India Medical Devices Market Size, Share, Trends and Forecast by Type, End User, and Region, 2026-2034

India Medical Devices Market Size, Share, Trends & Forecast (2026-2034)

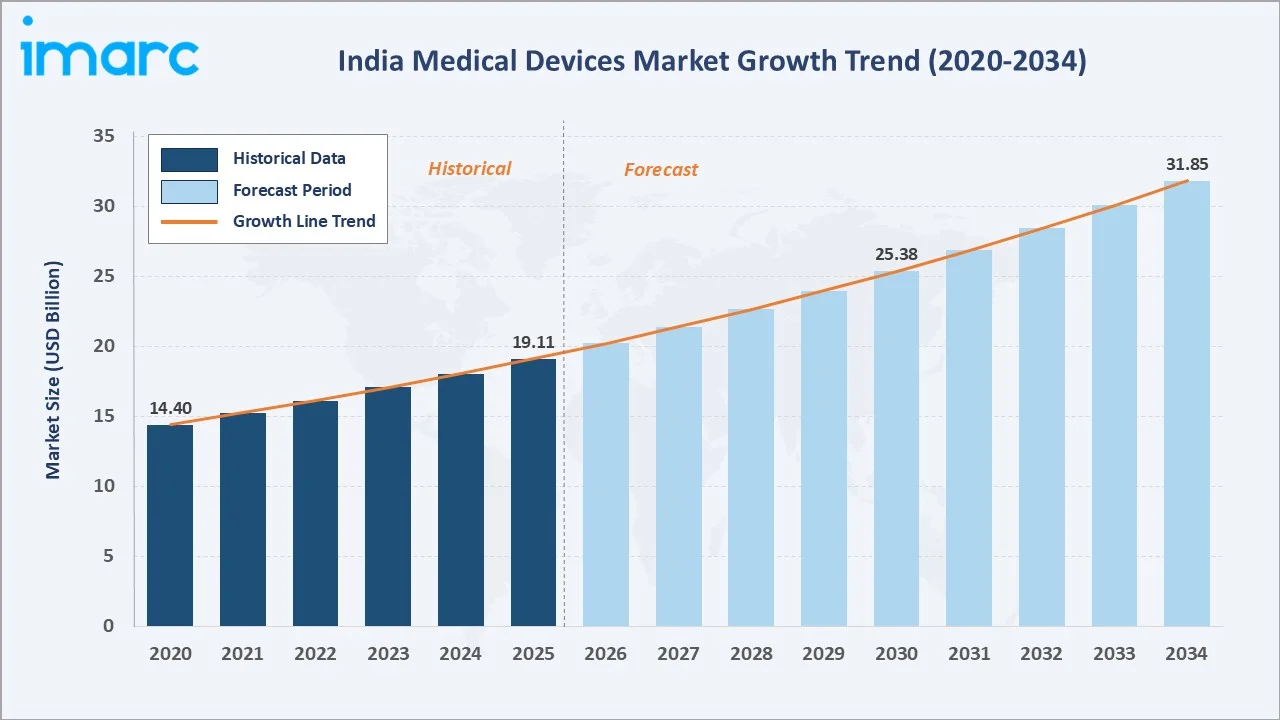

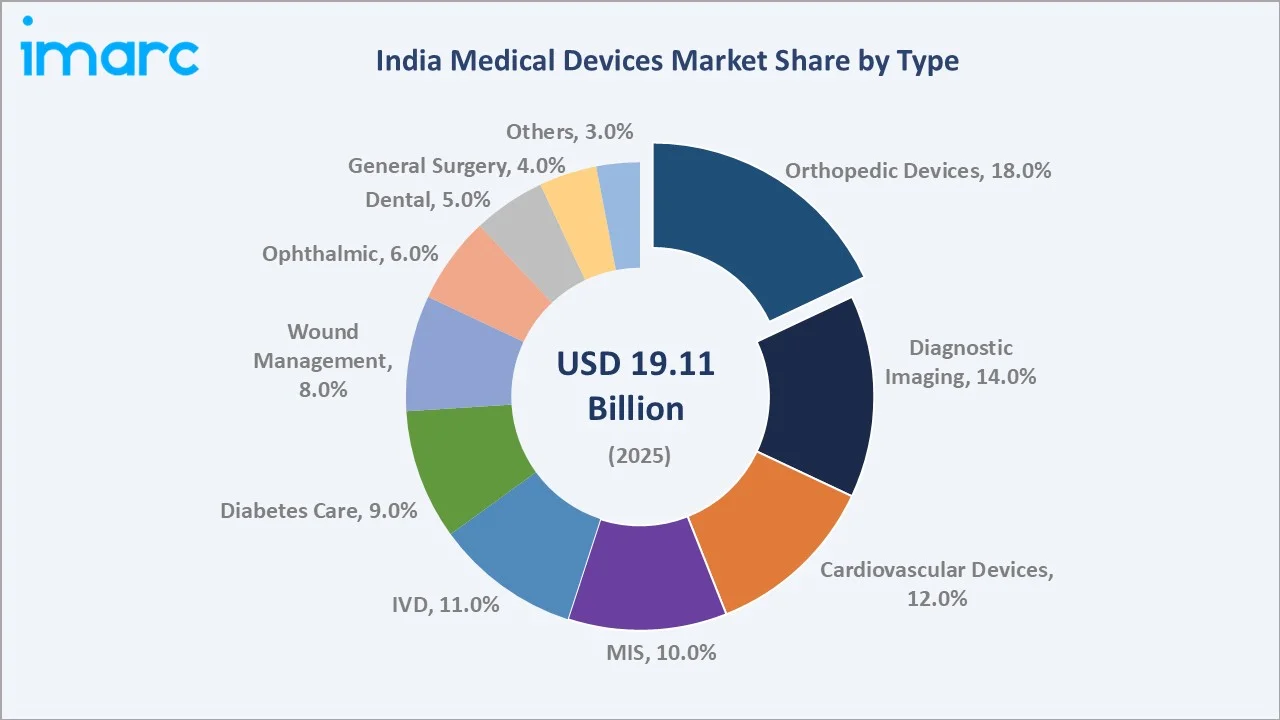

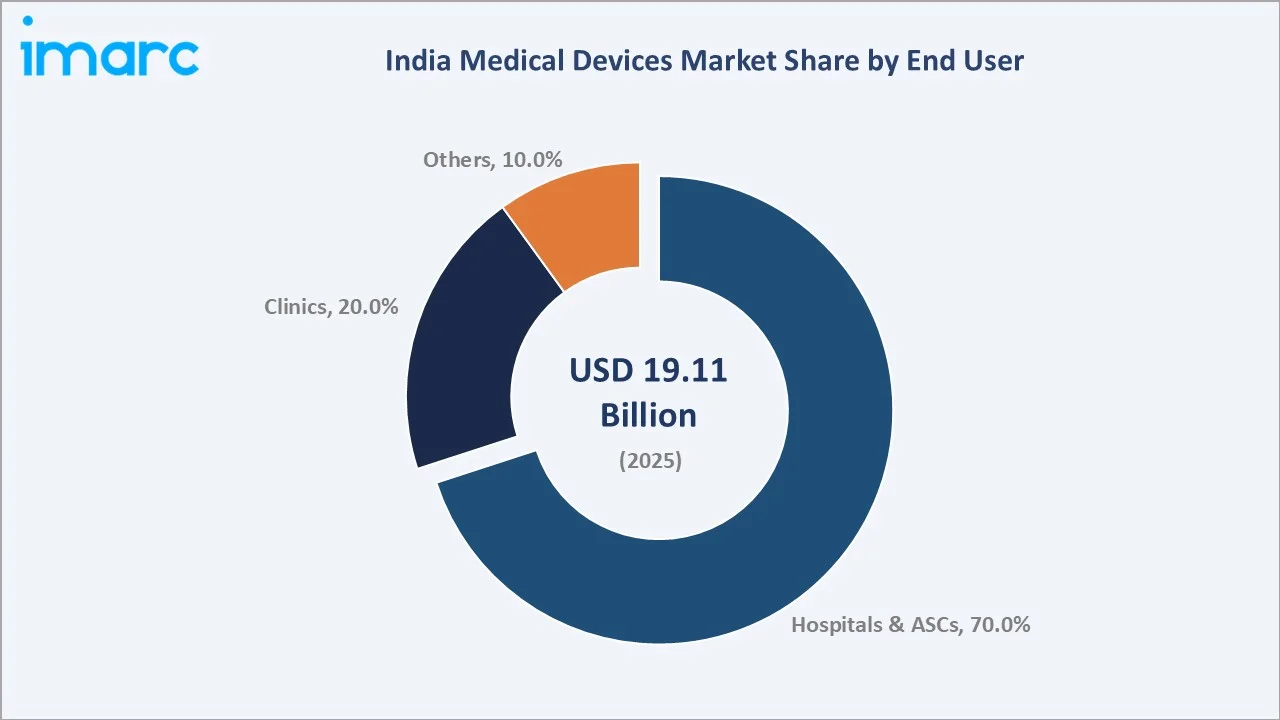

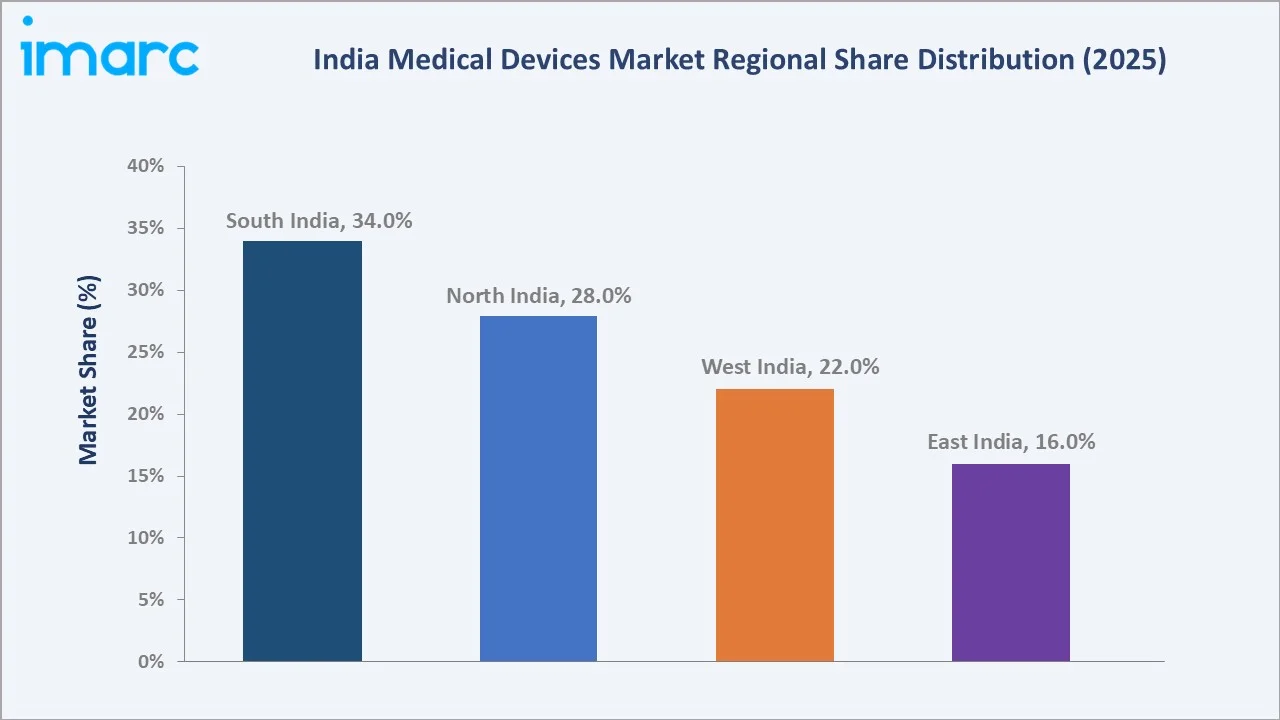

The India medical devices market size was valued at USD 19.11 Billion in 2025 and is projected to reach USD 31.85 Billion by 2034, exhibiting a CAGR of 5.83% during the forecast period 2026-2034. Orthopedic Devices lead the type segment at 18.0% in 2025, while Hospitals and ASCs dominate end-user demand at 70.0%. South India commands the largest regional share at 34.0%, anchored by Tamil Nadu's healthcare hub and Karnataka's device manufacturing ecosystem.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 19.11 Billion |

