India Malaria Vaccine Market Size, Share, Trends and Forecast by Vaccine Type, Route of Administration, and Region, 2026-2034

India Malaria Vaccine Market Size, Share, Trends & Forecast (2026-2034)

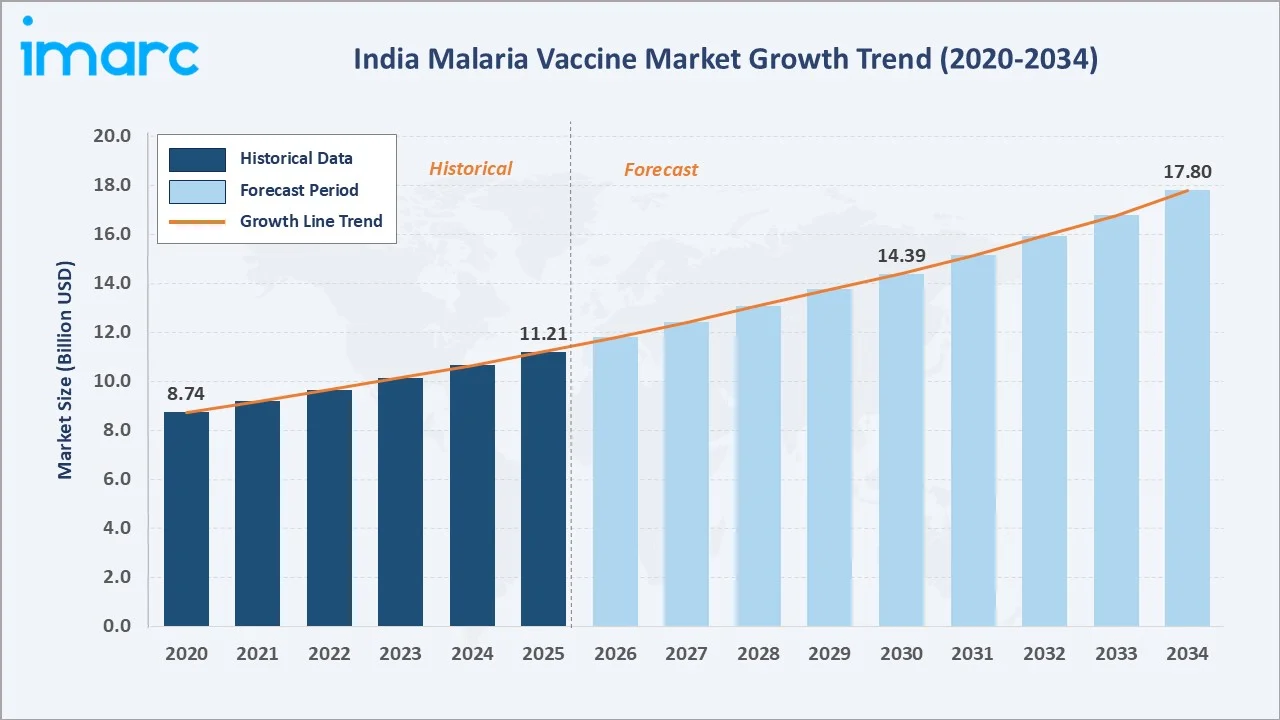

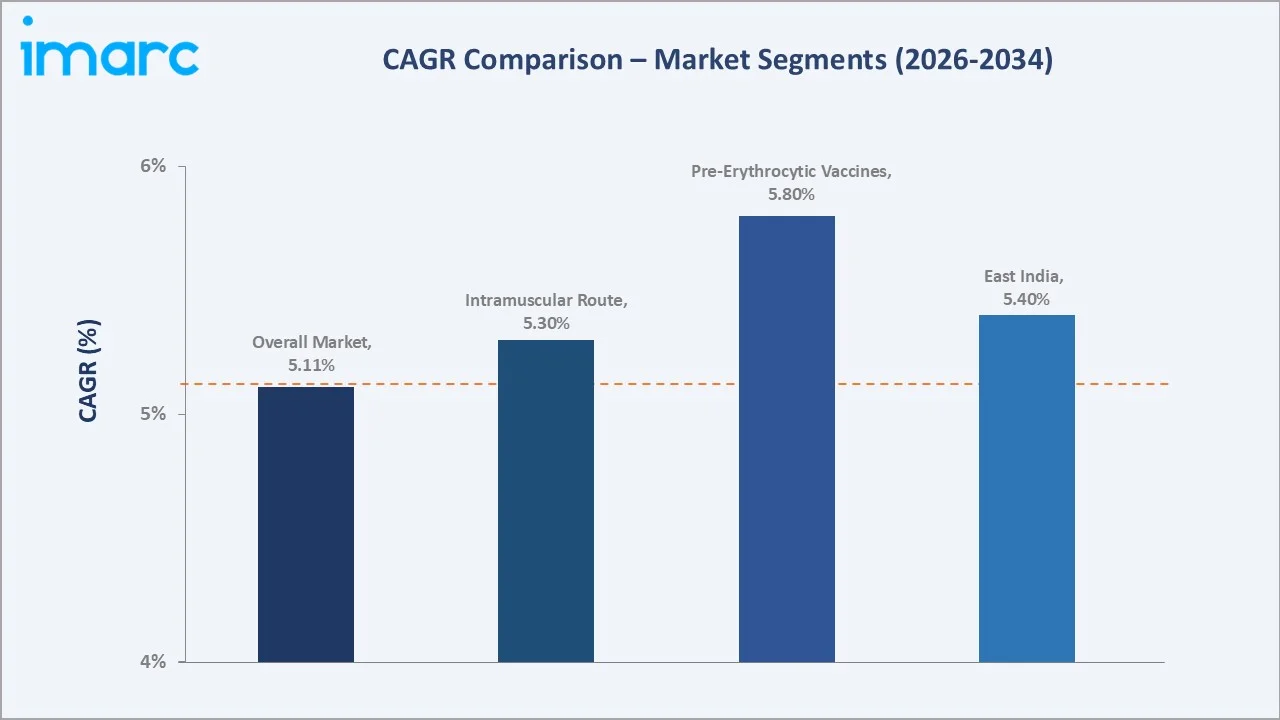

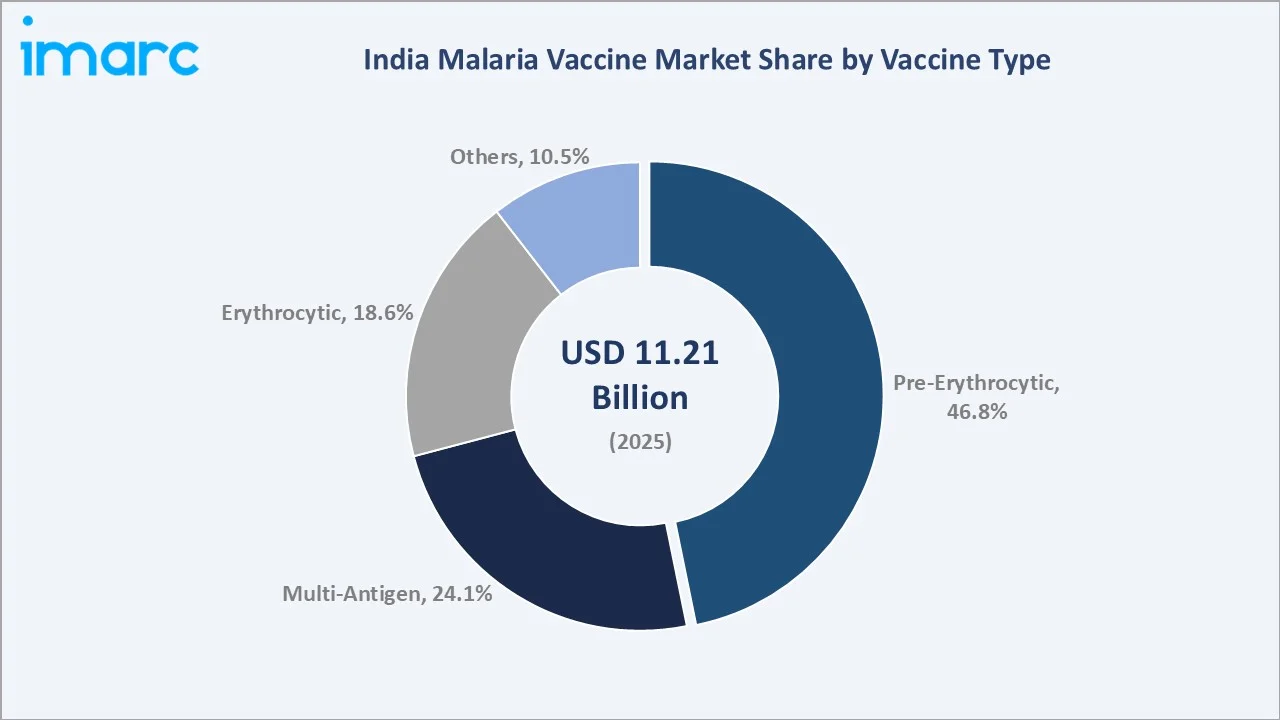

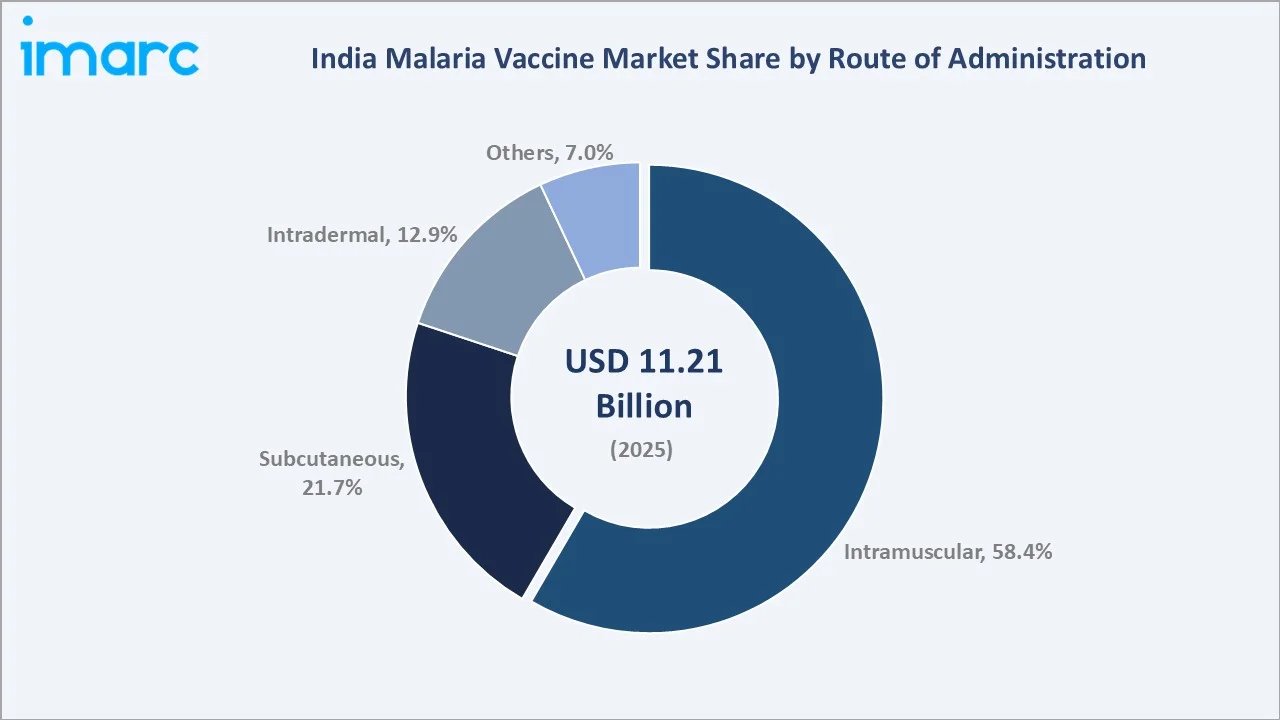

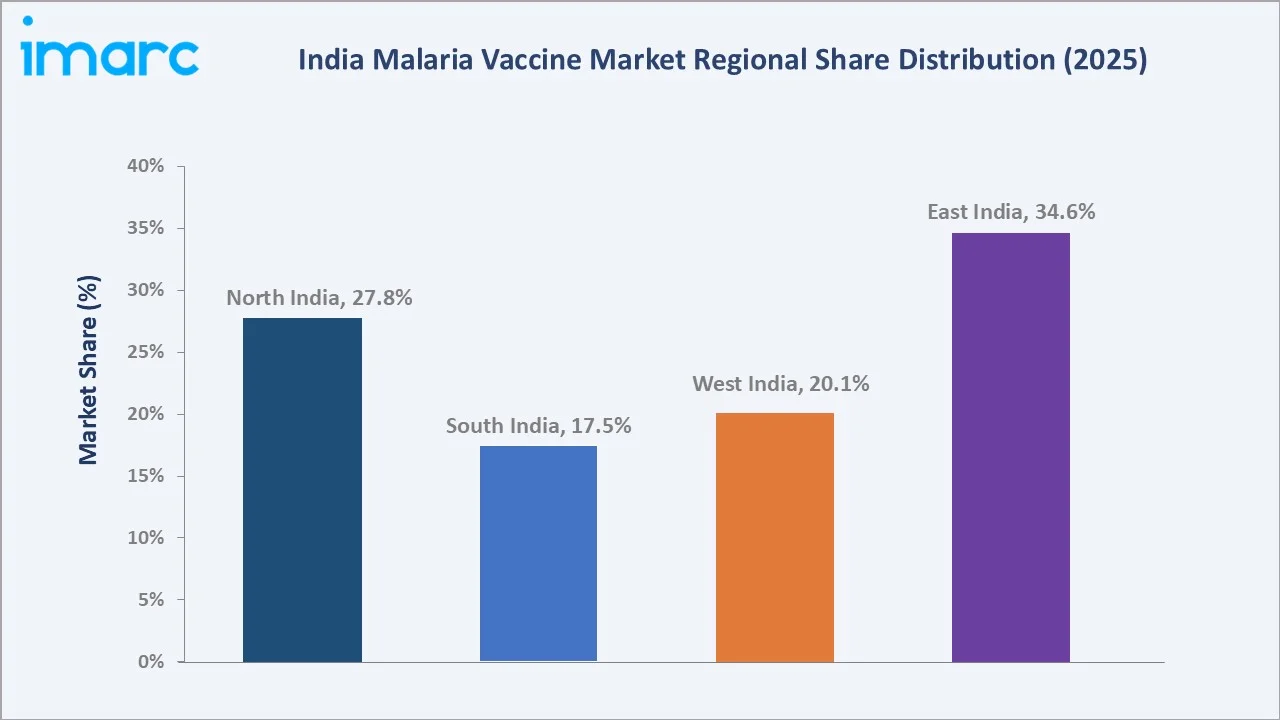

The India malaria vaccine market size reached USD 11.21 Billion in 2025 and is projected to reach USD 17.80 Billion by 2034, growing at a CAGR of 5.11% during 2026-2034. The market is driven by active government-led immunization programs, WHO-recommended vaccines, and expanding public-private collaborations. India has reduced malaria cases by over 97% since independence and officially exited the WHO's High Burden to High Impact group. Pre-Erythrocytic vaccines lead with 46.8% share, intramuscular administration commands 58.4%, and East India dominates regionally at 34.6% (2025).

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.21 Billion |

|

Forecast Market Size (2034) |

USD 17.80 Billion |

|

CAGR (2026-2034) |

5.11% |

|

Largest Region (2025) |

East India (34.6%) |

|

Dominant Vaccine Type |

Pre-Erythrocytic (46.8%, 2025) |

|

Leading Route of Administration |

Intramuscular (58.4%, 2025) |

To get more information on this market, Request Sample

The India malaria vaccine market expanded from USD 8.74 Billion in 2020 to USD 11.21 Billion in 2025, anchored at USD 14.39 Billion in 2030, and forecast to reach USD 17.80 Billion by 2034. The market trajectory reflects accelerating adoption of WHO-recommended vaccines, enhanced cold chain infrastructure, and sustained government commitment to malaria elimination by 2030 under the National Framework for Malaria Elimination (NFME) 2016-2030.

Executive Summary

