India Grinding Wheels Market Size, Share, Trends and Forecast by Type, Material, and Region, 2026-2034

India Grinding Wheels Market Summary:

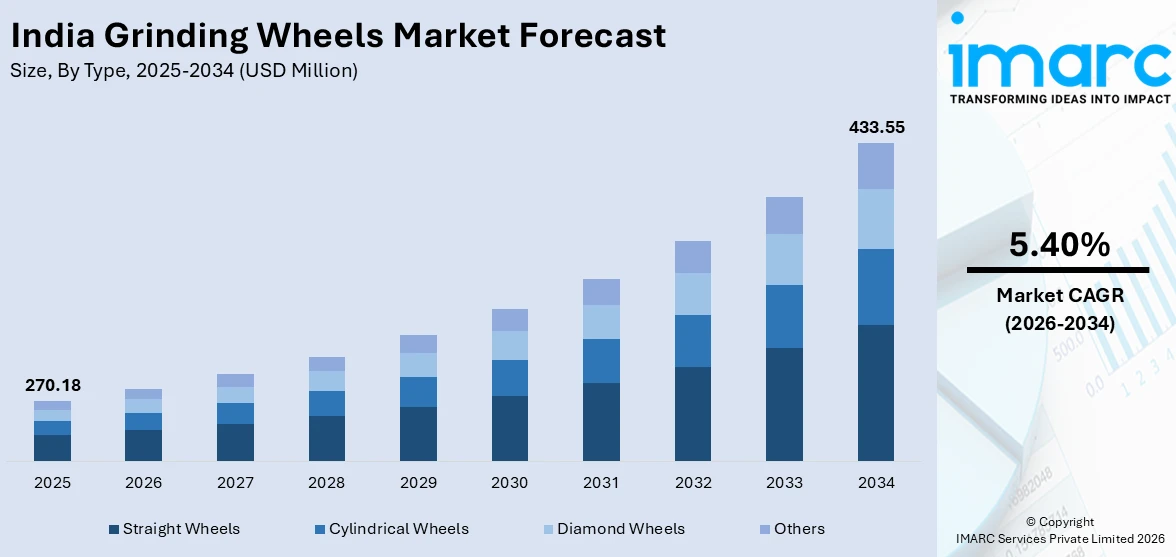

The India grinding wheels market size was valued at USD 270.18 Million in 2025 and is projected to reach USD 433.55 Million by 2034, growing at a compound annual growth rate of 5.40% from 2026-2034.

The India grinding wheels market is experiencing sustained expansion driven by the rapid growth of the country’s manufacturing and industrial sectors, particularly automotive, aerospace, and heavy engineering. Government-led initiatives promoting domestic production, rising infrastructure investments, and growing demand for precision machining solutions are fueling adoption. Advancements in abrasive material technologies, increasing emphasis on surface finishing quality, and the shift toward high-performance super-abrasive tools are further strengthening the India grinding wheels market share.

Key Takeaways and Insights:

- By Type: Straight wheels dominate the market with a share of 35% in 2025, driven by their widespread use in general-purpose grinding, metalworking, and surface finishing across diverse industrial applications.

