India Generic Injectables Market Size, Share, Trends and Forecast by Therapeutic Area, Container, Distribution Channel, and Region, 2026-2034

India Generic Injectables Market Summary:

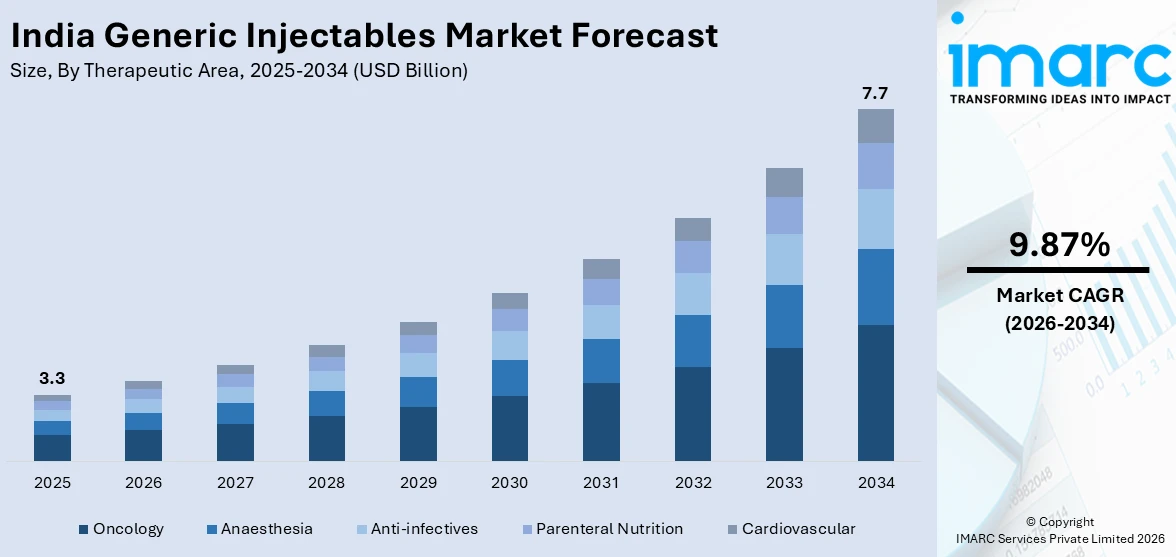

The India generic injectables market size was valued at USD 3.30 Billion in 2025 and is projected to reach USD 7.70 Billion by 2034, growing at a compound annual growth rate of 9.87% from 2026-2034.

The market is driven by the rising prevalence of chronic diseases such as cancer, diabetes, and cardiovascular disorders, along with increasing demand for cost-effective therapeutic alternatives. Expanding healthcare infrastructure, favorable government policies promoting domestic pharmaceutical manufacturing, and growing hospital networks are further strengthening adoption. Advancements in drug delivery systems, increasing patent expirations of branded biologics, and the expanding role of biosimilars are reshaping the treatment landscape, positively influencing the India generic injectables market share.

Key Takeaways and Insights:

- By Therapeutic Area: Oncology dominates the market with a share of 35% in 2025, driven by escalating cancer burden, increasing adoption of affordable generic chemotherapy agents, and expanding treatment infrastructure.

- By Container: Vials leads the market with a share of 50% in 2025, owing to their widespread compatibility with diverse injectable formulations, established manufacturing capabilities, and suitability for multi-dose applications.

