India IoT Insurance Market Size, Share, Trends and Forecast by Insurance Type, Component, Application, and Region, 2026-2034

India IoT Insurance Market Size, Share, Trends & Forecast (2026-2034)

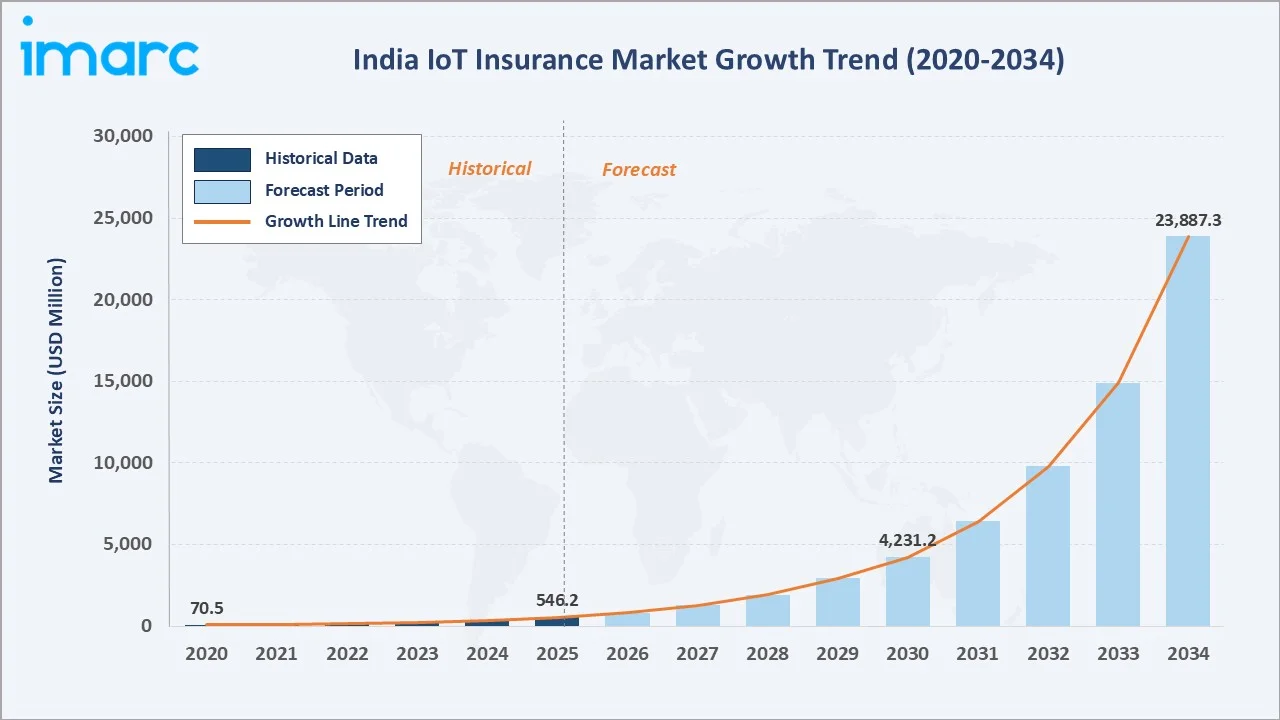

The India IoT insurance market size reached USD 546.2 Million in 2025 and is projected to reach USD 23,887.3 Million by 2034, exhibiting a CAGR of 50.60% during 2026-2034. Rapid IoT adoption, Digital India initiatives, and rising insurance penetration are the primary forces shaping this market.