The India malaria vaccine market reached USD 11.21 Billion in 2025 and is poised for steady expansion, driven by sustained government policy support and increasing vaccine adoption. The National Strategic Plan (NSP) for Malaria Elimination 2023-2027, backed by the Ministry of Health and Family Welfare (MoHFW), is focusing on “Testing, Treating, and Tracking" strategy, vector control, and surveillance to achieve zero indigenous cases. By the end of 2025, 160 districts in 23 states and union territories had reported zero indigenous malaria cases between 2022 and 2024, reflecting systematic progress toward India's 2027 interim elimination target.

Vaccine innovation is a core growth driver. The WHO recommendation of R21/Matrix-M (developed by the University of Oxford and Serum Institute of India) in October 2023, alongside the existing RTS,S/AS01 (Mosquirix), has significantly expanded the available vaccine toolkit. Serum Institute of India has established production capacity for up to 100 million doses per annum, ensuring supply security for large-scale immunization programs. Pre-Erythrocytic vaccines dominate market share at 46.8% in 2025 due to their established efficacy in targeting the sporozoite life stage of Plasmodium falciparum.

Regionally, East India leads with 34.6% market share in 2025, reflecting historically high malaria burden in states such as Odisha, Jharkhand, Chhattisgarh, and the northeastern region. North India holds 27.8% share, West India 20.1%, and South India 17.5%. The market outlook through 2034 is positive, supported by rising healthcare spending, expanding public-private partnerships, and the GAVI-backed vaccine procurement framework strengthening affordable access across high-burden districts.

Key Market Insights

|

Insight |

Data |

|

Largest Vaccine Type Segment |

Pre-Erythrocytic - 46.8% share (2025) |

|

Leading Route of Administration |

Intramuscular - 58.4% market share (2025) |

|

Leading Region |

East India - 34.6% share (2025) |

|

Fastest Growing Segment |

Multi-Antigen Vaccines (~6.2% CAGR, 2026-2034) |

|

Top Companies |

Serum Institute of India, Bharat Biotech, and Indian Immunologicals Ltd. |

Key Analytical Observations Supporting the Above Data:

- Pre-Erythrocytic vaccines at 46.8%: This segment leads due to the proven clinical efficacy of vaccines targeting the sporozoite and liver stages of the Plasmodium falciparum parasite, limiting infection before it reaches the bloodstream. RTS,S/AS01 and R21/Matrix-M, both pre-erythrocytic vaccines, are the only two WHO-recommended malaria vaccines globally as of 2025.