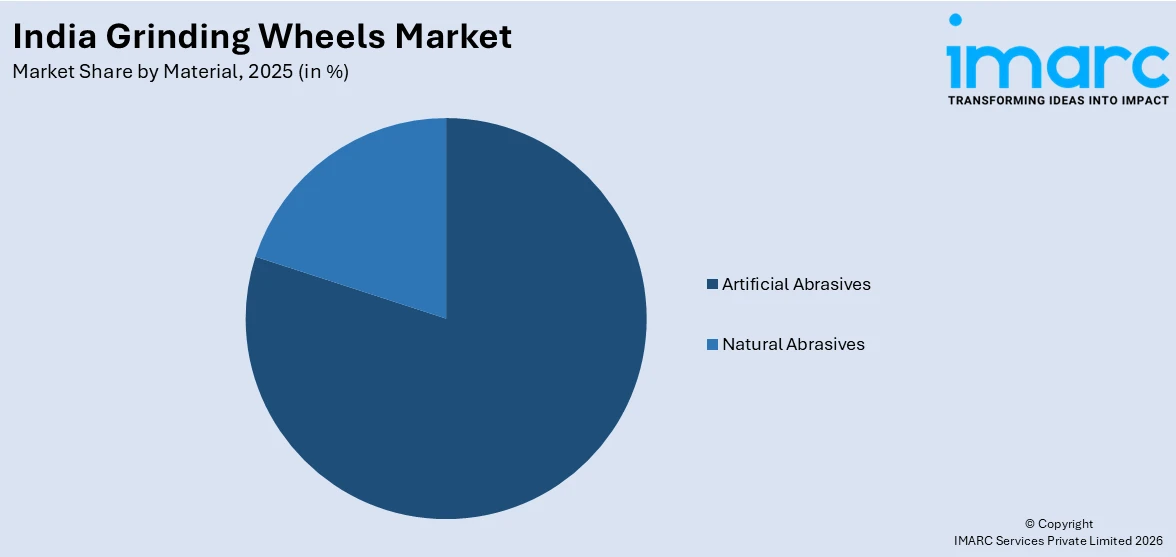

- By Material: Artificial abrasives lead the market with a share of 80% in 2025, owing to their superior hardness, consistent quality, and cost-effectiveness compared to natural alternatives in industrial grinding operations.

- Key Players: The India grinding wheels market features a moderately consolidated competitive landscape, with established domestic manufacturers and multinational abrasive companies competing through product innovation, capacity expansion, and strategic partnerships to strengthen their market positioning across diverse industrial segments.

To get more information of this market Request Sample

The India grinding wheels market is advancing as industries increasingly require precision-engineered abrasive solutions for metalworking, automotive component manufacturing, and infrastructure development. The expanding manufacturing base, bolstered by the Production Linked Incentive (PLI) schemes and Make in India initiatives, is generating robust demand for high-quality grinding wheels. For instance, by March 2025, PLI schemes had attracted actual investments of approximately INR 1.76 lakh crore across 14 key sectors, driving significant manufacturing capacity expansion. The automotive sector, as the fourth-largest producer globally with annual output exceeding 28 million vehicles, remains a primary consumption driver for grinding wheels used in engine component finishing, gear grinding, and precision surface treatment. Simultaneously, the adoption of super-abrasive technologies, including diamond and cubic boron nitride wheels, is reshaping product portfolios as manufacturers seek enhanced precision, longer tool life, and improved operational efficiency.

India Grinding Wheels Market Trends:

Rising Adoption of Super-Abrasive and Advanced Grinding Technologies

The India grinding wheels market is witnessing an accelerating shift toward super-abrasive technologies, including diamond and cubic boron nitride (CBN) wheels, as manufacturers demand tighter tolerances and improved surface finishes. These advanced abrasive tools provide extended service life and superior accuracy compared to traditional products, making them essential for machining high-strength alloys and composite materials. The industry is increasingly shifting toward faster delivery cycles and high-performance grinding solutions to meet evolving manufacturing demands. This trend reflects the growing emphasis on efficiency, precision, and reduced downtime across automotive and industrial applications, thereby supporting the overall advancement of the grinding wheels market in India.

Integration of Smart Manufacturing and IoT-Based Monitoring Systems

Grinding wheel manufacturers are increasingly incorporating smart sensors and IoT-enabled monitoring technologies into their processes to enhance performance optimization, minimize material loss, and improve overall productivity. This shift aligns with broader Industry 4.0 adoption across manufacturing facilities, allowing real-time performance analysis and predictive maintenance strategies. Leading companies in the sector are driving innovation through advanced material engineering and proprietary abrasive technologies, including the development of high-performance alumina grain solutions designed to improve grinding efficiency, extend tool life, and deliver superior precision in demanding industrial applications.

