India Medical Implants Market Size, Share, Trends and Forecast by Product, Material, and Region, 2026-2034

India Medical Implants Market Size, Share, Trends & Forecast (2026-2034)

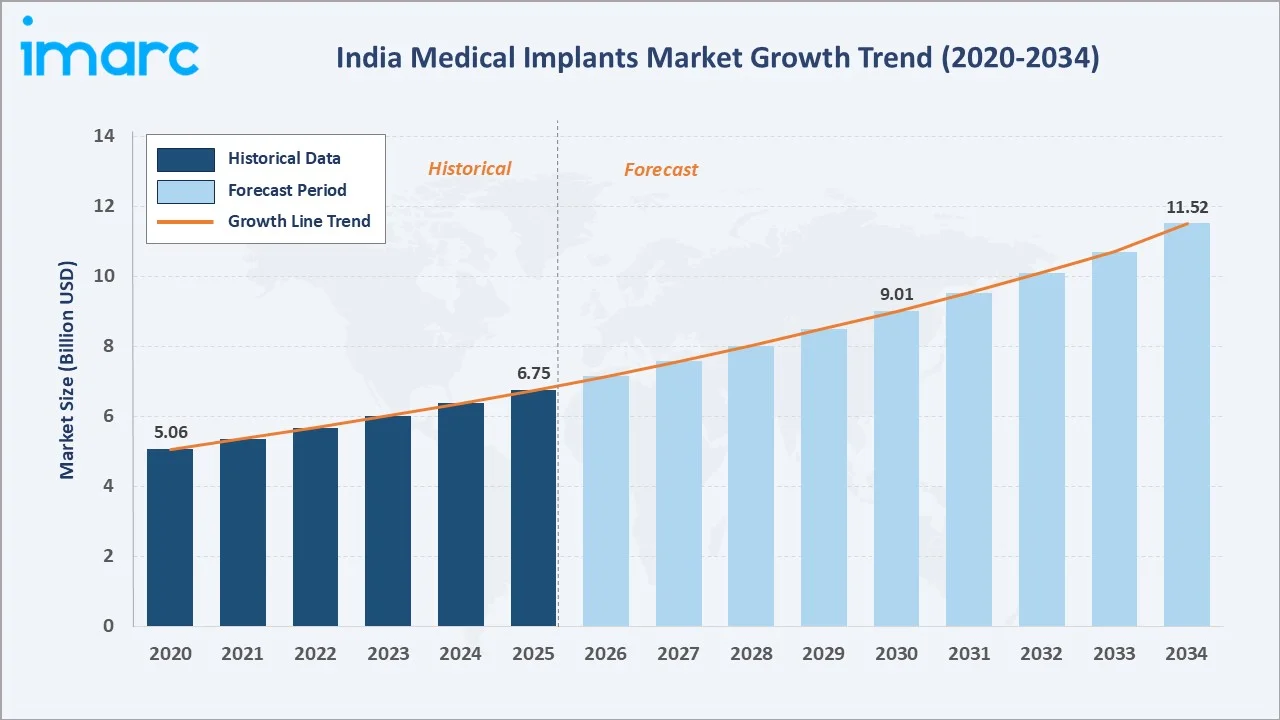

The India medical implants market was valued at USD 6.75 Billion in 2025 and is projected to reach USD 11.52 Billion by 2034, exhibiting a CAGR of 5.93% during 2026-2034. Increasing prevalence of chronic diseases, an aging population base, broadening medical tourism infrastructure, and rising adoption of minimally invasive surgical procedures are the primary drivers shaping market growth.

