chain restaurants |

|

Kitchen Operations |

On-site cooking, assembly, and quality control per standardized recipes; portion management, food safety compliance, HACCP (Hazard Analysis Critical Control Point) protocols |

|

Service Delivery |

Dine-in table service, takeaway counter operations, home delivery via in-house fleet or third-party aggregators, and drive-through for QSR formats |

|

Digital & Logistics Layer |

Online ordering through Swiggy/Zomato platforms and brand apps; cloud kitchen operations; loyalty and CRM program management |

|

End Consumer Segments |

Urban dining-out consumers, corporate and HORECA (Hotel/Restaurant/Cafe) customers, institutional buyers, and delivery-first consumers |

Technology Landscape in the India Food Service Industry

Online Food Delivery Platform Technology

Swiggy and Zomato operate sophisticated logistics technology platforms managing real-time order allocation, dynamic delivery partner routing, predictive demand forecasting, and restaurant capacity management across 700+ cities. Zomato’s Hyperpure B2B ingredient supply platform serves 1 Lakh+ restaurants with fresh, certified ingredients at 10–15% cost savings versus traditional wholesale markets.

Self-Order Kiosks and Kitchen Automation

QSR chains are deploying self-order kiosks to reduce labor costs and increase average order values. Westlife Foodworld (McDonald’s) implemented self-order kiosks across its estate, reporting a 15% reduction in labor costs and a 12% increase in average order value through upselling prompts. Kitchen automation, including robotic fry stations, automated beverage dispensers, and conveyor pizza ovens, is being adopted to address India’s food service labor shortage and improve output consistency.

Restaurant Management Systems and POS Technology

Integrated cloud-based restaurant management systems (RMS) from providers including Posist, Pine Labs, and Petpooja enable multi-outlet food service operators to manage centralized menu updates, real-time inventory tracking, staff scheduling, and financial reporting across hundreds of locations from a single platform.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Sector |

Commercial |

77.8% |

2025 |

|

Type of Restaurants |

Full-Service Restaurants |

49.8% |

2025 |

|

Systems |

🔒 |

🔒 |

2025 |

|

Region |

West and Central India |

44.9% |

2025 |

By Sector

The commercial sector dominates the India food service market with a 77.8% share in 2025, encompassing all profit-oriented food service establishments including standalone restaurants, QSR chains, hotel and resort F&B, airport dining, food courts in shopping malls, cinema food service, and commercial catering companies.

To access detailed market analysis, Request Sample

The non-commercial sector at 22.2% encompasses institutional food service operations, hospital and healthcare facility cafeterias, educational institution canteens, corporate campus cafeterias, military mess operations, and correctional facility catering.

By Type of Restaurants

Full-service restaurants hold the largest share at 49.8% in 2025, reflecting the dominance of the dine-in experience in India’s food service ecosystem. This category spans the full continuum from unbranded neighborhood restaurants to premium casual chains to fine-dining establishments in five-star hotels.

Fast food restaurants at 24.1% represent India’s fastest-growing restaurant type segment, driven by QSR chain expansion and the growing preference for quick, affordable, standardized meals across urban and emerging Tier-2 markets. Limited service restaurants at 16.5% include cafes, juice bars, quick-casual concepts, and self-service establishments.

Regional Market Insights

West and Central India’s market leadership (44.9%, 2025) is anchored by Mumbai’s position as India’s financial capital and premier restaurant market, Maharashtra’s dense concentration of organized food service outlet infrastructure, and Gujarat’s rapidly growing food-away-from-home culture driven by rising incomes and urbanization in Ahmedabad, Surat, and Vadodara.

South India at 19.6% is experiencing above-market food service growth driven by Bengaluru and Hyderabad’s large young professional population with high dining-out frequency. Furthermore, the rapid expansion of QSR chains into Tamil Nadu’s mid-sized cities and the growing premiumization of South Indian cuisine through regional fine-dining concepts drive the regional market.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West & Central India |

44.9% |

Dominant premium restaurant market, QSR and casual dining infrastructure, growing food-away-from-home culture, and emerging organized restaurant sector |

|

North India |

24.3% |

Diverse and sophisticated restaurant market spanning street food to fine dining, hospitality-led food service, and strong food culture driving per-capita restaurant spend |

|

South India |

19.6% |

Large IT professional consumer base driving premium casual dining, strong vegetarian restaurant culture, and growing tourism-linked food service sector. |

|

East India |

11.2% |

Established restaurant culture with Bengali cuisine specialty dining, growing QSR penetration, and Northeast India’s emerging tourism-linked food service market |