|

Forecast Market Size (2034) |

USD 31.85 Billion |

|

CAGR (2026-2034) |

5.83% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South India (34.0% share, 2025) |

|

Fastest Growing Region |

South India |

|

Leading Type (2025) |

Orthopedic Devices (18.0%) |

|

Leading End User (2025) |

Hospitals & ASCs (70.0%) |

The India medical devices market growth trajectory from 2020 through 2034 reflects a consistent historical expansion base against a sustained forecast curve powered by chronic disease burden, healthcare infrastructure reforms, PLI-driven domestic manufacturing, and growing adoption of advanced surgical and diagnostic technologies.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlighting Diabetes Care and AI Diagnostics as the two fastest-growing sub-categories within the India medical devices industry analysis through 2034.

Executive Summary

The India medical devices market is undergoing a fundamental transformation, driven by the convergence of healthcare policy reforms, demographic shifts, and accelerating technology adoption. Valued at USD 19.11 Billion in 2025, the market is forecast to reach USD 31.85 Billion by 2034 at a CAGR of 5.83%.

Orthopedic Devices command the dominant type share at 18.0% in 2025. Diagnostic Imaging, at 14.0%, is driven by significant under-penetration relative to WHO benchmarks and accelerating government imaging infrastructure investment.

South India leads with a 34.0% regional share in 2025, anchored by Chennai's super-specialty hospital concentration, Bengaluru's medical device manufacturing cluster, and Hyderabad's pharma-device nexus. Hospitals and ASCs command 70.0% of end-user demand, reflecting the procedural concentration of device utilization in organized healthcare settings.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment (2025) |

Orthopedic Devices – 18.0% share |

|

Second Largest Type Segment (2025) |

Diagnostic Imaging – 14.0% share |

|

Leading End User (2025) |

Hospitals & ASCs – 70.0% share |

|

Leading Region (2025) |

South India – 34.0% share |

|

Second Region (2025) |

North India – 28.0% share |

|

Top Companies |

Abbott, Siemens, GE HealthCare, Medtronic, Becton, Dickinson and Company, and Koninklijke Philips N.V. |

|

Market Opportunity |

PLI scheme; USD 9 Bn medical tourism; 101 Mn diabetic population |

Key Analytical Observations Supporting the Above Data:

- Orthopedic Devices' 18.0% dominance in 2025 reflects India's rapidly aging population - individuals aged 60+ are projected to reach 320 million by 2050.

- Diagnostic Imaging at 14.0% in 2025 is driven by government investment in district-level imaging centers, and expansion of PMJAY diagnostic package coverage

- Hospitals and ASCs command 70.0% of end-user demand due to the capital-intensive nature of most device categories.

- South India's 34.0% regional share reflects Chennai's status as India's healthcare capital with over 45 JCI/NABH-accredited hospitals and the largest medical tourism inflow, combined with Karnataka's device manufacturing ecosystem.

- IVD and Diabetes Care together represent 20.0% of market revenue in 2025.

India Medical Devices Market Overview

India’s medical devices sector encompasses diagnostic, therapeutic, monitoring, and surgical products regulated under the Medical Devices Rules, 2017, by the Central Drugs Standard Control Organization, with classification ranging from Class A (low risk) to Class D (high risk) and expanding regulatory coverage. The ecosystem includes domestic and multinational manufacturers, contract manufacturers, importers, distributors, hospitals, diagnostic labs, and pharmacies, with manufacturing concentrated in Andhra Pradesh, Gujarat, Tamil Nadu, and Maharashtra. The market remains import-dependent for high-end devices, driving policy emphasis on localization and domestic production. Applications span tertiary care (advanced imaging, implants, robotic surgery), secondary care (diagnostics and surgical equipment), primary care (point-of-care and basic monitoring), and home care (chronic disease management devices), with growth supported by economic expansion, rising healthcare investment, infrastructure development, and increasing health awareness beyond metro markets.

