India Motor Insurance Market Size, Share, Trends and Forecast by Insurance Type, Application, Distribution Channel, and Region, 2026-2034

India Motor Insurance Market Size, Share, Trends & Forecast (2026-2034)

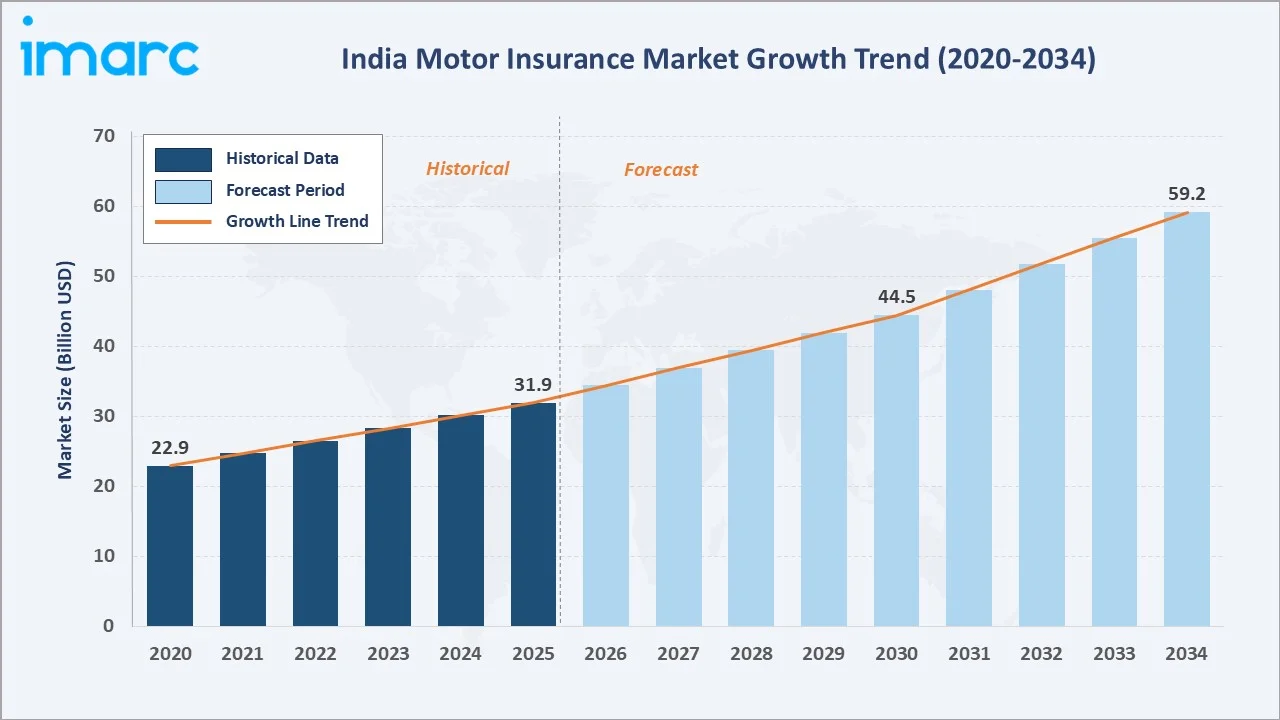

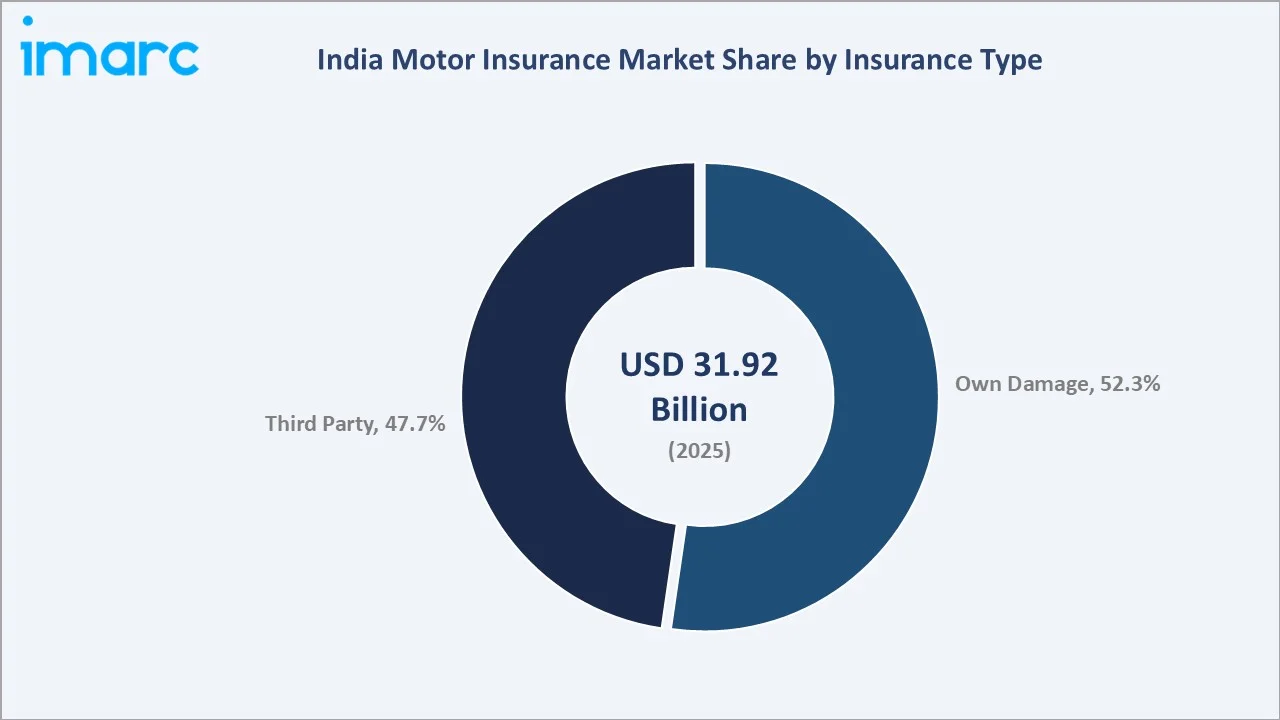

The India motor insurance market reached USD 31.92 Billion in 2025 and is projected to reach USD 59.18 Billion by 2034, growing at a CAGR of 6.84% during 2026-2034. The market is driven by rising vehicle ownership, mandatory third-party insurance regulations, and increasing awareness of comprehensive coverage. Digitalization, fueled by tech adoption and insurtech innovations, enhances customer convenience. Own Damage insurance dominates at 52.3%. Private Motor Insurance leads applications at 58.4%. West India commands 28.6% of the India motor insurance market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 31.92 Billion |

|

Forecast Market Size (2034) |

USD 59.18 Billion |

|

CAGR (2026-2034) |

6.84% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Insurance Type |

Own Damage (52.3%, 2025) |

|

Dominant Application |

Private Motor Insurance (58.4%, 2025) |

|

Leading Region |

West India (28.6%, 2025) |

The India motor insurance market expanded from USD 22.93 Billion in 2020 to USD 31.92 Billion in 2025, anchored at USD 44.45 Billion in 2030, and forecast to reach USD 59.18 Billion by 2034. Regulatory mandates, a rising vehicle parc, and post-pandemic digital adoption have sustained above-trend growth through the 2022-2025 period.