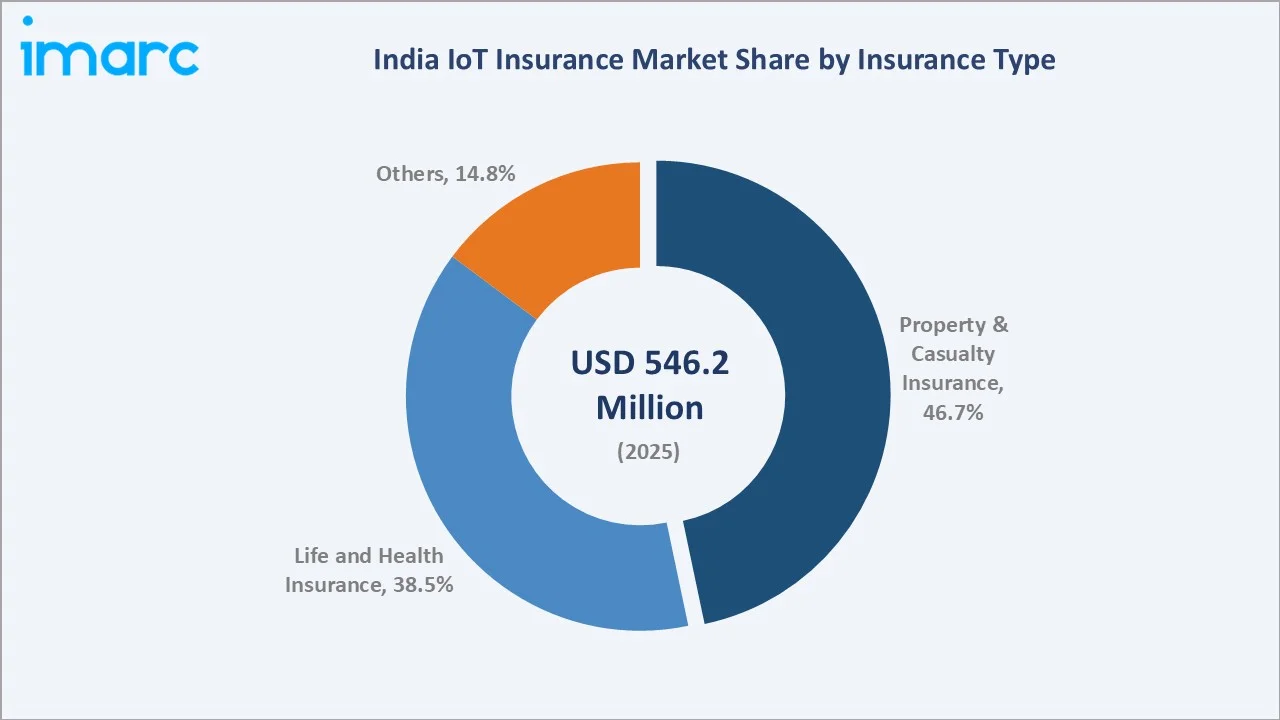

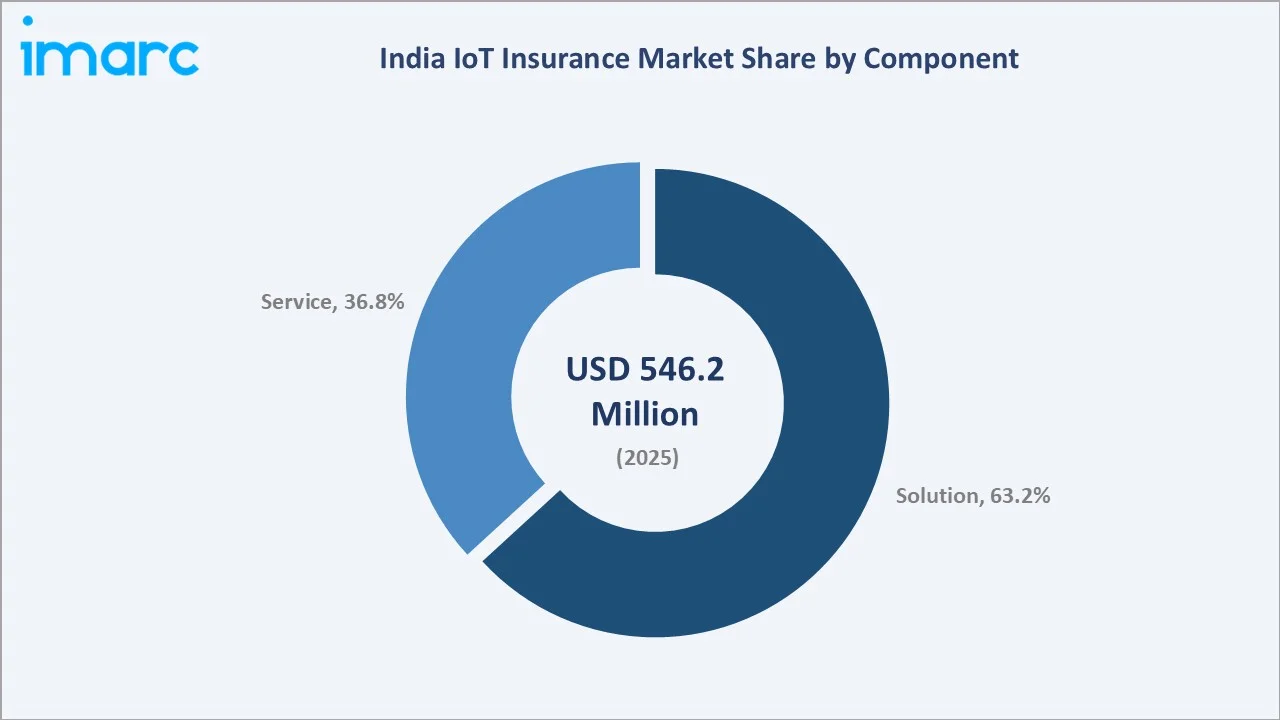

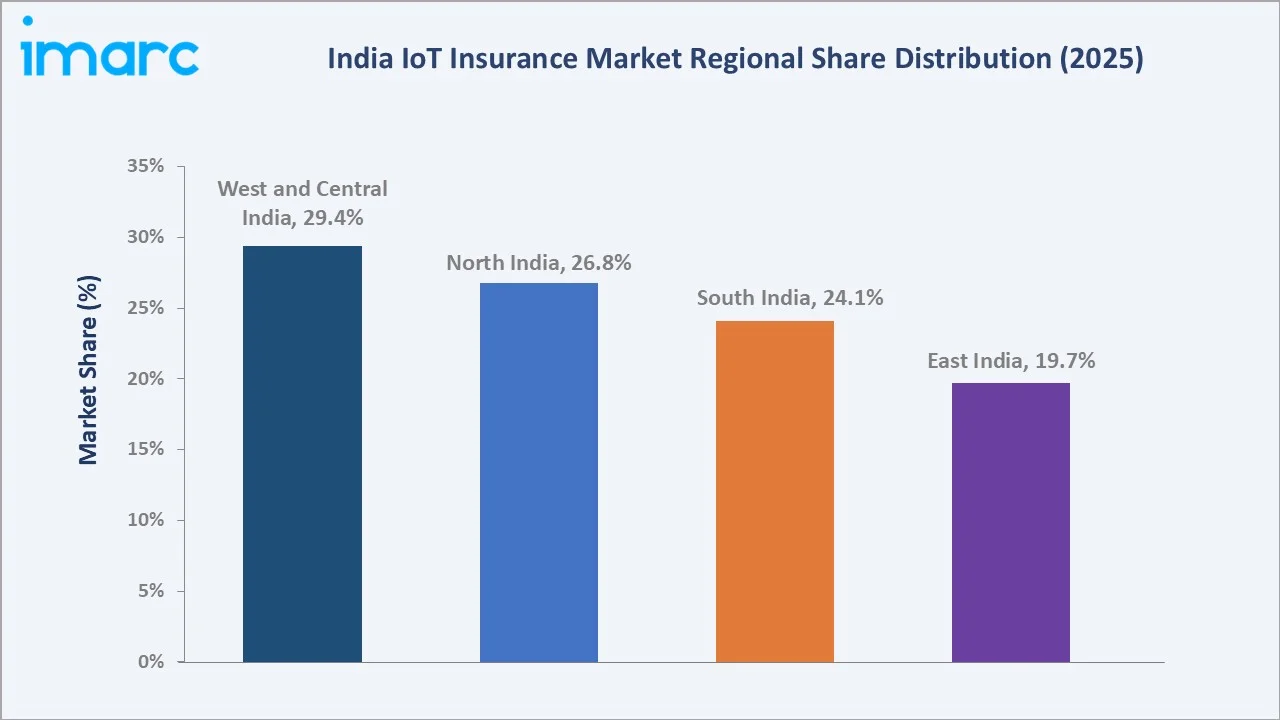

Property and Casualty Insurance lead the Insurance Type segment at 46.7% in 2025, driven by telematics and smart property applications. Solution dominates the Component segment at 63.2%. West and Central India accounts for 29.4% of the regional share, anchored by the Mumbai financial hub and Pune technology ecosystem.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 546.2 Million |

|

Forecast Market Size (2034) |

USD 23,887.3 Million |

|

CAGR (2026-2034) |

50.60% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Insurance Type |

Property and Casualty Insurance (46.7% share, 2025) |

|

Leading Component |

Solution (63.2% share, 2025) |

|

Leading Region |

West and Central India (29.4% share, 2025) |

The India IoT insurance market growth from 2020 through 2034 reflects accelerating digital transformation in the insurance sector. The forecast to USD 23,887.3 Million by 2034 captures expanding IoT device penetration, IRDAI regulatory support, and the adoption of data-driven underwriting and claims models.

To get more information on this market, Request Sample

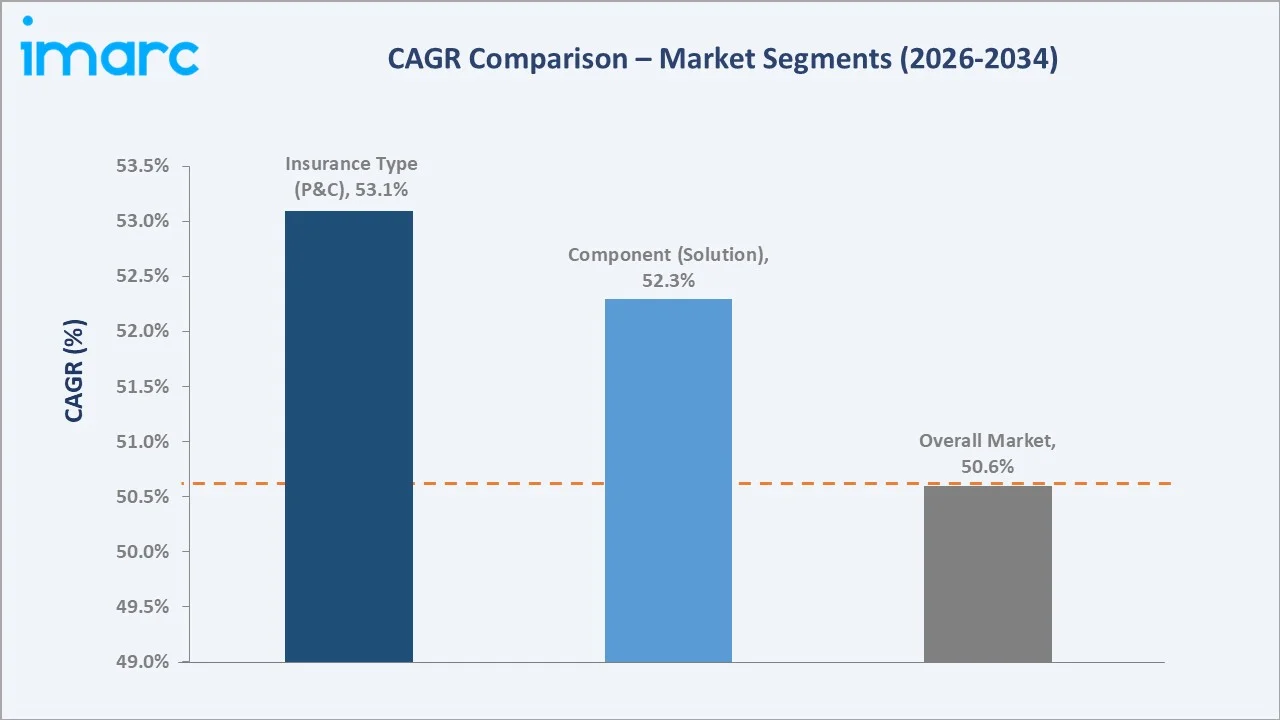

The CAGR trajectories across key Insurance Type and Component sub-segments highlight Property and Casualty Insurance at approximately 53.1% CAGR and Solution component at approximately 52.3% CAGR as the fastest-growing categories within the India IoT insurance market through 2034.

Executive Summary

The India IoT insurance market is on a high-growth trajectory from USD 546.2 Million in 2025 to USD 23,887.3 Million by 2034. The market integrates IoT-enabled data collection, AI-driven risk assessment, and usage-based policy frameworks across insurance verticals in India.

Property and Casualty Insurance leads at 46.7% in 2025, driven by telematics-based motor insurance, smart home coverage, and connected commercial property policies. Life and Health Insurance (38.5%) is growing through wearable-linked wellness programs and digital health integration.

Solution segment dominates at 63.2% in 2025, encompassing IoT analytics platforms, risk management software, and data integration middleware. Service segment (36.8%) provides implementation, integration, and managed services representing high-value recurring revenue streams for technology providers.

West and Central India leads at 29.4% in 2025, anchored by Mumbai's financial services ecosystem and Pune's technology sector. North India follows at 26.8%, driven by Delhi NCR-based InsurTechs and large enterprise IoT deployments across the northern commercial corridor.

