India Healthy Snacks Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region, 2026-2034

India Healthy Snacks Market Size, Share, Trends & Forecast (2026-2034)

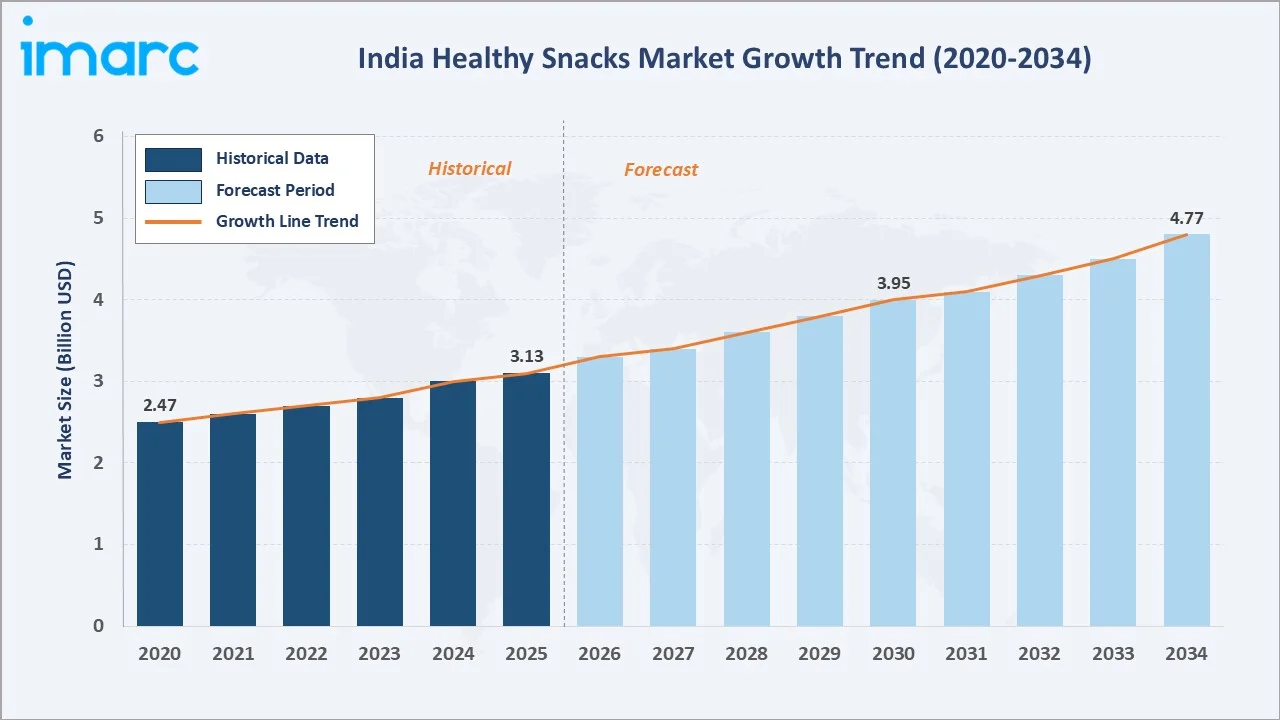

The India healthy snacks market reached USD 3.13 Billion in 2025 and is projected to reach USD 4.77 Billion by 2034, growing at a CAGR of 4.80% during 2026-2034. The market is driven by rising health consciousness, increasing demand for convenient on-the-go foods, and growing preference for low-calorie, high-protein, and natural snack options. A recent Farmley consumer insights study at the Indian Healthy Snacking Summit 2025 surveyed around 6,000 people across age groups. It found that health strongly influences snacking choices, with 72% seeking functional benefits such as energy, mood enhancement, and higher protein. Taste remained critical, as 94% wanted healthy snacks without sacrificing flavor, while 55% preferred natural, preservative-free options, showing that clean-label snacks are becoming mainstream. Nuts, seeds and trail mixes dominate at 34.8%. Supermarkets and hypermarkets lead distribution at 31.6%. North India commands 29.4% of the national market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 3.13 Billion |

| Forecast Market Size (2034) | USD 4.77 Billion |

| CAGR (2026-2034) | 4.80% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Product | Nuts, Seeds and Trail Mixes (34.8% share, 2025) |

| Dominant Distribution Channel | Supermarkets and Hypermarkets (31.6% share, 2025) |

| Leading Region | North India (29.4% share, 2025) |

India's healthy snacks market expanded from USD 2.47 Billion in 2020 to USD 3.13 Billion in 2025, anchored at USD 3.95 Billion in 2030, and forecast to reach USD 4.77 Billion by 2034. India's healthy snack market is defined by the most commercially compelling health motivation. COVID-19's immunity awareness surge created the structural market foundation sustaining the 4.80% CAGR forecast.

