India Footwear Market Size, Share, Trends and Forecast by Product, Material, Distribution Channel, Pricing, End User, and Region, 2026-2034

India Footwear Market Size, Share, Trends & Forecast (2026-2034)

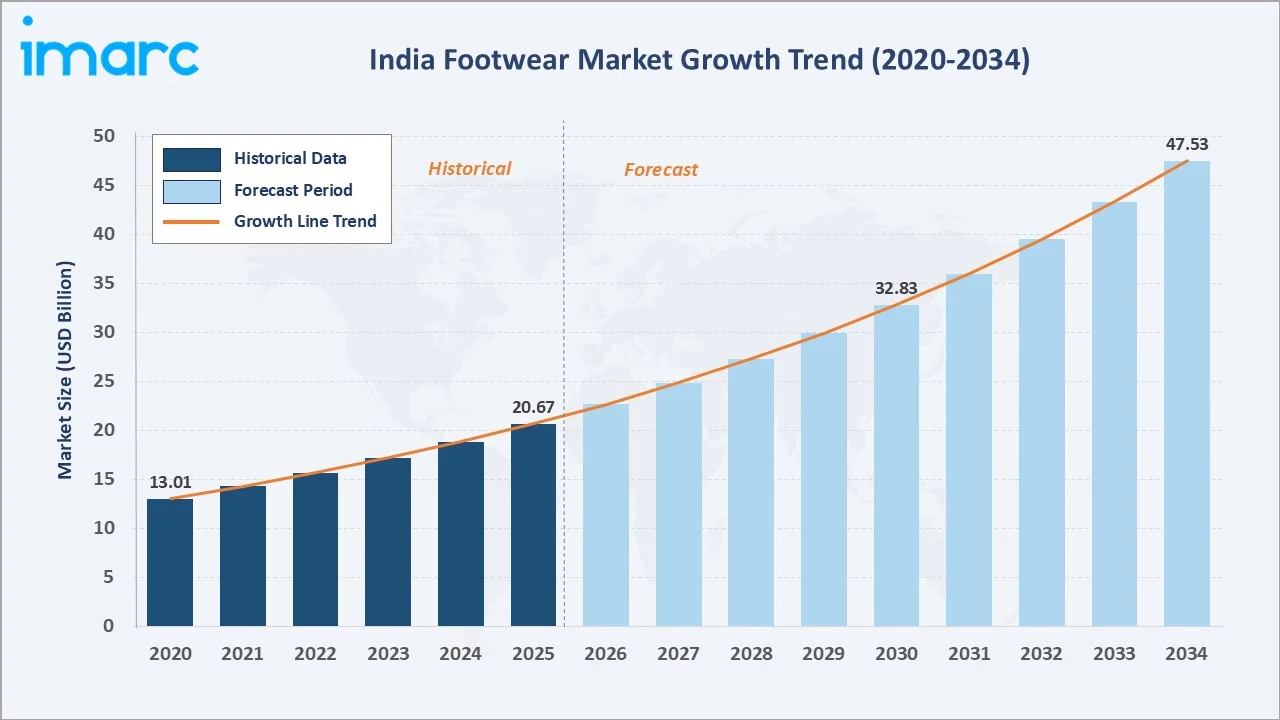

The India footwear market size increased from USD 20.67 Billion in 2025 to USD 22.67 Billion in 2026, and is projected to reach USD 47.53 Billion by 2034, exhibiting a CAGR of 9.7% during 2026-2034. Rapid urbanization, rising disposable incomes, and evolving consumer preferences toward fashionable and functional footwear are the primary forces driving market growth.

