India Luxury Car Market Size, Share, Trends and Forecast by Vehicle Type, Fuel Type, Price Range, Engine Capacity, and Region, 2026-2034

India Luxury Car Market Size, Share, Trends & Forecast (2026-2034)

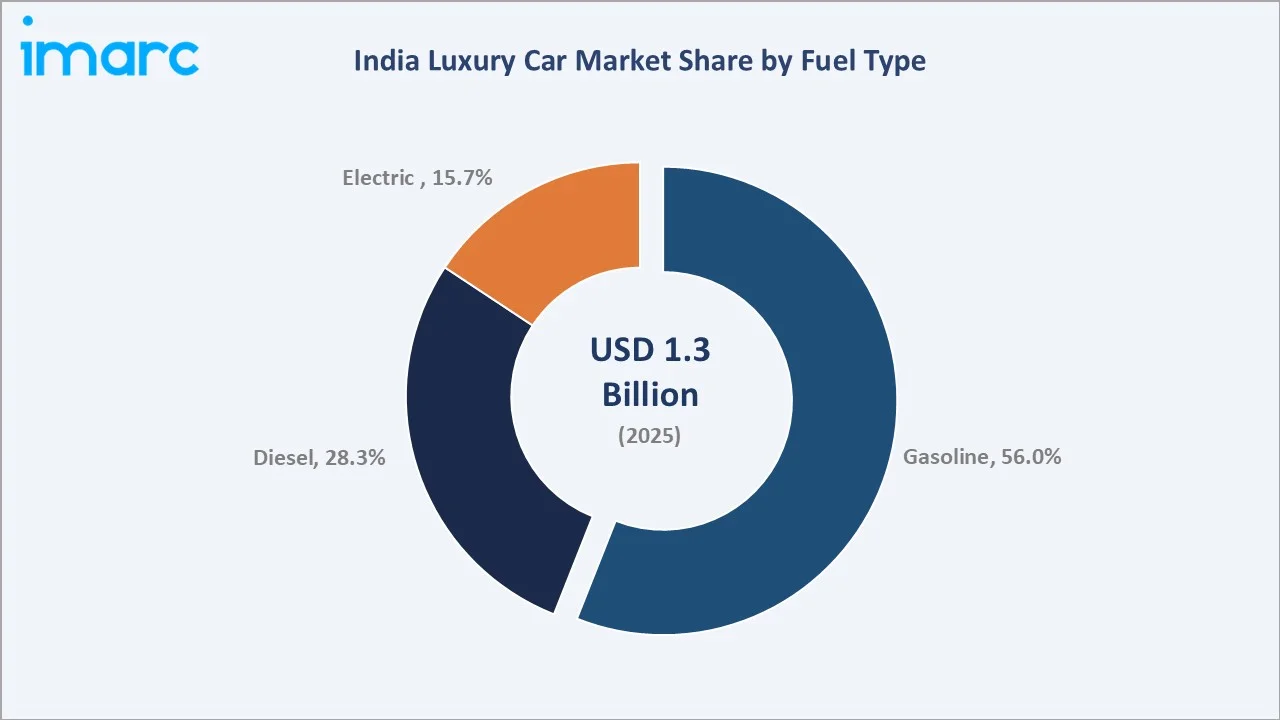

India luxury car market size was valued at USD 1.3 Billion in 2025 and is projected to reach USD 2.0 Billion by 2034, exhibiting a CAGR of 5.09% during 2026-2034. Rising high-net-worth individual (HNI) population, growing aspirational demand, and rapid urbanization are driving the India luxury car market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.3 Billion |

|

Forecast Market Size (2034) |

USD 2.0 Billion |

|

CAGR (2026-2034) |

5.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

West and Central India (28.4%) |

|

Fastest Growing Segment |

Electric Vehicles (EV) |

The India luxury car market growth trajectory from 2020 through 2034 illustrates a transition from post-pandemic recovery to a steady premiumization-led expansion phase.