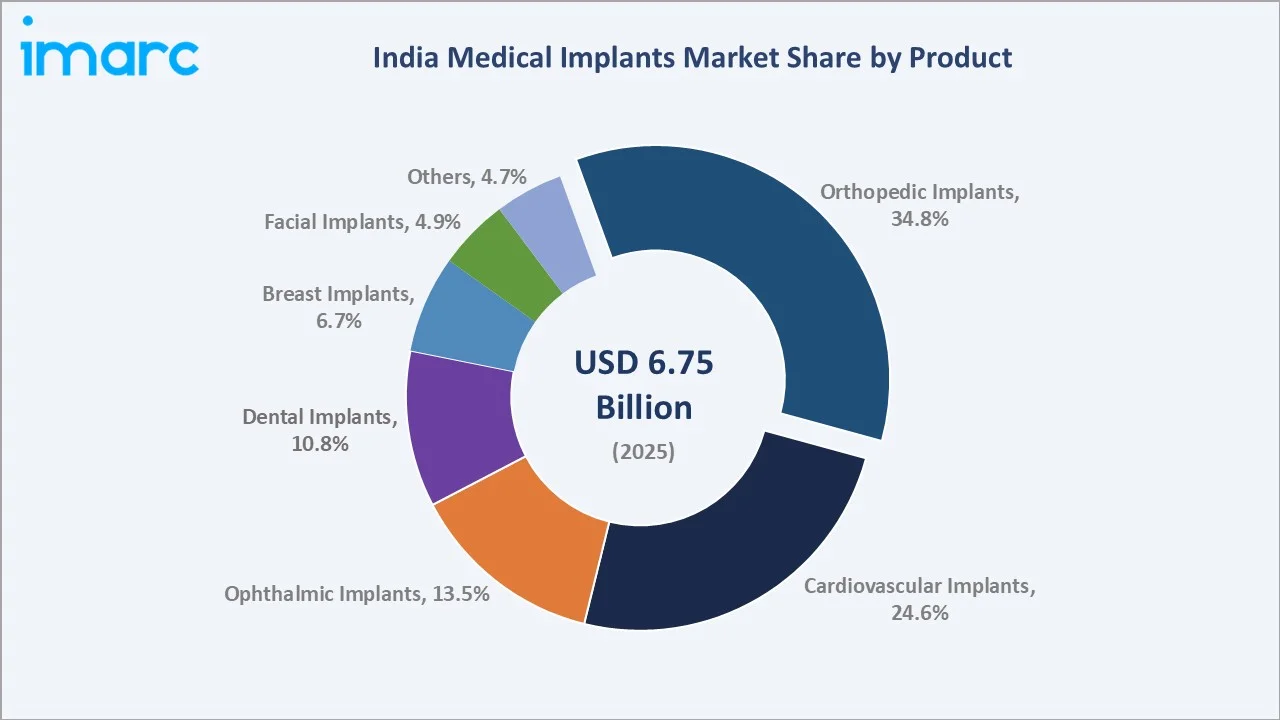

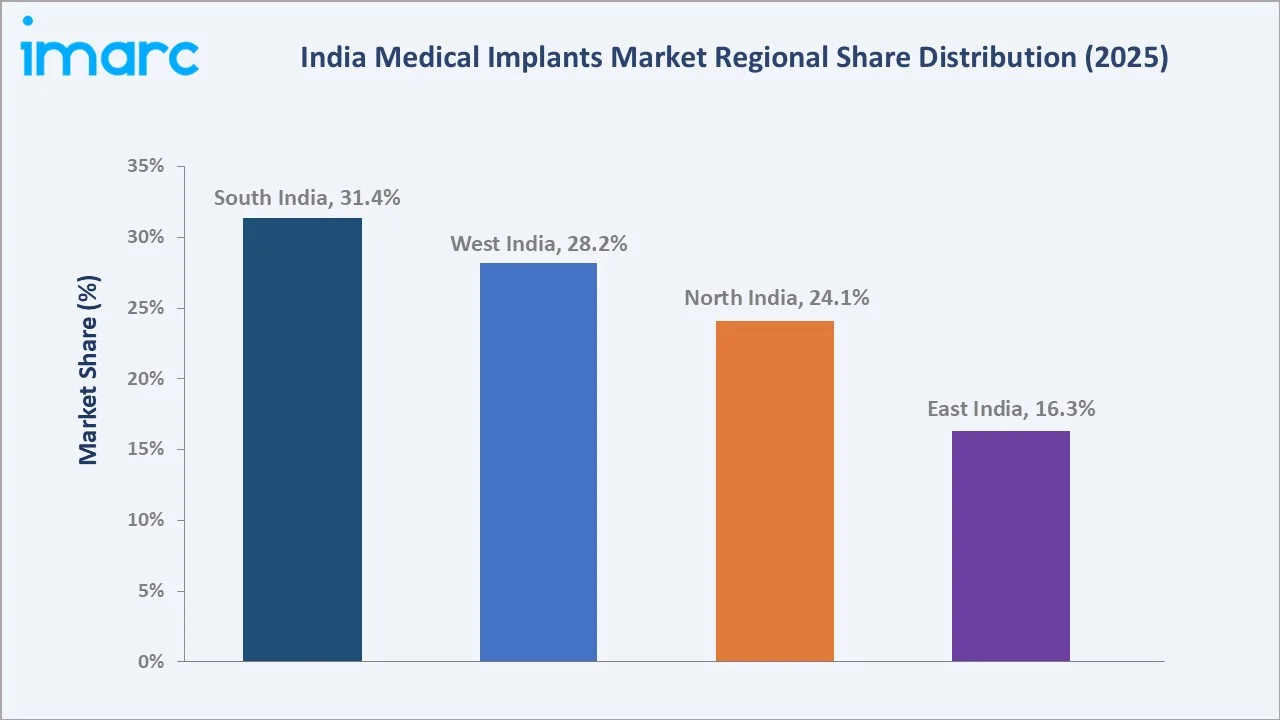

Orthopedic implants lead the product segment at 34.8%, metallic biomaterial dominates the material segment at 42.7%, and South India commands 31.4% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.75 Billion |

|

Forecast Market Size (2034) |

USD 11.52 Billion |

|

CAGR (2026-2034) |

5.93% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South India (31.4%, 2025) |

|

Second Largest Region |

West India (28.2%, 2025) |

|

Leading Product |

Orthopedic Implants (34.8%, 2025) |

|

Leading Material |

Metallic Biomaterial (42.7%, 2025) |

The India medical implants market expanded from USD 5.06 Billion in 2020 to USD 6.75 Billion in 2025, driven by widening hospital infrastructure, increasing surgical volumes, and accelerating adoption of imported and domestically manufactured implant devices. Anchored at USD 9.01 Billion in 2030, the forecast to USD 11.52 Billion by 2034 is supported by rising cardiovascular disease burden, expanding dental and ophthalmic care access, and growing government initiatives toward affordable healthcare delivery.

