Olive Oil Market Size, Share, Trends and Forecast by Type, Distribution Channel, Application, and Region, 2026-2034

Olive Oil Market Size, Share, Trends & Forecast (2026-2034)

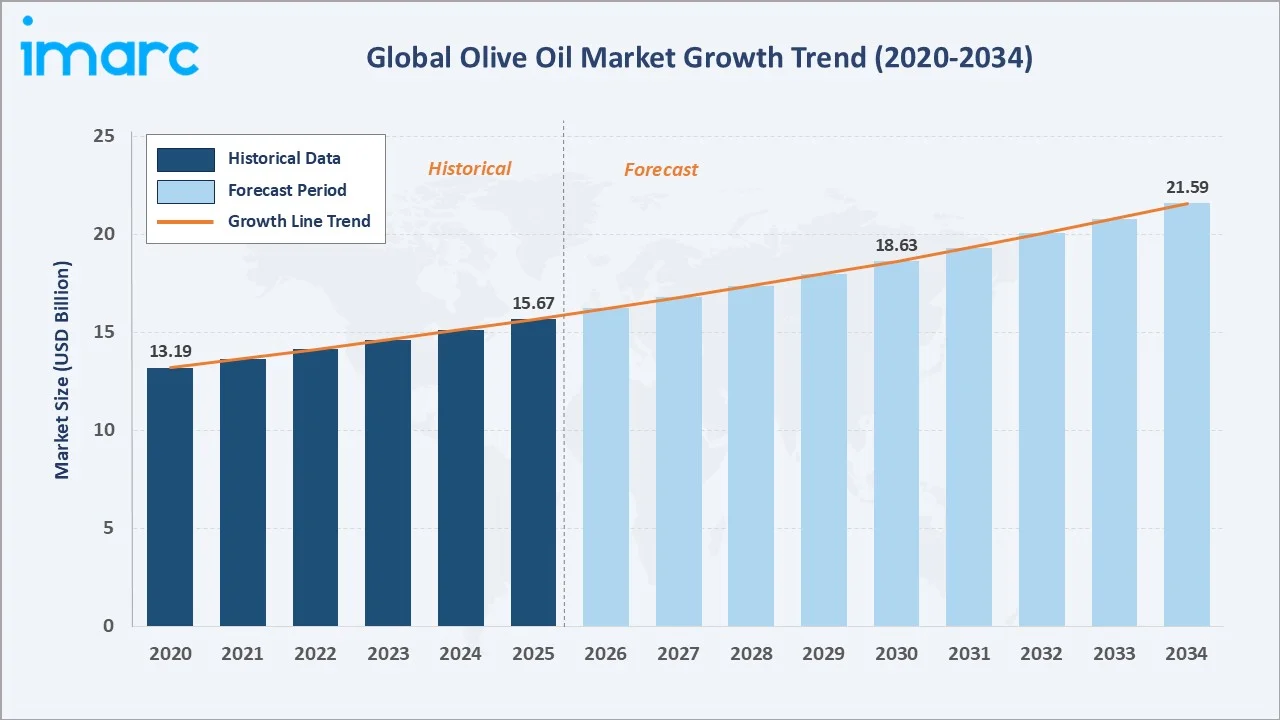

The global olive oil market reached USD 15.67 Billion in 2025 and is projected to reach USD 21.59 Billion by 2034, growing at a CAGR of 3.52% during 2026-2034. Rising health-conscious consumption anchored in the Mediterranean diet, accelerating premium and extra virgin adoption, expansion of e-commerce and direct-to-consumer channels, and growing applications in cosmetics and personal care are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.67 Billion |