Key Market Insights

|

Insight |

Data |

|

Largest Insurance Type |

Property and Casualty Insurance – 46.7% share (2025) |

|

Leading Component |

Solution – 63.2% share (2025) |

|

Leading Region |

West and Central India – 29.4% share (2025) |

|

Second Largest Region |

North India – 26.8% share (2025) |

|

Top Companies |

IBM Corporation, Microsoft, Verisk Analytics, Inc., Wipro, Cognizant |

- Property and Casualty Insurance at 46.7% dominates because India's vehicle-dense roads and rising smart home adoption drive telematics and connected property insurance demand. IRDAI sandbox experiments enable insurers to launch dynamic, IoT-linked premium models rapidly.

- Solution segment commands 63.2% share because insurance companies prioritise technology platforms for data ingestion, risk analytics, and policy management over standalone services. Platform scalability and real-time insight generation are critical for competitive differentiation.

- West and Central India's 29.4% regional dominance reflects concentration of India's leading insurers and financial institutions in Mumbai, the technology ecosystem in Pune, and the growing smart manufacturing corridor driving commercial IoT insurance adoption across Maharashtra and Gujarat.

India IoT Insurance Market Overview

The India IoT insurance market integrates connected device data, predictive analytics, and digital insurance infrastructure to enable real-time risk assessment, dynamic premium pricing, and automated claims management across motor, health, property, agriculture, and commercial insurance lines.

The ecosystem integrates IoT device manufacturers, telecom operators, cloud infrastructure providers, analytics platforms, IRDAI-regulated insurers, InsurTech startups, corporate enterprises, and individual consumers served through digital-first distribution models across all Indian regions.

Market Dynamics

To evaluate market opportunities, Request Sample

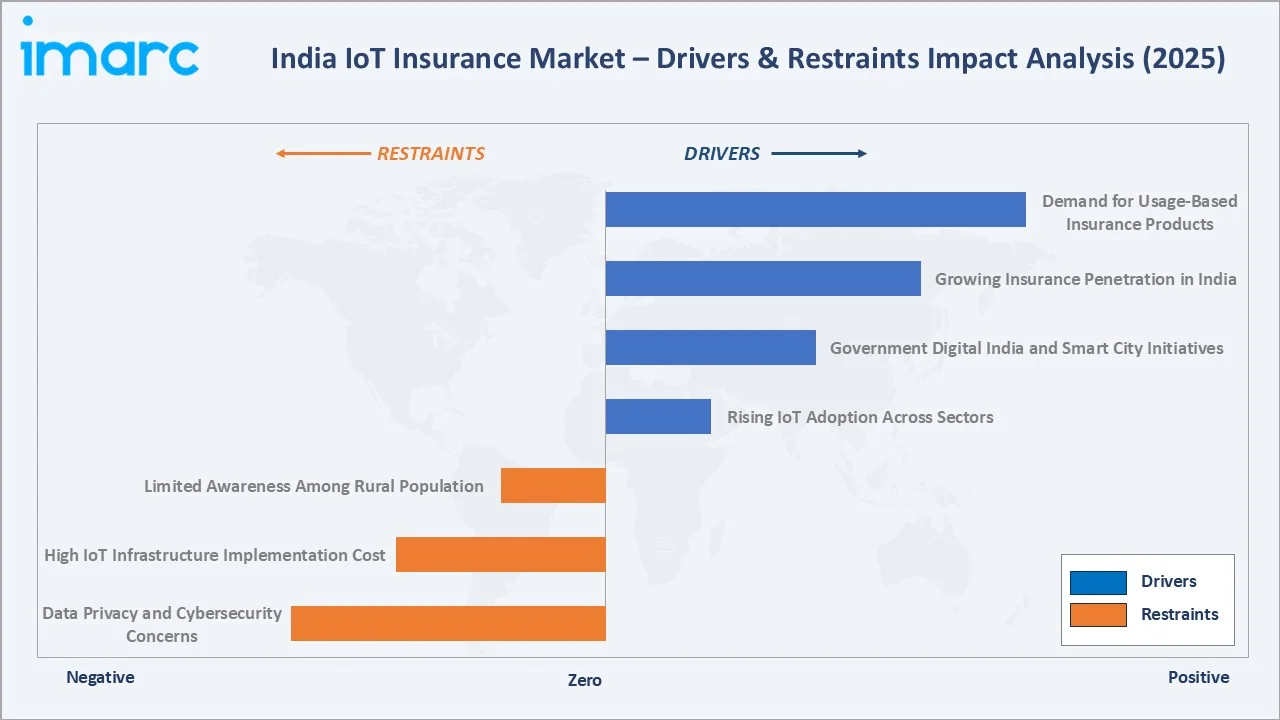

Market Drivers

- Rising IoT Adoption Across Sectors: India's accelerating deployment of connected devices in automotive, healthcare, agriculture, and smart homes generate vast data streams enabling insurers to develop usage-based and behaviour-linked products.

- Government Digital India and Smart City Initiatives: The Digital India programme and 100 Smart Cities Mission are accelerating IoT infrastructure deployment nationwide. Government mandates for connected vehicles, smart meters, and digital health infrastructure expand the insurable IoT ecosystem, providing strong regulatory momentum for market growth.

- Growing Insurance Penetration in India: India's insurance penetration remains below global averages, presenting vast untapped opportunity. IoT-enabled products make insurance more accessible, affordable, and personalised through real-time data, attracting previously uninsured consumers and businesses to formal insurance products across all income segments.

- Demand for Usage-Based Insurance Products: Indian consumers and fleet operators are increasingly adopting pay-as-you-drive, pay-how-you-drive, and usage-based health insurance models. Telematics data from connected vehicles and wearables enables precise premium calculation, improving affordability and driving new customer acquisition across the market.

Market Restraints

- Data Privacy and Cybersecurity Concerns: IoT insurance depends on continuous personal data collection, raising significant privacy and cybersecurity risks. India's evolving Digital Personal Data Protection Act and consumer concerns about data misuse create regulatory complexity and trust barriers limiting faster market adoption across segments.

