India Online Gambling Market Size, Share, Trends and Forecast by Game Type, Device, and Region, 2026-2034

India Online Gambling Market Summary:

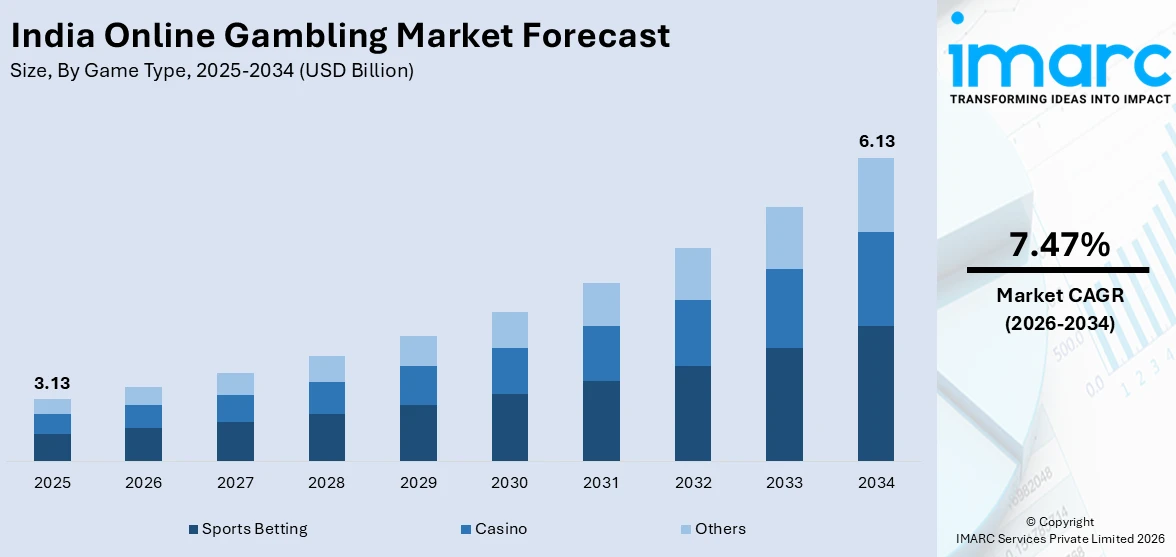

The India online gambling market size was valued at USD 3.13 Billion in 2025 and is projected to reach USD 6.13 Billion by 2034, growing at a compound annual growth rate of 7.47% from 2026-2034.

The India online gambling market is expanding steadily, fueled by rising smartphone adoption, affordable mobile internet plans, and a youthful demographic increasingly drawn to digital entertainment. The proliferation of secure digital payment solutions, including real-time transfer platforms, has simplified transactional processes across gambling platforms. Growing consumer interest in interactive sports engagement, particularly around cricket and emerging esports formats, continues to bolster participation. Evolving platform technologies and expanding accessibility through mobile-first designs are further reshaping the competitive environment, driving broader user engagement and strengthening the India online gambling market share.

Key Takeaways and Insights:

- By Game Type: Sports betting dominates the market with a share of 52.0% in 2025, driven by the deep-rooted cricket culture and surging popularity of fantasy sports platforms that blend sports knowledge with competitive wagering.