|

Forecast Market Size (2034) |

USD 21.59 Billion |

|

CAGR (2026-2034) |

3.52% |

|

Base Year |

2025 |

|

Historical Period |

2026-2034 |

|

Forecast Period |

2026-2034 |

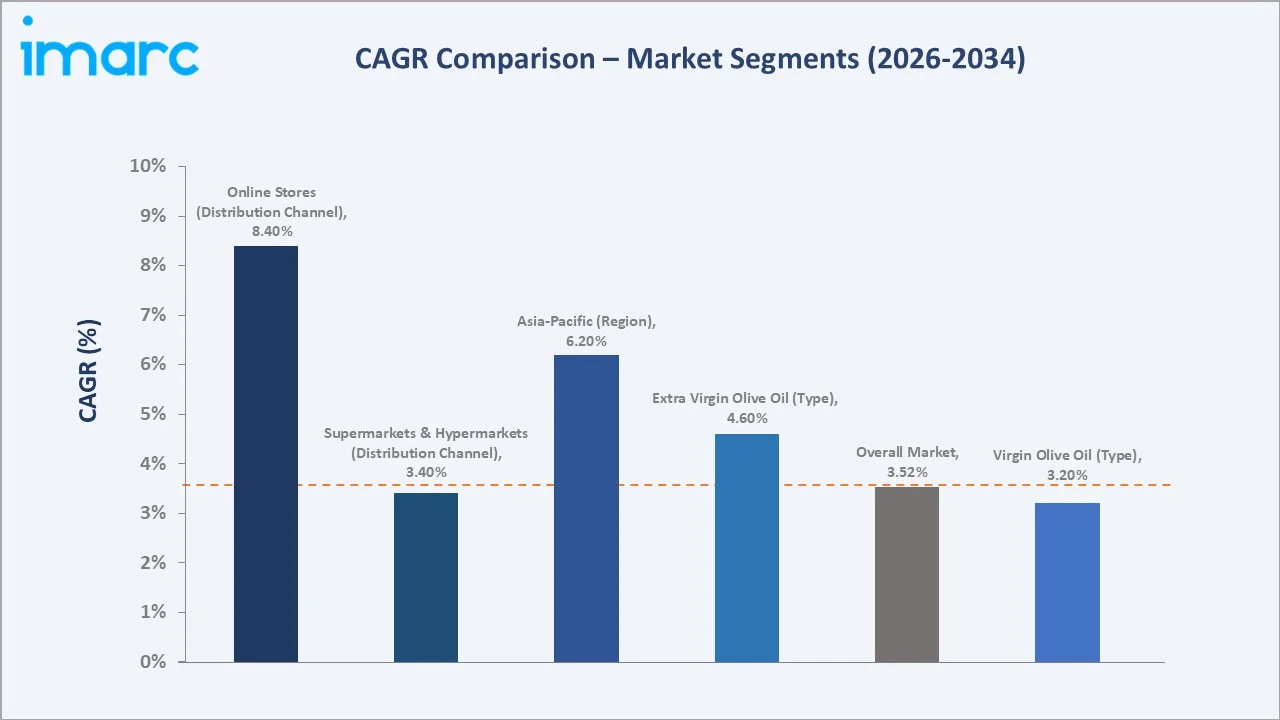

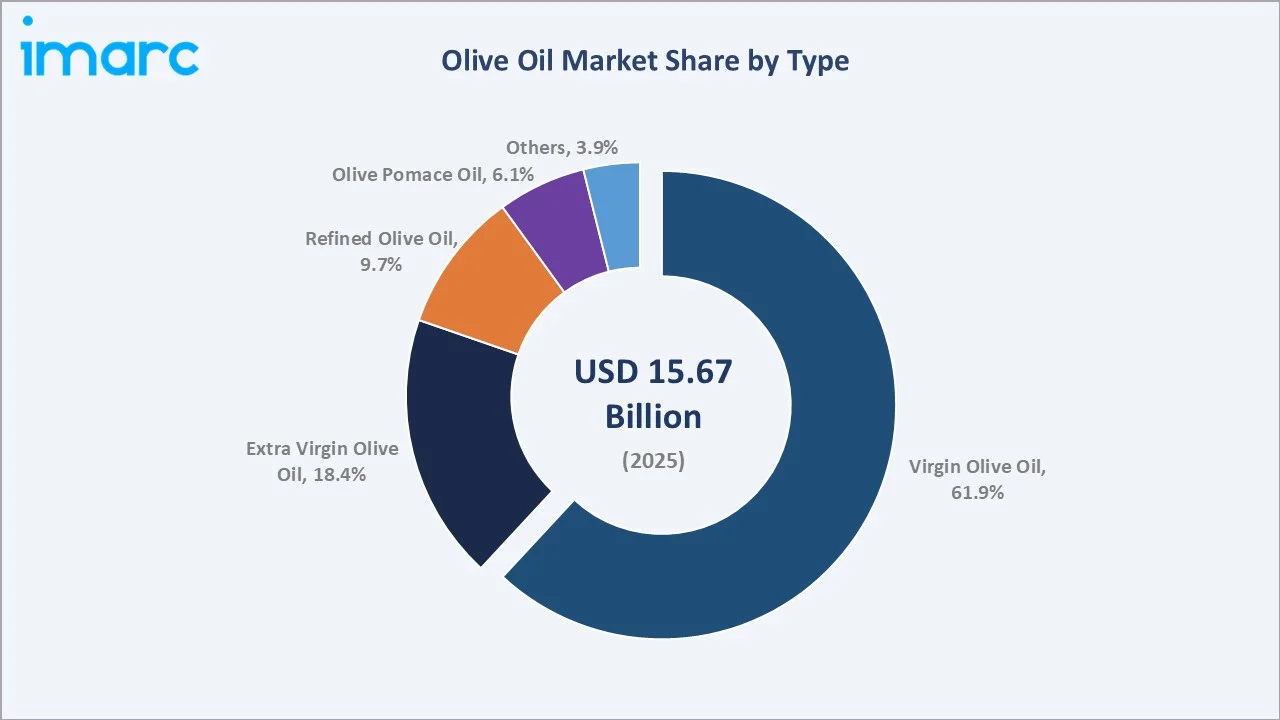

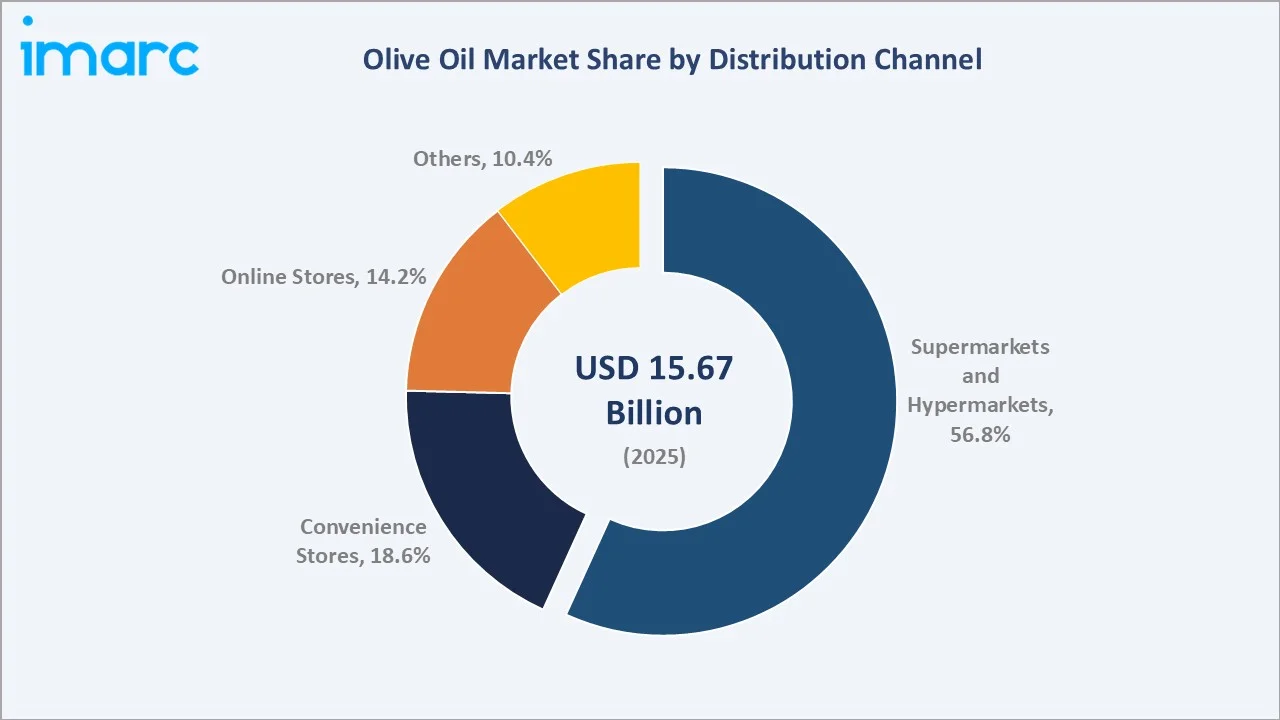

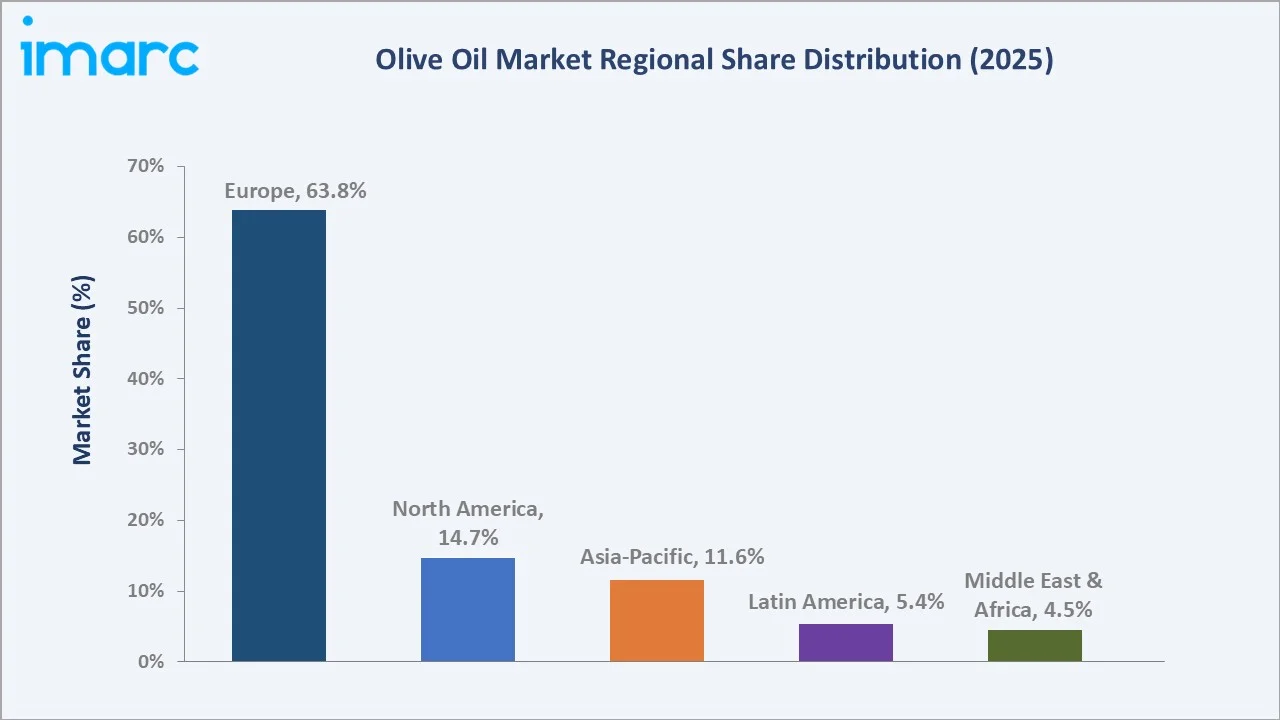

Europe leads regionally with a 63.8% share in 2025, anchored by the European Union, which accounts for approximately 67% of global olive oil production. Virgin olive oil commands the dominant type segment at 61.9%, while Supermarkets and hypermarkets account for 56.8% of the distribution channel breakdown, reflecting olive oil's established status as a mainstream grocery staple.

To get more information on this market, Request Sample

The market grew from USD 13.19 Billion in 2020 to USD 15.67 Billion in 2025, reflecting a historical CAGR of approximately 3.51%. The forecast period is supported by sustained premium extra virgin demand, e-commerce expansion, growing health-driven adoption across Asia-Pacific and North America, and rising cosmetic applications. The market reaches USD 18.63 Billion by 2030 before expanding to USD 21.59 Billion in 2034.

Executive Summary

The global olive oil market is experiencing steady expansion driven by converging consumer trends in healthy fats consumption, Mediterranean diet adoption, premium food positioning, and the rising prominence of olive oil in cosmetics and personal care. The market reached USD 15.67 Billion in 2025 and is forecast to reach USD 21.59 Billion by 2034, growing at a CAGR of 3.52%.

Virgin olive oil dominates the type segment with a 61.9% share in 2025, reflecting established household culinary use and broad price-point accessibility across mass-market retail. Extra virgin olive oil at 18.4% commands the premium segment, growing at approximately 4.6% CAGR driven by health-conscious demand.