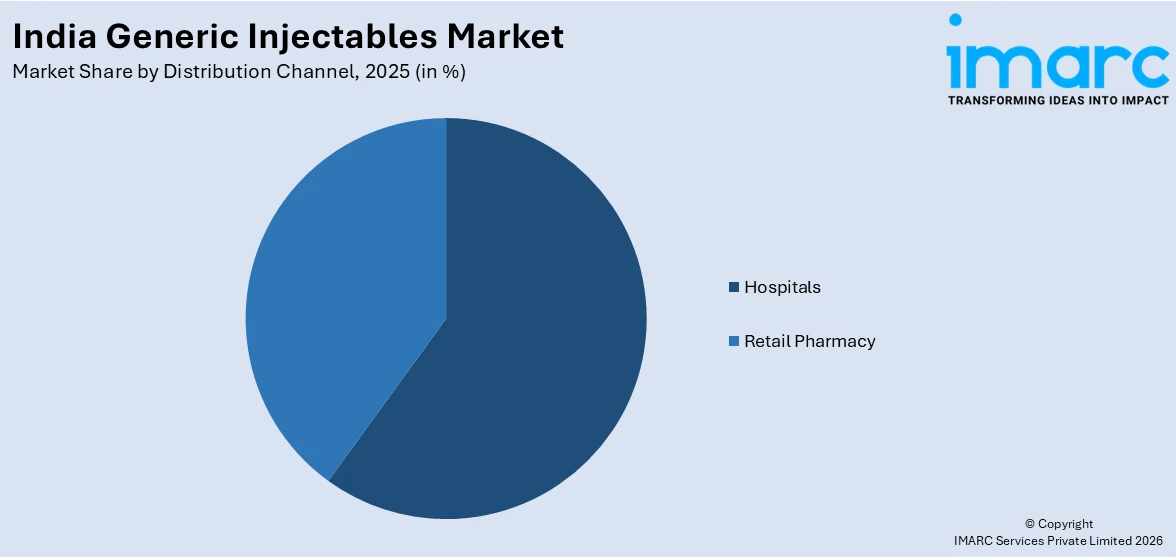

- By Distribution Channel: Hospitals represent the largest segment with a market share of 68% in 2025, driven by the concentration of injectable drug administration in clinical settings and growing government-funded healthcare programs.

- Key Players: The India generic injectables market exhibits a moderately fragmented competitive landscape, with established domestic pharmaceutical manufacturers competing alongside multinational corporations across therapeutic segments, leveraging cost-efficient production and expanding distribution networks.

To get more information on this market Request Sample

The India generic injectables market is advancing as healthcare systems prioritize affordable treatment options for the country's growing disease burden. In February 2026, Natco Pharma received CDSCO approval to manufacture and market generic Semaglutide injections in India, marking a key regulatory milestone for complex injectable biologics and expanding domestic portfolio offerings in diabetes care. Government initiatives supporting domestic bulk drug and injectable manufacturing are strengthening production capabilities and reducing import dependence for critical active pharmaceutical ingredients. Expanding public health insurance programs are broadening the insured population base and increasing institutional demand for cost-effective injectable therapies across hospitals nationwide. The convergence of rising chronic disease prevalence, favorable regulatory reforms, growing biosimilar adoption, and increasing healthcare expenditure is creating a supportive demand environment. Additionally, India's robust pharmaceutical manufacturing infrastructure and skilled workforce are reinforcing the country's position as a leading global hub for generic injectable production and export.

India Generic Injectables Market Trends:

Rising Adoption of Biosimilar Injectable Therapies

The growing acceptance of biosimilar injectables is reshaping India's pharmaceutical landscape, as healthcare providers increasingly prefer these cost-effective alternatives to expensive branded biologics. India leads globally in biosimilar approvals, with regulatory authorities continuously refining approval pathways to align with international standards. Revised draft guidelines on similar biologics are enabling faster commercialization across oncology, autoimmune, and metabolic therapeutic areas. In January 2026, Zydus Lifesciences launched India’s first nivolumab biosimilar, reducing treatment costs by 75% and expanding patient access to advanced immuno‑oncology therapies. This regulatory evolution, combined with strong domestic manufacturing expertise in complex biologic formulations, is accelerating the availability of affordable injectable biologics nationwide.

Advancement in Injectable Drug Delivery Technologies

Innovation in drug delivery systems is transforming the generic injectables segment, with manufacturers increasingly investing in prefilled syringes, auto-injectors, and long-acting depot formulations. These advanced delivery platforms enhance patient compliance by offering improved convenience, precise dosing accuracy, and reduced frequency of healthcare facility visits. In December 2025, Intas Pharmaceuticals partnered with Serum Institute of India‑backed IntegriMedical to introduce needle‑free injection systems across IVF and gynaecology clinics nationwide, reflecting rising adoption of patient‑centric delivery technologies that reduce discomfort and improve adherence. The integration of smart injection devices with digital health platforms is gaining traction, enabling real-time adherence tracking and therapy optimization. These developments are encouraging self-administration models and expanding the addressable patient population.