To get more information on this market, Request Sample

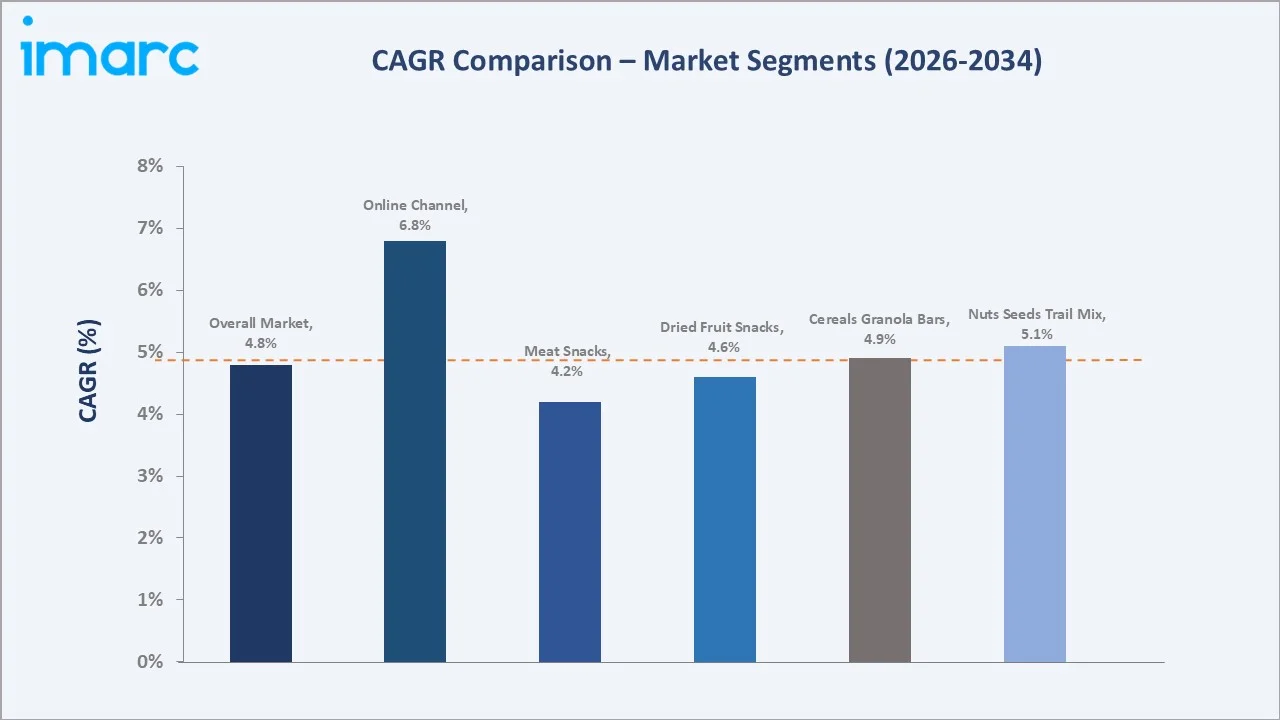

Online channel grows fastest at ~6.8% CAGR through quick commerce, D2C brand subscription boxes, and Amazon India, creating India's most commercially dynamic distribution channel transformation in the food category. Nuts, seeds and trail mixes grow at ~5.1% CAGR through premium California almond and walnut import branding, India-specific trail mix innovation, and seed superfood adoption by India's growing functional health snack consumer.

Executive Summary

India healthy snacks market reached USD 3.13 Billion in 2025, representing one of the most commercially dynamic national healthy snack markets, with India's consumers having the highest lifestyle disease burden, creating unprecedented health motivation, a rapidly growing middle class with disposable income for premium-priced healthy products, and the most disruptive D2C food brand ecosystem. Healthy snacks in India encompass food products marketed primarily on health and nutrition credentials, reduced calorie, high protein, high fiber, low fat, organic, natural ingredients, clean label, or functional health benefit claims, distinguishing the category from conventional snacks where taste, price, and convenience alone drive purchase. The market is projected to reach USD 4.77 Billion by 2034.

Nuts, seeds and trail mixes at 34.8% lead through India's deep cultural familiarity with dry fruits and nuts as premium healthy foods. Supermarkets and hypermarkets lead distribution at 31.6%. North India leads regionally at 29.4%.

Key Market Insights

| Insight Category | Data |

|---|---|

| Dominant Product | Nuts, Seeds and Trail Mixes – 34.8% market share (2025) |

| Dominant Distribution Channel | Supermarkets and Hypermarkets – 31.6% market share (2025) |

| Leading Region | North India – 29.4% market share (2025) |

| Market Opportunity | Clean-label and organic product premiumization, online D2C subscription snack boxes, corporate wellness snack procurement, plant-protein and millet-based snack development, and quick-commerce healthy snack delivery in metro cities. |

Key Analytical Observations Supporting The Above Data:

- Nuts, Seeds and Trail Mixes at 34.8%: The nuts, seeds, and trail mixes dominate due to their high protein, fiber, and nutrient content, making them popular among health-conscious consumers. Their convenience, clean-label appeal, and suitability for on-the-go snacking further support demand.

- Supermarkets and Hypermarkets at 31.6%: Supermarkets and hypermarkets dominate due to their wide product variety, trusted shopping environment, and strong visibility for branded healthy snack products. Discounts, in-store promotions, and easy product comparison further drive consumer purchases.

- North India at 29.4%: North India dominates regionally due to high urbanization, rising disposable incomes, and strong demand for packaged nutritious snacks in cities such as Delhi-NCR, Chandigarh, Jaipur, and Lucknow. Growing fitness awareness and modern retail penetration further support regional sales.

India Healthy Snacks Market Overview

India healthy snacks market operates as one of the most commercially contested national food categories, where multinational FMCG giants, traditional Indian FMCG companies, and a rapidly growing cohort of VC-funded D2C health food startups compete for India's urban health-conscious consumer wallet share.

The healthy snack ecosystem integrates agricultural raw material supply, processing and manufacturing, brand development, multi-channel distribution, and a regulatory environment. Macroeconomic factors include rising disposable incomes, rapid urbanization, expanding middle-class households, and higher spending on packaged foods.