Supermarkets and hypermarkets lead the distribution channel segment at 56.8%, supported by olive oil's grocery staple status. Online stores at 14.2% represent the fastest-growing channel at approximately 8.4% CAGR. Europe commands 63.8% of the regional share, while Asia-Pacific is the fastest-growing region at approximately 6.2% CAGR. Key players include DEOLEO S.A., NUTRINVESTE SGPS, S.A., BORGES INTERNATIONAL GROUP, S.L.U., and Palamidas Olive Oil.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Virgin Olive Oil – 61.9% share (2025) |

|

Fastest Growing Type |

Extra Virgin Olive Oil – ~4.6% CAGR (2026-2034) |

|

Largest Distribution Channel |

Supermarkets & Hypermarkets – 56.8% share (2025) |

|

Fastest Growing Channel |

Online Stores – ~8.4% CAGR (2026-2034) |

|

Leading Region |

Europe – 63.8% share (2025) |

|

Top Companies |

DEOLEO S.A., NUTRINVESTE SGPS, S.A., BORGES INTERNATIONAL GROUP, S.L.U., Palamidas Olive Oil |

Key Analytical Observations Supporting the Above Data:

- Virgin olive oil at 61.9% (2025) reflects its broad household culinary positioning across mass-market grocery retail. The segment benefits from price accessibility relative to extra virgin grades and consistent quality compatible with everyday cooking, salad, and food preparation applications.

- Extra virgin olive oil at 18.4% (2025), growing at approximately 4.6% CAGR, represents the highest-growth type segment, driven by health-conscious premium consumers, accelerating Mediterranean diet adoption in North America and Asia-Pacific, and rising chef and foodie-driven consumer education around polyphenol content and provenance.

- Supermarkets and hypermarkets at 56.8% (2025) reflect olive oil's status as a household grocery staple. Major retailers including Walmart, Tesco, Carrefour, Mercadona, and Costco dedicate substantial shelf space to multi-tier olive oil portfolios spanning private-label, mid-market, and premium imported segments.

- Europe's 63.8% share is structurally anchored by Spain (producing over 1.4 million tons annually), Italy, and Greece, together accounting for over 96% of the EU’s olive oil production. Mediterranean dietary culture, regulatory protection of designation-of-origin labels, and established export infrastructure to North America and Asia reinforce regional leadership.

Olive Oil Market Overview

Olive oil is a liquid fat derived from olives, the fruit of Olea europaea, produced primarily through cold-press mechanical extraction and subsequent refining. The global olive oil market spans four core type categories, virgin, extra virgin, refined, and olive pomace, serving culinary, food-service, cosmetics, pharmaceutical, and personal care end-uses.

The market is shaped by three structural forces: rising global health and wellness consumption, with olive oil positioned as a heart-healthy monounsaturated fat associated with the Mediterranean diet; climate vulnerability of Mediterranean olive production, with droughts and heat waves in Spain; and consumption diversification beyond Europe, with Asia-Pacific and North American consumers driving sustained demand growth at above-global-average rates.

Market Dynamics

To evaluate market opportunities, Request Sample

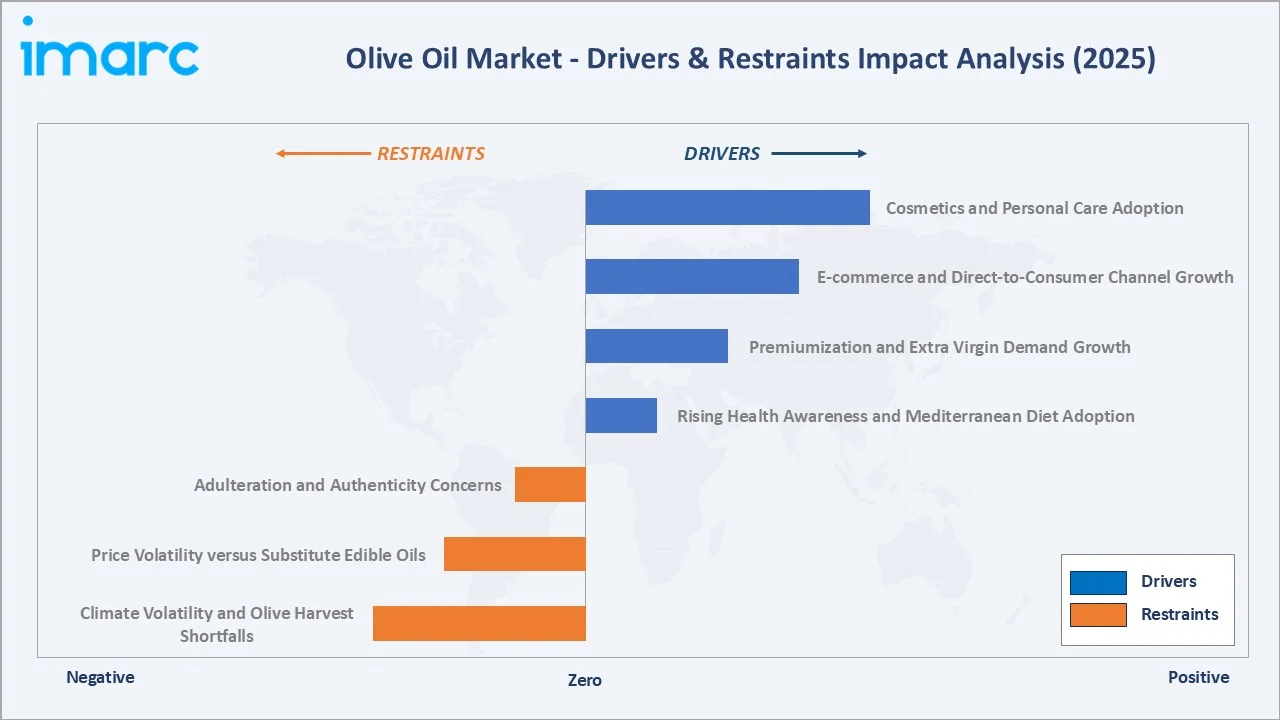

Market Drivers

- Rising Health Awareness and Mediterranean Diet Adoption: Olive oil's positioning as a heart-healthy monounsaturated fat, supported by clinical evidence including the PREDIMED study, has elevated consumer preference globally. American Heart Association and WHO endorsements have accelerated adoption across North America and Asia-Pacific.