- Intramuscular route at 58.4%: Intramuscular (IM) administration dominates due to superior bioavailability, faster immune response, and compatibility with standard immunization protocols used in India's national vaccination programs.

- East India at 34.6%: East India leads regionally as it encompasses the highest malaria burden states - Odisha, Jharkhand, West Bengal, and the northeastern region - which together accounted for the majority of India's reported malaria cases historically.

- Multi-Antigen vaccines at 6.2% CAGR: Multi-antigen approaches are growing fastest as they target multiple parasite life stages simultaneously, improving vaccine efficacy and reducing the risk of parasite escape. Active pipeline development from government R&D institutions and private players is accelerating this segment.

- Market Opportunity: Tribal and forested districts contribute approximately 32% of India's malaria cases per PMC data, representing an underserved priority zone for vaccine deployment. GAVI-funded procurement and cold chain expansion in these regions represents the most commercially significant near-term opportunity.

India Malaria Vaccine Market Overview

The India malaria vaccine market is defined by the procurement, distribution, and administration of preventive vaccines against malaria, a mosquito-borne disease caused primarily by Plasmodium falciparum and Plasmodium vivax. The market ecosystem integrates pharmaceutical R&D institutions, government health agencies (MoHFW, NVBDCP), international organizations (WHO, GAVI, UNICEF), domestic and multinational vaccine manufacturers, cold chain infrastructure providers, and public immunization centers. India accounts for approximately 73.3% of the estimated 2.7 million malaria cases in the WHO South-East Asia Region, underscoring the scale of market demand. Macroeconomic influences include rising Union Budget allocations to healthcare, GAVI co-financing frameworks, and the operationalization of the National Strategic Plan for Malaria Elimination 2023-2027.

