India Third Party Logistics (3PL) Market Size, Share, Trends and Forecast by Transport, Service Type, End Use, and Region, 2026-2034

India Third Party Logistics (3PL) Market Size, Share, Trends & Forecast (2026-2034)

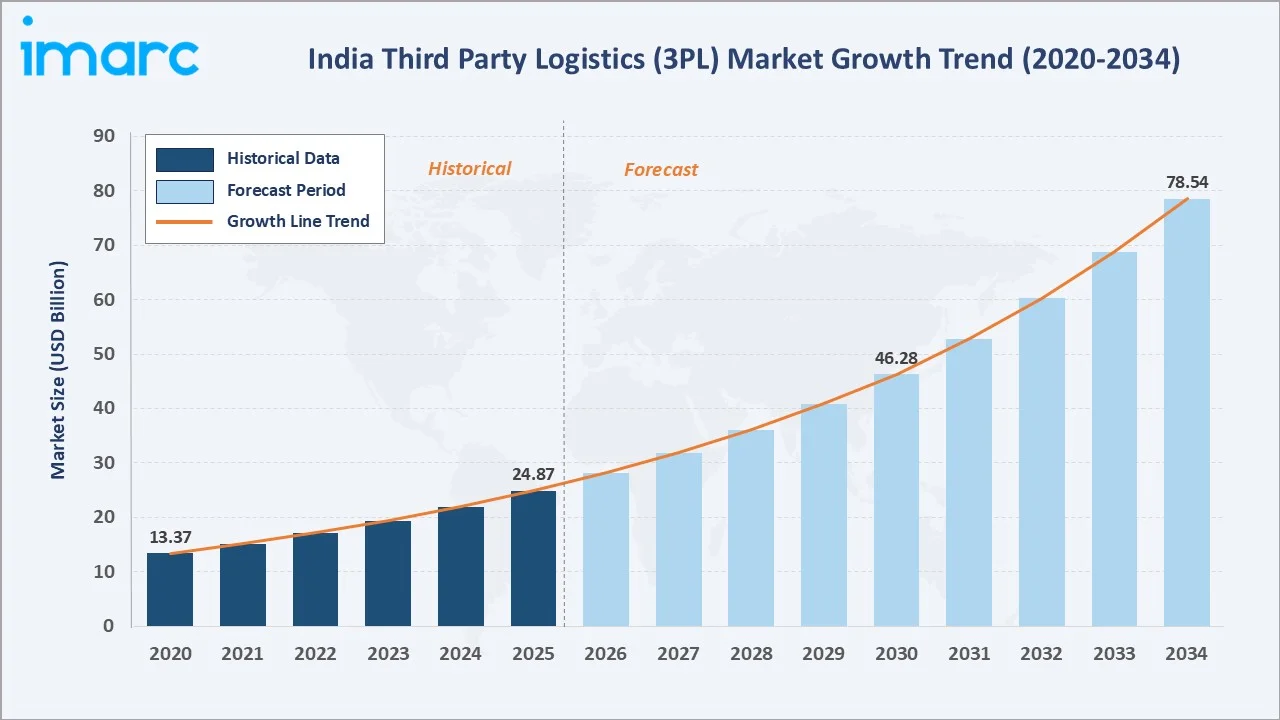

The India third party logistics (3PL) market was valued at USD 24.87 Billion in 2025 and is projected to reach USD 78.54 Billion by 2034, exhibiting a CAGR of 13.22% during 2026-2034. Rising manufacturing activity under production-linked incentive (PLI) schemes, expanding e-commerce penetration, and multimodal infrastructure development are primary market growth drivers.