Growing Emphasis on Sustainable and Eco-Friendly Abrasive Solutions

Environmental consciousness is reshaping the grinding wheels market as manufacturers prioritize dust-free grinding processes, energy-efficient production methods, and sustainable raw material sourcing. The industry is witnessing growing momentum toward the development of environmentally sustainable bonded abrasives and recyclable grinding wheel formulations. Manufacturers are increasingly prioritizing eco-conscious production methods and advanced material innovation to reduce environmental impact while maintaining high performance standards. Ongoing investments in new manufacturing facilities for thin wheels and high-purity silicon carbide highlight the sector’s focus on strengthening domestic capabilities and advancing sustainable abrasive technologies, supporting long-term growth and responsible industrial development.

Market Outlook 2026-2034:

The India grinding wheels market is poised for steady growth as manufacturing expansion, infrastructure modernization, and technological advancement continue to drive demand for precision abrasive solutions. Rising investments in automotive, aerospace, and renewable energy sectors will sustain consumption, while indigenous production capabilities strengthened by government incentives are reducing import dependency. The transition toward automation-compatible, high-consistency grinding solutions will further reshape demand patterns. Additionally, increasing emphasis on quality control, productivity enhancement, and cost efficiency across industrial operations is expected to accelerate the adoption of advanced abrasive technologies nationwide. The market generated a revenue of USD 270.18 Million in 2025 and is projected to reach a revenue of USD 433.55 Million by 2034, growing at a compound annual growth rate of 5.40% from 2026-2034.

India Grinding Wheels Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Straight Wheels |

35% |

|

Material |

Artificial Abrasives |

80% |

Type Insights:

- Straight Wheels

- Cylindrical Wheels

- Diamond Wheels

- Others

Straight wheels dominate with a market share of 35% of the total India grinding wheels market in 2025.

Straight grinding wheels represent the most widely utilized product type in India’s industrial landscape, serving as the standard choice for general-purpose grinding, surface finishing, and material removal operations across metalworking, fabrication, and construction sectors. Their flat, disc-shaped design offers versatility in applications ranging from bench grinding and tool sharpening to cylindrical and surface grinding. The automotive industry in India depends heavily on straight grinding wheels for critical machining applications, including engine block finishing, crankshaft grinding, and brake component processing. These abrasive tools play a vital role in ensuring dimensional accuracy, surface quality, and overall component performance across vehicle manufacturing operations.

The dominance of straight wheels is further reinforced by their cost-effectiveness, widespread availability through established distribution networks, and compatibility with standard grinding machinery deployed across small and medium enterprises. India’s expansive network of metalworking workshops and fabrication units, particularly concentrated in industrial clusters across western and northern regions, generates sustained demand for these versatile abrasive tools. Additionally, the growing emphasis on workplace safety standards and dust-minimization protocols is driving adoption of precision-engineered straight wheels with enhanced structural integrity and balanced performance characteristics.

Material Insights:

Access the comprehensive market breakdown Request Sample

- Artificial Abrasives

- Natural Abrasives

Artificial abrasives lead the market with a share of 80% of the total India grinding wheels market in 2025.

Artificial abrasives, primarily comprising aluminum oxide and silicon carbide, hold commanding dominance in India’s grinding wheels market due to their superior hardness, consistent grain quality, and cost-effective large-scale production capabilities. These engineered abrasive materials provide consistent and reliable performance, making them highly suitable for precision manufacturing requirements in automotive, aerospace, and heavy engineering applications. Leading domestic manufacturers operate specialized facilities to produce silicon carbide and fused alumina, supplying a broad portfolio of abrasive variants to both domestic and global markets. Their diversified product offerings support a wide range of industrial grinding, cutting, and finishing processes across multiple end-use sectors.