Market Dynamics

To evaluate market opportunities, Request Sample

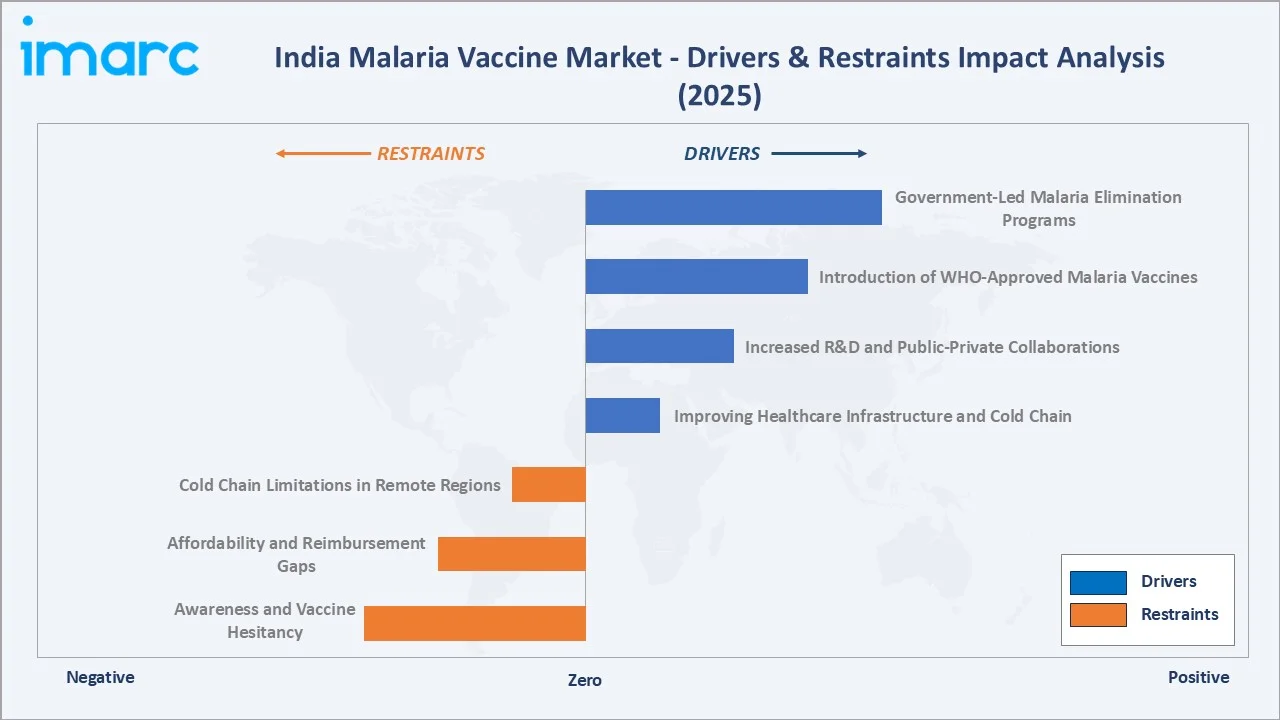

Market Drivers

- Government-Led Malaria Elimination Programs: India's National Framework for Malaria Elimination (NFME) 2016-2030, implemented by the National Vector Borne Disease Control Programme (NVBDCP) under the MoHFW, is the primary structural driver of vaccine market growth. The framework targets zero indigenous malaria cases nationally by 2030. The interim 2027 target of interrupting transmission across all high-burden states and UTs has accelerated government spending on vaccines, diagnostics, and vector control. By end-2025, 160 districts in 23 states/UTs reported zero indigenous cases between 2022-2024. India has achieved over a 70% reduction in malaria cases compared to 2015 levels (2024 data, WHO). This sustained policy commitment ensures consistent public procurement of malaria vaccines, providing a structurally stable demand base for the market.

- Introduction of WHO-recommended Malaria Vaccines: The WHO recommendation of R21/Matrix-M in October 2023, developed by the University of Oxford and the Serum Institute of India with Novavax's Matrix-M adjuvant, significantly expanded India's vaccine supply options. Serum Institute of India (the world's largest vaccine manufacturer by dose volume, producing 3.5 billion doses annually) has established annual production capacity of 100 million doses for R21/Matrix-M. Phase III trials across four African countries demonstrated 78% average vaccine efficacy in 5-17 month-old children. Combined with the existing RTS,S/AS01 (Mosquirix) from GlaxoSmithKline, India now has two WHO-backed tools for large-scale immunization, directly expanding market addressability and procurement volumes.

- Increased R&D and Public-Private Collaborations: Rising investment in malaria vaccine R&D, facilitated through public-private partnerships between government agencies, global health organizations, and pharmaceutical companies, is advancing next-generation vaccine development. Collaborations between institutions like the Indian Council of Medical Research (ICMR), NVBDCP, WHO India, and private vaccine manufacturers are accelerating clinical trials for multi-antigen and blood-stage vaccines. GAVI's Advance Market Commitment (AMC) for malaria vaccines, alongside UNICEF procurement support post-WHO prequalification, is reducing financial barriers for domestic adoption and encouraging manufacturers to scale Indian production capacity.

- Improving Healthcare Infrastructure and Cold Chain: Expansion of cold chain infrastructure under India's Intensified Mission Indradhanush (IMI) program and Electronic Vaccine Intelligence Network (eVIN) is improving last-mile vaccine delivery in remote and tribal areas. Enhanced cold chain reach in high-burden northeastern and central Indian states is directly enabling wider malaria vaccine distribution in regions where traditional immunization coverage has been limited.

Market Restraints

- Cold Chain Limitations in Remote Regions: Malaria-endemic districts in forested and tribal areas of Odisha, Jharkhand, West Bengal, and the northeast often lack reliable cold chain infrastructure, limiting effective vaccine distribution. These regions simultaneously represent the highest-burden zones requiring maximum vaccine coverage.

- Affordability and Reimbursement Gaps: While government programs provide free vaccines, privately administered doses remain unaffordable for a significant portion of the population in endemic areas. Limited private health insurance penetration in rural India constrains market expansion beyond the public procurement channel.

- Awareness and Vaccine Hesitancy: Low awareness of malaria vaccines in rural communities, compounded by existing hesitancy toward novel vaccine formulations, reduces uptake rates and challenges immunization program effectiveness in target populations.

Market Opportunities

- Expansion of GAVI-Funded Procurement: GAVI co-financing frameworks enable large-scale, affordable procurement for India's public immunization programs. As India qualifies for transitional GAVI support, structured procurement agreements represent a significant revenue opportunity for domestic vaccine manufacturers including Serum Institute of India and Bharat Biotech.

- Multi-Antigen Vaccine Pipeline Development: Active pipeline development of multi-antigen vaccines targeting blood-stage and sexual-stage parasites represents a next-generation product opportunity. Clinical success in this segment could create an entirely new sub-market and position India-based manufacturers at the forefront of global malaria vaccine innovation.

- Tribal District Health Mission Scaling: India's National Health Mission (NHM) Tribal Sub-Plan specifically targets healthcare access in forested districts. Scaling malaria vaccination under NHM in approximately 200 highly endemic tribal districts represents a systematic, policy-backed expansion opportunity through 2034.

Market Challenges

- Parasite Resistance and Strain Variability: Plasmodium falciparum's ability to evolve resistance and India's co-existence of both P. falciparum and P. vivax strains complicate single-vaccine efficacy. Vaccines approved for P. falciparum provide no cross-protection against P. vivax, the second dominant strain in India.

- Logistics Complexity in High-Burden Zones: Many of the highest malaria burden districts are geographically inaccessible, particularly post-monsoon, creating operational challenges for sustained 4-dose vaccine regimen delivery. Dropout rates between primary and booster doses reduce effective population immunity and program cost-efficiency.