To get more information on this market, Request Sample

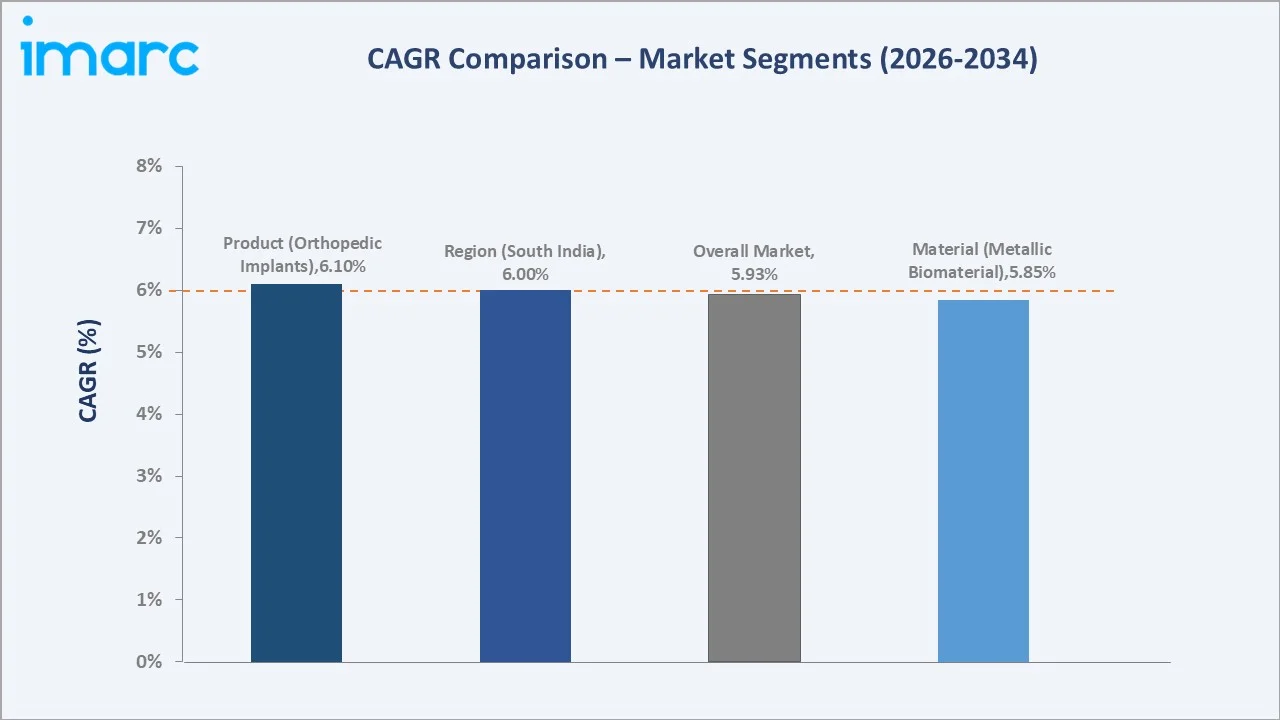

CAGR trajectories across product and material sub-segments show dental implants and polymers biomaterial expanding faster than the overall 5.93% market CAGR, driven by growing oral healthcare awareness, rising adoption of advanced biomaterials, and increasing disposable incomes supporting elective procedures.

Executive Summary

The India medical implants market is on a steady growth trajectory from USD 5.06 Billion in 2020 to USD 11.52 Billion by 2034. The sector has evolved from a predominantly import-dependent model to a hybrid ecosystem integrating domestic manufacturing under the Production Linked Incentive (PLI) scheme, increased clinical capacity at tier-2 city hospitals, and a rapidly expanding base of trained implant surgeons.

Orthopedic implants dominate the product segment at 34.8% in 2025, supported by growing joint replacement demand among the aging population and rising sports-related injury rates. Metallic biomaterial leads the material segment at 42.7%, benefiting from superior mechanical strength, biocompatibility, and well-established clinical track records in orthopedic and cardiovascular applications. South India commands 31.4% of regional share in 2025, underpinned by high-density private hospital networks in Tamil Nadu, Karnataka, and Telangana, superior physician availability, and strong medical tourism infrastructure.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Orthopedic Implants - 34.8% share (2025) |

|

Second Largest Product |

Cardiovascular Implants - 24.6% share (2025) |

|

Leading Material |

Metallic Biomaterial - 42.7% share (2025) |

|

Second Largest Material |

Polymers Biomaterial - 29.5% share (2025) |

|

Leading Region |

South India - 31.4% share (2025) |

|

Second Largest Region |

West India - 28.2% share (2025) |

|

Top Companies |

Johnson & Johnson, Stryker, Medtronic, Zimmer Biomet, HRS Navigation |

Key Analytical Observations Expanding On The Data Above:

- Orthopedic implants dominance at 34.8% is underpinned by the high and rising burden of osteoarthritis, hip fractures among elderly patients, and increasing joint replacement procedures at both corporate and government hospitals across India.

- Cardiovascular implants at 24.6% reflect India's significant and growing cardiovascular disease burden, directly driving demand for stents, pacemakers, and heart valves across tertiary care centers. According to the NSO Survey 2025, heart disease in India tripled over seven years, with those aged 15-29 also at risk.

- Metallic biomaterial leadership at 42.7% is driven by the superior mechanical properties, biocompatibility, and long clinical history of titanium alloys, cobalt-chromium alloys, and stainless steel in orthopedic and cardiovascular implant applications.

- Polymers biomaterial share at 29.5% is expanding due to its versatility, lightweight properties, ease of processing, and increasing adoption in minimally invasive procedures.

- South India at 31.4% leads regional share, anchored by high-density private hospital networks in Chennai, Bengaluru, and Hyderabad, coupled with advanced surgical infrastructure.

India Medical Implants Market Overview

Medical implants are devices manufactured from biocompatible materials and surgically placed within the human body to replace, support, or enhance biological structures and functions. The India medical implants market encompasses orthopedic, cardiovascular, ophthalmic, dental, breast, facial, and other implant categories, spanning metallic biomaterials, polymers, ceramics, and natural biomaterials as primary input substrates.

The Indian ecosystem integrates raw material suppliers, implant manufacturers and OEMs, regulatory bodies including CDSCO, quality and sterilization service providers, distributors and logistics partners, hospital procurement networks, and specialized surgical teams. Together, these entities enable delivery of implant-based therapeutic interventions across tertiary, secondary, and increasingly primary healthcare settings.