Market Dynamics

To evaluate market opportunities, Request Sample

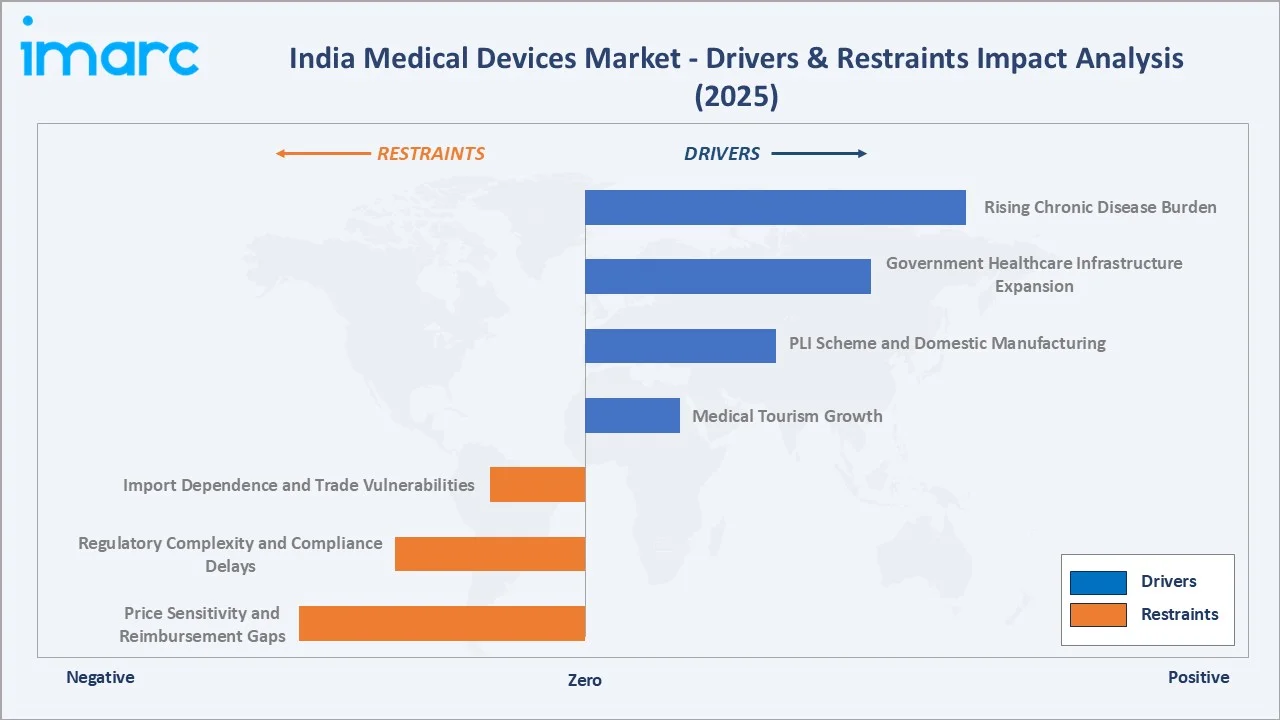

Market Drivers

- Rising Chronic Disease Burden: Increasing prevalence of diabetes, cardiovascular diseases, and cancer is structurally driving demand for diagnostics, cardiac devices, diabetes management, and oncology equipment, as indicated by national health bodies such as the Indian Council of Medical Research.

- Government Healthcare Infrastructure Expansion: Government programs such as Ayushman Bharat and PM-ABHIM are scaling primary, secondary, and critical care infrastructure, leading to sustained demand for medical devices across public health facilities.

- PLI Scheme and Domestic Manufacturing: The Production Linked Incentive (PLI) scheme is accelerating domestic manufacturing across key segments, including imaging, oncology, and implants, supporting import substitution and capacity creation.

- Medical Tourism Growth: India’s position as a cost-effective treatment hub for complex procedures (cardiac, orthopedic, ophthalmic) is driving demand for advanced medical technologies and faster equipment upgrades.

Market Restraints

- Import Dependence and Trade Vulnerabilities: Continued reliance on imported high-end devices exposes the market to supply chain risks, currency fluctuations, and cost pressures.

- Regulatory Complexity and Compliance Delays: Expanding compliance requirements under the Medical Devices Rules, 2017, by the Central Drugs Standard Control Organization can delay product approvals and create entry barriers, particularly for smaller manufacturers.

- Price Sensitivity and Reimbursement Gaps: High out-of-pocket healthcare spending and limited reimbursement coverage constrain adoption of premium medical technologies, especially in price-sensitive segments.

Market Opportunities

- Digital Health and Connected Devices: Initiatives such as the Ayushman Bharat Digital Mission are accelerating the adoption of connected monitoring devices, telehealth-enabled diagnostics, and AI-based imaging solutions.

- Tiered Market Expansion into Rural India: Expansion of healthcare access in rural India is driving demand for portable, affordable, and point-of-care diagnostic devices.

- Export Market Development: India is emerging as a competitive manufacturing base for medical devices, with growing exports to developing markets supported by cost advantages and improving quality standards.

Market Challenges

- Counterfeit and Sub-standard Products: Presence of sub-standard and unregulated products, particularly in low-cost segments, remains a challenge despite regulatory oversight.

- Healthcare Workforce Shortage for Advanced Devices: Limited availability of trained professionals for operating advanced equipment (e.g., imaging systems, robotic surgery platforms) restricts utilization in non-metro regions.