Market Dynamics

To evaluate market opportunities, Request Sample

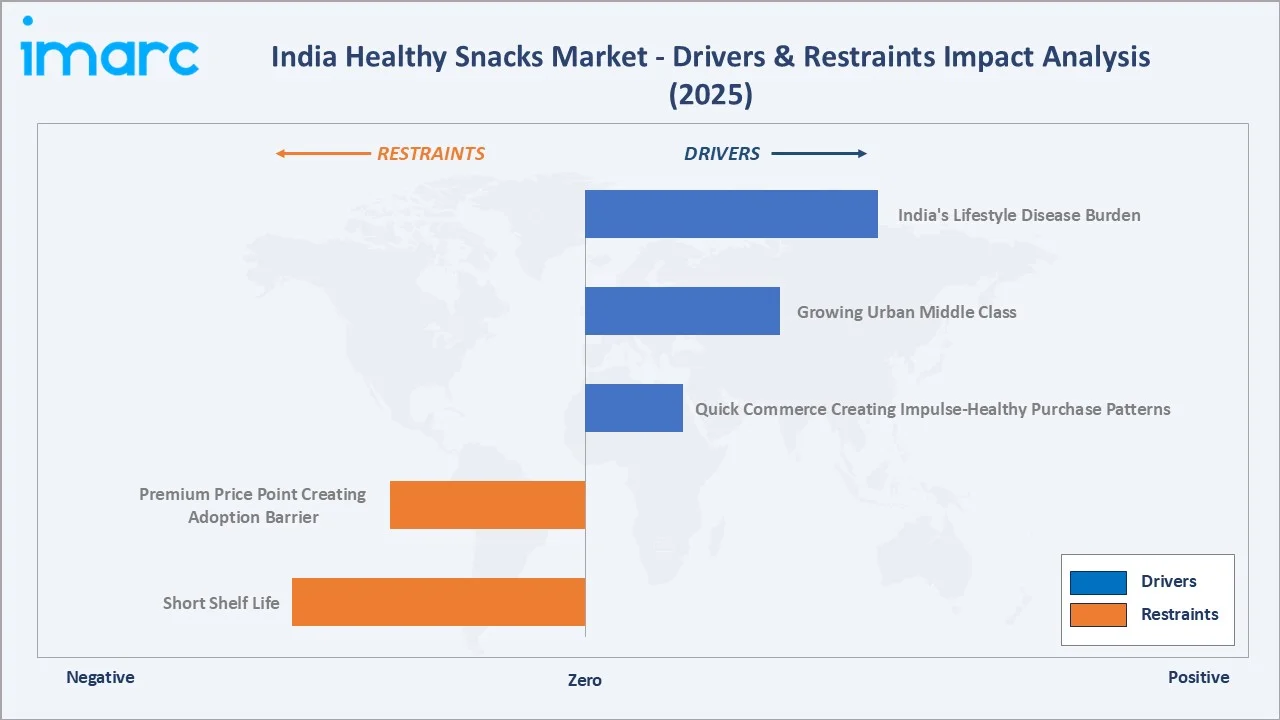

Market Drivers

- India's Lifestyle Disease Burden: India’s rising lifestyle disease burden is increasing the demand for healthy snacks as consumers are becoming more cautious about obesity, diabetes, cholesterol, and heart-related risks. In India, nearly 60% of tests were conducted among individuals aged 31–60 years, who showed higher cholesterol and triglyceride abnormalities. The younger population was also at risk, with over one-third of those aged 19–30 having low HDL levels and nearly 17% showing borderline high cholesterol. This is encouraging a shift from fried and sugar-heavy snacks to healthier options with protein, fiber, nuts, seeds, and natural ingredients. Urban consumers are increasingly choosing snacks that support weight management, energy, and overall wellness. As a result, demand for low-calorie, clean-label, and functional snacks is growing across India.

- Growing Urban Middle Class: By 2036, India’s middle-class and affluent consumers are expected to contribute 93% of total spending, compared to 80% in 2026. By 2035, more than 20% of consumers across major generations, including baby boomers, Gen X, millennials, and Gen Z, are projected to spend USD 45 or more per day. This supports the healthy snacks market by expanding the base of consumers willing to pay for premium, nutritious, and convenient packaged snacks. Rising spending capacity among urban middle-class households is boosting demand for protein bars, nuts, seeds, trail mixes, baked snacks, and clean-label products.

- Quick Commerce Creating Impulse-Healthy Purchase Patterns: Quick commerce is driving the market by making nutritious options easily available for instant purchase. Platforms offering 10–30 minute delivery encourage impulse buying of protein bars, roasted snacks, nuts, seeds, and low-calorie products. Easy app discovery, discounts, and curated health sections also increase consumer trials. This is helping healthy snacks become part of everyday convenience consumption.

Market Restraints

- Premium Price Point Creating Adoption Barrier: The premium price point of many healthy snacks limits affordability for price-sensitive consumers. Products such as protein bars, trail mixes, and imported health snacks often cost significantly more than traditional packaged snacks. This discourages frequent purchases, particularly among lower-income and rural households. As a result, healthy snacks remain concentrated among urban and higher-income consumer segments, restricting wider market penetration.

- Short Shelf Life: Short shelf life is hampering the market, as many products are made with natural ingredients and contain fewer artificial preservatives. This increases the risk of spoilage and limits the duration for which products can remain fresh on retail shelves. Manufacturers often face higher inventory management and distribution costs to maintain product quality. The challenge is particularly significant in regions with complex logistics networks and longer supply chains, restricting market expansion.

Market Opportunities

- Corporate Wellness and Institutional Snack Procurement: Corporate wellness and institutional snack procurement present a significant opportunity as companies increasingly promote employee health and well-being. Organizations are replacing traditional high-calorie snacks in offices with healthier alternatives such as nuts, seeds, protein bars, and low-sugar snacks. Growing adoption of workplace wellness programs and healthy cafeteria offerings is boosting bulk purchases. Educational institutions, hospitals, and corporate offices are also creating new demand channels for nutritious snack products.

- Clinical Nutrition Healthy Snack Positioning: Clinical nutrition healthy snack positioning is creating opportunities as consumers increasingly seek food products that support specific health needs, such as diabetes management, weight control, heart health, and protein supplementation. Brands are developing functional snacks fortified with protein, fiber, vitamins, and minerals to cater to health-conscious consumers. Growing awareness of preventive healthcare and personalized nutrition is further driving demand. This trend is also expanding opportunities in pharmacies, hospitals, and wellness-focused retail channels.

Market Challenges

- High Competition from Traditional Snacks: High competition from traditional snacks is a major challenge, as consumers continue to prefer familiar snacks. These products are widely available, affordable, and deeply embedded in Indian eating habits. Many traditional snacks are also perceived as more flavorful and satisfying than healthier alternatives. As a result, healthy snack brands face difficulties in changing consumer preferences and driving regular consumption.

- Taste Compromise Perception Among Consumers: Taste compromise perception challenges the market, as many consumers believe healthier snacks are less tasty than regular chips, namkeen, biscuits, and fried snacks. This reduces trial and repeat purchases, especially among taste-driven consumers. Since snacking is often linked with indulgence, brands must balance nutrition with flavor. Failure to deliver a familiar taste and texture can limit wider adoption.

Emerging Market Trends

1. Millet Revolution Creating an India-Origin Premium Healthy Snack Identity

The millet revolution is emerging as consumers increasingly recognize millets for their nutritional benefits, including high fiber, protein, and mineral content. Supported by government initiatives and growing awareness of traditional superfoods, brands are launching millet-based chips, crackers, puffs, and snack bars. In January 2026, WellBe Foods launched a new range of millet-based snacks to make traditional Indian snacks healthier and more accessible. The portfolio includes Millet Nippatu, Millet Kodbale, Millet Chakli, Millet Tengolu, and Millet Chivda, combining familiar Indian flavors with the nutritional benefits of millets while supporting the brand’s “No Nasties Ever” positioning. These products combine health benefits with India's agricultural heritage. As a result, millets are helping create a distinct India-origin premium healthy snack identity in both domestic and international markets.