Emerging Market Trends

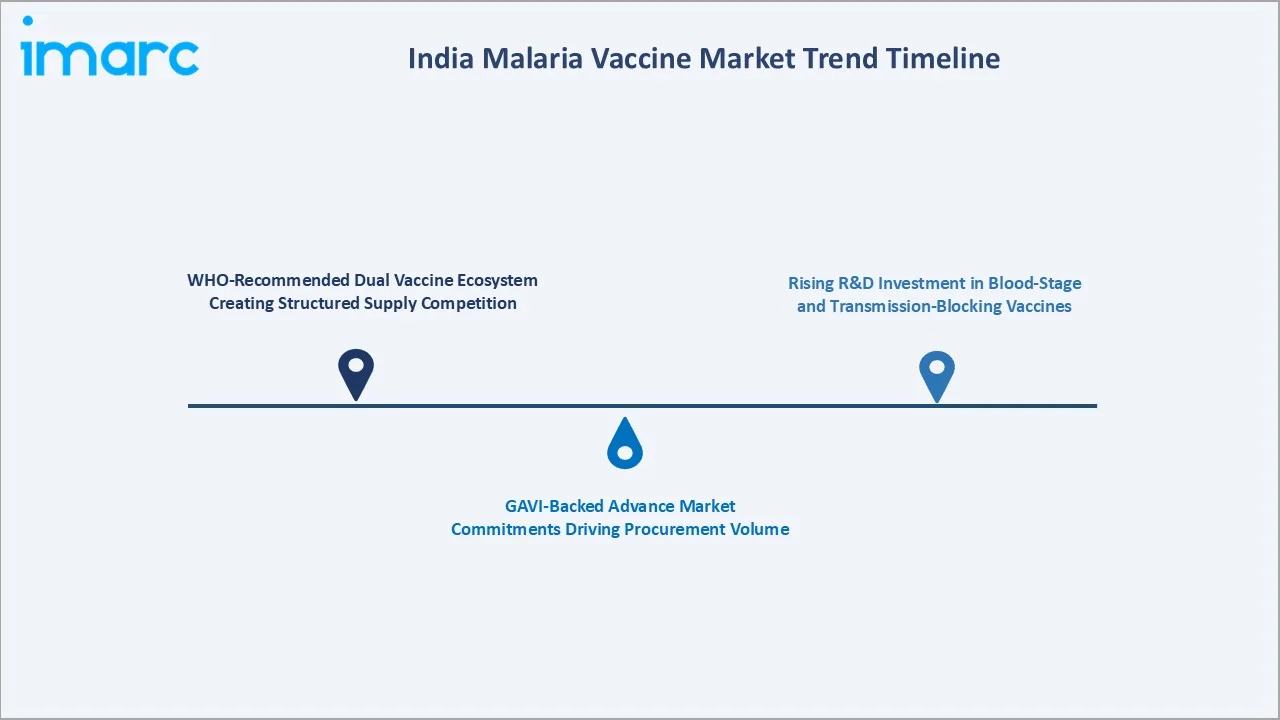

1. WHO-recommended Dual Vaccine Ecosystem Creating Structured Supply Competition

The co-existence of two WHO-recommended malaria vaccines, RTS,S/AS01 (GlaxoSmithKline) and R21/Matrix-M (Oxford/Serum Institute of India), is creating a structurally competitive supply environment that is improving affordability and procurement flexibility. R21/Matrix-M is priced below USD 4 per dose, compared to approximately USD 9 for RTS,S/AS01, creating a significant cost advantage for public procurement programs in India. Competitive supply is accelerating government program scalability and positioning Serum Institute of India as a dominant domestic supplier.

2. Rising R&D Investment in Blood-Stage and Transmission-Blocking Vaccines

Government funding through ICMR and international collaborations are accelerating research into blood-stage vaccines (targeting Plasmodium in the bloodstream post-liver infection) and transmission-blocking vaccines (reducing mosquito infection rates). These next-generation approaches address current vaccine limitations. India contributed to 51% of global P. vivax cases in 2016 (PMC, 2022), driving particular urgency for P. vivax-specific or multi-species vaccine development - an area where Indian research institutions and manufacturers hold emerging competitive positioning.

3. GAVI-Backed Advance Market Commitments Driving Procurement Volume

GAVI's Advance Market Commitment (AMC) mechanism for malaria vaccines, which guarantees a minimum purchase price to manufacturers delivering vaccines at reduced rates to eligible countries, is a critical commercial trend. As India operationalizes its malaria vaccine programs, GAVI-affiliated procurement support reduces financial risk for domestic manufacturers and enables large batch production planning. This trend is directly supporting Serum Institute of India's capacity planning at 100 million doses annually.

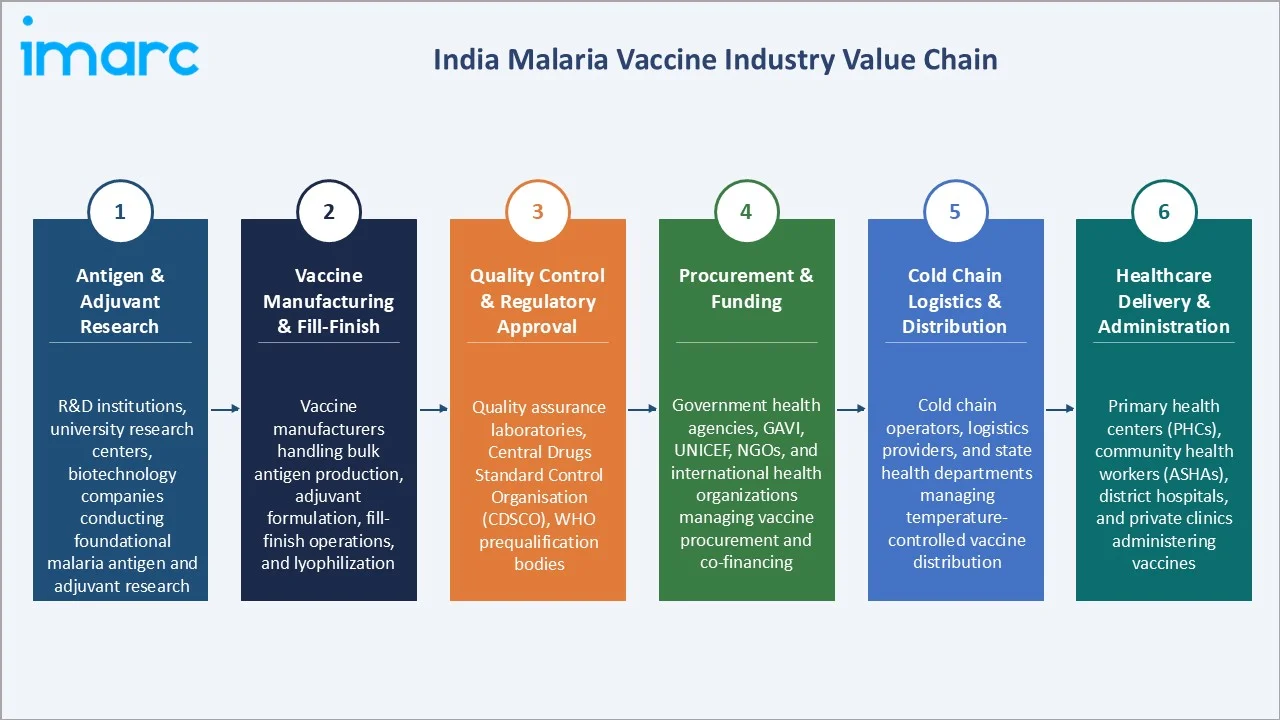

Industry Value Chain Analysis

|

Stage |

Key Participants |

|

Antigen & Adjuvant Research |

R&D institutions, university research centers, biotechnology companies conducting foundational malaria antigen and adjuvant research |