Market Dynamics

To evaluate market opportunities, Request Sample

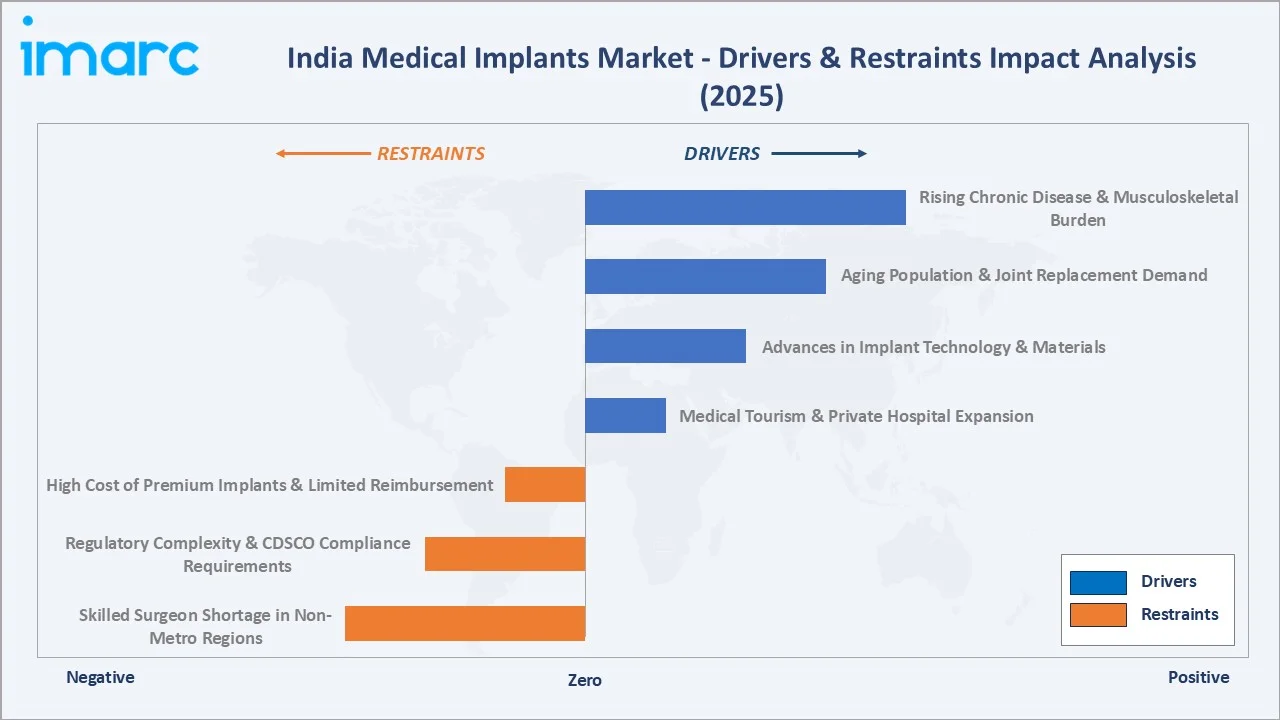

Market Drivers

- Rising Chronic Disease and Musculoskeletal Burden: India's growing incidence of osteoarthritis, osteoporosis, cardiovascular diseases, and diabetic complications is creating sustained and expanding demand for orthopedic, cardiovascular, and other therapeutic implants across all age cohorts.

- Aging Population and Joint Replacement Demand: India's population aged 60 and above is expected to reach 230 Million by 2036, according to PIB, generating accelerating demand for hip, knee, and spine implants as age-related musculoskeletal deterioration increases.

- Advances in Implant Technology and Materials: Rapid innovation in 3D-printed implants, bioabsorbable materials, antibacterial coatings, and minimally invasive delivery systems is improving clinical outcomes, reducing revision rates, and expanding the addressable patient population for implant-based treatments.

- Medical Tourism and Private Hospital Expansion: India's position as a leading global medical tourism destination, combined with continued expansion of Joint Commission International-accredited hospitals, is supporting higher implant procedural volumes through both domestic and international patient inflows. According to IMARC Group, the India medical tourism market reached USD 23.84 Billion in 2025.

Market Restraints

- High Cost of Premium Implants and Limited Reimbursement: Imported and technologically advanced implants carry significant cost premiums that place them beyond the reach of large segments of India's population. While government reimbursement schemes are expanding, coverage for implants remains inconsistent across states and insurance providers, constraining market penetration in lower-income patient cohorts.

- Regulatory Complexity and CDSCO Compliance Requirements: India's medical device regulatory framework imposes registration, quality, and post-market surveillance requirements that increase compliance costs, extend market entry timelines, and create barriers for smaller domestic manufacturers.

- Skilled Surgeon Shortage in Non-Metro Regions: The availability of trained implant surgeons, particularly orthopedic, cardiovascular, and ophthalmic specialists, remains concentrated in metro cities, limiting the geographic expansion of implant procedure volumes to tier-2 and tier-3 cities despite growing hospital infrastructure.

Market Opportunities

- Domestic Manufacturing Under PLI Scheme: The Government of India's PLI scheme for medical devices is accelerating investments in domestic implant manufacturing capacity, reducing import dependency, and creating cost-competitive domestic products for both Indian and export markets.

- Dental and Ophthalmic Care Penetration: Growing awareness of dental health, rising cataract surgery volumes under government eye care programs, and increasing adoption of intraocular lenses and dental implants in urban and semi-urban markets present significant growth opportunities for specialized implant categories.

- Emerging Bioabsorbable and Smart Implant Segment: The development of bioabsorbable implants for orthopedic and cardiovascular applications, and the integration of sensors and wireless communication into smart implants, represent emerging high-growth sub-segments aligned with India's technological advancement in medical devices.

Market Challenges

- Import Dependence and Supply Chain Fragility: A significant proportion of high-value orthopedic and cardiovascular implants continues to be imported, exposing the market to currency fluctuations, global supply chain disruptions, and trade policy changes that can affect availability and pricing.

- Post-Market Surveillance and Device Vigilance: Ensuring effective post-market surveillance, managing device recalls, and maintaining robust device vigilance infrastructure remains challenging in India's large and fragmented healthcare delivery system, posing risks to patient safety and manufacturer liability.