2. Functional Healthy Snacks Creating Premium Market Above Basic Nutrition Claims

Functional healthy snacks are emerging as consumers seek benefits beyond basic nutrition. Brands are introducing products enriched with protein, probiotics, fiber, vitamins, adaptogens, and immunity-boosting ingredients to support specific health goals. These value-added offerings command premium pricing and appeal to fitness-focused and wellness-conscious consumers. As a result, the market is shifting from simple healthy snacking to targeted functional nutrition solutions.

3. Clean Label and Organic Certification Creating Premium Market Stratification

Clean label and organic certification are creating premium market stratification as consumers increasingly prefer snacks with natural ingredients, fewer additives, and transparent labeling. Certified organic, preservative-free, non-GMO, and gluten-free products are positioned as higher-value offerings. These claims help brands differentiate themselves from mass-market snacks. As a result, the healthy snacks market is developing distinct premium tiers based on trust, quality, and ingredient transparency.

4. Plant Protein Snack Revolution Creating a New Category

Plant protein snacks are emerging as a new category in India as consumers seek protein-rich, vegetarian, and fitness-oriented snacking options. Brands are using ingredients such as soy, peas, chickpeas, lentils, nuts, and seeds to develop protein bars, chips, puffs, and trail mixes. This trend supports demand from gym-goers, working professionals, and health-conscious consumers. As a result, plant-based protein snacks are creating a premium and differentiated segment within the healthy snacks market.

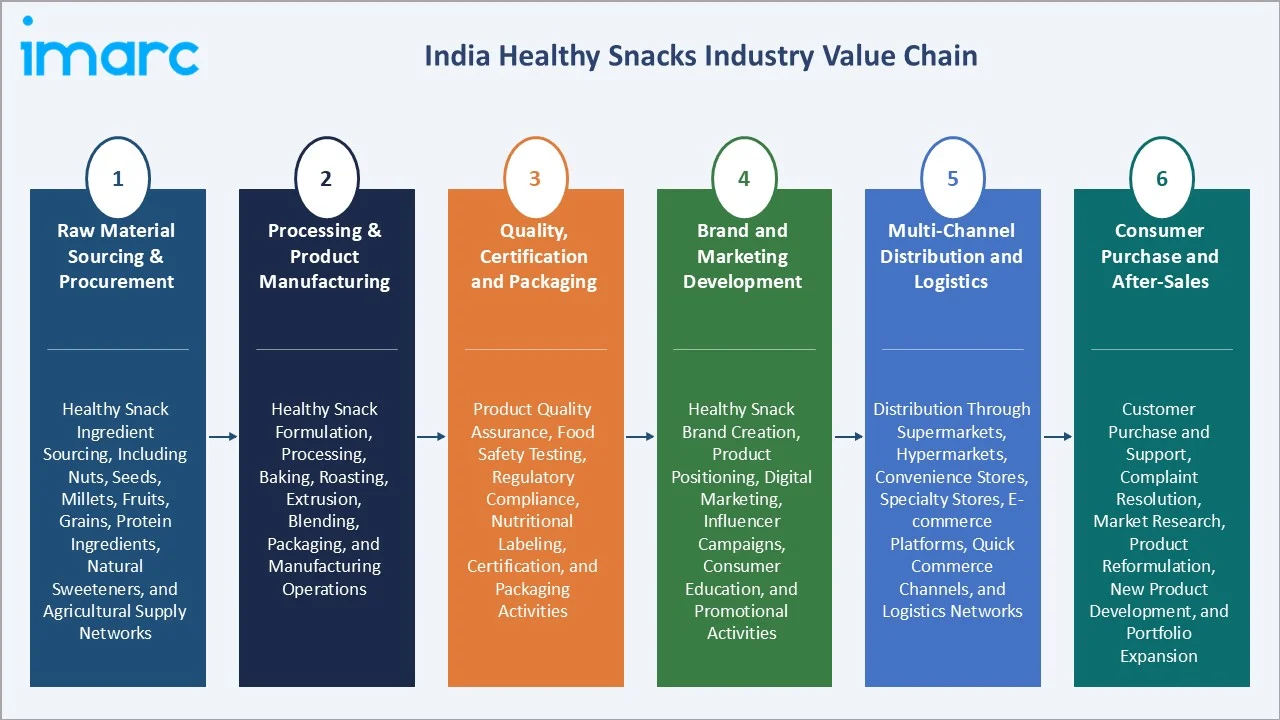

Industry Value Chain Analysis

India's healthy snack value chain encompasses global agricultural raw material procurement, processing and manufacturing, quality and regulatory certification, brand and marketing development, multi-channel distribution, and post-purchase consumer engagement.

| Stage | Key Participants |

|---|---|

| Quality, Certification & Packaging | Product quality assurance, food safety testing, regulatory compliance, nutritional labeling, certification, and packaging activities. |

| Brand & Marketing Development | Healthy snack brand creation, product positioning, digital marketing, influencer campaigns, consumer education, and promotional activities. |

| Multi-Channel Distribution & Logistics | Distribution through supermarkets, hypermarkets, convenience stores, specialty stores, e-commerce platforms, quick commerce channels, and logistics networks. |

| Consumer Purchase & After-Sales | Customer purchase and support, complaint resolution, market research, product reformulation, new product development, and portfolio expansion. |

The brand development and digital marketing stage is India's healthy snack value chain's most commercially intensive phase. The quick commerce distribution stage is the value chain's fastest-evolving commercial phase, with dark store networks requiring brands to manage dark store inventory, quick commerce category management, and impulse-healthy purchase shelf placement above conventional e-commerce planning.

Technology Landscape in the India Healthy Snacks Industry

Clean Processing and Natural Preservation Technology

Clean processing and natural preservation technology enable manufacturers to produce snacks with minimal additives, artificial colors, and preservatives. Techniques such as baking, roasting, freeze-drying, and vacuum drying help retain nutritional value while extending shelf life. Natural preservatives derived from plant-based ingredients are also gaining popularity to support clean-label claims. In April 2026, Good Goodies launched with a packaging-focused transparency strategy that highlights ingredients clearly on the front of the pack. The company introduced this at a time when Indian consumers are paying closer attention to food labels, ingredient lists, and nutrition details, increasing demand for more transparent and easy-to-assess snack products. These technologies align with growing consumer demand for healthier, minimally processed, and transparent food products.

