India Logistics Automation Market Size, Share, Trends and Forecast by Component, Function, Vertical, and Region, 2026-2034

India Logistics Automation Market Summary:

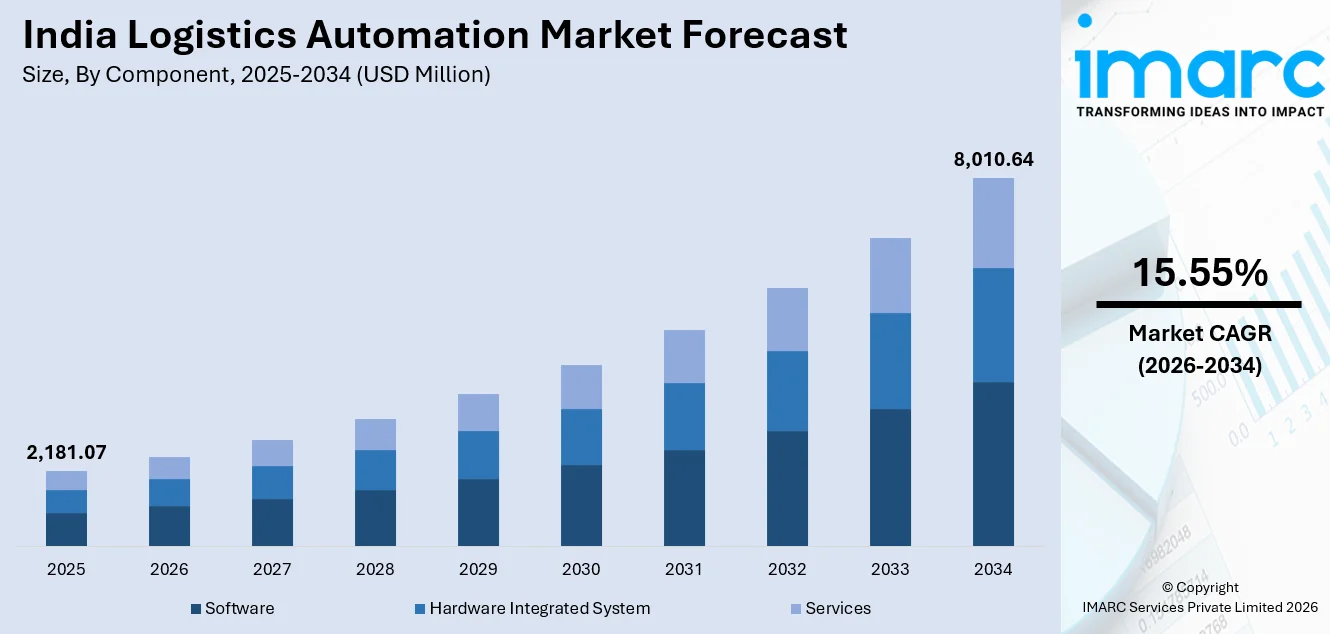

The India logistics automation market size was valued at USD 2,181.07 Million in 2025 and is projected to reach USD 8,010.64 Million by 2034, growing at a compound annual growth rate of 15.55% from 2026-2034.

The India logistics automation market is also witnessing a significant boost as various businesses from different industries are adopting smart supply chain solutions to optimize their efficiency. The increasing need for efficient order fulfillment, real-time visibility, and optimized warehousing processes is driving the adoption of technology-based logistics platforms. The increasing use of robotics, artificial intelligence, and Internet of Things technology is revolutionizing the conventional supply chain model, allowing for faster processing, increased accuracy, and minimal human intervention. The growing manufacturing sector, along with the increasing adoption of e-commerce and favorable government policies, is also fueling the adoption of logistics automation solutions, making India a rapidly developing destination for next-generation supply chain innovation.

Key Takeaways and Insights:

-

By Component: Software dominates the market with a share of 44% in 2025, driven by the increasing adoption of warehouse management systems, transportation management platforms, and cloud-based logistics solutions that enable real-time visibility and operational optimization across supply chains.

