India Micro-Mobility Market Size, Share, Trends and Forecast by Type, Propulsion Type, Sharing Type, Speed, Age Group, Ownership, and Region, 2026-2034

India Micro-Mobility Market Summary:

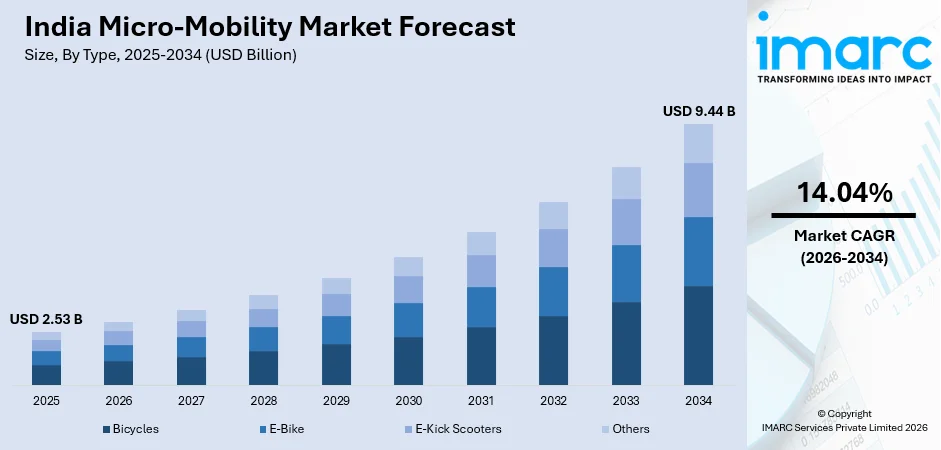

The India micro-mobility market size was valued at USD 2.53 Billion in 2025 and is projected to reach USD 9.44 Billion by 2034, growing at a compound annual growth rate of 14.04% from 2026-2034.

India's micro-mobility market is expanding rapidly, driven by accelerating urbanization, worsening traffic congestion, and rising environmental awareness among urban populations. Supportive government policies promoting sustainable last-mile transportation, growing integration of shared mobility platforms with public transit networks, and a large young demographic increasingly embracing flexible commuting options are collectively reinforcing the India micro-mobility market share across metropolitan and tier-two cities.

Key Takeaways and Insights:

- By Type: Bicycles dominate the market with a share of 62.4% in 2025, driven by their affordability, cultural familiarity, and suitability for short-distance urban and semi-urban commuting across diverse income groups.

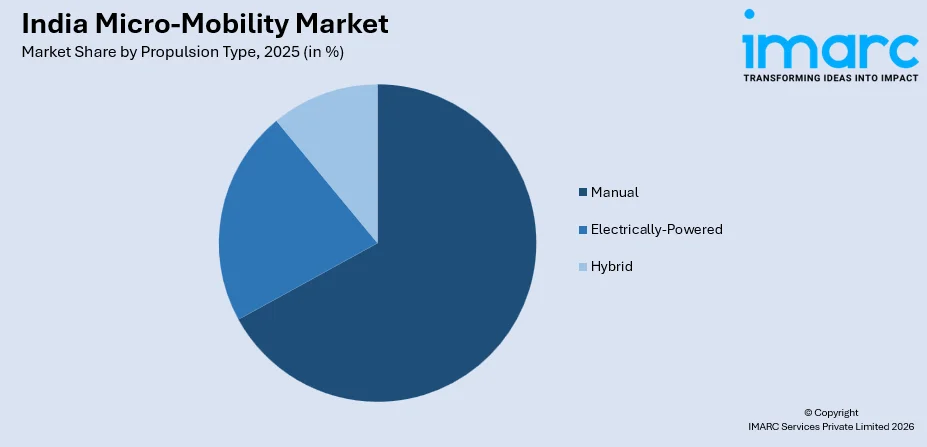

- By Propulsion Type: Manual leads the market with a share of 66.7% in 2025, reflecting widespread preference for low-cost, maintenance-free mobility that requires no charging infrastructure or fuel dependency.

