India Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Region, 2026-2034

India Logistics Market Size, Share, Trends & Forecast (2026-2034)

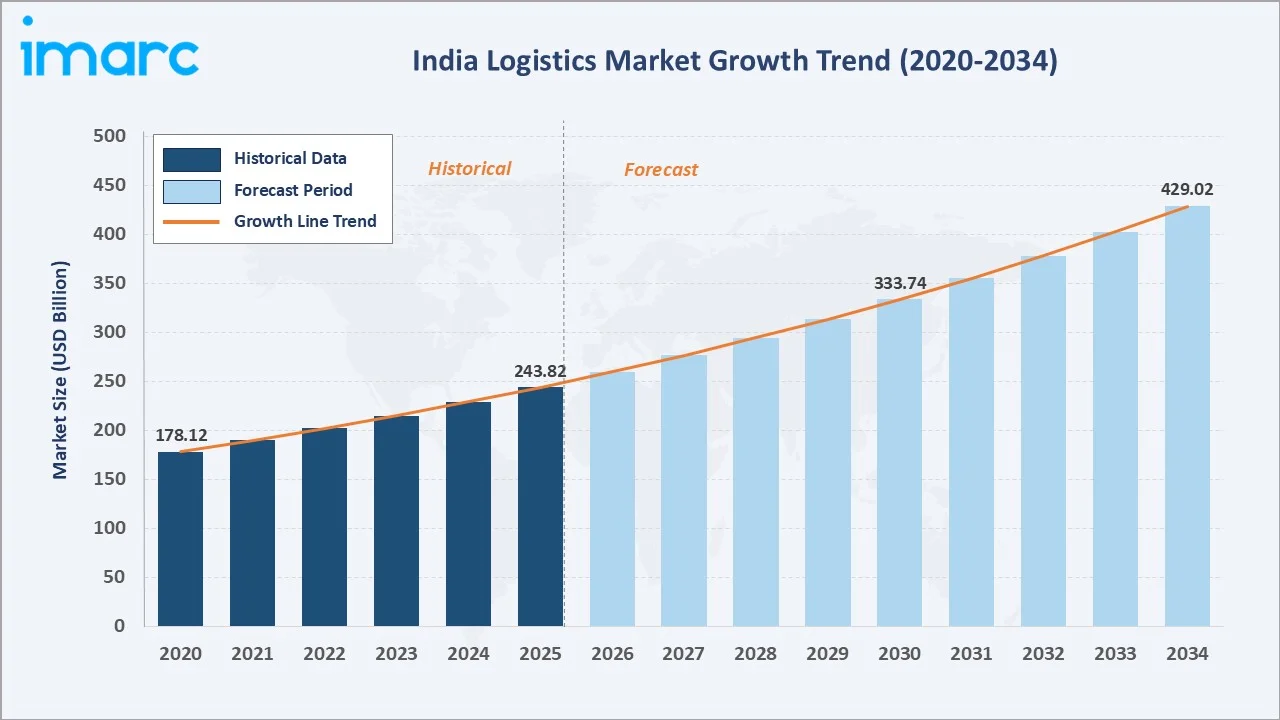

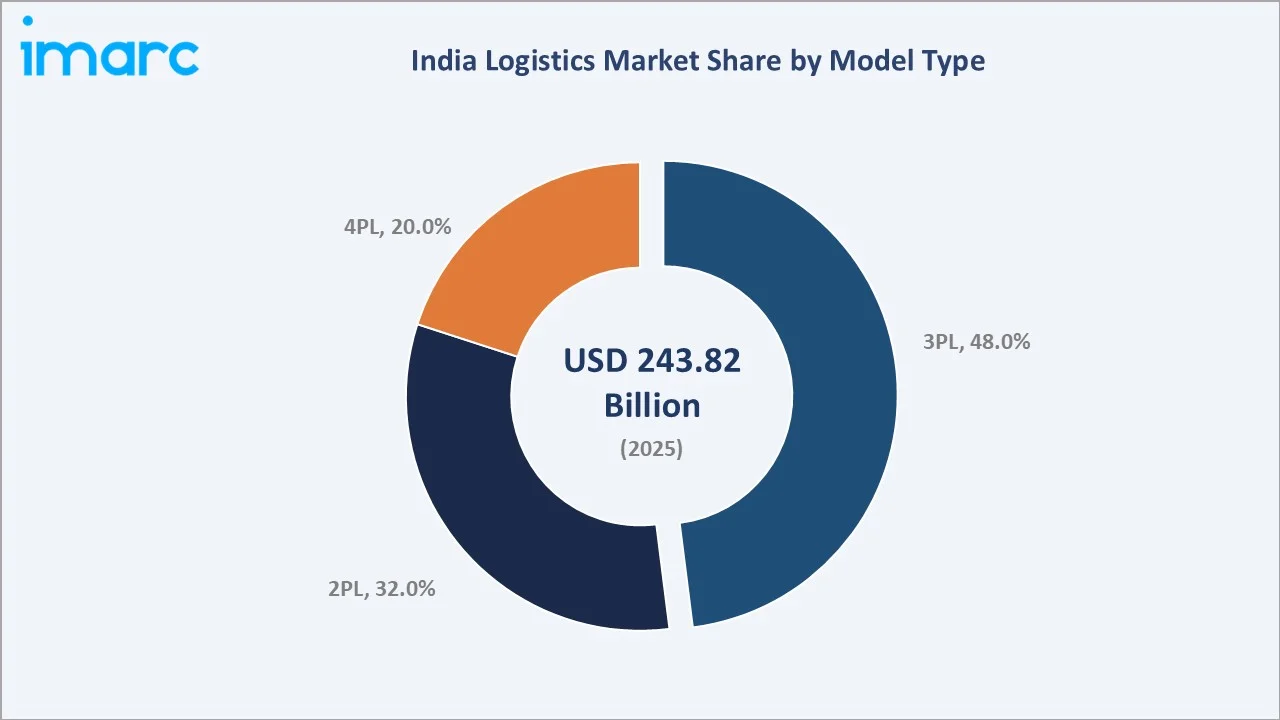

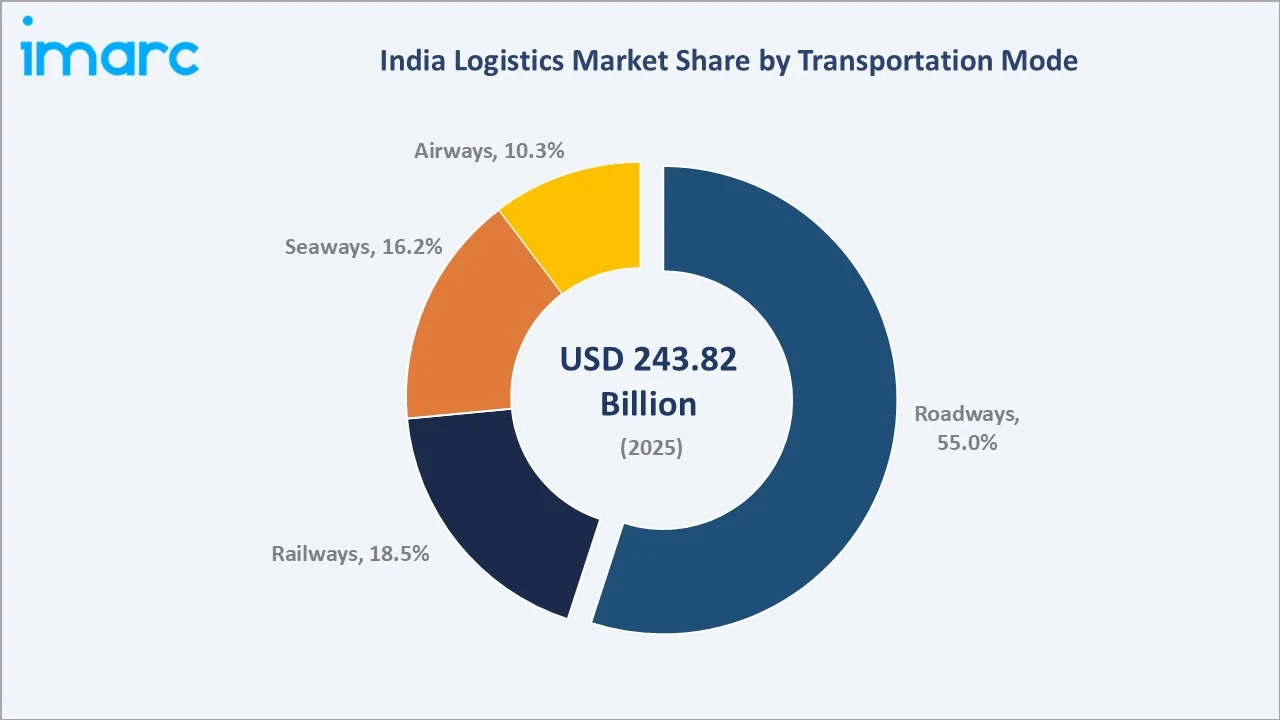

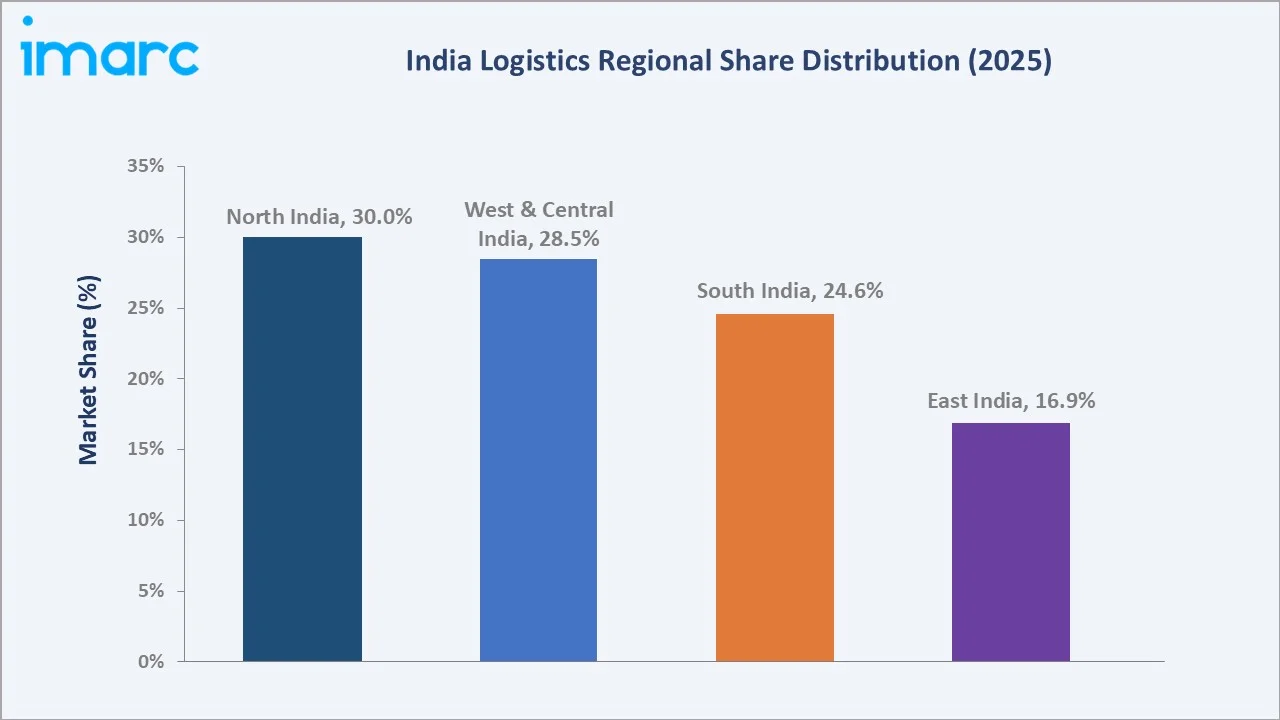

The India logistics market size reached USD 243.82 Billion in 2025 and is projected to touch USD 429.02 Billion by 2034, expanding at a CAGR of 6.48% during 2026-2034. Rapid e-commerce growth, the National Logistics Policy, manufacturing expansion under Make in India, and rising domestic consumption are powering market momentum. The 3PL segment leads model types with a 48.0% share in 2025, while Roadways dominates transportation with a 55.0% share. North India holds the largest regional share at 30.0% in 2025, anchored by NCR consumption clusters and northern industrial corridors.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 243.82 Billion |

