India Mutual Funds Market Size, Share, Trends and Forecast by Asset Class/Scheme Type, Source of Funds, and Region, 2026-2034

India Mutual Funds Market Size, Share, Trends & Forecast (2026-2034)

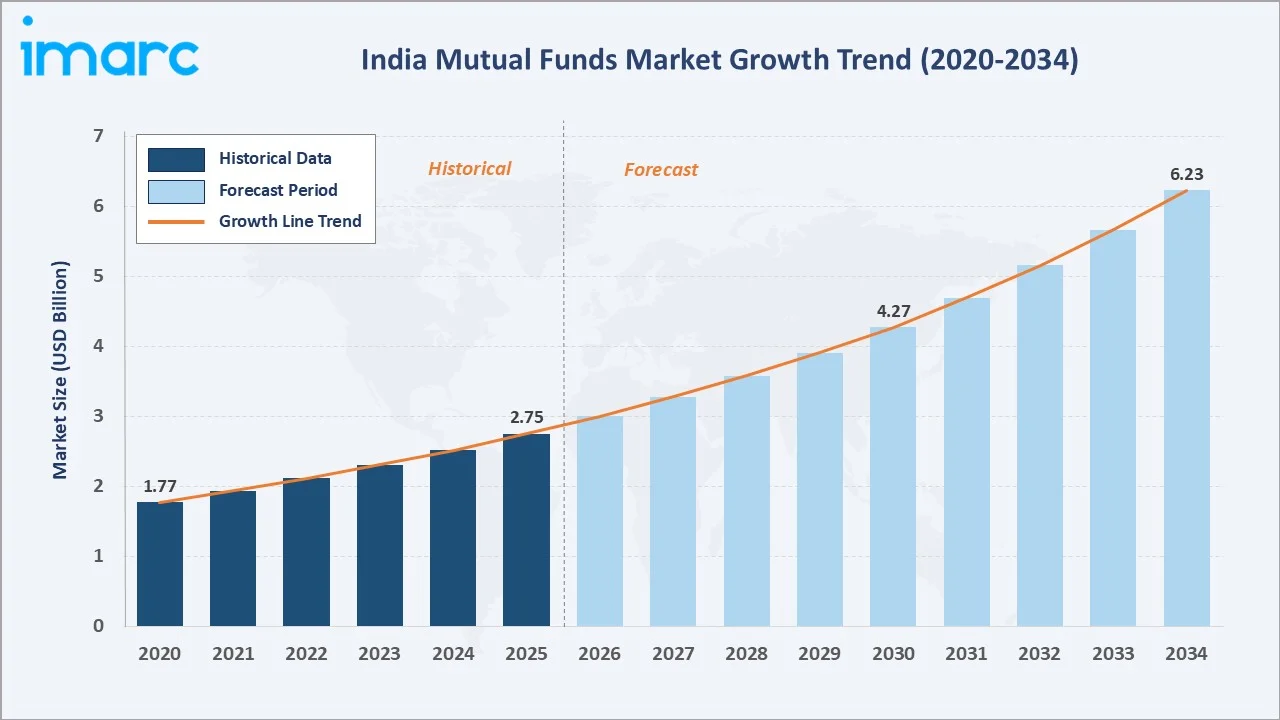

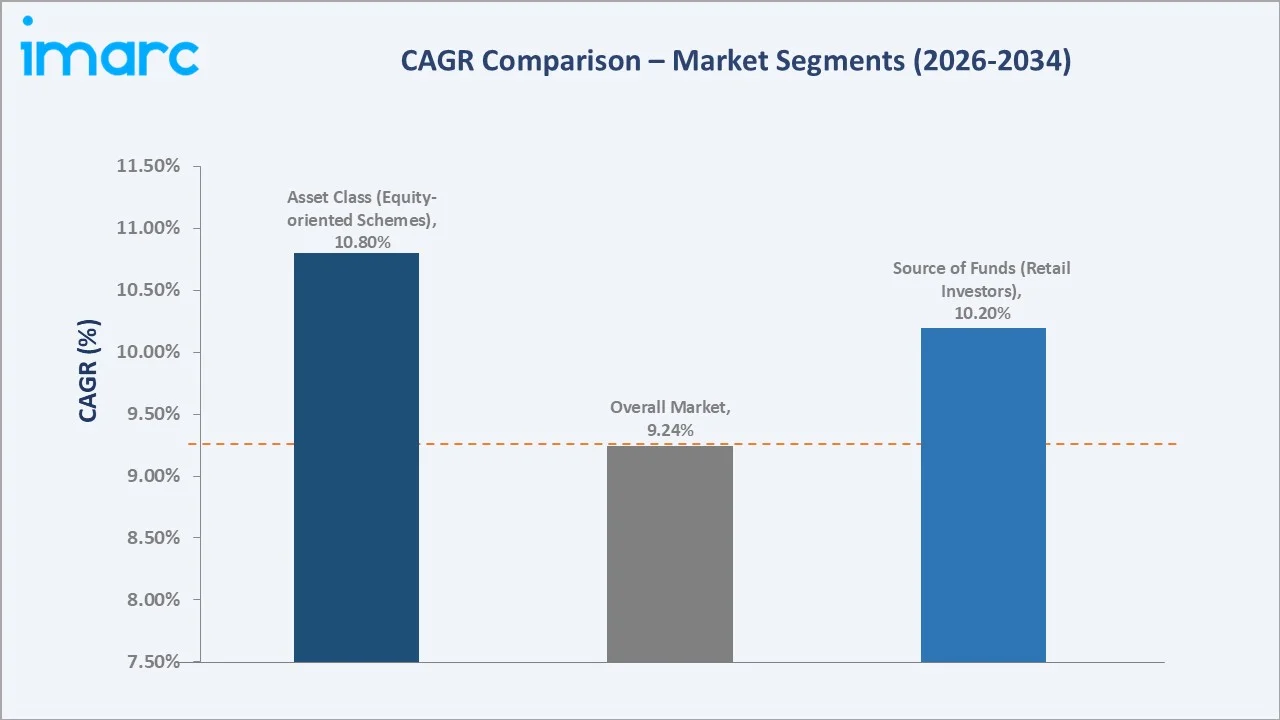

The India mutual funds market reached USD 2.75 Billion in 2025 and is projected to reach USD 6.23 Billion by 2034, growing at a CAGR of 9.24% during 2026-2034. Rising financial literacy, surging Systematic Investment Plan (SIP) inflows, deepening retail participation in B30 cities, accelerated digital and fintech onboarding, and supportive SEBI reforms are the principal forces shaping market trajectory across equity, debt, hybrid, and passive segments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.75 Billion |

|

Forecast Market Size (2034) |

USD 6.23 Billion |

|

CAGR (2026-2034) |

9.24% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (34.2% share, 2025) |

|

Fastest Growing Region |

North India |

West India dominates the market with a 34.2% share in 2025, anchored by Mumbai, the financial capital and the headquarters of nearly all major Asset Management Companies (AMCs). Equity-oriented schemes lead at 42.6% of total Assets Under Management (AUM), supported by sustained SIP inflows that crossed INR 29,361 crore in September 2025, up from INR 28,265 crore in August 2025.