To get more information on this market, Request Sample

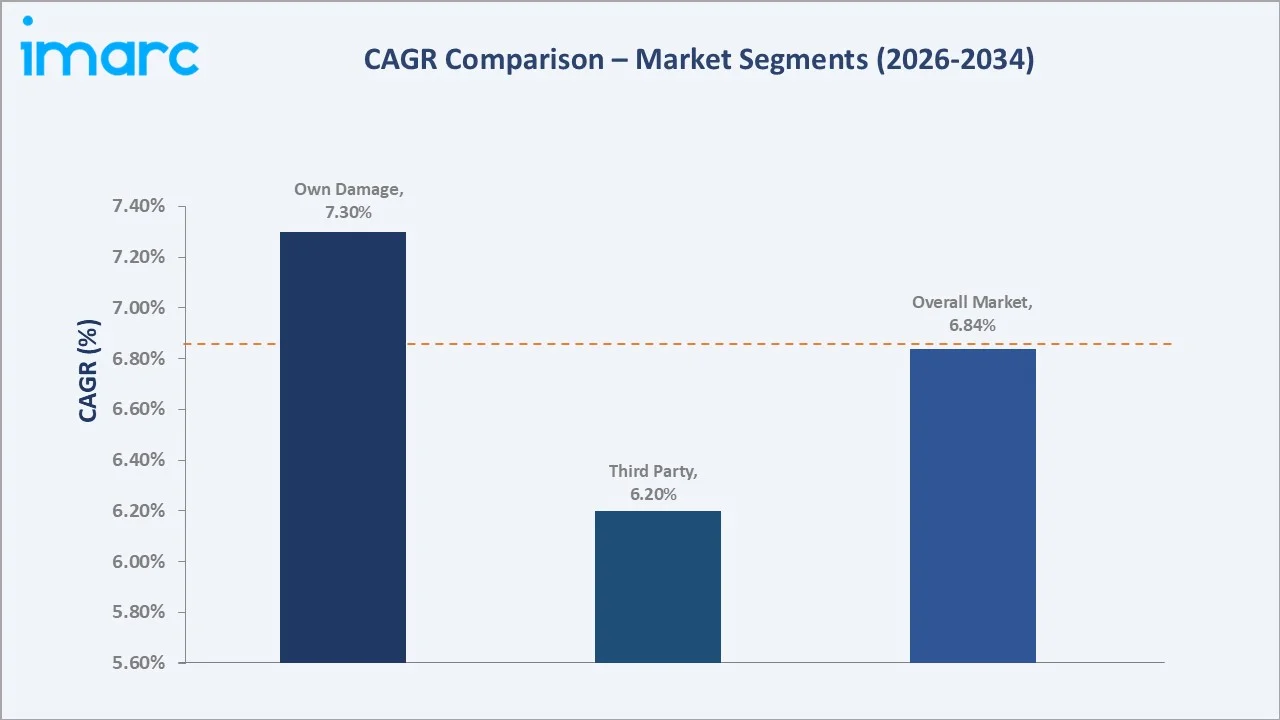

Own Damage insurance grows at approximately 7.3% CAGR as consumer awareness of comprehensive coverage benefits increases alongside rising vehicle values. Private Motor Insurance grows at approximately 7.1% CAGR as passenger vehicle ownership accelerates across urban and semi-urban India.

Executive Summary

The India motor insurance market reached USD 31.92 Billion in 2025, representing one of Asia's most dynamic insurance growth stories at the intersection of regulatory mandates, rising vehicle penetration, and rapid digitalization. The market encompasses own-damage coverage, third-party liability, and comprehensive motor insurance products for both private and commercial vehicles.

Own Damage insurance at 52.3% dominates through consumer preference for comprehensive protection. Private Motor Insurance at 58.4% leads through the structural growth of India's passenger vehicle market. West India at 28.6% leads regionally through Maharashtra and Gujarat's concentrated vehicle ownership and high-density urban markets.

Key Market Insights

|

Insight |

Data |

|

Dominant Insurance Type |

Own Damage – 52.3% share (2025) |

|

Dominant Application |

Private Motor Insurance – 58.4% market share (2025) |

|

Leading Region |

West India – 28.6% market share (2025) |

|

Market Opportunity |

EV-specific products; Usage-based insurance; Telematics integration; Bancassurance expansion; Digital-first insurtechs |

Key Analytical Observations Supporting the Above Data:

- Own Damage at 52.3%: Own Damage insurance dominates due to rising consumer awareness of comprehensive coverage and increasing adoption of high-value vehicles requiring protection beyond mandatory third-party coverage.

- Private Motor Insurance at 58.4%: Private motor insurance leads as passenger vehicle ownership expands rapidly across urban India. Rising middle-class income, EMI-linked vehicle financing, and dealer-led insurance bundling sustain this segment's dominance.

- West India at 28.6%: West India leads through Maharashtra's position as India's largest automotive market and Gujarat's expanding commercial vehicle base, both generating high insurance premium volumes.

India Motor Insurance Market Overview

The India motor insurance market encompasses mandatory third-party liability coverage and voluntary own-damage policies covering private cars, two-wheelers, and commercial vehicles. The Insurance Regulatory and Development Authority of India (IRDAI) governs premium structures, capital requirements, and product approvals.

.webp)

Macroeconomic drivers include India's expanding vehicle parc, government infrastructure investment, and rising urbanization expanding passenger vehicle demand. Climate risk awareness and increasing road accident incidence are also reinforcing demand for comprehensive motor coverage.