- By Function: Warehouse and storage management leads the market with a share of 60% in 2025, supported by the rising demand for automated inventory control, order processing efficiency, and optimized space utilization in fulfillment centers serving the rapidly expanding e-commerce sector.

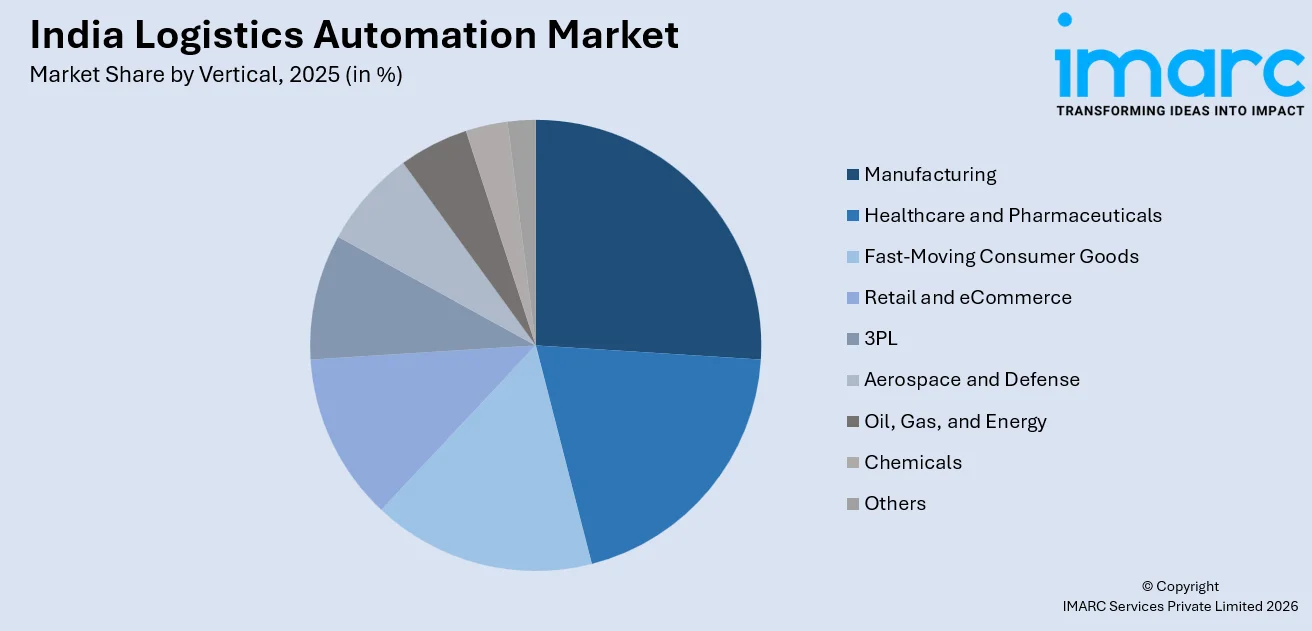

- By Vertical: Manufacturing holds the largest market share of 15% in 2025, reflecting the sector's emphasis on integrating automated material handling, production line logistics, and just-in-time inventory systems to meet growing industrial output demands.

- Key Players: The India logistics automation market exhibits a highly competitive landscape, with established multinational automation providers competing alongside emerging domestic technology firms across software solutions, hardware integration, warehouse automation, and end-to-end supply chain management services. Some of the key players operating in the market include ABB India Ltd. (ABB Ltd.), Beumer India Pvt Ltd. (Beumer Group), Daifuku Co. Ltd, Falcon Autotech Private Limited, Future Supply Chain Solutions Ltd, Hinditron Group of Companies, Inspirage, Mahindra Logistics Ltd., Muratec Machinery Ltd., SSI Schaefer AG. (Fritz Schäfer GmbH), and TCI Express Limited.