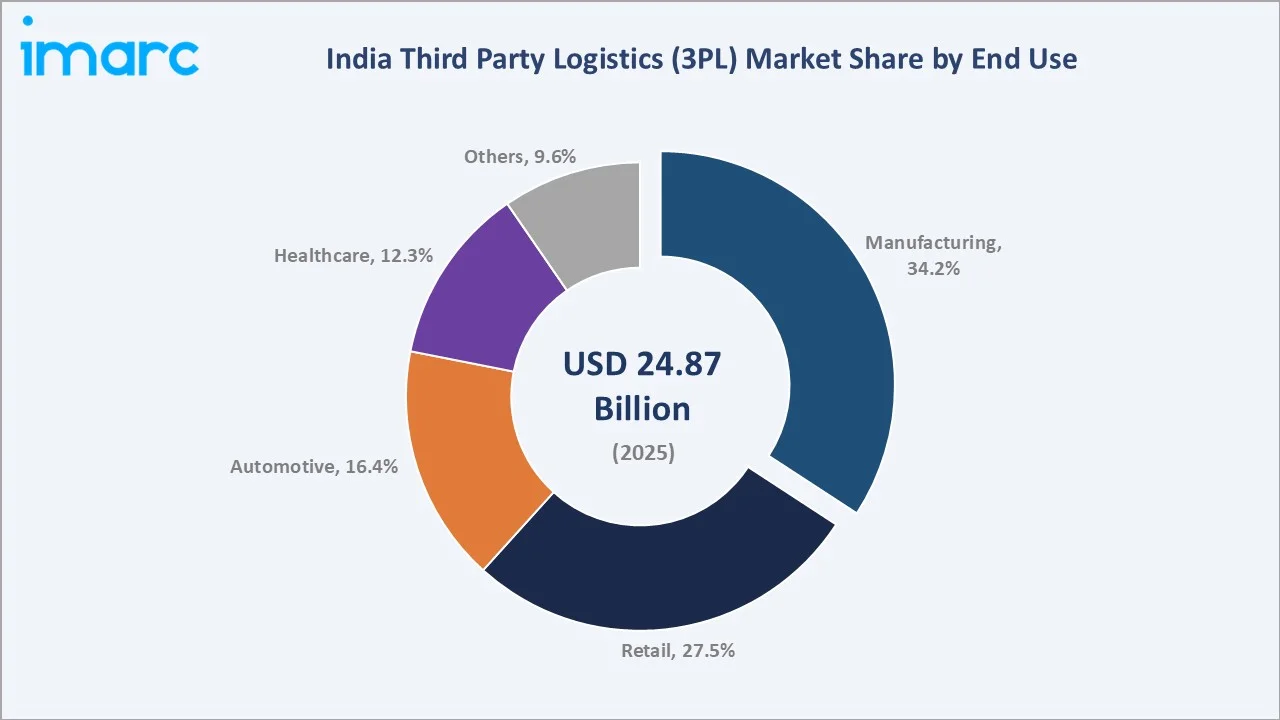

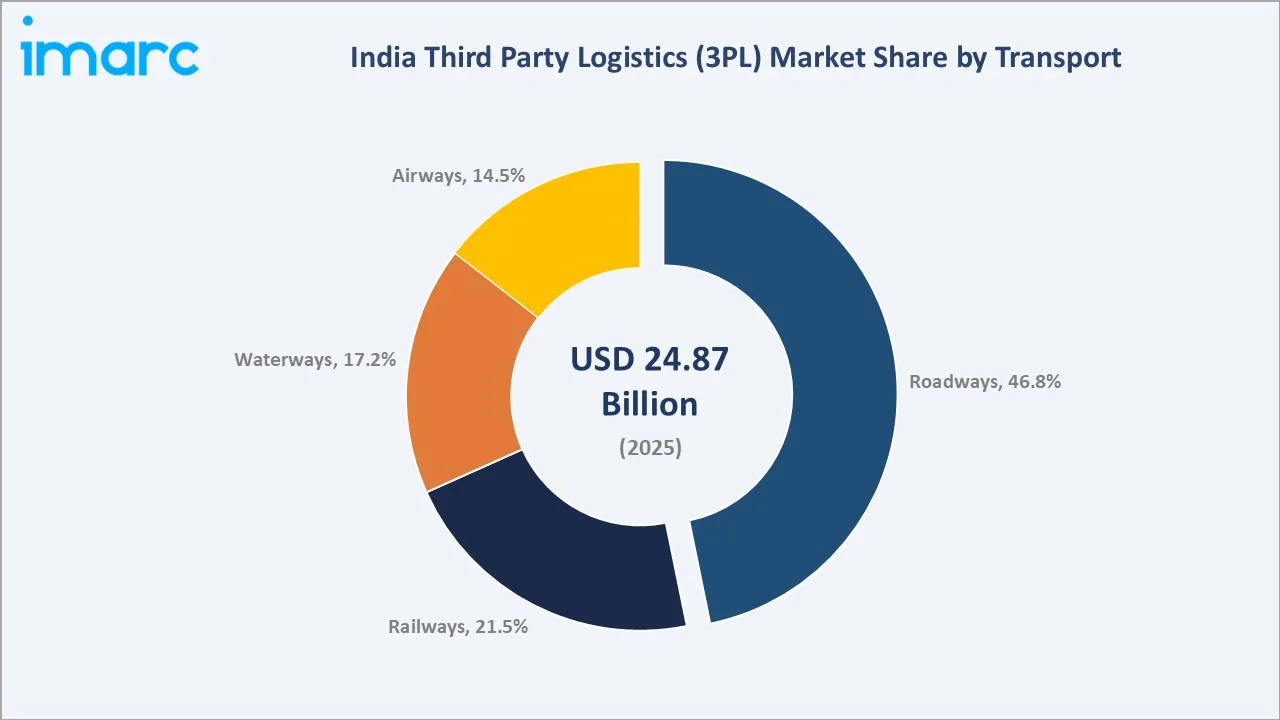

Manufacturing leads end use at 34.2%, roadways dominate transport at 46.8%, and West and Central India leads regional share at 31.8% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.87 Billion |

|

Forecast Market Size (2034) |

USD 78.54 Billion |

|

CAGR (2026-2034) |

13.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West and Central India (31.8%, 2025) |

|

Fastest Growing Region |

South India (23.4%, 2025) |

|

Leading End Use |

Manufacturing (34.2%, 2025) |

|

Leading Transport |

Roadways (46.8%, 2025) |

The India third party logistics (3PL) market expanded from USD 13.37 Billion in 2020 to USD 24.87 Billion in 2025, driven by widening e-commerce adoption, growing manufacturing outsourcing, and rapid expansion of organized warehousing and freight services across urban and semi-urban markets. Anchored at USD 46.28 Billion in 2030, the forecast trajectory extends to USD 78.54 Billion by 2034, supported by multimodal infrastructure development, technology-driven 3PL adoption, and deepening logistics outsourcing across the manufacturing, retail, automotive, and healthcare sectors.

To get more information on this market, Request Sample

CAGR trajectories across end use and transport sub-segments reveal healthcare and airways expanding faster than the overall 13.22% market CAGR, driven by pharmaceutical cold chain investments, rapid air cargo growth, and expanding multimodal logistics connectivity across the country.

Executive Summary

The India third party logistics (3PL) market expanded from USD 13.37 Billion in 2020 to USD 24.87 Billion in 2025, reflecting a robust historical growth trajectory. Driven by the convergence of digital commerce expansion, industrial policy reforms, and progressive infrastructure investments, the market is on a sustained upward path. The forecast period extends this growth to USD 78.54 Billion by 2034, underpinned by increasing outsourcing of logistics functions by domestic manufacturers, retailers, and healthcare companies.

Manufacturing accounts for the largest end use share at 34.2% in 2025, supported by robust expansion of industrial corridors and PLI-driven production scaling. Roadways lead the transport segment at 46.8%, fueled by rising e-commerce shipments, interstate freight movement, and last-mile delivery demand. As per IMARC Group, the India e-commerce market size was valued at USD 129.72 Billion in 2025. West and Central India commands the leading regional share at 31.8% in 2025, supported by established port infrastructure, dense industrial clusters, and strong FMCG and automotive manufacturing presence.

Key Market Insights

|

Insight |

Data |

|

Leading End Use |

Manufacturing – 34.2% share (2025) |

|

Second Largest End Use |

Retail – 27.5% share (2025) |

|

Leading Transport |

Roadways – 46.8% share (2025) |

|

Second Largest Transport |

Railways – 21.5% share (2025) |

|

Leading Region |

West and Central India – 31.8% share (2025) |

|

Fastest Growing Region |

South India – 23.4% share (2025) |

|

Top Companies |

DHL Group, Allcargo Group, Mahindra Group, Busybees Logistics Solutions Pvt. Ltd. |

Key Analytical Observations Expanding On The Data Above:

- Manufacturing leadership at 34.2% is anchored by India's approved PLI schemes covering 14 sectors and committing INR 1.97 Lakh Crore in production incentives, driving significant demand for integrated warehousing and distribution services across industrial corridors.

- Retail at 27.5% reflects the deepening integration of 3PL services into modern trade, quick commerce, and direct-to-consumer channels, with major e-commerce platforms and organized retailers outsourcing warehouse management, order fulfillment, and last-mile delivery.

- Roadways at 46.8% is supported by India's national highway network expansion and improved last-mile road infrastructure connecting industrial hubs to consumption centers across urban and semi-urban markets.

- Railways dominance at 21.5% reflects growing adoption of cost-efficient long-haul freight transportation for bulk goods, supported by dedicated freight corridor development and increasing multimodal logistics integration across industrial supply chains.

- West and Central India at 31.8% commands regional leadership, driven by established port connectivity at JNPA and Mundra, dense manufacturing clusters in Gujarat and Maharashtra, and strong FMCG and automotive 3PL demand.

India Third Party Logistics (3PL) Market Overview

Third party logistics (3PL) refers to the outsourcing of logistics and supply chain management functions, including warehousing, freight transportation, order fulfillment, inventory management, packaging, and value-added services to external service providers. These providers operate as integrated partners within the supply chains of manufacturers, retailers, automotive OEMs, healthcare companies, and e-commerce platforms. 3PL providers manage the physical flow of goods from origin through intermediate nodes to end consumers, enabling clients to focus on core business activities while achieving scale, efficiency, and flexibility in logistics operations.

The Indian 3PL ecosystem integrates freight carriers, warehouse operators, technology and IT solution providers, customs agents, freight forwarders, port and terminal operators, last-mile delivery partners, regulatory authorities at central and state levels, and end-use industries. Together, these participants form a complex, technology-driven supply chain network that moves goods across roadways, railways, waterways, and airways. The sector is transitioning from fragmented, asset-heavy models toward tech-enabled, asset-light, and integrated platforms, supported by digital freight matching, real-time tracking, and warehouse management systems.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

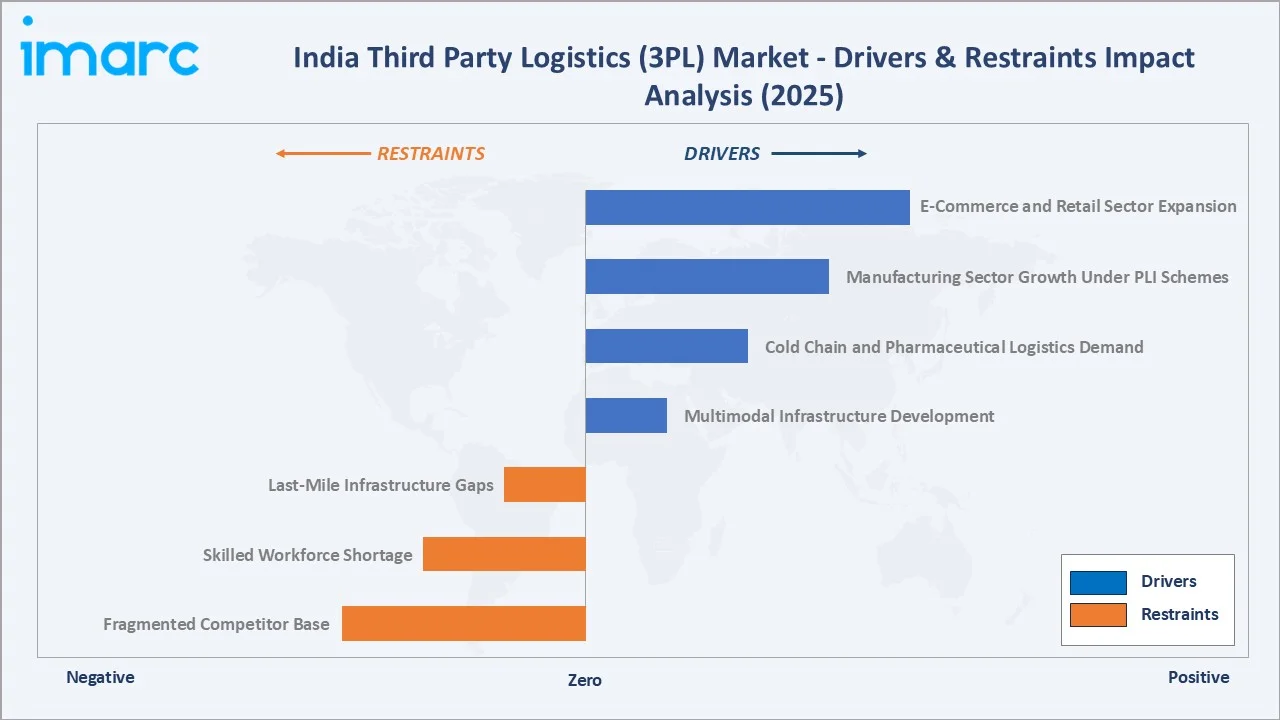

- E-Commerce and Retail Sector Expansion: The rapid expansion of e-commerce platforms, quick commerce operators, and organized retail chains is generating sustained demand for tech-enabled fulfillment centers, last-mile delivery networks, and returns management services across metro and tier-2 markets. 3PL providers offering seamless integration with marketplace platforms and digital inventory systems are capturing significant outsourcing contracts from both domestic and global retail operators expanding in India.

- Manufacturing Sector Growth Under PLI Schemes: Government-led infrastructure development initiatives, including freight connectivity upgrades and logistics park expansion, are improving supply chain efficiency and reducing transportation bottlenecks across India. Combined with PLI scheme-driven manufacturing expansion, these developments are generating strong demand for contract logistics, inbound supply chain management, and finished goods distribution services within the manufacturing sector.

- Cold Chain and Pharmaceutical Logistics Demand: Rising demand for temperature-controlled logistics from pharmaceutical manufacturers, vaccine distributors, food processors, and fresh produce exporters is driving investment in cold chain infrastructure and specialized 3PL capabilities. As per IBEF, India's cold chain market was valued at INR 2,28,700 Crore (USD 26.60 Billion) by 2024. Regulatory requirements for Good Distribution Practice (GDP) compliance are accelerating outsourcing of cold chain operations to certified 3PL providers with validated storage and transport systems.

- Multimodal Infrastructure Development: The ongoing expansion of dedicated freight corridors, inland waterways, and multimodal logistics parks under the PM GatiShakti National Master Plan is improving connectivity between production centers and consumption markets, reducing transit times and logistics costs for 3PL operators.

Market Restraints

- Infrastructure Quality Gaps in Last-Mile Connectivity: India's road network is among the largest in the world, yet significant portions of state and district roads remain inadequate for heavy freight operations, constraining last-mile delivery efficiency and increasing transit costs for 3PL providers in non-metro markets. Poor road quality and limited all-weather connectivity in tier-3 regions reduce network density and increase turnaround times for asset-based 3PL operators.

- Skilled Workforce Shortage Across Logistics Operations: The logistics and supply chain sector faces a structural deficit of skilled professionals including warehouse managers, logistics planners, cold chain technicians, and supply chain technology specialists. The shortage of trained manpower constrains 3PL operators from scaling operations rapidly, maintaining service quality, and deploying advanced automation and digital systems across distributed fulfillment networks.

- Fragmented and Unorganized Competitor Base: A large proportion of India's logistics market remains served by small, unorganized transporters and warehouse operators offering lower cost but inconsistent service quality, making it challenging for organized 3PL firms to compete on pricing alone. The fragmented competitive base also limits standardization of service levels, complicates compliance management, and increases cost pressures on formal 3PL providers.

Market Opportunities

- Technology-Driven Warehouse Automation: Growing adoption of automated storage and retrieval systems (ASRS), robotics, warehouse management systems (WMS), and real-time tracking technologies presents significant opportunities for 3PL providers to differentiate on service speed, accuracy, and scalability. Technology-led 3PL operators can command premium contracts from e-commerce, pharmaceutical, and consumer electronics clients demanding higher fulfillment accuracy and faster order processing.

- Cold Chain and Agri-Logistics Modernization: India's substantial agricultural output and growing organized food processing sector present significant opportunities for specialized cold chain 3PL services. Expansion of cold chain parks, reefer transport fleets, and temperature-monitored warehouses under government schemes offers 3PL providers a high-growth adjacent segment with strong CAGR potential through 2034.

- Cross-Border and Export Logistics Services: Rising exports of pharmaceuticals, auto components, textiles, and engineering goods are driving demand for integrated export logistics, freight forwarding, and customs clearance services. 3PL providers with multimodal and international freight management capabilities can capture substantial value-added revenues from India's growing export sector.

Market Challenges

- GST Compliance Complexity and Interstate Movement: Despite GST rationalization, multi-state logistics operations continue to face procedural complexity in documentation, e-way bill compliance, and state-level checkpost regulations. These compliance burdens increase operational overhead for 3PL providers managing pan-India distribution networks and reduce efficiency gains from scale.

- Rising Fuel and Operating Costs: Fluctuating diesel prices, increasing vehicle maintenance costs, and rising driver wage requirements are compressing margins for asset-heavy 3PL operators. The inability to fully pass fuel cost increases to clients under long-term contracts creates sustained margin pressure, particularly for road transport-intensive 3PL businesses.

Emerging Market Trends

-market-ppt-ishita-trivedi---3.webp)

1. Rise of Integrated and Technology-Enabled 3PL Platforms

3PL providers are rapidly transitioning from standalone warehousing or transport services to integrated, technology-driven platforms that offer end-to-end supply chain visibility, digital freight management, and automated order fulfillment. Real-time tracking, AI-driven demand forecasting, and cloud-based warehouse management systems are becoming standard capabilities for competitive 3PL operators, enabling clients to reduce inventory holding costs and improve distribution efficiency.

2. Growth of Cold Chain and Temperature-Controlled Logistics

India's cold chain logistics sector is witnessing accelerating investment driven by pharmaceutical export mandates, fresh food e-commerce, and domestic vaccine distribution requirements. India's cold chain network remains insufficient relative to growing pharmaceutical and agri-logistics demand, driving significant 3PL investment in temperature-controlled infrastructure, reefer fleets, and GDP-compliant distribution centers.

3. Multimodal Logistics and Intermodal Shift

The completion of DFCs and development of multimodal logistics parks are enabling a structural shift toward rail and waterway-based freight movement for long-haul routes. 3PL providers are building intermodal capabilities to integrate rail-road and sea-road logistics, reducing per-unit freight costs and transit times on high-volume corridors between industrial hubs and port gateways.

4. E-Commerce Fulfillment and Quick Commerce Logistics

The explosive growth of quick commerce and same-day delivery platforms is driving significant demand for dark stores, micro-fulfillment centers, and hyperlocal distribution networks. 3PL operators are investing in dense urban warehousing footprints and route optimization technologies to support rapid order fulfillment cycles for e-commerce clients, creating a high-growth vertical within the market.

