India Housing Loan Market Size, Share, Trends and Forecast by Type, Customer Type, Source, Interest Rate, Tenure, and Region, 2026-2034

India Housing Loan Market Summary:

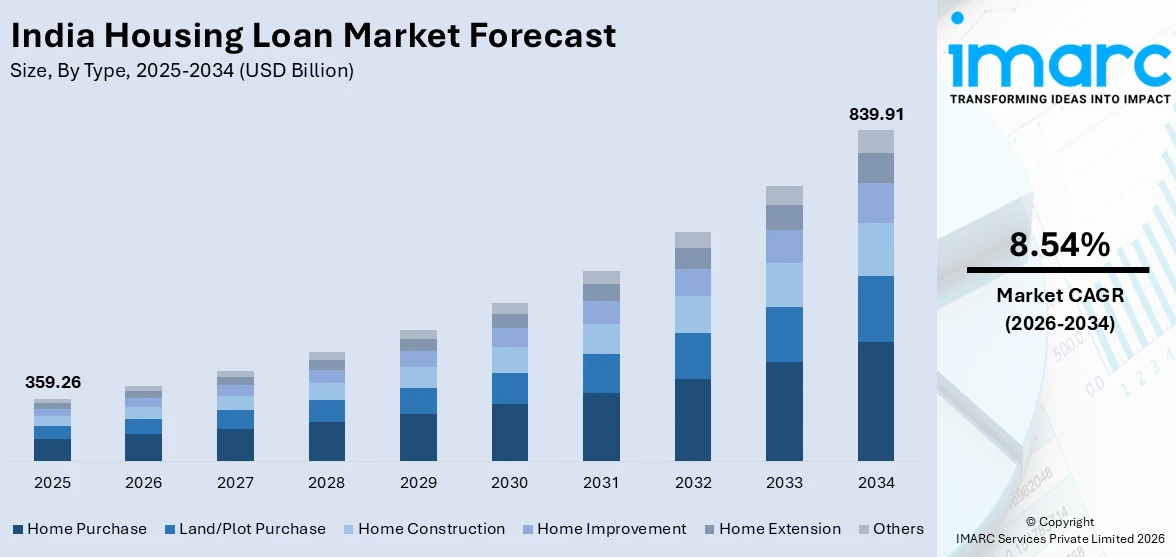

The India housing loan market size was valued at USD 359.26 Billion in 2025 and is projected to reach USD 839.91 Billion by 2034, growing at a compound annual growth rate of 8.54% during 2026-2034.

The India housing loan market is experiencing growth, driven by accelerating urbanization, government-led affordable housing schemes, and a rising salaried population with the growing aspirations for homeownership. Favorable monetary policy, increasing digital adoption in loan processing, and deeper penetration into Tier-2 and Tier-3 cities are collectively transforming the lending landscape. The convergence of demographic imperatives, supportive regulatory frameworks, and an expanding middle class is creating substantial opportunities across the India housing loan market share.

Key Takeaways and Insights:

- By Type: Home purchase dominates the market with a share of 78.5% in 2025, driven by strong demand from first-time homebuyers across metro and Tier-2 cities.