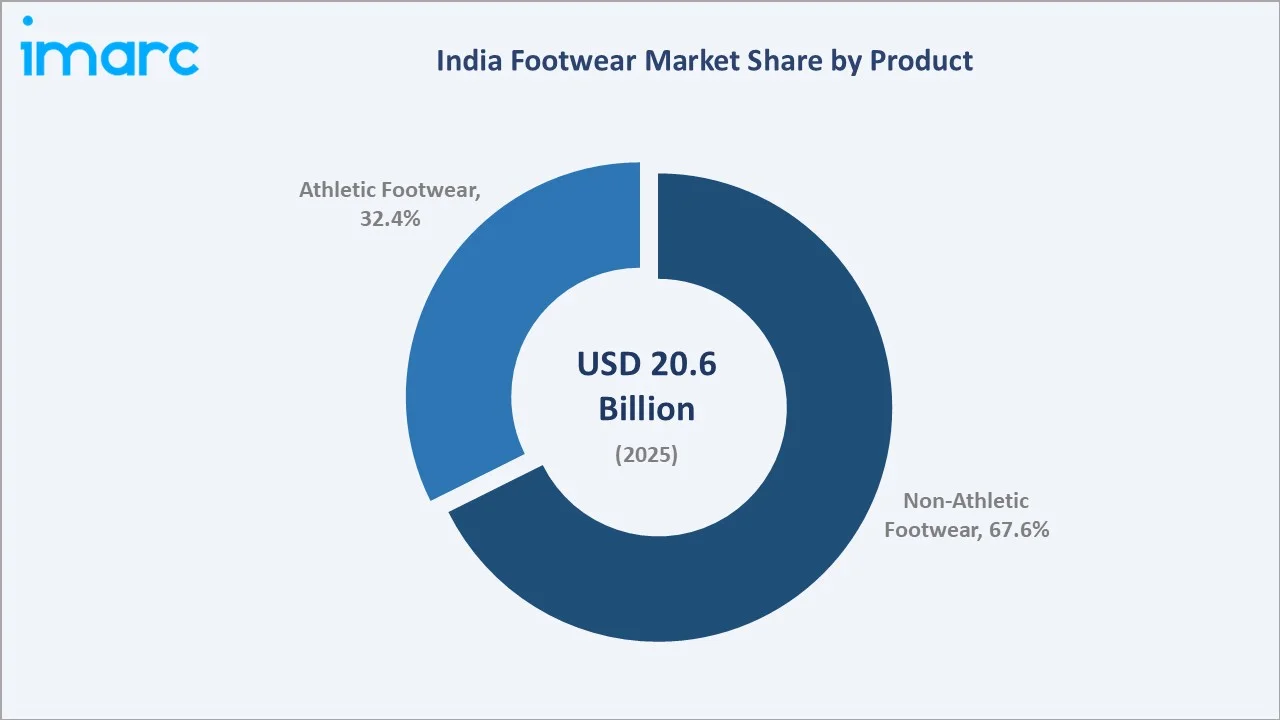

Non-athletic footwear dominates at 67.64% in 2025, premium pricing leads at 54%, and North India commands a 35% regional share.

Market Snapshot

|

Metric |

Value |

| Base Year Market Size (2025) |

USD 20.67 Billion |

|

Market Size (2026) |

USD 22.67 Billion |

|

Forecast Market Size (2034) |

USD 47.53 Billion |

|

CAGR (2026-2034) |

9.7% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (35% share, 2025) |

|

Leading Product |

Non-Athletic Footwear (67.64%, 2025) |

|

Leading Pricing Segment |

Premium (54%, 2025) |

The market growth trajectory from 2020 through 2034, with historical expansion to USD 20.67 Billion in 2025, and an estimated USD 22.67 Billion in 2026. reflects consistent consumer-driven demand. The forecast to USD 47.53 Billion captures accelerating e-commerce penetration, brand premiumization, and rising athletic footwear adoption across India's younger demographic.

To get more information on this market, Request Sample

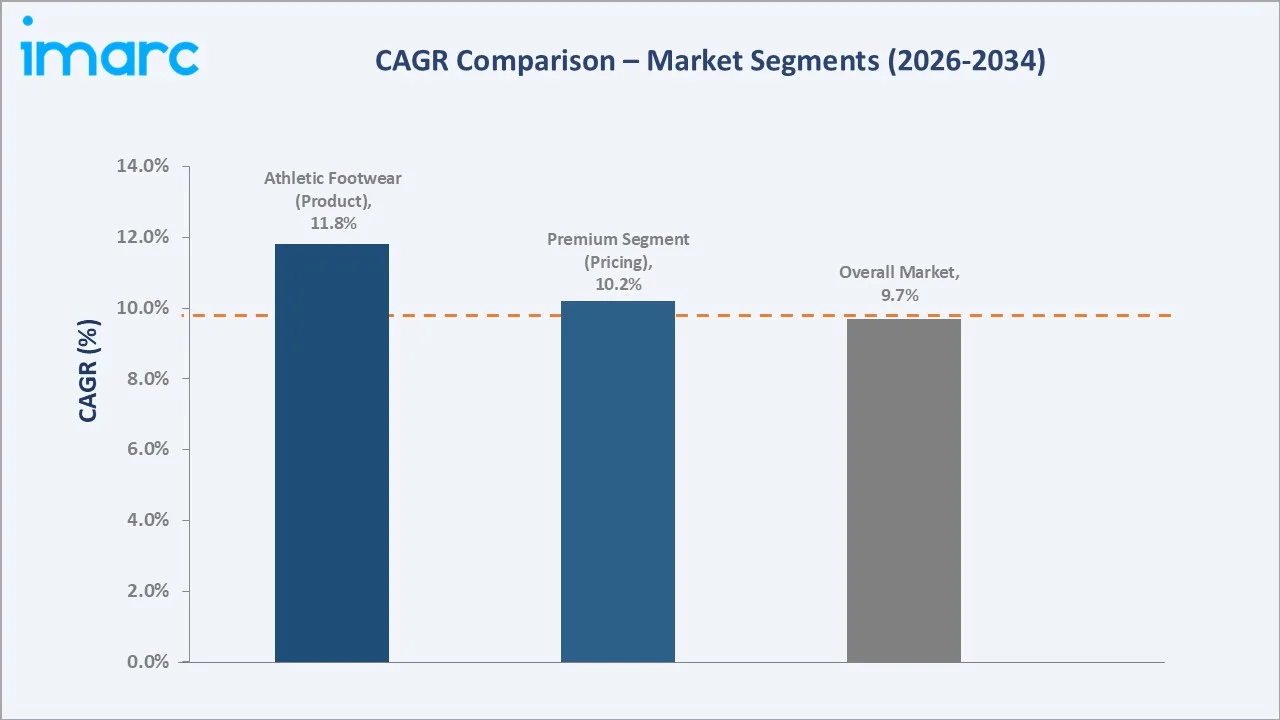

CAGR trajectories across product, pricing, and regional sub-segments show athletic footwear at ~11.8% CAGR and the premium segment at ~10.2% CAGR as the fastest-growing categories within the India footwear industry analysis through 2034.