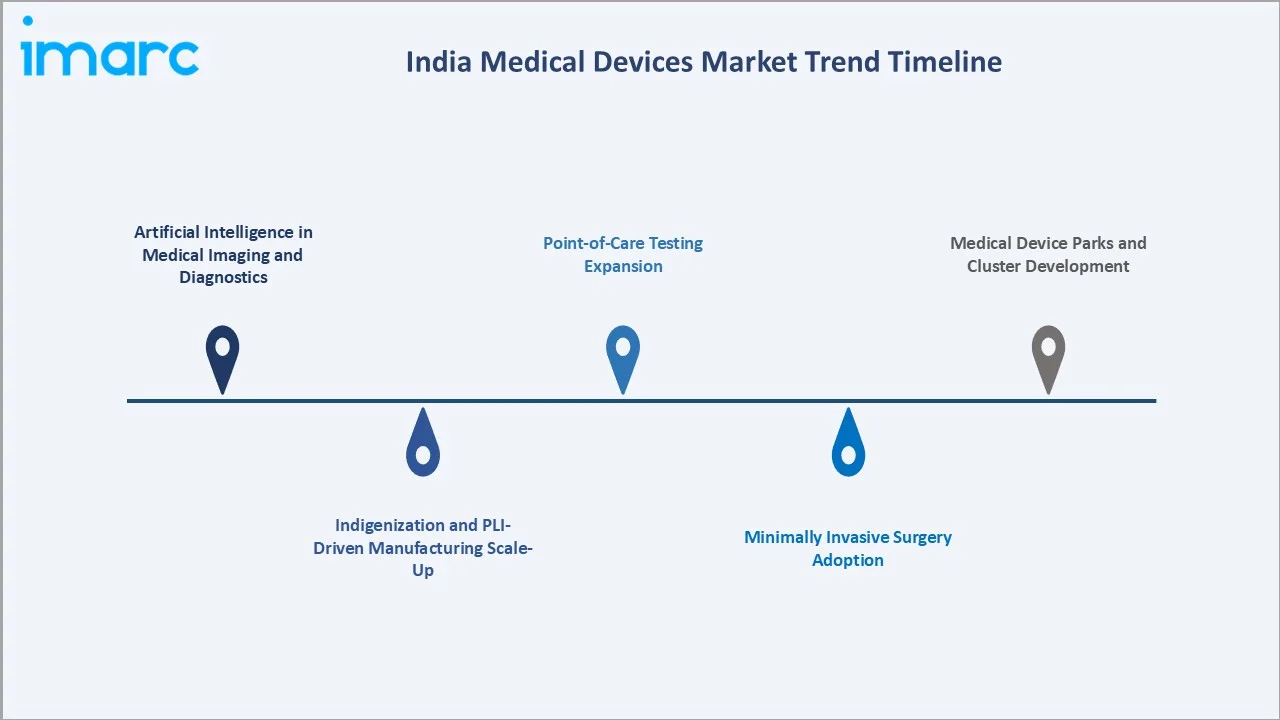

Emerging Market Trends

1. Artificial Intelligence in Medical Imaging and Diagnostics

AI-led imaging solutions are increasingly integrated into public health and hospital workflows, improving diagnostic speed and access. Companies such as Qure.ai are deploying AI for chest X-rays, TB screening, stroke detection, and diabetic retinopathy, supporting large-scale screening programs. These tools help optimize radiologist productivity and expand access in low-resource and underserved regions.

2. Indigenization and PLI-Driven Manufacturing Scale-Up

Government-led incentives are accelerating domestic production of high-end devices such as imaging systems and implants. Indian players like Skanray Technologies, Trivitron Healthcare, and Perfint Healthcare are strengthening capabilities in segments historically dominated by imports, supported by medical device parks and localization policies.

3. Point-of-Care Testing Expansion

Portable and rapid diagnostic solutions are gaining traction across primary and secondary care settings, driven by healthcare access expansion. Global platforms from Abbott Laboratories and Roche coexist with domestic manufacturers such as Transasia Bio-Medicals and J Mitra & Co, particularly in decentralized and rural healthcare delivery.

4. Minimally Invasive Surgery Adoption

Minimally invasive procedures are expanding due to shorter recovery times and improved outcomes. Advanced robotic systems like the da Vinci platform from Intuitive Surgical are increasingly deployed in leading hospitals, while domestic innovation such as the SSi Mantra system by SS Innovations is improving affordability and enabling adoption beyond metro cities.

5. Medical Device Parks and Cluster Development

The Government of India is developing dedicated medical device parks to strengthen manufacturing ecosystems. These clusters aim to reduce production costs, improve supply chain integration, and support domestic manufacturing across disposables, implants, and diagnostic equipment categories.

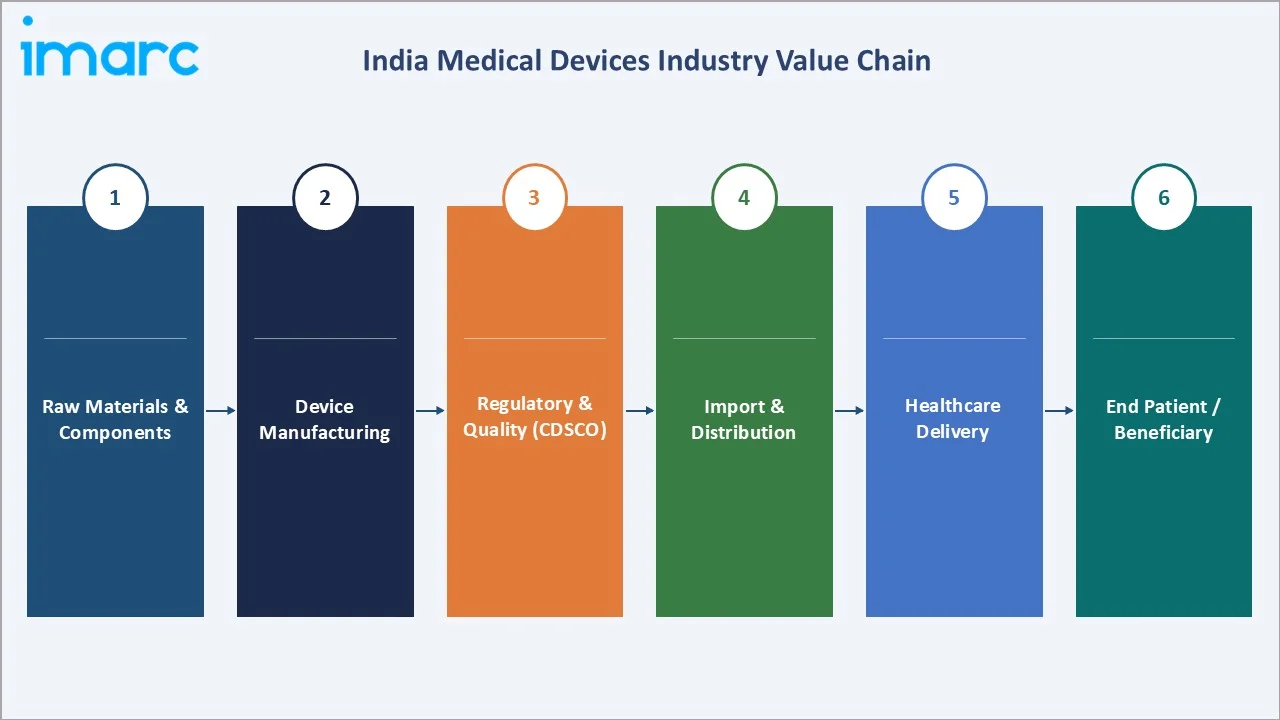

Industry Value Chain Analysis

The India medical devices value chain spans six integrated stages from component sourcing through end-use patient care delivery, with import and domestic manufacturing feeding into a tiered distribution network. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Polymers, Electronics, Precision Metals, Optical Components |