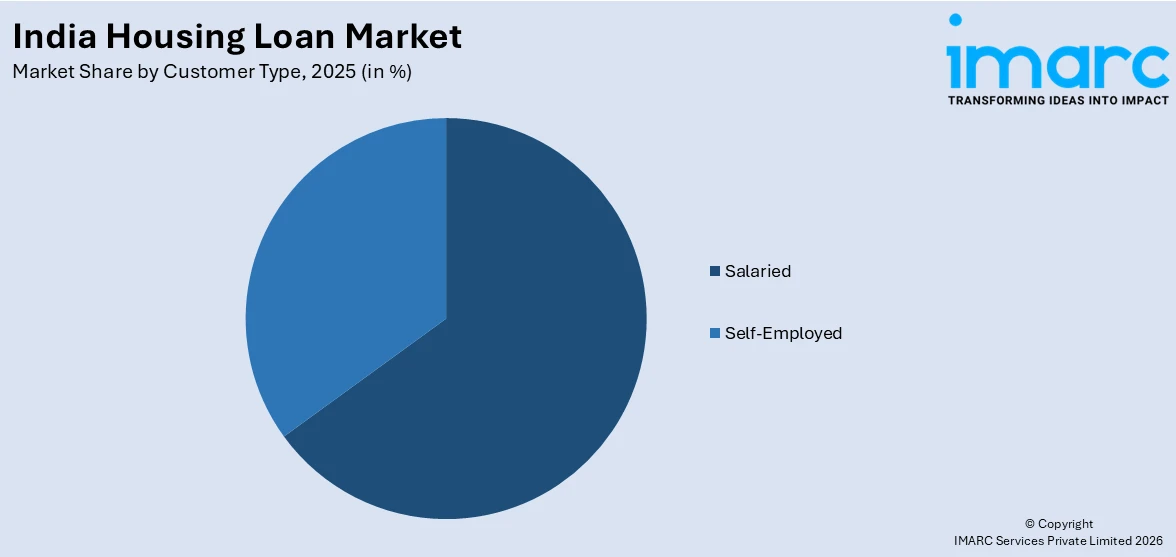

- By Customer Type: Salaried leads the market with a share of 64.7% in 2025, reflecting stable income documentation, higher credit eligibility, and employer-backed financial credibility with lenders.

- By Source: Bank represents the largest segment with a market share of 75.5% in 2025, underpinned by nationwide branch networks, competitive pricing, and deep borrower trust.

- By Interest Rate: Below 10% dominates the market with a share of 62.5% in 2025, as accommodative monetary policy and RBI rate cuts have made sub-10% home loans accessible to a broad borrower base.

- By Tenure: 10 to 20 years leads the market with a share of 42.5% in 2025, balancing manageable monthly installments with moderate total interest outflows for middle-income borrowers.

- By Region: North India represents the largest segment with a market share of 31.5% in 2025, anchored by the National Capital Region's robust real estate activity, rising urban populations, and strong banking infrastructure.

- Key Players: The India housing loan market is characterized by moderate-to-highly competitive intensity, with public-sector banks, private commercial banks, and housing finance companies competing across loan ticket sizes, customer segments, and geographic footprints.

To get more information on this market Request Sample

The housing loan sector in India is growing due to rising urbanization, increasing middle-class income levels, and supportive government housing initiatives. A growing working population and higher migration to urban centers are encouraging home ownership, which is strengthening the demand for housing finance across metropolitan as well as emerging cities. Financial institutions and housing finance companies are also expanding loan accessibility through digital lending platforms and flexible repayment options. According to the National Housing Bank’s Trends and Progress of Housing in India 2024 report, outstanding individual housing loans reached ₹33.53 lakh crore as of September 2024, reflecting a 14% year-on-year increase compared with the same period in the previous year. This steady rise highlights the growing reliance on housing finance to support residential property purchases. Government initiatives promoting affordable housing, along with improving access to formal credit, are further encouraging first-time homebuyers. As real estate development and urban housing demand continue to rise, the housing loan sector is expected to maintain strong growth momentum.

India Housing Loan Market Trends:

Increasing Participation of First-Time Homebuyers

Younger working professionals are entering the housing market earlier due to rising career opportunities and improved access to credit. Many households prefer purchasing homes rather than renting in order to build long-term financial security and asset ownership. Housing finance institutions are offering flexible repayment structures, longer loan tenures, and customized loan products designed to support first-time borrowers. These lending options reduce the financial burden associated with property purchases and encourage more individuals to apply for housing loans. In 2025, IFC announced an investment of up to INR 3 Billion in residential mortgage-backed securities issued by Grihum Housing Finance in India. The funding planned to expand affordable homeownership for low- and middle-income families, particularly first-time buyers. The initiative also aimed to strengthen India’s securitization and housing finance market by mobilizing private capital for mortgage lending.