Executive Summary

The India footwear market is on a sustained growth trajectory from USD 20.67 Billion in 2025 to an estimated USD 22.67 Billion in 2026 and is projected to reach USD 47.53 Billion by 2034. Footwear, spanning casual, formal, athletic, and traditional categories, benefits from India's structural demographic and economic tailwinds, supporting non-discretionary and aspirational demand simultaneously.

Non-athletic footwear dominates at 67.64% in 2025, driven by deeply entrenched consumer habits favouring formal, casual, and traditional Indian styles. Athletic footwear (32.36%) represents the fastest-growing product category at ~11.8% CAGR through 2034, fuelled by India's expanding fitness culture and major global brand investments.

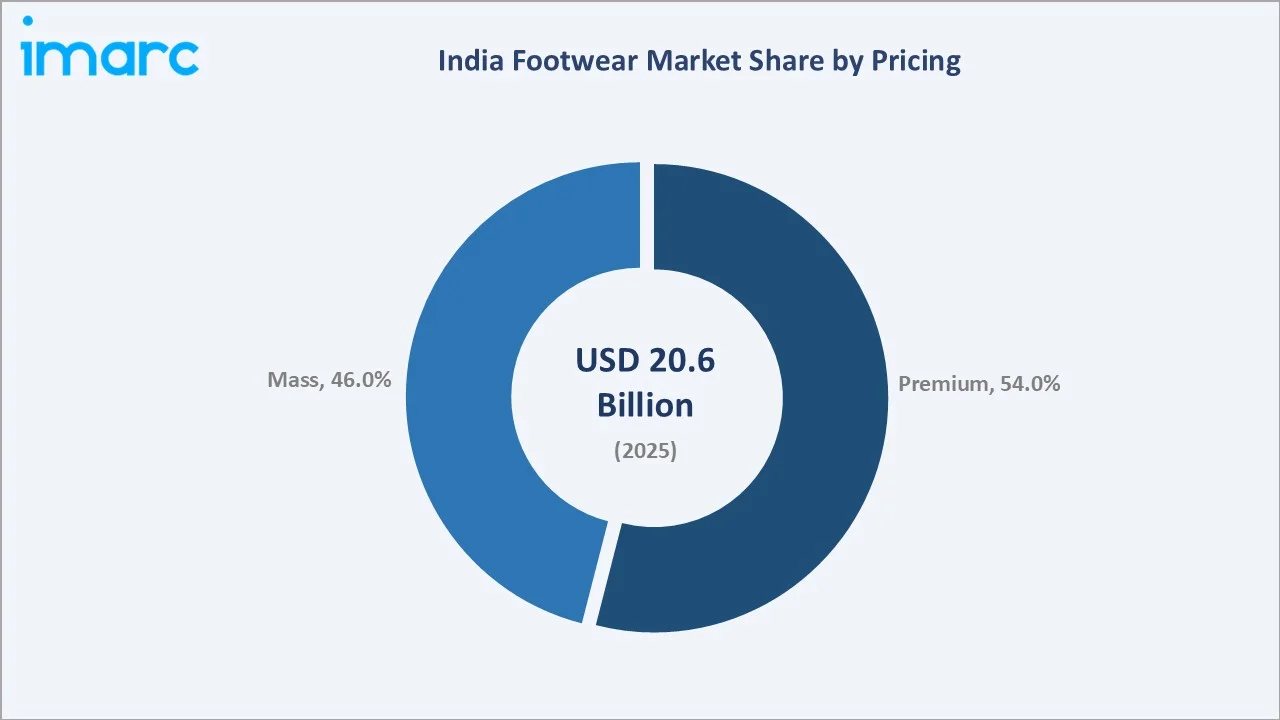

The premium segment commands 54% in 2025, reflecting rising brand consciousness, higher disposable incomes, and social media influence on purchasing aspirations among urban Indian consumers. Mass-market footwear (46%) remains robust, supported by competitive domestic manufacturers delivering value offerings.