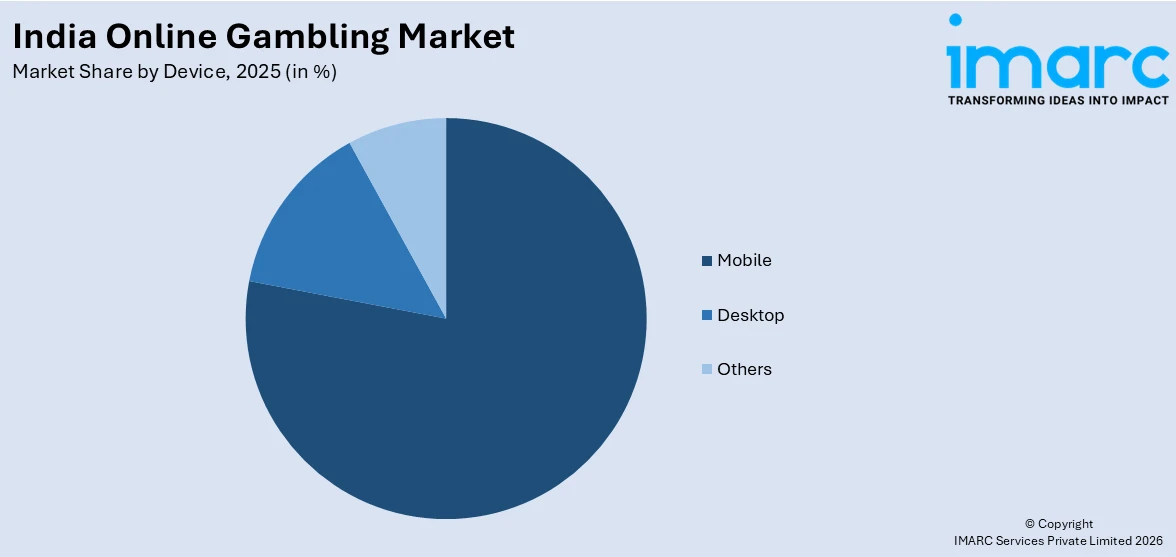

- By Device: Mobile leads the market with a share of 78.0% in 2025, reflecting India’s mobile-first digital ecosystem where affordable smartphones and expansive network coverage enable ubiquitous access to online gambling platforms.

- By Region: West and Central India represents the largest segment with a market share of 36.0% in 2025, supported by high urbanization rates, concentrated economic activity in Maharashtra and Gujarat, and greater digital infrastructure penetration.

- Key Players: The India online gambling market features a dynamic competitive landscape comprising both international operators and domestic platforms competing through technological innovation, localized content offerings, multilingual interfaces, and strategic partnerships with major sporting leagues to capture diverse user segments.

To get more information on this market Request Sample

The India online gambling market is experiencing transformative growth as digital infrastructure matures across the country and a young, tech-savvy population gravitates toward interactive entertainment formats. The India gaming market size was valued at USD 5.91 Billion in 2025 and is projected to reach USD 16.72 Billion by 2034, growing at a compound annual growth rate of 14.6% from 2026-2034, despite the imposition of heightened taxation measures on gaming activities. Real-money gaming remains the primary revenue contributor, while in-app purchases represent the fastest-growing monetization segment. The convergence of cricket fandom with digital betting has catalyzed platform innovation, with fantasy sports contests during the Indian Premier League season attracting tens of millions of active users. Concurrently, the expansion of India’s Unified Payments Interface, which processed over 228 billion transactions in 2025, has created a seamless transactional backbone that underpins secure and convenient participation in online gambling activities across the country.

India Online Gambling Market Trends:

Rise of Mobile-First Gambling Platforms and Progressive Web Applications

The India online gambling market is witnessing a pronounced shift toward mobile-optimized platforms as operators design applications specifically for smartphone users who represent most online gamblers. Progressive web applications and lightweight mobile interfaces are eliminating traditional barriers like large download sizes and device compatibility constraints. India had approximately 660 million smartphone users in 2024, and the proliferation of affordable devices continues to expand the addressable market. Additionally, enhanced mobile payment integration and faster internet connectivity are further strengthening real-time betting participation and seamless in-app wagering experiences.

Integration of Fantasy Sports with Traditional Sports Betting Formats

Fantasy sports platforms are increasingly integrating elements of traditional betting, creating hybrid engagement models that combine sports analysis with competitive wagering. These platforms enable users to assemble virtual teams and earn rewards based on real-match performances, sustaining engagement throughout sporting seasons. Strategic partnerships with major sporting leagues have strengthened brand visibility and mainstream acceptance of fantasy formats. This convergence is transforming consumer interaction with online gambling by introducing more skill-based, analytical participation models. The trend is particularly appealing to younger demographics who prefer interactive, data-driven, and strategy-focused wagering experiences over purely chance-based betting formats.

Growth of Live Casino and Real-Time Interactive Gambling Experiences

Live casino offerings are gaining strong momentum as platforms combine real-time streaming technology with interactive dealer-led experiences, recreating the ambiance of physical casinos in digital environments. Players can engage in card games, roulette, and other table formats with live hosts, enhancing transparency and user trust. The broader popularity of live-streamed competitive gaming events further reflects increasing consumer interest in real-time, interactive digital entertainment. This shift toward immersive, visually engaging formats is influencing the evolution of online gambling platforms, as operators prioritize instant engagement, social interaction, and dynamic participation experiences.

Market Outlook 2026-2034:

The Indian online gambling market is positioned for sustained expansion as technological infrastructure improvements, maturing digital payment ecosystems, and rising youth engagement converge to drive platform growth. Operators are increasingly deploying artificial intelligence to deliver personalized user experiences and responsible gambling features, while blockchain-based solutions are being explored to enable transparent transaction processing. Regulatory clarity at both central and state levels will play a critical role in shaping the market’s trajectory. The market generated a revenue of USD 3.13 Billion in 2025 and is projected to reach a revenue of USD 6.13 Billion by 2034, growing at a compound annual growth rate of 7.47% from 2026-2034.