To get more information on this market, Request Sample

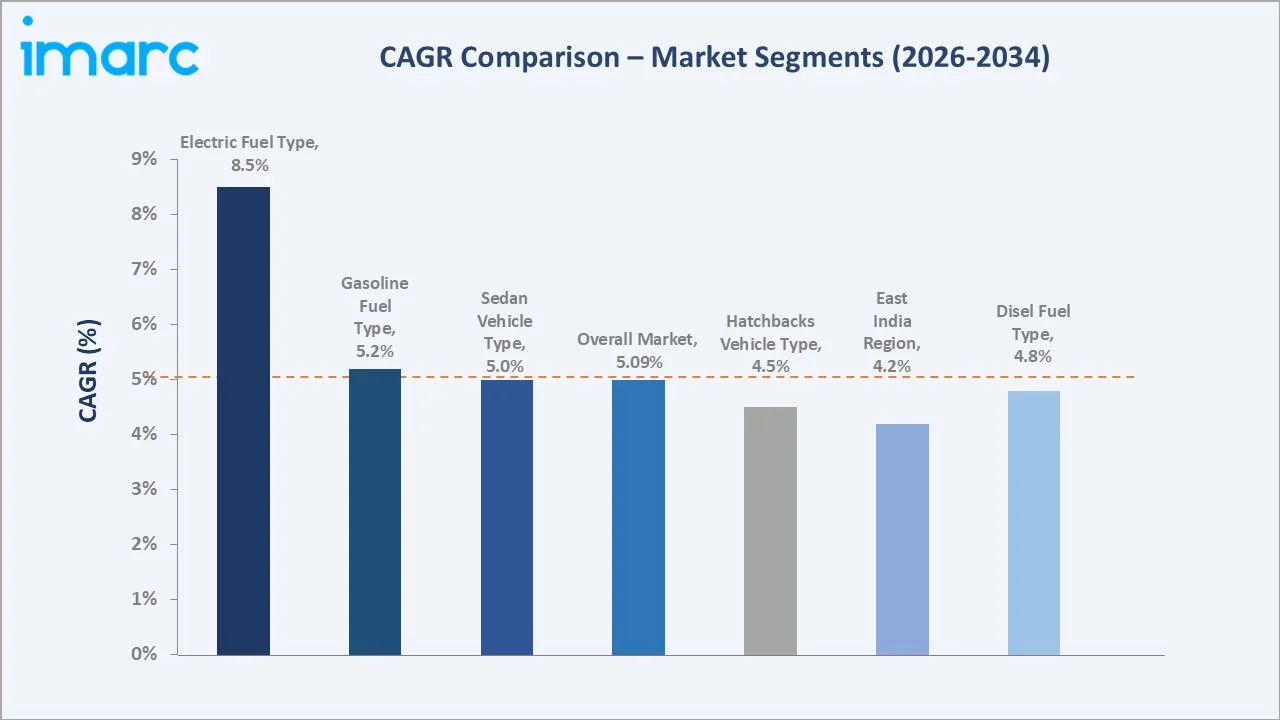

Segment-level CAGR comparisons in the India luxury car market highlight electric vehicles (EVs) and compact luxury SUVs as the fastest-growing sub-categories through 2034.

Executive Summary

The India luxury car market reached USD 1.0 Billion in 2020 and grew to USD 1.3 Billion by 2025, exhibiting steady recovery and expansion. Key growth drivers include rising disposable incomes among HNI households, expanding young professional demographics, and accelerating EV adoption. The market is projected to reach USD 1.6 Billion in 2030 and USD 2.0 Billion by 2034, at a CAGR of 5.09% during 2026-2034.

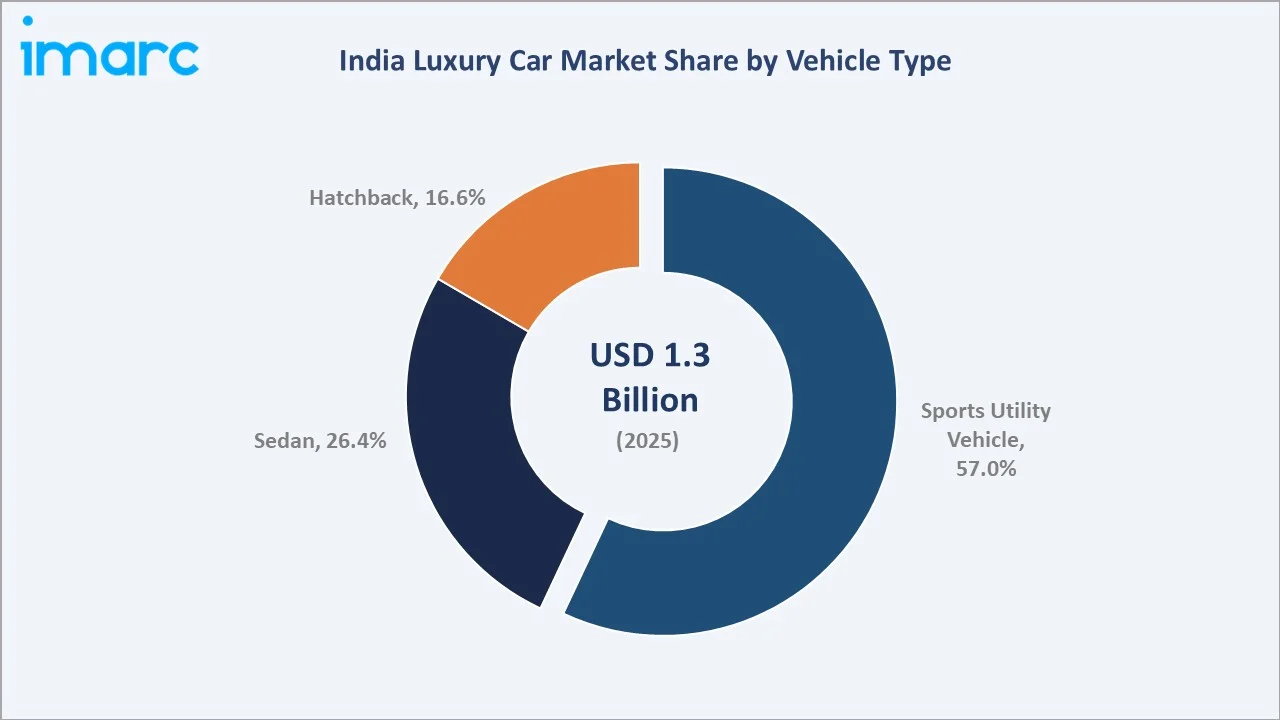

SUVs represent the dominant vehicle type at 57.0% share in 2025, driven by consumer preference for higher ground clearance and premium utility. Gasoline vehicles lead fuel-type segmentation at 56.0%, although Electric vehicles are fastest-growing, fueled by government incentives and infrastructure buildout. Entry-level luxury vehicles are opening new addressable customer segments.