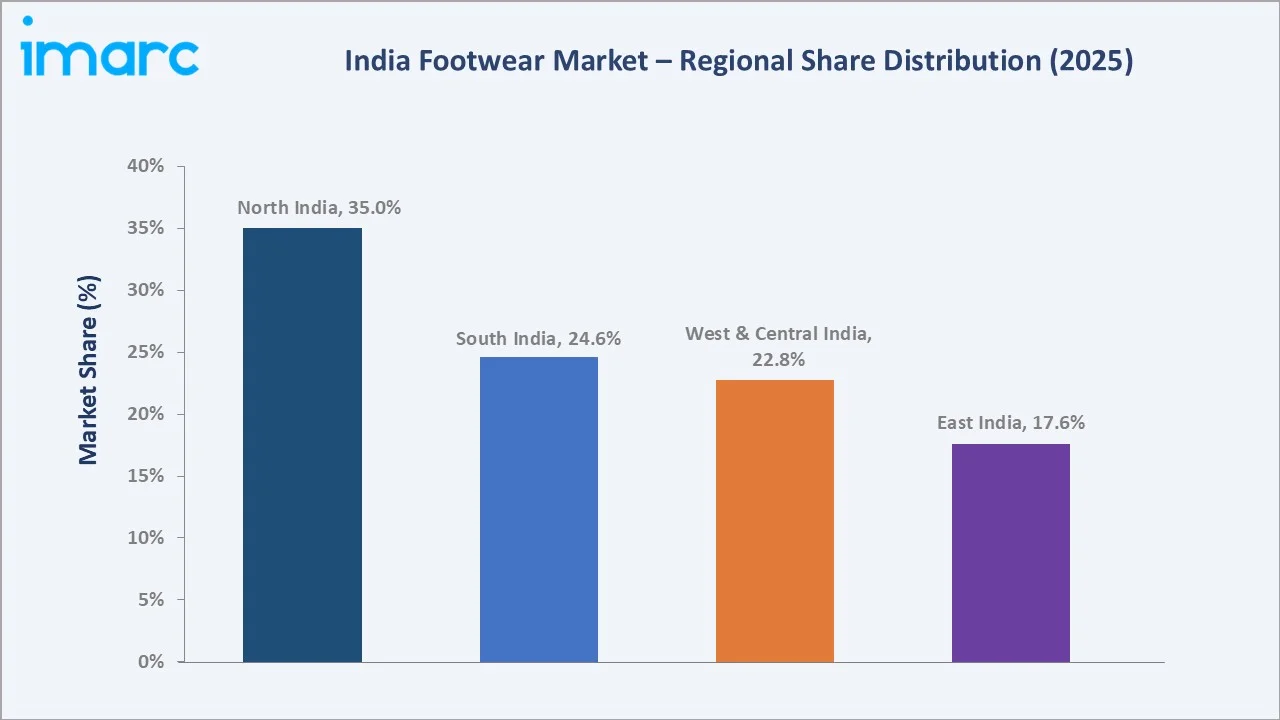

North India leads regional demand at 35.0%, anchored by Agra's manufacturing clusters and high population density. South India (24.6%) follows, driven by Chennai and Bengaluru urban growth, while West & Central India (22.8%) and East India (17.6%) contribute through expanding organized retail.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Non-Athletic Footwear – 67.64% share (2025) |

|

Fastest-Growing Product |

Athletic Footwear – 32.36% share (2025), ~11.8% CAGR |

|

Leading Pricing Segment |

Premium – 54% revenue share (2025) |

|

Leading Region |

North India – 35% revenue share (2025) |

|

Top Companies |

Bata Brand, Relaxo Footwears Limited, Nike, Inc., adidas India Marketing Pvt. Ltd, PUMA India Ltd., Campus Activewear Limited |

Key Analytical Observations Supporting the Above Data:

- Non-athletic footwear at 67.64% dominates because of India's culturally diverse footwear requirements, formal, ethnic, casual, and sandal styles, catering to office, daily wear, and festive occasions across all regions and income brackets.

- Athletic footwear at 32.36% is growing fastest as India's youth population embraces athleisure, fitness awareness rises, and global brands including Nike, adidas, and PUMA increase distribution reach to Tier-2 and Tier-3 cities.

- The premium segment's 54% dominance reflects brand-aspirational urban consumers willing to pay a premium for recognized brands, quality materials, and fashion-forward designs driven by social media influence and rising incomes.

- North India's 35.0% share is reinforced by its dual role as India's largest consumer market and dominant production hub, with Agra contributing approximately 28% of India's total footwear exports.

India Footwear Market Overview

Footwear encompasses outer coverings worn on feet to provide comfort, protection, and style across athletic and non-athletic activities. Products are manufactured from leather, rubber, plastic, fabric, and synthetic materials, offering diverse designs catering to formal, casual, athletic, traditional, and ethnic preferences across India's diverse consumer segments.

India's footwear ecosystem integrates raw material suppliers, component manufacturers, branded and unbranded footwear producers, organized and unorganized retail, and e-commerce distribution platforms. India ranks as the world's second-largest producer and consumer of footwear, with government PLI schemes driving manufacturing modernization and export growth.