Market Dynamics

To evaluate market opportunities, Request Sample

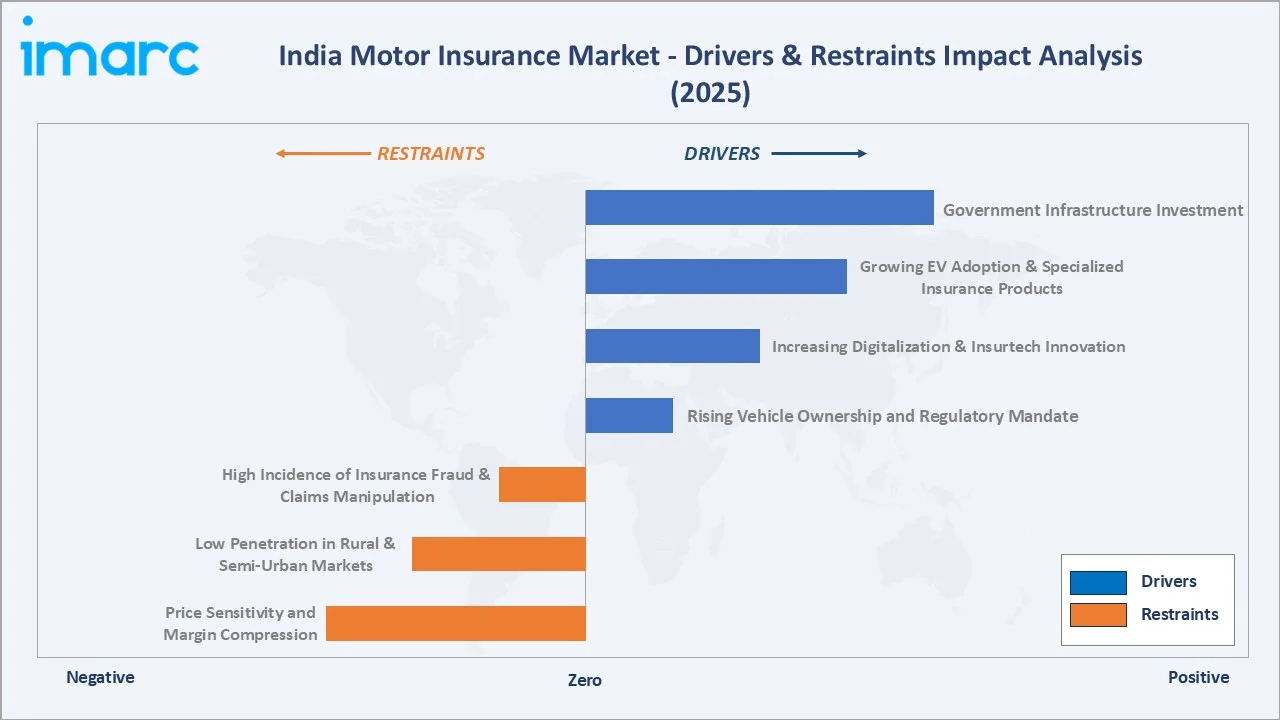

Market Drivers

- Rising Vehicle Ownership and Regulatory Mandate: Growing vehicle registrations, driven by rising per-capita income and accessible financing, coupled with the statutory requirement for third-party insurance coverage, create a structural and expanding demand base for motor insurance premiums across all vehicle categories.

- Increasing Digitalization and Insurtech Innovation: Increasing internet penetration and smartphone adoption are transforming policy distribution, renewal, and claims processing. Digital-first platforms, AI-powered chatbots, and online aggregators are reducing distribution costs and expanding access to underserved customer segments.

- Growing EV Adoption and Specialized Insurance Products: India's expanding electric vehicle market is generating incremental insurance demand for products specifically addressing battery risk, charging infrastructure, and residual value uncertainty, creating premium pool growth beyond conventional motor insurance categories.

- Government Infrastructure Investment: Sustained public investment in road networks and highway connectivity increases vehicle utilization and aggregate premium exposure, while also extending insurance distribution reach into Tier 2 and Tier 3 markets.

Market Restraints

- High Incidence of Insurance Fraud & Claims Manipulation: Motor insurance fraud, including staged accidents and inflated claims, remains a structural challenge that inflates claims costs, pressures underwriting margins, and increases operational burden across the industry.

- Low Penetration in Rural Markets & Semi-Urban Markets: Despite mandatory third-party requirements, enforcement gaps and digital infrastructure limitations leave large portions of the vehicle fleet underinsured in rural and semi-urban markets, constraining overall premium growth.

- Price Sensitivity and Margin Compression: Intense competition among licensed general insurers, combined with regulatory third-party premium caps, creates persistent pricing pressure that limits profitability, particularly for smaller market participants.

Market Opportunities

- Usage-Based Insurance and Telematics: Telematics-enabled UBI products offer risk-proportionate pricing, attracting safe drivers while improving underwriting accuracy and reducing fraudulent claims, creating sustainable competitive differentiation for early adopters.