India Online Gambling Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Game Type |

Sports Betting |

52.0% |

|

Device |

Mobile |

78.0% |

|

Region |

West and Central India |

36.0% |

Game Type Insights:

- Sports Betting

- Football

- Horse Racing

- E-Sports

- Others

- Casino

- Live Casino

- Baccarat

- Blackjack

- Poker

- Slots

- Others

- Others

Sports betting dominates the market with a share of 52.0% of India online gambling market in 2025.

Sports betting has established itself as the cornerstone of the India online gambling market, driven predominantly by the nation’s passionate cricket culture and the rapid proliferation of fantasy sports platforms. The Indian Premier League serves as the primary catalyst for betting activity, with platforms reporting surges in user engagement and transaction volumes during the tournament season. Fantasy sports platforms collectively generated approximately USD 510 million in gross gaming revenue during IPL 2024, reflecting a twenty-seven percent year-on-year increase. Football, horse racing, and emerging esports categories further diversify the sports betting landscape.

The segment’s growth is supported by continuous platform innovation, including live in-play betting options, real-time data analytics, and personalized odds engines that enhance engagement and retention. Operators are increasingly appealing to younger audiences through gamification features, interactive social elements, and seamless integration with widely used digital payment systems. Strategic partnerships with major sports leagues have become a key competitive tool, strengthening brand visibility and user acquisition. These collaborations highlight the importance of sports-linked wagering rights in expanding market presence and driving sustained revenue growth across the India online gambling ecosystem.

Device Insights:

Access the comprehensive market breakdown Request Sample

- Desktop

- Mobile

- Others

Mobile leads the market with a share of 78.0% of total India online gambling market in 2025.

Mobile devices have become the leading access point for online gambling in India, reflecting the country’s mobile-first digital environment where affordable smartphones and expanding network coverage have widened participation. Strong growth in internet adoption and mobile broadband usage has created a foundation for seamless digital engagement. Increased data consumption capacity supports bandwidth-intensive features such as live streaming, in-play wagering, and real-time casino gameplay. This connectivity landscape enables operators to deliver responsive, high-quality platforms optimized for smartphones, strengthening user acquisition and engagement across both metropolitan and emerging markets.

The dominance of mobile gambling is further strengthened by the integration of India’s Unified Payments Interface (UPI) into gaming platforms, enabling smooth and instant deposits and withdrawals within mobile applications. The widespread acceptance of UPI in digital commerce has enhanced user confidence in cashless transactions. Operators have designed lightweight applications compatible with varied devices and network conditions, ensuring accessibility across diverse user segments. Additionally, push notifications, loyalty programs, and personalized promotional strategies help sustain engagement, improve retention, and maximize lifetime value throughout the customer journey.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

West and Central India represents the largest share at 36.0% of the total India online gambling market in 2025.

West and Central India leads the market, anchored by the economic dynamism and high urbanization of Maharashtra and Gujarat. Mumbai, as the nation’s financial capital, concentrates a large population of digitally active professionals with higher disposable incomes and strong engagement with digital entertainment platforms. The region benefits from superior digital infrastructure, extensive broadband and mobile network penetration, and a well-developed fintech ecosystem that facilitates seamless transactions. Maharashtra’s relatively progressive stance on certain forms of skill-based gaming has also contributed to a more favorable operating environment for platform operators.

The concentration of India’s entertainment and technology industries in western urban centers creates a spillover effect that drives digital adoption across surrounding markets. Gujarat’s growing technology corridor and entrepreneurial culture further support platform engagement. The region’s demographic profile, characterized by a large young working population and high smartphone penetration, aligns strongly with the target user base for online gambling platforms. Operators have localized content in Marathi, Gujarati, and Hindi to maximize regional reach and user retention.

Market Dynamics:

Growth Drivers:

Why is the India Online Gambling Market Growing?

Rapid Smartphone Penetration and Affordable Internet Access

India’s rapidly expanding digital infrastructure serves as the primary enabler for online gambling market growth. The proliferation of affordable smartphones and competitive mobile data pricing has brought internet access to hundreds of millions of previously unconnected consumers, creating a vast addressable market for digital entertainment platforms. According to the Press Information Bureau, as of April 2024, approximately 95.15 percent of India’s 6,44,131 villages had access to 3G or 4G connectivity, demonstrating the depth of mobile network reach even in semi-urban and rural areas. India had over 751.5 million internet users at the start of 2024, with mobile connections exceeding 1.12 billion. The ongoing rollout of 5G networks is further enhancing connectivity speeds and reducing latency, enabling richer gambling experiences including live streaming and real-time interactive gaming formats.