Digital Commerce and Personalized Nutrition Technology

Digital commerce and personalized nutrition technology enable brands to offer targeted product recommendations based on consumer preferences, dietary goals, and health needs. AI-driven analytics and online platforms help companies understand purchasing behavior and customize product offerings. E-commerce and quick commerce channels also improve product accessibility and consumer engagement. These technologies are supporting the growth of premium, functional, and personalized healthy snack segments.

Freeze-Drying and Dehydration Technology

Freeze-drying and dehydration technology extend product shelf life while preserving nutrients, flavor, texture, and color. These technologies are widely used in fruit snacks, vegetable chips, protein-rich ingredients, and functional snack products. They help reduce the need for artificial preservatives, supporting clean-label and natural product positioning. As demand for convenient and minimally processed snacks grows, manufacturers are increasingly adopting these technologies to enhance product quality and market appeal.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Nuts, Seeds and Trail Mixes |

34.8% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

31.6% |

2025 |

|

Region |

North India |

29.4% |

2025 |

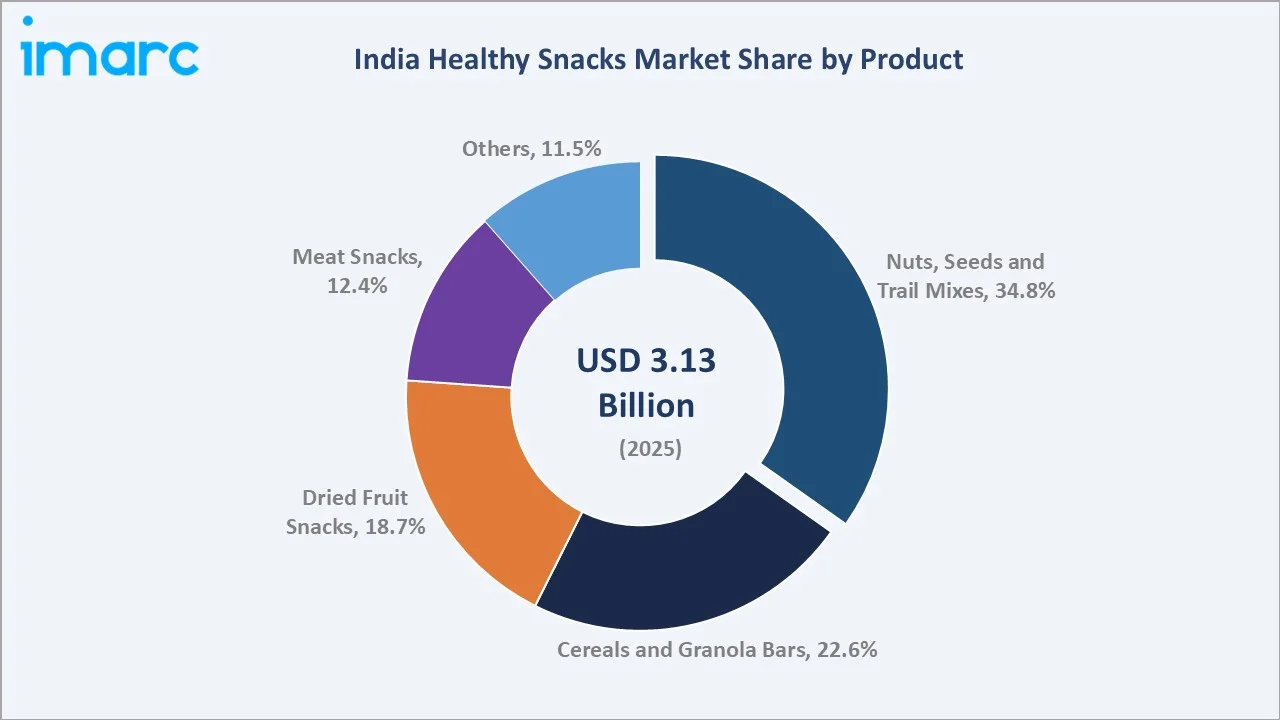

By Product

Nuts, seeds and trail mixes lead at 34.8% (2025). The segment encompasses bulk commodity dry fruit purchase through branded premium packaged nuts, seeds (pumpkin, sunflower, flax, chia), and curated trail mix combinations, creating India's most commercially diverse healthy snack sub-segment by product format and price range.

To access detailed market analysis, Request Sample

Cereals and granola bars at 22.6% represent the breakfast-occasion healthy snack crossover with oats, yoga bar, and protein bar sub-segments growing at ~4.9% CAGR through India's fitness culture and breakfast-on-the-go adoption. Dried fruit snacks at 18.7% reflect traditional consumption habit modernization through branded premium packaging. Meat snacks at 12.4% serve India's protein-seeking non-vegetarian health consumer. Others at 11.5% encompass roasted chickpeas, baked chips, and functional snack innovations growth.