- Bancassurance and OEM Partnership Expansion: Bank-led distribution and vehicle manufacturer-bundled insurance represent significantly under-penetrated channels capable of capturing first-policy conversions efficiently at the point of vehicle sale.

Market Challenges

- Third-Party Premium Pool Losses: Regulatory pricing constraints on mandatory third-party motor insurance generate sustained underwriting losses that reduce insurer appetite for rural and commercial vehicle exposure and cross-subsidize the broader motor portfolio.

- Claims Settlement Efficiency: Slow or disputed claims settlement erodes consumer trust and willingness to pay for comprehensive coverage, making faster digital claims processing a critical competitive capability for all market participants.

Emerging Market Trends

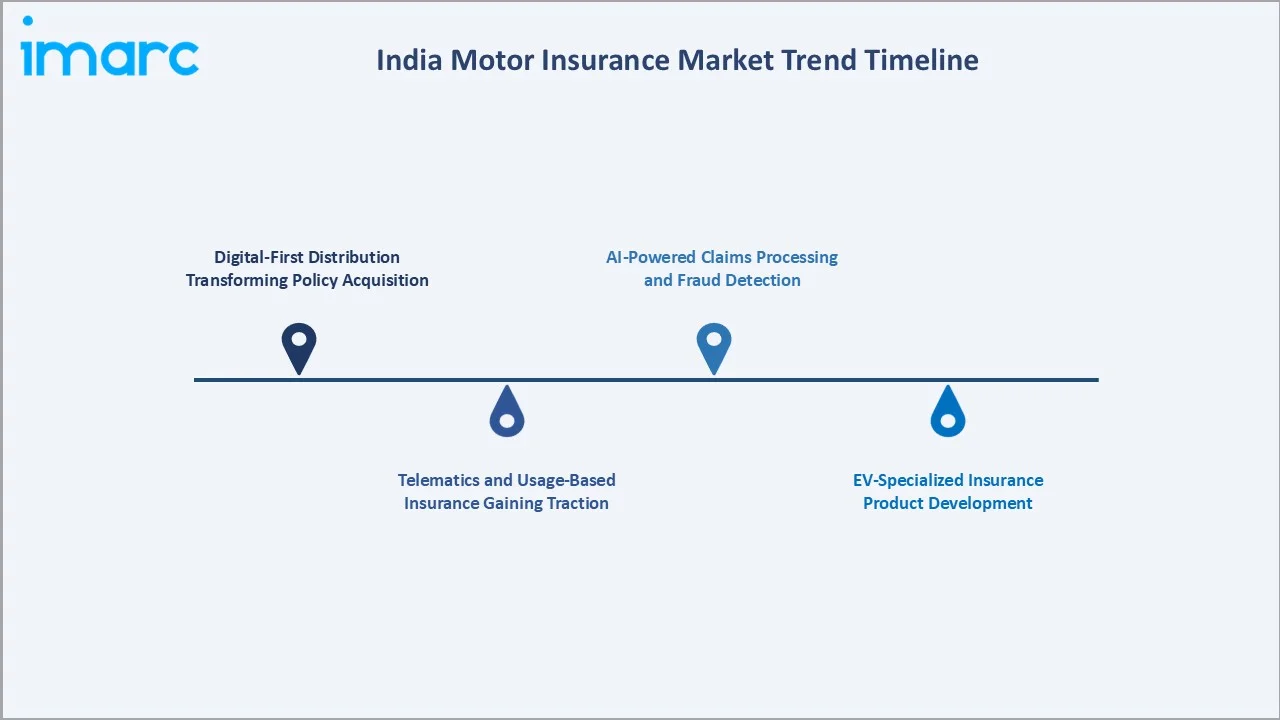

1. Digital-First Distribution Transforming Policy Acquisition

Online motor insurance aggregators, direct digital platforms, and mobile-first insurers are displacing agent-led distribution for renewal policies. Established players are responding through app-based renewal platforms and AI-enabled customer acquisition, driving structural shift in distribution cost economics.

2. Telematics and Usage-Based Insurance Gaining Traction

IRDAI's regulatory sandbox has enabled telematics-based UBI product pilots. OBD-device and smartphone telematic data allow dynamic risk pricing, with adoption concentrated among urban high-mileage fleet operators and younger drivers seeking premium discounts tied to safe driving behaviour.