Policy Reforms Supporting Housing Credit Expansion

Government and regulatory policy adjustments are playing an important role in improving the flow of credit to the housing sector. Revised lending frameworks encourage financial institutions to increase their exposure to housing finance by providing regulatory incentives and classification benefits. Such measures are particularly significant in expanding access to home loans for borrowers in urban and semi-urban regions where property demand continues to grow. By raising loan eligibility thresholds and refining lending guidelines, regulators are helping banks extend larger housing loans under priority lending categories. In 2025, the Reserve Bank of India revised its Priority Sector Lending norms, increasing housing loan limits eligible for PSL classification to ₹50 lakh in major urban centers, supporting broader credit availability for residential property financing.

Artificial Intelligence Transforming Home Loan Processing

Technological innovation is reshaping the housing finance industry in India through the adoption of artificial intelligence (AI) and advanced data analytics. AI-driven lending platforms enable financial institutions to analyze borrower profiles, property data, and credit histories more efficiently, reducing the time required for mortgage approvals. These technologies improve accuracy in risk assessment and enhance the customer experience by offering faster loan decisions and simplified documentation processes. Digital platforms also support multilingual interfaces and automated lender matching systems, making housing finance services more accessible to diverse borrower segments. In 2025, BASIC Home Loan launched HOM-i, an AI-powered instant home loan platform that analyzed three lakh customer profiles and two lakh property profiles during its beta phase, enabling loans worth approximately ₹30,000 crore. The system used generative AI and machine learning (ML) to provide instant credit checks, lender matching, and multilingual guidance for homebuyers.

Market Outlook 2026-2034:

The India housing loan market is expected to sustain strong revenue generation throughout the forecast period, supported by irreversible urbanization trends, government-backed affordable housing schemes, and improving mortgage penetration. The market generated a revenue of USD 359.26 Billion in 2025 and is projected to reach a revenue of USD 839.91 Billion by 2034, growing at a compound annual growth rate of 8.54% from 2026-2034. Falling repo rates, digital loan infrastructure, rising incomes, and deeper HFC penetration in semi-urban markets will collectively sustain momentum across borrower segments and geographies.

India Housing Loan Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Home Purchase |

78.5% |

|

Customer Type |

Salaried |

64.7% |

|

Source |

Bank |

75.5% |

|

Interest Rate |

Below 10% |

62.5% |

|

Tenure |

10 to 20 Years |

42.5% |

|

Region |

North India |

31.5% |

Type Insights:

- Home Purchase

- Land/Plot Purchase

- Home Construction

- Home Improvement

- Home Extension

- Others

The home purchase dominates with a market share of 78.5% of the total India housing loan market in 2025.

Home purchase leads the market due to the strong demand for residential property among urban and semi-urban households. Rising urbanization, population growth, and increasing migration to metropolitan areas are encouraging individuals and families to buy homes rather than rely on rental housing. Financial institutions and housing finance companies offer structured home purchase loans with longer repayment tenures and competitive interest rates, making property ownership more accessible to a broader user base. Government initiatives promoting affordable housing and interest subsidies for eligible buyers also support loan uptake. These factors collectively drive higher demand for housing loans specifically used for purchasing residential properties across India.

Another factor supporting the dominance of home purchase loan is the increasing availability of organized housing projects developed by private and public real estate companies. Large residential developments in major cities and emerging urban centers provide buyers with more property options across different price segments. Banks and housing finance companies actively partner with developers to offer pre-approved loan facilities, which simplifies the financing process for homebuyers. Rising disposable income and improving access to formal credit also encourage consumers to invest in home ownership. As the residential real estate sector continues to expand across India, home purchase loans remain the primary category within housing finance.

Customer Type Insights:

Access the comprehensive market breakdown Request Sample

- Salaried

- Self-Employed

Salaried leads with a market share of 64.7% of the total India housing loan market in 2025.

Salaried dominates the market owing to its stable income structure and predictable repayment capacity. Banks and housing finance companies typically prefer salaried borrowers because regular monthly income reduces credit risk and simplifies loan eligibility assessment. Employers in organized sectors also provide documented salary records, tax statements, and employment verification, which allow lenders to process housing loan applications more quickly. Many financial institutions design loan products specifically for salaried individuals, offering competitive interest rates, flexible tenure options, and higher loan approval rates. With a growing workforce employed in corporate, government, and service sectors across India, salaried borrowers continue to account for a large share of housing loan demand.