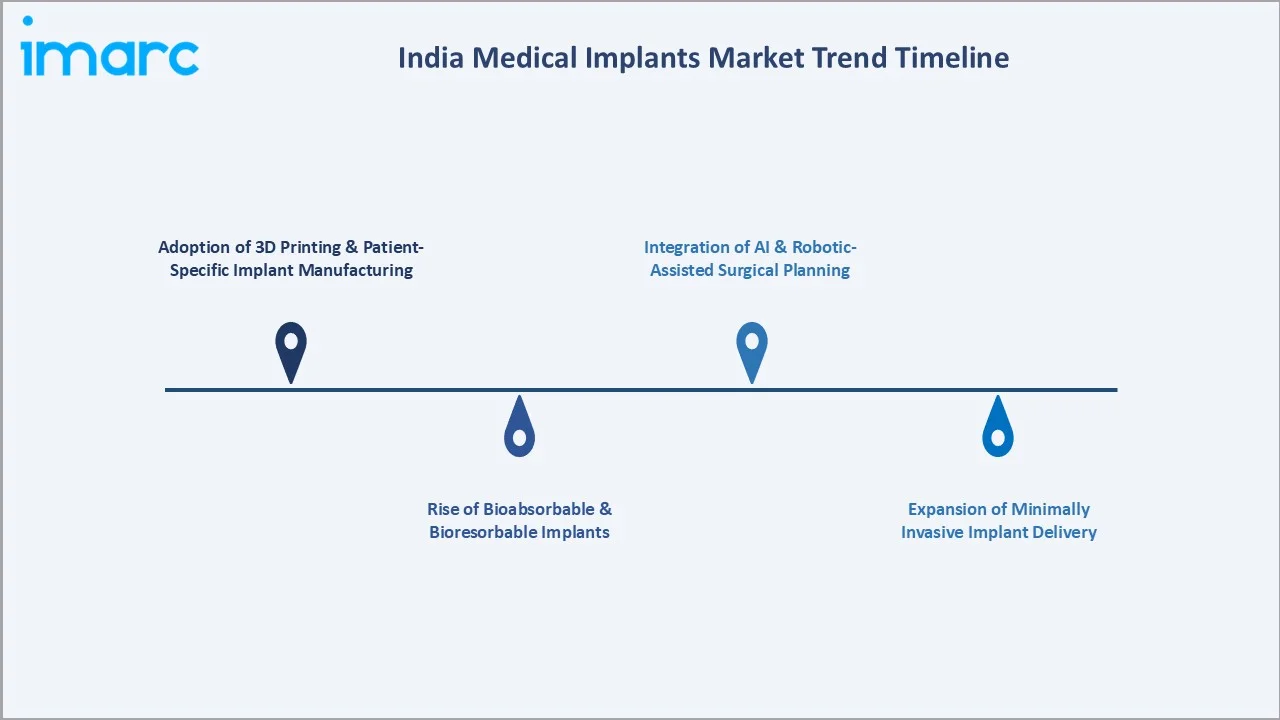

Emerging Market Trends

1. Adoption of 3D Printing and Patient-Specific Implant Manufacturing

Additive manufacturing is enabling the production of customized orthopedic, craniofacial, and dental implants tailored to individual patient anatomy, improving surgical fit, reducing operative time, and enhancing long-term clinical outcomes. Indian hospitals and manufacturers are increasingly investing in 3D printing infrastructure.

2. Rise of Bioabsorbable and Bioresorbable Implants

Bioabsorbable materials, including polylactic acid, polyglycolic acid, and magnesium alloys, are gaining adoption in orthopedic fixation, cardiovascular stenting, and dental applications. These materials eliminate the need for secondary removal surgeries, reduce long-term implant-related complications, and align with patient preference for less invasive long-term outcomes. Their adoption is accelerating across Indian tertiary care centers as clinical evidence strengthens.

3. Integration of AI and Robotic-Assisted Surgical Planning

AI tools for pre-operative planning, implant sizing, and surgical navigation are being adopted by leading Indian orthopedic and cardiovascular centers. Robotic-assisted joint replacement systems, while still limited to premium centers, are demonstrating superior implant placement accuracy, reduced hospital stays, and faster patient recovery, driving growing interest from hospital procurement teams.

4. Expansion of Minimally Invasive Implant Delivery

Surgeons and patients increasingly prefer minimally invasive approaches for joint replacement, cardiac device implantation, and ophthalmic procedures. Advances in delivery catheter technology, arthroscopic systems, and transcatheter valve implantation are expanding the eligible patient population, reducing surgical risk for elderly and high-comorbidity patients, and supporting higher procedural volumes across Indian hospitals.

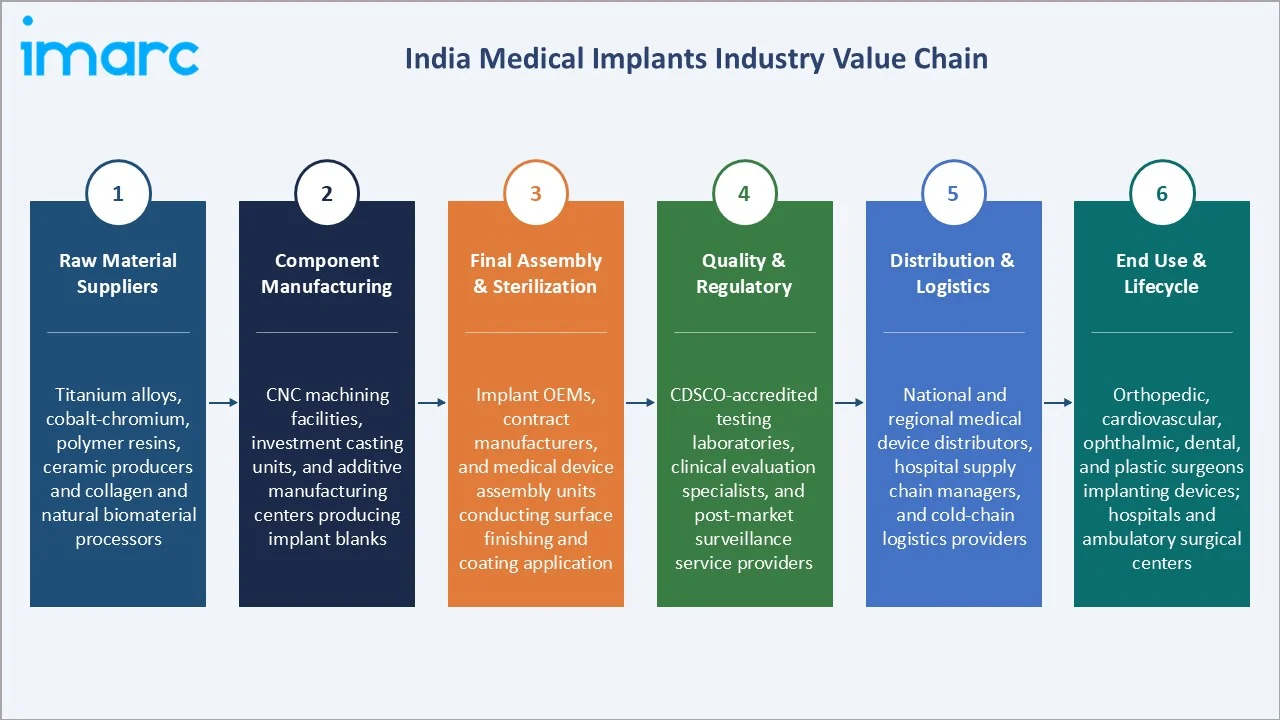

Industry Value Chain Analysis

The India medical implants value chain spans six stages from raw material supply through end-use clinical delivery and post-operative lifecycle management. Manufacturing, quality assurance, and regulatory compliance capture the highest value-add, while distribution and hospital procurement networks increasingly determine market access and penetration speed across geographic segments.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Titanium alloy producers, cobalt-chromium suppliers, polymer resin manufacturers, calcium phosphate ceramic producers, and collagen and natural biomaterial processors supplying base substrates for implant fabrication |

|

Component Manufacturing |

CNC machining facilities, investment casting units, injection molding shops, and additive manufacturing centers producing implant blanks, components, and semi-finished device subassemblies |

|

Final Assembly & Sterilization |

Implant OEMs, contract manufacturers, and medical device assembly units conducting surface finishing, coating application, component assembly, and EtO or gamma sterilization for sterile final products |

|

Quality & Regulatory |

CDSCO-accredited testing laboratories, clinical evaluation specialists, and post-market surveillance service providers supporting device registration and compliance |

|

Distribution & Logistics |

National and regional medical device distributors, hospital supply chain managers, cold-chain logistics providers, and direct manufacturer-to-hospital sales networks managing last-mile implant delivery |

|

End Use & Lifecycle |

Orthopedic, cardiovascular, ophthalmic, dental, and plastic surgeons implanting devices; hospitals and ambulatory surgical centers; patient rehabilitation services; and device vigilance programs managing post-implantation outcomes |