3. EV-Specialized Insurance Product Development

India's EV transition is catalyzing new insurance product architectures covering battery risk, residual value uncertainty, and charging infrastructure liability. Insurers are partnering with battery swap networks and EV manufacturers to develop tailored coverage structures for this fast-growing vehicle segment.

4. AI-Powered Claims Processing and Fraud Detection

Insurers are deploying AI image recognition for automated vehicle damage assessment from mobile-submitted photographs, reducing claims cycle time significantly. Predictive fraud detection models using claims history and behavioural analytics are also reducing fraudulent claim payouts across the industry.

Industry Value Chain Analysis

The India motor insurance value chain integrates product design and pricing, policy distribution, underwriting and risk assessment, policy administration, claims processing and settlement, and reinsurance and risk transfer.

|

Stage |

Key Participants |

|

Product Design & Pricing |

Actuarial teams, IRDAI tariff committees, insurtech pricing analytics firms |

|

Policy Distribution & Sales |

Individual agents, insurance brokers, bancassurance partners, online aggregators, OEM dealers, insurtechs |

|

Underwriting & Risk Assessment |

In-house underwriting teams, telematics data providers, credit bureaus, vehicle database providers |

|

Claims Processing & Settlement |

Surveyors and loss assessors, cashless garage networks, motor claims fraud detection platforms, AI assessment tools |

|

Reinsurance & Risk Transfer |

GIC Re (mandatory cession), international reinsurers, treaty and facultative reinsurance arrangements |

The claims processing and settlement stage is the value chain's most operationally critical phase, directly determining customer retention and brand reputation. The underwriting stage is increasingly differentiated through telematics data integration and AI risk modelling.

Technology Landscape in the India Motor Insurance Industry

AI and Machine Learning in Claims Management

AI-powered image recognition enables automated vehicle damage assessment from photographs submitted via mobile apps, reducing claims cycle time and surveyor dependency. Machine learning models detect anomalous patterns indicative of fraud, enabling significant reductions in fraudulent claim payouts and improving overall combined ratios.

Telematics and Connected Vehicle Technology

OBD-II device and smartphone telematics capture driving behaviour data including speed, braking, and cornering patterns. This data enables risk-proportionate premium pricing in usage-based insurance products, improving underwriting accuracy while creating customer value through safe-driver premium discounts.

Insurtech and API-Driven Distribution Technology

Open insurance APIs enable seamless integration between aggregator platforms, OEM dealer systems, and insurer policy engines. Conversational AI and Gen AI-powered chatbots are simplifying product discovery and purchase for digitally active consumers, accelerating digital distribution channel growth.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Insurance Type |

Own Damage |

52.3% |

2025 |

|

Application |

Private Motor Insurance |

58.4% |

2025 |

|

Distribution Channel |

Online |

32.5% |

2025 |

|

Region |

West India |

28.6% |

2025 |

By Insurance Type

Own Damage insurance leads at 52.3% (2025). The own-damage segment encompasses comprehensive policies covering accidental damage, theft, fire, and natural calamities for both private and commercial vehicles. Rising vehicle values and increased consumer awareness of comprehensive protection support this segment's leading position.

To access detailed market analysis, Request Sample

Third-Party insurance at 47.7% represents the mandatory minimum required under the Motor Vehicles Act. Despite lower premium per policy, the volume of vehicles requiring mandatory third-party coverage creates a large and captive premium base. Third-party premium rates are regulated by IRDAI, limiting pricing flexibility for insurers.

By Application

Private Motor Insurance leads at 58.4% (2025). The private segment encompasses passenger cars, utility vehicles, and two-wheelers for personal use. Strong passenger vehicle sales, dealer-bundled insurance, and rising consumer awareness of comprehensive coverage sustain private motor insurance leadership.

.webp)

Commercial Motor Insurance at 41.6% encompasses goods-carrying vehicles, passenger transport, and construction equipment. Fleet insurance programmes and operator-specific covers serve logistics companies and transport operators. Commercial motor insurance faces higher third-party liability exposure due to elevated vehicle utilization and accident risk.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

West India |

28.6% |

Maharashtra's large passenger vehicle market, Gujarat's commercial vehicle base, and high urbanization generating premium-dense insurance demand. |

|

North India |

26.4% |

Delhi-NCR's high vehicle density, Uttar Pradesh's expanding vehicle fleet, and highway infrastructure expansion increasing commercial vehicle insurance. |

|

South India |

24.8% |

Tamil Nadu's automotive manufacturing hub, Karnataka's tech-driven consumer segment, and strong digital insurance adoption in Bengaluru. |

|

East India |

20.2% |

West Bengal and Odisha's expanding commercial fleet, rising two-wheeler ownership, and increasing infrastructure investment expanding vehicle usage. |

West India's 28.6% market leadership is anchored by Maharashtra, which generates the highest motor premium volume through Mumbai's dense vehicle population, Pune's automotive industry, and high-income consumer preference for comprehensive coverage. North India's 26.4% reflects Delhi-NCR's extreme vehicle density and expanding NCR logistics network.