|

Forecast Market Size (2034) |

USD 429.02 Billion |

|

CAGR (2026-2034) |

6.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (30.0% share, 2025) |

|

Fastest Growing Region |

West and Central India |

|

Leading Model Type |

3PL (48.0%, 2025) |

|

Leading Transportation Mode |

Roadways (55.0%, 2025) |

The chart below shows the India logistics market growth trajectory from 2020-2034, supported by post-pandemic recovery, infrastructure investment, and rising e-commerce activity.

To get more information on this market, Request Sample

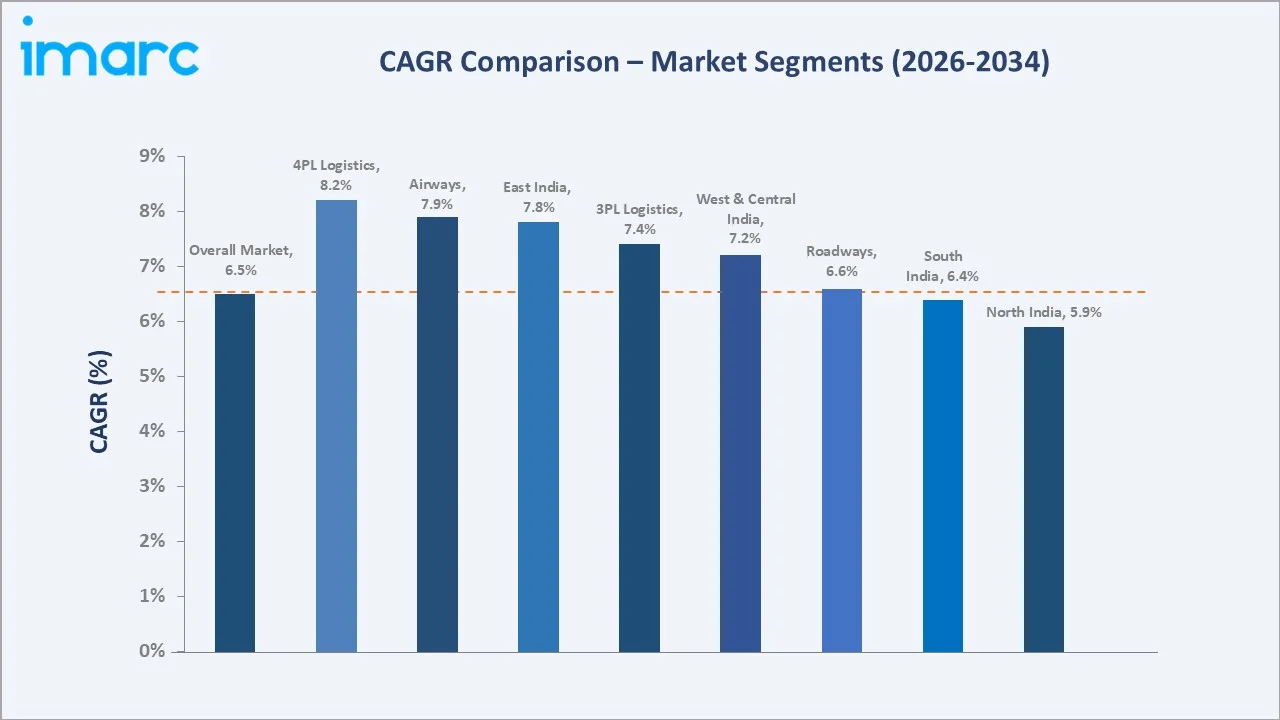

CAGR analysis identifies 4PL logistics and air cargo as the fastest-growing sub-segments, while 3PL and roadways continue to anchor overall market value through 2034.

Executive Summary

The India logistics market is undergoing structural transformation, driven by digital commerce, integrated infrastructure programs, and rising manufacturing output. Valued at USD 243.82 Billion in 2025, the market is forecast to reach USD 429.02 Billion by 2034, growing at a 6.48% CAGR. Rising organized retail penetration, formalization of supply chains, and government-led corridor projects are widening the addressable opportunity for service providers.

The 3PL segment commands a 48.0% share in 2025, supported by enterprise outsourcing across consumer goods, automotive, and pharma sectors. Roadways dominate transportation with a 55.0% share, reflecting last-mile flexibility and road network expansion. Key trends include warehouse automation, electric vehicle fleets in urban delivery, dedicated freight corridors, and rapid digitalization through control towers and AI-enabled visibility platforms.

North India leads the market with a 30.0% share in 2025, supported by NCR consumption density and Punjab-Haryana industrial output. West and Central India holds 28.5%, anchored by Mumbai, JNPT, and Gujarat ports. South India accounts for 24.6%, while East India holds 16.9%. The Indian government's Logistics Performance Index push and falling logistics cost-to-GDP ratio are reinforcing long-term competitiveness across regions.