5. Green and Sustainable Logistics Adoption

Environmental, social, and governance (ESG) commitments among global manufacturers and retailers operating in India are driving demand for green logistics solutions including electric vehicle (EV) fleets for last-mile delivery, solar-powered warehouses, and carbon footprint tracking across supply chains. 3PL providers adopting sustainable operations are gaining competitive advantages in winning contracts from multinational clients with Scope 3 emission reduction mandates.

Industry Value Chain Analysis

The India third party logistics (3PL) value chain spans six integrated stages from input sourcing through end user consumption, with technology, data integration, and compliance capabilities increasingly determining competitive advantage across all stages. Warehousing, transportation, and last-mile delivery capture the largest share of value-add, while 3PL value-added services including kitting, labeling, and reverse logistics represent the fastest growing component in organized 3PL contracts.

|

Stage |

Key Players / Examples |

|

Input Sourcing & Procurement |

Raw material suppliers, component manufacturers, import/export agents, customs brokers, freight forwarders, and procurement outsourcing firms |

|

Warehousing & Storage |

Multi-client and dedicated warehouse operators, cold storage providers, bonded warehouse managers, FMCG and automotive distribution center operators, and pharma cold chain facility managers |

|

Transportation & Distribution |

Road freight carriers, railway freight service providers, coastal and inland waterway shipping operators, air cargo handlers, and multimodal logistics park operators |

|

3PL Value-Added Services |

Integrated 3PL and contract logistics providers, supply chain technology firms, kitting and packaging service operators, reverse logistics specialists, and customs documentation consultants |

|

Last-Mile Delivery |

Express delivery and courier companies, quick commerce and hyperlocal fulfillment operators, last-mile technology platforms, and B2B distribution network providers |

|

End User Consumption |

Manufacturing companies, retail chains and e-commerce platforms, automotive OEMs and dealer networks, healthcare distributors, pharmaceutical companies, and institutional buyers |

Vertically integrated 3PL operators with proprietary warehouse management systems, dedicated transport fleets, and technology-enabled last-mile delivery capabilities are positioned to capture greater margin across the value chain compared to pure-play single-stage logistics providers.

Technology Landscape in the India Third Party Logistics (3PL) Industry

WMS and Automation

Advanced WMS platforms integrated with barcode, RFID, and IoT sensors are enabling 3PL operators to achieve real-time inventory visibility, automated putaway, and optimized picking across multi-client warehousing facilities. AGVs and conveyor systems are being deployed at large-scale fulfillment centers to increase throughput and reduce labor dependency in high-volume e-commerce and retail operations.

Transport Management Systems (TMS) and Digital Freight Matching

Cloud-based TMS platforms are enabling 3PL providers to optimize route planning, load consolidation, carrier selection, and real-time freight tracking across multi-mode shipments. Digital freight aggregator platforms connecting shippers with available truck capacity are improving fleet utilization and reducing empty running, while GPS-enabled telematics systems provide end-to-end shipment visibility to 3PL clients through integrated dashboards and mobile applications.

AI, Analytics, and Demand Forecasting

AI and machine learning applications in demand forecasting, inventory optimization, dynamic pricing, and predictive maintenance are enabling 3PL operators to deliver data-driven supply chain insights to clients. AI-powered demand sensing models help 3PL providers pre-position inventory across distributed warehousing nodes, reducing order fulfillment lead times and minimizing stockout risks for retail and e-commerce clients operating in India's fast-moving consumer markets.

Blockchain and Supply Chain Transparency

Blockchain-based track-and-trace platforms are being piloted across pharmaceutical, food, and automotive supply chains to provide immutable records of product provenance, custody transfers, and temperature compliance throughout the 3PL-managed distribution process. These systems support regulatory compliance for pharmaceutical GDP requirements, food safety standards, and automotive quality traceability mandates, making them a growing technology investment priority for specialized 3PL operators in India.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Transport |

Roadways |

46.8% |

2025 |

|

Service Type |

🔒 |

🔒 |

2025 |

|

End Use |

Manufacturing |

34.2% |

2025 |

|

Region |

West and Central India |

31.8% |

2025 |

By End Use

Manufacturing commands 34.2% of end use demand in 2025, reflecting the deep integration of 3PL services into India's production-linked industrial ecosystem. PLI scheme-driven capacity expansions across electronics, pharmaceuticals, automotive components, textiles, and specialty chemicals have accelerated demand for contract logistics, inbound supply chain management, and finished goods warehousing and distribution. Manufacturing clients typically require dedicated or build-to-suit warehousing facilities with specialized handling, packaging, and just-in-time delivery capabilities.

To access detailed market analysis, Request Sample

Retail accounts for 27.5% of end use demand in 2025, driven by the rapid expansion of organized retail, e-commerce fulfillment, and quick commerce logistics. Large retail chains, direct-to-consumer brands, and marketplace operators are increasingly outsourcing multi-echelon distribution, returns management, and last-mile delivery to 3PL providers offering technology-enabled, omni-channel logistics solutions across metro and tier-2 cities.

By Transport

Roadways lead the transport segment at 46.8% in 2025, reflecting India's road network dominance in domestic freight movement and the flexibility of road transport for first-mile, last-mile, and inter-city freight across diverse geographies. Road-based 3PL remains the default mode for small-to-mid-volume consignments, time-sensitive e-commerce deliveries, and distribution across markets not served by rail or waterway networks.

Railways account for 21.5% of the transport mix, supported by dedicated freight corridor development and competitive bulk freight pricing for long-haul movement of commodities, auto components, and FMCG goods. Increasing multimodal logistics integration and containerized cargo movement are further strengthening railway adoption among large-scale manufacturers and logistics providers.