Market Dynamics

To evaluate market opportunities, Request Sample

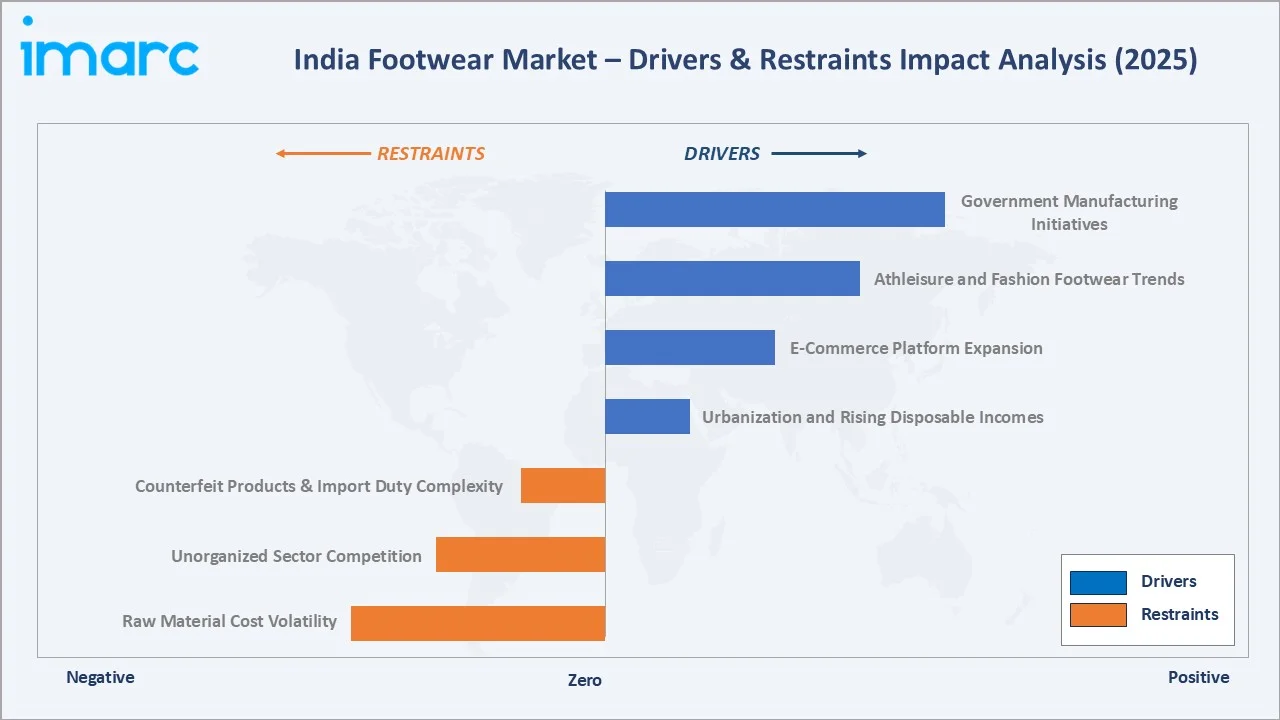

Market Drivers

- Urbanization and Rising Disposable Incomes: India's urban population is projected to reach 600 million by 2031, significantly expanding the addressable market and driving demand for footwear, particularly in branded and organized segments. This shift is accelerating premiumization trends, with consumers increasingly prioritizing style, comfort, and brand value. It is also enabling deeper market penetration across Tier I and Tier II cities, supporting sustained growth for organized footwear players.

- E-Commerce Platform Expansion: Rapid internet and smartphone penetration, especially in Tier-2 and Tier-3 cities, is transforming footwear distribution. E-commerce in India is expected to surpass US$ 145 billion in 2025, powered by mobile commerce and AI-driven hyper-personalization enhancing customer experiences. Platforms like Myntra, Amazon, and Flipkart offer access to thousands of SKUs, enabling international brands to reach previously inaccessible consumers cost-effectively.

- Athleisure and Fashion Footwear Trends: India's growing fitness awareness and youth-driven fashion preferences are fueling demand for versatile, stylish footwear. The hybrid work culture accelerates demand for comfortable, multipurpose footwear bridging athletic and casual categories, prompting rapid product innovation.

- Government Manufacturing Initiatives: The Indian government's 100% FDI allowance in footwear, Production-Linked Incentive (PLI) schemes, and leather cluster development programs attract global manufacturers, reduce import dependence, and strengthen India's footwear export competitiveness.

Market Restraints

- Raw Material Cost Volatility: Leather prices are subject to cattle supply fluctuations, global hide market movements, and tannery capacity constraints. Rubber and synthetic material costs track global commodity cycles, creating margin pressure for manufacturers unable to fully pass cost increases to price-sensitive segments.

- Unorganized Sector Competition: Over 95% of India's footwear manufacturing units are MSMEs operating informally. These unorganized producers, concentrated in Agra, Chennai, and Kolkata clusters, offer significantly lower price points, intensifying competition for organized branded players in the mass market segment.

Market Opportunities

- Direct-to-Consumer (D2C) Digital Brands: India's digital infrastructure is enabling new footwear brands to build direct consumer relationships through Instagram commerce, brand websites, and app-based platforms targeting specific niches, sustainable footwear, women's comfort wear, and vegan materials, with strong unit economics.

- Sustainable and Eco-Friendly Footwear: Consumer preference for environmentally responsible products is creating a premium segment opportunity. Brands offering footwear from recycled materials, natural rubber, and vegan leather alternatives are experiencing accelerated demand among younger, environmentally conscious urban consumers.

Market Challenges

- Counterfeit Products: Counterfeit footwear is a persistent challenge for premium and international brands in India, undercutting authentic pricing and damaging brand equity. The problem is particularly acute in unorganized wholesale markets and informal online marketplaces.

- Import Duty Complexity: India's multi-layered import duty structure on footwear components creates supply chain complexity for brands relying on imported uppers, soles, and specialty materials. Navigating customs classifications and GST compliance adds administrative costs for smaller branded players.

Emerging Market Trends

1. Rise of Athleisure and Performance-Comfort Hybrid Footwear

The convergence of athletic performance and everyday casual wear is reshaping India's footwear landscape. Lehar Footwear's 2025 launch of RANNR brand and Campus Activewear's expanding athleisure lines reflect how manufacturers are pivoting toward comfort-performance hybrids targeting fitness-conscious urban millennials and Generation Z consumers.

2. Accelerated E-Commerce and D2C Brand Growth

E-commerce platforms now account for a growing share of India's footwear sales, enabled by AI-driven personalization, virtual try-on features, and one-day delivery in metro markets. Meesho's 2025 AI expansion demonstrates how digital-first platforms are extending accessible footwear commerce to first-time online buyers in rural India.

3. Sustainable and Vegan Footwear Innovation

Metro Brands' March 2025 shoe recycling campaign and growing adoption of plant-based materials signal a structural shift toward circular economy principles. Brands leveraging sustainability as a differentiator are attracting environmentally conscious consumers willing to pay above-market prices for responsible products.