- High IoT Infrastructure Implementation Cost: Deploying IoT sensors, connectivity infrastructure, and data analytics platforms requires substantial capital investment. Smaller insurance companies and rural deployment scenarios face cost barriers that limit widespread adoption beyond urban and semi-urban markets in India.

- Limited Awareness Among Rural Population: Awareness of IoT-linked insurance products remain concentrated in urban centres. Rural populations, representing significant insurance growth opportunity, lack exposure to connected device benefits, constraining market penetration and requiring extensive consumer education investment from insurers.

Market Opportunities

- Agricultural IoT Insurance Opportunity: Agricultural IoT insurance presents a significant untapped opportunity as smart farming sensors, drone surveillance, and weather monitoring enable precise crop risk assessment. Government crop insurance mandates and smart agriculture investment create conditions for rapid deployment across Indian states.

- IRDAI Regulatory Sandbox Expansion: Expansion of IRDAI's regulatory sandbox for InsurTech encourages innovation in IoT-based product development, enabling startups and established insurers to pilot new connected insurance solutions with regulatory guidance and controlled market testing frameworks.

Market Challenges

- IoT Interoperability Complexity: Achieving interoperability across diverse IoT devices, platforms, and insurance systems is technically complex. Standardisation gaps in data formats and communication protocols increase integration costs and slow deployment of comprehensive IoT insurance ecosystems across India.

- Insurance-Tech Talent Shortage: Shortage of professionals combining insurance expertise with IoT, data science, and AI capabilities constrains innovation velocity and operational efficiency. India's insurance sector must invest significantly in talent development and cross-domain training programmes.

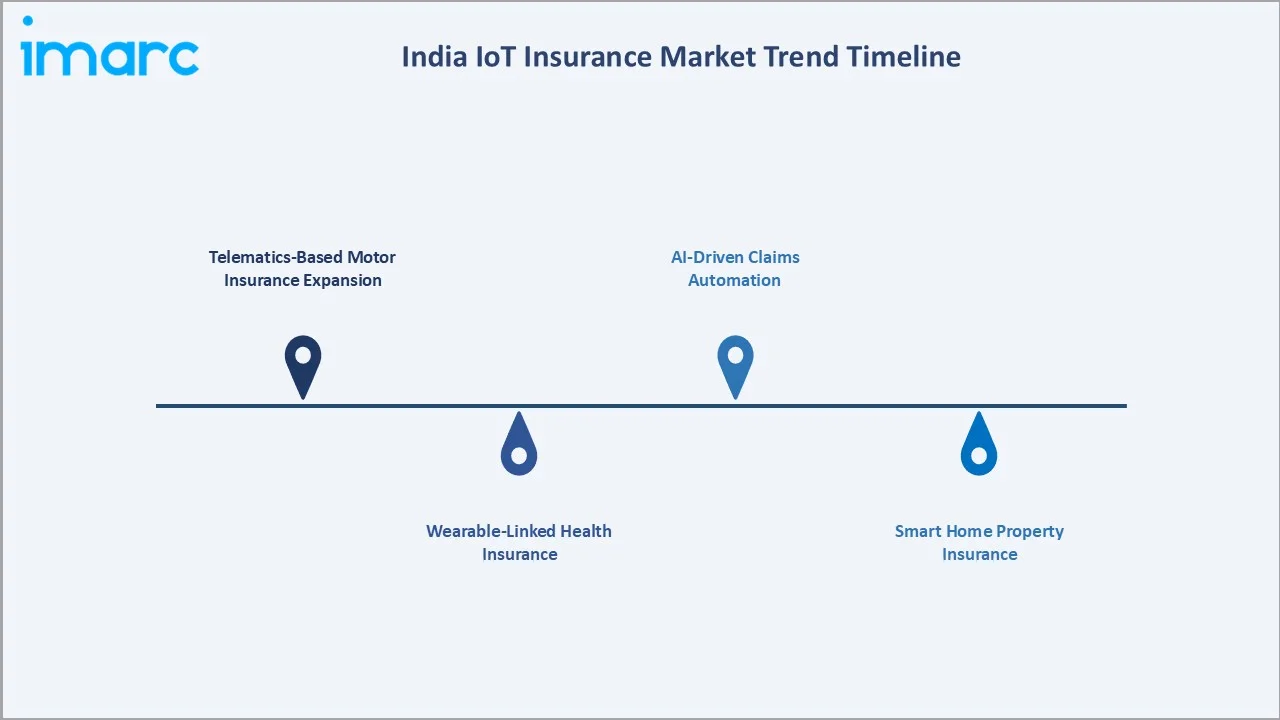

Emerging Market Trends

1. Telematics-Based Motor Insurance Expansion

India's motor insurance sector is rapidly integrating telematics devices for real-time driver behaviour monitoring. Insurers are deploying OBD-based and smartphone telematics solutions enabling risk-based premium differentiation across millions of vehicles on Indian roads.

2. Wearable-Linked Health Insurance

Health insurers are integrating fitness tracker data into wellness programme design and premium structures. IRDAI's health insurance innovation framework encourages behavioural incentive models, driving adoption of wearable-linked policies among urban health-conscious consumers in India.

3. Smart Home Property Insurance

Connected smoke detectors, security cameras, and water sensors are enabling dynamic property insurance pricing. Real-time risk monitoring allows insurers to offer proactive risk alerts and premium discounts for properties with active IoT safety infrastructure deployed.

4. AI-Driven Claims Automation

IoT-generated data streams enable straight-through claims processing for connected vehicle accidents, smart home incidents, and health events. AI-powered claims automation significantly reduces processing costs, improving insurer profitability and policyholder experience simultaneously.