The artificial abrasives segment is still increasing owing to the constant improvements in the grain design and bonding technologies to strengthen the durability and reduce cutting efficiency. A shift of the market towards high-quality products is also observed, which is associated with the growing demand for high-performance synthetic abrasives. This shift underscores the shift of the industry to value-added solutions that provide better precision, higher tool life, and higher operational consistency in the harsh industrial environment. With advances in ceramic alumina grains and microcrystalline structures, grinding wheels are now being made with increased cutting efficiency, less heat generation and longer working life, and, as such, artificial abrasives have become a necessity in the modern precision manufacturing requirements.

Regional Insights:

- North India

- South India

- East India

- West India

North India represents a significant market for grinding wheels, driven by the concentration of automotive manufacturing hubs, heavy engineering clusters, and large-scale infrastructure projects across states such as Uttar Pradesh, Haryana, Punjab, and Rajasthan. The region’s extensive industrial base generates sustained demand for both conventional and precision grinding solutions.

South India is a major consumption center, anchored by the presence of leading abrasive manufacturers including CUMI in Chennai and Grindwell Norton in Bangalore, alongside thriving automotive, aerospace, and electronics manufacturing sectors across Tamil Nadu, Karnataka, and Telangana.

East India contributes growing demand for grinding wheels, supported by expanding steel production, mining operations, and industrial development in states like West Bengal, Jharkhand, and Odisha. Government-led industrial investment initiatives are accelerating manufacturing capacity expansion in the region.

West India serves as a key market hub, with Maharashtra and Gujarat hosting major automotive, engineering, and construction industry clusters. Mumbai and Pune’s manufacturing corridors and Gujarat’s petrochemical and heavy industry zones drive consistent grinding wheel consumption.

Market Dynamics:

Growth Drivers:

Why is the India Grinding Wheels Market Growing?

Expansion of India’s Manufacturing Sector Under Government Initiatives

India’s manufacturing landscape is expanding steadily, supported by government-led initiatives aimed at strengthening domestic production and enhancing global competitiveness. The local manufacturing policies and sector-based incentives are attracting both local and foreign investments to the industrial infrastructure. This is a good momentum that is carrying over to increased demand for industrial abrasives and grinding solutions in various end-use sectors. The demand for bonded abrasives in industries like metalworking, electrical equipment, and the heavy machine industry is increasing as new production plants are set up and the existing ones are upgraded to enhance their capacity. The use of grinding wheels during these growing manufacturing processes is required to perform precision machining, finishing of components, and preparation of surfaces.

Robust Growth in Automotive and Aerospace Industries

India’s automotive industry, the fourth-largest globally, is a primary driver of grinding wheel demand. Vehicle manufacturing requires extensive use of grinding wheels for engine component finishing, gear grinding, transmission machining, brake rotor surfacing, and precision surface treatment. According to the Society of Indian Automobile Manufacturers, the two-wheeler segment recorded a 9.1% increase in sales during 2024, achieving 19.6 million units. The aerospace sector is similarly driving demand for specialized grinding solutions, with advanced ceramic and hybrid grinding wheels being adopted for turbine blade machining and airframe component finishing. The growing electric vehicle segment is creating additional requirements for specialized grinding of battery components, lightweight alloys, and high-strength materials used in EV drivetrains and motor assemblies.

Large-Scale Infrastructure Development Initiatives

India’s ambitious infrastructure development programs are generating substantial demand for grinding wheels used in construction, steel fabrication, and metal processing applications. The National Infrastructure Pipeline expanded to cover 13,000 projects with a total cost of Rs 185 trillion by March 2025, nearly doubling from 6,800 projects when launched. The Union Budget 2025-26 allocated INR 11.21 lakh crore for infrastructure development, covering highways, railways, ports, industrial corridors, and urban development projects. Major infrastructure and construction projects involve intensive metal cutting, weld edge preparation, surface grinding, and finishing tasks, all of which rely on durable, high-performance grinding wheels. The continued expansion and modernization of transportation networks, including highways and rail systems, are further stimulating demand across the broader construction and industrial supply chain, reinforcing the need for reliable abrasive solutions in heavy engineering and fabrication activities.