Another factor reinforcing the dominance of salaried segment is its stronger access to formal banking channels and credit history. Many salaried individuals maintain salary accounts with banks, making it easier for lenders to assess repayment behavior and offer pre-approved housing loans. Financial institutions also provide simplified documentation and faster loan processing for employees working with reputed organizations. Rising employment in information technology, financial services, healthcare, and other organized industries has expanded the pool of eligible salaried borrowers. As urban employment opportunities continue to grow and financial institutions focus on low-risk lending segments, salaried customers remain a major contributor to housing loan demand across India.

Source Insights:

- Bank

- Housing Finance Companies (HFCs)

Bank exhibits a clear dominance with a 75.5% share of the total India housing loan market in 2025.

Banks represent the largest segment because of their strong financial capacity, extensive branch networks, and wide range of mortgage products offered to borrowers. Public and private sector banks provide housing loans with competitive interest rates, flexible repayment tenures, and higher loan amounts, making them a preferred financing option for homebuyers. Their established presence across urban and semi-urban areas allows them to reach a large customer base seeking property financing. Banks also maintain strong regulatory oversight and standardized lending practices, which increases borrower confidence. With easier access to funding and well-developed credit evaluation systems, banks continue to dominate the housing loan segment across India.

Another factor influencing the leadership of banks is their ability to provide integrated financial services along with housing finance. Many borrowers already maintain savings or salary accounts with banks, making it convenient to apply for home loans through existing banking relationships. Banks frequently offer bundled services, including insurance products, property valuation assistance, and digital loan processing platforms that simplify the borrowing process. Large banking institutions also partner with real estate developers to offer pre-approved housing loans for specific residential projects. As digital banking services expand and home financing becomes more accessible, banks remain the primary source of housing loans across India’s residential property market.

Interest Rate Insights:

- Below 10%

- Above 10%

Below 10% dominates with a market share of 62.5% of the total India housing loan market in 2025.

Below 10% holds the biggest market share attributed to the strong borrower preference for affordable financing options that reduce long-term repayment burden. Housing loans typically involve extended repayment tenures, often spanning 15 to 30 years, making interest rates a critical factor influencing loan selection. Rates below 10% allow borrowers to manage monthly installments more comfortably, encouraging higher loan uptake among middle-income households. Banks and housing finance companies frequently compete by offering interest rates within this range to attract a larger user base. Stable monetary policies and competitive lending practices among financial institutions have also helped maintain housing loan interest rates at relatively accessible levels.

Another factor supporting the dominance of housing loans below 10% in India is the increasing availability of promotional offers and flexible interest rate structures provided by lenders. Financial institutions regularly introduce special home loan schemes for salaried individuals, first-time homebuyers, and women borrowers, often featuring interest rates within this range. Government-supported housing programs and interest subsidy schemes for eligible borrowers also contribute to lower effective borrowing costs. These measures make home ownership more financially feasible for a broader segment of the population. As housing demand continues to grow across urban and semi-urban areas, interest rates below 10% remain the most common and preferred borrowing bracket.

Tenure Insights:

- Below 5 Years

- 5 to Below 10 Years

- 10 to 20 Years

- Above 20 Years

10 to 20 years leads with a market share of 42.5% of the total India housing loan market in 2025.

The 10 to 20 years tenure is leading the market driven by its balance between manageable monthly installments and reasonable total interest outflow. Borrowers often prefer this tenure because it allows them to spread repayments over a longer period without extending the loan for several decades. Compared to shorter tenures, monthly installments remain affordable, which helps middle-income households manage home loan obligations alongside other expenses. Furthermore, the total interest paid over the loan lifecycle stays relatively controlled compared with very long tenures. Banks and housing finance companies commonly structure housing loans within this range, making it a widely offered and easily accessible repayment option.

The segment also benefits from the financial stability of borrowers during their primary earning years. Many homebuyers secure housing loans during the early or middle stages of their careers and prefer to complete repayment before retirement. A tenure within this range aligns well with typical career income progression, allowing borrowers to repay loans while maintaining financial flexibility. Lenders also consider this tenure favorable since it balances credit risk and repayment stability. With steady income growth and predictable repayment schedules, borrowers increasingly choose the 10 to 20 years range as a practical housing loan tenure option.