|

Device Manufacturing |

Abbott, Siemens, GE HealthCare, Medtronic, Becton, Dickinson and Company, and Koninklijke Philips N.V. |

|

Regulatory & Quality (CDSCO) |

CDSCO/DCGI licensing, ISO 13485, BIS certification, MDR 2017 compliance |

|

Import & Distribution |

Cardinal Health, Redington, Maharashtra/Gujarat regional distributors |

|

Healthcare Delivery |

Apollo Hospitals, Fortis, AIIMS, Max Healthcare, and the government hospitals |

|

End Patient / Beneficiary |

Outpatients, inpatients, diagnostic center patients, homecare users |

Domestic manufacturers currently occupy the lower-to-mid value chain stages, primarily producing disposables, basic diagnostic equipment, and commodity implants. High-value imaging systems, advanced implants, and robotic platforms remain predominantly imported, representing the key import-substitution opportunity targeted by PLI and device park policies.

Technology Landscape in the India Medical Devices Industry

AI and Digital Diagnostics

India’s diagnostics landscape is rapidly digitizing, with AI platforms moving from pilots to scaled deployments in public health systems. Solutions from Qure.ai are being integrated into national programs for chest X-ray interpretation, supporting TB screening and early disease detection. Emerging applications include digital pathology, AI-assisted fundus imaging for diabetic retinopathy, and AI-enabled ECG interpretation—expanding diagnostic accuracy and reach, particularly in resource-constrained settings.

Robotic and Minimally Invasive Surgical Technology

Robotic surgery is gaining traction as a high-end technology segment within Indian healthcare. Systems such as the da Vinci platform by Intuitive Surgical are increasingly deployed across specialties like urology, gynecology, and general surgery. At the same time, cost-optimized domestic innovations like the SSi Mantra system from SS Innovations are improving affordability and enabling adoption in Tier-II hospitals, supporting broader access to minimally invasive procedures.

Point-of-Care and Connected Monitoring Technologies

The rise of connected healthcare is reshaping device utilization across care settings. Bluetooth-enabled glucometers, cloud-connected continuous glucose monitoring (CGM) systems, portable ultrasound devices, and smartphone-integrated diagnostics are creating a ‘connected diagnostics’ ecosystem. National digital infrastructure initiatives such as the Ayushman Bharat Digital Mission are enabling interoperability and health data exchange, supporting the integration of these devices into telehealth and remote monitoring workflows.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Orthopedic Devices |

18.0% |

2025 |

|

End User |

Hospitals and Ambulatory Surgery Centers (ASCs) |

70.0% |

2025 |

|

Region |

South India |

34.0% |

2025 |

By Type

Orthopedic Devices command an 18.0% majority share in 2025, reflecting industry-wide growth in joint replacement demand, India's aging population, and the country's established position as a global orthopedic medical tourism destination.

To access detailed market analysis, Request Sample

Diagnostic Imaging at 14.0% in 2025 benefits from significant under-penetration relative to WHO benchmarks and accelerating government procurement. Cardiovascular Devices at 12.0% are driven by India's growing burden of cardiovascular disease and rapid cath lab expansion, with approximately 1,200+ active cardiac catheterization laboratories as of 2024.

By End User

Hospitals and Ambulatory Surgery Centers dominate at 70.0% of total end-user demand in 2025, reflecting the procedural and capital-intensive nature of most device categories. India currently has approximately 70,000 registered hospitals and 600+ functional ASCs, with the ASC segment growing at approximately 18-20% annually, driven by the shift toward cost-efficient outpatient procedures.

Clinics represent 20.0% of demand in 2025, primarily served by smaller diagnostic devices, POC testing equipment, and basic monitoring instruments. The Others category at 10.0% encompasses home care users, diagnostic laboratories, and academic institutions.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

34.0% |

Chennai medical hub, Bengaluru med-tech cluster, Hyderabad pharma-device nexus, AP Device Park |

|

North India |

28.0% |

Delhi NCR tertiary care, AIIMS network expansion, UP healthcare investment |

|

West India |

22.0% |

Mumbai super-specialty hospitals, Gujarat device manufacturing, Pune med-tech R&D |

|

East India |

16.0% |

Kolkata referral centers, Odisha/West Bengal PMJAY expansion, and emerging NE markets |

South India commands the largest regional share at 34.0% of the India medical devices market in 2025. This dominance is anchored by Tamil Nadu - home to Chennai, India's healthcare capital with over 45 JCI/NABH-accredited hospitals and the largest medical tourism inflow volume. Andhra Pradesh hosts one of the four PLI-designated Medical Device Parks in Visakhapatnam.

North India, at 28.0%, is anchored by Delhi NCR's concentration of India's highest-tier super-specialty hospitals, including AIIMS New Delhi, Medanta, Fortis, and Apollo Delhi. The AIIMS expansion program, covering 22 new AIIMS institutions nationally, is creating substantial device procurement demand across the public sector.

West India holds 22.0% share in 2025. Mumbai remains the financial and healthcare administration hub, home to leading private hospital chains and medical device importers. Gujarat is emerging as a key manufacturing hub. East India's 16.0% share is anchored by Kolkata but is growing rapidly as PMJAY coverage in West Bengal, Odisha, and Jharkhand drives device procurement through government channels.