- By Sharing Type: Dock-less holds the largest market share of 54.5% in 2025, valued for its operational flexibility and user convenience in locating and returning vehicles across any permissible urban location.

- By Speed: The less than 25 Kmph dominates the market with a share of 96.2% in 2025, aligning with urban traffic realities, regulatory frameworks, and rider safety preferences in India's congested metropolitan environments.

- By Age Group: 15-34 leads with a share of 67.8% in 2025, reflecting younger consumers' openness to sustainable, technology-enabled mobility and active usage of app-based shared vehicle platforms.

- By Ownership: Business-To-Consumer holds the largest share of 56.5% in 2025, as individual consumers increasingly invest in personal micro-mobility vehicles for daily commuting amid growing affordability and environmental consciousness.

- By Region: South India dominates the market with a share of 32.2% in 2025, supported by progressive state-level policies, high urban density, and active smart city infrastructure development.

- Key Players: The India micro-mobility market features a competitive mix of domestic operators and international players offering bicycle and e-scooter sharing services, fleet-based ownership models, and integrated urban mobility platforms.

To get more information on this market Request Sample

India's micro-mobility sector has emerged as a vital component of the country's urban transportation ecosystem, addressing persistent challenges of congestion, pollution, and last-mile connectivity gaps. The market spans a diverse range of vehicles including bicycles, e-scooters, and e-bikes deployed across personal ownership and shared-use models. Rapid urbanization has intensified demand for flexible, low-emission commuting alternatives, particularly among cost-conscious young professionals and students. In March 2024, the Government of India launched the Electric Mobility Promotion Scheme (EMPS 2024) to accelerate adoption of electric two- and three-wheelers by providing financial incentives for eligible vehicles and strengthening the domestic EV ecosystem. Government programs promoting sustainable urban mobility, investments in dedicated cycling infrastructure, and the proliferation of digital platforms enabling seamless vehicle access have created a conducive growth environment. As cities prioritize green transportation agendas, integrating micro-mobility within broader public transit systems is stimulating adoption and deepening market penetration across diverse demographic groups nationwide.

India Micro-Mobility Market Trends:

Growing Integration with Public Transit Systems

Micro-mobility vehicles in India are increasingly being embedded within multimodal urban transport frameworks, functioning as reliable first- and last-mile connectors to metro rail and bus rapid transit systems. Urban planners and local authorities are allocating dedicated lanes and secure parking zones for bicycles and scooters near transit hubs. For instance, in April 2025, the Delhi Metro Rail Corporation launched the ‘Sarthi-Momentum 2.0’ integrated mobility service, enabling commuters to book bike taxis and auto-rickshaws for first- and last-mile travel along with metro tickets through a single mobile application. This integration enhances commute efficiency, reduces private vehicle dependency, and encourages adoption among daily transit users seeking seamless, low-emission travel experiences.

Rising Demand for App-Based Shared Mobility Platforms

Digital technology is transforming how urban residents access micro-mobility vehicles across Indian cities. Mobile applications enabling real-time vehicle location, cashless payments, and instant booking have significantly lowered adoption barriers. For instance, in April 2024, shared electric mobility company Yulu launched its app-enabled electric two-wheeler service in Indore through a partnership with Yuva Mobility, deploying IoT-enabled EVs that users can locate, unlock, and rent through a smartphone platform. Expanding smartphone penetration in metropolitan and tier-two cities accelerates the shift toward platform-driven micro-mobility services. This trend is particularly pronounced among tech-savvy younger commuters who prioritize convenience, affordability, and environmentally responsible transportation choices in their daily urban mobility decisions.

Expansion of Smart City Initiatives Driving Infrastructure Development

India's Smart Cities Mission is catalyzing infrastructure investments that directly benefit the micro-mobility sector. Development of non-motorized transport corridors, dedicated cycling tracks, and pedestrian-friendly urban zones is creating safer environments for bicycle and scooter users. For instance, in January 2024, the Ministry of Housing and Urban Affairs reported that more than 600 km of cycle tracks had been developed across 100 cities under the Smart Cities Mission to promote non-motorized and sustainable urban mobility. These planned urban interventions are encouraging residents to transition from private motorized vehicles toward sustainable short-distance transportation, establishing micro-mobility as a central pillar of future-ready, low-carbon urban mobility planning across Indian cities.

Market Outlook 2026-2034:

India's micro-mobility market is poised for sustained expansion over the forecast period, driven by accelerating urbanization, rising environmental consciousness, and progressive policy frameworks championing sustainable urban transportation. Growing consumer preference for shared and electric mobility solutions, coupled with continued investments in cycling infrastructure and smart city initiatives, will unlock significant growth opportunities. Favorable demographic trends, deepening digital platform ecosystems, and increasing integration of micro-mobility within multimodal transit networks will collectively shape the market's long-term trajectory and broaden adoption across diverse urban populations. The market generated a revenue of USD 2.53 Billion in 2025 and is projected to reach a revenue of USD 9.44 Billion by 2034, growing at a compound annual growth rate of 14.04% from 2026-2034.

India Micro-Mobility Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Bicycles |

62.4% |

|

Propulsion Type |

Manual |

66.7% |

|

Sharing Type |

Dock-Less |

54.5% |

|

Speed |

Less than 25 Kmph |

96.2% |

|

Age Group |

15-34 |

67.8% |

|

Ownership |

Business-To-Consumer |

56.5% |

|

Region |

South India |

32.2% |

Type Insights:

- Bicycles

- E-Bike

- E-Kick Scooters

- Others

The bicycles dominates with a market share of 62.4% of the total India micro-mobility market in 2025.

Bicycles signify the most deeply rooted category of micro-mobility vehicles, which are an integral part of the daily commuting habits of millions of citizens across the country, cutting across urban, semi-urban, and rural domains. The cost factor of these vehicles, which is naturally low, makes them accessible to the broad spectrum of the country’s economic population, ranging from students and daily wage laborers to urban professionals looking for efficient means of short-distance commutation. The lack of dependency on fuel or electrical energy makes these vehicles more attractive and contributes to their sustained popularity among the country’s diverse population.

In addition to their use as personal commuting vehicles, bicycles are increasingly being leveraged for the purpose of bike-sharing, which enables the seamless movement of individuals between hubs and destinations. The adaptability of these vehicles in traversing the complex network of urban roads and streets makes them the most appropriate category of vehicles for the country’s road infrastructure. The growing recognition of the fitness and environmental advantages of cycling has resulted in the widening scope of the bicycle’s user demographic, with urban citizens looking for healthy and environment-friendly means of personal commutation.

Propulsion Type Insights:

Access the comprehensive market breakdown Request Sample

- Manual

- Electrically-Powered

- Hybrid

The manual leads with a share of 66.7% of the total India micro-mobility market in 2025.

Manual micro-mobility vehicles, primarily conventional bicycles and non-motorized scooters, dominate India's market owing to their cost accessibility and simplicity of operation. For instance, in April 2024, the All India Cycle Manufacturers’ Association reported that bicycle sales in India reached about 10.67 million units in FY2023–24, reflecting sustained demand for affordable manual mobility solutions used for daily commuting. The absence of battery charging requirements makes manual vehicles highly practical across areas with inconsistent electricity supply or limited charging infrastructure. For a vast portion of India's urban population, particularly in smaller cities and peri-urban zones, manual vehicles represent the most reliable and economically viable short-distance transport option, sustaining widespread adoption across diverse geographic segments.

The manual segment benefits from minimal maintenance requirements and extended operational lifespans compared to electric counterparts, substantially reducing total cost of ownership. Traditional commuters and delivery personnel favor manual vehicles for their robustness across varied road conditions encountered in Indian urban environments. Cultural familiarity with bicycles and non-motorized transport has further entrenched manual propulsion as the dominant mode within India's micro-mobility landscape, even as electric alternatives steadily gain momentum in premium urban and technology-forward markets among higher-income demographic groups.

Sharing Type Insights:

- Docked

- Dock-Less

The dock-less dominates with a market share of 54.5% of the total India micro-mobility market in 2025.