4. Manufacturing FDI and Export Hub Development

Hwaseung Footwear Group's USD 210 million Tamil Nadu investment in 2025, creating 20,000 jobs, exemplifies India's growing appeal as a global footwear manufacturing destination. FDI inflows are modernizing production infrastructure and positioning India to capture export share from China amid supply chain diversifications.

Industry Value Chain Analysis

The India footwear value chain spans six stages from raw material supply through consumer purchase. Manufacturing and branded distribution capture the highest value-add margins, while organized retail and e-commerce logistics generate working capital requirements that favor well-capitalized mid-to-large manufacturers.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Tanneries (Chennai, Kanpur), rubber producers, synthetic material importers, fabric mills |

|

Component Manufacturing |

Sole manufacturers, insole producers, lace and accessory suppliers in Kanpur, Chennai clusters |

|

Footwear Manufacturing |

Bata India, Relaxo Footwears, Liberty Shoes, Paragon, Ajanta Shoes, Campus Activewear |

|

Brand & Design |

Nike India, adidas India, PUMA India, Khadim India |

|

Distribution & Retail |

Footwear specialists, multi-brand outlets, company-owned stores, franchise networks |

|

E-Commerce & D2C |

Amazon, Flipkart, Myntra, brand websites, Meesho, Nykaa Fashion |

Vertically integrated footwear players, with in-house design, manufacturing, and retail capabilities, achieve higher margin capture compared to fragmented or outsourced models. Strong brand positioning, efficient supply chain management, and inventory optimization are critical cost and differentiation drivers for participants in the Indian footwear market.

Technology Landscape in the India Footwear Industry

Advanced Materials and Manufacturing Technology

Indian footwear manufacturers are adopting EVA foam injection molding, TPU sole technologies, and memory foam cushioning systems. Automated lasting machines, computer-controlled stitching, and CNC cutting systems are progressively replacing manual labor in organized-sector factories, improving consistency and reducing per-unit costs.

Digital Retail and AI-Driven Commerce

AI-powered size recommendation engines, virtual try-on augmented reality features, and personalized product discovery algorithms deployed by Myntra and brand apps are reducing return rates and increasing conversion. These technologies particularly benefit athletic footwear sales where precise fit directly impacts consumer satisfaction.

Sustainable Material Innovation

Plant-based leather alternatives from pineapple fiber (Pinatex), mushroom leather (mycelium), and recycled PET bottle uppers are entering India's premium footwear segment. Domestic tanneries are investing in chrome-free leather processing and waterless dyeing technologies to meet environmental regulations and ESG-conscious brand procurement requirements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Non-Athletic Footwear |

67.64% |

2025 |

|

Material |

Leather |

45.0% |

2025 |

|

Distribution Channel |

Footwear Specialists |

38.0% |

2025 |

|

Pricing |

Premium |

54.0% |

2025 |

|

End User |

Women |

54.36% |

2025 |

|

Region |

North India |

35.0% |

2025 |

By Product

Non-athletic footwear commands a 67.64% majority share in 2025, reflecting India's culturally diverse footwear ecosystem encompassing formal office shoes, casual sandals, traditional ethnic footwear (chappals, mojaris, kolhapuris), and everyday casual shoes. The segment's dominance is anchored in India's formal work culture and religious and festive footwear traditions.

To access detailed market analysis, Request Sample

Athletic footwear at 32.36% in 2025, growing fastest at ~11.8% CAGR, is driven by India's expanding sports participation, government Khelo India programs, growing gym culture, and the powerful aspirational marketing of global performance brands. The segment increasingly blurs with lifestyle athleisure, expanding total addressable market beyond traditional sports participants.

By Pricing

The premium segment leads with 54.0% share in 2025, reflecting rising brand aspirations among India's growing middle class. Urban consumers increasingly associate premium branded footwear with social status, quality assurance, and personal style expression, driving trading-up behavior across income categories.

Mass-market footwear at 46.0% in 2025 remains essential given India's large price-sensitive consumer base. Domestic champions Relaxo, Paragon, Khadim, and Ajanta serve this segment with affordable, durable products leveraging efficient manufacturing in established production clusters, providing revenue stability especially in rural and semi-urban markets.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

35.0% |

Agra manufacturing hub; Delhi NCR premium demand; UP production clusters; Chandigarh retail growth |

|

South India |

24.6% |

Chennai leather industry; Bengaluru IT consumer affluence; rising urban middle class; e-commerce penetration |

|

West & Central India |

22.8% |

Mumbai premium retail: Maharashtra and Gujarat organized retail expansion; Pune youth consumer growth |

|

East India |

17.6% |

Kolkata traditional manufacturing; rising Odisha and West Bengal consumption; e-commerce-driven access |

North India's 35.0% market dominance in 2025 is underpinned by structural advantages as both India's largest footwear production hub and consumption center. Agra's footwear cluster produces approximately 65% of domestic leather shoe consumption and contributes 28% of India's footwear exports, creating an integrated manufacturing-to-retail ecosystem with unmatched supply chain efficiency.

South India at 24.6% benefits from Chennai's world-class leather tannery infrastructure and Bengaluru's affluent IT sector consumer base. The region has been a preferred destination for international footwear manufacturing FDI, exemplified by Hwaseung Footwear Group's 2025 Tamil Nadu investment, which will strengthen South India's production capacity significantly.