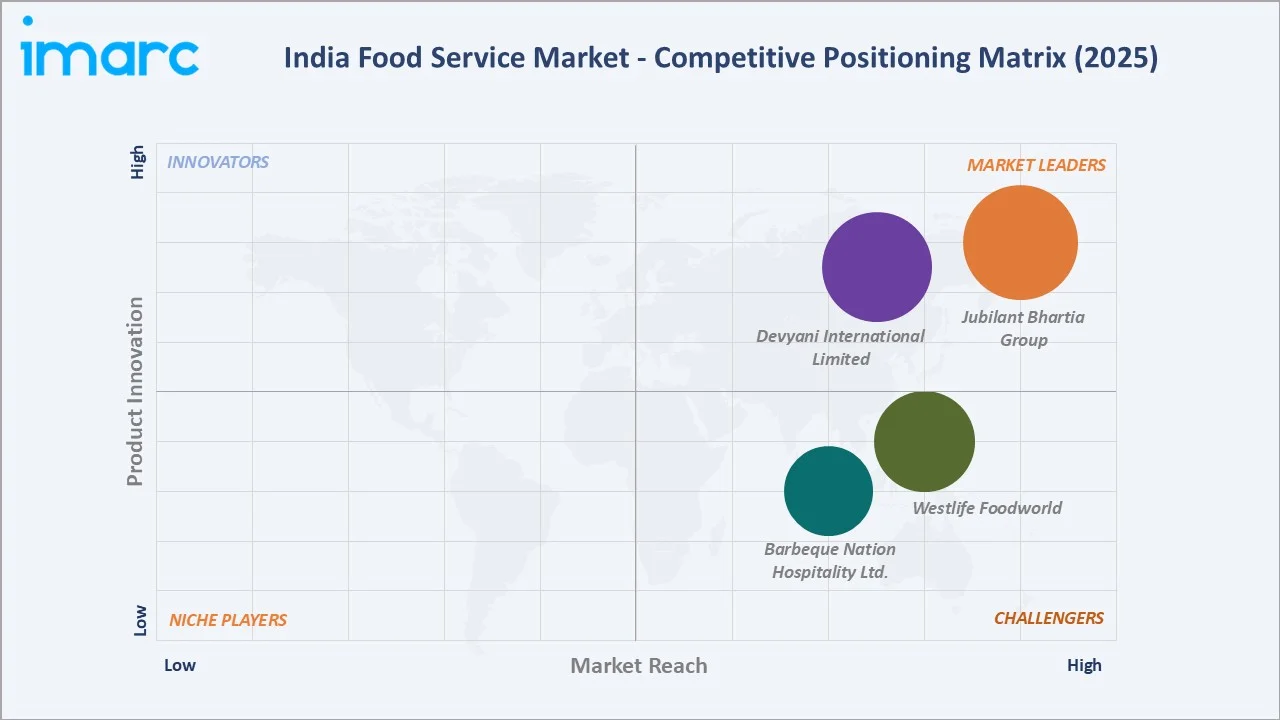

Competitive Landscape

India’s food service market exhibits high fragmentation at the national level, with unorganized eateries accounting for 65–70% of revenue. However, within the organized segment, a small cohort of publicly listed franchise operators dominate QSR, fast-casual, and casual dining: Jubilant Bhartia Group, Devyani International Limited, and Westlife Foodworld.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Jubilant Bhartia Group |

Domino’s, Hong’s Kitchen, Popeyes |

Market Leader |

India’s largest listed food service company; dominant pizza delivery market leader; AI-driven supply chain and digital ordering excellence |

|

Devyani International Limited |

KFC, Pizza Hut, Costa, Vaango |

Market Leader |

Largest franchisee of Yum! Brands in India; diversified QSR and cafe portfolio; strong Tier-2 city penetration strategy |

|

Westlife Foodworld |

McDonald’s (Brand Extensions including McCafe, McBreakfast, McDelivery, and Dessert Kiosk) |

Strong Challenger |

Exclusive McDonald’s franchisee for West and South India; self-order kiosk technology leadership; McCafé premiumization and delivery channel expansion |

|

Barbeque Nation Hospitality Ltd. |

Barbeque Nation |

Strong Challenger |

India’s leading casual dining chain; live-grill buffet format differentiation; successful premiumization through prix-fixe dining experiences |

Quick-service restaurants, casual dining chains, cafés, and delivery-led formats are gaining traction due to rising urbanization, higher disposable income, changing lifestyles, and growing demand for convenience. Competition is also intensifying as companies invest in technology-led operations, loyalty programs, app-based ordering, kitchen automation, and hyperlocal delivery models to improve customer experience and operational efficiency.