Key Market Insights

|

Insight |

Data |

|

Largest Model Type Segment |

3PL - 48.0% share (2025) |

|

Second Model Type Segment |

2PL - 32.0% share (2025) |

|

Leading Transportation Mode |

Roadways - 55.0% share (2025) |

|

Leading Region |

North India - 30.0% (2025) |

|

Second Region |

West and Central India - 28.5% (2025) |

|

Top Companies |

Delhivery, Mahindra Logistics Ltd., Allcargo Logistics Limited, Blue Dart Express Limited, and TCIEXPRESS LIMITED. |

|

Market Opportunity |

Multimodal logistics parks and DFC-led freight rebalancing |

Key Analytical Observations Supporting the Data Points are Summarized Below.

- 3PL leadership at 48.0% in 2025 reflects accelerating outsourcing among Indian and multinational enterprises seeking warehousing scale, technology integration, and pan-India distribution capabilities not feasible through in-house teams.

- 2PL share of 32.0% in 2025 remains material in sectors with captive fleets such as cement, steel, and FMCG primary distribution, where direct fleet control protects service levels and route economics.

- Roadways dominance at 55.0% is supported by the 1.46 million-km national highway-state highway network and expanding e-commerce demand, where flexibility, door-to-door coverage, and fragmented loads favor trucking over rail.

- North India's 30.0% lead is anchored by NCR's consumption density, Ludhiana-Panipat manufacturing, and Inland Container Depot connectivity to JNPT and Mundra through Western DFC alignment.

- West and Central India at 28.5% is driven by strong cargo throughput at major ports like Jawaharlal Nehru Port (JNPT) and Mundra, along with Gujarat’s large chemical manufacturing base and Maharashtra’s automotive hub, supporting steady regional market growth.

India Logistics Market Overview

Logistics in India encompasses transportation, warehousing, freight forwarding, value-added services, and supply chain solutions across road, rail, air, and water. The ecosystem includes shippers, 3PL/4PL providers, ports, terminals, ICDs, customs brokers, technology platforms, and regulators such as DPIIT and the Ministry of Commerce.

End-use applications span e-commerce, retail, automotive, pharmaceuticals, FMCG, agriculture, chemicals, and engineering goods. Growth drivers include the National Logistics Policy targeting cost reduction to under 9% of GDP, PM Gati Shakti coordination, GST-driven warehouse consolidation, and continued urbanization across Tier-2 and Tier-3 cities.

Market Dynamics

To evaluate market opportunities, Request Sample

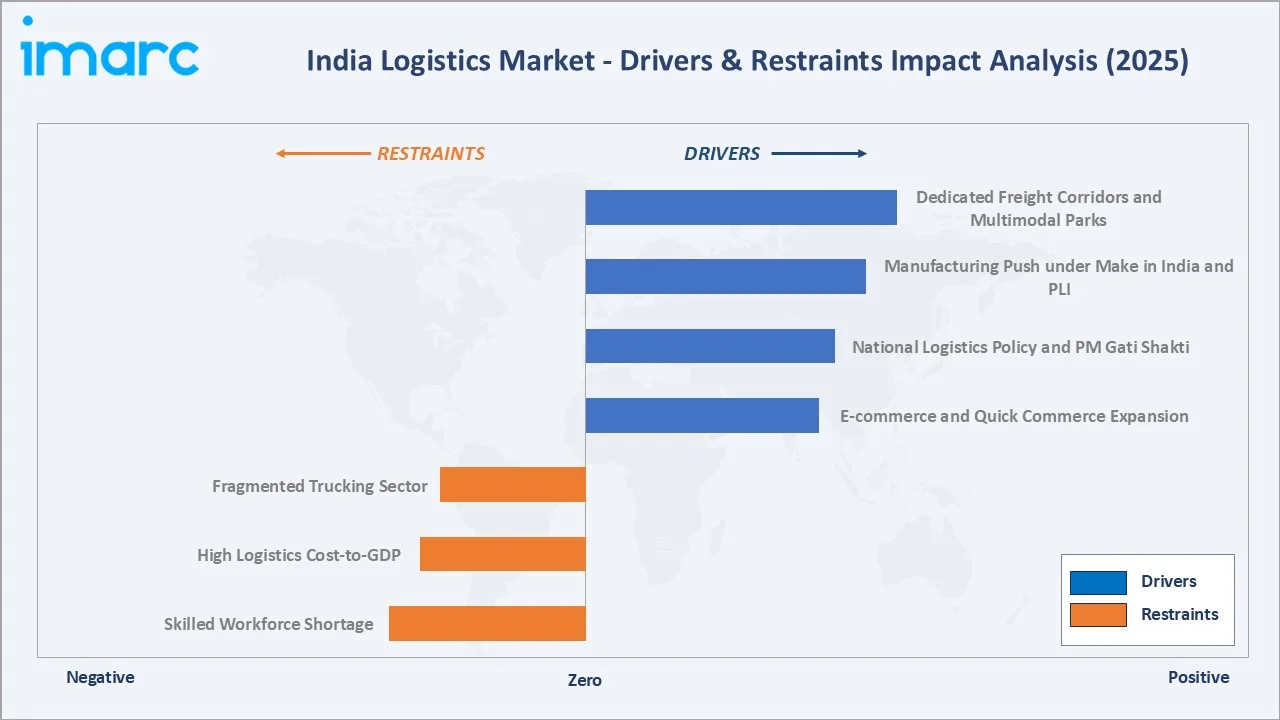

Market Drivers

- E-commerce and Quick Commerce Expansion: India's e-commerce gross merchandise value crossed USD 125 Billion in 2024, fueling demand for warehousing, sortation hubs, and last-mile networks across metros and Tier-2 cities.

- National Logistics Policy and PM Gati Shakti: Coordinated infrastructure planning across 16 ministries is unlocking faster project execution, integrated transport corridors, and a Unified Logistics Interface Platform improving visibility and efficiency.

- Manufacturing Push under Make in India and PLI: Production-linked incentive schemes worth USD 26 Billion across 14 sectors are expanding factory output, multiplying inbound and outbound freight volumes for organized logistics service providers.

- Dedicated Freight Corridors and Multimodal Parks: The 2,843-km DFC network and over 35 planned multimodal logistics parks under Bharatmala are shifting freight share toward rail and integrated parks, lowering per-tonne logistics cost.

Market Restraints

- Fragmented Trucking Sector: Over 75% of road freight capacity sits with operators owning fewer than five trucks, creating utilization, compliance, and digital adoption gaps that constrain network optimization.

- High Logistics Cost-to-GDP: Logistics costs in India are estimated near 13-14% of GDP, materially higher than the 8-9% seen in mature economies, weighing on export competitiveness and shipper margins.

- Skilled Workforce Shortage: Demand for warehouse automation engineers, transport managers, and supply chain analysts is outpacing supply, limiting the pace of technology rollouts at mid-tier 3PL operators.

Market Opportunities

- Cold Chain Expansion: India's cold chain capacity gap exceeds 30 million tonnes for perishables and pharmaceuticals, opening multi-billion-dollar greenfield investment opportunity for integrated cold logistics players.

- Electric and Green Logistics: EV-led last-mile fleets, solar-powered warehouses, and rail modal shift can cut emissions and operating costs, attracting ESG-aligned capital from Indian and global infrastructure funds.

- Rural and Tier-3 Penetration: Rising rural disposable income and Bharat e-commerce orders are pulling logistics networks into smaller towns, where Delhivery, Ecom Express, and India Post are scaling delivery infrastructure.

Market Challenges

- Regulatory and Tax Complexity: Despite GST harmonization, varied state-level permits, RTO checks, and e-way bill compliance still slow long-haul movements and add hidden costs to multi-state freight planning.

- Diesel Volatility and Margin Pressure: Diesel prices contribute 50-55% of trucking operating cost, exposing fleet operators to fuel-driven margin compression and elevating the appeal of CNG, LNG, and EV alternatives.

- Infrastructure Bottlenecks at Ports and Cities: Urban congestion, delayed dwell times at major ports, and limited night-time warehousing capacity continue to constrain throughput growth in dense corridors.

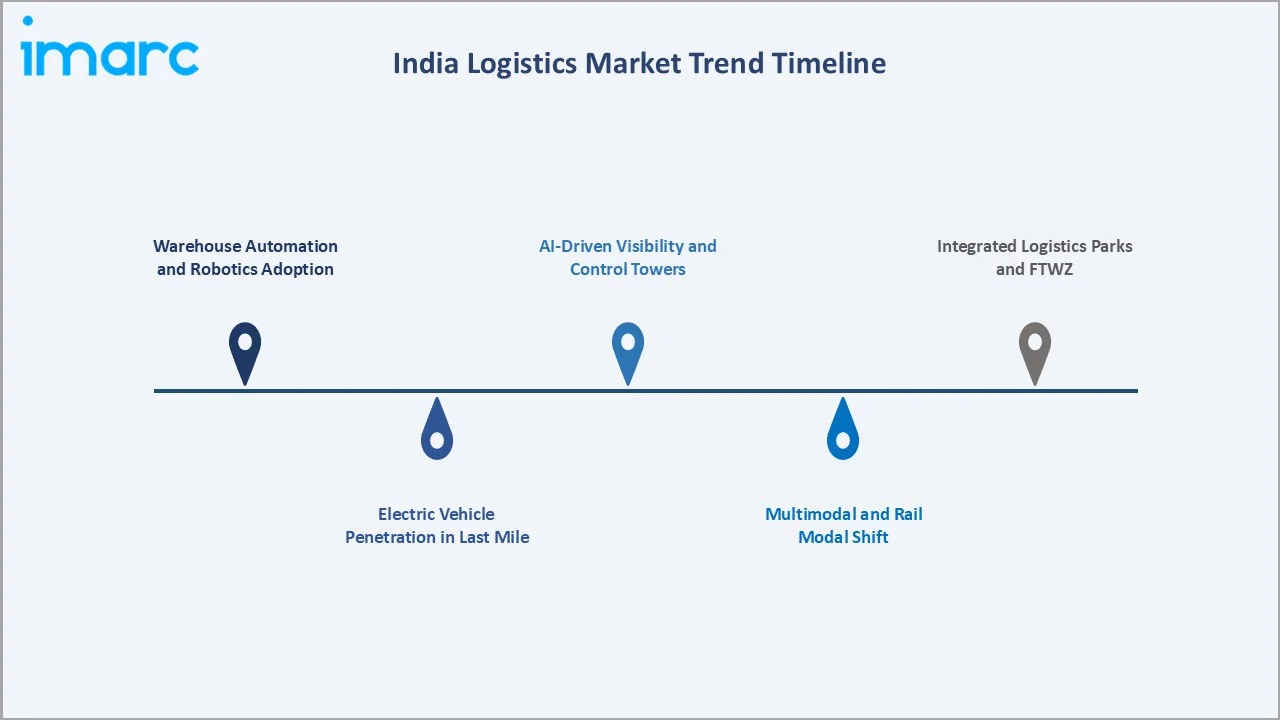

Emerging Market Trends

1. Warehouse Automation and Robotics Adoption

Automation in fulfilment centers is expanding, with companies like Delhivery, Flipkart, and Amazon India deploying robotics and sortation systems to improve efficiency, accuracy, and faster order processing across large warehouses.

2. Electric Vehicle Penetration in Last Mile

Last-mile EV adoption is rising in India, supported by government incentives under FAME II, with logistics players increasingly deploying electric two- and three-wheelers to reduce delivery costs and emissions in urban distribution networks.

3. Multimodal and Rail Modal Shift

The Eastern and Western Dedicated Freight Corridors are improving rail freight reliability and transit times. Container rail volumes are expected to expand at over 8% annually, gradually rebalancing the road-to-rail mix in long-haul lanes.