Competitive Landscape

The India footwear market is moderately competitive, featuring domestic champions with mass-market scale and premium international brands competing across product categories, pricing tiers, and distribution channels. Domestic players including Bata, Relaxo, Liberty, and Paragon hold strong mass-market positions, while Nike, adidas, and PUMA lead the aspirational athletic and premium segments.

|

Company |

Key Products |

Market Position |

Strategic Focus |

|

Bata Brand |

Formal, casual, athletic, kids |

Leader |

Pan-India network; affordable premium; store modernization |

|

Relaxo Footwears Limited |

Sparx, Flite, Bahamas |

Leader |

Mass market leader; value pricing; rural reach |

|

Nike, Inc. |

Athletic footwear, lifestyle sneakers |

Leader |

Premium athletic; youth marketing; D2C digital |

|

adidas India Marketing Pvt. Ltd |

Running, training, originals lifestyle |

Leader |

Performance + lifestyle; sustainability; digital |

|

PUMA India Ltd. |

Sports, athleisure, motorsport-inspired |

Leader |

Youth-centric; celebrity collaborations; D2C |

|

Campus Activewear Limited |

Sports, athleisure, casual footwear |

Challenger |

Affordable athletic; Tier-2/3 expansion; brand building |

|

Liberty |

Formal, casual, sports, kids |

Challenger |

Multi-brand portfolio; women's footwear focus |

|

Khadim India Ltd. |

Casual, formal, school shoes |

Challenger |

East India stronghold; affordable family footwear |

|

Paragon Polymer Product Private Limited |

Slippers, sandals, casual shoes |

Challenger |

South India mass market; durable value products |

Key players include Bata Brand, Relaxo Footwears Limited, Nike, Inc., adidas India Marketing Pvt. Ltd, PUMA India Ltd., Campus Activewear Limited, Liberty, Khadim India Ltd., Paragon Polymer Product Private Limited, and others.

Key Company Profiles

Bata Brand

Bata is the country's largest organized footwear retailer. Bata's heritage brand equity spanning formal to casual categories and all age groups makes it the default footwear destination for aspirational middle-class consumers across India's urban and semi-urban markets.

- Product Portfolio: Formal shoes, casual footwear, athletic shoes, sandals, school shoes, and children's footwear across Bata, Hush Puppies, and Scholl brands

- Recent Developments: In October 2024, Bata introduced a revamped website aimed at delivering a more seamless and user-friendly online shopping experience. The upgraded platform focuses on improving navigation, enhancing product discovery, and providing a smoother end-to-end digital journey for customers.

- Strategic Focus: Bata's strategy centers on store format modernization, expansion of aspirational premium sub-brands, and digital channel investment to defend market leadership amid intensifying competition from global athletic brands and emerging D2C players.

Nike, Inc.

Nike, operating as Nike India Private Limited, functions as the dominant premium athletic and lifestyle footwear brand, leveraging global innovation, celebrity athlete endorsements, and an expanding network of exclusive brand stores and digital channels. Nike's product pipeline of performance and street-culture lines commands the highest brand equity among Indian youth consumers.

- Product Portfolio: Running shoes, basketball footwear, training shoes, Jordan Brand, Air Max lifestyle, and Nike Golf lines

- Recent Developments: In March 2026, Nike unveiled the Nike Air Liquid Max, a bold new addition to its Air Max lineup that blends advanced cushioning technology with striking design. The sneaker builds on decades of Air Max innovation, introducing a fresh silhouette aimed at delivering both comfort and visual impact.

- Strategic Focus: Nike's India strategy focuses on premium positioning, digital-first consumer engagement, and selective Tier-2 city expansion to capture India's growing aspirational athletic footwear consumer base while defending premium price points from local challengers.

Relaxo Footwears Limited

Relaxo Footwears is India's largest footwear company by volume, manufacturing and marketing affordable mass-market footwear through its Sparx, Flite, and Bahamas brand portfolio. Relaxo's manufacturing scale and distribution reach into rural India provide a competitive moat virtually impossible for organized-sector challengers to replicate.

- Product Portfolio: Sparx, Flite, Bahamas, and others.

- Recent Developments: In November 2024, Relaxo Footwears expanded its retail presence with the launch of a new exclusive brand outlet in Kalol, Gandhinagar, Gujarat. This addition marks a key step in strengthening the company’s footprint in the western region and improving accessibility for customers. The new store offers a wide range of footwear across Relaxo’s brands, catering to men, women, and children, and aims to deliver a comprehensive shopping experience.

- Strategic Focus: Relaxo's strategy leverages its cost leadership in mass-market EVA and rubber footwear to defend rural market dominance while gradually trading up through Sparx toward the lower-premium athletic segment where margin potential is higher.

Campus Activewear Limited

Campus Activewear has emerged as India's leading domestically manufactured affordable athletic and athleisure footwear brand, capturing significant market share from global brands in the mid-market price segment. Campus's vertically integrated manufacturing and targeted marketing toward Tier-2 and Tier-3 city youth consumers represent a differentiated competitive strategy.

- Product Portfolio: Running shoes, athleisure sneakers, casual footwear, and sports performance shoes across the Campus brand

- Recent Developments: In September 2025, Campus Activewear announced plans to invest ₹230 crore to expand its manufacturing capacity, supporting its growth ambitions in the Indian footwear market. The expansion includes setting up a new facility in Pantnagar, Uttarakhand, to enhance production capabilities. The project will add significant capacity for both footwear uppers and assembly, helping the company meet rising demand while improving backward integration.