Key Company Profiles

Jubilant Bhartia Group

Jubilant Bhartia Group, headquartered in Noida, Uttar Pradesh, is India’s largest listed food service company. The company operates multiple outlets across its brand portfolio and has established a benchmark for QSR operational efficiency, digital ordering integration, and technology-enabled supply chain management in the Indian food service industry.

- Product Portfolio: Domino’s Pizza (pizza, sides, beverages across dine-in, takeaway, and delivery), Hong’s Kitchen (Chinese casual dining) and Popeyes.

- Recent Developments: Jubilant FoodWorks reported a 6.2% rise in domestic revenue to INR 1,686 crore in Q4 FY26, while consolidated quarterly revenue grew 19.1% year-on-year to INR 2,505.8 crore.

- Strategic Focus: Tier-2 and Tier-3 city expansion with smaller-format, delivery-optimized restaurant configurations; technology investment in AI-driven supply chain and customer experience personalization.

Devyani International Limited

Devyani International Limited, headquartered in Gurugram, is one of India’s largest food service companies. The company also operates Costa Coffee outlets and the proprietary Vaango South Indian casual dining brand.

- Product Portfolio: KFC (fried chicken QSR), Pizza Hut (pizza casual dining and delivery), Costa (premium cafe chain), and Vaango (South Indian vegetarian casual dining).

- Recent Developments: In April 2025, Devyani International acquired a controlling stake in Sky Gate Hospitality, the parent company of Biryani By Kilo, Goila Butter Chicken, and The Bhojan. The deal strengthens DIL’s House of Brands strategy and expands its presence in India’s organized biryani and delivery-led foodservice market.

- Strategic Focus: Multi-brand portfolio diversification across QSR, casual dining, and cafe to reduce cyclical risk; Costa premiumization leveraging the growing Indian premium coffee market; Vaango scaling to capture the large South Indian vegetarian dining segment.

Westlife Foodworld

Westlife Foodworld, headquartered in Mumbai, is the exclusive franchisee of McDonald’s restaurants in West and South India. The company is a technology pioneer in the Indian QSR sector, having invested in self-order kiosks, kitchen automation, mobile app ordering, and loyalty program integration across its restaurant estate.

- Product Portfolio: McDonald’s (burgers, wraps, McAloo Tikki, McSpicy, Happy Meals across dine-in, drive-through, takeaway, and delivery), and brand extensions including McCafe, McBreakfast, McDelivery, and Dessert Kiosk)

- Recent Developments: Westlife Foodworld reported 8.7% Q4 of FY 26 growth, supported by steady demand, digital sales, and improved dine-in performance. The company added 21 new restaurants during the quarter, expanding its total network to 478 outlets across 70+ cities.

- Strategic Focus: Technology-driven operational efficiency through self-order kiosks and AI kitchen management; drive-through format expansion at highway and suburban locations; mobile loyalty program building a data-driven customer engagement ecosystem.

Market Concentration Analysis

India’s food service market remains highly fragmented at the national level. The top five organized operators (Jubilant Bhartia Group, Devyani International Limited, Westlife Foodworld, Barbeque Nation Hospitality Ltd.) collectively account for approximately 8–10% of total industry revenue, underlining the vast opportunity for organized chain penetration into a market still dominated by independent operators, dhabas, and street food vendors.

Consolidation is occurring progressively within the organized segment through both organic expansion and strategic acquisitions. FMCG-backed dark kitchen brands and private equity-funded cloud kitchen operators are creating a new tier of consolidated virtual restaurant operators between the independent unorganized segment and the large publicly listed QSR chains.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud kitchens (~18–22% CAGR), QSR Tier-2 city expansion (~12.5% CAGR within fast food), corporate and institutional catering (~11–13% CAGR), and premium casual dining (~12–15% CAGR) represent the highest-growth investment vectors through 2034. Together, these sub-categories address a combined incremental addressable market of approximately USD 40–50 Billion within the India food service ecosystem by 2034.

Emerging Market Expansion

India’s 700+ Tier-2 cities, each with populations between 500,000 and 3 million, represent the primary frontier for QSR and casual dining expansion. Cities including Lucknow, Jaipur, Indore, Coimbatore, Visakhapatnam, Bhubaneswar, and Rajkot are experiencing 15–20% annual food service revenue growth driven by rising incomes, QSR chain entry, and mall-based food court development that aggregates organized food service in high-footfall suburban retail environments.