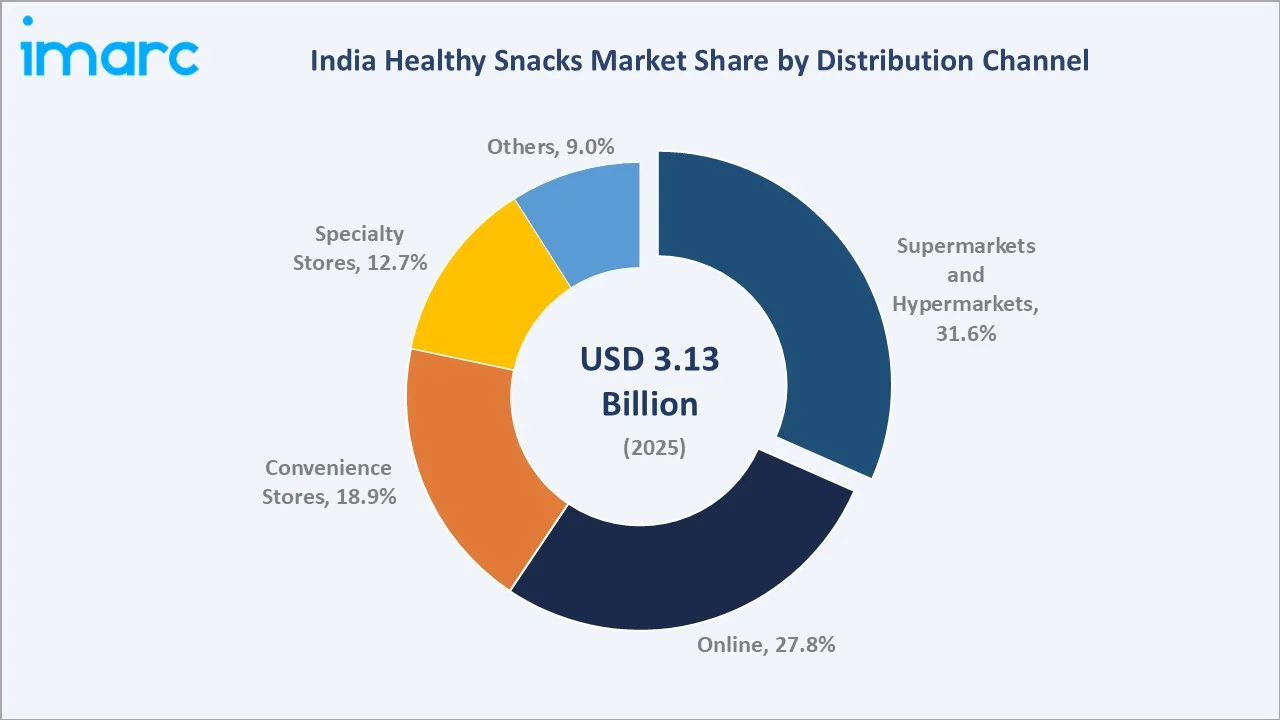

By Distribution Channel

Supermarkets and hypermarkets lead at 31.6% (2025) through D-Mart, Reliance Smart, and premium chains, creating the optimal healthy snack purchase environment. Online at 27.8% grows fastest at ~6.8% CAGR through Amazon, Flipkart, quick commerce Blinkit, Instamart, and D2C brand direct websites.

Convenience stores at 18.9% represent the neighbourhood kirana and petrol station retail, progressively adding premium healthy snack SKUs. Specialty stores at 12.7% encompass organic retail, health food chains, and premium grocery providing the highest per-SKU healthy snack variety per outlet in India's retail landscape. Others at 9.0% include corporate procurement, institutional food service, and direct farm-to-consumer platforms representing India's emerging B2B healthy snack distribution channel.

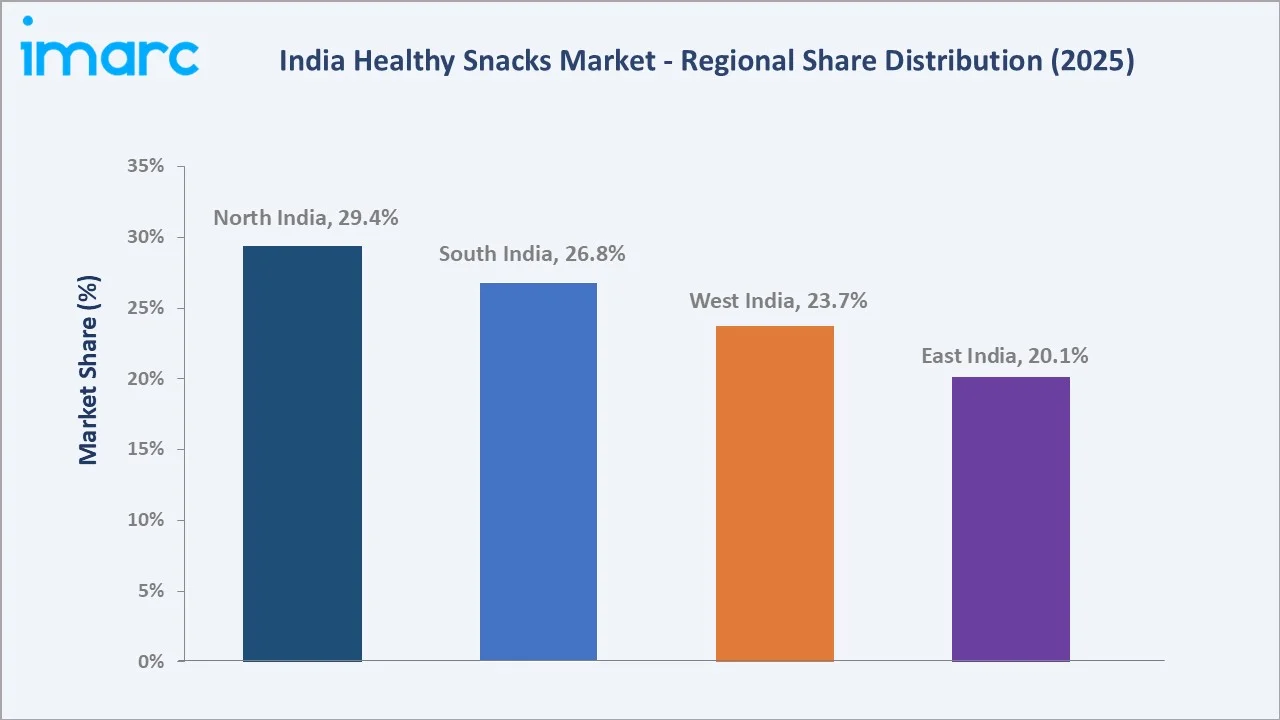

Regional Market Insights

| Geography | Share | Key Market Drivers & Characteristics |

|---|---|---|

| North India | 29.4% | Driven by urbanization, rising disposable incomes, growing fitness awareness, and strong demand for nutritious on-the-go snack options. |

| South India | 26.8% | Driven by increasing health awareness, higher spending on premium food products, and strong adoption of clean-label and functional snacks. |

| West India | 23.7% | Supported by affluent urban populations, a strong presence of modern retail formats, and growing demand for protein-rich and convenience-oriented snack products. |

| East India | 20.1% | Driven by increasing urbanization, improving consumer purchasing power, and rising awareness of healthy eating habits. |

North India's 29.4% market leadership reflects Delhi-NCR's combination of India's highest per-capita income, the most advanced quick commerce infrastructure, and North India's corporate wellness culture, creating institutional procurement above domestic retail. South India's 26.8% reflects Bengaluru's D2C brand innovation hub, creating India's most commercially sophisticated healthy snack supply ecosystem.