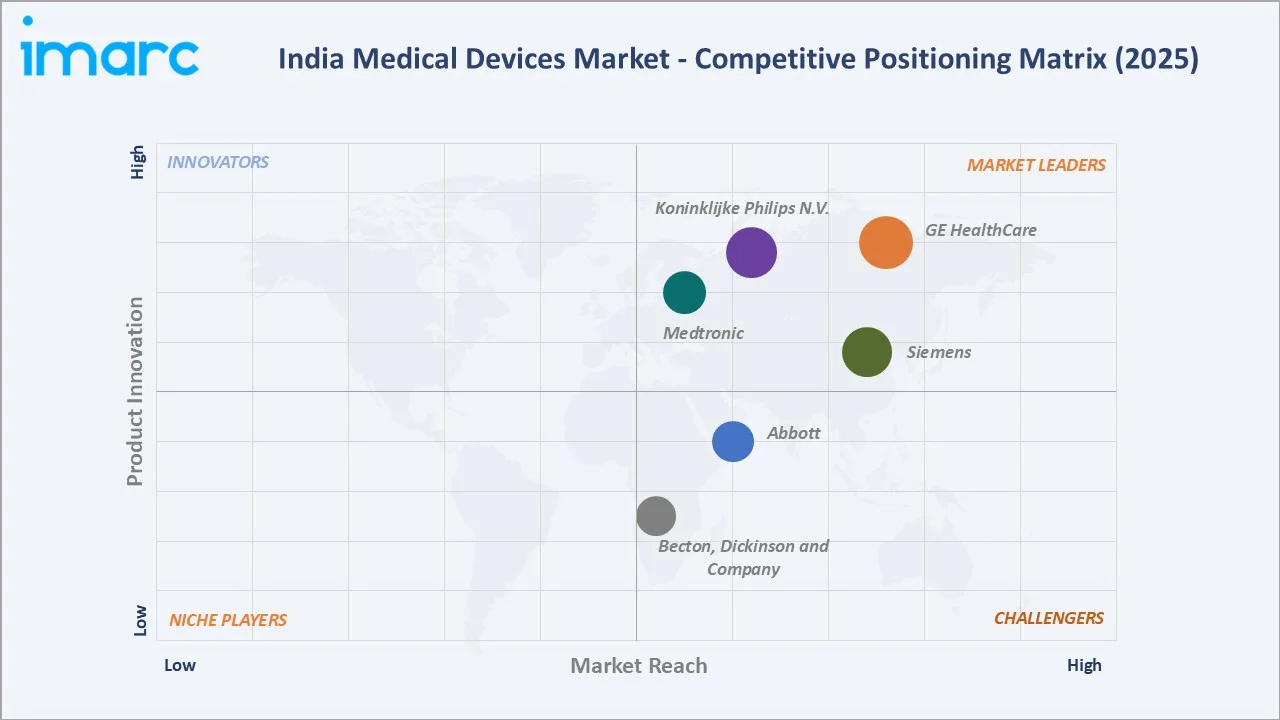

Competitive Landscape

|

Company Name |

Key Brand/ Offerings |

Market Position |

Core Strength |

|

Abbott |

FreeStyle Libre, i-STAT, |

Challenger |

Largest diagnostics franchise; CGM market expansion |

|

Siemens |

SOMATOM CT, Magnetom MRI |

Leader |

Premium imaging; expanding to Tier-II cities |

|

GE HealthCare |

Voluson Ultrasound |

Leader |

Portable imaging; 'Made in India' push |

|

Medtronic |

Cardiac Resynchronization Therapy (CRT) Systems |

Leader |

Cath lab presence; InPen insulin; surgical robotics |

|

Becton, Dickinson and Company |

BD Veritor Plus System |

Challenger |

IVD, vascular, specimen management |

|

Koninklijke Philips N.V. |

Lumify |

Leader |

Patient monitoring; portable ultrasound |

The India medical devices competitive landscape is characterized by dominant multinational Tier-1 suppliers in high-value imaging, implant, and cardiovascular segments, alongside a growing cohort of domestic companies capturing share in diagnostics, disposables, and increasingly in complex equipment categories supported by PLI incentives. The top 5 multinationals collectively hold approximately 35-40% of total market revenue in 2025.

Key Company Profiles

Abbott

Abbott is the leading diagnostics and diabetes care company in the Indian medical devices market, with a comprehensive portfolio spanning IVD, continuous glucose monitoring, point-of-care testing, and vascular devices.

- Product & Platform Portfolio: FreeStyle Libre CGM system, i-STAT POC analyzer, Architect clinical chemistry, vascular intervention portfolio.

- Recent Developments: In August 2025, Abbott introduced the FreeStyle Libre 2 Plus sensor, which provides automatic glucose readings every minute directly to a person's phone, enabling diabetics to confidently, accurately, and easily control their disease.

- Strategic Focus: Abbott's India strategy centers on expanding CGM penetration among India's 101 million diabetics through affordability initiatives and digital connectivity, while scaling POC diagnostics infrastructure across primary health centers under ABDM integration.

Siemens

Siemens Healthineers is one of the leading medical imaging and laboratory diagnostics companies in India, with a comprehensive portfolio spanning CT, MRI, X-ray, ultrasound, and molecular diagnostics.

- Product & Platform Portfolio: SOMATOM CT, Magnetom MRI, ACUSON ultrasound, Atellica clinical chemistry, Symbia nuclear medicine.

- Recent Developments: In April 2025, Siemens Healthineers officially launched MAGNETOM Flow and SOMATOM Pro.Pulse.

- Strategic Focus: Siemens Healthineers' India strategy prioritizes geographic expansion beyond the top 8 metro markets into Tier-II and Tier-III cities where imaging infrastructure density is 60-70% below the national average.

GE HealthCare

GE HealthCare is a leading player in India’s medical devices market, with a strong presence across diagnostic imaging, ultrasound, patient monitoring, and life care solutions, supported by localized manufacturing and R&D capabilities.

- Product & Platform Portfolio: Revolution CT systems, SIGNA MRI platforms, LOGIQ and Vivid ultrasound, CARESCAPE patient monitoring systems, and Edison AI-enabled digital health platform.