Venture and Institutional Investment Trends

- Swiggy’s INR 11,327 Crore IPO in November 2024 and Zomato’s continued market leadership with a USD 25+ Billion market capitalization validate the investment thesis for digital food delivery infrastructure, attracting sustained FII and DII capital into the food service technology ecosystem.

- Private equity interest in multi-outlet casual dining and QSR chains continues to be strong, with Advent International’s investment in Barbeque Nation, Samara Capital’s investment in Rebel Foods, and several Series B–D rounds for regional cloud kitchen brands reflecting deep institutional conviction in India’s food service growth story.

Future Market Outlook (2026-2034)

India’s food service market is positioned for near double-digit sustained growth through 2034. From a base of USD 56.24 Billion in 2025, the market is projected to reach USD 138.21 Billion by 2034, representing incremental value creation of USD 81.97 Billion at a CAGR of 9.98%. This growth is structurally driven by India’s irreversible urbanization trajectory, the formalization of food service from unorganized to organized operators, and the technology-enabled expansion of food service accessibility to India’s 600+ million urban and semi-urban consumers.

The food service landscape by 2034 will be characterized by greater technology integration (AI menu personalization, robotics, dark kitchens), higher organizer penetration, and the maturation of India’s first generation of domestically born food service brands (Barbeque Nation, Wow! Momo, Rebel Foods, Haldiram’s) to national and potentially international scale alongside the continued expansion of global QSR franchises.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 140 industry participants in 2024–2025, including QSR chain operators, full-service restaurant groups, food delivery platform executives, institutional catering managers, food tech investors, and FSSAI regulatory advisors across India’s major food service markets.

Secondary Research

Secondary research encompassed company annual reports (Jubilant FoodWorks, Devyani International, Westlife Foodworld, Barbeque Nation, Zomato, Swiggy), NRAI India Food Services Report, Ministry of Tourism hospitality data, FSSAI licensing databases, and trade publications including Restaurant India, Food Service India, and Hotel & Food Service Magazine.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating urban population growth projections, per-capita dining-out expenditure trends, outlet count growth by restaurant category, and average transaction value inflation. A base-case CAGR of 9.98% reflects consensus estimates validated against sector revenue indicators and consumer spending data from FY 2020 to FY 2025.

India Food Service Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Commercial, Non-Commercial |

| Systems Covered | Conventional Foodservice System, Centralized foodservice System, Ready Prepared Foodservice System, Assembly-Serve Foodservice System |

| Type of Restaurants Covered |

Fast Food Restaurants, Full-Service Restaurants, Limited Service Restaurants, Special Food Services Restaurants |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Jubilant Bhartia Group, Devyani International Limited, Westlife Foodworld, Barbeque Nation Hospitality Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India food service market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India food service market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India food service industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Food Service Market Report

The India food service market reached USD 56.24 Billion in 2025 and is projected to reach USD 138.21 Billion by 2034.

The market is expected to grow at a CAGR of 9.98% during 2026-2034, driven by urbanization, rising incomes, QSR chain expansion, online food delivery growth, and the increasing formalization of India’s food service sector.

West and Central India leads with a 44.9% share in 2025, anchored by Mumbai’s premium restaurant market, Maharashtra’s dense QSR infrastructure, and Gujarat’s growing food-away-from-home consumer base.

The commercial sector holds the largest share at 77.8% in 2025, encompassing profit-oriented establishments including standalone restaurants, QSR chains, hotel F&B, airport dining, food courts, and commercial catering companies.

Full-service restaurants hold the largest share at 49.8%, reflecting India’s strong cultural preference for sit-down dining experiences spanning neighborhood restaurants to premium fine-dining establishments.

Key players include Jubilant Bhartia Group, Devyani International Limited, Westlife Foodworld, and Barbeque Nation Hospitality Ltd.

Fast food restaurants are growing at approximately 12.5% CAGR because QSR chains are systematically penetrating India’s 700+ Tier-2 cities with affordable, standardized menus, technology-enabled operations, and localized product adaptations that achieve strong consumer acceptance in new geographies.

Key challenges include high food inflation compressing operator margins, intense competition from the large unorganized sector, premium real estate costs in urban locations, and the structural challenges of cold-chain logistics that underpin food safety and quality standards.

Online food delivery via Swiggy and Zomato represents the fastest-growing food service channel at 18–22% CAGR, serving 100+ million active users across 700+ cities.

Technology is transforming the sector through AI-powered demand forecasting (reducing food waste by up to 18%), self-order kiosks, dynamic pricing algorithms, cloud kitchen management platforms, and personalized loyalty programs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)