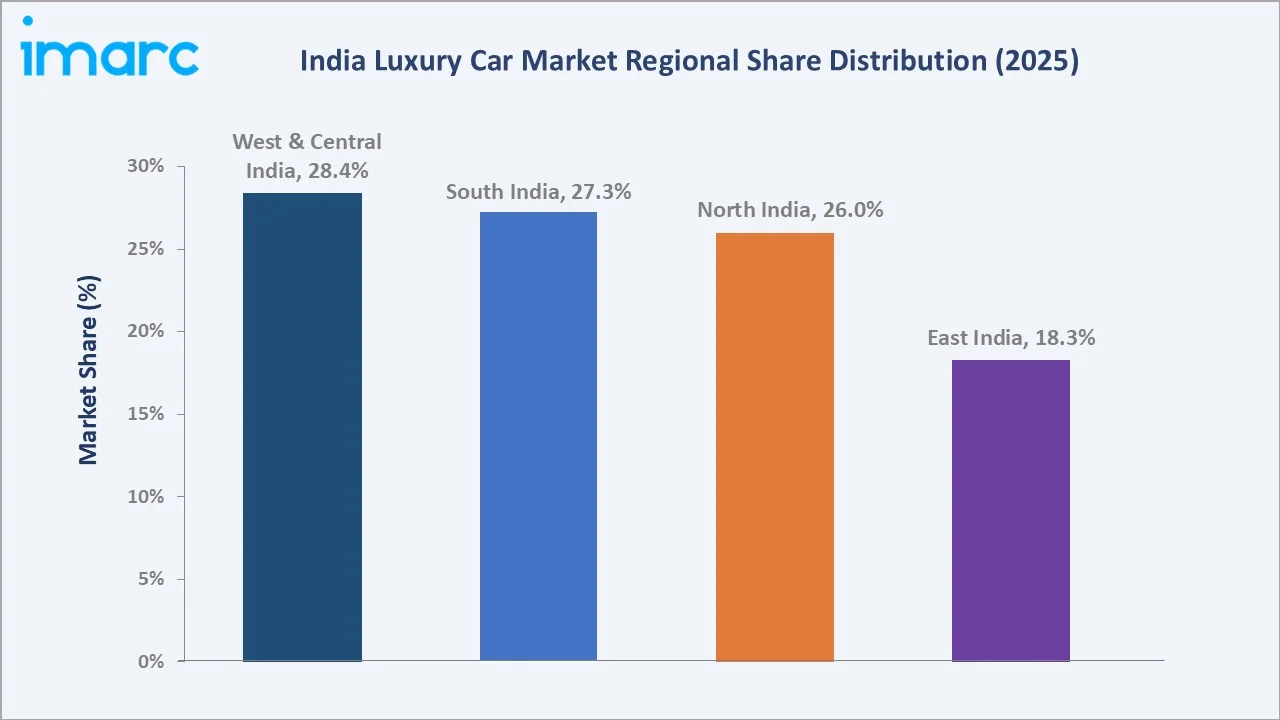

West and Central India commands 28.4% of total India luxury car revenue in 2025, followed closely by South India at 27.3%. Key players operating in this market include Mercedes-Benz Group AG, BMW Group, Volkswagen Group, Geely Auto, Jaguar Land Rover Automotive PLC, Lexus, Stellantis India Private Limited. Premium digital showrooms and experiential marketing campaigns continue reshaping India's luxury automotive market trends.

Key Market Insights

|

Insight |

Data |

|

Largest Vehicle Type |

Sports Utility Vehicle (SUV) – 57.0% in 2025 |

|

Largest Fuel Type |

Gasoline – 56.0% in 2025 |

|

Leading Region |

West and Central India – 28.4% in 2025 |

|

Fastest Growing Vehicle |

Electric Vehicles – 8.5% CAGR (2026-2034) |

|

Top Companies |

Mercedes-Benz Group AG, BMW Group, Volkswagen Group, Geely Auto, Jaguar Land Rover Automotive PLC, Lexus, Stellantis India Private Limited |

|

Market Opportunity |

EV luxury segment and tier-2 city expansion |

- SUVs dominate India luxury car market share at 57.0% in 2025, driven by demand for premium utility vehicles among urban HNI buyers seeking versatility alongside status.

- Gasoline vehicles hold 56.0% fuel-type share in 2025, while EV luxury vehicles are growing fastest at approximately 8.5% CAGR, supported by FAME III subsidies and green mobility mandates.

- West and Central India leads regionally at 28.4% in 2025, with Mumbai, Pune, and Ahmedabad as anchor markets for European luxury OEMs.

- Top-5 companies – Mercedes-Benz Group AG, BMW Group, Volkswagen Group, Geely Auto, Jaguar Land Rover Automotive PLC – account for approximately 85% of total market revenue in 2025.

- Electric and hybrid luxury vehicles represent USD 300 Million in opportunity by 2030 as EV infrastructure reaches tier-1 and select tier-2 Indian cities.

- India luxury car market industry analysis reveals that entry-level luxury vehicles are expanding the buyer base, bringing aspirational buyers into premium segments.