Young Demographics and Rising Digital Entertainment Adoption

India’s demographic composition represents a powerful structural driver for the online gambling market, with a median age of approximately 28.8 years in 2025 and roughly sixty-five percent of the population below the age of thirty-five. This youthful population is inherently tech-savvy, digitally connected, and receptive to interactive entertainment formats that blend competition with potential financial rewards. India had approximately 591 million gamers in 2024, representing about one-fifth of the global gaming population, with the vast majority engaging through mobile platforms. Rising disposable incomes among the urban middle class and growing familiarity with digital commerce further support willingness to participate in online gambling activities, making India one of the most attractive emerging markets for global and domestic gaming operators.

Expansion of Secure Digital Payment Infrastructure

The maturation of India’s digital payment ecosystem, led by the Unified Payments Interface (UPI), has significantly improved the transaction experience on online gambling platforms. UPI has become the backbone of digital payments, offering users a fast, secure, and seamless method for transferring funds. Its integration alongside e-wallets and credit-linked payment features within gambling applications enables instant deposits and quick withdrawals, enhancing convenience and trust. These advancements have lowered transactional barriers, strengthened payment reliability, and improved user conversion rates, allowing operators to deliver smoother onboarding experiences and sustain higher levels of platform engagement.

Market Restraints:

What Challenges the India Online Gambling Market is Facing?

Fragmented and Evolving Regulatory Framework

The legal framework of online gambling in India is still inconsistent, as gambling and betting are state subjects under the Constitution, which results in a problem of diverse approaches to various states. Some states have embraced the progressive approach to skill-based gaming, but others have placed a total prohibition on it. The adoption of the Promotion and Regulation of Online Gaming Act in September 2025 presented a national ban on online money games, which left operators and investors in the changing regulatory landscape in a lot of confusion.

Heavy Taxation Burden on Online Gaming Activities

The imposition of a higher Goods and Services Tax on online gaming deposits has increased operational costs for operators and reduced player payouts. Proposed further tax hikes have intensified concerns about profitability, investment sustainability, and the risk of users shifting toward unregulated offshore platforms operating outside the domestic taxation framework.

Risk of Problem Gambling and Social Concerns

Growing participation in online gambling has raised concerns about addictive behavior, particularly among younger users who are disproportionately exposed to digital gambling platforms. Issues such as debt accumulation, mental health impacts, and inadequate responsible gambling mechanisms have drawn scrutiny from regulators, health authorities, and consumer advocacy groups. These social concerns are prompting stricter age verification requirements, spending limits, and self-exclusion mandates that may constrain market expansion.

Competitive Landscape:

The India online gambling market is characterized by an intensely competitive environment where international operators and domestic platforms vie for market share through technological differentiation, localized offerings, and strategic partnerships. Competition centers on platform reliability, breadth of game offerings, odds competitiveness, and the quality of mobile user experiences. Operators are investing in artificial intelligence, machine learning, and data analytics to personalize recommendations, optimize odds, and detect fraudulent activities. Strategic collaborations with major sporting leagues and franchise teams have become essential for brand visibility and customer acquisition. The market also features significant investment in multilingual support and regional content to penetrate diverse geographic and linguistic segments across India.

Recent Developments:

- In March 2024, My11Circle, a fantasy sports platform from Games24x7, secured a five-year partnership with the Indian Premier League by outbidding the incumbent Dream11 with a total commitment of Rs 625 crore. The partnership established My11Circle as the official fantasy sports partner starting from IPL 2024, signaling intensified competition in the fantasy sports segment.

India Online Gambling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Game Types Covered |

|

| Devices Covered | Desktop, Mobile, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Online Gambling Market Report

The India online gambling market size was valued at USD 3.13 Billion in 2025.

The India online gambling market is expected to grow at a compound annual growth rate of 7.47% from 2026-2034 to reach USD 6.13 Billion by 2034.

Sports betting held the largest revenue share at 52.0% in 2025, driven by India’s deep-rooted cricket culture, the expanding popularity of fantasy sports platforms, and growing consumer engagement with live in-play betting formats during major sporting events.

Key factors driving the India online gambling market include rapid smartphone penetration and affordable internet access, a youthful and digitally engaged demographic, expansion of secure digital payment infrastructure, rising popularity of fantasy sports, and growing consumer preference for mobile-first entertainment platforms.

Major challenges include a fragmented regulatory landscape with evolving state and central legislation, heavy taxation through the twenty-eight percent GST on gaming deposits, risk of problem gambling among younger users, migration to unregulated offshore platforms, and inconsistent enforcement across jurisdictions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)