.webp)

South India's 24.8% is anchored by Tamil Nadu's automotive cluster and Karnataka's technology-driven urban consumer base adopting digital insurance channels. East India at 20.2% represents the market's highest-growth potential region as vehicle ownership penetration expands from a lower base.

Competitive Landscape

The India motor insurance competitive landscape is moderately concentrated, with public sector insurers holding a significant aggregate market position alongside large private carriers. The market is served by 30+ IRDAI-licensed general insurers competing on pricing, digital service, and claims settlement capability.

|

Company Name |

Key Products/Services |

Market Position |

Core Strength |

|

ICICI Lombard General Insurance Company Limited |

Comprehensive, Third-Party, Own Damage, Personal Accident for cars, two-wheelers & CVs |

Market Leader |

Largest private-sector general insurer; 12,000+ cashless garages; AI-driven claims processing; deep OEM partnerships |

|

Bajaj Allianz General Insurance Company |

Comprehensive, Standalone OD, Third Party, Pay-as-you-go, Accident Prime, Eco Assure |

Market Leader |

Second-largest private insurer; Gen AI chatbot; innovative product launches; strong digital and agency channel network |

|

HDFC ERGO General Insurance Company Limited |

Private car insurance, Two-wheeler policies, Commercial vehicle coverage |

Established Player |

Strong bancassurance channel through HDFC Bank; broad product variety; customer-first approach; digital claims capability |

|

TATA AIG General Insurance Company Limited |

Flexible motor plans, Customizable comprehensive coverage, Commercial vehicle insurance |

Established Player |

Flexible product range; hassle-free claims reputation; strong customer service network; Tata group brand trust |

The competitive landscape saw a landmark consolidation in March 2025 when Bajaj Group acquired Allianz SE's 26% shareholding in Bajaj Allianz for INR 24,180 crore, creating the country's largest domestic private insurance company. Private carriers' digital capability investment is expanding even as public sector players scale similar technology capabilities.

.webp)

Key Company Profiles

ICICI Lombard General Insurance Company Limited

ICICI Lombard is India's largest private sector general insurance company, headquartered in Mumbai. The company offers comprehensive motor insurance solutions with industry-leading digital claims processing capabilities and an extensive cashless garage network spanning 12,000+ locations across India.

- Key Products: Comprehensive motor insurance, standalone own damage, third-party liability, and personal accident cover for private cars, two-wheelers, and commercial vehicles.

- Recent Developments: In April 2026, ICICI Lombard General Insurance reported a 7.3% year-on-year increase in Q4 FY26 profit, with profit after tax rising to ₹547 crore from ₹510 crore a year earlier. The growth was supported by strong premium collections from its retail health and motor insurance segments, despite higher claims payouts. The Board also recommended a final dividend of ₹7 per equity share.

- Strategic Focus: AI-enabled claims automation, deepening OEM dealer partnerships, and expanding digital-first customer acquisition for comprehensive motor coverage.

Bajaj Allianz General Insurance Company

Bajaj Allianz General Insurance is headquartered in Pune and is a leading private motor insurer known for innovative product launches and rapid claims turnaround. Following Bajaj Group's acquisition of Allianz SE's 26% stake in March 2025, it became the largest domestic private general insurer in India.

- Key Products: Comprehensive motor insurance, standalone own damage, third-party, pay-as-you-go (UBI), Accident Prime, and Eco Assure Repair Protection add-on.

- Recent Developments: In December 2024, Bajaj Allianz launched Eco Assure Repair Protection and Named Driver Cover add-ons. The company also launched "Insurance Samjho", a Gen AI-powered chatbot to simplify insurance for customers.

- Strategic Focus: Digital innovation, UBI product development, AI-powered customer engagement, and leveraging the Bajaj Finserv distribution ecosystem for deeper market penetration.

Market Concentration Analysis

The India motor insurance market is moderately concentrated at the top tier, with the largest carriers accounting for approximately 40-45% of total motor premium volume. Public sector carriers collectively hold around 35% of the non-life market despite losing share to private players over the past decade.