4. AI-Driven Visibility and Control Towers

Logistics companies are adopting AI-enabled platforms integrating telematics, GPS, and enterprise systems to enhance shipment visibility, optimize routes, and improve delivery timelines, supporting more efficient and data-driven supply chain operations across India.

5. Integrated Logistics Parks and Free Trade Warehousing Zones

Government initiatives like Bharatmala Pariyojana and FTWZ development are promoting integrated logistics parks with multimodal connectivity, warehousing, and customs infrastructure, attracting manufacturing and export-oriented supply chains.

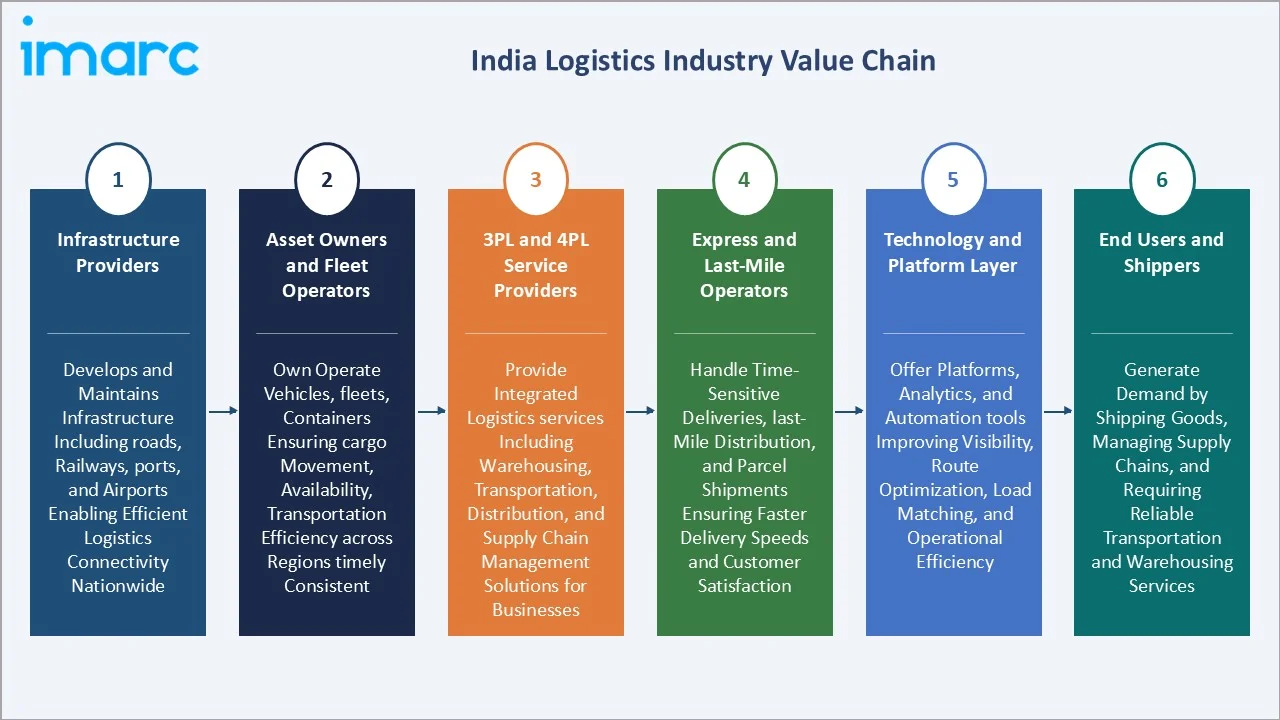

Industry Value Chain Analysis

The India logistics value chain spans six interconnected stages, each with distinct competitive dynamics, asset intensity, and margin structures shaping supplier-customer relationships.

|

Stage |

Key Players / Examples |

|

Infrastructure Providers |

Develops and maintains infrastructure including roads, railways, ports, and airports enabling efficient logistics connectivity nationwide |

|

Asset Owners and Fleet Operators |

Own operate vehicles, fleets, containers ensuring cargo movement, availability, transportation efficiency across regions timely consistent |

|

3PL and 4PL Service Providers |

Provide integrated logistics services including warehousing, transportation, distribution, and supply chain management solutions for businesses |

|

Express and Last-Mile Operators |

Handle time-sensitive deliveries, last-mile distribution, and parcel shipments ensuring faster delivery speeds and customer satisfaction |

|

Technology and Platform Layer |

Offer platforms, analytics, and automation tools improving visibility, route optimization, load matching, and operational efficiency |

|

End Users and Shippers |

Generate demand by shipping goods, managing supply chains, and requiring reliable transportation and warehousing services |

Integrated 3PL operators capture the highest value position by combining warehousing, transport, technology, and customs services. Their scale enables superior asset utilization unmatched by smaller asset-light or single-mode players.

Technology Landscape in the India Logistics Industry

AI-Powered Routing and Demand Forecasting

AI-based logistics platforms from Locus and Shipsy optimize routing, load planning, and ETA predictions, improving delivery efficiency and reducing empty miles, though exact percentage reductions vary by operator and use case.

Warehouse Management Systems and Automation

Cloud-based WMS and warehouse automation technologies are expanding across Grade-A warehousing hubs in India, driven by e-commerce and 3PL demand, with increasing adoption of conveyor systems and smart picking solutions in modern logistics parks.

IoT, Telematics, and Cold Chain Monitoring

IoT-enabled telematics, including GPS and temperature sensors, are increasingly used in cold chain logistics for pharmaceuticals and perishables, improving shipment visibility, regulatory compliance, and reducing spoilage risks during transportation across India.

Blockchain, ULIP, and Digital Documentation

The Unified Logistics Interface Platform (ULIP) integrates multiple government systems to enable paperless logistics, while blockchain pilots at ports enhance transparency and efficiency in documentation and trade processes.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | 3 PL | 48.0% | 2025 |

| Transportation Mode | Roadways | 55.0% | 2025 |

| End Use | Manufacturing | 18.0% | 2025 |

| Region | North India | 30.0% | 2025 |

By Model Type

3PL services lead the India logistics market with a 48.0% share in 2025, driven by enterprise outsourcing across e-commerce, automotive, FMCG, and pharma. Operators provide integrated warehousing, transportation, and value-added services at national scale.

To access detailed market analysis, Request Sample

The 2PL segment holds 32.0% in 2025, dominated by captive fleets in cement, steel, and primary FMCG distribution where shippers retain transport assets to control reliability, route economics, and brand-sensitive last-mile delivery. 4PL services account for 20.0% in 2025 and represent the fastest-growing model, projected to expand at over 8% CAGR through 2034 as large multinationals adopt single-window orchestration partners managing multi-3PL ecosystems and digital control towers.

By Transportation Mode

Roadways command 55.0% of the India logistics market in 2025, anchored by extensive highway coverage, last-mile flexibility, and the dominance of road freight in e-commerce, agriculture, and consumer goods movements across all regions.

Railways hold 18.5% in 2025, used heavily for bulk commodities such as coal, cement, and containers. The Western and Eastern DFCs are expected to lift rail's share over the forecast period through reliable, faster long-haul transit. Seaways represent 16.2% in 2025, supported by major ports including JNPT, Mundra, Chennai, and Visakhapatnam collectively handle significant cargo volumes, total cargo handled across all Indian major ports stood at approximately 817 million tonnes in FY 2023–24. Airways at 10.3% are growing rapidly, fueled by high-value e-commerce, pharma exports, and express trade.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

30.0% |

Delhi NCR consumption density, Ludhiana-Panipat manufacturing, growing ICDs |

|

West and Central India |

28.5% |

JNPT and Mundra port throughput, Gujarat chemicals belt, Maharashtra auto cluster, MMR e-commerce hubs |

|

South India |

24.6% |

Electronics manufacturing, Chennai and Visakhapatnam port hubs |

|

East India |

16.9% |

Paradip and Haldia port expansion, mining and steel logistics, Northeast connectivity |

North India commands a 30.0% share of the India logistics market in 2025, supported by NCR demand density, agricultural belts, and a growing concentration of Grade-A warehousing parks at Bhiwandi, Farukhnagar, and Luhari nodes.

West and Central India holds 28.5% in 2025 and is the fastest-growing regional sub-market, fueled by JNPT and Mundra port volumes, Gujarat's industrial belt, and rising auto and chemical exports through 2034. South India at 24.6% benefits from electronics manufacturing growth and the Chennai-Bengaluru-Hyderabad corridor, while East India at 16.9% is rising on Eastern DFC operationalization, mining freight, and Paradip-Haldia port expansion.

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Delhivery |

Delhivery, Delhivery Direct |

Leader |

Pan-India network, automation, e-commerce scale |

|

Mahindra Logistics Ltd. |

Mahindra Logistics |

Leader |

Auto and enterprise 3PL, mobility services |

|

Allcargo Logistics Limited |

Allcargo Gati |

Leader |

LCL consolidation, multimodal, express |

|

Blue Dart Express Limited |

Blue Dart |

Challenger |

Premium air express, e-commerce B2C |

|

TCIEXPRESS LIMITED. |

TCIEXPRESS |

Challenger |

Express SCM, sorting hubs, tier-2 reach |

The India logistics market is led by a mix of national 3PL leaders, multinational integrators, and asset-heavy public-sector operators. Delhivery reported revenue of around USD 1 Billion in FY2025, while CONCOR handled 3.64 million TEUs, illustrating scale at the top of the industry.

Key Company Profiles

Delhivery

Delhivery is a Gurugram-based integrated logistics provider offering parcel, freight, and supply chain services across India. It reported FY25 revenue of about ₹89,319 million (~USD 1.03 billion) and operates a large nationwide network serving e-commerce and enterprise customers.

- Service Portfolio: Delhivery provides express parcel delivery, part-truckload and full-truckload freight, warehousing, supply chain services, and cross-border logistics solutions across e-commerce and enterprise segments.

- Recent Developments: In 2025, Delhivery launched its on-demand intracity service, Delhivery Direct, in Delhi-NCR and Bengaluru, enabling pickups within 15 minutes via a mobile app. The service caters to individuals and small businesses, using two-, three-, and four-wheelers to support fast, flexible, and reliable citywide deliveries.

- Strategic Focus: Delhivery focuses on network optimization, automation, EV adoption, and expanding B2B freight and cross-border logistics to improve profitability and scale.

Mahindra Logistics Ltd.

Mahindra Logistics, headquartered in Mumbai, is a leading asset-light third-party logistics provider offering integrated supply chain solutions across industries. The company reported FY25 revenue of about ₹61,050 million, supported by nationwide transportation and warehousing operations.

- Service Portfolio: Mahindra Logistics provides contract logistics, warehousing, transportation, freight forwarding, last-mile delivery, and mobility solutions across automotive, e-commerce, and industrial sectors.

- Recent Developments: In 2024, Mahindra Logistics strengthened its EV-led last-mile delivery operations through its eDeL platform, expanding deployment of electric fleets across multiple cities to support sustainable logistics. The company scaled IoT-enabled EV networks, improving efficiency, lowering emissions, and supporting enterprise customers with green delivery solutions.

- Strategic Focus: Asset-light expansion, EV-led mobility solutions, integrated warehousing, and technology-driven supply chain optimization for enterprise customers.

Allcargo Logistics Limited

Allcargo Logistics Limited, headquartered in Mumbai, is a global multimodal logistics provider operating through Allcargo Gati.

- Service Portfolio: Multimodal transport, LCL/FCL consolidation, express distribution, contract logistics, container freight stations, and logistics infrastructure services.

- Recent Developments: In 2025, Allcargo Logistics strengthened its India network by expanding operations to 71 locations, improving regional connectivity and turnaround efficiency. Its express arm, Allcargo Gati, also enhanced capacity and service reliability to support rising B2B and e-commerce logistics demand across the country.