- Premiumization and Extra Virgin Demand Growth: Mature-market consumers are trading up from refined to extra virgin grades, with single-origin, organic, and PDO varieties commanding premium pricing. Specialty retailers and direct-to-consumer e-commerce are accelerating this premiumization.

- E-commerce and Direct-to-Consumer Channel Growth: Online channels are expanding at over 8% CAGR, driven by D2C premium brands, subscription services, and Amazon's growing premium specialty food share. Online platforms enable provenance storytelling that resonates with affluent consumers.

- Cosmetics and Personal Care Adoption: Olive oil's emollient, antioxidant, and squalene-rich profile is driving expanded use in soaps, skincare, hair care, and natural personal care. Brands including L'Occitane and Korres feature olive-oil-based ranges.

Market Restraints

- Climate Volatility and Olive Harvest Shortfalls: According to data from the Universidad de Alcalá, severe drought conditions during 2022 and 2023 led to a decline of at least 10% in olive yields, triggering historic price spikes. Climate change is intensifying these supply risks, impacting price stability and consumer affordability.

- Price Volatility versus Substitute Edible Oils: In January 2024, every EU country recorded a year-on-year rise in olive oil inflation, with Portugal registering the highest increase at 69%, followed by Greece at 67% and Spain at 63% compared to January 2023. In price-sensitive markets and food-service, this differential drives substitution toward lower-cost oils.

- Adulteration and Authenticity Concerns: Adulteration with cheaper vegetable oils, grade mislabeling, and counterfeit premium brands erode consumer trust. Regulatory enforcement, blockchain traceability, and laboratory authentication are emerging as compliance priorities.

Market Opportunities

- Asia-Pacific Consumption Expansion: China, Japan, South Korea, and India represent the highest-growth demand markets at approximately 6.2% CAGR. Per-capita consumption in China and Japan remains 0.03 kg and 0.44 kg annually versus 7.5+ kg in Spain, indicating substantial structural growth headroom.

- Organic and Sustainable Certified Olive Oil: Around 73% of consumers are willing to pay a premium for olive oil with reduced pesticide use, with average premiums ranging from 22% in Italy to 26% in France above the standard price of a 1-liter bottle of conventional extra virgin olive oil.

Market Challenges

- Supply Concentration Risk: Over 90% of global olive cultivation, spanning more than 10 million hectares, is concentrated in the Mediterranean basin, with nearly half located in Greece, Italy, and Spain, creating concentrated exposure to Mediterranean climate, regulatory, and political risks.

- Consumer Education and Grade Confusion: Consumer confusion across virgin, extra virgin, refined, and pomace grades, compounded by inconsistent labeling and authenticity issues, constrains willingness-to-pay for premium grades, particularly in non-traditional markets.

Emerging Market Trends

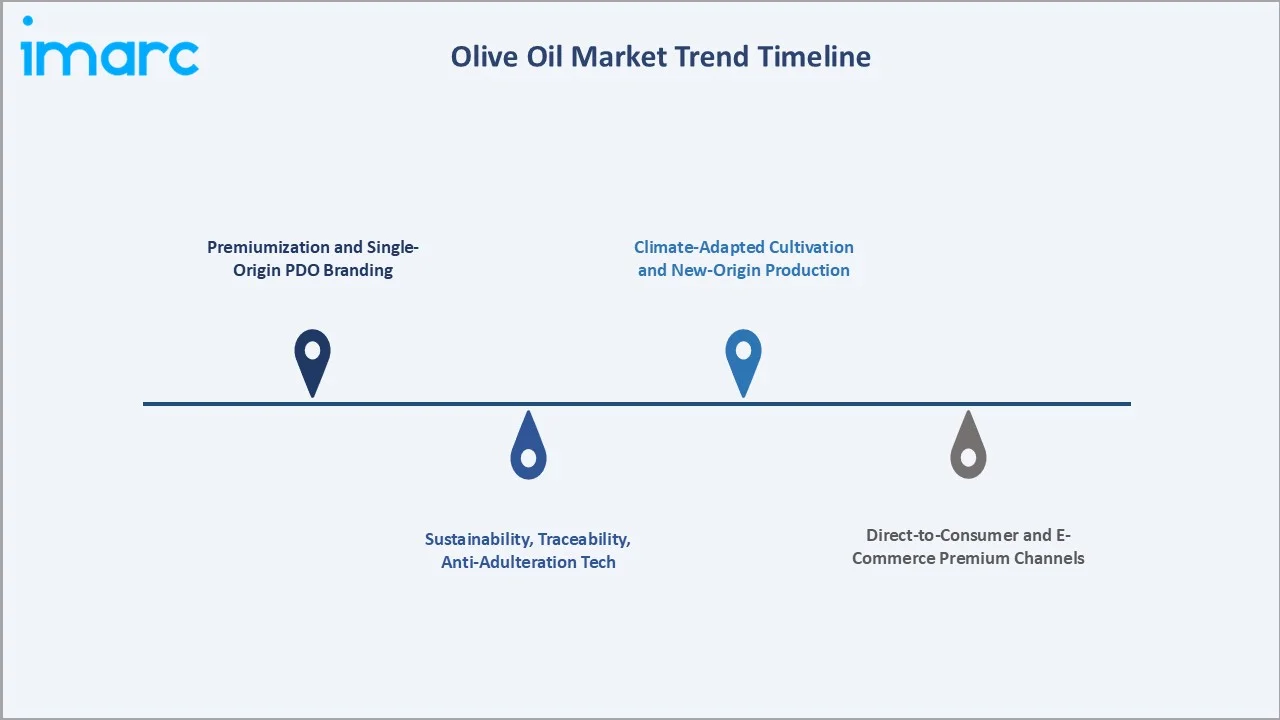

1. Premiumization and Single-Origin PDO Branding

Single-origin, single-estate, and Protected Designation of Origin (PDO) olive oils are commanding sustained premium positioning across mature markets. Spanish PDO regions (Sierra Mágina, Priego de Córdoba), Italian DOP designations (Toscano, Umbria), and Greek PGI labels (Kalamata, Lakonia) drive double-digit premiums and consumer willingness-to-pay for verified provenance.