Medical implant manufacturers with end-to-end capabilities spanning design, production, regulatory approval, and market access are likely to capture greater value than firms dependent on external manufacturing partners or niche product offerings.

Technology Landscape in the India Medical Implants Industry

Advanced Biomaterials and Surface Engineering

Material science innovation is central to improving implant longevity, biocompatibility, and osseointegration. Titanium alloys with enhanced fatigue resistance, cobalt-chromium alloys for cardiovascular devices, zirconia ceramics for dental prosthetics, and PEEK for spinal applications are established platforms. Emerging surface engineering techniques, including hydroxyapatite coatings, antibacterial nano-silver layers, and plasma spray treatments, are reducing infection risk and improving long-term fixation.

Additive Manufacturing and Digital Implant Design

3D printing of patient-specific implants using titanium powder bed fusion, stainless steel selective laser sintering, and polymer fused deposition modeling is enabling surgeons to preoperatively plan and physically test implant fit. Digital design workflows integrating CT scan data, finite element analysis, and computer-aided design tools are compressing the lead time for custom implant fabrication from weeks to days.

Smart Implants and Connected Monitoring

Research and early commercial deployment of implants embedded with pressure sensors, accelerometers, and wireless communication chips are enabling real-time monitoring of implant loading, joint kinematics, and device performance. Smart implants for joint replacements and cardiac rhythm management are in various stages of clinical validation globally, with Indian academic medical centers beginning to participate in related trials.

Minimally Invasive and Robotic Delivery Systems

Robotic-assisted surgical systems for knee and hip replacement, transcatheter delivery systems for cardiac valves and closure devices, and phacoemulsification platforms for cataract and intraocular lens implantation are expanding the precision and safety profile of implant delivery. These technologies are increasingly available at leading Indian tertiary care hospitals, driving higher adoption of advanced implant systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Orthopedic Implants |

34.8% |

2025 |

|

Material |

Metallic Biomaterial |

42.7% |

2025 |

|

Region |

South India |

31.4% |

2025 |

By Product

Orthopedic implants command a 34.8% majority share in 2025, driven by high and growing joint replacement volumes for knee, hip, and shoulder conditions, expanding spine surgery adoption, and rising trauma fixation demand from road accidents and sports injuries. The segment benefits from strong surgical infrastructure at leading orthopedic centers, growing penetration of imported implant systems, and expanding domestic manufacturing under PLI incentives.

To access detailed market analysis, Request Sample

Cardiovascular implants at 24.6% in 2025 cover coronary stents, pacemakers, implantable cardioverter-defibrillators, heart valves, and vascular grafts. India's significant cardiovascular disease burden, high stent procedure volumes, and expanding cardiac surgery capacity at both public and private hospitals support sustained demand.

By Material

Metallic biomaterial dominates with 42.7% share in 2025, underpinned by the widespread use of titanium and its alloys in orthopedic implants, cobalt-chromium in cardiovascular and orthopedic applications, and stainless steel in trauma fixation devices. The superior mechanical strength, corrosion resistance, and decades of established clinical evidence for metallic implants sustain their leadership across high-volume surgical categories.

7.webp)

Polymers biomaterial at 29.5% in 2025 covers a broad range of implant applications, supported by its design flexibility, lightweight characteristics, biocompatibility, and suitability for both permanent and bioresorbable medical devices.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

31.4% |

High-density private hospital networks, advanced surgical infrastructure, strong medical tourism inflows, and large specialist physician base in Tamil Nadu, Karnataka, and Telangana |

|

West India |

28.2% |

Established metro healthcare markets in Maharashtra and Gujarat, high concentration of orthopedic and cardiac centers, growing corporate hospital chains, and robust health insurance penetration |

|

North India |

24.1% |

Large and dense population base, rapidly expanding private hospital capacity in Delhi-NCR and Uttar Pradesh, growing government health scheme coverage, and increasing medical tourism from neighboring countries |

|

East India |

16.3% |

Emerging private healthcare investment, expanding government hospital upgradation in West Bengal and Odisha, growing urban population, and rising health awareness driving implant procedure adoption |

South India at 31.4% in 2025 leads the regional landscape, anchored by Tamil Nadu, Karnataka, Andhra Pradesh, and Telangana. High-density tertiary care hospital infrastructure, a deep pool of orthopedic, cardiovascular, and ophthalmic specialists, and India's surging medical tourism inflows from international patients seeking cost-effective implant procedures sustain its regional leadership across all major implant categories.

West India at 28.2% is among the fastest-growing regions. Maharashtra and Gujarat offer a mature corporate hospital ecosystem, high private insurance penetration, and a growing base of trained implant surgeons across orthopedic, dental, and cosmetic specialties.