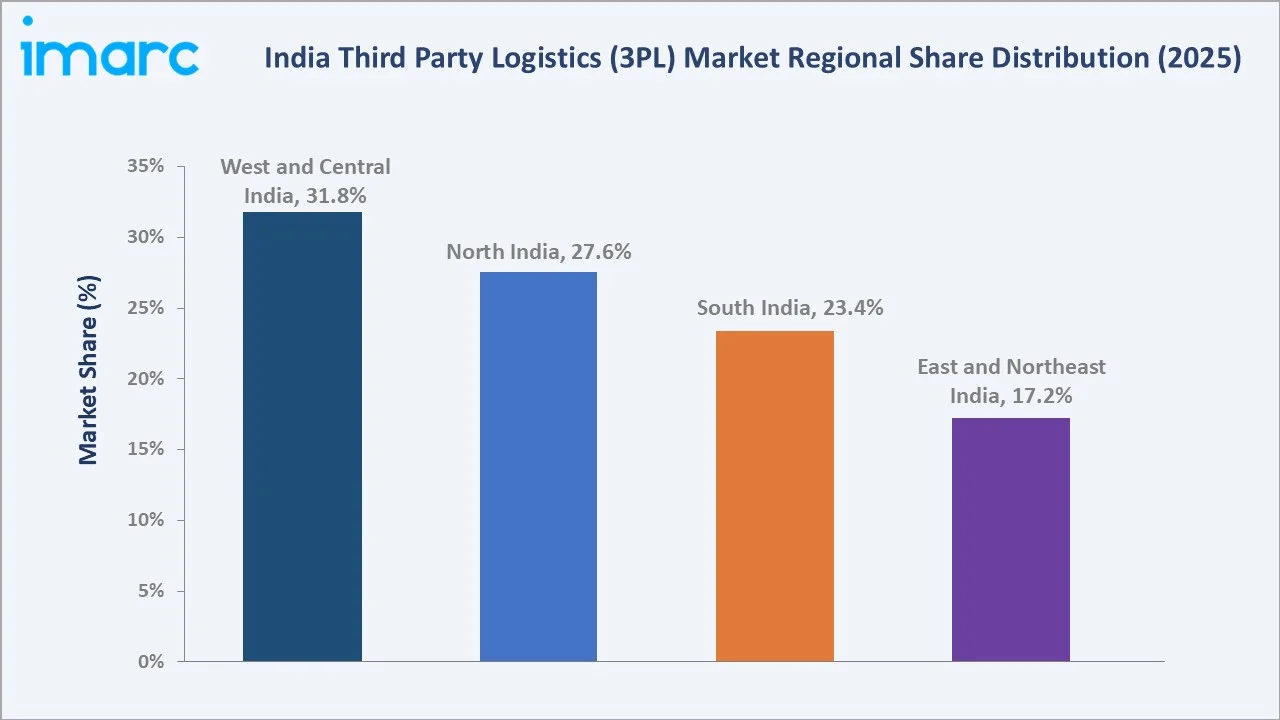

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West and Central India |

31.8% |

Leading industrial clusters in Maharashtra and Gujarat, strong port connectivity at JNPT and Mundra, established FMCG and automotive supply chain networks, and high concentration of organized 3PL demand |

|

North India |

27.6% |

Delhi-NCR as a primary retail and e-commerce distribution hub, large consumer population base, expanding road and rail connectivity across Punjab, Haryana, and Uttar Pradesh, and growing cold chain demand |

|

South India |

23.4% |

Expanding IT-driven consumer markets, rising pharmaceutical and auto component exports through Chennai and Kochi ports, growing organized retail penetration, and increasing e-commerce fulfillment center investments |

|

East and Northeast India |

17.2% |

Expanding FMCG and consumer goods distribution networks, improving infrastructure under government connectivity programs, growing organized retail and e-commerce penetration, and rising cross-border trade potential |

West and Central India leads the regional landscape with a 31.8% share in 2025, supported by the highest concentration of industrial activity, established port infrastructure, and a mature 3PL ecosystem serving manufacturing, automotive, and FMCG sectors. The region houses major logistics hubs, including Pune, Nagpur, Ahmedabad, and Mumbai, which serve as critical nodes in the national supply chain network.

South India at 23.4% is poised as the fastest growing region, driven by rapid digital adoption, expanding multi-sector manufacturing exports, and rising tier-2 city logistics demand across Bengaluru, Hyderabad, and Chennai clusters.