- Strategic Focus: Campus's strategy targets the price-value gap between international athletic brands and domestic mass-market players, offering contemporary designs and performance features at accessible price points resonating with aspirational youth consumers across India's smaller cities.

Market Concentration Analysis

The India footwear market is highly fragmented, with the organized sector accounting for approximately 30-35% of total market value while the unorganized sector commands the remaining share. No single company holds more than 6-8% of total market revenue, reflecting diversity across price points, product categories, and geographies.

Consolidation is accelerating in organized premium and mid-market segments through retail acquisitions, brand licensing deals, and e-commerce aggregation. International brands are increasing India market investments through subsidiary expansions and direct digital channels, progressively formalizing consumer demand away from unbranded and counterfeit alternatives.

Investment & Growth Opportunities

Fastest-Growing Segments

Athletic footwear at ~11.8% CAGR through 2034 represents the highest-growth product opportunity, driven by India's growing fitness culture and sports participation. The premium segment at ~10.2% CAGR captures rising brand aspirations among India's expanding upper-middle-class consumer cohort, offering above-market revenue growth with superior margin profiles.

Emerging Markets

Tier-2 and Tier-3 Indian cities represent the most significant untapped growth opportunity, with urbanization driving rising incomes and fashion awareness in markets including Lucknow, Jaipur, Coimbatore, Surat, and Indore. These markets are rapidly transitioning from unorganized to organized branded footwear consumption, creating first-mover advantages for investing brands.

Venture & Investment Trends

D2C footwear startups focusing on sustainable materials, customization, women's comfort footwear, and athleisure niches are attracting venture capital investment. Manufacturing FDI continues to flow into Tamil Nadu and Andhra Pradesh footwear clusters, supported by state government incentive packages and India's improving industrial infrastructure.

Future Market Outlook (2026-2034)

The India footwear market is forecast to expand from USD 20.67 Billion in 2025 to an estimated USD 22.67 Billion in 2026 and further to USD 47.53 Billion by 2034 at a CAGR of 9.7%, adding over USD 26 Billion in incremental annual market value over the forecast period. This growth reflects the market's dual drivers of expanding consumer base and rising per-capita spending as India urbanizes.

Three forces will shape India's footwear market through 2034: digital commerce reaching 30%+ of footwear sales by 2030; athletic and athleisure demand convergence creating a blended product category; and manufacturing FDI modernizing production capacity to support both domestic demand and export growth simultaneously.

India's footwear industry is positioned to emerge as a top-three global exporter by 2034, leveraging its established manufacturing base, competitive labor costs, improving quality standards, and government export promotion policies, reinforcing domestic brand building as manufacturers invest in design capabilities required for international markets.

Research Methodology

Primary Research

Primary research encompassed structured interviews with footwear industry stakeholders including senior brand executives, retail chain managers, e-commerce category heads, footwear exporters, and industry association representatives from CLE (Council for Leather Exports) and FDDI. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Ministry of Commerce footwear export statistics, CLE annual reports, Footwear Export Promotion Council data, DPIIT FDI data, IMARC Group proprietary databases, company annual reports (Bata, Relaxo, Campus, Liberty, Metro Brands), industry trade publications, and macroeconomic data from World Bank, IMF, and MOSPI.

Forecasting Models

Market size estimations and growth projections were derived using bottom-up and top-down forecasting models incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

India Footwear Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Non-Athletic Footwear, Athletic Footwear |

| Materials Covered | Rubber, Leather, Plastic, Fabric, Others |

| Distribution Channels Covered | Footwear Specialists, Online Sales, Supermarkets and Hypermarkets, Departmental Stores, Clothing Stores, Others |

| Pricings Covered | Premium, Mass |

| End Users Covered | Men, Women, Kids |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Bata Brand, Relaxo Footwears Limited, Nike, Inc., adidas India Marketing Pvt. Ltd, PUMA India Ltd., Campus Activewear Limited, Liberty, Khadim India Ltd., Paragon Polymer Product Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Footwear Market Report

The India footwear market grew from USD 20.67 Billion in 2025 to an estimated USD 22.67 Billion in 2026, and is projected to reach USD 47.53 Billion by 2034, growing at a CAGR of 9.7% during 2026-2034.

Non-athletic footwear dominates with a 67.64% share in 2025. Athletic footwear (32.36%) is the fastest-growing segment at ~11.8% CAGR through 2034.

The premium segment leads with 54.0% share in 2025, reflecting rising brand consciousness and higher disposable incomes. The mass segment accounts for the remaining 46%.

North India leads with a 35.0% share in 2025, supported by Agra's manufacturing clusters and strong retail infrastructure. South India follows at 24.6%.

Key players include Bata Brand, Relaxo Footwears Limited, Nike, Inc., adidas India Marketing Pvt. Ltd, PUMA India Ltd., Campus Activewear Limited, Liberty, Khadim India Ltd., Paragon Polymer Product Private Limited, and others.

The primary growth drivers include rapid urbanization, rising disposable incomes, expanding e-commerce and D2C channels, growing athleisure and fitness culture, government PLI schemes encouraging domestic manufacturing, and increasing FDI from global footwear manufacturers seeking to establish India as a production and export hub.

Athletic footwear is the fastest-growing product segment, projected to grow at ~11.8% CAGR from 2026 to 2034. Growth is driven by India's rising fitness awareness, government Khelo India sports programs, expanding gym culture, and aggressive marketing and distribution expansion by global brands including Nike, adidas, PUMA, and domestic challenger Campus Activewear.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade