India Household Cleaners Market Size, Share, Trends and Forecast by Product, Ingredients, Distribution Channel, Income Group, Application, Premiumization, and Region, 2026-2034

India Household Cleaners Market Size, Share, Trends & Forecast (2026-2034)

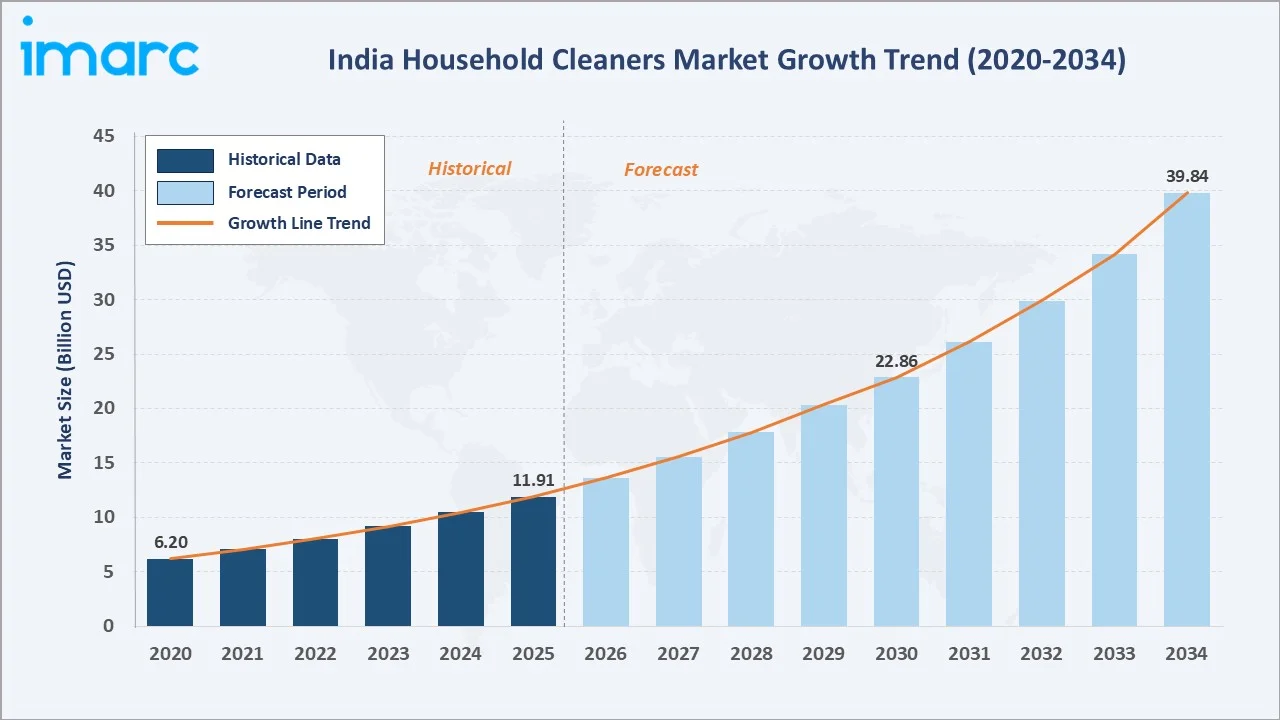

The India household cleaners market reached USD 11.91 Billion in 2025 and is projected to reach USD 39.84 Billion by 2034, growing at a CAGR of 13.93% during 2026-2034. The market is driven by rising hygiene awareness, urbanization, growing middle-class incomes, and increased availability of specialized cleaning formulations.

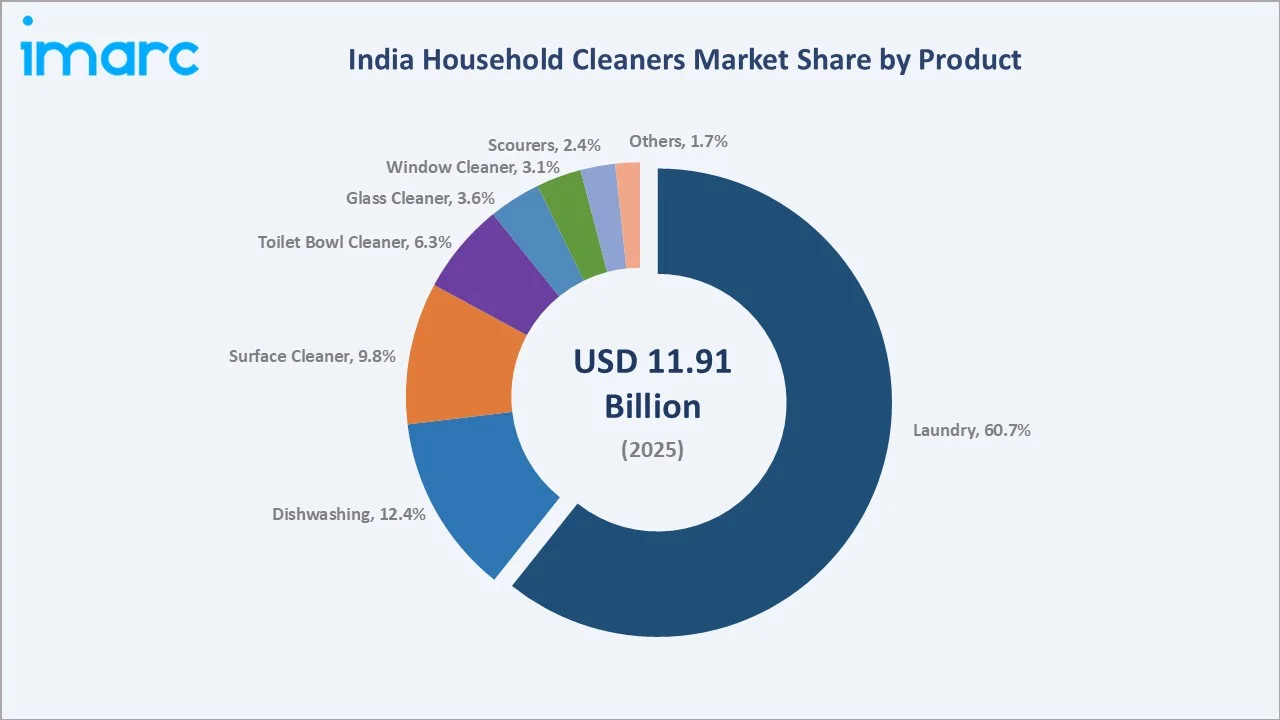

India's rapid urban growth, expanding organized retail, and post-pandemic hygiene consciousness are structurally accelerating demand across laundry, surface, and toilet care categories. Laundry leads at 60.7%, Builders dominates the ingredients segment at 41.8%, and North India commands 45.2% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.91 Billion |

|

Forecast Market Size (2034) |

USD 39.84 Billion |

|

CAGR (2026-2034) |

13.93% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

Laundry (60.7%, 2025) |

|

Dominant Ingredient |

Builders (41.8%, 2025) |

|

Leading Region |

North India (45.2%, 2025) |

The market expanded significantly over the historical period 2020-2025, anchored by consistent demand for detergents and surface cleaners. Rising hygiene standards, nuclear family formations, and premiumization trends are compounding growth through the forecast period to 2034.

To get more information on this market, Request Sample

Laundry grows robustly at approximately 14.8% CAGR as washing machine penetration increases and fabric care premiumization accelerates. Builders’ ingredient segment grows at approximately 13.5% CAGR driven by performance-formulation demand in detergents. North India leads regional growth at 14.2% CAGR through urban consumption expansion.

Executive Summary

The India household cleaners market reached USD 11.91 Billion in 2025, representing one of the fastest-growing FMCG segments driven by hygiene awareness and urban lifestyle transformation. The market is projected to reach USD 39.84 Billion by 2034.

Laundry at 60.7% dominates through daily-use frequency and increasing washing machine adoption. Builders at 41.8% leads in ingredients through indispensable cleaning performance in detergents. North India at 45.2% reflects its dominant urban consumption base and retail infrastructure.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Laundry – 60.7% share (2025) |

|

Dominant Ingredient |

Builders – 41.8% market share (2025) |

|

Leading Region |

North India – 45.2% market share (2025) |

|

Market Opportunity |

Eco-friendly formulations; premium surface cleaners; rural distribution expansion; antimicrobial specialization |

Key Analytical Observations Supporting the Above Data:

- Laundry at 60.7%: The laundry segment dominates as it covers daily household fabric care requirements, including hand-wash and machine-wash detergents, fabric softeners, and stain removers. Widespread washing machine penetration and evolving consumer preferences for specialized fabric-care formulations are sustaining the laundry category's leadership.

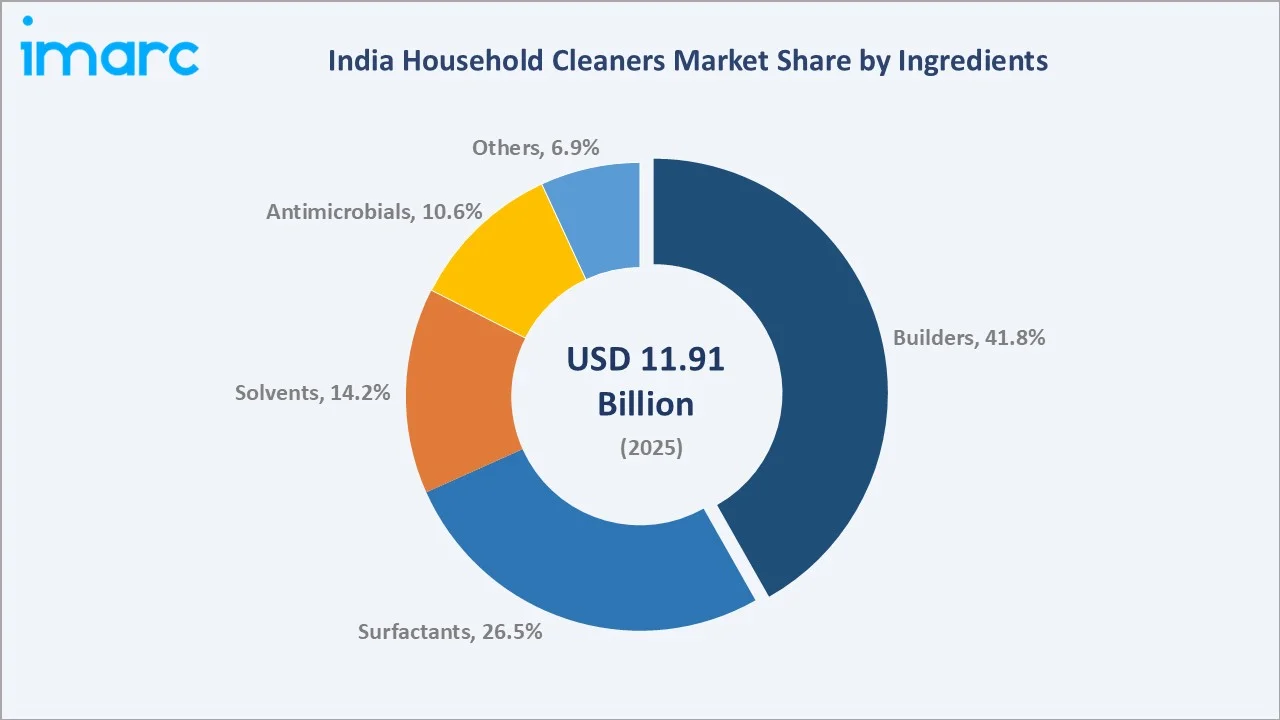

- Builders at 41.8%: Builders dominate the ingredients segment as they are indispensable for enhancing detergent performance by sequestering calcium and magnesium ions, softening water hardness, and improving overall cleaning efficacy. Their extensive use across laundry powders, bar soaps, and dishwashing products makes them the highest-volume functional ingredient.

- North India at 45.2%: North India leads through its high population density, the largest concentration of urban consumption centers, and robust organized retail infrastructure. The region's combination of aspirational middle-class consumers and deep rural distribution networks drives sustained household cleaner demand.

India Household Cleaners Market Overview

The India household cleaners market encompasses the manufacture and distribution of all cleaning products used in residential settings, including laundry detergents, dishwashing products, surface cleaners, toilet bowl cleaners, glass cleaners, window cleaners, scourers, and specialty cleaning solutions.

The ecosystem integrates chemical ingredient suppliers, product manufacturers, contract manufacturers, packaging providers, retail distributors, including supermarkets, kirana stores, and e-commerce platforms, and regulatory bodies governing product safety and labeling standards. Macroeconomic factors include rising disposable incomes, urbanization, changing hygiene habits, and expanding organized retail formats.

Market Dynamics

To evaluate market opportunities, Request Sample

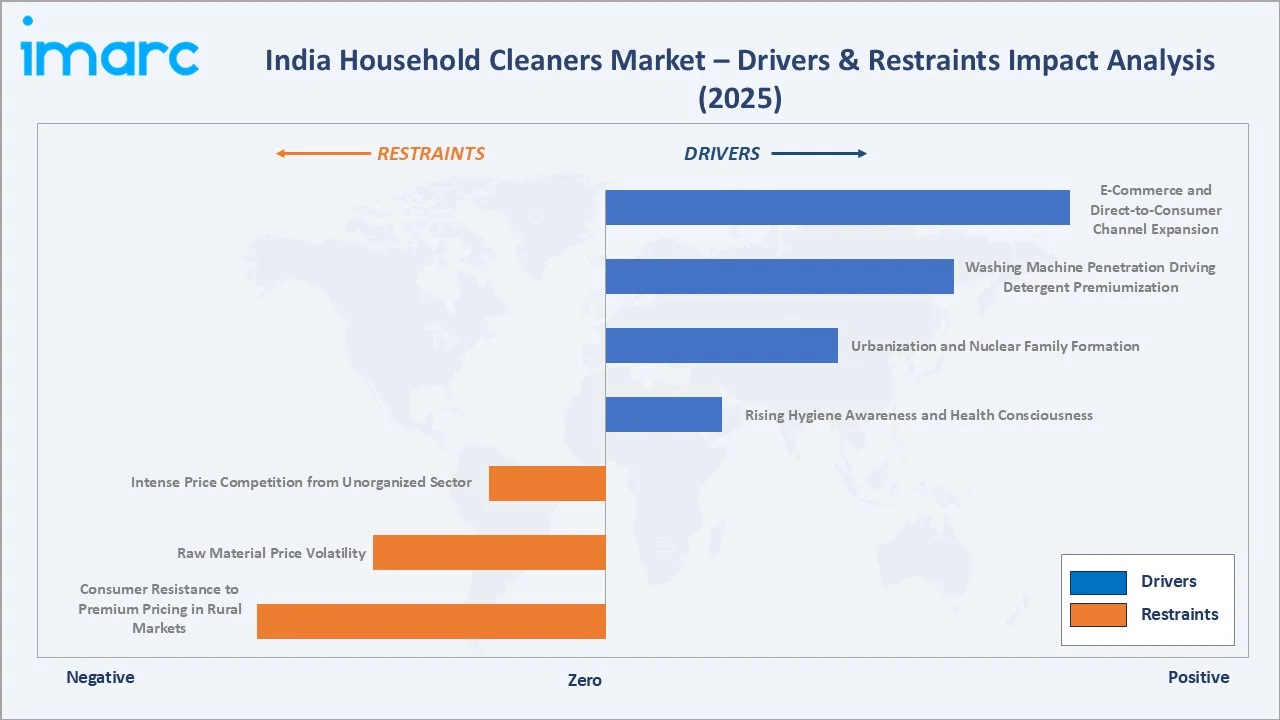

Market Drivers

- Rising Hygiene Awareness and Health Consciousness: Heightened consumer awareness around household hygiene is structurally increasing demand for disinfectant-grade cleaners, surface sanitizers, and antimicrobial formulations. Urban consumers actively seek products with prolonged surface protection and germ-elimination claims, driving volume growth across toilet, surface, and floor cleaner segments.