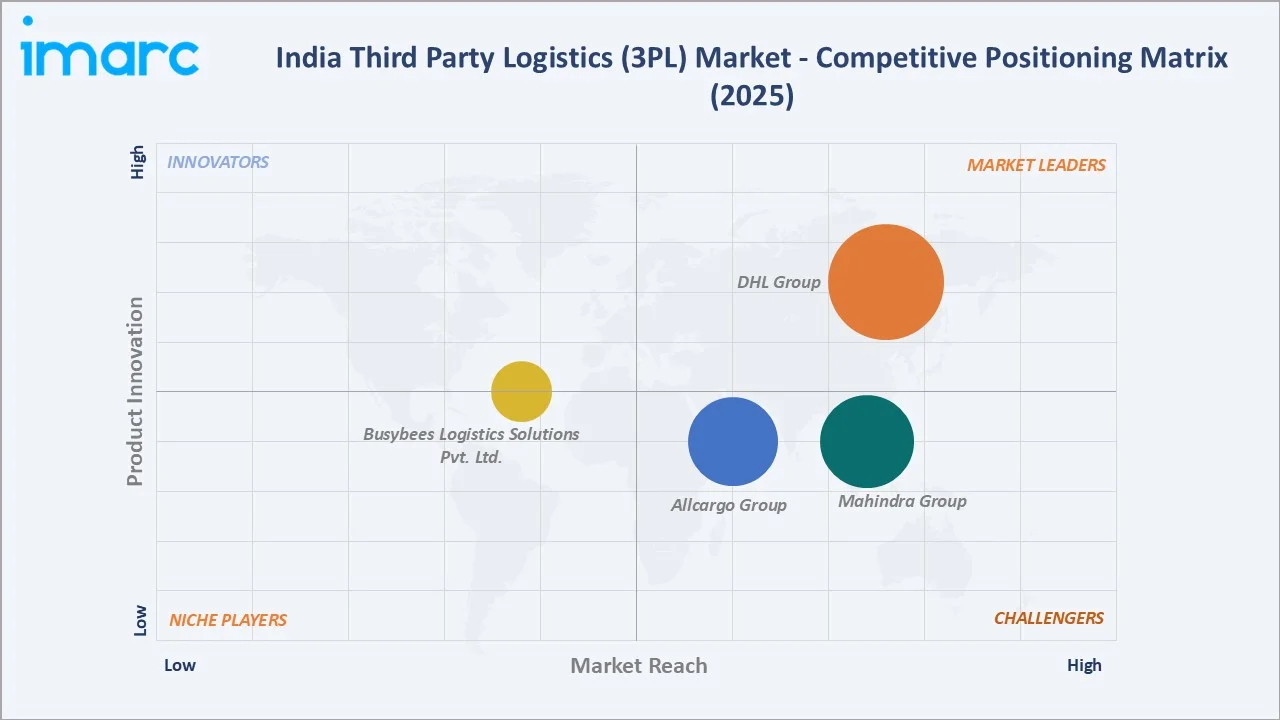

Competitive Landscape

The India third party logistics (3PL) market is moderately fragmented, with established international operators, listed domestic 3PL companies, and technology-native logistics platforms competing across warehousing, freight, express delivery, and integrated supply chain segments. Key competitive differentiators include technology platform capability, pan-India network density, sector-specific logistics expertise, scalability of fulfillment operations, and strength of client relationships across manufacturing, retail, and healthcare verticals.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

DHL Group |

DHL Supply Chain India |

Leader |

Technology-driven integrated supply chain and contract logistics with global network reach |

|

Allcargo Group |

Allcargo Logistics |

Challenger |

Multimodal logistics and container freight station operations with pan-India reach |

|

Mahindra Group |

Mahindra Logistics |

Challenger |

Integrated third party logistics and enterprise mobility solutions across sectors |

|

Busybees Logistics Solutions Pvt. Ltd. |

XpressBees |

Emerger |

Technology-driven e-commerce logistics and fulfillment platform with B2B, B2C, and cross-border capabilities |

Leading players include DHL Group, Allcargo Group, Mahindra Group, and Busybees Logistics Solutions Pvt. Ltd., among others.

Key Company Profiles

Allcargo Group

Allcargo Group is one of India's leading integrated logistics conglomerates. The group serves a wide range of industries, including FMCG, retail, automotive, and e-commerce across India through a comprehensive ground distribution and logistics management network.

- Product Portfolio: Domestic express distribution and ground transportation, contract logistics, warehousing, consultative supply chain solutions, inland container depot and container freight station operations, and e-commerce fulfillment services across India.

- Recent Developments: Allcargo Group continues to strengthen its domestic logistics operations, invest in technology-driven supply chain solutions, and grow its express distribution network.

- Strategic Focus: Deepening domestic express distribution and contract logistics capabilities across India's key industrial and consumption markets.

Mahindra Group

Mahindra Group is one of India's leading diversified industrial and automotive conglomerates, operating a dedicated third party logistics business. The logistics arm provides integrated supply chain management, transportation, warehousing, and enterprise mobility solutions to clients across automotive, engineering, consumer goods, pharmaceutical, and e-commerce sectors.

- Product Portfolio: Integrated 3PL services including transportation management, multi-client and dedicated warehousing, freight forwarding, value-added supply chain services, enterprise mobility and people logistics solutions, and technology-enabled last-mile delivery.

- Recent Developments: Mahindra Group continues to expand its integrated supply chain capabilities, invest in technology-driven logistics platforms, and grow its warehousing and distribution footprint across key industrial corridors to serve a broader range of enterprise clients.

- Strategic Focus: Growing integrated third party logistics and enterprise mobility solutions with increasing emphasis on technology-enabled supply chain services and sector-specific expertise.

Busybees Logistics Solutions Pvt. Ltd.

Busybees Logistics Solutions Pvt. Ltd. is one of India's leading technology-enabled e-commerce logistics companies. The company provides end-to-end domestic supply chain solutions and international logistics services to e-commerce businesses, enterprises, and individual clients across a nationwide network of service centers and hubs.

- Product Portfolio: B2C express parcel delivery, B2B freight and surface logistics, third party logistics and fulfillment services, cross-border e-commerce logistics, reverse logistics and returns management, and payment collection and value-added services.

- Recent Developments: Busybees Logistics Solutions Pvt. Ltd. continues to expand its B2B and 3PL service lines, strengthen its nationwide delivery network, and invest in technology platform enhancements to improve real-time shipment visibility and operational efficiency for enterprise and e-commerce clients.

- Strategic Focus: Expanding technology-driven e-commerce logistics with growing emphasis on B2B freight, third party logistics, and cross-border services across India.

Market Concentration Analysis

The India third party logistics (3PL) market is moderately fragmented, with the top four organized players collectively accounting for a meaningful share of the overall market in 2025. However, a large proportion of total logistics expenditure remains served by unorganized and regional operators, particularly in road freight and local warehousing.

Barriers to entry for organized 3PL include high capital requirements for warehouse infrastructure, the need for pan-India transport networks and last-mile coverage, technology investment for WMS and TMS platforms, and client-specific compliance capabilities. These barriers are favoring larger incumbents with established scale, brand recognition, and diversified client portfolios. However, technology-native startups are disrupting specific segments including express delivery, B2B freight aggregation, and last-mile solutions by leveraging asset-light models and platform-based matching.