Regional Insights:

- North India

- South India

- East India

- West India

North India exhibits a clear dominance with a 31.5% share of the total India housing loan market in 2025.

North India leads the market due to the large population base and strong demand for residential properties across major urban centers. Cities, such as Delhi, Noida, Gurugram, Chandigarh, and Lucknow have experienced steady real estate development, attracting homebuyers seeking both affordable and premium housing options. Rapid urban expansion, the growing employment opportunities, and infrastructure improvements are encouraging more individuals to purchase homes in the region. Financial institutions and housing finance companies maintain a strong presence across these cities, making housing loans easily accessible to a wide customer base. This combination of population growth and real estate activity continues to drive housing loan demand across North India.

Another factor supporting the leadership of North India is the expansion of residential projects in emerging urban and semi-urban areas. Real estate developers are increasingly launching housing developments in cities and townships across states, such as Uttar Pradesh, Haryana, Punjab, and Rajasthan. For example, in 2025, DLF announced planned to invest INR 23,500 crore to complete its ongoing residential housing projects across Delhi-NCR and Mumbai. These projects cater to middle-income and first-time homebuyers who often rely on housing loans to finance property purchases. Government investments in road networks, metro systems, and smart city initiatives have also improved connectivity and increased housing demand in the region. As residential construction continues to grow across northern states, housing loan disbursements remain strong, reinforcing the region’s leading position in the market.

Market Dynamics:

Growth Drivers:

Why is the India Housing Loan Market Growing?

Digital Transformation of Housing Loan Services

Digitalization is significantly improving the efficiency and accessibility of housing loan services in India. Financial institutions are increasingly adopting digital platforms that allow customers to apply for loans, submit documents, and track application status online. These technologies enable lenders to serve customers across a broader geographic area without relying heavily on physical branches. Digital platforms also improve transparency and convenience for borrowers, particularly younger consumers who prefer online financial services. In line with this, in 2024, Jio Financial Services launched the upgraded JioFinance App in India to provide a wide range of digital financial services. The platform offered products, including home loans, loans against property, and loans on mutual funds, along with insurance and digital banking features. The app also provided an aggregated view of users’ bank and mutual fund holdings to simplify financial management.

Expanding Housing Finance for Self-Employed Borrowers

A significant portion of India’s workforce operates in self-employment or informal sectors, creating demand for specialized housing finance solutions. Traditional lending models often rely on stable salary documentation, which can limit credit access for entrepreneurs and small business owners. Housing finance providers are increasingly adopting alternative credit evaluation methods that analyze transaction histories, business activity, and other financial indicators to assess borrower reliability. These approaches allow lenders to extend housing loans to individuals who were previously underserved by conventional banking systems. In 2025, Gaja Capital, Lightspeed India Partners, and Premji Invest launched People’s Home Finance with an initial funding of about INR 1,400 crore to provide affordable housing loans to self-employed borrowers using AI-based underwriting models.

Adoption of Cloud Infrastructure for Digital Lending Operations

Cloud computing is playing an increasingly important role in modernizing housing finance operations in India. Financial institutions are adopting cloud-based platforms to improve loan processing speed, strengthen data management systems, and support scalable lending operations. These technologies allow lenders to securely store and analyze large volumes of financial data while maintaining efficient loan servicing and customer management. Cloud infrastructure also supports digital lending channels that reach customers across diverse geographic regions without extensive physical infrastructure. In 2024, Unico Housing Finance implemented Oracle Cloud Infrastructure to enhance its digital housing loan services, enabling faster loan processing, stronger data security, and improved operational scalability while expanding affordable housing finance access across underserved communities.

Market Restraints:

What Challenges the India Housing Loan Market is Facing?

Rising Property Prices Limiting Affordability for First-Time Buyers

Escalating residential property prices in major urban centers present a persistent affordability challenge that constrains loan eligibility among middle and lower-income borrowers. Rising land acquisition costs, project approval delays, and construction material price pressures pass through to end-unit pricing, widening the gap between household income levels and the capital required for even affordable housing purchases.