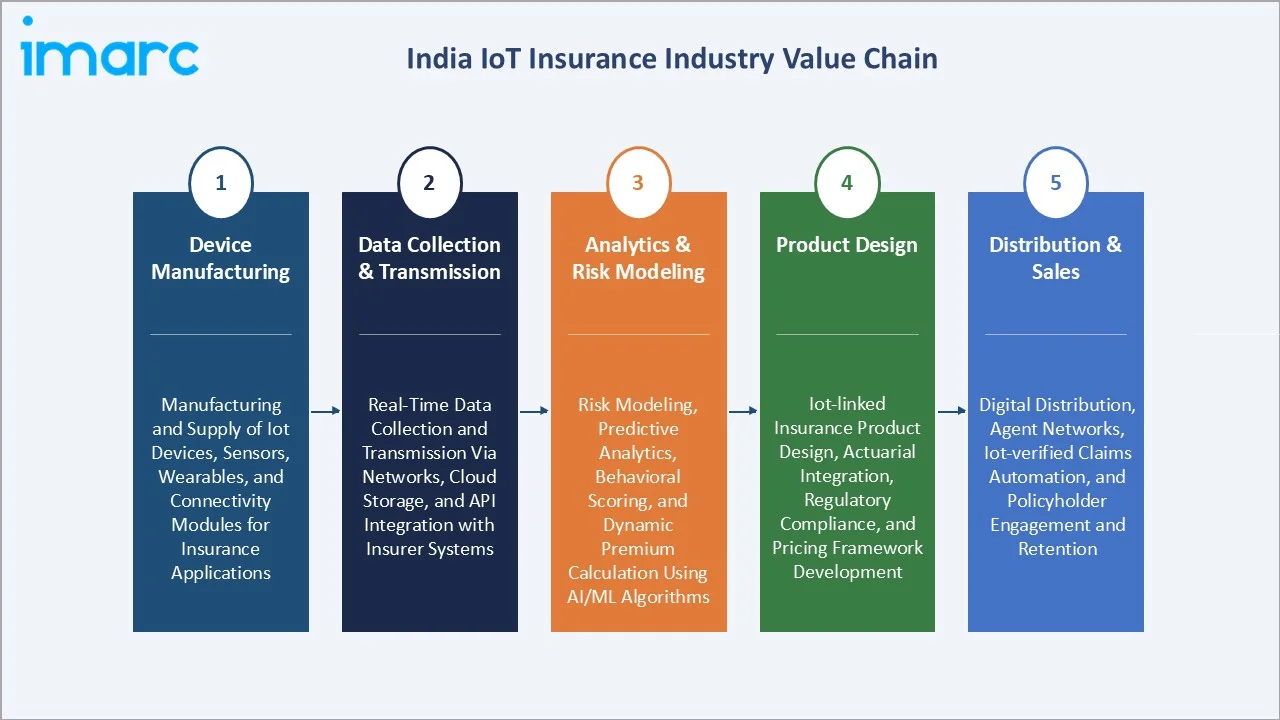

Industry Value Chain Analysis

The India IoT insurance value chain spans five integrated stages from device manufacturing through claims settlement. Analytics and product design stages capture primary value, while distribution and after-sales generate recurring revenue supporting long-term customer relationships.

|

Value Chain Stage |

Key Activities |

|

Device Manufacturing |

Manufacturing and supply of IoT devices, sensors, wearables, and connectivity modules for insurance applications |

|

Data Collection & Transmission |

Real-time data collection and transmission via networks, cloud storage, and API integration with insurer systems |

|

Analytics & Risk Modeling |

Risk modeling, predictive analytics, behavioral scoring, and dynamic premium calculation using AI/ML algorithms |

|

Product Design |

IoT-linked insurance product design, actuarial integration, regulatory compliance, and pricing framework development |

|

Distribution & Sales |

Digital distribution, agent networks, IoT-verified claims automation, and policyholder engagement and retention |

Analytics and AI modeling stages capture the highest value in the chain, requiring specialised data science capabilities and proprietary IoT risk databases. Distribution through digital platforms and automated claims processing represent rapidly growing revenue streams for insurers.

Technology Landscape in the India IoT Insurance Industry

IoT Platform and Data Integration Architecture

Enterprise IoT platforms enabling real-time data ingestion from millions of connected devices, standardised API frameworks for insurer system integration, and edge computing capabilities are foundational technologies driving operational efficiency across India's IoT insurance ecosystem.

AI and Machine Learning for Risk Assessment

Machine learning models analysing behavioural data from telematics, wearables, and smart sensors enable predictive risk scoring and fraud detection. Insurers are deploying AI-driven underwriting engines that significantly reduce manual assessment time for IoT-linked policies.

Blockchain for Claims Transparency

Distributed ledger technology is emerging in India's IoT insurance space for immutable claims records, transparent smart contracts, and automated trigger-based payouts. Blockchain reduces disputes and accelerates parametric insurance settlements in agriculture and commercial lines.

5G and LPWAN Connectivity Infrastructure

India's expanding 5G network and Low-Power Wide-Area Network infrastructure improve reliability and cost-efficiency of IoT data transmission. Enhanced connectivity in semi-urban regions is broadening the geographic addressable market for IoT insurance products.

Market Segmentation Analysis

The report covers the following segments

|

Segment Category |

Segment |

Market Share |

Year |

|

Insurance Type |

Property and Casualty Insurance |

46.7% |

2025 |

|

Component |

Solution |

63.2% |

2025 |

|

Application |

Automotive, Transportation and Logistics |

🔒 |

2025 |

|

Region |

West and Central India |

29.4% |

2025 |

By Insurance Type

Property and Casualty Insurance commands 46.7% in 2025, driven by telematics-based motor policies and connected commercial property coverage. India's vehicle population exceeding 300 million and rising smart home penetration create an expansive addressable market for IoT-linked P&C products.

To access detailed market analysis, Request Sample

Life and Health Insurance (38.5%) benefits from wearable health monitoring, wellness incentive programmes, and digital health integration. IRDAI's supportive policy framework for InsurTech enables innovative usage-based health products. Others (14.8%) covers agriculture, specialty, and commercial lines.