Consolidation is accelerating within the organized 3PL segment as larger operators acquire smaller specialized players, scale warehousing networks, and develop integrated service portfolios spanning contract logistics, express delivery, and freight management. Strategic alliances between 3PL providers and e-commerce platforms, automotive manufacturers, and pharmaceutical companies are further deepening client relationships and reinforcing competitive positions in the growing market.

Investment & Growth Opportunities

Fastest-Growing Segments

Healthcare at 12.3% represents the fastest growing end use segment, driven by India's expanding pharmaceutical manufacturing base, rising medical device exports, GDP compliance mandates, and vaccine distribution infrastructure investments. Retail at 27.5% of end use demand continues to expand as quick commerce and omni-channel retail deepen logistics outsourcing to specialized 3PL providers.

Emerging Markets

South India at 23.4% is positioned as the fastest growing region through 2034, anchored by rapid pharmaceutical export expansion, IT-enabled consumer demand growth, and rising organized logistics infrastructure investment across Bengaluru, Hyderabad, Chennai, and Kochi hubs. East and Northeast India at 17.2% represents the highest incremental opportunity, with government infrastructure programs improving connectivity and enabling organized 3PL entry into previously underserved markets. Tier-2 and tier-3 city markets across all regions present significant untapped demand for standardized warehousing, express delivery, and value-added 3PL services.

Venture & Investment Trends

Investment activity in the India 3PL market is concentrated in technology-native logistics platforms, automated fulfillment infrastructure, cold chain expansion, and express delivery networks. Private equity and strategic investors are channeling capital into listed 3PL companies and growth-stage logistics startups with differentiated technology platforms. Government-backed logistics infrastructure programs are attracting infrastructure investment alongside private 3PL operator expansion, creating a favorable environment for capacity-building across the full value chain through 2034.

Future Market Outlook (2026-2034)

The India third party logistics (3PL) market is forecast to expand from USD 24.87 Billion in 2025 to USD 78.54 Billion by 2034 at a CAGR of 13.22%, adding approximately USD 53.67 Billion in incremental annual market value over the forecast period. The market will cross USD 46.28 Billion by 2030, reflecting the sustained compounding effect of manufacturing scale-up, e-commerce growth, and logistics modernization across the country.

Four structural forces will shape the India 3PL market through 2034: continued penetration of organized and tech-enabled logistics into previously unstructured market segments; accelerating adoption of automation, AI, and digital platforms across warehouse and transport operations; rapid expansion of cold chain, last-mile, and multimodal service capabilities; and progressive deepening of outsourcing by manufacturing, retail, healthcare, and automotive clients seeking supply chain efficiency and flexibility.

By 2034, the India 3PL market is expected to be defined by integrated, platform-led supply chain management, with technology-driven warehousing, multimodal freight optimization, and data-enabled demand forecasting becoming standard capabilities for competitive 3PL providers. Green logistics, regulatory compliance, and customer-centric service design will emerge as additional competitive differentiators as the market matures into a globally benchmarked 3PL ecosystem serving India's expanding industrial and consumer economy.

Research Methodology

Primary Research

Primary research for the India third party logistics (3PL) market included structured interviews with 3PL company executives, logistics heads of manufacturing and retail companies, freight forwarders, warehouse technology providers, and regulatory and industry body representatives. Primary inputs validated market sizing assumptions, segment growth drivers, competitive positioning, and emerging trends across end use, transport mode, and regional dimensions.

Secondary Research

Secondary research sources included Ministry of Commerce and Industry publications, Ministry of Ports Shipping and Waterways reports, Ministry of Road Transport and Highways data, PM GatiShakti program documentation, annual reports and investor presentations of listed 3PL companies, industry association databases, logistics and supply chain trade publications, and government budgetary and infrastructure program disclosures.

Forecasting Models

Market forecasts were developed using top-down and bottom-up modeling approaches, combining total logistics expenditure projections, 3PL penetration rate evolution, end use segment growth rates, transport mode mix shifts, and macroeconomic variables including GDP growth, industrial output, and e-commerce expansion. Scenario analysis addressed infrastructure development pace, PLI scheme production scale-up trajectories, and organized 3PL market penetration rate assumptions through 2034.

India Third Party Logistics (3PL) Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Transports Covered | Railways, Roadways, Waterways, Airways |

| Service Types Covered | Dedicated Contract Carriage, Domestic Transportation Management, International Transportation Management, Warehousing and Distribution, Value Added Logistics Services |

| End Uses Covered | Manufacturing, Retail, Healthcare, Automotive, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | DHL Group, Allcargo Group, Mahindra Group, Busybees Logistics Solutions Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India third party logistics (3PL) market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India third party logistics (3PL) market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India third party logistics (3PL) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Third Party Logistics (3PL) Market Report

The India third party logistics (3PL) market was valued at USD 24.87 Billion in 2025, driven by e-commerce growth, manufacturing expansion, and increasing logistics outsourcing across sectors.

The market is projected to reach USD 78.54 Billion by 2034, growing at a CAGR of 13.22% from 2026 to 2034, supported by technology adoption and infrastructure expansion.

Manufacturing leads end use demand at 34.2% in 2025, driven by PLI scheme-led production expansion, industrial corridor development, and growing demand for contract logistics across the sector.

Roadways lead with 46.8% share in 2025, supported by India's extensive national highway network and the flexibility of road freight for diverse shipment sizes and geographies.

West and Central India commands the largest regional share at 31.8% in 2025, supported by port infrastructure, manufacturing clusters, and established 3PL ecosystems in Maharashtra and Gujarat.

Leading players include DHL Group, Allcargo Group, Mahindra Group, Busybees Logistics Solutions Pvt. Ltd., among others.

Technology including WMS, TMS, AI-driven forecasting, and real-time tracking is enabling 3PL providers to improve fulfillment accuracy, reduce costs, and offer data-driven supply chain solutions to clients.

Pharmaceutical manufacturing expansion, vaccine distribution infrastructure, GDP compliance requirements, and medical device export growth are key drivers of healthcare-focused 3PL demand in India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)