To get more information on this market Request Sample

The India logistics automation market is experiencing a transformative phase as businesses across sectors prioritize efficiency, accuracy, and scalability in their supply chain operations. The convergence of digital technologies with traditional logistics processes is creating a new paradigm where automated sorting systems, robotic picking solutions, and intelligent transportation management platforms are becoming standard components of modern warehouses and distribution networks. In 2026, Addverb, an Indian robotics and automation company, launched its latest humanoid industrial robot, Elixis‑W, at LogiMAT India, underscoring how home‑grown automation providers are pushing the boundaries of warehouse and supply chain robotics in the country. The rapid expansion of e-commerce, combined with rising consumer expectations for faster deliveries, is compelling logistics operators to invest in end-to-end automation solutions. Additionally, government initiatives focused on infrastructure modernization and digital transformation are providing a supportive environment for technology adoption. The growing availability of cloud-based platforms and software-as-a-service models is further lowering entry barriers, enabling small and medium enterprises to participate in the automation ecosystem and contribute to the broader market expansion.

India Logistics Automation Market Trends:

Accelerated Adoption of AI and Machine Learning in Supply Chains

Artificial intelligence and machine learning technologies are increasingly being integrated into logistics operations to enable predictive analytics, demand forecasting, and intelligent route optimization. For example, at the India International Cargo & Logistics Show (IICS) in 2025, Softlink Global highlighted its AI‑powered LogiBRAIN analytics layer, which is designed to provide predictive insights and real‑time visibility across freight operations, automating tasks like document processing and shipment forecasting to reduce manual intervention and improve decision‑making. These capabilities allow enterprises to anticipate supply chain disruptions, optimize inventory levels, and enhance delivery precision. The shift toward data-driven decision-making is transforming warehousing and transportation functions, improving overall operational agility and responsiveness in the India logistics automation market growth.

Rise of Autonomous Mobile Robots in Warehouse Operations

Autonomous mobile robots are gaining traction across Indian warehouses and distribution centers, enabling efficient goods-to-person picking, sorting, and internal transportation. For instance, an Ahmedabad‑based robotics startup secured a major contract to deploy over 500 Autonomous Mobile Robots (AMRs) across several large logistics hubs, including facilities in Hyderabad, Bhiwandi, and Ahmedabad, highlighting how domestic robotics firms are rapidly scaling AMR deployments to meet India’s warehousing automation needs. These robotic systems reduce manual handling requirements, minimize errors, and significantly increase throughput capacity. Their deployment is being driven by the growing need for scalable and flexible automation solutions that can adapt to fluctuating order volumes and seasonal demand peaks.

Expansion of Cloud-Based Logistics Platforms

Cloud-based logistics management platforms are witnessing widespread adoption across India, offering real-time visibility, centralized control, and seamless integration across multiple supply chain nodes. In February 2025, Allcargo Gati migrated its mission‑critical ERP and control‑tower operations to Oracle Cloud Infrastructure, improving system performance and operational efficiency by about 20 percent and enabling real‑time data tracking across its fleet through cloud integration. These platforms enable businesses to scale operations efficiently, enhance collaboration between stakeholders, and leverage advanced analytics for continuous performance improvement. The transition to cloud infrastructure is particularly accelerating among mid-sized logistics providers seeking cost-effective automation pathways.

Market Outlook 2026-2034:

The Indian logistics automation market is expected to grow at a steady pace, driven by the increasing digitization of supply chain networks, smart warehousing investments, and the need for complete logistics visibility. The growing e-commerce industry, along with the government's efforts to reduce logistics costs and upgrade logistics infrastructure, is expected to create a positive influence on the adoption of automation in the industry. Technological developments in robotics, sensors, and software solutions are expected to increase operational efficiencies and create a competitive logistics environment in the country. The market generated a revenue of USD 2,181.07 Million in 2025 and is projected to reach a revenue of USD 8,010.64Million by 2034, growing at a compound annual growth rate of 15.55% from 2026-2034.

India Logistics Automation Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Software |

44% |

|

Function |

Warehouse and Storage Management |

60% |

|

Vertical |

Manufacturing |

15% |

Component Insights:

- Software

- Hardware Integrated System

- Services

The software dominates with a market share of 44% of the total India logistics automation market in 2025.