To get more information on this market, Request Sample

Retail investors are the largest source of funds at 38.5%, reflecting a structural shift away from traditional savings instruments toward market-linked, professionally managed investment products.

With over 9.25 crore contributing SIP accounts, while SIP assets under management (AUM) climbed to INR 15.52 lakh crore, and B30 (beyond top 30) cities contributing 19.1% of industry assets, India’s mutual fund industry is on a structural growth trajectory underpinned by demographic dividend, financialization of household savings, and regulatory rationalization of expense ratios.

Executive Summary

India’s mutual funds industry is experiencing a sustained boom, propelled by rising household financialization, a rapidly expanding retail investor base, and the structural shift of savings toward equity markets. The market reached USD 2.75 Billion in 2025 and is projected to reach USD 6.23 Billion by 2034, driven by deepening SIP penetration, fintech-led onboarding, and product innovation across actively and passively managed strategies.

West India leads regionally with a 34.2% share in 2025, followed by North India at 27.6%, reflecting Mumbai’s dominance in fund management and the strength of the Delhi NCR investor base. Equity-oriented schemes dominate the asset class segmentation at 42.6%, while retail investors represent 38.5% of all sourced funds.

Key activities in 2025 included AMFI’s ‘Chhoti SIP, Tarun Yojana, and MITRA’ launched in February 2025 to expand small-ticket SIP participation, HDFC Bank’s ‘SmartWealth’ digital platform, SEBI’s March 2025 social media advertising guidelines for registered intermediaries, and the December 2025 SEBI (Mutual Funds) Regulations 2026, lowering base expense ratios across categories.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Asset Class/Scheme Type) |

Equity-oriented Schemes – 42.6% (2025) |

|

Largest Segment (Source of Funds) |

Retail Investors – 38.5% (2025) |

|

Leading Region |

West India – 34.2% share (2025) |

|

Fastest Growing Region |

North India (B30 SIP expansion) |

|

Top Companies |

State Bank of India, ICICI Bank, HDFC Bank Ltd., Nippon India Mutual Fund, and Kotak Mahindra Bank Limited |

Key Analytical Observations Supporting the Above Data:

- Equity-oriented schemes account for 42.6% of the Indian mutual funds market in 2025, supported by sustained SIP inflows and a 55-month streak of net positive equity inflows.

- Retail investors lead the source of funds segmentation at 38.5% (2025), driven by 9.25 crore active SIP accounts and rising participation in tier-2 and tier-3 cities.

- West India holds 34.2% of the total market in 2025, anchored by Mumbai’s status as India’s financial capital and home to most major AMCs.

- Industry AUM-to-bank-deposits ratio rose from 19.7% in March 2020 to 28.7% by March 2025, evidencing the structural shift in household savings allocation.

- Top 5 fund houses managed 56% of total industry assets in 2025, with SBI Mutual Fund holding the largest share at INR 12.77 lakh crore in QAAUM.

India Mutual Funds Market Overview

A mutual fund is a professionally managed investment vehicle that pools capital from multiple investors to acquire a diversified portfolio of securities, including equities, fixed income, money market instruments, and exchange-traded products.

India’s mutual fund industry is regulated by the Securities and Exchange Board of India (SEBI) under the SEBI (Mutual Funds) Regulations, 1996, and is supported by the Association of Mutual Funds in India (AMFI) as the apex industry body. As of September 2025, the industry comprises 54 registered mutual funds offering over 1,500 schemes across equity, debt, hybrid, solution-oriented, and passive categories.

Drivers include rising incomes, a young demographic, smartphone penetration, and weak FD real returns. QAAUM reached INR 77.1 trillion (Sept 2025), a six-year CAGR of 18.4%, making the industry the fastest-growing segment of household savings.