Expansion of Contract Development and Manufacturing Services

The contract development and manufacturing organization segment for sterile injectables is witnessing significant expansion in India, driven by increasing global outsourcing of complex parenteral drug production. Indian manufacturing facilities are attracting international pharmaceutical companies seeking regulatory-ready infrastructure and cost-efficient production solutions. In October 2025, Recipharm inaugurated newly commissioned parenteral development and sterility laboratories at its Bengaluru site, significantly enhancing its sterile injectable formulation development and analytical testing capabilities for global partners. Growing investments in advanced aseptic processing capabilities, isolator-based filling lines, and flexible multi-product manufacturing platforms are enabling contract manufacturers to accommodate diverse formulation requirements across therapeutic categories, reinforcing India's competitive advantage in the global injectable supply chain.

Market Outlook 2026-2034:

The India generic injectables market is poised for sustained revenue growth through the forecast period, underpinned by rising chronic disease prevalence, expanding healthcare access, and strengthening domestic manufacturing capabilities. Revenue expansion will be driven by increasing biosimilar adoption, growing hospital infrastructure investment under government-funded programs, and rising export opportunities to regulated international markets. The convergence of favorable regulatory reforms, technology-driven manufacturing advancements, and expanding insurance coverage is expected to create a robust demand environment for affordable injectable therapies, positioning India as a critical global hub for generic injectable production. The market generated a revenue of USD 3.30 Billion in 2025 and is projected to reach a revenue of USD 7.70 Billion by 2034, growing at a compound annual growth rate of 9.87% from 2026-2034.

India Generic Injectables Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Therapeutic Area |

Oncology |

35% |

|

Container |

Vials |

50% |

|

Distribution Channel |

Hospitals |

68% |

Therapeutic Area Insights:

- Oncology

- Anaesthesia

- Anti-infectives

- Parenteral Nutrition

- Cardiovascular

Oncology dominates with a market share of 35% of the total India generic injectables market in 2025.

The oncology leads the India generic injectables market owing to the escalating cancer burden driven by lifestyle changes, environmental factors, and an aging population. The availability of affordable generic chemotherapy agents has made injectable cancer treatment more accessible across public and private hospital settings. According to reports, in February 2026, the Government of India exempted basic customs duty on 17 key cancer drugs in the Union Budget 2026–27, a move expected to lower prices and expand access to essential oncology injectables nationwide.

The development of cancer care infrastructure in tier-two and tier-three cities is also fueling the demand for generic oncology injectables. National health programs related to cancer prevention and control are also strengthening cancer care capabilities at the district level. In addition, the increasing use of biosimilar monoclonal antibodies in cancer treatment for various types of cancers is also increasing the market for generic oncology injectables, including both chemotherapy centers and new outpatient facilities.

Container Insights:

- Vials

- Ampoules

- Premix

- Prefilled Syringes

Vials leads with a share of 50% of the total India generic injectables market in 2025.

Vials remain the preferred container format due to their versatility in accommodating a wide range of injectable formulations, including lyophilized powders, liquid solutions, and suspensions across multiple therapeutic categories. In March 2025, Sovereign Pharma secured EU approval for aseptic and terminally sterilized injectable products, including vials, ampoules, cartridges, and pre‑filled syringes reinforcing international regulatory confidence in India’s sterile injectable production quality. Their compatibility with both single-dose and multi-dose applications makes them suitable for diverse hospital and clinical settings.

The dominant position of vials is further supported by their established use in critical care, oncology, and anti-infective injectable therapies. Improvements in manufacturing, such as better glass quality, improved closure systems, and automated filling lines, are improving the quality of vials. Additionally, the ready availability of vial-based formulations through government procurement contracts ensures a steady demand for vials, making them the backbone of the generic injectable packaging industry in India.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Retail Pharmacy

Hospitals exhibit a clear dominance with a 68% share of the total India generic injectables market in 2025.