2. Climate-Adapted Cultivation and New-Origin Production

California, Australia, Chile, Argentina, and South Africa have emerged as new-origin producers, with California Olive Ranch and Australian estate brands gaining international share. Climate-adapted cultivation and Mediterranean-equivalent terroirs are diversifying supply geography away from concentrated Mediterranean dependence.

3. Direct-to-Consumer and E-Commerce Premium Channels

Direct-to-consumer brands, Amazon's premium food category, and subscription-based olive oil clubs are scaling rapidly. Brands such as Brightland, Graza, and Fat Gold have built premium positioning through D2C channels emphasizing harvest dates, single-origin sourcing, and design-led packaging resonating with affluent millennial and Gen Z consumers.

4. Sustainability, Traceability, and Anti-Adulteration Technology

Blockchain-based traceability platforms, isotopic and NMR-based authentication, and supply chain transparency initiatives are emerging to address adulteration concerns. Major retailers and FMCG brands are deploying these technologies to verify provenance from grove to bottle, supporting premium positioning and consumer trust.

Industry Value Chain Analysis

The olive oil value chain spans olive grove cultivation through retail and food-service distribution, with significant value creation at the milling, blending, and brand-marketing stages. Mediterranean cooperatives, estate millers, and integrated brand owners capture differential margin depending on positioning across mass-market versus premium tiers.

|

Stage |

Key Players / Examples |

|

Olive Cultivation |

Mediterranean olive growers; emerging new-origin olive farms in temperate climates; agricultural cooperatives and olive-harvesting suppliers |

|

Milling & Extraction |

Local cooperative mills, estate millers, mechanical cold-press operators; centrifugation and decanter-based extraction facilities producing virgin and extra virgin oil grades |

|

Refining & Blending |

Large-scale olive oil refiners; multi-origin blenders; integrated bottlers handling neutralization, deodorization, and quality grading |

|

Bottling & Branding |

Heritage olive oil brand owners; premium and gourmet brand marketers; private-label co-packers; emerging direct-to-consumer brand operators |

|

Distribution & Retail |

Supermarkets and hypermarkets; convenience and specialty grocery stores; online retailers and e-commerce platforms; food-service operators and HoReCa channels |

Technology Landscape in the Olive Oil Industry

Cold-Press Mechanical Extraction

Two-phase and three-phase decanter centrifugation systems dominate modern olive oil milling, replacing traditional press-cloth systems. Continuous cold-extraction below 27°C preserves polyphenol content, flavor profile, and extra virgin qualification per International Olive Council standards.

Refining and Solvent Extraction

Olive pomace oil and lower-grade virgin oils are refined through neutralization, bleaching, and deodorization to produce refined olive oil for price-sensitive applications. Hexane solvent extraction recovers residual oil from pomace.

Quality Authentication and Adulteration Detection

Nuclear Magnetic Resonance (NMR), gas chromatography-mass spectrometry (GC-MS), and stable isotope ratio analysis are deployed to verify olive oil authenticity, detect adulteration, and authenticate single-origin and PDO claims.

Sustainable Processing and By-Product Valorization

Olive milling generates significant by-products including pomace, mill wastewater, and leaves. Emerging valorization technologies extract polyphenols (hydroxytyrosol, oleuropein) for nutraceutical and cosmetic applications, while pomace is used in biomass energy, animal feed, and biorefining.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Virgin Olive Oil |

61.9% |

2025 |

|

Distribution Channel |

Supermarkets & Hypermarkets |

56.8% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Europe |

63.8% |

2025 |

By Type

Virgin olive oil dominates the type segment with a 61.9% share in 2025. This category encompasses oils produced solely through mechanical extraction at temperatures preserving natural quality, with acidity levels typically between 0.8% and 2.0%. Virgin olive oil serves the broadest household culinary market, offering balanced flavor and price accessibility across mass-market grocery retail.

To access detailed market analysis, Request Sample

Extra virgin olive oil at 18.4% represents the premium type segment, defined by maximum 0.8% acidity, superior organoleptic qualities, and the strictest International Olive Council quality standards. This segment is the fastest-growing at approximately 4.6% CAGR, driven by health-conscious consumers, gourmet-cooking trends, and consumer education around polyphenol content.

By Distribution Channel

Supermarkets and hypermarkets command a 56.8% share in 2025, reflecting olive oil's status as a mainstream grocery staple. Large-format retailers including Walmart, Tesco, Carrefour, Mercadona, and Costco dedicate substantial shelf space to multi-tier olive oil portfolios spanning private-label, national-brand, and premium imported segments.

Online stores at 14.2% represent the fastest-growing distribution channel at approximately 8.4% CAGR, driven by Amazon's expanding premium food category, D2C brand growth, and subscription olive oil services. E-commerce enables provenance storytelling and harvest-date transparency that commands premium pricing.