India Luxury Car Market Overview

The India luxury car market encompasses premium passenger vehicles includes sedans, SUVs, and hatchbacks from European, American, and Asian luxury OEMs. The ecosystem spans raw material suppliers, tier-1 component manufacturers, OEM assembly units, authorized dealership networks, and after-sales service providers. Macroeconomic tailwinds – According to the latest Mercedes-Benz Hurun India Wealth Report 2025, the country is projected to have 871,700 millionaire families by 2025, urbanization, and India's emerging position as a global premium consumer market – underpin structural demand growth.

The market serves residential, corporate fleet, and chauffeur-driven applications, with primary demand concentrated in metro cities including Delhi-NCR, Mumbai, Bangalore, Hyderabad, and Chennai. Increasing localization investments by OEMs are improving pricing competitiveness in the India luxury car market.

Market Dynamics

To evaluate market opportunities, Request Sample

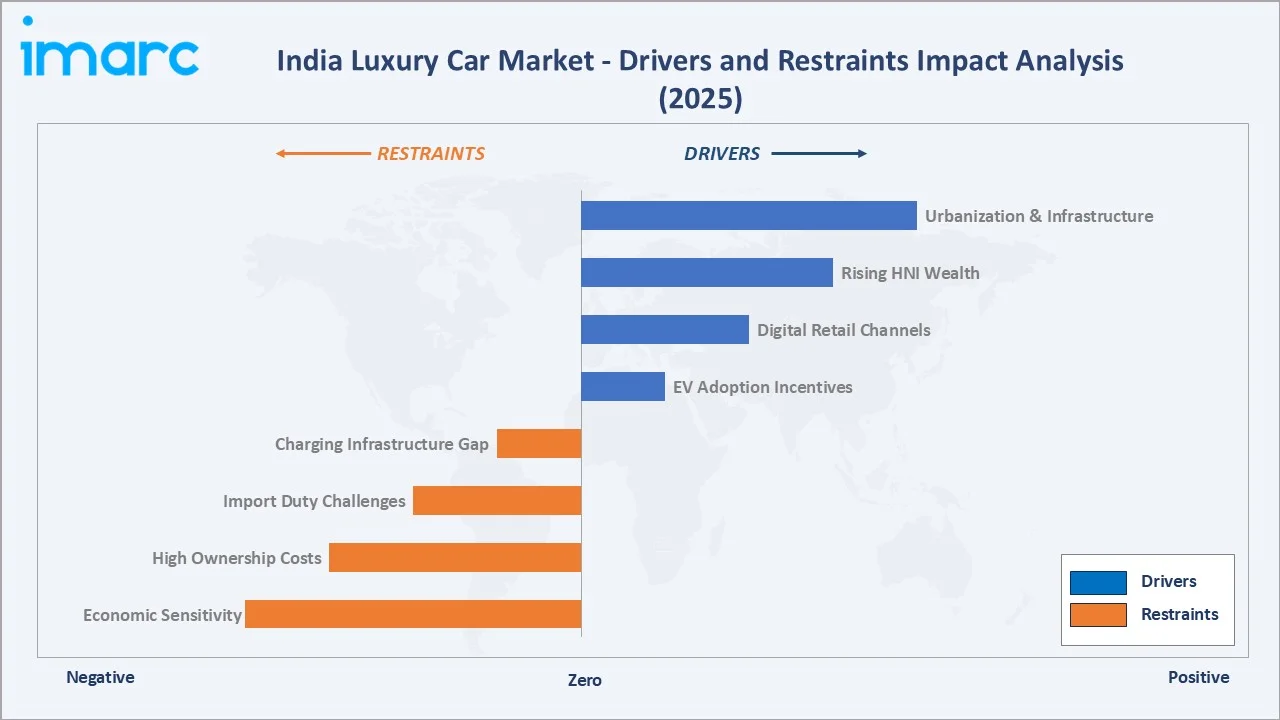

Market Drivers

- Rising HNI and UHNI population: India's HNI count is projected to grow at 10-12% CAGR through 2030, directly expanding the addressable luxury car buyer base.

- Urbanization and infrastructure expansion: Over 600 million urban residents by 2031 are expected, with improved road infrastructure supporting luxury vehicle adoption.

- Growing aspirational youth segment: India's working-age population under 35 years with premium lifestyle preferences fuels demand for entry-level luxury models, particularly BMW 2-Series and Audi A3-class vehicles.

- Government EV incentives: FAME III scheme and state-level EV subsidies are accelerating adoption of electric luxury vehicles, with Mercedes-Benz EQS and BMW iX generating strong pre-booking traction.

Market Restraints

- High import duties: India levies high import duties on CBU (Completely Built Units) luxury vehicles, elevating sticker prices above global benchmarks and limiting demand.

- Economic sensitivity: Luxury auto purchases are highly discretionary, making this segment vulnerable to economic downturns, rising fuel prices, and RBI monetary tightening cycles.

- Charging infrastructure gaps: Limited EV fast-charging networks in tier-2 and tier-3 cities constrain electric luxury vehicle adoption beyond metro geographies.

Market Opportunities

- EV luxury segment: With domestic EV policy support, the electric luxury car sub-segment is projected to see strong growth by 2034, creating significant first-mover advantages.

- Tier-2 city expansion: Cities like Pune, Chandigarh, Kochi, and Coimbatore are emerging luxury auto consumption centers, offering untapped dealership and volume opportunities.

- Subscription and flex-ownership models: Digital-first ownership alternatives are attracting millennial HNI buyers.

Market Challenges

- Localization pressure: OEMs face margin compression as the government incentivizes CKD (Completely Knocked Down) assembly to increase local content.

- Competitive intensity: Entry of Lexus, Genesis, and premium Chinese luxury OEMs is fragmenting market share from established European brands.

- Regulatory evolution: Upcoming CAFE (Corporate Average Fuel Economy) Phase III norms require OEMs to accelerate powertrain electrification, requiring capital-intensive product transitions.

Emerging Market Trends

1. SUV Premiumization

SUVs have captured 57.0% of India luxury car market share in 2025. The shift reflects consumer preference for versatile, high-riding luxury vehicles. BMW X5, Mercedes-Benz GLC, and Audi Q7 are the volume leaders, collectively accounting for a significant share of SUV luxury sales.

2. Electric Luxury Vehicle (ELV) Adoption

Electric vehicles represented 15.7% of India luxury car fuel-type sales in 2025, Growing from near-zero in 2020, Mercedes-Benz EQS, BMW iX3, and Volvo EX40 are driving this transition. The ELV segment is forecast to grow faster than the overall market, outpacing its growth rate through 2034.

3. Digital Retail and Phygital Showrooms

Luxury OEMs are investing in augmented reality (AR) car configurators and virtual showroom experiences. Mercedes-Benz India reported a significant share of leads originating via digital channels. Online luxury car sales are projected to grow steadily in India through 2030.

4. Connected and ADAS-Enabled Vehicles

Advanced Driver Assistance Systems (ADAS) and connected vehicle features are becoming standard across luxury segments. Volvo Pilot Assist, BMW Driving Assistant Professional, and Mercedes-Benz MBUX are key differentiators, with connected vehicle penetration in India’s luxury segment reaching a high level.

5. Bespoke and Personalization Services

High-end buyers in India are increasingly opting for factory-order and bespoke customization programs. Customization orders account for a significant share of luxury vehicle volumes, indicating a maturing luxury consumer base with stronger preference for exclusivity, personalization, and premium ownership experiences.

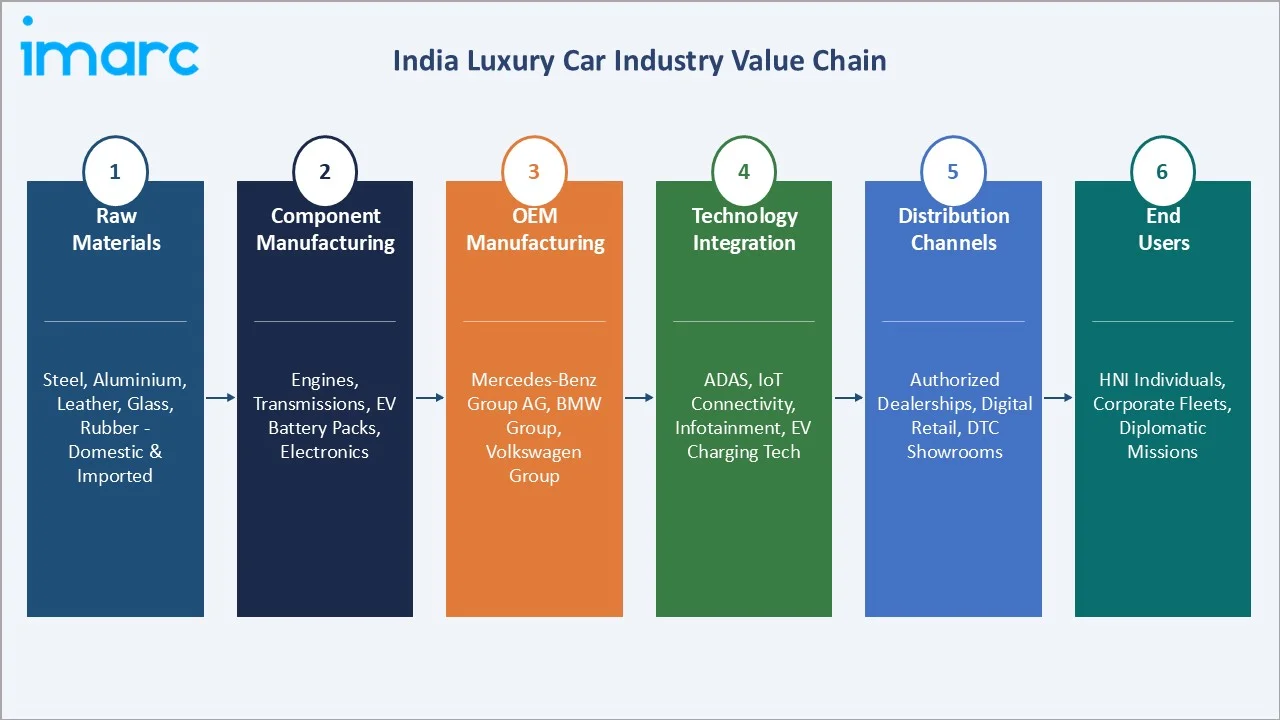

Industry Value Chain Analysis

|

Stage |

Key Players / Description |

|

Raw Materials |

Steel, Aluminium, Leather, Glass, Rubber – sourced from domestic and imported suppliers |

|

Component Manufacturing |

Supplying engines, transmissions, EV battery packs, and electronics |

|

OEM Manufacturing |

Mercedes-Benz Group AG, BMW Group, Volkswagen Group, Geely Auto, Jaguar Land Rover Automotive PLC |

|

Technology Integration |

ADAS systems, IoT connectivity, infotainment, EV charging tech integration |

|

Distribution Channels |

Authorized dealerships, digital retail platforms, direct-to-consumer showrooms |

|

End Users |

HNI individuals, corporate fleets, diplomatic missions, chauffeur-driven services |

OEMs hold the highest strategic value by delivering integrated mobility solutions combining performance, technology, and brand experience. Meanwhile, digital and direct-to-consumer channels are reshaping distribution, enabling automakers to bypass intermediaries, strengthen customer engagement, and capture higher margins.

Technology Landscape in the India Luxury Car Industry

Electric Vehicle (EV) Technology

The EV powertrain revolution is central to India luxury car market trends. Battery energy density improvements are extending range beyond 500 km per charge. Mercedes-Benz's EQXX concept demonstrated 1,000 km range, signaling near-term commercial potential.

Materials Innovation

Ultra-high-strength steel (UHSS) and carbon-fiber composites are replacing traditional steel in structural components, reducing vehicle weight while improving crash safety. Sustainable interior materials – recycled leather, bio-based plastics, and Alcantara alternatives – are gaining prominence in luxury vehicle launches.

Smart Connectivity

5G-enabled connected vehicles with over-the-air (OTA) software update capability are becoming standard in the luxury segment. Mercedes-Benz's MBUX Hyperscreen, BMW iDrive 9, and Audi MMI Touch are benchmark infotainment platforms.

Automation and ADAS

Level 2+ autonomous driving features – including adaptive cruise control, lane-keep assist, automated parking, and highway pilot – are standard in luxury vehicles above premium price points. BMW Highway Assistant and Volvo Pilot Assist are particularly popular with India’s chauffeur-driven luxury segment.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

Sports Utility Vehicle |

57.0% |

2025 |

|

Fuel Type |

Gasoline |

56.0% |

2025 |

|

Price Range |

High-End |

40.0% |

2025 |

|

Engine Capacity |

Upto 3,000 CC |

77.0% |

2025 |

|

Region |

West and Central India |

28.4% |

2025 |

Breakup by Vehicle Type

Sports Utility Vehicles (SUVs) dominate with 57.0% share in 2025. The segment is driven by consumer preference for premium utility, higher driving position, and family versatility. BMW X5, Mercedes GLC, and Volvo XC90 are volume leaders.

To access detailed market analysis, Request Sample

Sedans hold 26.4% share in 2025. The Mercedes-Benz E-Class, BMW 5 Series, and Audi A6 remain aspirational benchmarks for executive buyers. Sedan sales are modestly declining as SUV appeal broadens, but the ultra-luxury sedan segment (S-Class, 7 Series) remains resilient.

Hatchbacks account for 16.6% share in 2025, primarily driven by Mini (BMW Group) and Audi A1 class vehicles. This segment appeals to younger, urban luxury first-buyers.

Breakup by Fuel Type

Gasoline vehicles lead at 56.0% share in 2025, supported by broader model availability and the well-established refueling infrastructure across India's tier-1 and tier-2 markets.

Diesel accounts for 28.3% of luxury car sales in 2025. Despite stricter emission norms (BS-VI Phase II from 2023), diesel retains a loyal customer base among high-mileage corporate and fleet buyers, particularly for long-wheelbase models.

Electric vehicles hold 15.7% share in 2025. Government FAME III subsidies, corporate ESG mandates, and expanding DC fast-charging networks are the primary demand catalysts.

Regional Market Insights

|

Region |

Market Share (2025) |

Key Drivers |

Major Cities / States |

|

West and Central India |

28.4% |

Highest HNI density; strong dealership network; financial hub Mumbai |

Maharashtra, Gujarat, Rajasthan, MP |

|

South India |

27.3% |

Tech economy growth; Bangalore startup wealth; NRI remittance wealth |

Karnataka, TN, Telangana, Kerala |

|

North India |

26.0% |

Political and business capital; old-money wealth concentration; Punjab affluence |

Delhi-NCR, UP, Punjab, Haryana |

|

East India |

18.3% |

Emerging HNI segment; Kolkata old economy wealth; growing corporate sector |

West Bengal, Odisha, Jharkhand |

West and Central India commands the largest share at 28.4% in 2025, anchored by Mumbai's financial capital status and Pune's growing tech-manufacturing corridor. Maharashtra alone contributes approximately 18% of total India luxury car market revenue.

South India at 27.3% reflects the rapid wealth creation in India's IT/tech ecosystem – Hyderabad and Bangalore are the two fastest-growing luxury car markets nationally as of 2025. The two regions combined (West+South) represent over 55% of total luxury car sales.

North India at 26.0% is driven primarily by Delhi-NCR, which accounts for approximately 16% of national luxury vehicle sales. The National Capital Region hosts the highest concentration of luxury car authorized dealerships in India.

East India at 18.3% represents the smallest but emerging regional market. Kolkata and Bhubaneswar are witnessing increasing luxury dealership openings as HNI wealth creation in eastern India accelerates post-2022.

Competitive Landscape

|

Company Name |

Brand Name |

Market Position |

Remarks |

|

Mercedes-Benz Group AG |

Mercedes-Benz / EQ |

Market Leader |

Largest luxury car seller in India since 2015; EV portfolio expanding |

|

BMW Group |

BMW |

Market Leader |

Strong SUV lineup; leading in electric luxury with iX, i4 |

|

Volkswagen Group |

Audi, Porsche |

Challenger |

Rebounding post-2022 restructuring; aggressive product launches in 2024-25 |

|

Geely Auto |

Volvo |

Challenger |

Leading in sustainability; highest EV share among luxury brands in India |

|

Jaguar Land Rover Automotive PLC |

Jaguar / Land Rover |

Established |

Strong SUV demand via Discovery, Defender; Range Rover ultra-luxury leader |

|

Lexus |

Lexus |

Emerging |

Japanese luxury alternative gaining traction; strong hybrid portfolio |

|

Stellantis India Private Limited |

Jeep |

Challenger |

Compass and Meridian in premium-near-luxury zone; expanding distribution |

The India luxury car market’s competitive landscape is moderately concentrated, with global premium automakers competing alongside niche luxury and performance brands. Leading players compete on product innovation, electrification, brand positioning, dealership experience, and aftersales service capabilities.

Key Company Profiles

Mercedes-Benz Group AG

Mercedes-Benz Group AG is a German multinational automotive company and one of the world’s leading luxury vehicle manufacturers. Headquartered in Stuttgart, Germany, the company designs, manufactures, and sells premium passenger cars, luxury SUVs, vans, and electric vehicles under the Mercedes-Benz and Mercedes-AMG brands.

- Product Portfolio: A-Class, C-Class, E-Class, S-Class sedans; GLA, GLC, GLE, GLS, G-Class SUVs; and EQ electric vehicle portfolio including EQB, EQS.

- Recent Developments: In 2026, Mercedes-Benz Group AG has launched two new performance-focused models in India—the Mercedes-AMG A45 S Aero Track Edition 4MATIC+ and the Mercedes-AMG GLE 53 Coupe Performance Edition—expanding its top-end luxury portfolio. The company highlighted strong demand for its premium offerings, driven by exclusivity, personalization, and sustained interest across both AMG and core model lines such as the C-Class, E-Class, GLC, and GLE.

- Strategic Focus: Market leadership through product breadth, localization of EV manufacturing, and premium retail experience.

BMW Group

BMW Group is a German multinational premium automotive company headquartered in Munich, Germany. It is one of the world’s leading luxury vehicle manufacturers, producing premium automobiles and motorcycles under the BMW, MINI, and Rolls-Royce brands.

- Product Portfolio: BMW 2, 3, 5, 7 Series sedans; X1, X3, X5, X7 SUVs; Mini hatchbacks; and BMW i electric range including iX, i4, i7.

- Recent Developments: In 2026, BMW Group plans a major expansion in the Indian luxury car market, including the launch of 10 new cars and increased local sourcing to strengthen its presence and improve cost efficiency. The strategy is aimed at scaling its portfolio across EVs and MINI models while targeting the country’s fast-growing premium segment.

- Strategic Focus: Driving performance heritage paired with electrification; expanding BMW i sub-brand as the primary EV growth vehicle in India.

Jaguar Land Rover Automotive PLC

Jaguar Land Rover Automotive PLC is a British multinational automotive company and a subsidiary of Tata Motors Limited. Headquartered in Coventry, United Kingdom, it operates two iconic luxury automotive brands Jaguar and Land Rover focused on premium sedans, performance cars, and luxury SUVs.

- Product Portfolio: Jaguar F-Pace, F-Type; Land Rover Defender, Discovery, Discovery Sport, Range Rover, Range Rover Sport, Range Rover Velar, Range Rover Evoque.

- Recent Developments: In 2025, Jaguar Land Rover Automotive PLC is preparing a major electric vehicle push in India with two key launches planned for 2026, marking its entry into the next phase of luxury electrification. According to the upcoming product roadmap, the lineup will include the Range Rover Electric and an all-new Jaguar electric 4-door GT, both built on advanced EV platforms aimed at high-performance luxury positioning.

- Strategic Focus: Ultra-luxury SUV market dominance; electrification roadmap includes all-electric Range Rover by 2026; strengthening tier-2 city presence.

Market Concentration Analysis

The India luxury car market is moderately concentrated, with the top-5 players – Mercedes-Benz Group AG, BMW Group, Volkswagen Group, Geely Auto, Jaguar Land Rover Automotive PLC – collectively accounting for approximately 85% of total market revenue in 2025.

Luxury car market industry analysis identifies consolidation at the ultra-luxury tier, where Rolls-Royce Motor Cars, Bentley Motors, Porsche, and Ferrari operate in a collectively stable niche despite accounting for limited annual unit volumes.

Strategic M&A activity is limited in this market, as global OEMs operate through wholly owned subsidiaries. The primary consolidation trend is dealership network rationalization, with OEMs reducing dealer presence in underperforming geographies while expanding into high-potential tier-2 markets.

Investment & Growth Opportunities

- Electric Luxury Vehicle (ELV) Manufacturing – Domestic EV assembly of luxury models qualifies for PLI (Production-Linked Incentive) benefits, offering subsidies for OEMs investing above INR 4,150 Crore.

- Tier-2 City Dealership Expansion – Cities like Surat, Coimbatore, Vizag, and Jaipur represent underpenetrated luxury car markets with growing high-net-worth individual bases, making them key expansion hubs for luxury OEMs.

- Luxury Fleet and Subscription Services – Corporate India's growing preference for managed fleet and luxury car subscription services (Mercedes-Benz Flexi-Use, BMW Subscribe) creates recurring revenue streams.

- Aftersales and Digital Service Revenue – India’s installed luxury car base generates substantial aftersales, maintenance, and warranty revenue, forming a high-margin revenue stream for OEMs and service networks.

- Pre-owned Luxury Car Market – India’s certified pre-owned luxury car segment is growing steadily, with structured programs strengthening trust and accessibility in the secondary market. Mercedes-Benz India “Certified Pre-Owned” program is driving significant used luxury vehicle sales annually, reflecting rising demand for value-led premium ownership.

- Charging Infrastructure Investment – EV charging network operators serving luxury residential complexes, office parks, and hotel properties are beneficiaries of luxury EV adoption tailwinds.

Future Market Outlook (2026-2034)

The India luxury car market is projected to reach USD 2.0 Billion by 2034, growing at a CAGR of 5.09% during 2026-2034.

Technological disruption through autonomous driving, over-the-air software-defined vehicles, and AI-powered personalization is expected to redefine value propositions in the luxury segment. Premium brands investing early in India-specific digital retail and EV ecosystems are positioned for outperformance.

India luxury car market forecast models indicate that electric vehicles will capture a growing share of luxury car sales by 2034, rising significantly from current levels. SUVs will retain dominance with a majority share, supported by strong consumer preference for versatility, comfort, and status appeal. The India luxury car market size milestone is expected around the end of the decade, marking a key inflection point in the country’s transition toward a premium-first automotive ecosystem.

Research Methodology

Primary Research

IMARC's primary research methodology encompasses structured interviews with C-suite executives of luxury OEMs, authorized dealership principals, industry consultants, and HNI consumer panels. Over 50 in-depth interviews were conducted for this report across India's top-4 luxury car markets (Delhi-NCR, Mumbai, Bangalore, Hyderabad).

Secondary Research

Secondary data sources include Society of Indian Automobile Manufacturers (SIAM) registration data, Automotive Component Manufacturers Association (ACMA) reports, Ministry of Heavy Industries EV data portals, OEM annual reports, SEBI disclosures, and proprietary IMARC databases covering 15+ years of India luxury automotive market data.

Market Forecasting Models

Bottom-up and top-down approaches are combined to estimate market sizes and growth trajectories. CAGR projections are stress-tested against GDP growth scenarios, import duty sensitivity analysis, and EV adoption pace assumptions. Scenario modeling (Base, Optimistic, Conservative) ensures robust forecast banding.

India Luxury Car Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Hatchback, Sedan, Sports Utility Vehicle |

| Fuel Types Covered | Gasoline, Diesel, Electric |

| Price Ranges Covered | Entry-Level, Mid-Level, High-End, Ultra |

| Engine Capacities Covered | Upto 3,000 CC, Above 3,000 CC |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Mercedes-Benz Group AG, BMW Group, Volkswagen Group, Geely Auto, Jaguar Land Rover Automotive PLC, Lexus, Stellantis India Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Luxury Car Market Report

The India luxury car market was valued at USD 1.3 Billion in 2025, supported by rising HNI consumer base, growing SUV demand, and expanding luxury dealership networks.

The market is projected to grow at a CAGR of 5.09% during 2026-2034, reaching USD 2.0 Billion by 2034 driven by EV adoption and income growth.

Key trends include SUV dominance, electric vehicle growth, digital retail expansion, ADAS technology adoption, and premiumization of entry-level luxury segment in tier-2 cities.

Sports Utility Vehicles (SUVs) hold the dominant position with 57.0% of India luxury car market share in 2025, led by BMW X5, Mercedes GLC, and Volvo XC90.

Electric vehicles are the fastest-growing fuel type, with an estimated CAGR of 8.5% during 2026-2034, supported by FAME III subsidies and expanding EV charging infrastructure.

West and Central India leads with 28.4% share in 2025, anchored by Mumbai (financial capital) and Pune. South India is a close second at 27.3%.

Key players include Mercedes-Benz Group AG, BMW Group, Volkswagen Group, Geely Auto, Jaguar Land Rover Automotive PLC, Lexus, and Stellantis India Private Limited.

Major drivers include India's growing HNI population, urbanization, rising aspirational youth segment, government EV incentives, and digital retail transformation of luxury buying experience.

Key challenges include high import duties on Completely Built Unit (CBU) vehicles (100%), limited EV charging infrastructure in non-metro areas, economic sensitivity of luxury purchases, and CAFE Phase III compliance costs.

The India luxury car market is projected to reach USD 1.6 Billion by 2030, growing at a steady 5.09% CAGR as EV luxury adoption accelerates and tier-2 city markets mature.

Electric vehicles represented 15.7% of India luxury car sales in 2025. supported by accelerating premium electrification and expanding model availability from leading OEMs.

Industry analysis indicates structural demand growth driven by demographics and digital commerce, moderate market concentration (top-5 at ~85% share), and transformative EV transition over 2026-2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)