Hospitals dominate the distribution landscape as injectable drugs are predominantly administered in clinical settings requiring professional supervision, sterile environments, and patient monitoring capabilities. The expanding network of public and private hospitals across India, coupled with increasing surgical procedures, emergency care admissions, and chronic disease management protocols, is driving institutional demand. In 2025, the Central Government Health Scheme (CGHS) expanded its network by empanelling 468 hospitals nationwide, significantly widening treatment access for beneficiaries at government‑approved facilities.

Government spending on healthcare infrastructure is further strengthening the hospital-based distribution channels. The national missions emphasize the need to improve the public health laboratories, emergency care, and critical care hospitals are increasing the treatment capacities in the country. Increased spending on public health, which is a result of the government's increasing commitment to ensuring healthcare access, is further increasing hospital capacities and treatment numbers, thereby increasing demand for injectable pharmaceuticals.

Regional Insights:

- North India

- West and Central India

- South India

- East India

The market for generic injectables in North India is quite substantial, owing to the presence of a large population base, an increasing number of hospitals, and rising healthcare spending in the key states. The well-developed pharmaceutical distribution network, increasing government-funded health insurance coverage, and rising incidence of chronic diseases have fueled the demand for generic injectable medications in both the urban metropolitan cities and the emerging semi-urban healthcare settings.

West and Central India is a major segment in the generic injectable market, owing to the strong pharmaceutical manufacturing infrastructure, advanced healthcare infrastructure, and presence of prominent hospital chains. The region has strong industrial capabilities, well-developed supply chain infrastructure, and an increasing patient base looking for affordable injectable treatments in the key therapeutic areas of oncology, cardiology, and critical care.

South India contributes significantly to the generic injectables market, supported by advanced healthcare infrastructure, high health literacy levels, and a well-established network of specialty hospitals and research institutions. The region's strong pharmaceutical manufacturing base, skilled workforce, and progressive adoption of advanced drug delivery technologies are reinforcing demand for generic injectable products across both institutional and retail distribution channels.

East India represents an emerging market for generic injectables, driven by expanding healthcare access, increasing government investment in hospital infrastructure, and growing awareness about affordable treatment options. The region is witnessing gradual improvement in healthcare delivery capabilities, with rising establishment of secondary and tertiary care facilities and expanding public health program coverage accelerating demand for essential injectable pharmaceutical products across underserved populations.

Market Dynamics:

Growth Drivers:

Why is the India Generic Injectables Market Growing?

Escalating Chronic Disease Burden and Expanding Treatment Access

The rising prevalence of chronic diseases including cancer, diabetes, cardiovascular disorders, and autoimmune conditions is fundamentally driving demand for generic injectable therapies across India. The country faces a growing non-communicable disease epidemic fueled by lifestyle changes, urbanization, environmental pollution, and demographic shifts toward an aging population. As per sources, India’s Ministry of Health launched an intensified National Programme for Prevention and Control of Non‑Communicable Diseases (NP‑NCD), scaling up screening and management of hypertension, diabetes, and common cancers across all states. Expanding healthcare access through government-funded health assurance programs is ensuring that more patients receive timely treatment with affordable generic alternatives.

Government Policy Support and Domestic Manufacturing Incentives

The Indian government's strategic initiatives to strengthen domestic pharmaceutical manufacturing are creating a robust ecosystem for generic injectable production. Production linked incentive schemes targeting bulk drug manufacturing and pharmaceutical product diversification are incentivizing domestic production of critical active pharmaceutical ingredients previously imported. As per sources, the government reported that the PLI Scheme for Bulk Drugs enabled import savings of Rs 1,362 crore by March 2025 through creation of domestic API capacity for 25 key inputs, reducing reliance on foreign suppliers. Complementary initiatives including bulk drug park development programs and streamlined regulatory approval processes are collectively enhancing manufacturing capacity, quality standards, and self-reliance in injectable drug production.