Regional Market Insights

Europe's market leadership (63.8%, 2025) reflects the region's combined production dominance, established consumption culture, and export infrastructure. Over 90% of global olive cultivation is located in the Mediterranean basin, with strong Mediterranean dietary tradition, regulatory protection of PDO/PGI designations, and mature retail distribution sustaining the region's leadership.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

63.8% |

Dominant Spain, Italy, Greece production base; established Mediterranean dietary tradition; mature retail distribution; export hub for global markets |

|

North America |

14.7% |

Strong health-driven consumption growth; expanding Mediterranean diet adoption; rising premium and organic segment demand |

|

Asia-Pacific |

11.6% |

Fastest-growing region; rising per-capita consumption in China, Japan, South Korea; expanding affluent middle-class health awareness; growing premium gourmet segment |

|

Latin America |

5.4% |

Argentine and Chilean domestic production; growing Brazilian and Mexican consumer demand; rising premium retail availability |

|

Middle East & Africa |

4.5% |

Tunisian and Moroccan production base; GCC premium consumption growth; rising urban health-conscious middle-class demand |

Asia-Pacific at 11.6% represents the fastest-growing regional market at approximately 6.2% CAGR. China's per-capita olive oil consumption remains under 0.03 kg annually versus 7.5+ kg in Spain, indicating substantial growth headroom as urban affluent consumers adopt Mediterranean dietary practices.

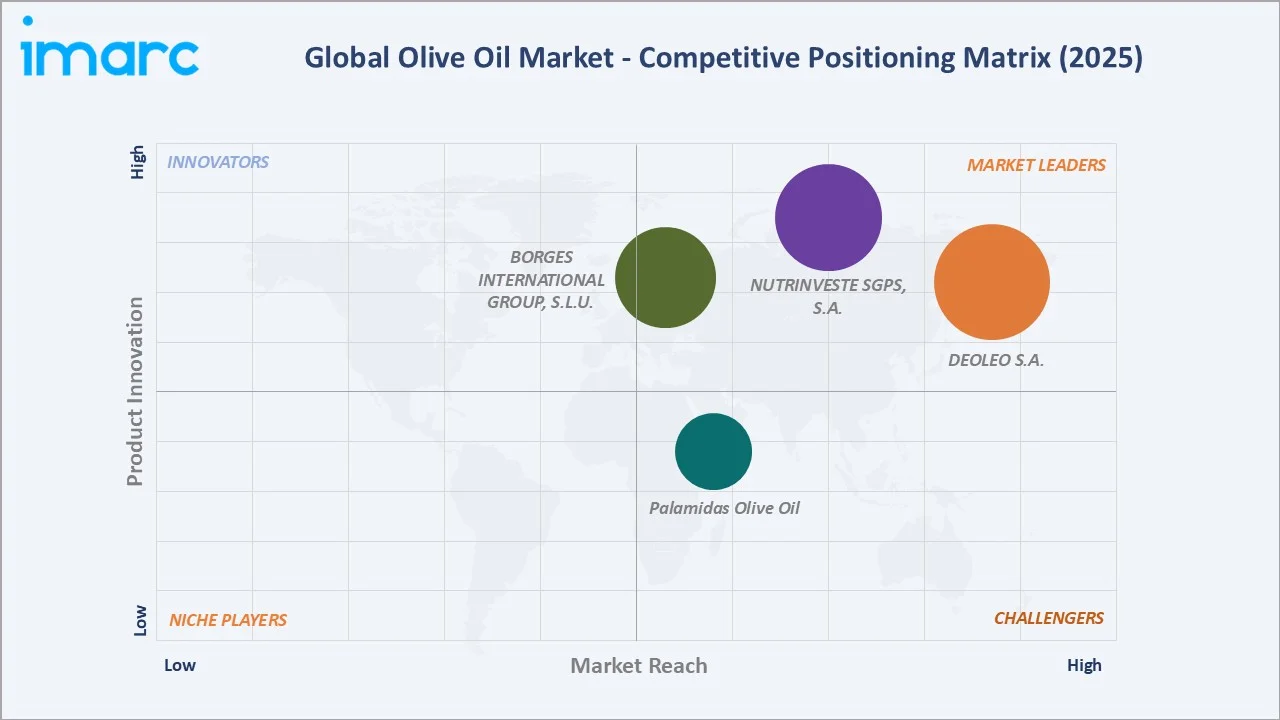

Competitive Landscape

The global olive oil market exhibits moderate concentration, with the top players (DEOLEO S.A., NUTRINVESTE SGPS, S.A., BORGES INTERNATIONAL GROUP, S.L.U, and Palamidas Olive Oil) collectively holding approximately 35–40% of global market revenue in 2025.

|

Company Name |

Brand Name / Portfolio |

Market Position |

Core Strength |

|

DEOLEO S.A. |

Bertolli, Carapelli, Carbonell, Hojiblanca, Fígaro |

Market Leader |

World's largest olive oil bottler; global brand portfolio; mass-market and premium reach |

|

NUTRINVESTE SGPS, S.A. |

Oliveira da Serra, Andorinha, Fontoliva, Olivari, SOLEADA, FLOR DE OLIVO |

Market Leader |

Vertically integrated; private-label leadership |

|

BORGES INTERNATIONAL GROUP, S.L.U. |

Borges, Star, Capricho Andaluz, ITLV, Tramier |

Market Leader |

Spanish-heritage brand; multi-category olive oil portfolio |

|

Palamidas Olive Oil |

Palamidas |

Challenger |

Turkey’s established manufacturer of olive oils, uses cold extraction method and controlled bottling. |

Rising demand for healthier cooking oils and Mediterranean diets is encouraging producers to diversify portfolios with flavored, cold-pressed, and high-polyphenol olive oil variants, while private-label competition from supermarkets continues to intensify pricing pressure across global markets.

Key Company Profiles

DEOLEO S.A.

DEOLEO S.A. is the world's largest olive oil bottler and brand owner, with global operations across Europe, the Americas, and Asia-Pacific and brand presence in more than 60 countries.

- Product Portfolio: Bertolli, Carapelli, Carbonell, Hojiblanca, and Fígaro, among others.

- Recent Developments: In February 2026, DEOLEO S.A. reported EBITDA rising 50% year-on-year to EUR 50 million and net profit reaching EUR 20 million, driven by its “EVOO-lution” strategic roadmap and recovering olive oil demand.

- Strategic Focus: Global brand portfolio leadership; premiumization through Bertolli and Carapelli; sustainability investments; Asia-Pacific expansion.