Market Restraints:

What Challenges the India Grinding Wheels Market is Facing?

Volatility in Raw Material Prices and Supply Constraints

The grinding wheels industry is confronted by the unstable prices of some of its main raw materials, such as aluminum oxide, silicon carbide, and resin-based bonding agents. The effects of global supply chain disturbances and volatility in commodity prices have a direct effect on the cost of production, causing price strains on manufacturers and profit margins. Some specialty abrasive material, on which the company depends for importation, also places the market at risk of currency effects and uncertainties on trade policies.

Intense Competition from the Unorganized Sector

A substantial portion of India’s grinding wheel market is served by unorganized and small-scale manufacturers offering low-cost products that compete primarily on price rather than quality. These producers often operate with lower overhead costs and minimal regulatory compliance, creating downward pressure on pricing and challenging established manufacturers seeking to maintain quality standards and invest in technological innovation.

High Import Duties and Costs for Premium Abrasive Materials

Elevated import duties on specialty raw materials and advanced abrasive compounds increase production costs for manufacturers seeking to produce high-performance grinding wheels. This cost burden limits the domestic availability of premium super-abrasive products and constrains the ability of smaller manufacturers to offer competitively priced advanced grinding solutions, slowing the overall market transition toward higher-value product segments.

Competitive Landscape:

The India grinding wheels market exhibits a moderately consolidated competitive structure, with established domestic manufacturers and multinational corporations competing across diverse product segments and price points. Market participants are differentiating through investments in research and development, capacity expansion, and the development of application-specific abrasive solutions. Companies are focusing on strengthening distribution networks, enhancing product portfolios with advanced super-abrasive offerings, and forging strategic partnerships to capture emerging demand from automotive, aerospace, and infrastructure sectors. The competitive dynamics are further shaped by the coexistence of an organized segment delivering premium, technology-driven products and an extensive unorganized sector catering to price-sensitive industrial users.

Recent Developments:

- In June 2024, Carborundum Universal Ltd (CUMI), a leading player within the Murugappa Group, announced plans to invest INR 350 crore in FY25 toward establishing two new manufacturing plants in India. The facilities will produce thin wheels and high-purity silicon carbide, with the silicon carbide plant planned for Kerala with a capacity of six tons per month, requiring approximately 18 months for completion.

- In August 2024, Weiler Abrasives introduced its Precision Express program, significantly reducing lead times for custom gear grinding wheels from several months to just days. The initiative aims to address the growing demand for rapid turnaround on precision grinding solutions in automotive and industrial manufacturing applications.

India Grinding wheels Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Straight Wheels, Cylindrical Wheels, Diamond Wheels, Others |

| Materials Covered | Artificial Abrasives, Natural Abrasives |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Grinding Wheels Market Report

The India grinding wheels market size was valued at USD 270.18 Million in 2025.

The India grinding wheels market is expected to grow at a compound annual growth rate of 5.40% from 2026-2034 to reach USD 433.55 Million by 2034.

Straight wheels held the largest market share at 35% in 2025, driven by their versatility, cost-effectiveness, and widespread application across metalworking, automotive component finishing, and general-purpose industrial grinding operations throughout India.

Key factors driving the India grinding wheels market include expanding manufacturing under Make in India and PLI initiatives, robust automotive and aerospace sector growth, large-scale infrastructure development, and rising adoption of advanced super-abrasive technologies.

Major challenges include raw material price volatility and supply chain disruptions, intense competition from unorganized manufacturers, high import duties on specialty abrasive materials, and the slow pace of technological adoption among smaller industrial users.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)