Patent Expirations and Biosimilar Market Expansion

The expiration of patents on high-value branded biologics is creating substantial opportunities for generic injectable manufacturers in India. Numerous blockbuster biologic drugs are scheduled to lose exclusivity over the coming years, opening significant addressable markets for biosimilar alternatives. In January 2026, Biocon Biologics announced it will expand its oncology biosimilar portfolio with three major assets including trastuzumab, nivolumab and pembrolizumab, blockbuster drugs losing patent protection, underscoring India’s role in affordable biologic alternatives globally. India's well-established biosimilar ecosystem, backed by experienced manufacturers and a streamlined domestic regulatory framework, positions the country as a global leader in affordable biologic alternatives.

Market Restraints:

What Challenges the India Generic Injectables Market is Facing?

Stringent Regulatory and Quality Compliance Requirements

The manufacturing of sterile injectable products demands rigorous compliance with evolving domestic and international regulatory standards. Meeting current good manufacturing practice requirements, maintaining sterility assurance, and navigating complex multi-jurisdictional approval processes impose significant operational and financial burdens on manufacturers. Periodic regulatory inspections and evolving quality expectations from international agencies create additional compliance challenges requiring continuous investment.

High Capital Investment and Infrastructure Demands

Establishing and maintaining sterile injectable manufacturing facilities requires substantial capital investment in cleanroom infrastructure, aseptic processing equipment, environmental monitoring systems, and continuous validation programs. These high fixed costs and ongoing maintenance expenditures create significant entry barriers for smaller manufacturers and limit capacity expansion, particularly for complex and specialized injectable formulations requiring dedicated production lines.

Active Pharmaceutical Ingredient Import Dependence

Despite ongoing government initiatives promoting domestic active pharmaceutical ingredient production, India continues relying on imports for several critical raw materials and intermediates from single-source international suppliers. This dependency creates supply chain vulnerabilities, price fluctuations, and potential production disruptions impacting consistent availability and cost-effectiveness of generic injectable products. Addressing this reliance requires sustained investment in backward integration capabilities.

Competitive Landscape:

The India generic injectables market features a moderately fragmented competitive structure characterized by the presence of large-scale domestic pharmaceutical manufacturers alongside multinational corporations and emerging specialized players. Competition is primarily driven by product portfolio breadth, manufacturing quality certifications, pricing strategies, and distribution network strength across institutional and retail channels. Market participants are increasingly investing in complex generic formulations, biosimilar development, and advanced drug delivery technologies to differentiate their offerings. Strategic acquisitions, capacity expansions, and international regulatory approvals are shaping competitive positioning as companies seek to capture growing domestic demand while simultaneously strengthening their presence in regulated export markets across multiple geographies.

Recent Developments:

- In January 2026, Sun Pharmaceutical Industries secured DCGI approval to produce and market a generic semaglutide injection in India for chronic weight management. Branded as Noveltreat, it will launch after patent expiry, offered in five dose strengths via a prefilled pen, enhancing accessibility to affordable GLP-1 therapies across the country.

India Generic Injectables Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Therapeutic Areas Covered | Oncology, Anaesthesia, Anti-infectives, Parenteral Nutrition, Cardiovascular |

| Containers Covered | Vials, Ampoules, Premix, Prefilled Syringes |

| Distribution Channels Covered | Hospitals, Retail Pharmacy |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Generic Injectables Market Report

The India generic injectables market size was valued at USD 3.30 Billion in 2025.

The India generic injectables market is expected to grow at a compound annual growth rate of 9.87% from 2026-2034 to reach USD 7.70 Billion by 2034.

Oncology held the largest India generic injectables market share, driven by the rising cancer burden, increasing adoption of affordable generic chemotherapy agents, and expanding treatment infrastructure across public and private hospitals.

Key factors driving the India generic injectables market include rising chronic disease prevalence, government manufacturing incentives, expanding healthcare insurance coverage, patent expirations of branded biologics, and growing biosimilar adoption across therapeutic categories.

Major challenges include stringent regulatory compliance requirements for sterile manufacturing, high capital investment demands for facility establishment, active pharmaceutical ingredient import dependence creating supply chain vulnerabilities, pricing pressures, and evolving international quality standards.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)