- Strategic Focus: Allcargo focuses on global LCL leadership, scaling express logistics through Gati, expanding multimodal infrastructure, and strengthening integrated cross-border logistics capabilities.

Market Concentration Analysis

The India logistics market is moderately fragmented at the national level, with the top players estimated to hold 18-22% of organized market revenue in 2025. Delhivery, Mahindra Logistics Ltd., Allcargo Logistics Limited, and Blue Dart Express Limited, anchor the leadership tier through scale, technology, and integrated networks.

Fragmentation is deeper in trucking and small parcel segments, where over 75% of fleet capacity sits with operators owning fewer than five vehicles. This long tail constrains digitalization but also creates aggregator opportunities for technology-led platforms.

Consolidation is accelerating through acquisitions and joint ventures. Delhivery's Spoton integration and Allcargo's Gati restructuring exemplify the playbook of leaders absorbing regional specialists to deepen B2B PTL, express, and contract logistics capabilities.

Investment & Growth Opportunities

Fastest-Growing Segments

4PL and contract logistics services are projected to grow at over 8% CAGR through 2034, driven by enterprise demand for orchestration, control towers, and tech-enabled visibility. Air cargo and cold chain services follow, supported by pharma exports and quick commerce.

Emerging Markets and Geographies

Tier-2 and Tier-3 cities, North-East corridors, and the Eastern DFC catchment offer high-growth opportunities. Investment-friendly states like Gujarat, Maharashtra, Tamil Nadu, and Telangana continue to attract greenfield warehousing parks and multimodal projects.

Venture and Strategic Investment Trends

India’s logistics technology sector has attracted significant investments, with funding directed toward digital freight, supply chain platforms, and last-mile solutions, including companies like BlackBuck, Shadowfax, Locus, and Freight Tiger.

Future Market Outlook (2026-2034)

The India logistics market is expected to expand from USD 243.82 Billion in 2025 to USD 429.02 Billion by 2034 at a CAGR of 6.48%, adding more than USD 185 Billion in value. Growth will be powered by infrastructure modernization, e-commerce scale, manufacturing expansion, and accelerating outsourcing across enterprise segments.

Three transformations will reshape the industry through 2034. First, digitalization through ULIP, GPS tracking, and AI-driven planning will compress logistics cost-to-GDP toward 9%. Second, multimodal corridor maturity will rebalance modal share, lifting rail and coastal shipping. Third, sustainability mandates and EV adoption will redefine fleet economics.

By 2034, India's logistics industry is expected to evolve into a digitally integrated, multimodal, and sustainability-led ecosystem. Operators investing in automation, EV fleets, integrated parks, and AI platforms will capture disproportionate value across e-commerce, manufacturing, and global trade flows.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024-2025 with senior supply chain officers at Indian and multinational shippers, leadership at major 3PL/4PL operators, port and rail authorities, freight forwarders, and logistics technology platform executives.

Secondary Research

Secondary sources include annual reports of Delhivery, Mahindra Logistics Ltd., Allcargo Logistics Limited, Blue Dart Express Limited, and TCIEXPRESS LIMITED, government data from DPIIT, Ministry of Road Transport, Indian Railways, MoPSW, and DGCA, plus publications from CII, FICCI, the World Bank LPI, and industry trade media.

Forecasting Models

Market size and forecasts use a combination of top-down and bottom-up modeling, integrating GDP growth, manufacturing output, e-commerce GMV, port traffic, modal split, and corridor-level investment under base, optimistic, and conservative macroeconomic scenarios.

India Logistics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Model Types Covered | 2 PL, 3 PL, 4 PL |

| Transportation Modes Covered | Roadways, Seaways, Railways, Airways |

| End Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Delhivery, Mahindra Logistics Ltd., Allcargo Logistics Limited, Blue Dart Express Limited, TCIEXPRESS LIMITED., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Logistics Market Report

The India logistics market was valued at USD 243.82 Billion in 2025, supported by e-commerce expansion, manufacturing growth, and rapid infrastructure investment under PM Gati Shakti and the National Logistics Policy.

The India logistics market is projected to reach USD 429.02 Billion by 2034, expanding at a CAGR of 6.48% during 2026-2034, fueled by digitalization, modal shift, and outsourcing penetration.

3PL services lead the India logistics market with a 48.0% share in 2025, driven by enterprise outsourcing across e-commerce, automotive, FMCG, and pharmaceuticals seeking integrated warehousing and transport solutions.

Roadways dominate the India logistics market with a 55.0% share in 2025, supported by extensive highway connectivity, last-mile flexibility, and the dominant role of trucking in e-commerce and consumer goods movement.

North India leads the India logistics market with a 30.0% share in 2025, driven by NCR consumption, Punjab-Haryana manufacturing, and growing Inland Container Depot connectivity to western coast ports.

Key drivers include e-commerce growth, the National Logistics Policy, Make in India and PLI manufacturing schemes, dedicated freight corridors, multimodal parks, and accelerating outsourcing to 3PL and 4PL specialists.

West and Central India is the fastest-growing region, supported by JNPT and Mundra port volumes, Gujarat's chemical and engineering exports, and Maharashtra's auto and e-commerce demand through 2034.

Leading companies include Delhivery, Mahindra Logistics Ltd., Allcargo Logistics Limited, Blue Dart Express Limited, and TCIEXPRESS LIMITED.

4PL services hold a 20.0% share in 2025 and represent the fastest-growing model type, driven by demand for orchestration, control towers, and integrated digital supply chain platforms among large enterprises.

3PL growth is driven by enterprise outsourcing, GST-led warehouse consolidation, demand for automation, e-commerce scale, and access to technology, networks, and compliance handling unavailable in-house.

E-commerce and retail represent one of the largest end-use segments, supported by over USD 125 Billion in 2024 GMV, expanding rapid commerce, and growing tier-2 and tier-3 city consumption nationwide.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)