Market Dynamics

To evaluate market opportunities, Request Sample

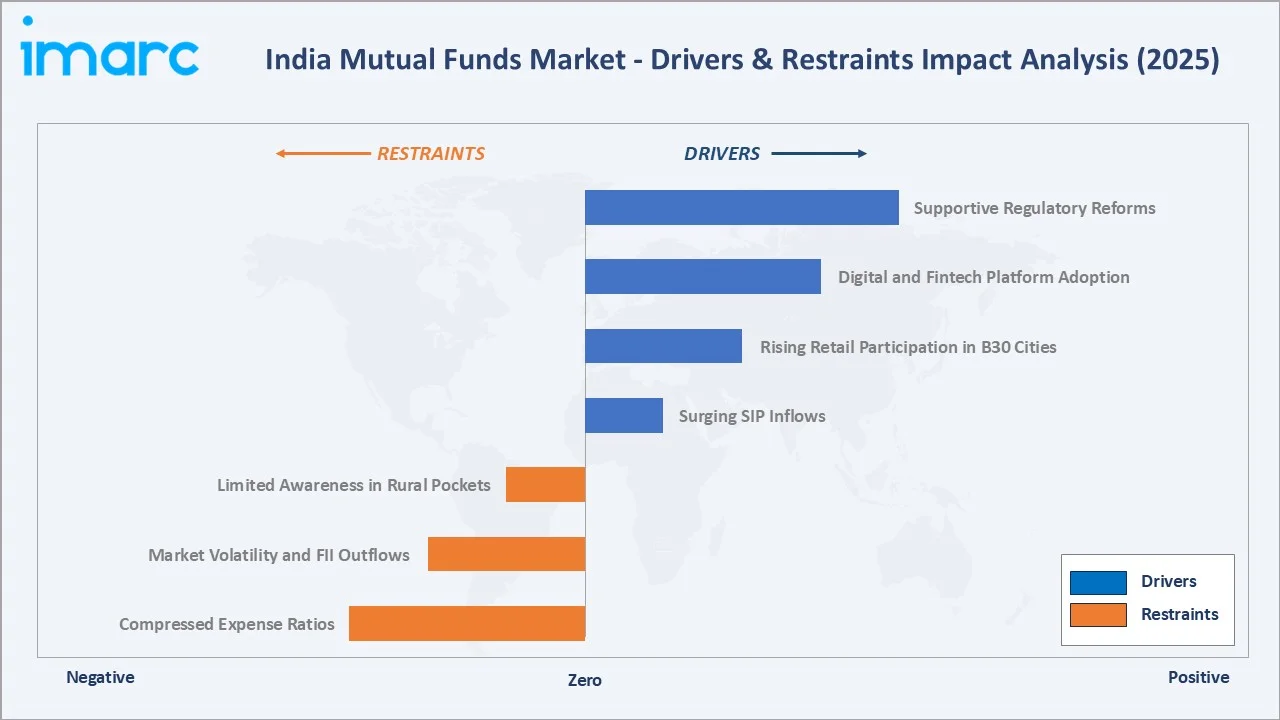

Market Drivers

- Surging SIP Inflows: Monthly SIP contributions reached an all-time high of INR 29,361 crore in September 2025, with 9.25 crore active SIP accounts, reflecting deeply entrenched, disciplined retail investing behavior.

- Rising Retail Participation in B30 Cities: B30 locations now contribute 19% of total AUM and account for INR 15.35 lakh crore, evidencing the geographical broadening of investor participation.

- Digital and Fintech Platform Adoption: Platforms such as Groww, Zerodha Coin, and ET Money, complemented by AMC-led offerings such as HDFC Bank’s SmartWealth, are simplifying onboarding, KYC, and portfolio management for first-time investors across geographies.

- Supportive Regulatory Reforms: SEBI’s March 2025 advertising guidelines, December 2025 SEBI (Mutual Funds) Regulations 2026, and AMFI’s Chhoti SIP initiative collectively enhance transparency, reduce fraud risk, and broaden financial inclusion across underserved segments.

Market Restraints

- Compressed Expense Ratios: SEBI’s mutual fund regulations 2026 (effective April 2026) lower base expense ratios across select categories, unbundle statutory levies, and rationalize brokerage limits, putting pressure on AMC profit margins, particularly for smaller and mid-sized players.

- Market Volatility and FII Outflows: The past two financial years recorded the highest number of premature SIP terminations, with 1.90 crore in FY24 rising sharply to 4.82 crore in FY25.

- Limited Awareness in Rural Pockets: Despite B30 expansion, mutual fund penetration in tier-3 and tier-4 towns remains shallow, with the top 30 cities still accounting for over 80% of total AUM, constraining incremental retail inflows from deeper rural markets.

Market Opportunities

- Passive Investing Expansion: Passive fund AUM surged sixfold from INR 1.91 lakh crore in 2019 to INR 12.2 lakh crore in 2025, with 68% of retail investors now holding at least one passive fund in 2025, opening substantial product innovation opportunities for index, smart-beta, and thematic ETFs.

- Women-Centric Schemes: SEBI’s incentive framework for women investors, designed to enhance gender-balanced participation, complements the AMFI Chhoti SIP initiative launched in February 2025 and creates a high-priority customer acquisition channel.

- GIFT City and Offshore Products: IndusInd International Holdings and Invesco completed a joint sponsor arrangement for Invesco Mutual Fund in November 2025, illustrating the growing appetite for cross-border and offshore-linked product structures targeting NRI and high-net-worth investors.

Market Challenges

- Data Sharing Restrictions: AMFI’s September 2025 directive to MF Central halting direct investor data sharing with third-party apps, pending consent and security clarifications, has reset integration pathways and constrained certain fintech-led aggregation models.

- Compliance Cost Pressure: Continuous tightening of disclosure, advertising, and stewardship norms by SEBI is increasing operating costs for AMCs, particularly during a period of compressing expense ratios and rising distributor commissions for B30 and women investors.

Emerging Market Trends

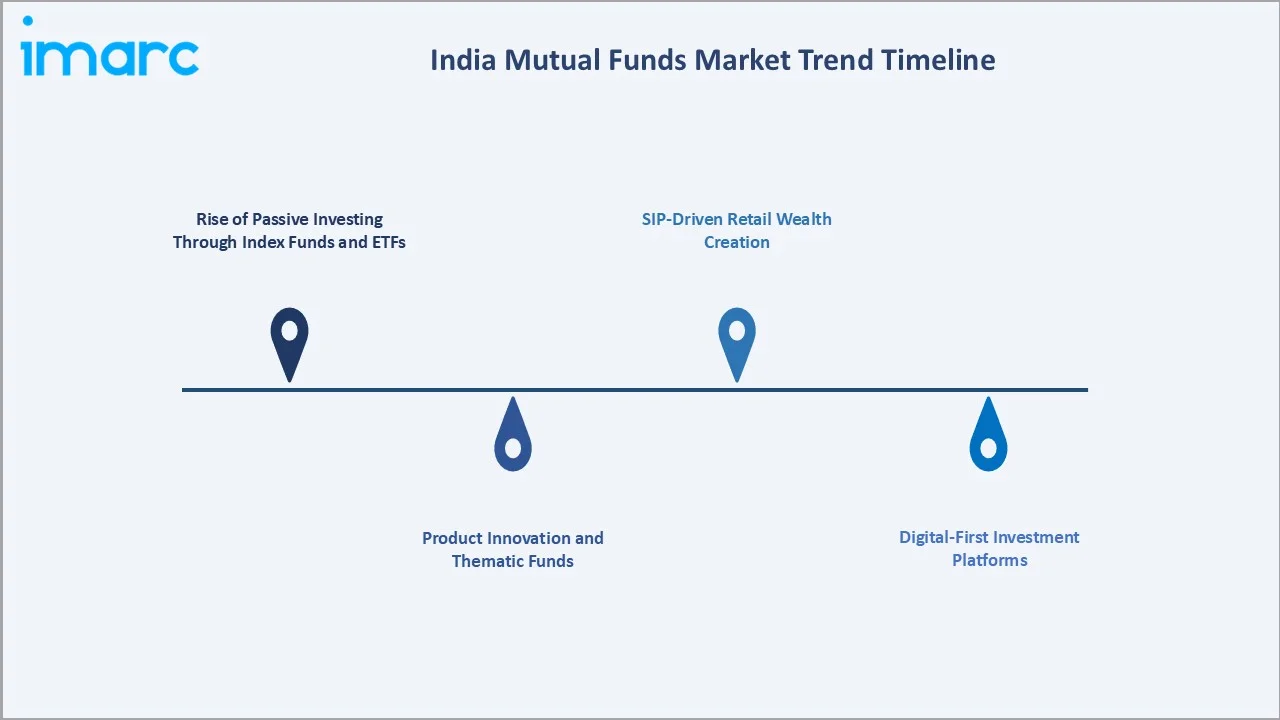

1. Rise of Passive Investing Through Index Funds and ETFs

Passive baskets are expanding rapidly as cost-conscious investors and institutional allocators recognize the underperformance of many actively managed funds against benchmark indices. Passive fund AUM grew sixfold from INR 1.91 lakh crore in 2019 to INR 12.2 lakh crore by 2025, with 68% of retail investors now holding at least one passive product.

2. SIP-Driven Retail Wealth Creation

Systematic Investment Plans have become the cornerstone of retail participation. Monthly SIP contributions reached a record INR 29,361 crore in September 2025, with active SIP accounts crossing 9.25 crore. AMFI’s ‘Chhoti SIP, Tarun Yojana, and Mitra’ initiative, launched on February 21, 2025, encourages young, first-time investors to participate in small-ticket SIPs, expanding the investor base in the 18–30 age cohort and tier-2 and tier-3 cities.

3. Digital-First Investment Platforms

Fintech platforms and AMC-led digital offerings are democratizing wealth management. HDFC Bank introduced its ‘SmartWealth’ digital investment platform in June 2024, offering a unified suite of mutual funds, fixed deposits, and insurance with personalized recommendations. Pure-play platforms such as Groww and Zerodha Coin have onboarded over 5 crore users collectively, of which a significant share are first-time investors transacting via UPI mandates and standardized digital KYC.

4. Product Innovation and Thematic Funds

AMCs are launching differentiated equity exposures targeting structural themes. Nippon India Mutual Fund launched the Nippon India Active Momentum Fund (February 2025), an open-ended scheme employing a multifactor quantitative approach. Invesco rolled out the Invesco India Consumption Fund in October 2025, while BlackRock has signalled plans for an active India ETF, reflecting deepening product breadth across factor, thematic, and sector strategies.

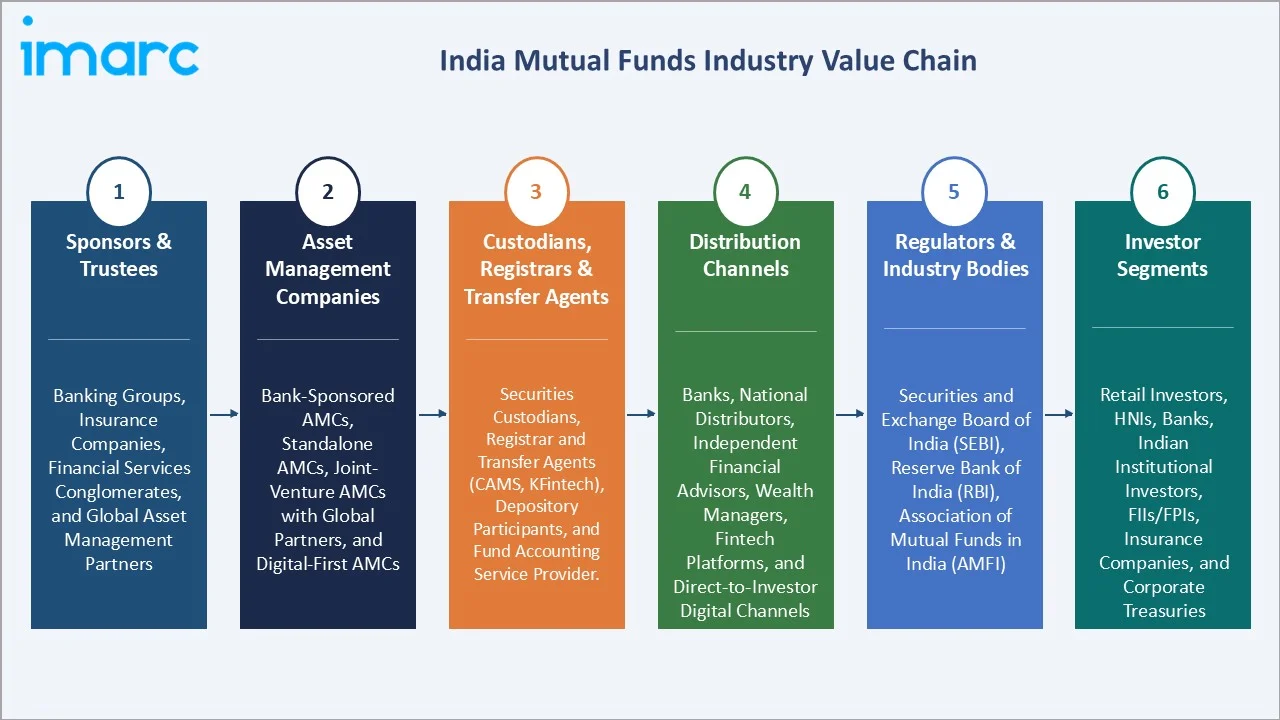

Industry Value Chain Analysis

The India mutual funds industry value chain spans capital provision, fund management, custody and administration, distribution, regulation, and end-investor servicing. Each stage is anchored by specialized institutional participants whose interactions determine product flow, cost structure, and investor experience across the lifecycle.

|

Stage |

Key Players / Examples |

|

Sponsors & Trustees |

Banking groups, insurance companies, financial services conglomerates, and global asset management partners |

|

Asset Management Companies |

Bank-sponsored AMCs, standalone AMCs, joint-venture AMCs with global partners, and digital-first AMCs |

|

Custodians, Registrars & Transfer Agents |

Securities custodians, registrar and transfer agents (CAMS, KFintech), depository participants, and fund accounting service providers |

|

Distribution Channels |

Banks, national distributors, independent financial advisors, wealth managers, fintech platforms, and direct-to-investor digital channels |

|

Regulators & Industry Bodies |

Securities and Exchange Board of India (SEBI), Reserve Bank of India (RBI), Association of Mutual Funds in India (AMFI) |

|

Investor Segments |

Retail investors, HNIs, banks, Indian institutional investors, FIIs/FPIs, insurance companies, and corporate treasuries |

Technology Landscape in the India Mutual Funds Industry

Digital KYC and UPI-Linked SIPs

Aadhaar eKYC, video KYC, and UPI mandates have reduced onboarding from days to minutes, while UPI Autopay-linked SIPs streamline recurring investments and reduce mandate failures.

AI-Driven Personalization

AMCs and fintech platforms deploy ML models for goal-based recommendations, risk profiling, and behavioral nudges. HDFC SmartWealth and similar tools curate scheme baskets dynamically.

Blockchain-Based Registries

CAMS and KFintech, the two RTAs handling industry transactions, are piloting distributed ledger systems for reconciliation and consent-led data sharing under AMFI's September 2025 MF Central directive.

Robo-Advisory and Goal-Based Tools

Platforms such as Scripbox, Kuvera, and INDmoney offer algorithm-driven, goal-based advisory with automated rebalancing and tax-loss harvesting, expanding access to professional-grade advice.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

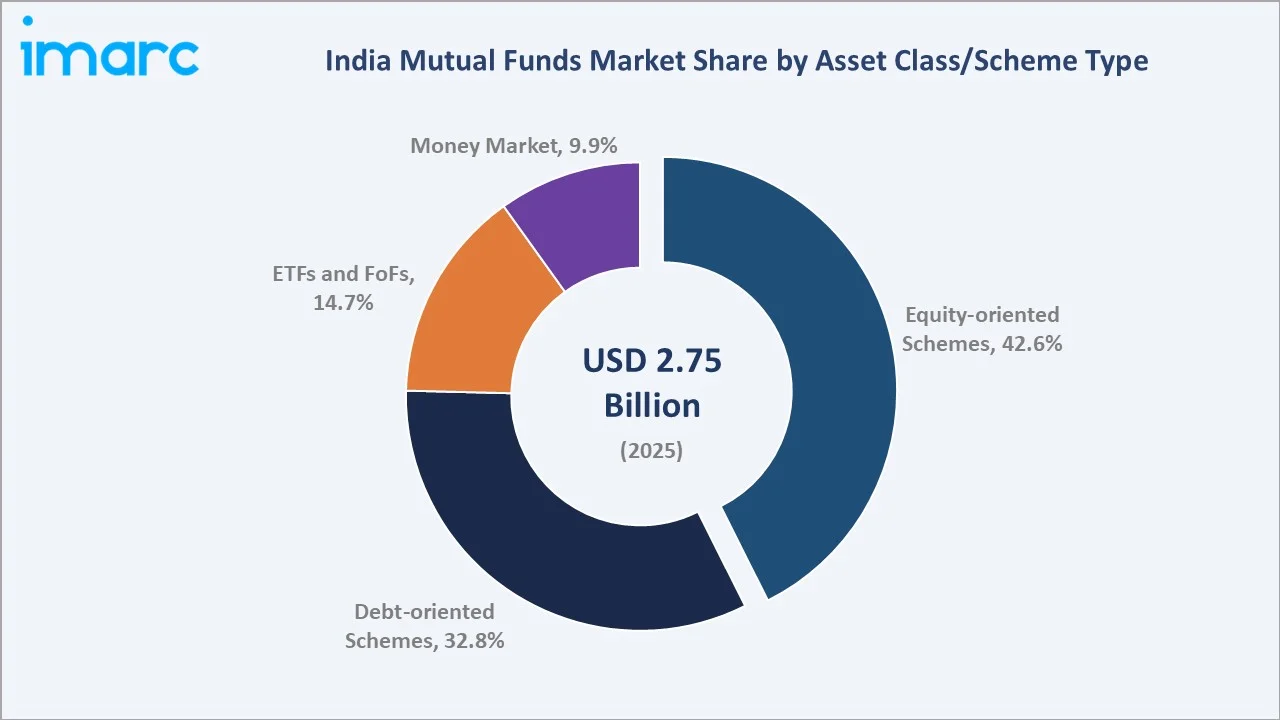

| Asset Class/Scheme Type | Equity-oriented Schemes | 42.6% | 2025 |

| Source of Funds | Retail Investors | 38.5% | 2025 |

| Region | West India | 34.2% | 2025 |

By Asset Class/Scheme Type

Equity-oriented schemes lead the asset class segment with a 42.6% share in 2025. Their dominance reflects sustained SIP-led inflows, a 55-month consecutive streak of net positive equity flows, and rising investor preference for long-term capital appreciation amid a maturing equity market.

To access detailed market analysis, Request Sample

Debt-oriented schemes hold 32.8%, benefiting from heightened interest rate volatility that pushed allocators toward stable coupon income and duration strategies. ETFs and FoFs account for 14.7%, driven by accelerating passive investing adoption. While money market schemes hold 9.9%, favored by treasuries and corporates for short-term liquidity management.

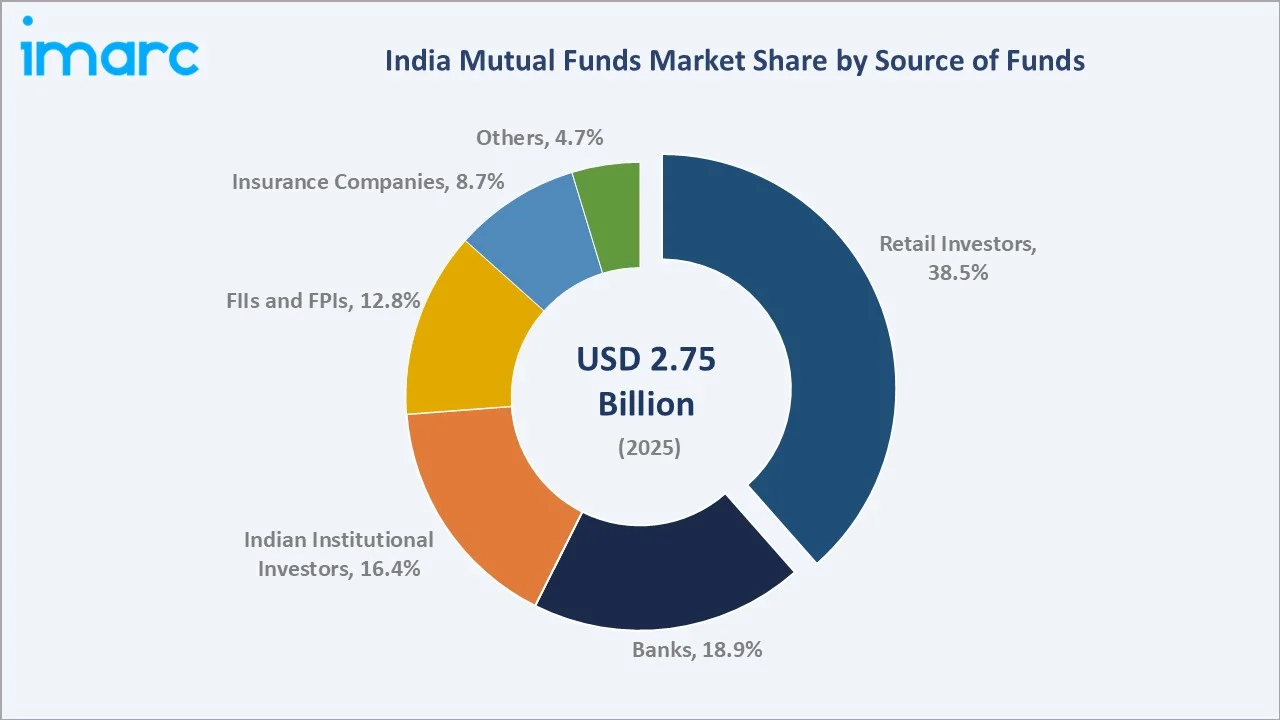

By Source of Funds

Retail investors lead the source of funds segment at 38.5% of the India mutual funds market in 2025, evidencing the structural shift in household financial asset allocation. The share of individual investors (retail and HNI) in total industry AUM rose to 60.9% as of September 2025, supported by 9.25 crore active SIP accounts and aggressive distributor outreach in B30 cities.

Banks contribute 18.9%, primarily through treasury allocations and bank-sponsored AMC distribution. Indian institutional investors account for 16.4%, FIIs and FPIs hold 12.8% tied to equity and debt market exposure, insurance companies represent 8.7% primarily via debt and hybrid mandates, while others contribute the residual 4.7% covering trusts, NRIs, and corporate treasuries.

Regional Market Insights

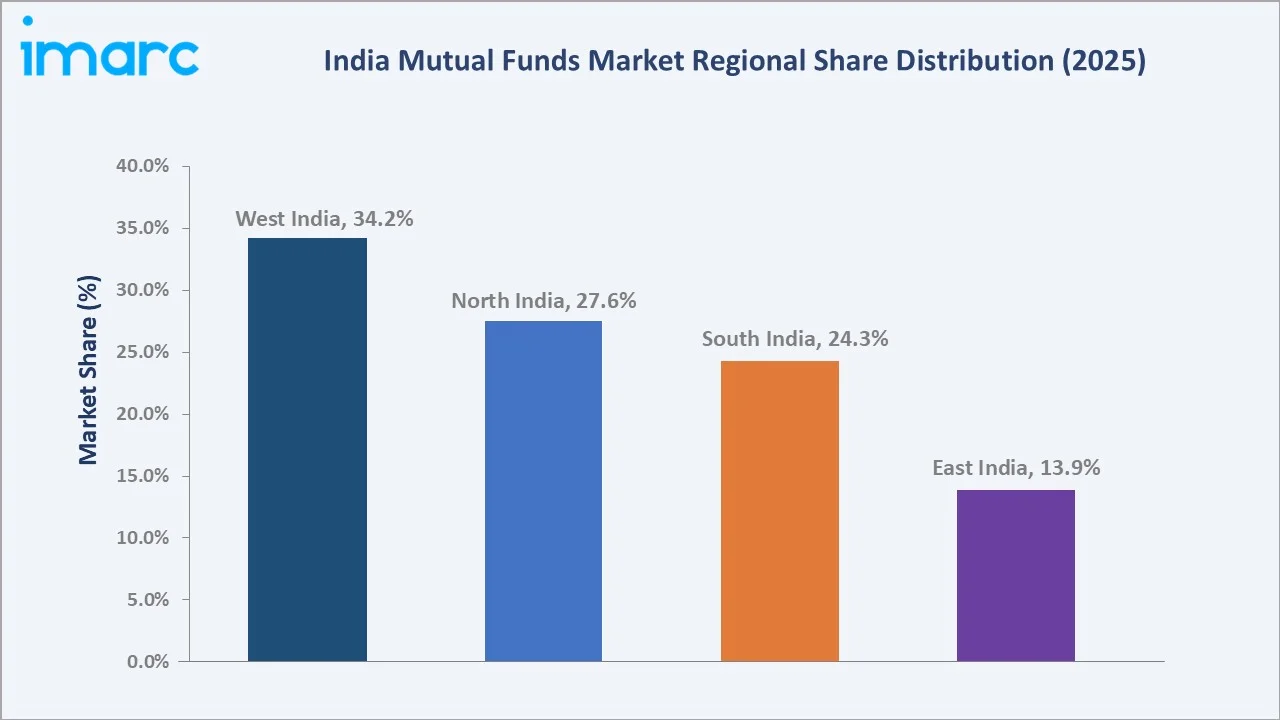

West India leads with a 34.2% share in 2025, anchored by Mumbai, India’s financial capital and the headquarters of all major AMCs, including SBI Mutual Fund, HDFC Mutual Fund, Nippon India Mutual Fund, Kotak Mahindra Mutual Fund, and Aditya Birla Sun Life Mutual Fund. Maharashtra and Gujarat alone account for the bulk of industry AUM, driven by deep institutional participation, high HNI density, and a mature distributor ecosystem.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

34.2% |

Financial capital with the highest concentration of AMC headquarters, deepest institutional and HNI investor base, mature distributor ecosystem, and regulatory infrastructure |

|

North India |

27.6% |

Affluent, digitally engaged retail investor base; rising B30 city participation; growing SIP penetration in tier-2 urban centers |

|

South India |

24.3% |

IT-services-led HNI households; strong fintech ecosystem driving digital onboarding; deep tier-2 retail penetration |

|

East India |

13.9% |

Emerging regional market with growing B30 city participation; digital-first onboarding accelerating SIP additions and retail inflows |

North India follows at 27.6%, driven by Delhi NCR, Punjab, Haryana, and Uttar Pradesh. The Delhi NCR investor base is among the most affluent and digitally engaged, while smaller cities such as Lucknow, Chandigarh, and Jaipur are emerging B30 growth centers backed by rising SIP registrations.

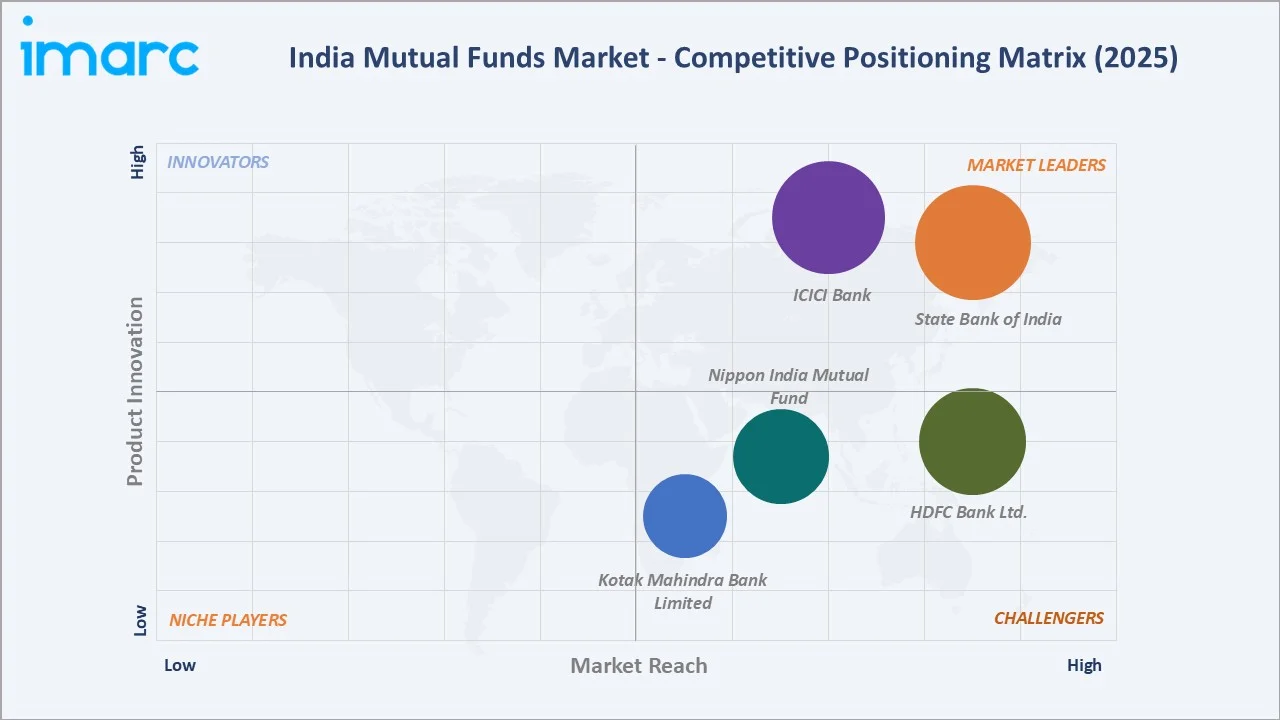

Competitive Landscape

The India mutual funds market exhibits a moderately concentrated structure. The top 5 AMCs (State Bank of India, ICICI Bank, HDFC Bank Ltd., Nippon India Mutual Fund, and Kotak Mahindra Bank Limited) collectively manage approximately 56% of total industry assets in 2025.

|

Company |

Brand / Platform/Programs |

Market Position |

Core Strength |

|

State Bank of India |

SBI MUTUAL FUND |

Market Leader |

Equity, debt, hybrid, ETF, and ELSS schemes via 22,000+ SBI branches |

|

ICICI Bank |

ICICI Prudential Mutual Fund |

Market Leader |

One of the largest active MF AMC by QAAUM; bluechip, balanced advantage, multi-asset, gilt, retirement schemes |

|

HDFC Bank Ltd. |

HDFC Mutual Fund |

Strong Challenger |

Flexi cap, mid-cap opportunities, balanced advantage, top 100, gold funds |

|

Nippon India Mutual Fund |

Nippon India Mutual Fund (NIMF) |

Strong Challenger |

21M+ retail folios; small cap, multi-cap, momentum, ETFs (largest passive franchise) |

|

Kotak Mahindra Bank Limited |

Kotak Mahindra Mutual Fund |

Challenger |

QAAUM of INR 5.73 lakh crore; bluechip, equity arbitrage, debt hybrid, PMS |

Bank-sponsored AMCs benefit from captive distribution networks, while standalone players such as Mirae Asset and Tata Mutual Fund compete on innovative product design, performance consistency, and digital reach. Strategic alliances, fund-of-funds offerings, and GIFT City presence are emerging as differentiation levers in a market with compressing expense ratios.

Key Company Profiles

State Bank of India

State Bank of India’s SBI Mutual Fund is a joint venture between State Bank of India and AMUNDI of France. It is India’s largest AMC with a QAAUM of INR 12.5 lakh crore as of December 2025, supported by SBI’s nationwide branch network of over 22,000 branches.

- Product Portfolio: Equity, debt, hybrid, ETFs, fund of funds, solution-oriented, and ELSS schemes.

- Recent Developments: In March 2026, India’s largest asset manager, SBI Funds Management Ltd., prepared to file draft IPO papers with SEBI for a major public listing, expected to be entirely an offer-for-sale by promoters State Bank of India and Amundi, meaning no fresh capital will be raised.

- Strategic Focus: Branch-led B30 expansion, retirement and life-stage solutions, ETF capability scale-up.

ICICI Bank

ICICI Bank’s ICICI Prudential Mutual Fund is a JV between ICICI Bank and Prudential Plc (UK). It is India’s second-largest AMC with a QAAUM of INR 10.76 lakh crore as of December 2025. The company is recognized for its disciplined process orientation across equity and debt categories.

- Product Portfolio: Bluechip, balanced advantage, multi-asset, gilt, retirement, and child care plans; growing PMS franchise.

- Recent Developments: In April 2026, ICICI Prudential Mutual Fund reduced the minimum investment thresholds in select schemes, significantly lowering entry barriers for investors, with changes effective May 2026.

- Strategic Focus: Hybrid solutions for first-time investors; deepening direct-channel digital engagement.

HDFC Bank Ltd.

HDFC Bank Ltd.’s HDFC Mutual Fund is India’s third-largest AMC with a QAAUM of INR 9.25 lakh crore as of December 2025, is publicly listed, and recognized for its strong active equity franchise and consistent fund manager continuity.

- Product Portfolio: Flexi cap, mid-cap opportunities, balanced advantage, top 100, gold, and small-cap funds.

- Recent Developments: In May 2026, HDFC Mutual Fund capped SIP investments in the HDFC Defence Fund at INR 25,000 per investor and allowed fresh STP subscriptions only on a monthly basis with the same INR 25,000 limit, effective May 4, 2026.

- Strategic Focus: Equity-led wealth creation; bank-channel synergies; passive product expansion.

Market Concentration Analysis

The India mutual funds market is moderately concentrated. The top 5 fund houses (State Bank of India, ICICI Bank, HDFC Bank Ltd., Nippon India Mutual Fund, and Kotak Mahindra Bank Limited) collectively manage 56% of total industry assets in 2025, while the top 10 (adding Aditya Birla Sun Life, UTI, Axis, Tata, and Mirae Asset Mutual Funds) command nearly 80%.

The remaining share is held by 39 mid-sized and emerging players, with 19 AMCs managing assets above INR 1,00,000 crore. Mid-tier players, including Mirae Asset and Tata Mutual Fund, are gaining share through equity outperformance and innovative product launches, while emerging entrants such as Bandhan, Helios, and Groww Mutual Fund are reshaping the digital-first competitive frontier.

Investment & Growth Opportunities

Fastest Growing Segments

Passive funds (estimated CAGR ~14%), thematic and sectoral equity funds (~12%), and SIP-led equity flows (SIP AUM CAGR of 25–27% expected over FY25–FY30) represent the highest-growth investment vectors through 2034. Passive fund AUM is projected to scale from INR 12.2 lakh crore in 2025 to over INR 35 lakh crore by 2030, supported by lower expense ratios under SEBI 2026 Regulations. Hybrid and multi-asset allocation funds are also gaining share among first-time and conservative investors as a balanced entry point into market-linked investing.

Emerging Market Expansion

B30 cities now contribute over 19% of total AUM, representing 58% of all incremental SIP additions. Tier-2 and tier-3 city expansion through fintech-led, hyperlocal distribution, vernacular investor education content, and the AMFI Chhoti SIP, Tarun Yojana, and Mitra initiative (February 2025) targeting young first-time investors collectively define the most material long-term opportunity. Women-focused product offerings aligned with SEBI's incentive framework, and GIFT City and offshore mandates targeting NRI investors and global allocators, further extend the addressable market.

Venture and Institutional Investment Trends

Strategic capital is flowing through cross-border alliances. IndusInd International Holdings and Invesco completed a joint sponsor arrangement for Invesco MF (November 2025), while BlackRock has signalled plans for an active India ETF. Consolidation is accelerating with 19 fund houses managing INR 1 lakh crore+, and digital-first entrants like Bandhan, Helios, and Groww MF are reshaping the competitive frontier.

Future Market Outlook (2026-2034)

India’s mutual funds market is positioned for sustained, broad-based growth through 2034. From a base of USD 2.75 Billion in 2025, the market is projected to reach USD 6.23 Billion by 2034, growing at a CAGR of 9.24%.

Three structural macro-themes will shape the trajectory: deepening household financialization with mutual fund AUM rising as a share of bank deposits; geographic broadening into B30 and emerging tier-3 cities; and product diversification into passive, thematic, and offshore-linked schemes. AMCs that combine digital-first onboarding, distribution scale, and disciplined active management will be best positioned to capture share in a market that is rapidly maturing into a genuine alternative to traditional savings instruments.

Research Methodology

Primary Research

Primary research comprised interviews with 130+ industry participants in 2024–2025, including AMC executives, RTAs, distributors, fintech platforms, SEBI-registered advisers, and end investors across all four Indian regions.

Secondary Research

Secondary research included AMFI factbooks, SEBI circulars, RBI Financial Stability Reports, CRISIL Intelligence and ICICI Pru AMC studies, AMC annual reports, and trade publications. Over 220 sources were triangulated.

Forecasting Models

A hybrid top-down and bottom-up approach combines household savings projections, SIP trajectories, AUM-to-GDP ratios, and AMC asset growth pipelines. The base-case 9.24% CAGR reflects consensus across regulatory milestones and observed flows.

India Mutual Funds Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Asset Classes/Scheme Types Covered | Debt-oriented Schemes, Equity-oriented Schemes, Money Market, ETFs, FoFs |

| Source of Funds Covered | Banks, Insurance Companies, Retail Investors, Indian Institutional Investors, FIIs and FPIs, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | State Bank of India, ICICI Bank, HDFC Bank Ltd., Nippon India Mutual Fund, Kotak Mahindra Bank Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India mutual funds market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India mutual funds market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India mutual funds industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Mutual Funds Market Report

The India mutual funds market reached USD 2.75 Billion in 2025 and is projected to reach USD 6.23 Billion by 2034.

The market is expected to grow at a CAGR of 9.24% during the forecast period 2026-2034, supported by surging SIP inflows, rising retail participation, and digital platform adoption.

West India leads with a 34.2% share in 2025, anchored by Mumbai’s status as India’s financial capital and the location of all major AMC headquarters.

Equity-oriented schemes dominate the asset class segment at 42.6% in 2025, supported by sustained SIP inflows, strong long-term performance, and rising investor preference for capital appreciation.

Retail investors lead the source of funds segment at 38.5% in 2025, driven by 9.25 crore active SIP accounts and deepening participation across B30 cities.

Key players include State Bank of India, ICICI Bank, HDFC Bank Ltd., Nippon India Mutual Fund, and Kotak Mahindra Bank Limited.

Digital KYC, UPI-linked SIPs, and platforms such as HDFC SmartWealth, Groww, and Zerodha Coin have accelerated retail onboarding, reduced mandate failure rates, and democratized access to mutual fund investing across geographies.

Key challenges include compressed expense ratios under SEBI 2026 Regulations, episodic FII outflows, premature SIP terminations during volatile cycles, and limited deep-rural awareness despite B30 growth.

Major opportunities lie in passive funds, thematic and sectoral equity strategies, women-focused offerings, GIFT City offshore products, and B30 fintech-led distribution targeting first-time investors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)