West India's 23.7% reflects Maharashtra and Gujarat's premium food retail infrastructure and Gujarat's culturally health-aligned vegetarian consumer base, creating natural healthy snack adoption above the national average. East India's 20.1% is growing at above-national CAGR from a lower penetration base, as Kolkata's food-sophisticated professional class, Odisha's IT city growth, and Northeast India's indigenous organic ingredient awareness create above-background first-time buyer market entry.

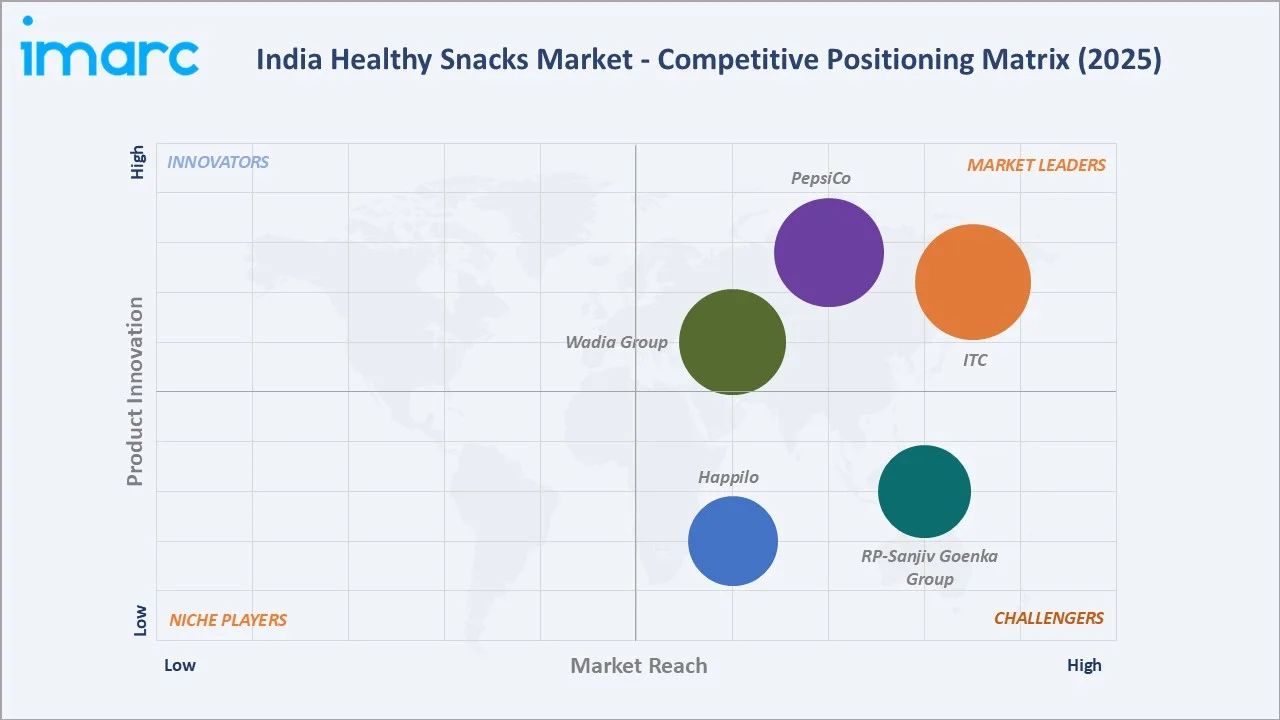

Competitive Landscape

India's healthy snack market competitive landscape is the most commercially dynamic in India's FMCG sector, simultaneously experiencing D2C disruption, multinational defensive investment, traditional FMCG incumbents' health pivot, and new-entrant innovation. This four-way competitive dynamic creates the most commercially fertile new product innovation cycle in India's FMCG history.

| Company Name | Key Brands | Market Position | Core Strength |

|---|---|---|---|

| ITC | Sunfeast Farmlite | Market Leader | Rapidly expanding its role in India's healthy snacks market through protein-rich, millet-based, and better-for-you food products. |

| PepsiCo | Quaker | Market Leader | Transforming its portfolio toward healthier options by reducing sodium, saturated fats, and added sugars. |

| Wadia Group | Britannia | Market Leader | Through Britannia Industries, a dominant force in India's health-conscious food segment with a strong nutrition-focused portfolio. |

| RP-Sanjiv Goenka Group | Evita, Too Yumm! | Strong Challenger | Significant player in healthy snacking through Guiltfree Industries and the Too Yumm! brand. |

| Happilo | Happilo | Strong Challenger | Driving consumer adoption of premium, hygienic, packaged dry fruits and healthy snacks. |

Companies are increasingly focusing on millet-based snacks, protein-rich products, natural ingredients, and omnichannel distribution strategies to strengthen their market presence and capture health-conscious consumers.

Key Company Profiles

ITC

ITC is a leading player in the India healthy snacks market through brands such as Sunfeast Farmlite and select products under its broader foods portfolio. The company offers a range of health-oriented snacks, including digestive biscuits, multigrain products, millet-based offerings, and fiber-rich snacks, catering to the growing demand for nutritious and convenient food options.

- Key Brands: Sunfeast Farmlite.

- Recent Developments: In April 2026, ITC Sunfeast Farmlite launched an all-new sugar-free cookies range. This launch aligns with the larger vision of ITC's ‘Help India Eat Better’.

- Strategic Focus: Expanding its portfolio of health-oriented and clean-label products, including millet-based, multigrain, fiber-rich, and functional snacks, while leveraging its strong distribution network and investing in product innovation to meet the growing demand for nutritious snacking options.

PepsiCo

PepsiCo is a prominent participant in the India healthy snacks market through its nutrition-focused snack portfolio, including products made from oats, whole grains, and healthier ingredient formulations. The company leverages its strong brand presence, extensive distribution network, and innovation capabilities to address the growing demand for better-for-you snacks among health-conscious consumers.

- Key Brands: Quaker.

- Strategic Focus: Expanding its portfolio of protein-rich, whole-grain, baked, and clean-label snacks, while leveraging product innovation, health-oriented formulations, and its extensive distribution network to meet the growing demand for healthy snacking options.