Dock-less micro-mobility services have emerged as the preferred sharing model across India, driven by their operational flexibility and exceptional user convenience. Unlike docked systems requiring designated parking stations, dock-less vehicles allow users to locate, unlock, and return vehicles at virtually any permissible urban location via smartphone applications. This model reduces dependence on physical infrastructure investment, enabling rapid service expansion across dense urban neighborhoods, campuses, and transit corridors without requiring extensive upfront capital allocation from platform operators.

The dock-less model aligns naturally with the spontaneous and varied mobility needs of Indian urban commuters who require adaptable transportation options across unpredictable routes and schedules. Operators benefit from lower infrastructure costs while achieving broader geographic coverage across city zones. Advances in GPS tracking and IoT-enabled vehicle management have addressed earlier concerns around improper parking, making dock-less services increasingly viable for large-scale urban deployment. Growing digital literacy further supports seamless app-based interactions, enhancing service adoption among users of varying technological proficiency.

Speed Insights:

- Less than 25 Kmph

- Above 25 Kmph

The less than 25 Kmph leads with a share of 96.2% of the total India micro-mobility market in 2025.

Vehicles operating below 25 Kmph constitute the overwhelming majority of India's micro-mobility fleet, encompassing conventional bicycles, shared cycles, and entry-level electric scooters governed to comply with regulatory speed thresholds. This speed category aligns with urban traffic realities where congestion naturally limits vehicle movement in densely populated metropolitan areas. Regulatory frameworks in India classify low-speed electric vehicles more favorably than high-speed motorized alternatives, facilitating easier registration and operation for both individual owners and platform operators serving daily commuting needs.

Safety considerations among urban commuters, particularly first-time riders and elderly users, reinforce consistent preference for lower-speed mobility options in mixed-traffic environments. Reduced speeds lower collision risk severity, building consumer confidence and encouraging everyday adoption across a broader demographic spectrum. Compatibility of sub-25 Kmph vehicles with dedicated cycling lanes and pedestrian zones expands accessible route options, making them integral to India's non-motorized urban transport networks. Their alignment with regulatory mandates and public safety objectives ensures continued dominance within the market's vehicle speed composition.

Age Group Insights:

- 15-34

- 35-54

- 55 and Above

The 15-34 dominates with a market share of 67.8% of the total India micro-mobility market in 2025.

Young adults between 15 and 34 years constitute the primary consumer base of India's micro-mobility market, reflecting generational preferences for sustainable, flexible, and technology-enabled transportation. This demographic demonstrates high comfort with app-based service interactions and readily embraces shared mobility concepts that reduce ownership burdens and associated costs. University students, young working professionals, and gig economy workers represent particularly active users, leveraging micro-mobility for daily commutes, campus navigation, and last-mile connections enhancing their overall urban mobility experience.

This age cohort's environmental consciousness and desire for alternatives that bypass congestion align naturally with micro-mobility's core value proposition. The demographic drives demand for technologically integrated vehicle designs featuring connectivity, real-time navigation, and smart locking systems. Their comfort with subscription-based and pay-per-use pricing models further accelerates platform-driven service adoption. As India's young urban population continues growing and concentrating in metropolitan centers, this age group will remain the primary driver of micro-mobility adoption, shaping product development and marketing strategies across the sector.

Ownership Insights:

- Business-To-Business

- Business-To-Consumer

Business-to-consumer leads with a share of 56.5% of the total India micro-mobility market in 2025.

Business-to-consumer ownership models reflect individual consumers' growing preference for personally owned micro-mobility vehicles as dependable daily commuting tools. Rising disposable incomes, affordable product pricing, and accessible financing options have collectively lowered barriers to personal vehicle acquisition among urban and semi-urban populations. The increasing availability of diverse product ranges, including feature-rich bicycles and stylish personal electric scooters targeting lifestyle-conscious buyers, has broadened the addressable consumer base and sustained strong direct sales across organized retail and expanding e-commerce channels.

Consumer awareness of micro-mobility's cost-saving advantages over conventional motorized transport, including reduced maintenance costs and elimination of parking fees, reinforces B2C demand across income segments. Personal ownership addresses hygiene and availability reliability concerns that some consumers associate with shared-use models. As urban Indian households increasingly recognize micro-mobility vehicles as practical everyday assets rather than recreational items, personal ownership is expected to maintain its market-leading position, supported by growing product diversity and expanding retail accessibility throughout the forecast period.

Regional Insights:

- North India

- South India

- East India

- West India

South India exhibits a clear dominance with a 32.2% share of the total India micro-mobility market in 2025.

South India's market leadership is underpinned by high urban density, progressive state-level policies on sustainable transportation, and the presence of technology-forward cities fostering smart mobility ecosystems. States including Karnataka, Tamil Nadu, Telangana, and Kerala have proactively supported cycling infrastructure development, introduced bike-sharing programs within smart city frameworks, and demonstrated relatively higher consumer openness to adopting shared and electric micro-mobility as practical urban commuting alternatives, cultivating a mature and receptive user base across the region.

The region's robust technology and knowledge economy workforce, concentrated in cities characterized by challenging daily commutes, has cultivated an environmentally conscious demographic predisposed to micro-mobility adoption. Favorable weather conditions across much of South India extend the practical usability of bicycles and scooters throughout the year. Continued smart city investments and transit-oriented development across southern metropolitan areas are expected to further consolidate the region's leadership position, attracting platform operators and infrastructure investors throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Micro-Mobility Market Growing?

Rapid Urbanization and Growing Traffic Congestion

India's sustained urbanization is generating unprecedented demand for efficient short-distance transportation in cities overwhelmed by traffic congestion. As urban populations expand and road infrastructure struggles to accommodate growing vehicle volumes, commuters actively seek flexible alternatives that offer speed and convenience without contributing to gridlock. Micro-mobility vehicles, uniquely suited for navigating dense urban environments, emerge as a natural and practical response to this systemic challenge. For instance, in November 2024, Yulu launched its shared electric mobility services in Kolkata through a partnership with Electrie, expanding app-based electric two-wheeler access for last-mile commuting and delivery services in the city. The concentration of economic activity, educational institutions, and commercial centers within compact urban cores shortens average commuting distances, enhancing the inherent practicality of micro-mobility.

Favorable Government Policies and Smart City Initiatives

Government policies at central and state levels play a pivotal role in shaping the expansion of India's micro-mobility sector. The Smart Cities Mission and related urban development programs have catalyzed investments in cycling infrastructure, non-motorized transport corridors, and intermodal transit hubs that support micro-mobility integration. For instance, in February 2025, the Directorate of Urban Transport in Uttar Pradesh announced a public-private partnership initiative to deploy rental e-bikes and e-cycles across 15 cities including Lucknow, Kanpur, and Varanasi to enhance last-mile connectivity and promote sustainable commuting. State governments are actively formulating electric vehicle policies extending benefits to low-speed electric micro-mobility vehicles, including reduced registration requirements and infrastructure support. The alignment of micro-mobility with national sustainability objectives, particularly the reduction of vehicular emissions and fossil fuel dependency, ensures continued policy backing. Urban local bodies are incorporating cycling-friendly design into city master plans, creating enabling environments that stimulate demand and improve safety for micro-mobility users across Indian cities.

Growing Environmental Consciousness and Preference for Sustainable Commuting

A discernible shift in consumer attitudes toward environmental responsibility is accelerating micro-mobility adoption across India's urban demographic landscape. Heightened awareness of air pollution's impact on public health, combined with global conversations about climate change and carbon reduction, is motivating urban residents to reconsider daily commuting choices. For instance, in April 2023, the International Energy Agency reported that India witnessed one of the fastest increases in electric two-wheeler adoption globally, supported by government incentives and growing consumer interest in low-emission urban mobility solutions. Younger demographics demonstrate strong preferences for transportation modes that minimize carbon footprints and contribute to cleaner urban environments, shaping purchasing behaviors accordingly. Educational institutions, corporate campuses, and residential communities are actively promoting cycling and micro-mobility within broader sustainability commitments, normalizing non-motorized commuting as a responsible and progressive lifestyle choice among environmentally aware urban citizens.