Software solutions are the primary drivers of logistics automation in the Indian market, as more and more businesses adopt sophisticated warehouse management solutions, transportation management systems, and supply chain analytics tools. Software solutions allow for real-time tracking of consignments, automated inventory replenishment, and demand-driven planning, thereby increasing accuracy and efficiency in logistics operations. The trend of adopting cloud-based and software-as-a-service solutions is also widening the adoption base among businesses of different sizes and complexity.

The increasing complexity of multi-channel logistics networks and the need for seamless connectivity between warehousing, transportation, and last-mile delivery are driving the adoption of comprehensive software solutions. Businesses are adopting modular and scalable software solutions that enable end-to-end logistics management, predictive analytics, and dynamic route optimization. This trend is further emphasizing the importance of software as a key driver of change in the Indian logistics industry.

Function Insights:

- Warehouse and Storage Management

- Transportation Management

The warehouse and storage management leads with a share of 60% of the total India logistics automation market in 2025.

Warehouse and storage management solutions currently command a dominant market share, which is a testament to the pivotal importance of automated warehousing solutions in enabling the growing e-commerce market in India. Automated storage and retrieval systems, robotic picking systems, and intelligent inventory management solutions are being increasingly adopted in modern fulfillment centers to improve processing capacity, cut processing times, and eliminate order discrepancies. The growing need for faster delivery times is also fueling continued investment in warehouse automation solutions.

The growing trend of multi-tier warehousing and the increasing focus on space optimization are also fueling the adoption of advanced storage management solutions. Organizations are increasingly adopting automated conveyor systems, goods-to-person systems, and digital twin simulations to optimize warehouse layouts and operations. This continued investment in warehousing infrastructure is poised to make the function the key growth driver for the overall India logistics automation market.

Vertical Insights:

Access the comprehensive market breakdown Request Sample

- Manufacturing

- Healthcare and Pharmaceuticals

- Fast-Moving Consumer Goods

- Retail and eCommerce

- 3PL

- Aerospace and Defense

- Oil, Gas, and Energy

- Chemicals

- Others

The manufacturing dominates with a market share of 15% of the total India logistics automation market in 2025.

The manufacturing sector is at the forefront of logistics automation adoption in India, driven by the imperative to streamline production line logistics, enhance material handling efficiency, and support just-in-time inventory management. According to the latest World Robotics data, India’s installed base of industrial robots reached a record level in 2024, placing the country among the top industrial robot adopters globally and underscoring accelerating automation adoption across manufacturing facilities. Automated guided vehicles, robotic palletizing systems, and integrated manufacturing execution platforms are being deployed to reduce lead times, minimize production bottlenecks, and improve overall supply chain responsiveness across diverse industrial operations throughout the country.

The expanding manufacturing base, supported by government initiatives to boost domestic production capacity, is creating sustained demand for intelligent logistics solutions that connect inbound material flows with outbound distribution networks. Manufacturers are increasingly adopting integrated automation platforms that provide end-to-end visibility across procurement, production, and distribution processes. This holistic approach to supply chain automation is enabling manufacturers to achieve higher operational efficiency and effectively meet growing domestic and export demand.

Regional Insights:

- North India

- West and Central India

- East India

- South India

North India is witnessing growing adoption of logistics automation driven by expanding industrial corridors, increasing warehousing capacity, and rising demand for efficient freight movement across key manufacturing and consumption hubs. The development of dedicated freight networks and modernization of distribution infrastructure are further strengthening the region's logistics capabilities, enabling enterprises to achieve greater supply chain efficiency and operational scalability.

West and Central India leads automation adoption, supported by strong port-based logistics networks, thriving manufacturing clusters, and a concentration of modern warehousing facilities catering to both domestic distribution and international trade operations. The region's strategic positioning as a major commercial and industrial gateway continues to attract significant investments in advanced automation technologies and smart logistics infrastructure.

East India is gradually embracing logistics automation as infrastructure development initiatives, dedicated freight corridors, and expanding industrial activity create new opportunities for technology-enabled supply chain solutions. Growing investments in warehousing modernization and transportation connectivity are enhancing the region's logistics readiness, supporting broader automation adoption across manufacturing, mining, and agricultural supply chain operations.