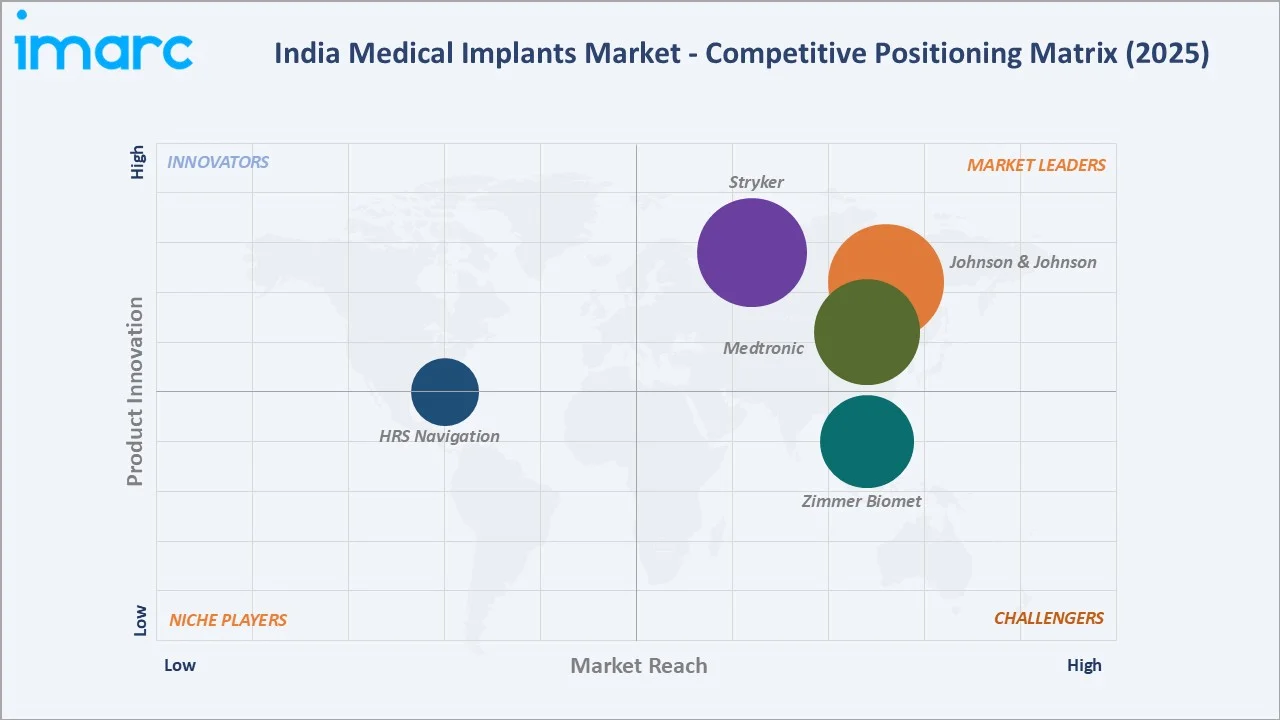

Competitive Landscape

The India medical implants market is moderately concentrated, with multinational corporations holding leading shares in high-value orthopedic, cardiovascular, and ophthalmic implant categories, while domestic manufacturers are strengthening positions in standardized orthopedic fixation, dental, and lower-cost implant segments. Brand equity, regulatory approvals, surgeon relationships, product breadth, and service network quality form the primary competitive differentiators.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Johnson & Johnson |

DePuy Synthes, VELYS |

Leader |

Broad orthopedic portfolio with strong surgeon training and hospital partnership programs |

|

Stryker |

Mako SmartRobotics, Triathlon Knee |

Leader |

Technology-driven orthopedic and surgical equipment company with advanced robotic-assisted joint replacement systems |

|

Medtronic |

Mazor X Stealth |

Leader |

Global leader in cardiac rhythm management, spinal, and neurovascular implants with expanding India market presence |

|

Zimmer Biomet |

Persona The Personalized Knee, ROSA Robotic Solutions |

Challenger |

Specialized orthopedic implants across hip, knee, spine, and extremities with strong distributor network in India |

|

HRS Navigation |

easyNav |

Emerging |

Indian surgical navigation technology company offering image-guided systems for cranial, spine, and ENT surgeries across domestic hospital networks |

Key players include Johnson & Johnson, Stryker, Medtronic, Zimmer Biomet, and HRS Navigation, among others.

Key Company Profiles

Johnson & Johnson

Johnson & Johnson is a global healthcare conglomerate headquartered in New Brunswick, New Jersey, United States. The firm has maintained a long-standing presence in the Indian market through its hospital and surgical device businesses.

- Product Portfolio: DePuy Synthes orthopedic implants covering hip, knee, spine, and trauma fixation; VELYS robotic-assisted surgical system for joint replacement; surgical instruments and enabling technologies across orthopedic and general surgery specialties; and vision care devices including intraocular lenses for ophthalmic procedures.

- Recent Developments: Johnson & Johnson has continued to invest in orthopedic innovation, robotic-assisted surgery capabilities, and digital surgical technologies while expanding clinical education initiatives and strengthening collaborations with healthcare providers to support advanced patient care.

- Strategic Focus: Advancing orthopedic innovation through robotic and digital surgery platforms, expanding hospital partnerships, and strengthening its presence in high-growth emerging markets including India.

Stryker

Stryker is a global medical technology company headquartered in Kalamazoo, Michigan, United States. The firm serves hospitals, ambulatory surgical centers, and healthcare systems across several countries, with an established commercial presence in India.

- Product Portfolio: Mako SmartRobotics robotic-arm assisted surgical system for hip, knee, and spine procedures; Triathlon knee reconstruction system; hip and trauma implant systems; surgical instruments and power tools; and a range of enabling technologies and navigation solutions for orthopedic surgery.

- Recent Developments: Stryker continues to expand its orthopedic robotics and implant portfolio, investing in next-generation surgical technologies and strengthening its hospital network across key markets including India.

- Strategic Focus: Driving adoption of robotic-assisted surgery, expanding its orthopedic implant portfolio across reconstruction and trauma segments, and deepening hospital and surgeon relationships in high-growth markets.

Medtronic

Medtronic is a global healthcare technology company with operational headquarters in Minneapolis, Minnesota, United States. The company develops and manufactures a wide range of medical devices and therapies across cardiovascular, neuroscience, medical surgical, and diabetes segments, operating in several countries.

- Product Portfolio: Cardiac rhythm management devices including pacemakers and implantable defibrillators; structural heart and coronary therapies; Mazor X Stealth robotic guidance system; spinal implants and instruments; and neuromodulation devices for pain and movement disorders.

- Recent Developments: Medtronic continues to expand its presence in India across cardiac, spinal, and surgical segments, investing in clinical education programs and strengthening its distribution and service infrastructure for hospital customers.

- Strategic Focus: Advancing minimally invasive and robotic-assisted surgical solutions, driving adoption of its enabling technologies in spine and neuroscience, and expanding access to cardiac therapies in emerging markets including India.