Credit Access Challenges for Self-Employed and Informal Sector Borrowers

A significant portion of India's working population earns income through self-employment, informal trade, or agriculture, making standardized documentation and income verification difficult. Traditional underwriting frameworks employed by major banks are poorly suited to assess creditworthiness based on GST returns, bank statement patterns, or alternate data, resulting in systematic exclusion of otherwise creditworthy borrowers. Inadequate loan product design for irregular income profiles limits formal housing credit penetration among this large demographic cohort.

Regional Imbalances in Housing Credit Distribution

Housing credit flows are highly concentrated in Southern, Western, and Northern urban regions, while Eastern and Northeastern states remain structurally underserved. The NHB's 2024 Trends and Progress report explicitly identified sharp regional disparities in housing credit availability, noting that lower per-capita incomes, limited retail banking infrastructure, underdeveloped land record systems, and constrained real estate supply pipelines in eastern and northeastern markets impede the equitable spread of formal mortgage credit, slowing aggregate market growth potential and deepening financial inequality across India's geographic landscape.

Competitive Landscape:

The India housing loan market exhibits moderate-to-highly competitive intensity, characterized by a tiered structure involving public-sector banks, large private commercial banks, dedicated housing finance companies, and non-banking financial companies. Market participants compete across dimensions of interest rate pricing, loan-to-value ratios, digital onboarding efficiency, and geographic coverage. Public-sector banks leverage deposit-funded cost advantages and government alignment to dominate volume-based disbursements, while private banks and HFCs differentiate through product innovation, faster processing, and niche segment focus. The co-lending model is reshaping competitive dynamics by enabling HFCs to combine origination agility with bank capital access. International institutional investments are also deepening capital market participation and broadening the competitive ecosystem.

Recent Developments:

- July 2025: EQT completed the acquisition of Niwas Housing Finance and committed INR 5 billion (about USD 58 million) to support the company’s growth in India. The investment aimed to expand affordable mortgage access and strengthen digital capabilities across its operations. Niwas serves low-income households and small businesses, with over 47,000 customers and assets under management of around INR 30 billion.

- May 2025: India listed its first mortgage-backed Pass Through Certificates (PTCs) on the National Stock Exchange. The issuance of ₹1,000 crore, backed by housing loans from LIC Housing Finance, was fully subscribed and carried a 7.26% annual coupon with nearly 20-year maturity. The listing aims to strengthen the housing finance market and promote securitization in India’s financial system.

- March 2025: Aditya Birla Housing Finance launched ‘Khushi’, a customized home loan offering designed specifically for women borrowers in India. The program provides flexible financing solutions with loan amounts ranging from ₹5 lakh to ₹1 crore, along with features such as express loan sanction, digital onboarding, and a “Track My Loan” facility. The initiative aims to promote financial independence and make homeownership more accessible for women through tailored lending solutions.

India Housing Loan Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Home Purchase, Land/ Plot Purchase, Home Construction, Home Improvement, Home Extension, Others |

| Customer Types Covered | Salaried, Self-Employed |

| Sources Covered | Bank, Housing Finance Companies (HFCs) |

| Interest Rates Covered | Below 10%, Above 10% |

| Tenures Covered | Below 5 Years, 5 to below 10 Years, 10 to 20 Years, Above 20 Years |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Housing Loan Market Report

The India housing loan market size was valued at USD 359.26 Billion in 2025.

The India housing loan market is expected to grow at a compound annual growth rate of 8.54% during 2026-2034 to reach USD 839.91 Billion by 2034.

The home purchase segment holds the largest share of 78.5% in 2025, driven by strong first-time buyer demand, government subsidy programs, and rising urban homeownership aspirations across income segments.

Key factors driving the India housing loan market include the rising participation of young professionals seeking early homeownership and improved access to housing credit. Flexible loan structures support first-time buyers. In 2025, IFC invested up to INR 3 billion in mortgage-backed securities issued by Grihum Housing Finance.

Major challenges include rising property prices limiting affordability, inadequate credit access for self-employed and informal sector borrowers, and significant regional imbalances in housing credit distribution that leave Eastern and Northeastern markets underserved relative to their housing finance potential.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)