Market concentration is increasing at the digital distribution platform tier, where online aggregators command a significant and growing share of motor insurance transactions. Consolidation activity, exemplified by the Bajaj-Allianz transaction, is also increasing concentration at the private insurer tier.

Investment & Growth Opportunities

Highest Growth Segments

EV insurance, usage-based insurance and telematics-based products, digital-first insurtechs, and bancassurance-driven comprehensive coverage expansion represent the highest-growth investment vectors through 2034, supported by structural vehicle parc growth, regulatory evolution, and rapid digitalization.

Emerging Investment Opportunities

EV-specific motor insurance product development represents the largest structural growth opportunity through 2030. Insurers that build battery risk pricing expertise, charging infrastructure coverage, and EV manufacturer partnerships early are positioned to capture premium share as EV penetration scales.

Investment Themes

- Telematics and UBI Platform Development: UBI products create premium pricing accuracy that improves combined ratios while attracting safe drivers. Investment in telematics data platforms positions insurers for full commercial rollout as vehicle connectivity expands.

- AI Claims Automation and Fraud Detection: AI claims automation reduces surveyor costs and cycle time while fraud detection AI reduces loss ratios, creating sustainable competitive advantages as the cost and accuracy gap versus traditional processes widens.

Future Market Outlook (2026-2034)

The India motor insurance market is projected to grow from USD 31.92 Billion in 2025 to USD 59.18 Billion by 2034, delivering a 6.84% CAGR over the forecast period. The market anchor value of USD 44.45 Billion in 2030 represents an inflection where digital distribution, UBI, and EV insurance products achieve commercial mainstream adoption.

Three structural forces define India motor insurance growth through 2034: India's expanding vehicle parc driven by rising per-capita income and accessible financing; IRDAI's progressive digitalization reforms enabling new distribution channels and product innovations; and the EV transition creating specialized insurance demand. These forces support sustained above-GDP premium growth through the forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders including Chief Underwriting Officers, Digital Distribution Heads, Claims Management Directors, IRDAI-licensed insurance brokers, and regional motor insurance market specialists across India.

Secondary Research

Secondary research encompassed IRDAI annual reports and regulatory circulars, General Insurance Council premium data, motor vehicle registration statistics, company annual reports, and insurtech industry publications. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a segment bottom-up model incorporating vehicle registration data by category, average premium per vehicle by coverage type, IRDAI-regulated premium rate adjustments, and distribution channel growth projections calibrated to 2020-2025 historical data.

India Motor Insurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Insurance Types Covered | Own Damage, Third Party |

| Applications Covered | Commercial Motor Insurance, Private Motor Insurance |

| Distribution Channels Covered | Individual Agents, Brokers, Banks, Online, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | ICICI Lombard General Insurance Company Limited, Bajaj Allianz General Insurance Company, HDFC ERGO General Insurance Company Limited, TATA AIG General Insurance Company Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India motor insurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India motor insurance market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India motor insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Motor Insurance Market Report

The India motor insurance market reached USD 31.92 Billion in 2025. Rising vehicle ownership, mandatory third-party regulations, and increasing adoption of comprehensive coverage are primary drivers. Digitalization and insurtech innovations are further accelerating growth.

The market grows at a CAGR of 6.84% during 2026-2034, reaching USD 59.18 Billion by 2034. EV insurance and usage-based insurance products represent the fastest-growing sub-segments within this growth trajectory.

Own Damage insurance leads at 52.3% through rising consumer preference for comprehensive protection, increasing vehicle values, and growing awareness of financial risk beyond mandatory third-party requirements.

Private Motor Insurance leads at 58.4% through structural expansion of India's passenger vehicle market, dealer-bundled insurance at point of sale, and rising middle-class income driving comprehensive coverage adoption.

West India leads at 28.6% through Maharashtra's large passenger vehicle market, Mumbai's high vehicle density, and Gujarat's commercial vehicle base generating high insurance premium volumes.

Leading companies include ICICI Lombard General Insurance Company Limited, Bajaj Allianz General Insurance Company, HDFC ERGO General Insurance Company Limited, and TATA AIG General Insurance Company Limited, among others.

The market is projected to reach approximately USD 44.45 Billion by 2030, with usage-based insurance achieving commercial mainstream, EV-specific insurance reaching material premium volumes, and digital-first distribution commanding the majority of renewal policy transactions across India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)