Market Concentration Analysis

India healthy snacks market is moderately concentrated at the mass-market tier and highly fragmented at the premium tier. M&A dynamics are reshaping market concentration. Amazon India's increasing private-label healthy snack investment creates vertical integration pressure from the distribution channel that reduces independent D2C brand margin and market access, a competitive dynamic that brands must address through differentiation above commodity-equivalent private label alternatives.

Investment & Growth Opportunities

Highest Growth Segments

Online distribution channel (~6.8% CAGR through quick commerce and D2C subscription), premium nuts and trail mix branded segment (~6-8% CAGR through brand premiumization), functional healthy snacks (~15-20% CAGR from small base through clinical nutrition positioning), millet-based snacks (~25-30% CAGR from small base), plant protein snacks (~20% CAGR from minimal base through fitness protein awareness), and corporate B2B healthy snack procurement (~18% CAGR from near-zero 2022 base) represent India's highest-growth healthy snack investment vectors through 2034.

Emerging Investment Opportunities

India's below-10% healthy snack market penetration in Tier-2 and Tier-3 cities represents the healthy snack category's most commercially significant structural expansion opportunity. The Tier-2 Indian cities with above-INR 3 lakh annual household income, representing 150+ million urban households, are potential healthy snack buyers if distribution, price, and awareness barriers are addressed through regional distribution investment and affordable healthy snack product development.

Investment Themes

- Clinical nutrition healthy snack co-development for India's diabetes patient medically motivated addressable market: Partnering with Indian diabetes hospital networks to co-develop and receive clinical endorsement for diabetic-appropriate snack products creates B2B clinical distribution, supplementing conventional retail with medically qualified consumer purchase intent.

- Quick commerce dark store specialized healthy snack portfolio creating impulse-healthy purchase at scale: Developing a quick commerce-first healthy snack brand or portfolio specifically designed for dark store rapid delivery economics creates the most commercially differentiated quick commerce healthy snack proposition above brands offering quick commerce as an additional channel to primary retail strategy.

Future Market Outlook (2026-2034)

India healthy snacks market is projected to grow from USD 3.13 Billion in 2025 to USD 4.77 Billion by 2034, delivering a 4.80% CAGR over the forecast period. The market's anchor value of USD 3.95 Billion in 2030 represents India's healthy snack industry at a critical commercial maturation point. Premium healthy snacks will have crossed from 'niche urban health food' to 'mainstream middle-class food category' as Tier-1 city household penetration approaches, quick commerce establishes impulse-healthy purchase patterns sustaining above-income demand growth, and the millet revolution creates an India-specific healthy snack identity above Western health food import category positioning.

Three structural forces define India's healthy snack market growth through 2034 with confidence. India's lifestyle disease demographic megatrend creates a permanently expanding medical motivation for healthy eating behaviour change, driving healthy snack demand independent of discretionary income cycles. The D2C and quick commerce distribution revolution creates geographic and occasion-based healthy snack access, removing the primary distribution barriers currently limiting adoption to modern trade physical retail geographies. India's millet cultural renaissance.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including Chief Executive Officers; Marketing Directors; Brand Managers; Technical experts for nutrition labeling and front-of-pack labeling policy; quick commerce category managers; and consumer survey data from 800 Indian healthy snack consumers across Delhi-NCR, Mumbai, Bengaluru, Hyderabad, Kolkata, and Tier-2 city consumers.

Secondary Research

Secondary research encompassed India health and wellness food market report; Young India wellness economy report; India food delivery and quick commerce data; IDF Diabetes Atlas India data; company annual reports; Amazon India healthy snack bestseller category data; India non-communicable disease report. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using the category adoption model: India urban household base multiplied by healthy snack purchase frequency multiplied by average healthy snack purchase value per occasion. Online channel modelled separately using quick commerce and D2C subscription growth rates. Commercial B2B segment modelled using corporate office count growth multiplied by estimated healthy snack allocation per employee per year.

India Healthy Snacks Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Nuts, Seeds, and Trail Mixes, Dried Fruit Snacks, Cereals and Granola Bars, Meat Snacks, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | ITC, PepsiCo, Wadia Group, RP-Sanjiv Goenka Group, Happilo, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India healthy snacks market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India healthy snacks market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India healthy snacks industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Healthy Snacks Market Report

India's healthy snacks market reached USD 3.13 Billion in 2025, driven by rising health consciousness, increasing prevalence of lifestyle diseases, and growing demand for nutritious, convenient, and on-the-go food options. Rising disposable incomes, urbanization, and expanding availability through modern retail and e-commerce channels are further supporting market growth.

India's healthy snacks market grows at 4.80% CAGR during 2026-2034, reaching USD 4.77 Billion by 2034. The overall growth is sustained by India's lifestyle disease burden, creating medical nutrition motivation and D2C brand innovation, creating premium healthy snack category expansion.

Nuts, seeds and trail mixes lead at 34.8% through India's unique cultural foundation, where dry fruits and nuts carry Ayurvedic health credentials, gifting culture significance, and a premium food quality association that no other snack category matches in India's consumer psychology.

Supermarkets and hypermarkets lead at 31.6% through D-Mart, Reliance Smart, and premium chains, creating the optimal healthy snack purchase environment with health food aisles, product variety, and label reading convenience.

North India leads at 29.4% through Delhi-NCR's combination of India's highest per-capita income, the country's most advanced quick commerce infrastructure, and North India's corporate wellness culture, creating institutional procurement.

Leading companies include ITC, PepsiCo, Wadia Group, RP-Sanjiv Goenka Group, and Happilo, among others.

India's healthy snacks market is projected to reach approximately USD 3.95 Billion by 2030, with the mainstream affordable healthy snack tier reaching commercial scale as competitive brands create price parity with conventional chips, millet-based traditional grain snacks achieving modern trade mainstream distribution, and online quick commerce establishing impulse-healthy purchase patterns.

India's millet-based healthy snack opportunity is the most commercially unique national food category creation opportunity in India's packaged food industry. The millet snack market's most commercially distinctive characteristic is cultural authenticity, Indian consumers recognizing ragi, jowar, and bajra as their grandmother's health grains, creating intergenerational trust that no marketing investment can substitute and that no imported health food brand can claim through any strategy.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)