NUTRINVESTE SGPS, S.A.

NUTRINVESTE SGPS, S.A. operates Sovena Group, a vertically integrated olive oil major spanning olive grove ownership, milling, refining, bottling, and distribution. The company is the world's largest private-label olive oil supplier.

- Brand Portfolio: Oliveira da Serra, Andorinha, Olivari, Fontoliva, SOLEADA, and FLOR DE OLIVO.

- Recent Developments: In February 2025, Sovena Group announced that it achieved 100% renewable electricity usage across its olive oil production and processing operations in the Iberian Peninsula, reinforcing its decarbonization and sustainability strategy.

- Strategic Focus: Vertical integration across cultivation-to-retail; private-label leadership; Iberian and Americas presence; sustainability-driven differentiation.

Market Concentration Analysis

The global olive oil market exhibits moderate concentration, with the top four players holding approximately 35–40% of revenue in 2025. The next tier includes regional brands which collectively account for an additional 20–25% of share. Private-label and regional brands complete the landscape, particularly in European mass retail.

Consolidation patterns are concentrated around vertical integration, brand portfolio acquisitions, and D2C brand emergence. Established players invest in supply traceability, sustainability certifications, and digital channels to differentiate premium offerings, while new-origin producers in California, Australia, and Chile diversify global supply geography.

Investment & Growth Opportunities

Fastest Growing Segments

Online stores (~8.4% CAGR), Asia-Pacific consumption (~6.2% CAGR), extra virgin olive oil (~4.6% CAGR), and organic/PDO premium grades (~7% CAGR) represent the highest-growth investment vectors through 2034. These subcategories together address a combined incremental opportunity of approximately USD 3 Billion by 2034.

Emerging Market Expansion

China, India, Japan, South Korea, and the GCC represent the highest-growth emerging consumption markets. Per-capita consumption gaps versus Mediterranean baselines indicate decade-long structural demand growth potential as health-driven dietary practices expand among urban affluent consumers.

New-Origin Production and Sustainability Investment

- California, Australia, Chile, and Argentina are emerging as new-origin producer regions, attracting investment in olive grove cultivation, modern milling, and premium brand-building.

- Organic, PDO-certified, and sustainability-verified olive oils command 25–40% price premiums and represent the most attractive premium investment segments for established and emerging brands.

- Direct-to-consumer brands such as Brightland, Graza, and Fat Gold demonstrate the viability of premium positioning through e-commerce, design-led packaging, and storytelling-based consumer engagement.

Future Market Outlook (2026-2034)

The global olive oil market is positioned for steady expansion through 2034. From USD 15.67 Billion in 2025, the market is projected to reach USD 21.59 Billion by 2034, representing incremental value creation of USD 5.92 Billion at a CAGR of 3.52%. This trajectory is underpinned by sustained health-driven consumption, premiumization in mature markets, and emerging-market expansion across Asia-Pacific.

Three structural shifts will define 2026–2034: accelerating consumer trade-up to extra virgin and PDO-certified grades in mature markets; rapid scale-up of e-commerce and direct-to-consumer channels capturing premium consumers; and diversification of global supply through new-origin production in California, Australia, and Chile reducing Mediterranean concentration risk.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 100 industry participants in 2024–2025, including olive growers, mill operators, refining and bottling executives, brand owners, retail buyers, and food-service procurement specialists across Spain, Italy, Greece, the US, China, and the UK.

Secondary Research

Secondary research encompassed International Olive Council statistics, EU agricultural data, USDA FAS reports, company annual reports, retail audit data, and industry publications (Olive Oil Times, Mintec, ICIS).

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating global olive oil production data, regional consumption trends, type-level price trajectories, and channel-mix evolution. A base-case CAGR of 3.52% reflects consensus estimates validated against International Olive Council projections, retail point-of-sale data, and historical consumption growth patterns from FY2020 to FY2025.

Olive Oil Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Virgin Olive Oil, Refined Olive Oil, Extra Virgin Olive Oil, Olive Pomace Oil, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Applications Covered | Food and Beverage, Pharmaceuticals, Cosmetics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | DEOLEO S.A., NUTRINVESTE SGPS, S.A., BORGES INTERNATIONAL GROUP, S.L.U., Palamidas Olive Oil, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the olive oil market from 2020-2034.

- The olive oil market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the olive oil industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Olive Oil Market Report

The global olive oil market reached USD 15.67 Billion in 2025 and is projected to reach USD 21.59 Billion by 2034.

The market is expected to grow at a CAGR of 3.52% during 2026-2034, driven by Mediterranean diet adoption, premiumization, e-commerce expansion, and Asia-Pacific consumption growth.

Europe leads with a 63.8% share in 2025, anchored by Spain (producing over 1.4 million tons annually, Italy, and Greece together producing the majority of global olive oil output.

Virgin olive oil dominates with a 61.9% share in 2025, supported by household culinary use and broad price-point accessibility across mass-market retail.

Supermarkets and hypermarkets hold the largest share at 56.8%, reflecting olive oil's status as a mainstream grocery staple.

Key players include DEOLEO S.A., NUTRINVESTE SGPS, S.A., BORGES INTERNATIONAL GROUP, S.L.U., and Palamidas Olive Oil.

Extra virgin olive oil is growing at approximately 4.6% CAGR driven by health-conscious premium consumers, accelerating Mediterranean diet adoption in North America and Asia-Pacific, and rising consumer education around polyphenol content and provenance.

Key challenges include climate volatility and Mediterranean harvest shortfalls, high price volatility versus substitute edible oils, adulteration and authenticity concerns, supply concentration risk in Spain/Italy/Greece, and consumer confusion across olive oil grades.

Online and direct-to-consumer channels, Asia-Pacific consumption expansion, extra virgin and PDO premium grades, organic certified production, and new-origin cultivation in California, Australia, and Chile represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)