|

Vaccine Manufacturing & Fill-Finish |

Vaccine manufacturers handling bulk antigen production, adjuvant formulation, fill-finish operations, and lyophilization |

|

Quality Control & Regulatory Approval |

Quality assurance laboratories, Central Drugs Standard Control Organisation (CDSCO), WHO prequalification bodies |

|

Procurement & Funding |

Government health agencies, GAVI, UNICEF, NGOs, and international health organizations managing vaccine procurement and co-financing |

|

Cold Chain Logistics & Distribution |

Cold chain operators, logistics providers, and state health departments managing temperature-controlled vaccine distribution |

|

Healthcare Delivery & Administration |

Primary health centers (PHCs), community health workers (ASHAs), district hospitals, and private clinics administering vaccines |

The India malaria vaccine value chain is characterized by a strong public sector procurement model, with government agencies and international organizations (GAVI, UNICEF) as dominant buyers. The cold chain logistics stage is the most operationally challenging, particularly for distribution to tribal and forested districts where continuous electricity supply is unreliable. Value chain integrity at the healthcare delivery stage is critical - effective 4-dose regimen completion requires robust community health worker engagement and ASHA-led follow-up systems.

Technology Landscape in the India Malaria Vaccine Industry

Pre-Erythrocytic Vaccine Technologies

Pre-erythrocytic vaccine technologies, targeting the sporozoite and liver stages of Plasmodium falciparum before blood infection, represent the most advanced and commercially deployed segment. RTS,S/AS01 uses the circumsporozoite protein (CSP) of P. falciparum fused to HBsAg as a recombinant protein, adjuvanted with AS01 to elicit strong immune responses. R21/Matrix-M improves on this design by increasing the CSP-to-HBsAg ratio and utilizing Novavax's Matrix-M saponin-based adjuvant, achieving 78% average Phase III efficacy. This technology forms the foundation of India's current malaria vaccine market, and continued refinement of CSP-based antigen presentation is the most active area of vaccine R&D.

Multi-Antigen and Blood-Stage Vaccine Research

Multi-antigen vaccines are under active development, targeting antigens across multiple parasite life stages simultaneously, circumsporozoite protein (pre-erythrocytic), merozoite surface proteins (blood-stage), and gametocyte antigens (sexual stage). This multi-target approach can significantly improve population-level efficacy and reduce parasite escape mechanisms. ICMR and international academic consortia are conducting India-based trials on blood-stage candidate vaccines, which would complement pre-erythrocytic vaccines and address P. vivax specifically - a critical gap given India's dual P. falciparum and P. vivax burden.

Adjuvant Technology Innovations

Adjuvant technologies play a critical role in malaria vaccine efficacy. Novavax's Matrix-M saponin-based adjuvant, incorporated in R21/Matrix-M, stimulates antigen-presenting cells at the injection site and enhances antigen presentation in lymph nodes, producing significantly higher antibody titers than non-adjuvanted formulations. AS01 (used in RTS,S) combines MPL and QS-21 to activate innate and adaptive immunity. Ongoing research in adjuvant optimization aims to extend vaccine efficacy duration, reduce required booster doses, and maintain protective immunity in younger age groups - critical for India's infant immunization programs.

Cold Chain and Vaccine Stability Technology

Thermostability innovation is an emerging technology priority for India's malaria vaccine market, given the cold chain challenges in remote endemic districts. Research into heat-stable formulations and novel delivery mechanisms (microencapsulation, microneedle patch delivery) could significantly reduce cold chain dependency and improve last-mile accessibility in areas where India's malaria burden is highest.

Market Segmentation Analysis

The report also covers the following market segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vaccine Type |

Pre-Erythrocytic |

46.8% |

2025 |

|

Route of Administration |

Intramuscular |

58.4% |

2025 |

|

Region |

East India |

34.6% |

2025 |

By Vaccine Type

Pre-Erythrocytic vaccines lead at 46.8% in 2025. This segment encompasses the two WHO-recommended malaria vaccines - RTS,S/AS01 and R21/Matrix-M - which target the sporozoite life stage of Plasmodium falciparum. Their dominance reflects the maturity of pre-erythrocytic antigen technology, established clinical evidence base, and integration into government immunization programs. The segment benefits from Serum Institute of India's 100 million dose annual production capacity for R21/Matrix-M, ensuring supply scalability for national programs.

To access detailed market analysis, Request Sample

Multi-Antigen vaccines hold 24.1% share and are the fastest-growing segment at approximately 6.2% CAGR during 2026-2034, driven by ongoing pipeline development and their superior potential to provide broader parasite stage coverage. Erythrocytic vaccines account for 18.6%, primarily serving blood-stage treatment-complementary approaches. The Others segment, at 10.5%, includes transmission-blocking vaccines and emerging experimental candidates in early clinical stages.

By Route of Administration

Intramuscular (IM) route leads at 58.4% in 2025. IM administration is the standard delivery route for both RTS,S/AS01 and R21/Matrix-M as per WHO recommended protocols. The IM route provides optimal antigen uptake, consistent dose delivery, and compatibility with India's standard vaccination protocols under the numerous immunization programs. Healthcare worker training for IM administration is well-established across India's 1.5 lakh primary health centers, supporting consistent and scalable delivery.

Subcutaneous (SC) administration holds 21.7% share, used in specific trial protocols and select vaccine formulations where SC delivery provides equivalent immunogenicity. Intradermal (ID) delivery accounts for 12.9%, attracting interest for dose-sparing strategies that could significantly reduce vaccine costs in large-scale programs. The Others segment at 7.0% includes experimental oral and transdermal delivery approaches in early research stages.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

East India |

34.6% |

Highest historical malaria burden in Odisha, Jharkhand, West Bengal, and northeastern states. Government priority region for NVBDCP interventions and vaccine rollout under NFME 2016-2030. |

|

North India |

27.8% |

Covers high-population states with urban-rural malaria exposure gradient. Strong NVBDCP district-level programs and improving healthcare infrastructure drive vaccine uptake. |

|

West India |

20.1% |

Includes Maharashtra, Gujarat, and Rajasthan with moderate malaria burden. Urban healthcare access supports vaccine distribution; tribal districts in Rajasthan and Maharashtra are priority targets. |

|

South India |

17.5% |

Lower overall malaria burden with focused endemic pockets in Kerala, Karnataka, and Andhra Pradesh. Strong healthcare infrastructure and high literacy support program effectiveness. |

East India's 34.6% regional dominance reflects the convergence of the highest malaria case load, the densest deployment of NVBDCP resources, and the most active government vaccination programs. States like Odisha have been at the forefront of India's malaria elimination efforts - in 2023, 34 states/UTs achieved an annual parasite incidence (API) of less than one, with Tripura (5.69 API) and Mizoram (14.23 API) remaining as high-burden exceptions requiring intensified vaccine intervention.

North India's 27.8% share reflects a large addressable population base with urban transmission risk and rural district programs. West India at 20.1% encompasses Maharashtra's tribal districts (Gadchiroli, Nandurbar) that carry disproportionate malaria burden relative to state averages. South India at 17.5%, while lower in aggregate share, reflects higher vaccine program effectiveness and coverage rates driven by better healthcare access and historically lower endemicity in most southern states.

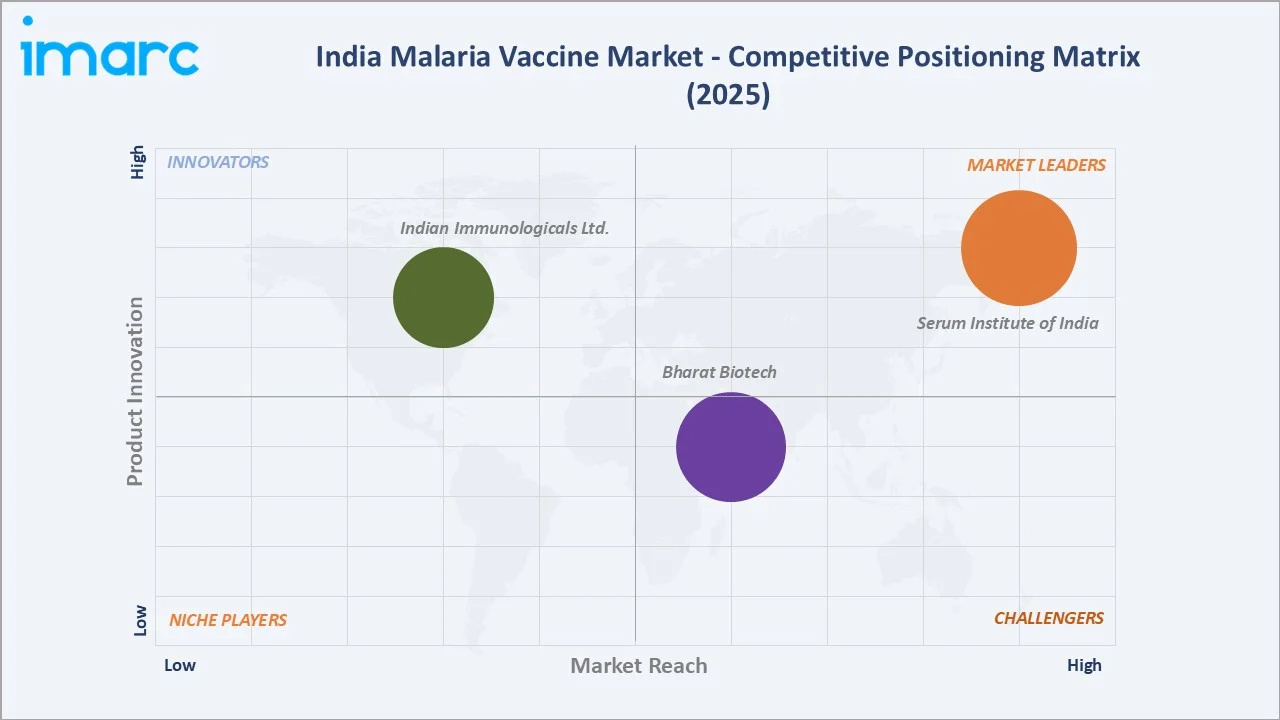

Competitive Landscape

The India malaria vaccine market competitive landscape is concentrated among a small number of global and domestic manufacturers with WHO prequalified or pipeline products. Serum Institute of India (SII) holds the dominant position as the exclusive manufacturer of the WHO-recommended R21/Matrix-M vaccine, operating 100 million doses per annum production capacity. GlaxoSmithKline entered the technology transfer agreement for RTS,S/AS01 (Mosquirix) with Bharat Biotech.

|

Company |

Key Products / Pipeline |

Market Position |

Core Strength |

|

Serum Institute of India |

R21/Matrix-M |

Market Leader |

Scaling R21/Matrix-M manufacturing; affordable pricing at under USD 4/dose for GAVI programs |

|

Bharat Biotech |

RTS,S (Mosquirix) (Antigen manufacturing) |

Emerging Challenger |

Holds the manufacturing rights from GlaxoSmithKline (GSK) for the antigen part of the RTS,S (Mosquirix) |

|

Indian Immunologicals Ltd. |

AdFalciVax (co-developed) |

Niche Player |

A recombinant, chimeric vaccine that attacks the Plasmodium falciparum parasite at multiple stages of its lifecycle. |

Key Company Profiles

Serum Institute of India

Serum Institute of India (SII) is the world's largest vaccine manufacturer by volume and holds a pivotal position in India's malaria vaccine landscape, leveraging its large-scale manufacturing capabilities, established regulatory relationships, and extensive distribution infrastructure to drive affordable malaria vaccine access across India and broader low- and middle-income country (LMIC) markets.

- Portfolio: Licensed manufacturing and supply of the R21/Matrix-M malaria vaccine

- Strategic Focus: Scaling domestic and export manufacturing of the R21/Matrix-M vaccine to meet WHO-recommended malaria immunization demand; technology transfer and cold-chain optimization for last-mile delivery in high-burden Indian states such as Odisha, Jharkhand, and West Bengal; cost-reduction strategies to sustain sub-USD 2.99 per-dose pricing for LMIC accessibility.

Bharat Biotech

Bharat Biotech is an Indian multinational biotechnology company based in Hyderabad, which is engaged in drug discovery, drug development, and the manufacture of vaccines, biotherapeutics, pharmaceuticals and healthcare products. The company partnered with GSK to transfer the technology and production of the world’s first WHO-recommended malaria vaccine, RTS,S (Mosquirix).

- Portfolio: Licensed manufacturing of the RTS,S (Mosquirix) malaria vaccine

- Strategic Focus: through process improvements and highly optimized, cost-effective manufacturing lines, the company, alongside GSK, committed to halving the vaccine's price to under $5 per dose by 2028. The company’s operations are integrated with the broader roll-out plan of Gavi, the Vaccine Alliance and the WHO to supply routine immunization programs.

Market Concentration Analysis

The India malaria vaccine market is highly concentrated at the manufacturing level, with Serum Institute of India commanding the dominant market position through exclusive R21/Matrix-M production rights. SII's 100 million dose annual production capacity makes it the single largest supplier of a WHO-recommended malaria vaccine globally by volume. This concentrated supply structure provides India with a significant domestic manufacturing advantage for national malaria vaccine programs, reducing import dependency and ensuring price control through domestic production.

At the procurement level, the market is characterized by public monopsony, the Indian government, through MoHFW and NVBDCP, is the dominant buyer of malaria vaccines. Private channel procurement remains limited given the disease's concentrated burden in low-income rural and tribal populations with limited private healthcare access. This public procurement structure creates stable, policy-driven demand but limits the market's commercial diversification beyond government program cycles.