Market Restraints:

What Challenges the India Micro-Mobility Market is Facing?

Inadequate Road Infrastructure and Safety Concerns

The absence of dedicated cycling lanes and safe micro-mobility pathways across large portions of India's urban road network remains a significant deterrent to broader adoption. Mixed-traffic conditions, poorly maintained road surfaces, and inadequate street lighting create genuine safety risks for micro-mobility users. Fear of accidents in high-speed traffic environments discourages potential riders, particularly among older demographics, women, and first-time users unfamiliar with navigating complex urban road scenarios where motorized vehicles dominate.

High Upfront Costs of Electric Micro-Mobility Vehicles

While manual bicycles remain affordable, electric micro-mobility vehicles including e-bikes and e-scooters continue to carry relatively high purchase prices compared to conventional alternatives. For price-sensitive consumer segments constituting a significant portion of India's urban population, initial acquisition costs present a meaningful adoption barrier. Although financing options and government subsidies partially mitigate this challenge, total ownership costs remain prohibitive for lower-income urban households seeking personal electric micro-mobility solutions.

Limited Charging Infrastructure for Electric Variants

Widespread adoption of electric micro-mobility solutions is constrained by insufficient public charging infrastructure, particularly in tier-two and tier-three cities. Unlike manual vehicles requiring no energy replenishment infrastructure, electric bikes and scooters depend on accessible, reliable charging points. Uneven distribution of charging stations, combined with inconsistent electricity supply in some urban and peri-urban areas, creates operational uncertainty among potential users and limits effective coverage areas for electric micro-mobility service providers.

Competitive Landscape:

India's micro-mobility market features a dynamic and evolving competitive landscape characterized by the coexistence of established domestic operators, emerging startups, and technology-driven platform businesses. Market participants compete across fleet size, geographic coverage, pricing models, and technological innovation embedded within vehicle design and app-based service offerings. The sector has attracted considerable investor interest, reflecting strong long-term growth potential and the strategic importance of last-mile mobility within India's urban transport ecosystem. Competitive differentiation increasingly centers on user experience enhancements including intuitive mobile applications, real-time tracking, seamless payment integration, and loyalty programs. Operators offering diversified service portfolios spanning both owned and shared models maintain broader market reach. Strategic partnerships with transit authorities and urban developers are emerging as key priorities, embedding micro-mobility within integrated urban mobility frameworks.

Recent Developments:

- In November 2025, Hero MotoCorp introduced a micro electric four-wheeler concept under its mobility brand VIDA Novus. The company also showcased NEX 1 wearable personal mobility and NEX 2 electric trike, designed for short urban trips and last-mile commuting solutions.

India Micro-Mobility Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Bicycles, E-Bike, E-Kick Scooters, Others |

| Propulsion Types Covered | Manual, Electrically-Powered, Hybrid |

| Sharing Types Covered | Docked, Dock-Less |

| Speeds Covered | Less than 25 Kmph, Above 25 Kmph |

| Age Groups Covered | 15-34, 35-54, 55 and Above |

| Ownerships Covered | Business-To-Business (B2B), Business-To-Consumer (B2C) |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Micro-Mobility Market Report

The India micro-mobility market size was valued at USD 2.53 Billion in 2025.

The India micro-mobility market is expected to grow at a compound annual growth rate of 14.04% from 2026-2034 to reach USD 9.44 Billion by 2034.

Bicycles held the largest India micro-mobility market share of 62.4%, owing to their affordability, widespread availability, and deep-rooted cultural acceptance as a primary mode of short-distance urban commuting.

Key factors driving the India micro-mobility market include rapid urbanization and traffic congestion, favorable government policies and Smart Cities Mission investments, growing environmental consciousness, a large young demographic base, increasing last-mile connectivity demand, and rising adoption of app-based shared mobility platforms.

Major challenges include inadequate dedicated road infrastructure, safety concerns in mixed-traffic urban environments, high upfront costs for electric micro-mobility variants, limited charging infrastructure in tier-two and tier-three cities, and regulatory inconsistencies across different states regarding micro-mobility operations and vehicle classification.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)