Market Concentration Analysis

The India medical implants market exhibits moderate concentration, with the top four multinational corporations - Johnson & Johnson, Stryker, Medtronic, and Zimmer Biomet - collectively accounting for an estimated 50-60% of the organized market value across high-value orthopedic, cardiovascular, and ophthalmic implant categories as of 2025.

Barriers to entry in premium implant segments include extensive regulatory approval processes under CDSCO, high capital investment in clinical validation and post-market surveillance, deep surgeon relationship requirements, and the need for comprehensive service and repair infrastructure. These factors favor well-capitalized multinational incumbents with established India operations and trained sales force networks.

The market is simultaneously witnessing consolidation at the premium end and fragmentation at the value segment. Domestic manufacturers are gaining share in standardized trauma fixation, lower-cost joint replacement, and dental implant categories, supported by PLI incentives, government procurement programs, and import substitution policies.

Investment & Growth Opportunities

Fastest-Growing Segments

Dental implants are expanding at the fastest CAGR among product categories, driven by rising consumer awareness of osseointegrated implant-based tooth restoration, growing dental tourism in metropolitan centers, and increasing availability of implant-trained dentists across India. Cardiovascular implants are the next-fastest segment as cardiac procedure volumes accelerate with the expanding specialist physician base and growing health insurance coverage.

Emerging Markets

West India and North India are the fastest-growing regions for implant adoption. Maharashtra and Gujarat in the west are seeing rapid private hospital investment in orthopedic and cardiac device capabilities, while Delhi-NCR and Uttar Pradesh in the north are benefiting from government hospital upgradation and expanding Ayushman Bharat coverage for implant procedures.

Venture & Investment Trends

Investment is concentrated in domestic implant manufacturing scale-up under the PLI scheme, medical device startup ecosystems in Bengaluru and Hyderabad focused on bioabsorbable and smart implants, and digital surgery platforms enabling robotic-assisted implant placement. Capital is also flowing into hospital chains expanding orthopedic and cardiac surgery departments in tier-2 cities, directly driving implant volume growth in underserved geographies.

Future Market Outlook (2026-2034)

The India medical implants market is forecast to expand from USD 6.75 Billion in 2025 to USD 11.52 Billion by 2034 at a CAGR of 5.93%, adding approximately USD 4.77 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: a modernizing and more efficient CDSCO regulatory framework; the emergence of domestic manufacturing competitiveness under PLI and allied government programs; the rise of minimally invasive, robotic-assisted, and personalized implant delivery models; and the continued expansion of health insurance and government scheme reimbursement coverage driving volume penetration across lower-income patient segments.

By 2034, the India medical implants market is expected to be defined by a more balanced mix of domestic and imported implant products, with Indian manufacturers capturing meaningful share in standardized orthopedic, dental, and biomaterial categories.

Research Methodology

Primary Research

Primary research included structured interviews with orthopedic, cardiovascular, ophthalmic, and dental surgeons; hospital procurement managers; implant distributor executives; regulatory affairs specialists at medical device companies; and government health program administrators. These interviews validated market sizing, segmentation dynamics, regional demand patterns, and product category evolution across the India medical implants ecosystem.

Secondary Research

Secondary sources included CDSCO medical device registration databases, Ministry of Health and Family Welfare publications, National Health Authority reports, DPIIT PLI scheme disclosures, industry association reports from AIMED and FICCI Health, company annual reports, press releases, and investor presentations from listed implant manufacturers and distributors operating in India.

Forecasting Models

Market forecasts used bottom-up models combining procedure volume estimates by implant category, average implant unit values, import versus domestic supply split evolution, insurance reimbursement expansion trajectories, and macroeconomic variables including GDP growth, healthcare expenditure trends, and demographic projections. Scenario analysis addressed regulatory timeline uncertainty, domestic manufacturing ramp-up pace, and medical tourism growth rate assumptions.

India Medical Implants Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Materials Covered | Metallic Biomaterial, Polymers Biomaterial, Natural Biomaterial, Ceramic Biomaterial |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Johnson & Johnson, Stryker, Medtronic, Zimmer Biomet, HRS Navigation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India medical implants market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India medical implants market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India medical implants industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Medical Implants Market Report

The India medical implants market was valued at USD 6.75 Billion in 2025, driven by rising chronic disease burden, aging population, growing surgical volumes, and expanding hospital infrastructure.

The market is projected to grow at a CAGR of 5.93% from 2026 to 2034, reaching USD 11.52 Billion, supported by domestic manufacturing expansion, rising implant accessibility, and growing cardiovascular and orthopedic procedure volumes.

Orthopedic implants lead with 34.8% share in 2025, fueled by high joint replacement volumes, rising sports injuries, and growing orthopedic surgery infrastructure across Indian hospitals.

Metallic biomaterial dominates at 42.7% in 2025, benefiting from the widespread use of titanium alloys, cobalt-chromium, and stainless steel in orthopedic and cardiovascular implant applications.

South India commands 31.4% in 2025, led by high-density private hospital networks, strong medical tourism inflows, and advanced surgical infrastructure in Tamil Nadu, Karnataka, and Telangana.

Leading players include Johnson & Johnson, Stryker, Medtronic, Zimmer Biomet, and HRS Navigation, among others.

The PLI scheme is accelerating domestic implant manufacturing investment, reducing import dependency, improving cost competitiveness for Indian-made implants, and supporting export market development by domestic manufacturers.

Medical tourism generates significant additional implant procedure volumes, particularly for orthopedic joint replacement and cardiac procedures, as patients from neighboring countries and global markets seek cost-effective, high-quality implant surgeries in India.

Key challenges include high implant costs limiting affordability, import dependency for premium devices, skilled surgeon concentration in metro cities, regulatory compliance complexity, and inconsistent insurance reimbursement coverage for implant procedures.

Dental implant growth is driven by rising consumer awareness of osseointegrated implants over dentures, expanding dental tourism, growing availability of implant-trained dentists, and increasing disposable incomes supporting elective dental procedures in urban markets.

3D printing for patient-specific implants, robotic-assisted surgical systems, bioabsorbable materials, smart implant sensors, and AI-driven surgical planning are transforming implant design, delivery precision, and long-term clinical outcomes across Indian hospital networks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)