Market concentration is evolving through two forces: SII's continued capacity scaling, reinforcing its manufacturing dominance; and emerging domestic pipeline development from Bharat Biotech, Indian Immunologicals, and other participants, gradually reducing single-supplier dependency and creating competitive pressure on pricing for public procurement programs.

Investment & Growth Opportunities

Highest Growth Segments

Multi-Antigen vaccines are the highest growth sub-segment at approximately 6.2% CAGR, driven by R&D pipeline advancement and superior clinical efficacy potential versus single-antigen approaches. Pre-Erythrocytic vaccines maintain the largest absolute revenue share but grow at a comparatively moderate 5.8% CAGR as market penetration deepens. East India represents the highest absolute growth geography given its dominant market share base of 34.6% and continued high malaria burden driving vaccine program expansion.

Emerging Investment Opportunities

- Cold Chain Infrastructure Investment: India's remotely-endemic districts represent a critical infrastructure gap. Investment in solar-powered vaccine storage units, cold chain logistics networks in tribal districts, and electronic vaccine intelligence systems (eVIN) expansion supports both market growth and public health outcomes.

- P. vivax-Targeted Vaccine Development: India's significant P. vivax burden (contributing 51% of global P. vivax cases in 2016 per PMC data) creates an unaddressed market opportunity for P. vivax-specific or multi-species vaccines. Manufacturers who develop effective P. vivax vaccines would access a commercially underserved segment with strong government procurement support.

- GAVI-Eligible Procurement Partnerships: As India evaluates GAVI-co-financed procurement for domestic malaria vaccine programs, manufacturers with GAVI supply agreements and WHO prequalification hold a structural commercial advantage. Domestic manufacturers can leverage India's existing GAVI relationship to secure favorable procurement frameworks.

- Combination and Booster Dose Market: The 4-dose regimen requirement for current malaria vaccines (primary series + booster) creates a recurring commercial opportunity. Investment in booster dose reminder systems, community health worker incentive programs, and dose completion monitoring technology addresses dropout rates and expands market revenue per vaccinated individual.

Future Market Outlook (2026-2034)

The India malaria vaccine market is projected to grow from USD 11.21 Billion in 2025 to USD 17.80 Billion by 2034, delivering a 5.11% CAGR over the forecast period. The market anchor value of USD 14.39 Billion in 2030 represents India malaria vaccine industry at a structural inflection - aligned with India's national malaria elimination target year, when government vaccination programs are expected to reach peak intensity before transitioning to prevention-of-reintroduction frameworks post-elimination.

Three structural forces define India malaria vaccine market growth through 2034: government policy momentum (NFME 2016-2030, NSP 2023-2027) providing sustained public procurement; Serum Institute of India's manufacturing scale enabling affordable supply at volume; and international partnership frameworks (GAVI, WHO, UNICEF) ensuring co-financing for affordable large-scale program delivery. India is on track to meet the WHO Global Technical Strategy (GTS) goal of reducing malaria cases by 75% by 2025 compared to 2015 levels, having already achieved over 70% reduction in 2024.

Beyond 2027, as India approaches its interim elimination target, the market dynamic may shift from high-volume primary vaccination to surveillance-focused booster programs and outbreak-response procurement. This shift will require manufacturers to adapt commercial strategies from volume-based to value-based models. The emergence of next-generation multi-antigen vaccines through 2030-2034 is expected to introduce a premium product segment, expanding the market's value beyond volume-driven growth alone.

Research Methodology

Primary Research

Primary research comprised structured interviews with India malaria vaccine industry stakeholders, including public health officials from NVBDCP and state health departments, vaccine procurement officers, cold chain logistics specialists, community health program managers (ASHA coordinators), district malaria officers from high-burden regions in Odisha, Jharkhand, and West Bengal, and R&D scientists from vaccine manufacturing institutions. Consumer and healthcare provider surveys were conducted across endemic districts in East, North, West, and South India, covering both public health center staff and community awareness programs.

Secondary Research

Secondary research encompassed government publications including the National Framework for Malaria Elimination 2016-2030 (NVBDCP/MoHFW), National Strategic Plan for Malaria Elimination 2023-2027, World Malaria Reports (WHO), WHO South-East Asia Region malaria statistics, Serum Institute of India press releases (seruminstitute.com), peer-reviewed clinical trial publications from The Lancet and PMC, GAVI vaccine program documentation, UNICEF procurement data, Ministry of Health and Family Welfare annual reports, and India's Union Budget healthcare allocations. Over 50 secondary sources were reviewed and triangulated.

Forecasting Models

Market revenue forecasts were developed using an epidemiological demand model: India's malaria case burden by district multiplied by government vaccination program coverage targets and per-dose procurement prices, aggregated across all market segments (vaccine type, route of administration, region). Public procurement program spending data from government budget allocations, GAVI co-financing data, and manufacturer pricing information were used to validate bottom-up market size estimates. Sensitivity analysis across three scenarios (base, conservative, optimistic) was conducted using government policy milestone timelines as primary scenario drivers.

India Malaria Vaccine Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vaccine Types Covered | Pre-Erythrocytic, Erythrocytic, Multi-Antigen, Others |

| Route of Administrations Covered | Intramuscular, Subcutaneous, Intradermal, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Serum Institute of India, Bharat Biotech, Indian Immunologicals Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India malaria vaccine market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India malaria vaccine market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India malaria vaccine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Malaria Vaccine Market Report

The India malaria vaccine market reached USD 11.21 Billion in 2025, driven by government elimination programs, WHO-recommended vaccines, and rising public-private R&D investment across high-burden states.

The India malaria vaccine market grows at a CAGR of 5.11% during 2026-2034, reaching USD 17.80 Billion by 2034, supported by national elimination policy, new vaccine approvals, and infrastructure expansion.

Pre-Erythrocytic vaccines lead at 46.8% share in 2025, driven by WHO-recommended RTS,S/AS01 and R21/Matrix-M, both targeting the sporozoite life stage of Plasmodium falciparum with 75-78% efficacy in clinical trials.

Intramuscular route leads at 58.4% in 2025 as it is the standard delivery protocol for both WHO-recommended malaria vaccines and aligns with India's immunization programs administration guidelines.

East India leads at 34.6% in 2025, encompassing the highest malaria burden states - Odisha, Jharkhand, West Bengal - and northeastern states with concentrated government vaccine programs.

Leading companies include Serum Institute of India, Bharat Biotech, and Indian Immunologicals Ltd., among others.

India targets zero indigenous malaria cases by 2030 under the National Framework for Malaria Elimination (NFME) 2016-2030. India has already reduced malaria cases by over 70% compared to 2015 levels as of 2024.

The India malaria vaccine market is projected to reach USD 14.39 Billion by 2030, coinciding with India's national malaria elimination target year and expected peak immunization program intensity.

Key drivers include government NFME elimination programs, WHO-recommended vaccine availability, Serum Institute's manufacturing scale, GAVI co-financing frameworks, and improving cold chain infrastructure in high-burden rural districts.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)