- Urbanization and Nuclear Family Formation: India's accelerating urbanization and rise of nuclear families are creating sustained demand for branded, ready-to-use household cleaning products. Urban households prioritize convenience, efficacy, and packaging formats, including trigger sprays and concentrated refills, supporting premiumization and volume growth.

- Washing Machine Penetration Driving Detergent Premiumization: Increasing washing machine adoption across urban and semi-urban households is driving demand for machine-compatible liquid detergents and premium fabric-care formulations. This shift from hand-wash powders to liquid detergents and fabric conditioners is accelerating average selling price improvement within the dominant laundry segment.

- E-Commerce and Direct-to-Consumer Channel Expansion: Rapid expansion of e-commerce platforms and quick-commerce delivery networks is improving household cleaner accessibility across Tier-2 and Tier-3 cities. Digital channels enable brands to launch new SKUs, test premium formulations, and reach consumers previously underserved by traditional retail.

Market Restraints

- Intense Price Competition from Unorganized Sector: The market faces persistent pricing pressure from the unorganized sector manufacturing and distributing low-cost cleaning products. This limit branded companies' ability to implement premium pricing strategies in price-sensitive rural and semi-urban markets.

- Raw Material Price Volatility: Manufacturers face significant cost pressures from volatility in petrochemical-derived surfactants, builders, and solvents. Input cost fluctuations impair margin predictability and compress profitability, particularly for mid-size domestic manufacturers with limited hedging capabilities.

- Consumer Resistance to Premium Pricing in Rural Markets: A significant proportion of rural household cleaner consumers remain highly price sensitive, limiting premiumization potential outside urban and semi-urban areas. Low per-unit spending habits and preference for economy-segment products constrain average revenue per household.

Market Opportunities

- Eco-Friendly and Plant-Based Formulation Development: Growing consumer preference for biodegradable, plant-based, and non-toxic cleaning solutions creates significant product innovation opportunity. Brands investing in enzyme-based formulations, recyclable packaging, and natural ingredient integration can capture a rapidly expanding premium eco-conscious consumer segment.

- Rural Market Penetration through Sachets and Affordable SKUs: India's vast rural population represents a largely underpenetrated household cleaner market. Brands introducing affordable sachet formats and regionally adapted product variants can achieve high-volume penetration and long-term brand loyalty in rural markets.

Market Challenges

- Distribution Complexity Across India's Fragmented Retail Landscape: India's retail ecosystem comprising millions of independent kirana stores, wholesale distributors, and emerging modern trade formats presents significant distribution complexity. Maintaining brand standards and consistent availability requires substantial operational investment.

- Counterfeit and Substandard Product Proliferation: The market is susceptible to counterfeit products mimicking established brand packaging, particularly in rural markets. Counterfeits proliferation damages brand equity, erodes consumer trust, and creates product safety risks requiring ongoing anti-counterfeiting investment.

Emerging Market Trends

1. Rise of Eco-Friendly and Plant-Based Cleaning Products

The market is witnessing a rapid consumer shift toward biodegradable, plant-based, and non-toxic cleaning solutions. Natural ingredients, including neem, tulsi, lemon, and eucalyptus, are being blended with enzyme-based solutions and recyclable packaging formats, creating a distinct premium eco-segment with strong urban growth momentum.

2. E-Commerce and Direct-to-Consumer Channel Expansion

Expanding e-commerce and quick-commerce delivery networks are transforming household cleaner distribution. Digital-native brands are leveraging AI-driven personalization, influencer collaborations, and subscription models to capture urban consumers seeking convenience and product variety beyond traditional retail formats.

3. Premiumization and Specialized Product Development

Growing consumer demand for multifunctional and premium household cleaners is accelerating product innovation. Concentrated formulations, water-soluble pods, fragrance-infused products, and 2-in-1 cleaner-disinfectant combinations are gaining market share as consumers seek enhanced performance and emotional value.

4. Antimicrobial and Disinfectant Product Mainstreaming

Sustained post-pandemic hygiene awareness is mainstreaming antimicrobial claims across surface, floor, and toilet cleaners. Products offering prolonged surface protection and broad-spectrum germ elimination are experiencing durable demand expansion beyond seasonal or outbreak-driven purchasing cycles.

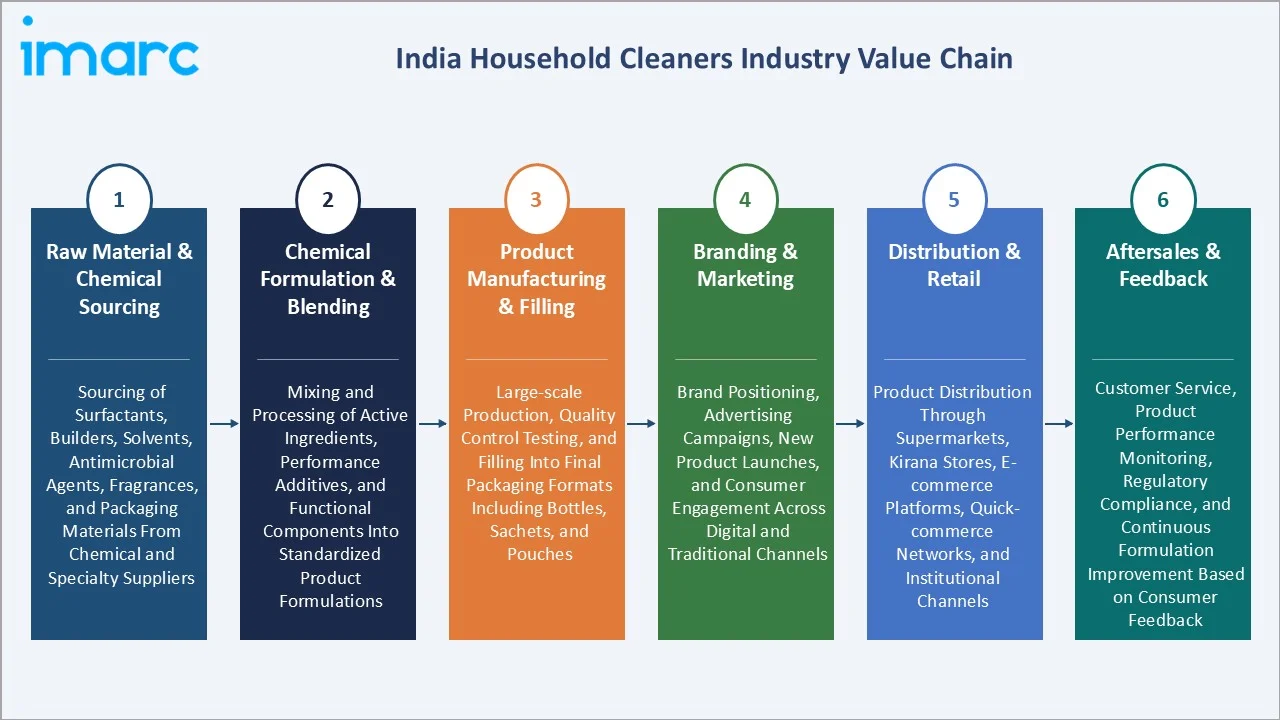

Industry Value Chain Analysis

The India household cleaners value chain integrates chemical raw material procurement, product formulation and manufacturing, quality testing, packaging, and multi-channel distribution to end consumers across organized retail, traditional trade, and digital platforms.

|

Stage |

Key Activities |

|

Raw Material & Chemical Sourcing |

Sourcing of surfactants, builders, solvents, antimicrobial agents, fragrances, and packaging materials from chemical and specialty suppliers |

|

Chemical Formulation & Blending |

Mixing and processing of active ingredients, performance additives, and functional components into standardized product formulations |

|

Product Manufacturing & Filling |

Large-scale production, quality control testing, and filling into final packaging formats including bottles, sachets, and pouches |

|

Branding & Marketing |

Brand positioning, advertising campaigns, new product launches, and consumer engagement across digital and traditional channels |

|

Distribution & Retail |

Product distribution through supermarkets, kirana stores, e-commerce platforms, quick-commerce networks, and institutional channels |

|

Aftersales & Consumer Feedback |

Customer service, product performance monitoring, regulatory compliance, and continuous formulation improvement based on consumer feedback |

The manufacturing and formulation stage holds the highest value creation potential through proprietary technology and performance differentiation. The distribution tier is experiencing rapid transformation as organized trade and e-commerce capture share from traditional kirana-dominated networks.

Technology Landscape in the India Household Cleaners Industry

Enzyme-Based Cleaning Technology

Enzyme-based cleaning technology uses biological catalysts to break down complex organic stains, including proteins, fats, and starches, at lower temperatures. This enables effective cold-water washing performance while reducing energy consumption, supporting sustainability goals, and meeting consumer demand for eco-friendly cleaning formulations.

Concentrated and Solid-Format Formulation Technology

Concentrated liquid detergents and solid cleaning tablets represent the next generation of sustainable household cleaner formats. By reducing water content, these formats minimize packaging requirements, lower transportation costs, and reduce plastic waste, aligning with regulatory and consumer sustainability priorities.

Antimicrobial and Disinfectant Technology

Advanced antimicrobial formulation technology using quaternary ammonium compounds, silver ion technology, and botanical antimicrobials offers prolonged surface protection beyond immediate cleaning. These technologies are increasingly integrated into mainstream floor, surface, and toilet cleaners, expanding beyond specialist disinfectant categories.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Laundry |

60.7% |

2025 |

|

Ingredients |

Builders |

41.8% |

2025 |

|

Distribution Channel |

Supermarkets/Hypermarkets |

60.1% |

2025 |

|

Income Group |

Middle (INR 2.5 lacs- INR 27.5 lacs) |

57.0% |

2025 |

|

Application |

Fabric |

60.7% |

2025 |

|

Premiumization |

Economy |

54.5% |

2025 |

|

Region |

North India |

45.2% |

2025 |

By Product

Laundry leads at 60.7% in 2025, encompassing fabric detergents, washing powders, liquid detergents, fabric softeners, and stain removers. This segment's dominance reflects daily-use frequency, universal household requirement, and the expanding portfolio of machine-wash detergent subcategories driven by appliance penetration.

To access detailed market analysis, Request Sample

Dishwashing at 12.4% captures strong growth from increasing urban kitchen hygiene awareness and dishwasher appliance penetration. Surface cleaners at 9.8% benefit from mainstreaming of regular surface disinfection. Toilet bowl cleaners at 6.3%, glass cleaners at 3.6%, window cleaners at 3.1%, and scourers at 2.4% represent specialized categories with growing adoption.

By Ingredients

Builders lead at 41.8% as the dominant functional ingredient class, essential for enhancing detergent performance by sequestering calcium and magnesium ions that reduce cleaning efficacy. Their extensive usage across laundry detergents, dishwashing bars, and surface cleaners makes them the highest-volume ingredient in the market.

Surfactants at 26.5% are the primary active cleaning agents across all product categories, generating foam and emulsifying oils and soils. Solvents at 14.2% are critical for glass cleaners, degreasers, and multi-surface sprays. Antimicrobials at 10.6% reflect sustained demand for disinfectant-grade formulations across floor, surface, and toilet cleaners.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

North India |

45.2% |

High urban population density, strong consumer spending, established retail infrastructure, and dominant presence of organized trade channels |

|

South India |

21.3% |

Driven by high hygiene awareness, urban middle-class growth, and strong demand for premium surface and toilet care cleaners |

|

West & Central India |

19.6% |

Supported by industrial urbanization, growing mid-income households, and expanding organized retail presence in Maharashtra and Gujarat |

|

East India |

13.9% |

Emerging growth driven by rising per capita income, e-commerce penetration, and increasing hygiene awareness across urban centers |

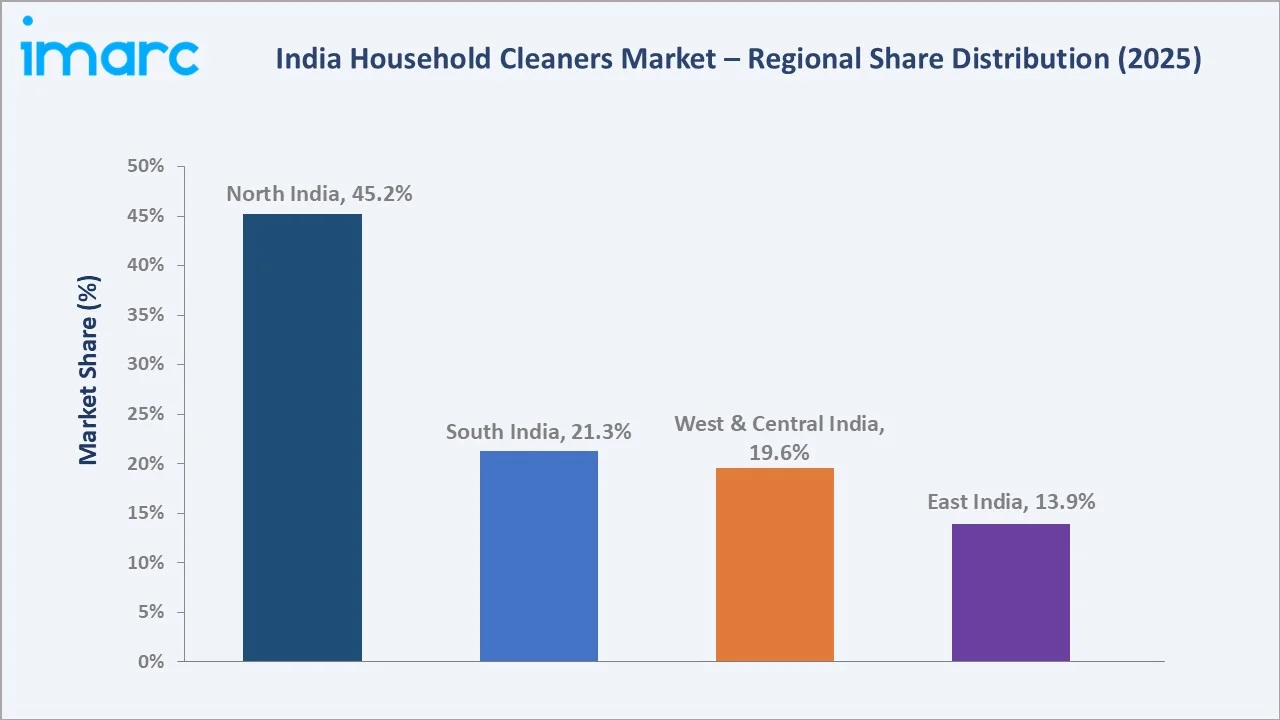

North India, at 45.2%, leads through Delhi-NCR's massive urban consumption base, strong organized retail presence, and established distribution infrastructure supporting both economy and premium household cleaner penetration across all income segments.

South India, at 21.3%, reflects high hygiene consciousness and urban middle-class premiumization. West and Central India, at 19.6%, benefits from industrial urbanization in Maharashtra and Gujarat. East India, at 13.9%, represents an emerging growth region with rising incomes and expanding e-commerce penetration, driving household cleaner adoption.

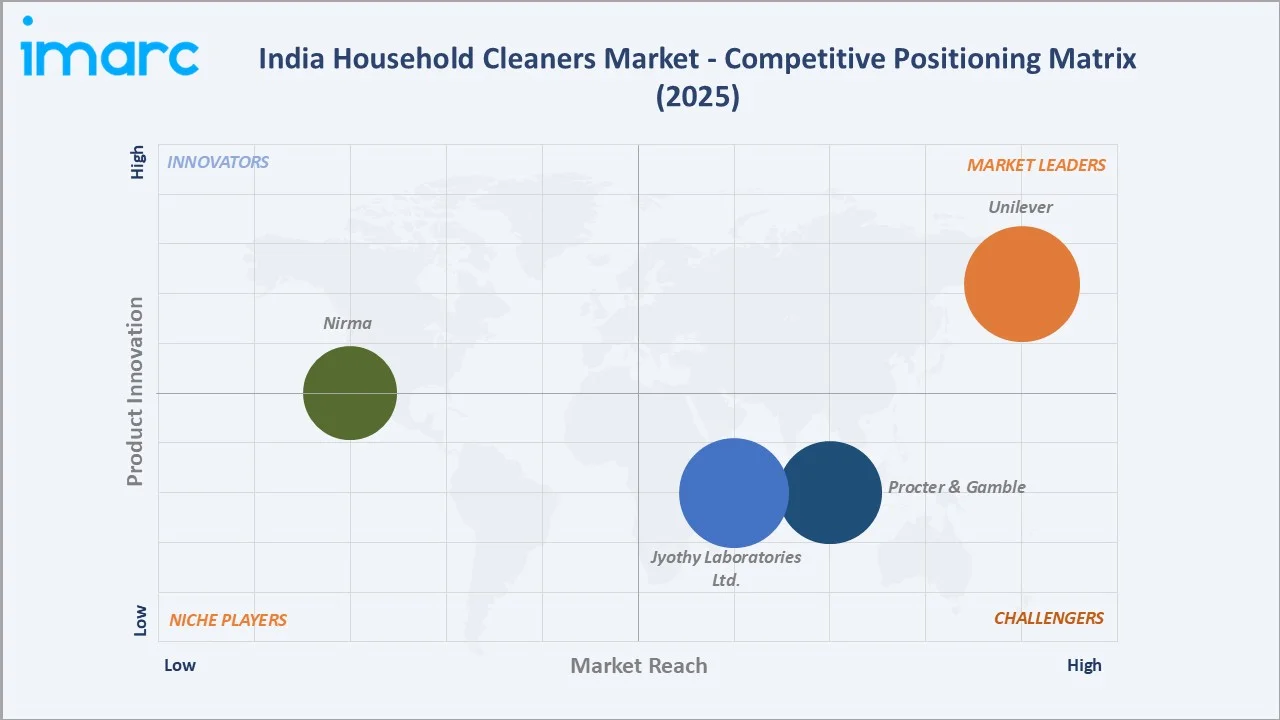

Competitive Landscape

The India household cleaners market competitive landscape is moderately concentrated, led by multinational FMCG corporations alongside strong domestic players. Three competitive tiers exist: global multinational leaders, domestic branded players, and regional or economy-segment manufacturers.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Unilever |

Rin, Surf Excel, Vim, Domex, Comfort, Active Wheel 2 in 1, Cif |

Market Leader |

Leads India's household cleaners market through deep brand equity across laundry and surface care categories. |

|

Procter & Gamble |

Ariel, Tide |

Strong Challenger |

Competes with premium fabric care solutions targeting urban and aspirational consumers. |

|

Jyothy Laboratories Ltd. |

Ujala, Exo, Margo, Henko |

Strong Challenger |

Domestic leader across fabric care and dishwash segments with strong rural penetration. |

|

Nirma |

Nirma |

Regional Player |

Maintains a strong cost-competitive position in the economy detergent and cleaning segments. |

Key players include Unilever, Procter & Gamble, Jyothy Laboratories Ltd., Nirma, and others.

Key Company Profiles

Unilever

Unilever, regionally operating as Hindustan Unilever Limited (HUL), is India's leading household and personal care FMCG company with the broadest household cleaner portfolio spanning laundry, surface care, and dishwashing categories.

- Key Products: Rin, Surf Excel, Vim, Domex, Comfort, Active Wheel 2 in 1, Cif

- Recent Developments: In February 2026, Hindustan Unilever Limited (HUL) invested up toINR 2,000 crore to expand manufacturing capacity across multiple locations in India. The investment strengthens HUL’s presence in fast-growing premium segments within Beauty & Wellbeing, Home Care, including skincare, haircare, and personal care.

- Strategic Focus: Expanding premium and eco-conscious household cleaner formulations while strengthening direct-to-consumer digital channels and sachets-led rural market penetration.

Procter & Gamble

Procter & Gamble is a global FMCG leader operating in India's premium fabric care segment through Ariel and Tide, targeting urban and aspirational consumers.

- Key Products: Ariel, Tide

- Strategic Focus: Driving premiumization in laundry care through superior formulation performance, e-commerce channel investment, and digital marketing targeting urban millennial consumers.

Market Concentration Analysis

The India household cleaners’ market is moderately concentrated at the branded national player level. The top four multinational and domestic players collectively account for approximately 55-65% of the organized branded household cleaners market revenue.

The unorganized sector retains a significant 20-25% share, primarily in rural and semi-urban markets through economy detergents and generic cleaning products. Market concentration is expected to increase modestly through the forecast period as organized players expand rural distribution and e-commerce penetration.

Investment & Growth Opportunities

Highest Growth Segments

Laundry premium segment (~14.8% CAGR), surface disinfectants (~15.5% CAGR), eco-friendly formulations (~20%+ CAGR from a small base), e-commerce channel growth (~22% CAGR), and antimicrobial specialization (~16% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Rural market penetration through affordable sachet formats and direct distribution investment represents India's household cleaners market's highest-volume incremental growth opportunity.

Investment Themes

- Sustainable and Eco-Friendly Formulation Innovation: Consumer demand for plant-based, biodegradable, and low-plastic household cleaners is structurally growing. Investments in enzyme technology, concentrated formats, and sustainable packaging represent high-return opportunities as regulatory and consumer pressure on conventional chemical formulations increases.

- E-Commerce and Quick-Commerce Channel Infrastructure: Building robust direct-to-consumer and quick-commerce distribution capability represents a structural competitive advantage in India's rapidly digitalizing retail landscape, enabling premium product launches, subscription models, and direct consumer relationships beyond traditional trade constraints.

Future Market Outlook (2026-2034)

The India household cleaners market is projected to grow from USD 11.91 Billion in 2025 to USD 39.84 Billion by 2034, delivering a 13.93% CAGR. The market's growth is underpinned by structural urbanization, rising household incomes, and accelerating hygiene awareness across urban and semi-urban India.

Three structural forces define market growth through 2034. Urban household formation creates compounding detergent and surface cleaner demand as India adds millions of new urban households annually. Premiumization of the laundry segment through liquid detergent and fabric softener adoption creates significant average selling price expansion. E-commerce channel penetration enables premium product accessibility across Tier-2 and Tier-3 cities, previously limited to economy-segment branded cleaners.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025), including household cleaner brand managers, key distribution channel executives, surfactant and ingredient suppliers, organized retail buyers, and e-commerce category managers.

Secondary Research

Secondary research encompassed company annual reports, industry association publications, trade data from the Indian FMCG sector, Nielsen retail measurement data, IMARC Group household care market tracking, and regulatory filings. Over 50 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a category-level demand model incorporating urban household formation rates, per-capita spending trends, product premiumization trajectories, and channel-level distribution expansion assumptions across organized trade, traditional trade, and e-commerce.

India Household Cleaners Market Report Scope:

|

Report Features |

Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Laundry, Dishwashing, Surface Cleaner, Toilet Bowl Cleaner, Window Cleaner, Glass Cleaner, Scourers, Others |

| Ingredients Covered | Builders, Solvents, Surfactants, Antimicrobials, Others |

| Distribution Channels Covered | Convenience Stores, Supermarkets and Hypermarkets, Online, Others |

| Income Groups Covered | Middle (INR 2.5 lacs- INR 27.5 lacs), Low (Less than INR 2.5 Lacs), High (Greater than INR 27.5 lacs) |

| Applications Covered | Fabric, Kitchen, Bathroom, Floor, Others |

| Premiumizations Covered | Economy, Mid-Sized, Premium |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Unilever, Procter & Gamble, Jyothy Laboratories Ltd., Nirma, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Household Cleaners Market Report

The India household cleaners market reached USD 11.91 Billion in 2025, driven by the laundry segment dominant at 60.7%, builders as the leading ingredient at 41.8%, and North India commanding 45.2% regional market share through high urban population density, strong retail infrastructure, and the largest concentration of aspirational middle-class consumers.

The India household cleaners market grows at 13.93% CAGR during 2026-2034, reaching USD 39.84 Billion by 2034. Growth reflects urban household formation, washing machine-driven detergent premiumization, e-commerce channel expansion, and rising consumer preference for specialized and eco-friendly formulations.

Laundry leads at 60.7%, capturing daily-use fabric care requirements including machine-wash detergents, fabric softeners, and stain removers. The segment grows at approximately 14.8% CAGR through washing machine penetration and premiumization toward liquid and concentrated formats.

Builders dominate at 41.8% through indispensable performance enhancement in detergent formulations, softening water hardness and boosting cleaning efficacy across laundry, dishwash, and surface cleaner categories. Their extensive utilization across the highest-volume product segments sustains their ingredient dominance.

North India leads at 45.2% through its high urban population concentration, dominant organized retail infrastructure, and strong presence of aspirational middle-class consumers driving both economy and premium household cleaner demand.

Leading companies include Unilever, Procter & Gamble, Jyothy Laboratories Ltd., and Nirma, among others.

The India household cleaners market is projected to reach approximately USD 22.86 Billion by 2030, driven by continued urbanization, washing machine-driven detergent premiumization, eco-friendly product adoption, and e-commerce channel expansion, accelerating household cleaner accessibility across Tier-2 and Tier-3 cities.

Three priority investment opportunities: eco-friendly and plant-based formulation innovation, capturing premium urban consumers, rural market penetration through affordable sachet formats and direct distribution, and e-commerce channel investment enabling premium product launches and direct-to-consumer relationship building beyond traditional trade constraints.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)