By Component

Solution segment dominates at 63.2% in 2025, encompassing IoT analytics platforms, risk management software, policy administration systems, and data integration middleware. Technology investment is concentrated in platform capabilities enabling real-time risk insight generation at scale.

Service segment (36.8%) covers IoT system integration, consulting, managed analytics, and platform maintenance. As IoT deployments scale, recurring service revenues are growing faster than initial solution sales, improving long-term profitability for technology vendors and insurers.

Regional Market Insights

|

Region |

Share |

Key Characteristics |

|

West and Central India |

29.4% |

High insurance company concentration; strong InsurTech ecosystem and commercial IoT deployment |

|

North India |

26.8% |

Significant enterprise technology buyers; government digital infrastructure investment |

|

South India |

24.1% |

Technology corridor advantage; health insurance innovation and agricultural IoT applications |

|

East India |

19.7% |

Growing smart city deployments; expanding digital financial services and agricultural coverage |

West and Central India's 29.4% market dominance in 2025 is driven by the concentration of India's largest insurance companies, the InsurTech ecosystem, and the smart manufacturing sector. Large enterprise IoT deployments and sophisticated financial services infrastructure accelerate adoption.

North India at 26.8% is anchored by Delhi NCR's concentration of enterprise technology buyers and government digital infrastructure investment. South India at 24.1% benefits from the technology-insurance convergence. East India at 19.7% is an emerging frontier with significant smart city potential.

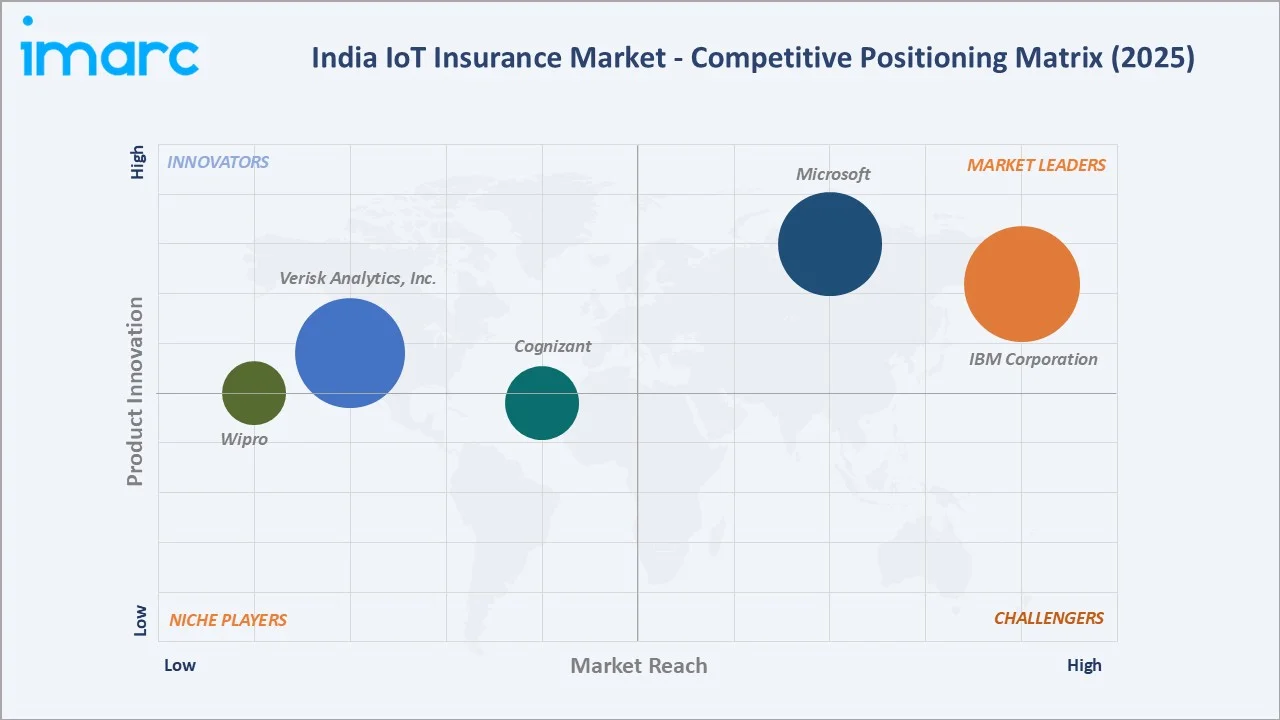

Competitive Landscape

The India IoT insurance market is moderately concentrated, with global technology majors and specialised analytics providers commanding significant market positions. Established IT services companies leverage cloud, AI, and IoT capabilities alongside deep insurance domain expertise to maintain competitive advantage.

|

Company Name |

Key Products / Operations |

Market Position |

Strategic Focus |

|

IBM Corporation |

watsonx Orchestrate, watsonx.governance, IBM watsonx.data |

Leader |

Advancing AI risk analytics; cloud-native insurance modernisation |

|

Microsoft |

Azure IoT Hub, Azure AI, Microsoft Cloud for Financial Services |

Leader |

Scaling Azure-based IoT insurance platforms; InsurTech partnerships |

|

Verisk Analytics, Inc. |

P&C insurance |

Established |

Providing risk data assets and catastrophe modelling for IoT lines |

|

Wipro |

IoT Analytics |

Growing |

Deploying IoT analytics for Indian insurance clients; P&C focus |

|

Cognizan |

Insurance Platform Modernization (IPM) |

Growing |

Enabling insurer IoT transformation across policy and claims lifecycle |

Key players include IBM Corporation, Microsoft, Verisk Analytics, Inc., Wipro, Cognizant, and others.

Key Company Profiles

IBM Corporation

IBM Corporation is a global technology leader providing AI, cloud, and data analytics solutions for the insurance sector. IBM's IoT and Watson AI platforms enable Indian insurers to develop data-driven, connected insurance products at enterprise scale.

- Product Portfolio: watsonx Orchestrate, watsonx.governance, IBM watsonx.data

- Strategic Focus: IBM is focused on accelerating cloud migration of Indian insurance core systems, embedding Watson AI into underwriting and claims workflows, and delivering hybrid cloud solutions enabling secure, scalable IoT data processing for analytics at enterprise scale.

Microsoft

Microsoft provides cloud computing, AI, and IoT infrastructure through Azure that forms the backbone of many India IoT insurance deployments. Microsoft Industry Cloud for Financial Services delivers purpose-built insurance technology capabilities on Azure.

- Product Portfolio: Azure IoT Hub, Azure AI, Microsoft Cloud for Financial Services

- Strategic Focus: Microsoft is deepening partnerships with Indian InsurTech companies, traditional insurers, and IRDAI to build Azure-native IoT insurance ecosystems, integrating Copilot AI capabilities into insurance workflow automation and customer engagement platforms.

Market Concentration Analysis

The India IoT insurance market features moderate concentration among global technology providers and specialised analytics firms. Global IT majors hold dominant positions through comprehensive platform capabilities, while Indian IT services firms are rapidly gaining share through domain expertise and cost-competitive delivery.

At the segment level, Solution segment concentration reflects large enterprise contracts for IoT analytics platforms among major insurers. Service segment is more fragmented, with numerous mid-size technology integrators and consulting firms competing on domain specialisation and implementation capability.

Investment & Growth Opportunities

Fastest-Growing Segments

Property and Casualty Insurance represents the highest-growth segment at approximately 53.1% CAGR through 2034, driven by telematics motor insurance and commercial IoT coverage expansion. Solution component leads at 52.3% CAGR as platform investment dominates insurer technology spending.

Emerging Markets

East India and Tier-2 cities represent significant investment frontiers with expanding smart infrastructure and rising digital insurance adoption. Agricultural IoT insurance is an untapped multi-billion-dollar opportunity as precision farming technology penetration accelerates across India.

Venture & Investment Trends

Private equity and venture capital are increasing allocation to India InsurTech companies combining IoT data capabilities with insurance distribution platforms. IRDAI's regulatory sandbox and government-backed innovation programmes are catalysing ecosystem investment across the value chain.

Future Market Outlook (2026-2034)

The India IoT insurance market is forecast to expand from USD 546.2 Million in 2025 to USD 23,887.3 Million by 2034 at a CAGR of 50.60%, driven by digital India transformation, IoT device proliferation, and IRDAI's progressive regulatory framework supporting connected insurance product innovation.

Three structural forces will shape the market through 2034: accelerating IoT device adoption across automotive, health, and property sectors will expand the addressable market; AI-driven underwriting and claims automation will improve the economics of IoT insurance deployment; and India's growing middle class will demand personalised, data-driven insurance aligned with connected lifestyles.

Research Methodology

Primary Research

Primary research encompassed structured interviews with IoT insurance platform providers, IRDAI-regulated insurers, InsurTech entrepreneurs, technology integrators, and enterprise IoT deployment managers. Primary data validated market sizing, segment shares, and technology adoption trends across the market.

Secondary Research

Key secondary sources include IRDAI annual reports and circulars, Ministry of Electronics and Information Technology data, insurance industry association publications, IoT industry databases, company annual reports, and digital insurance market intelligence publications covering India.

Forecasting Models

Market size estimations were derived using bottom-up IoT device adoption modelling, insurance premium elasticity analysis, and top-down insurance sector growth projections. Scenario modelling encompassed base, optimistic, and conservative cases incorporating regulatory assumptions through 2034.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Insurance Types Covered | Life and Health Insurance, Property and Casualty Insurance, Others |

| Components Covered | Solution, Service, |

| Applications Covered | Automotive, Transportation and Logistics, Life and Health, Commercial and Residential Buildings, Business and Enterprise, Agriculture, Others |

| Regions Covered | North India, West and Central India, East India, South India |

| Companies Covered | IBM Corporation, Microsoft, Verisk Analytics Inc., Wipro, Cognizant, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India IoT insurance market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India IoT insurance market.

- The study maps the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India IoT insurance industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the India IoT Insurance Market Report

The India IoT insurance market reached USD 546.2 Million in 2025, reflecting accelerating IoT device adoption, IRDAI regulatory support, and growing demand for usage-based and telematics insurance products across motor, health, and property segments.

The market is projected to reach USD 23,887.3 Million by 2034, growing at a CAGR of 50.60% during 2026-2034, driven by expanding IoT infrastructure, AI-powered underwriting, digital insurance distribution, and India's rapidly growing digitally connected consumer and enterprise base.

Property and Casualty Insurance leads with 46.7% share in 2025, driven by telematics motor insurance and smart property coverage. This segment is expected to maintain leadership through 2034 as connected vehicle and smart home penetration expands across Indian markets.

Solution segment commands 63.2% share in 2025. Insurance companies prioritise IoT analytics platforms, risk management software, and data integration solutions over services, as platform capabilities directly determine underwriting accuracy and competitive differentiation.

West and Central India dominates with 29.4% share in 2025, anchored by Mumbai's insurance financial hub, Pune's technology ecosystem, and Gujarat's manufacturing sector. The region is expected to maintain leadership through 2034.

Key drivers include rising IoT adoption across sectors, Digital India and Smart City government initiatives, growing insurance penetration presenting greenfield opportunity, and increasing consumer demand for usage-based, personalised insurance products enabled by connected device data.

Major challenges include data privacy and cybersecurity concerns, high IoT infrastructure implementation costs, limited consumer awareness in rural markets, interoperability gaps across device ecosystems, and a shortage of professionals combining insurance knowledge with IoT and data science expertise.

Leading companies include IBM Corporation, Microsoft, Verisk Analytics, Inc., Wipro, Cognizant, and others.

Key technologies include IoT platform and data integration architecture, AI and ML risk assessment engines, blockchain for transparent claims settlement, 5G and LPWAN connectivity enabling broader geographic coverage, and edge computing reducing IoT data latency for real-time applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)