South India is a key automation hub, driven by a strong technology ecosystem, established automotive and pharmaceutical manufacturing clusters, and growing investments in smart warehousing and automated distribution center infrastructure. The region's skilled workforce availability and proximity to major port facilities further reinforce its position as a leading destination for advanced logistics automation deployment and innovation.

Market Dynamics:

Growth Drivers:

Why is the India Logistics Automation Market Growing?

Rapid Expansion of E-Commerce and Direct-to-Consumer Channels

The exponential growth of e-commerce and direct-to-consumer distribution channels in India is fundamentally reshaping logistics requirements and driving unprecedented demand for automation solutions. The India e‑commerce market was valued at USD 129.72 Billion in 2025, reflecting the massive scale of online retail and the corresponding need for efficient, technology-driven supply chains. Online retail platforms are experiencing consistently rising order volumes, with consumers expecting faster deliveries, accurate order fulfillment, and seamless returns processing. These expectations necessitate highly automated warehousing environments where robotic picking, automated sorting, and intelligent packaging systems operate in coordination to meet demanding throughput targets. The proliferation of quick-commerce models, which promise delivery within minutes, is further intensifying the need for hyperlocal automated fulfillment centers strategically positioned across urban areas.

Rising Labor Costs and Workforce Availability Challenges

Increasing labor costs and the growing difficulty in recruiting and retaining skilled warehouse and logistics workers are compelling enterprises to accelerate their automation investments. The repetitive and physically demanding nature of manual logistics operations leads to high employee turnover, inconsistent productivity levels, and elevated training expenditures. During the 2025 Diwali peak, several Indian 3PL providers reported acute worker shortages and strain on supply chains, with executives noting that limited manpower availability at warehouses, despite proactive planning, intensified operational pressure and highlighted the need for automation solutions to sustain timely fulfillment. Automation technologies offer a compelling alternative by delivering consistent performance, operating continuously without fatigue, and maintaining high accuracy levels regardless of workload fluctuations. Furthermore, the seasonal nature of logistics demand, particularly during festive periods and major sales events, creates acute labor shortages that automated systems can effectively address. By reducing dependency on manual processes, enterprises achieve greater operational predictability, improved workplace safety, and enhanced ability to scale operations in response to market demand without proportional increases in workforce requirements. This structural shift toward automation is becoming a fundamental strategic priority across Indian logistics operations.

Government Initiatives Supporting Infrastructure Modernization

Comprehensive government initiatives aimed at modernizing India's logistics infrastructure are creating a highly favorable environment for automation adoption. According to reports, the integration of 36 logistics‑related digital systems across eight ministries on the Unified Logistics Interface Platform (ULIP) provides real‑time data on more than 1,800 logistics fields, enabling seamless information flow and faster decision‑making for supply chain operations, which is a foundational step toward digital automation. National policies focused on reducing logistics costs as a percentage of economic output are encouraging enterprises to invest in technology-driven solutions that improve efficiency and reduce waste across supply chain networks. The development of dedicated freight corridors, multimodal logistics parks, and industrial corridors is providing the physical infrastructure foundation upon which automated logistics systems can be deployed effectively. Additionally, digital transformation programs promoting paperless transactions, electronic documentation, and unified logistics platforms are streamlining regulatory processes and enabling seamless integration of automated systems.

Market Restraints:

What Challenges the India Logistics Automation Market is Facing?

High Initial Capital Investment Requirements

The substantial upfront capital expenditure required for implementing comprehensive logistics automation systems presents a significant barrier, particularly for small and medium enterprises with constrained budgets. Advanced robotic systems, automated storage infrastructure, and integrated software platforms demand considerable financial commitment, along with ongoing maintenance and upgrade costs. The extended payback periods associated with full-scale automation projects can deter organizations from pursuing transformative investments, slowing broader market penetration.

Integration Complexity with Legacy Systems

Many Indian logistics operators continue to rely on legacy infrastructure and traditional operational processes that are not readily compatible with modern automation technologies. Integrating advanced automated solutions with existing warehouse management systems, enterprise resource planning platforms, and transportation networks often involves significant technical complexity and operational disruption. The lack of standardized protocols and interoperability frameworks across different technology vendors further complicates seamless system integration, creating implementation challenges.

Shortage of Skilled Technical Workforce

The limited availability of professionals with specialized expertise in robotics, automation engineering, artificial intelligence, and advanced logistics technologies constrains the pace of automation adoption. Operating and maintaining sophisticated automated systems requires technical skills that remain scarce across the Indian workforce. The gap between industry requirements and available talent necessitates substantial investment in training and development programs, adding to overall implementation timelines and costs for organizations pursuing automation.

Competitive Landscape:

The India logistics automation market is characterized by a dynamic and increasingly competitive environment, with participants ranging from established global automation conglomerates to innovative domestic technology startups. The market structure reflects a blend of multinational enterprises offering comprehensive end-to-end automation platforms and specialized local providers developing solutions tailored to India-specific logistics challenges and operational requirements. Competition is intensifying as enterprises recognize the strategic importance of logistics automation, driving market players to differentiate through technological innovation, service quality, and implementation expertise. Strategic partnerships between technology providers and logistics operators are becoming increasingly prevalent, enabling collaborative development of customized solutions that address sector-specific needs. Market participants are also focusing on expanding their service portfolios to include consulting, system integration, and post-deployment support, creating more comprehensive value propositions. The growing emphasis on scalability, flexibility, and rapid deployment is reshaping competitive dynamics, with players that can demonstrate measurable return on investment and operational excellence gaining preferential positioning in procurement decisions.

Some of the key players include:

- ABB India Ltd. (ABB Ltd.)

- Beumer India Pvt Ltd. (Beumer Group)

- Daifuku Co. Ltd

- Falcon Autotech Private Limited

- Future Supply Chain Solutions Ltd

- Hinditron Group of Companies

- Inspirage

- Mahindra Logistics Ltd.

- Muratec Machinery Ltd.

- SSI Schaefer AG. (Fritz Schäfer GmbH)

- TCI Express Limited

Recent Developments:

- In January 2026, India’s logistics firm Delhivery has launched an AI‑driven TransportOne Transport Management System (TMS) that automates freight procurement, routing, execution monitoring and invoice reconciliation with minimal manual input, allowing natural‑language commands via WhatsApp and Microsoft Teams.

India Logistics Automation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Hardware Integrated System, Services |

| Functions Covered | Warehouse and Storage Management, Transportation Management |

| Verticals Covered | Manufacturing, Healthcare and Pharmaceuticals, Fast-Moving Consumer Goods, Retail and eCommerce, 3PL, Aerospace and Defense, Oil, Gas, and Energy, Chemicals, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | ABB India Ltd. (ABB Ltd.), Beumer India Pvt Ltd. (Beumer Group), Daifuku Co. Ltd, Falcon Autotech Private Limited, Future Supply Chain Solutions Ltd, Hinditron Group of Companies, Inspirage, Mahindra Logistics Ltd., Muratec Machinery Ltd., SSI Schaefer AG. (Fritz Schäfer GmbH) and TCI Express Limited |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Logistics Automation Market Report

The India logistics automation market size was valued at USD 2,181.07 Million in 2025.

The India logistics automation market is expected to grow at a compound annual growth rate of 15.55% from 2026-2034 to reach USD 8,010.64 Million by 2034.

Software, holding the largest share of 44%, remains pivotal for India's logistics automation landscape, enabling real-time supply chain visibility, intelligent inventory management, and seamless operational coordination across warehousing and transportation functions.

Key factors driving the India logistics automation market include rapid e-commerce expansion, rising labor costs, growing demand for supply chain efficiency, government infrastructure modernization initiatives, Industry 4.0 adoption, and increasing investments in robotic and AI-powered logistics solutions.

Major challenges include high initial capital investment requirements, integration complexity with legacy systems, shortage of skilled technical workforce, limited standardization across automation platforms, and uneven digital infrastructure readiness across different regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)