- Recent Developments: In April 2022, Wipro GE Healthcare, a leading global medical technology and digital solutions innovator, announced the launch of its next-generation Revolution Aspire CT (Computed Tomography) scanner.

- Strategic Focus: GE HealthCare’s India strategy centers on affordable innovation, localization, and digital integration, with a strong push into Tier-II and Tier-III markets. The company is leveraging AI, remote monitoring, and tele-radiology capabilities to address infrastructure and specialist gaps while strengthening its footprint in public and private healthcare segments.

Market Concentration Analysis

The India medical devices market exhibits moderate-to-high concentration in premium device segments (imaging, cardiovascular implants, robotic surgery) and low-to-moderate concentration in commodity segments (disposables, glucometers, wound care). The top 10 companies account for approximately 40-50% of market revenue in 2025, with concentration varying significantly by sub-segment.

The competitive landscape is experiencing bifurcated structural dynamics. In the premium segment, growing complexity and regulatory requirements are concentrating market share among global Tier-1 players. In the mid-to-low tier, domestic brands are gaining share through competitive pricing, government tender wins, and PLI-supported manufacturing scale-up. The entry of domestic startups in AI diagnostics (Qure.ai, Niramai) and robotic surgery (SS Innovations) is beginning to disrupt incumbents in technology-driven niches.

Investment & Growth Opportunities

Fastest-Growing Segments

Diabetes care devices—particularly continuous glucose monitoring systems—are the fastest-growing segment, with solutions from Abbott Laboratories and Dexcom expanding adoption beyond metros as care shifts toward continuous monitoring. IVD point-of-care diagnostics form the second high-growth segment, driven by decentralized testing, expanding diagnostic infrastructure, and integration with digital health ecosystems such as the Ayushman Bharat Digital Mission.

Emerging Market Expansion

Robotic and AI-assisted surgical systems are transitioning from niche tertiary settings to broader hospital networks, with cost-optimized platforms like SSi Mantra by SS Innovations enabling wider adoption. At the same time, connected homecare devices—including remote monitoring and smartphone-linked diagnostics—are emerging as a high-volume growth category as patients increasingly shift toward home-based care.

Venture & Investment Trends

Investor interest in India’s medical device and healthtech space is rising, led by AI diagnostics players such as Qure.ai. Policy support through the PLI scheme is accelerating capital deployment into domestic manufacturing, while government-backed medical device parks are attracting private equity and strategic investors due to their scalable, cost-efficient cluster-based infrastructure.

Future Market Outlook (2026-2034)

The India medical devices market is projected to sustain a 5.83% CAGR through 2034, reaching USD 31.85 Billion - a near-doubling of the 2025 market value. Three structural forces will shape market evolution through the forecast period.

India’s medical devices sector is shifting toward domestic manufacturing under PLI and device park initiatives, reducing import dependence while improving cost competitiveness and local margins. At the same time, digital health integration—driven by the Ayushman Bharat Digital Mission, AI diagnostics, and connected devices—is creating new demand for smart medical technologies.

Parallelly, expansion of advanced healthcare into Tier-II and Tier-III cities by hospital chains such as Apollo Hospitals, Fortis Healthcare, Healthcare Global Enterprises, and Narayana Health is widening the addressable market. Overall, India is emerging as a global manufacturing and innovation hub, with growth driven by a mix of multinational leadership, domestic players, and AI-led healthtech entrants.

Research Methodology

Primary Research

Primary research comprised structured interviews with medical device procurement heads at leading Indian hospital chains, regulatory affairs managers at domestic and multinational device companies, CDSCO-registered importers, and institutional healthcare investors. Primary insights validated market sizing, segmentation estimates, technology adoption rates, and competitive positioning assessments across device categories.

Secondary Research

Secondary sources include CDSCO Annual Reports, Ministry of Health and Family Welfare (MoHFW) data, AIMED publications, FICCI Healthcare reports, IBEF Medical Devices Sector reports, IQVIA India healthcare data, IDF Diabetes Atlas 2023, ICMR National Cancer Registry, WHO Global Health Observatory, company annual reports, and trade publications including Express Healthcare and Medical Buyer India.

Forecasting Models

Market size estimations were derived using a combination of bottom-up segment modeling (device category volumes x average selling prices x utilization rates) and top-down macro-healthcare expenditure allocation. Scenario analysis covering base, optimistic, and conservative growth cases was performed, incorporating GDP growth sensitivity, PLI scheme execution risk, and regulatory reform pace as primary variables.

India Medical Devices Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Orthopedic Devices, Diagnostic Imaging, Cardiovascular Devices, Wound Management, Minimally Invasive Surgical (MIS), Diabetes Care, Dental Devices, Ophthalmic Devices, In Vitro Diagnostics (IVD), General Surgery, Others |

| End Users Covered | Hospitals and Ambulatory Surgery Centers (ASCs), Clinics, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Abbott, Siemens, GE HealthCare, Medtronic, Becton, Dickinson and Company, Koninklijke Philips N.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Medical Devices Market Report

The India medical devices market was valued at USD 19.11 Billion in 2025.

The market is projected to reach USD 31.85 Billion by 2034, growing at a CAGR of 5.83% during 2026-2034.

Orthopedic Devices lead with an 18.0% share in 2025.

Hospitals and ASCs dominate at 70.0% share in 2025.

South India leads with a 34.0% share in 2025.

Key drivers include India's diabetic population, CVD patients, Ayushman Bharat PMJAY expansion, PM-ABHIM infrastructure investment, and the medical tourism sector.

Diabetes Care devices - particularly CGM systems - are the fastest-growing sub-segment at approximately 25-30% annually, given India's position as the country with the world's largest diabetic population at 101 million per IDF 2023.

Leading companies include Abbott, Siemens, GE HealthCare, Medtronic, Becton, Dickinson and Company, and Koninklijke Philips N.V.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade