India Olive Oil Market Size, Share, Trends and Forecast by Type, Distribution Channel, Application, and Region, 2026-2034

India Olive Oil Market Size, Share, Trends & Forecast (2026-2034)

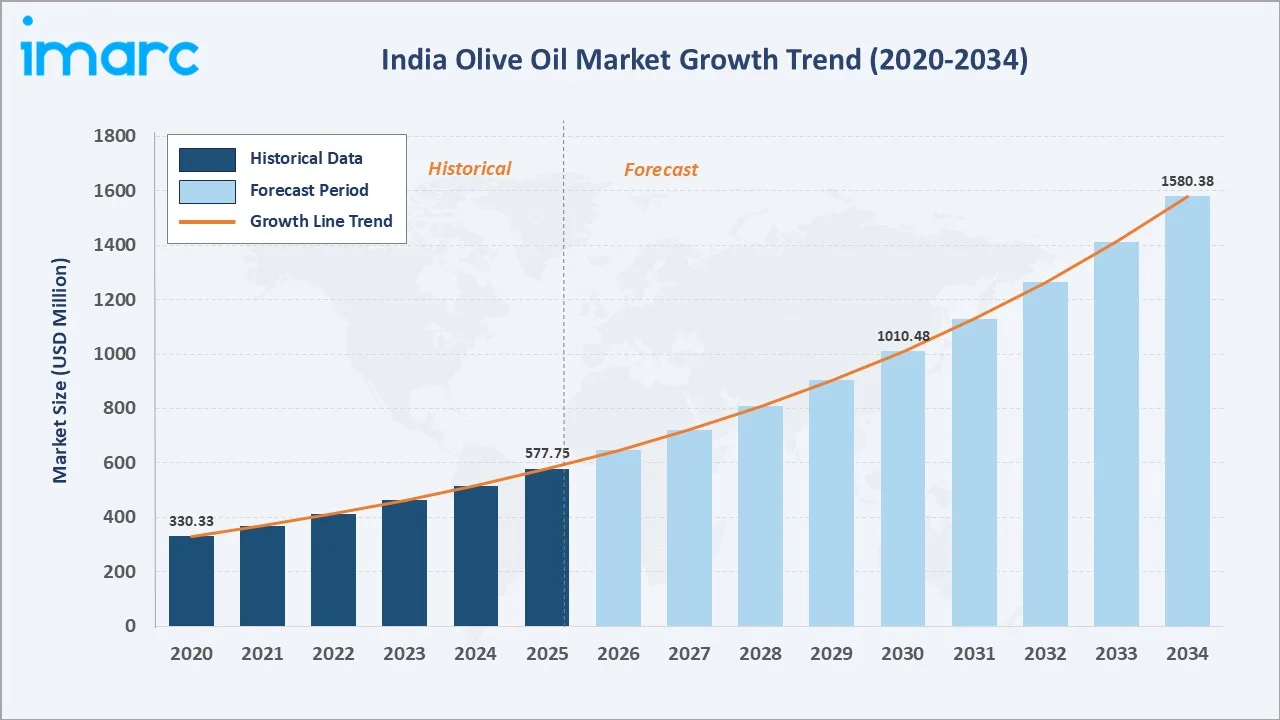

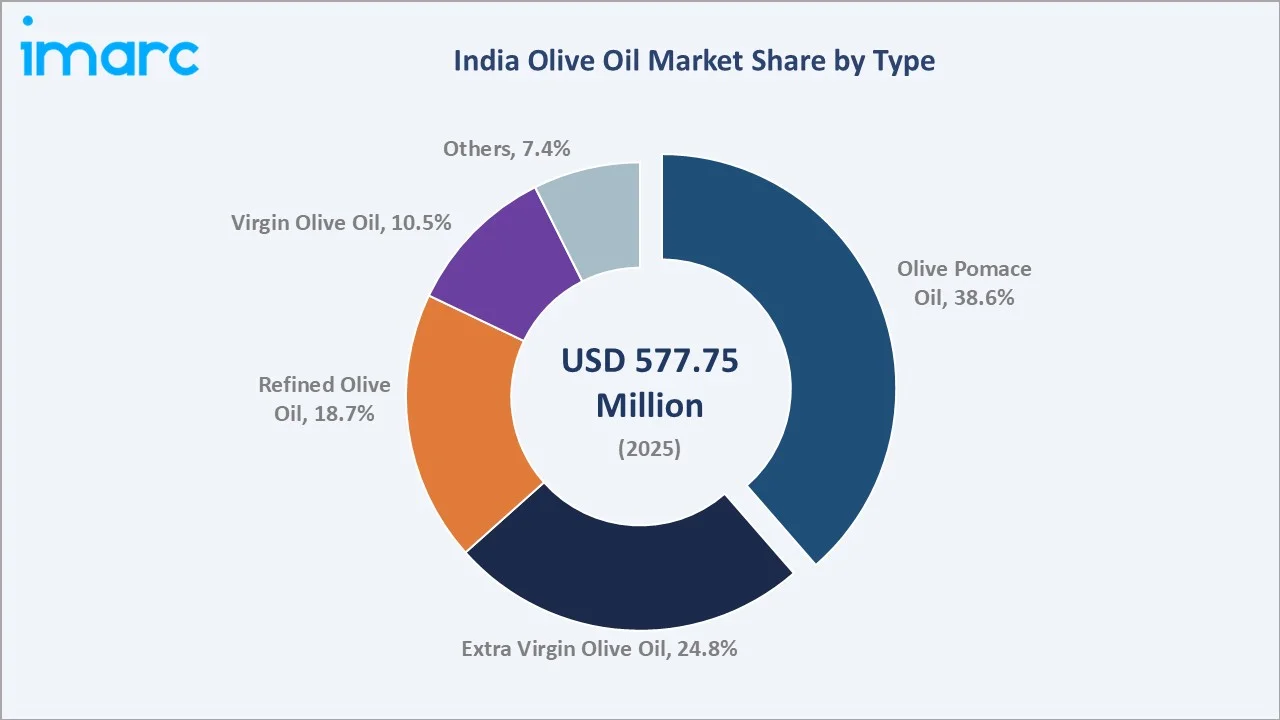

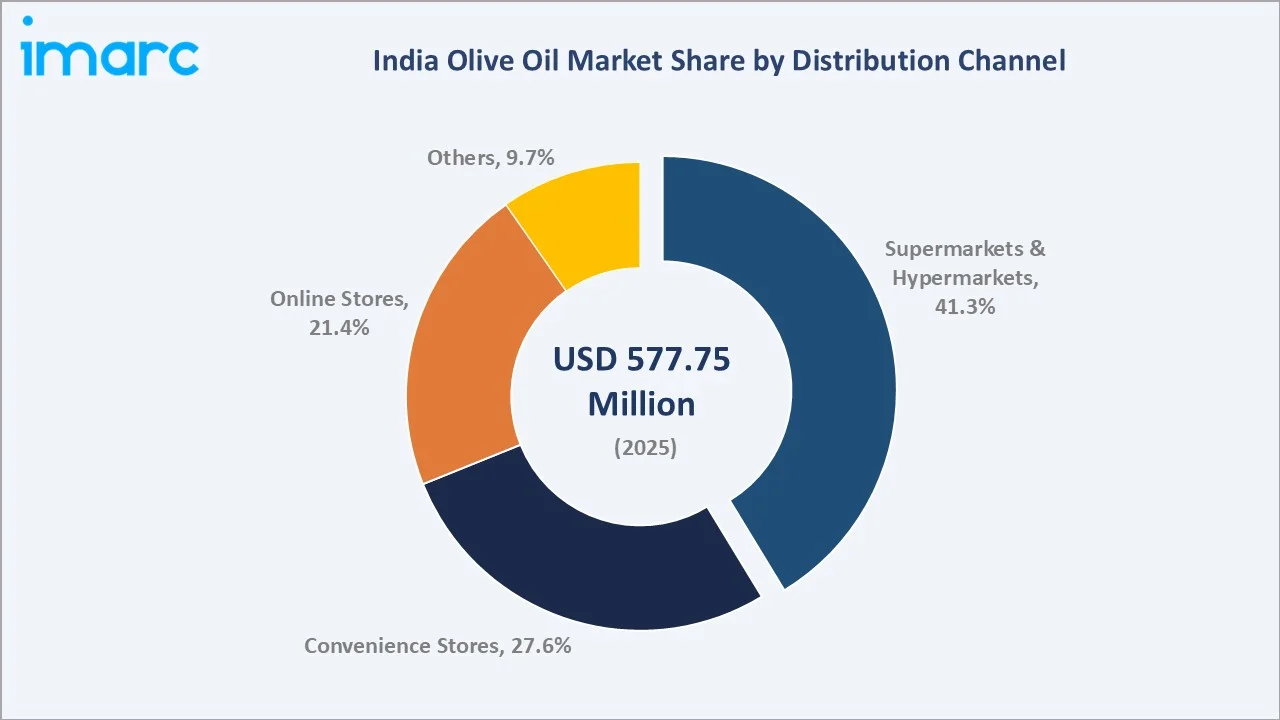

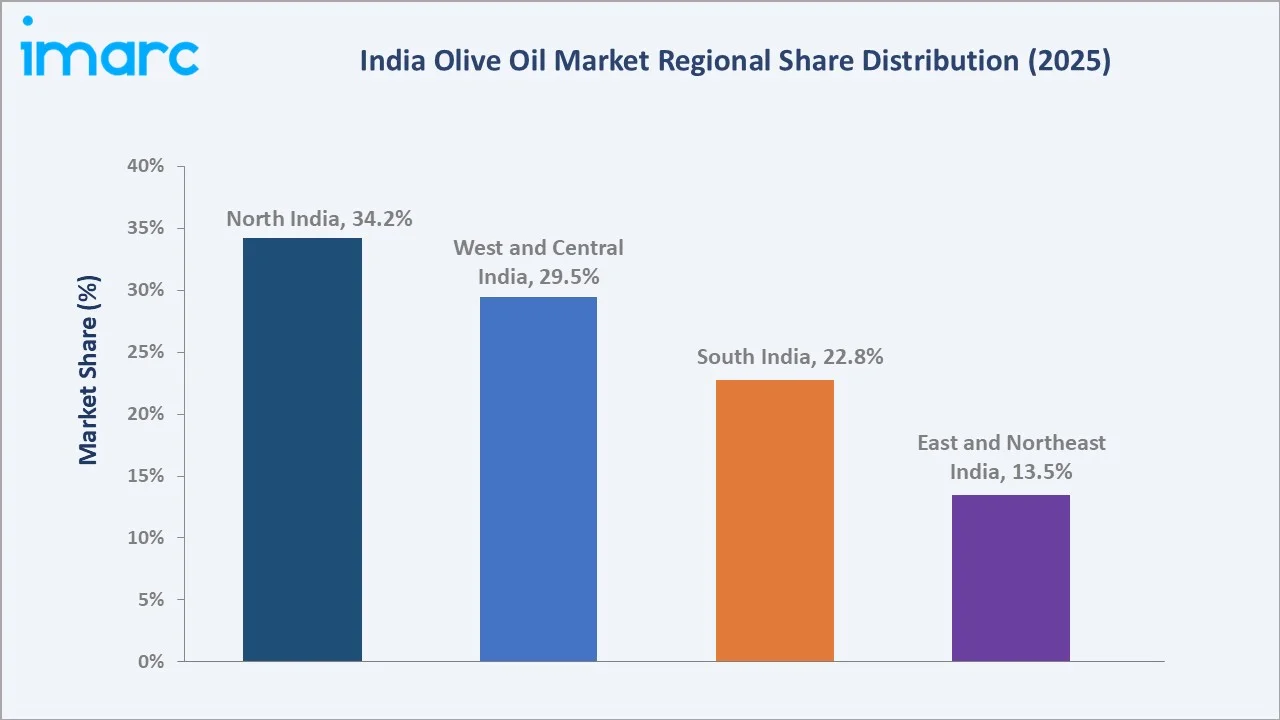

The India olive oil market size was valued at USD 577.75 Million in 2025 and is projected to reach USD 1,580.38 Million by 2034, exhibiting a CAGR of 11.83% during the forecast period 2026-2034. Rising health awareness among urban consumers, growing penetration of Mediterranean cuisine, expanding e-commerce reach for premium edible oils, and increasing applications in cosmetics and pharmaceuticals are driving the growth of the Indian olive oil market. Olive Pomace Oil leads the type segment at 38.6% in 2025, while Supermarkets and Hypermarkets dominate distribution at 41.3%. North India accounts for 34.2% of revenue in 2025, the country's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 577.75 Million |

|

Forecast Market Size (2034) |

USD 1,580.38 Million |

|

CAGR (2026-2034) |

11.83% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (34.2% share, 2025) |

|

Fastest Growing Region |

West and Central India (CAGR ~12.0%) |

|

Leading Type |

Olive Pomace Oil (38.6%, 2025) |

|

Leading Distribution Channel |

Supermarkets & Hypermarkets (41.3%, 2025) |

The India olive oil market growth trajectory from 2020 through 2034 reflects steady historical expansion supported by rising health consciousness, followed by a forecast curve powered by premium product adoption, e-commerce scale-up, and indigenous olive cultivation in Rajasthan and Himachal Pradesh.

To get more information on this market, Request Sample

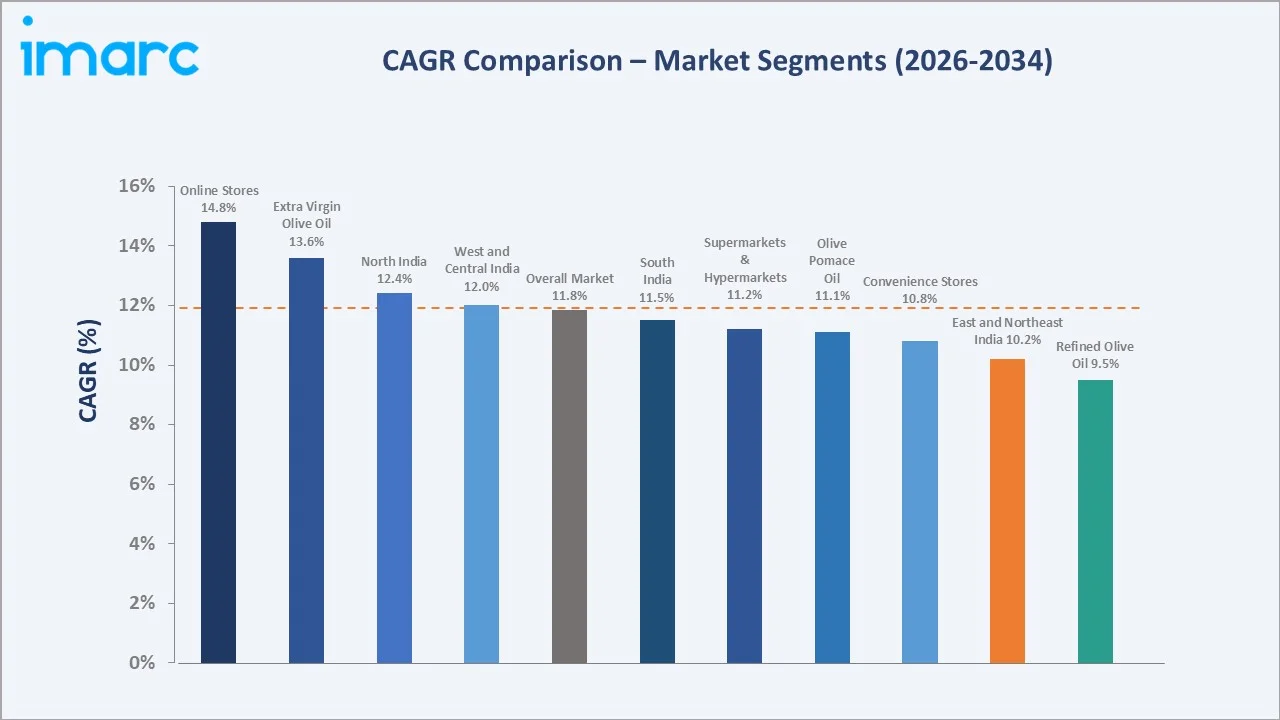

Segment-level CAGR comparisons highlight online stores and extra virgin olive oil as the two fastest-growing categories, both outpacing the overall 11.83% market expansion across the forecast horizon.

Executive Summary

The India olive oil market is undergoing a structural shift as health-conscious consumption replaces traditional cooking oil habits in metropolitan households. Valued at USD 577.75 Million in 2025, the market is projected to reach USD 1,580.38 Million by 2034 at a CAGR of 11.83%. Rising disposable incomes, exposure to Mediterranean cuisine, and the growing footprint of premium grocery retail are sustaining double-digit volume growth across major urban clusters.

Olive Pomace Oil dominates the type segment at 38.6% in 2025, supported by its lower price point and suitability for high-heat Indian cooking. Extra Virgin Olive Oil follows at 24.8%, anchored by health-led premium positioning. Supermarkets and Hypermarkets lead distribution with a 41.3% share in 2025, while Online Stores at 21.4% are the fastest-growing channel as digital grocery deepens its reach in tier-2 and tier-3 cities.

North India leads with a 34.2% share in 2025, driven by Delhi-NCR's premium grocery density and concentrated HoReCa demand. West and Central India follow at 29.5%, anchored by Mumbai-Pune's affluent households. South India holds 22.8%, supported by Bengaluru and Chennai's urban consumption, while East and Northeast India account for 13.5%, reflecting an early-stage but rapidly improving adoption curve.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Olive Pomace Oil - 38.6% share (2025) |

|

Leading Distribution Channel |

Supermarkets & Hypermarkets - 41.3% share (2025) |

|

Leading Region |

North India - 34.2% revenue share (2025) |

|

Second Region |

West and Central India - 29.5% revenue share (2025) |

|

Top Companies |

Borges India, Cargill, Incorporated, Figaro Olive Oil, Del Monte Foods Private Limited, Tata Consumer Products Limited, Deoleo, Disano, and Olitalia S.R.L. |

Key Analytical Observations Supporting the Above Data:

- Olive Pomace Oil's 38.6% lead in 2025 reflects its price-accessibility for Indian cooking applications versus extra virgin variants, especially in mass-market households across metro cities.

- Supermarkets and Hypermarkets' 41.3% dominance is anchored by Reliance Retail, DMart, and Spencer's expanding premium edible oil shelves in tier-1 and tier-2 cities through 2025.

- North India's 34.2% share in 2025 is driven by Delhi-NCR affluence, premium grocery store density, and a growing HoReCa segment serving Mediterranean and continental cuisines.

- Online Stores at 21.4% are the fastest-growing channel, fuelled by Amazon, Flipkart, and BigBasket scaling olive oil assortments and direct-to-consumer brand launches.

India Olive Oil Market Overview

Olive oil in India refers to edible oil extracted from olives (Olea europaea), available in extra virgin, virgin, refined, and pomace grades. The ecosystem combines large-scale imports from Spain, Italy, and Greece with small but growing domestic cultivation in Rajasthan and Himachal Pradesh.

Applications span household cooking, salad dressings, marinades, HoReCa kitchens, cosmetics, hair care, and pharmaceutical formulations. Macroeconomic enablers include India's rising USD 4 trillion+ GDP base, increasing urban household incomes, and 850 million internet users powering e-commerce expansion of premium edible oils through 2025.

Market Dynamics

To evaluate market opportunities, Request Sample

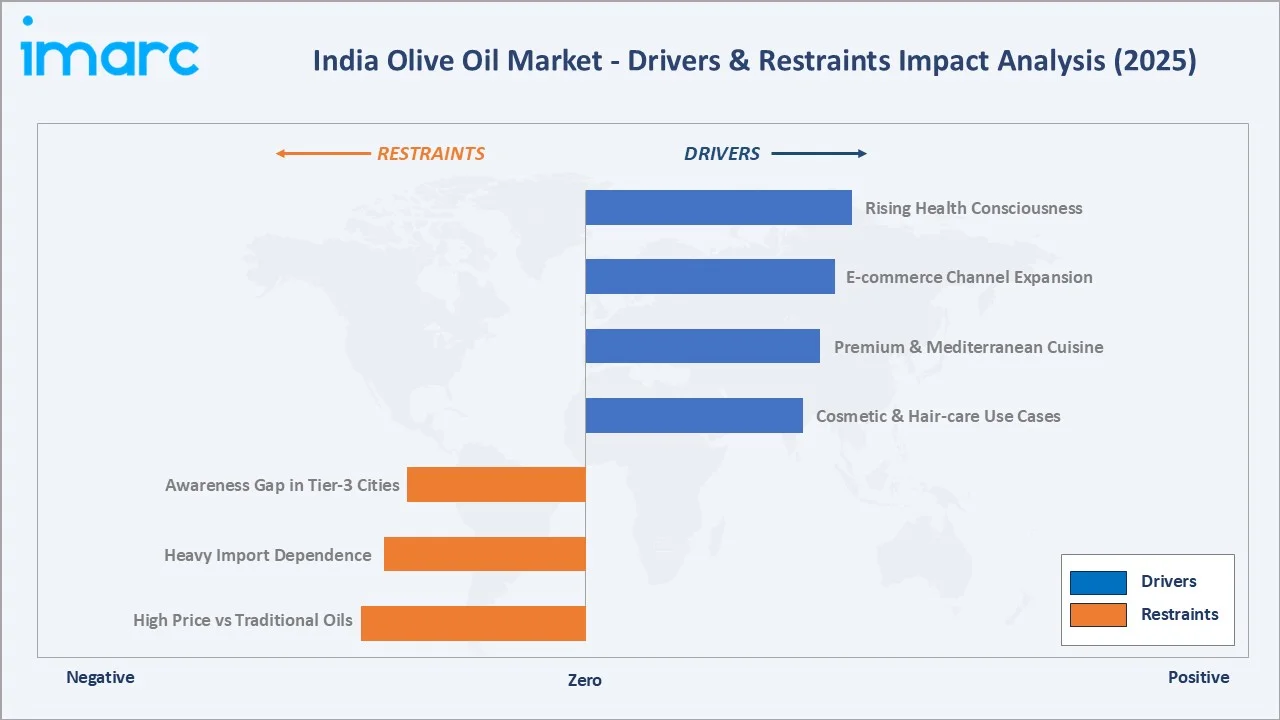

Market Drivers

- Rising Health Consciousness and Premiumisation: Indian urban consumers, particularly millennials and Gen Z, are willing to pay 4-6 times the price of refined sunflower or mustard oil for extra virgin olive oil, citing cardiovascular benefits and high monounsaturated fat content.

- E-commerce Channel Expansion: Online Stores account for 21.4% of olive oil sales in 2025 and are projected to grow significantly, led by Amazon, Flipkart, BigBasket, and direct-to-consumer brands targeting tier-2 and tier-3 cities.

- Mediterranean Cuisine Penetration: The HoReCa segment is expanding olive oil consumption through Italian, Greek, and Lebanese restaurant chains, supported by India’s large base of over 500,000 restaurants and the rapid expansion of QSR and casual dining outlets across metro markets.

- Cosmetic and Hair-care Applications: Olive oil is increasingly used in shampoos, conditioners, and Ayurveda-inspired hair care formulations. Products such as Love Beauty and Planet’s olive oil shampoos and Palmer’s olive oil-based hair care range are supporting the expansion of a growing non-food revenue stream.

Market Restraints

- High Price versus Traditional Cooking Oils: Olive oil retails at INR 800-1,500 per litre in 2025 versus INR 130-200 for sunflower or mustard oil, capping mass-market penetration in tier-3 and rural India.

- Heavy Import Dependence: Over 95% of olive oil consumed in India in 2025 is imported, primarily from Spain and Italy, exposing the market to global crop volatility and shipping cost shocks.

- Awareness Gap in Tier-3 Cities: Consumer familiarity with grade differences (extra virgin, virgin, pomace) remains limited beyond the top 8 metros, slowing adoption of premium variants in smaller urban centres.

Market Opportunities

- Tier-2 and Tier-3 City Expansion: Expanding urban centers beyond metros remain under-penetrated for premium edible oils, offering a substantial greenfield opportunity. Brands such as Borges and Figaro leverage e-commerce platforms like Amazon and Flipkart and are expanding modern retail networks to reach new consumers.

- Domestic Olive Cultivation Scale-up: Rajasthan's olive farming initiative, supported by the state government and partnered with Israeli agronomy expertise, can reduce import dependence and price volatility through the forecast period.

- Functional and Flavoured Variants: Herb-infused, garlic-infused, and chilli-infused olive oils are emerging as a premium sub-category, aligned with Indian taste profiles and recipe-led marketing.

Market Challenges

- Currency and Tariff Volatility: Rupee depreciation against the Euro and import duty changes have driven olive oil retail prices up in recent years, creating affordability shocks for mid-income households.

- Adulteration and Mislabelling Risks: FSSAI and consumer associations have flagged instances of mislabelled or blended olive oil in 2024-2025, undermining brand trust in unorganised retail channels.

- Cooking-Suitability Perceptions: A persistent perception that olive oil is unsuitable for high-heat Indian cooking limits its substitution against ghee, mustard, and groundnut oil in traditional kitchens.

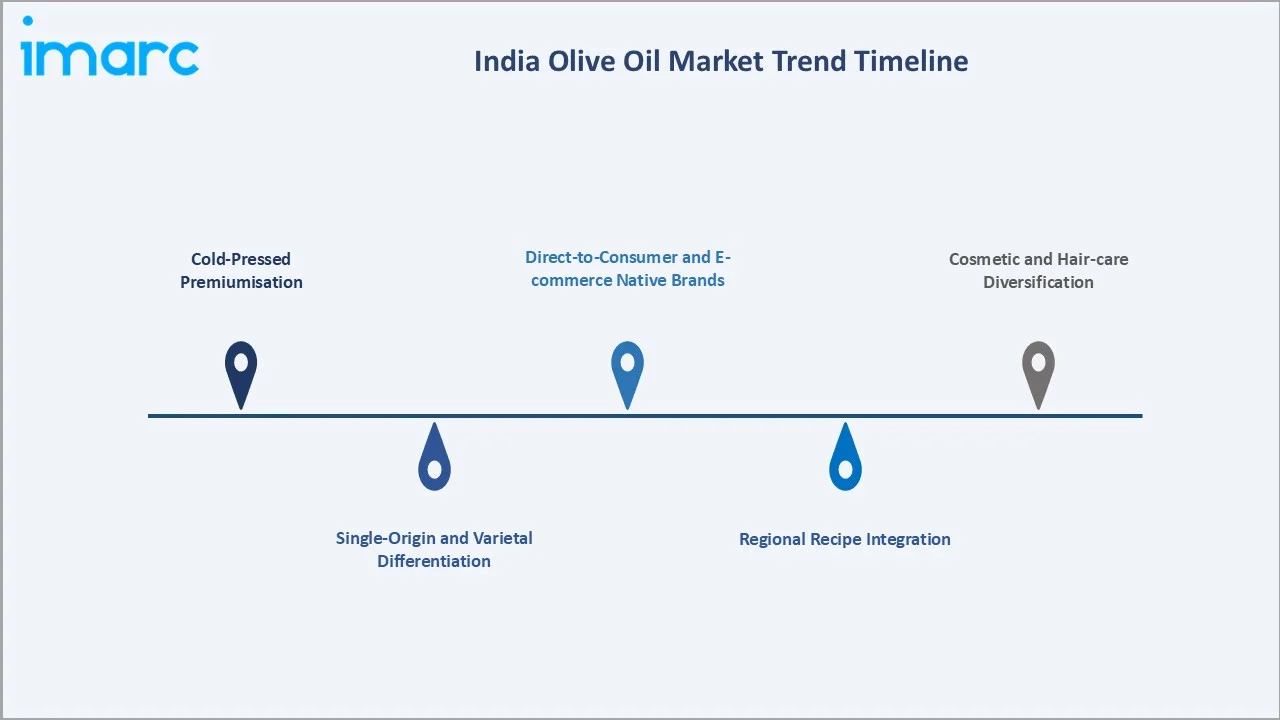

Emerging Market Trends

1. Cold-Pressed Premiumisation

Cold-pressed extra virgin olive oil is becoming the flagship premium variant. In April 2025, Tata Simply Better launched cold-pressed Extra Virgin Olive Oil and Sesame Oil in 1-litre PET bottles, signalling a major Indian FMCG entry into the segment.

2. Single-Origin and Varietal Differentiation

Brands are introducing varietal-led olive oil ranges, mirroring premium wine positioning. In January 2025, Borges India launched single-variety Arbequina-based 'Fruity' and Picual-based 'Character' extra virgin olive oils, both available across online and offline channels.

3. Direct-to-Consumer and E-commerce Native Brands

D2C-first olive oil brands using subscription, recipe-led content, and influencer partnerships are scaling rapidly. Online Stores' share is projected to expand significantly by 2034 as digital grocery deepens.

4. Regional Recipe Integration

Olive oil is being adapted to Indian cooking, with North Indian use in tandoor and grilling, and South Indian application in sautéed vegetables and dals. Celebrity chefs and television cooking shows are accelerating this culinary integration.

5. Cosmetic and Hair-care Diversification

Olive oil is increasingly used in personal care, especially in Ayurveda-inspired hair-care lines. The cosmetic and pharmaceutical end-use segments are growing steadily, creating a structural non-food demand stream.

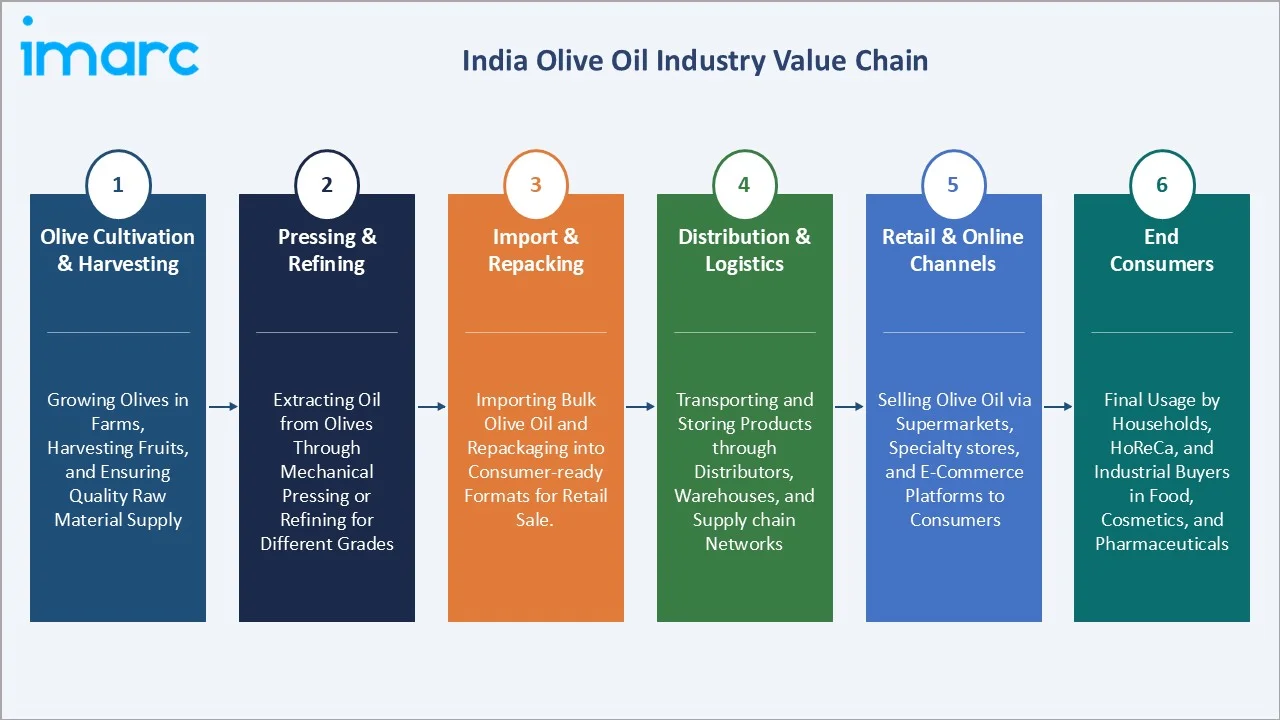

Industry Value Chain Analysis

The India olive oil value chain spans six integrated stages, from cultivation through end consumption, with imports dominating raw material supply and modern retail plus e-commerce dominating distribution.

|

Stage |

Key Players / Examples |

|

Olive Cultivation & Harvesting |

Growing olives in farms, harvesting fruits, and ensuring quality raw material supply. |

|

Pressing & Refining |

Extracting oil from olives through mechanical pressing or refining for different grades. |

|

Import & Repacking |

Importing bulk olive oil and repackaging into consumer-ready formats for retail sale. |

|

Distribution & Logistics |

Transporting and storing products through distributors, warehouses, and supply chain networks. |

|

Retail & Online Channels |

Selling olive oil via supermarkets, specialty stores, and e-commerce platforms to consumers. |

|

End Consumers |

Final usage by households, HoReCa, and industrial buyers in food, cosmetics, and pharmaceuticals. |

Importers and bottlers occupy the highest strategic value position in the chain, controlling brand equity, retail pricing, and consumer marketing. Domestic cultivators remain a small but strategically important node with long-term potential to compress import costs.

Technology Landscape in the India Olive Oil Industry

Cold-Pressing and Extraction Technology

Cold-pressed extraction at temperatures below 27°C preserves polyphenols, antioxidants, and flavour profiles, supporting premium positioning. Indian bottlers are partnering with European mills to import cold-pressed concentrate for domestic packaging through 2025.

Domestic Cultivation and Agronomy

Israeli drip-irrigation and varietal innovation have enabled Rajasthan's olive cultivation across over 800 hectares by 2025, supported by Rajasthan Olive Cultivation Limited. Climate-resistant varietals are being trialled to boost yields and reduce import dependence.

Smart Packaging and Traceability

Brands are adopting QR-code-based traceability, dark-glass bottles to preserve polyphenols, and tamper-evident closures. FSSAI-compliant labelling and origin certification are emerging as key trust-building tools.

E-commerce Personalisation and AI Recommendations

Online platforms are deploying AI-driven recommendation engines, recipe pairings, and subscription bundles for olive oil. These tools have lifted average order values on direct-to-consumer olive oil sites.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Olive Pomace Oil | 38.6% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 41.3% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Region | North India | 34.2% | 2025 |

By Type

Olive Pomace Oil dominates at 38.6% in 2025, anchored by its lower price point of INR 600-900 per litre and suitability for high-heat Indian cooking. Pomace remains the volume engine of the Indian olive oil market through the forecast period.

To access detailed market analysis, Request Sample

Extra Virgin Olive Oil holds 24.8% in 2025, growing significantly as health-conscious urban consumers premiumise. Refined Olive Oil at 18.7% serves a mid-tier price band for everyday cooking, while Virgin Olive Oil at 10.5% captures niche culinary use.

Others, at 7.4%, include flavoured, infused, and organic specialty variants. This sub-segment is projected to grow over the forecasted year, supported by D2C brand experimentation and Indian-cuisine-ready flavours.

By Distribution Channel

Supermarkets and Hypermarkets lead at 41.3% in 2025, anchored by Reliance Retail, DMart, Spencer's, and More Retail, expanding premium edible oil shelves across tier-1 and tier-2 cities. Modern trade remains the dominant discovery and trial channel for olive oil.

Convenience Stores account for 27.6% in 2025, supported by neighbourhood kirana modernisation and chain stores like 24Seven and Reliance Smart Bazaar. Online Stores at 21.4% are the fastest-growing channel, led by Amazon, Flipkart, and BigBasket. Others, at 9.7%, include specialty gourmet stores and HoReCa-direct channels.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

34.2% |

Delhi-NCR affluence, premium grocery density, HoReCa Mediterranean cuisine demand |

|

West and Central India |

29.5% |

Mumbai-Pune affluent households, Gujarat health-conscious consumers, MP urban growth |

|

South India |

22.8% |

Bengaluru tech ecosystem, Chennai HoReCa, Kerala Ayurveda cosmetic use |

|

East and Northeast India |

13.5% |

Kolkata premium retail, Guwahati emerging e-commerce, slow but rising adoption |

North India commands a 34.2% share in 2025, anchored by Delhi-NCR's affluent household concentration, dense premium grocery retail (DLF Promenade, Ambience Mall), and a vibrant Mediterranean and continental restaurant scene that drives steady HoReCa demand.

West and Central India holds 29.5% in 2025, with Mumbai's affluent households, Pune's IT and corporate base, and Ahmedabad-Surat's Gujarati health-conscious consumers driving demand. Mumbai and Delhi together represent over 70% of regional consumption.

South India contributes 22.8% in 2025, supported by Bengaluru's tech-driven affluent base, Chennai's premium grocery and HoReCa demand, Hyderabad's growing modern retail, and Kerala's Ayurveda and cosmetic application of olive oil in hair-care products.

East and Northeast India accounts for 13.5% in 2025, with Kolkata's premium grocery hubs anchoring regional demand. The region is the fastest-improving on a percentage basis as e-commerce and modern retail close historic distribution gaps in tier-2 cities.

Competitive Landscape

|

Company Name |

Key Brand / Range |

Market Position |

Core Strength |

|

Borges India |

Borges Extra Virgin |

Leader |

Strong premium portfolio, varietal differentiation, omnichannel reach |

|

Cargill, Incorporated |

Leonardo EVOO |

Leader |

Wide pricing tiers, deep modern trade penetration |

|

Figaro Olive Oil |

Figaro Olive Oil |

Leader |

Iconic brand recognition, mass-premium positioning |

|

Del Monte Foods Private Limited |

Del Monte Italian Range |

Leader |

FMCG distribution scale, multi-category presence |

|

Tata Consumer Products Limited |

Tata Simply Better EVOO |

Challenger |

FMCG trust, cold-pressed launch April 2025 |

|

Deoleo |

Bertolli Olive Oil |

Challenger |

Italian heritage positioning, premium retail focus |

|

Disano |

Disano Olive Oil |

Challenger |

Value-tier mass-market reach |

|

Olitalia S.R.L |

Olitalia Olive Oil |

Niche |

Italian specialty, gourmet retail presence |

The competitive landscape combines established global olive oil brands with strong Indian distribution alongside FMCG majors entering the segment and emerging domestic cultivators leveraging indigenous origin stories. Premiumisation is the dominant strategic theme through 2025-2034.

Key Company Profiles

Borges India

Borges is one of the largest olive oil brands in India, part of Spain's Borges International Group. Borges India offers a broad portfolio across pomace, virgin, and extra virgin olive oil, with strong omnichannel distribution across modern trade and e-commerce.

- Product & Brand Portfolio: Borges Extra Virgin Olive Oil, Borges Pomace Olive Oil, single-variety Arbequina 'Fruity' and Picual 'Character' EVOO, and infused variants.

- Recent Developments: In January 2025, Borges India launched two single-variety extra virgin olive oils, Arbequina-based 'Fruity' and Picual-based 'Character', distributed across online and offline channels.

- Strategic Focus: Borges prioritises premium varietal differentiation, single-origin storytelling, and digital-first marketing to reinforce its leadership in the extra virgin segment.

Tata Consumer Products

Tata Consumer Products is one of India's largest FMCG groups with a fast-expanding edible oil and food platform. The Tata Simply Better range has positioned the group as a credible domestic challenger in the cold-pressed olive oil segment.

- Product & Brand Portfolio: Tata Simply Better Extra Virgin Olive Oil, Tata Simply Better Cold-Pressed Sesame Oil, and adjacent clean-label edible oil ranges.

- Recent Developments: In April 2025, Tata Simply Better launched two cold-pressed oil variants, Extra Virgin Olive Oil and Sesame Oil, in 1-litre PET bottles, marketed as clean-label and produced without heat or chemicals.

- Strategic Focus: Tata Consumer focuses on clean-label premiumisation, FMCG distribution leverage, and trust-led positioning targeting health-conscious urban Indian households.

Cargill, Incorporated

Cargill is one of the world's largest privately held food and agriculture companies, headquartered in Minnetonka, Minnesota, with operations across 70+ countries. In India, Cargill Foods India operates a multi-brand consumer portfolio across edible oils, fats, and flour, reaching over 100 million consumers.

- Product & Brand Portfolio: Leonardo Extra Virgin Olive Oil, Leonardo Refined, Leonardo Pomace, and flavoured variants.

- Recent Developments: In 2025, Cargill showcased new food and edible oil solutions at AAHAR 2025, signaling continued investment in consumer-facing food categories in India.

- Strategic Focus: Cargill prioritises wide-grade portfolio coverage, modern-trade visibility, and digital recipe-led marketing to convert traditional cooking-oil users.

Market Concentration Analysis

The India olive oil market exhibits moderate concentration. The top 5 brands, including Borges India, Cargill, Figaro, Del Monte, and Tata Simply Better, collectively account for an estimated 55-62% of revenue in 2025, with the remainder distributed across challenger and emerging brands.

Fragmentation is highest in the flavoured and specialty olive oil segment, where boutique D2C brands compete with global imports. Mass-market pomace is more concentrated, dominated by Borges, Leonardo, and Figaro, which together hold an estimated 45-50% of pomace revenue in 2025.

Consolidation is gradually accelerating as Indian FMCG groups like Tata Consumer scale-up and global private equity invests in domestic gourmet portfolios. M&A activity is expected to intensify through the forecast period as olive oil moves from niche to mainstream premium.

Investment & Growth Opportunities

Fastest-Growing Segments

Online Stores are the fastest-growing distribution channel, followed by Extra Virgin Olive Oil within types. Together, these segments represent the highest absolute and relative investment opportunity in the Indian olive oil market.

Emerging Market Expansion

Tier-2 and tier-3 cities, where olive oil household penetration remains below 4% in 2025, represent a multi-hundred-million-dollar greenfield market through 2030. East and Northeast India are emerging as high-growth regions, driven by improving urban consumption and rising health awareness.

Venture & Private Investment Trends

India's direct-to-consumer (D2C) sector raised approximately USD 930 million in 2023 and USD 757 million in 2024 across all consumer categories. Within this, the food and beverage segment continues to attract steady early-stage investor interest. Premium edible oils and gourmet pantry brands remain a niche but emerging sub-category, supported by FMCG investments such as Tata Consumer Products' 2023 launch of Tata Simply Better cold-pressed oils.

Future Market Outlook (2026-2034)

The India olive oil market forecast projects revenue to scale from USD 577.75 Million in 2025 to USD 1,580.38 Million by 2034 at a CAGR of 11.83%, a near-three-times expansion driven by health-led premiumisation, e-commerce scale-up, HoReCa demand, and gradual domestic cultivation.

Three structural shifts are most likely to reshape the market through 2034: cold-pressed and varietal extra virgin olive oil entering mainstream premium, Online Stores crossing 30% channel share, and indigenous Indian olive cultivation contributing meaningfully to supply.

By 2034, the India olive oil industry is forecast to evolve from a primarily import-led premium niche into a fully developed mainstream-premium edible oil category, with broader use across food, HoReCa, cosmetics, and pharmaceuticals supported by trusted FMCG and gourmet brand portfolios.

Research Methodology

Primary Research

Primary research included over 40 structured interviews conducted in 2024-2025 with category heads at olive oil brands, modern trade buyers, e-commerce category managers, HoReCa procurement leads, domestic cultivators in Rajasthan and Himachal Pradesh, and consumer research panels across metro and tier-2 India.

Secondary Research

Secondary sources include FSSAI publications, DGFT import data, International Olive Council (IOC) global trade reports, Ministry of Agriculture and Farmers Welfare data, NielsenIQ retail audit data, brand annual reports, and trade publications, including The Economic Times, Business Standard, and Food and Beverage News.

Forecasting Models

Market size estimation and forecasts were derived using a combination of top-down and bottom-up models, incorporating GDP growth, household disposable income, urbanisation indices, premium grocery footprint expansion, e-commerce edible oil penetration, and historical type-and-channel mix evolution. Scenario analysis covering base, optimistic, and conservative cases was performed.

India Olive Oil Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Virgin Olive Oil, Refined Olive Oil, Extra Virgin Olive Oil, Olive Pomace Oil, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Applications Covered | Food and Beverage, Pharmaceuticals, Cosmetics, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Borges India, Cargill, Incorporated, Figaro Olive Oil, Del Monte Foods Private Limited, Tata Consumer Products Limited, Deoleo, Disano, Olitalia S.R.L, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India olive oil market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India olive oil market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India olive oil industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Olive Oil Market Report

The India olive oil market was valued at USD 577.75 Million in 2025, supported by rising health awareness, premium grocery expansion, and growing Mediterranean cuisine adoption.

The market is projected to reach USD 1,580.38 Million by 2034, expanding at a CAGR of 11.83% during 2026-2034, driven by premiumisation and e-commerce growth.

Olive Pomace Oil leads with a 38.6% share in 2025, anchored by its accessible price point and suitability for high-heat Indian cooking applications across households.

Supermarkets and Hypermarkets lead at 41.3% in 2025, supported by Reliance Retail, DMart, and Spencer's expanding premium edible oil shelves across tier-1 and tier-2 cities.

North India leads with a 34.2% share in 2025, driven by Delhi-NCR's affluent households, premium grocery store density, and a strong HoReCa Mediterranean cuisine ecosystem.

Key drivers include rising health consciousness, premium grocery expansion, Mediterranean cuisine penetration, e-commerce scale-up, and growing cosmetic and hair-care applications of olive oil.

Online Stores are the fastest-growing channel at over 14.8% CAGR through 2034, followed closely by Extra Virgin Olive Oil within types growing at over 13.6% CAGR.

Leading companies include Borges India, Cargill, Incorporated, Figaro Olive Oil, Del Monte Foods Private Limited, Tata Consumer Products Limited, Deoleo, Disano, and Olitalia S.R.L.

E-commerce platforms like Amazon, Flipkart, and BigBasket are scaling olive oil reach into tier-2 and tier-3 cities, supporting D2C launches and recipe-led brand marketing.

Rajasthan and Himachal Pradesh olive farming initiatives are gradually scaling up, aiming to reduce import dependence, ease price volatility, and support indigenous brand storytelling.

Key applications include household cooking, salad dressings, HoReCa kitchens, hair-care formulations, Ayurveda cosmetics, and pharmaceutical bases. Food and Beverage remains the largest end-use segment.

Main challenges include high prices versus traditional oils, heavy import dependence, currency volatility, awareness gaps in tier-3 cities, and adulteration risks in unorganised retail channels.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)