India Online Retail Market Size, Share, Trends and Forecast by Product Category, Payment Method, Sales Channel, and Region, 2026-2034

India Online Retail Market Size, Share, Trends & Forecast (2026-2034)

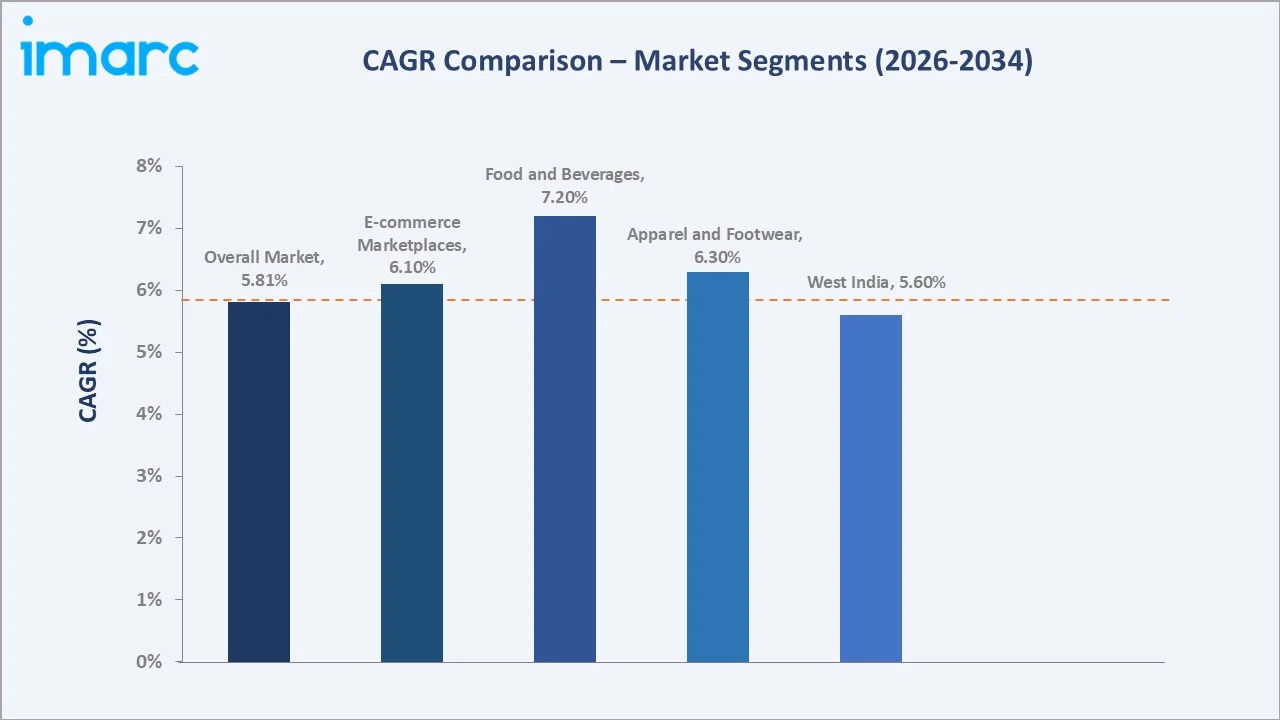

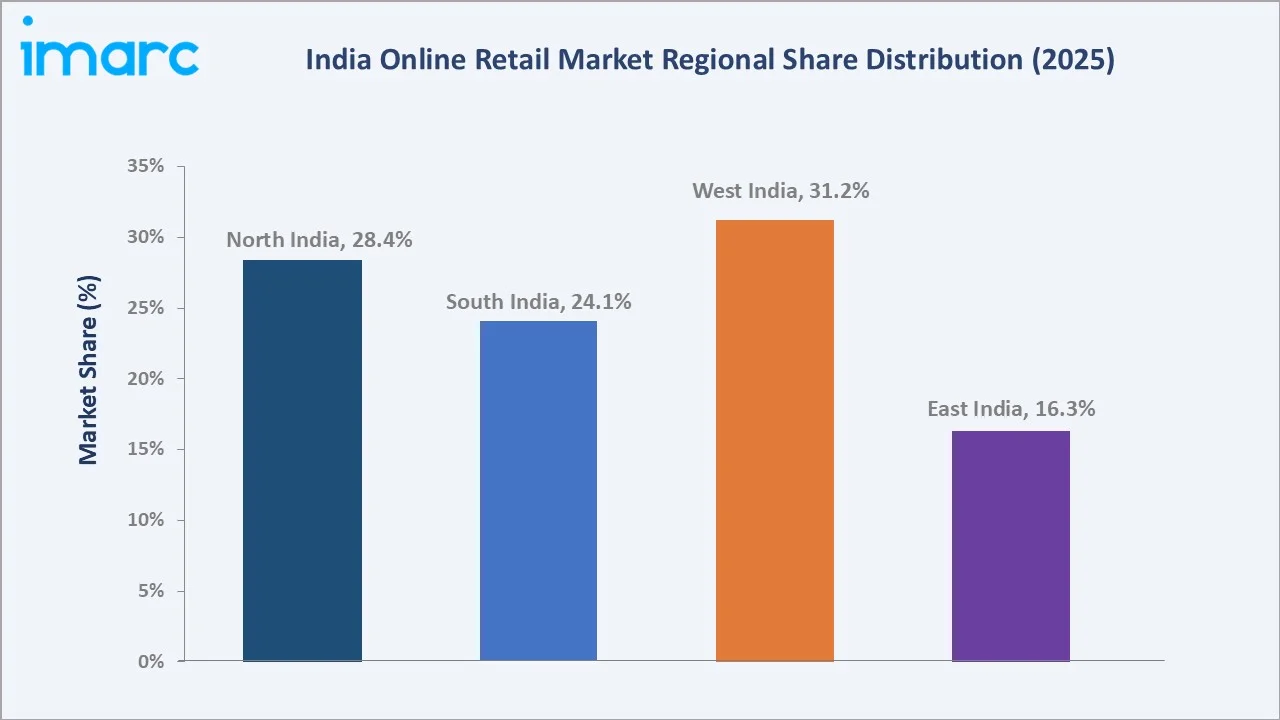

The India online retail market reached USD 217.16 Billion in 2025 and is projected to reach USD 366.42 Billion by 2034, growing at a CAGR of 5.81% during 2026-2034. The market is driven by rising internet penetration, rapid adoption of digital payments via UPI, expanding logistics infrastructure, and government-backed initiatives such as the Open Network for Digital Commerce (ONDC) and the Government e-Marketplace (GeM). India's internet user base is anticipated to exceed 900 million by 2025, fueling the accessibility of e-commerce platforms across urban and rural areas. E-Commerce marketplaces lead at 81.3% while electronics and appliances dominate product categories at 28.6%. West India commands the highest regional share at 31.2%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 217.16 Billion |

|

Forecast Market Size (2034) |

USD 366.42 Billion |

|

CAGR (2026-2034) |

5.81% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (31.2%, 2025) |

|

Fastest Growing Segment |

Food & Beverages (~7.2% CAGR) |

|

Dominant Sales Channel |

E-Commerce Marketplaces (81.3%, 2025) |

|

Dominant Product Category |

Electronics & Appliances (28.6%, 2025) |

The India online retail market expanded from USD 163.77 Billion in 2020 to USD 217.16 Billion in 2025, anchored at USD 287.95 Billion in 2030, and forecast to reach USD 366.42 Billion by 2034. This growth trajectory reflects accelerating smartphone adoption, expanding digital payment ecosystems, and post-COVID consumer behavior permanently shifting toward online channels. India has emerged as the world's second-largest online shopper base, positioning it as one of the most commercially significant digital commerce markets globally.

To get more information on this market, Request Sample

The e-commerce marketplaces segment, led by platforms such as Amazon India, Flipkart, and Reliance JioMart, commands 81.3% of total market revenue in 2025. Brand-specific websites have grown consistently at 4.8% CAGR, underpinned by D2C brand expansion strategies. Food and Beverages, growing at ~7.2% CAGR, emerges as the fastest-growing product category.

Executive Summary

The India online retail market at USD 217.16 Billion in 2025 represents one of the largest and most dynamic digital commerce ecosystems in Asia. The market's structural growth is anchored by India's population scale, with over 1.4 billion consumers, and an expanding middle class with rising disposable incomes. India's digital infrastructure, particularly the Unified Payments Interface (UPI), processed over 18.68 billion transactions in May 2025, providing a seamless payment backbone for e-commerce growth.

The market is projected to reach USD 287.95 Billion by 2030 and USD 366.42 Billion by 2034, at a CAGR of 5.81% during 2026-2034. E-Commerce Marketplaces dominate at 81.3% due to network effects, competitive pricing, and extensive product assortments. Electronics and Appliances leads product categories at 28.6%, driven by India's growing consumer electronics appetite. West India holds the highest regional share at 31.2%, reflecting Mumbai's high-income consumer base and Maharashtra's extensive digital adoption.

Government-backed programs, including ONDC, which reached over 1,200 cities and 7 lakh+ sellers by early 2025, and the GeM platform with cumulative GMV of approximately USD 171.3 Billion as of August 2025, are democratizing digital commerce across India's Tier-2 and Tier-3 cities. The market outlook through 2034 remains highly constructive, supported by AI-driven personalization, rapid logistics expansion, and increasing cross-border e-commerce activity.

Key Market Insights

|

Insight |

Data |

|

Dominant Sales Channel |

E-Commerce Marketplaces - 81.3% share (2025) |

|

Dominant Product Category |

Electronics & Appliances - 28.6% market share (2025) |

|

Leading Region |

West India - 31.2% share (2025) |

|

Fastest Growing Product Segment |

Food & Beverages (~7.2% CAGR, 2026-2034) |

|

Top Companies |

Amazon.com, Inc., Walmart Inc., Reliance Retail Ventures Limited (RRVL), Tata Group, and Swiggy |

|

Key Market Opportunity |

ONDC network expansion across 1,200+ cities; D2C brand scaling; quick commerce penetration |

Key Analytical Observations Supporting the Above Data:

- E-Commerce Marketplaces at 81.3% (2025): Marketplace dominance stems from unmatched product depth, competitive pricing algorithms, established seller networks, and superior logistics capabilities. Platforms like Amazon India and Flipkart attract hundreds of millions of monthly active users through aggressive customer acquisition and loyalty programs.

- Electronics & Appliances at 28.6% (2025): The category leads due to India's growing aspirational consumer class investing in smartphones, laptops, and home appliances. Festival season sales on platforms such as Flipkart Big Billion Days and Amazon Great Indian Festival drive disproportionate category volumes.

- West India at 31.2% (2025): West India's leadership is powered by Mumbai's high-income urban demographic, Pune's tech-educated workforce, and Gujarat's strong e-commerce adoption among business communities. The region benefits from superior last-mile logistics infrastructure and high digital payment penetration.

- Food & Beverages as the fastest-growing category: The quick commerce revolution, led by Swiggy Instamart, Blinkit, and BigBasket, is restructuring grocery consumption habits. Swiggy Instamart expanded to 76 cities by January 2025, and the segment is benefiting from India's convenience-first urban consumer shift.

- ONDC as a structural market enabler: The Open Network for Digital Commerce, launched by DPIIT, has onboarded over 3,70,000 sellers as of March 2024, targeting MSMEs in Tier-4 and rural belts and fundamentally expanding the addressable seller base for online retail.

India Online Retail Market Overview

India's online retail market encompasses the sale of goods and services through internet-based platforms, including multi-brand e-commerce marketplaces, brand-specific D2C websites, quick commerce apps, and social commerce channels. The ecosystem integrates product manufacturers, third-party sellers, logistics providers, payment gateways, and technology infrastructure.

Macroeconomic factors driving structural growth include India's expanding middle-class population, rising per capita incomes, accelerating urbanization, and government investments in digital public infrastructure. The India Brand Equity Foundation notes that Reliance Industries has highlighted India's trajectory to become the world's third-largest retail market by 2030, with government initiatives boosting disposable incomes and digital consumption.

Market Dynamics

To evaluate market opportunities, Request Sample

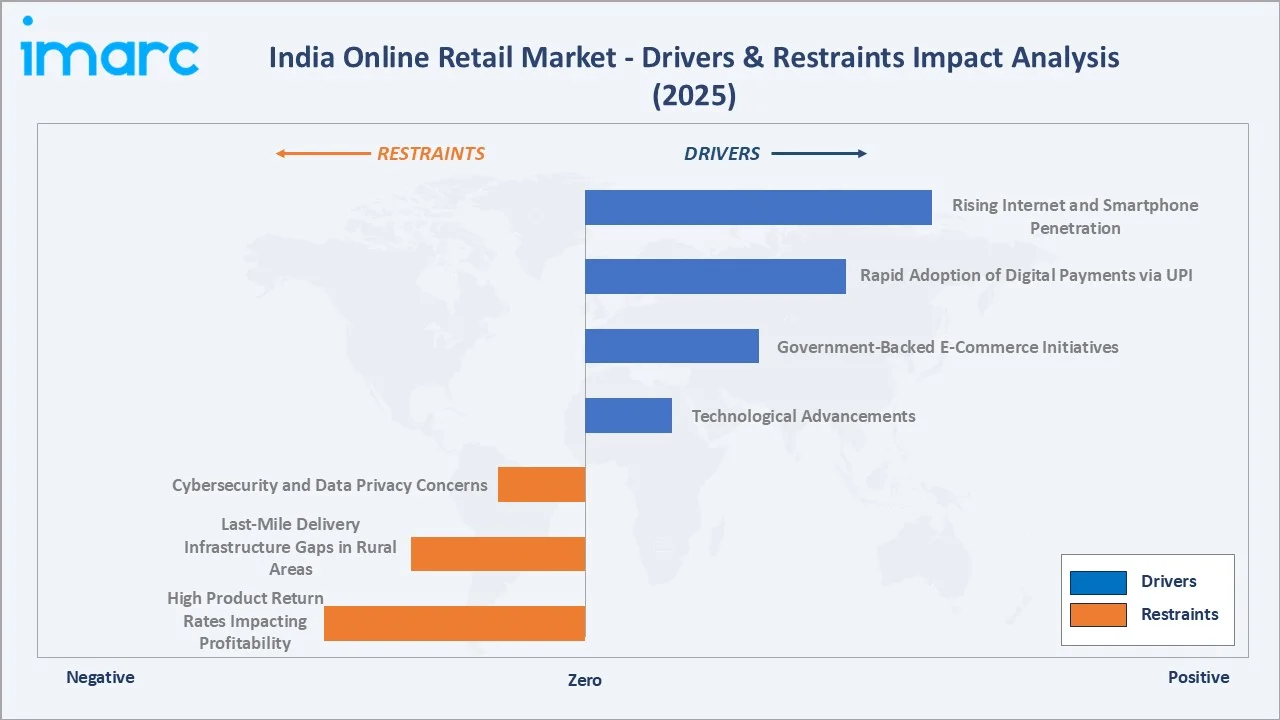

Market Drivers

- Rising Internet and Smartphone Penetration: India's internet user base is anticipated to exceed 1 billion by 2026, fueled by affordable smartphones and low-cost data plans from providers such as Jio. Affordable mobile internet has been a catalyst for a drastic growth in the value of mobile retail e-commerce since 2020. Customers from Tier-2 and Tier-3 cities are rapidly adopting online shopping. Increased connectivity is bridging the urban-rural digital divide, unlocking hundreds of millions of new e-commerce consumers annually.

- Rapid Adoption of Digital Payments via UPI: India's Unified Payments Interface (UPI) processed over 18.68 billion transactions in May 2025, creating a frictionless payment backbone for online retail. Digital payment adoption has directly increased checkout conversion rates and expanded the online consumer base to previously unbanked populations. The government's Digital India initiative continues to push payment infrastructure into rural markets.

- Government-Backed E-Commerce Initiatives: The Open Network for Digital Commerce (ONDC), launched by DPIIT, onboarded over 3,70,000 sellers as of March 2024, targeting Tier-4 and rural markets. The Government e-Marketplace (GeM) generated cumulative GMV of approximately USD 171.3 Billion as of August 2025, per Press Information Bureau data, showcasing the scale of digitized procurement. These initiatives structurally expand both the seller and buyer bases for online retail.

- Technological Advancements: AI, AR, and Personalization: AI-driven recommendation engines, augmented reality product trials, and ML-based inventory optimization are improving conversion rates and reducing return losses. In December 2024, Gurugram-based generative AI startup CurveAi launched DealSpy, India's first AI-powered shopping agent suite, providing real-time deal discovery across platforms. Voice search, chatbots, and live-stream shopping are further catalyzing engagement across consumer segments.

Market Restraints

- Cybersecurity and Data Privacy Concerns: With e-commerce platforms handling sensitive consumer financial data, the frequency of cyber breaches and data theft incidents is dampening consumer trust. India's evolving Digital Personal Data Protection (DPDP) Act creates compliance uncertainty for platforms. Consumer skepticism around data privacy, particularly in Tier-1 cities with digitally aware populations, limits the willingness to store payment credentials and share personal information online.

- Last-Mile Delivery Infrastructure Gaps in Rural Areas: While urban logistics networks are maturing, rural India continues to face challenges in last-mile delivery reliability, return logistics, and cold-chain for perishables. Online retailers currently extend delivery to only 15,000-20,000 pin codes out of approximately 100,000 in the country, limiting geographic market reach and suppressing demand from underserved areas.

- High Product Return Rates Impacting Profitability: India's online retail market records significant return rates, particularly in apparel and footwear (28-35%), driven by sizing inconsistencies, quality mismatches, and liberal return policies. High reverse logistics costs erode seller margins and contribute to unit economics challenges for marketplace platforms.

Market Opportunities

- Tier-2 and Tier-3 City E-Commerce Expansion: Tier-3 cities increased their share of e-commerce from 34.2% in 2021 to 41.5% in 2022, surpassing Tier-1 cities. Growing affluence, improved logistics, and localized content in regional languages are making smaller cities the next major growth frontier. E-commerce platforms investing in regional language support and vernacular content stand to capture disproportionate market share in the next decade.

- Quick Commerce and 10-Minute Delivery Revolution: The instant delivery segment, serviced by Blinkit, Swiggy Instamart, and Zepto, is redefining consumer expectations around delivery speed. Swiggy Instamart launched a standalone application in January 2025 and expanded to 76 cities, signaling the structural permanence of quick commerce. The category creates new revenue streams and consumer touchpoints beyond traditional e-commerce.

- Social Commerce and Influencer-Driven Sales: Social media platforms are fostering online shopping through influencer-driven marketing and direct product promotions. Live-stream shopping and interactive video content are increasing customer engagement. India's large youth demographic and extremely high social media penetration create a compelling environment for social commerce, opening an estimated USD 16-20 Billion incremental opportunity by 2030.

Market Challenges

- Intense Price Competition Compressing Seller Margins: Multi-brand marketplaces engage in persistent price-based competition, training Indian consumers to expect steep discounts, particularly during major shopping festivals. This erodes seller profitability and forces platforms to subsidize growth through heavy discounting. Sustainable unit economics remain a structural challenge for the majority of e-commerce participants.

- Regulatory and FDI Policy Uncertainty: India's e-commerce sector is subject to ongoing regulatory scrutiny. FDI restrictions in inventory-based e-commerce models limit the ability of foreign-owned marketplaces to hold and sell inventory directly. Evolving rules on flash sales, data localization, and mandatory sourcing from domestic vendors create compliance burdens and strategic uncertainty for international and domestic platforms alike.

Emerging Market Trends

1. Quick Commerce Becoming a Structural Category in India's Online Retail Landscape

Quick commerce, offering delivery in 10-30 minutes for groceries and daily essentials, has shifted from a novelty to a mainstream retail channel. Swiggy Instamart expanded to 76 cities and launched a standalone app in January 2025. Blinkit and Zepto are expanding dark store networks aggressively. This trend is permanently compressing consumer tolerance for standard 1-2 day delivery timelines, elevating convenience as the primary competitive differentiator.

2. AI-Powered Personalization and Generative AI Shopping Agents

Artificial intelligence is fundamentally transforming the online shopping experience. In December 2024, CurveAi launched DealSpy, India's first AI-powered shopping agent suite, enabling real-time deal discovery across platforms via WhatsApp and Chrome extensions. Machine learning algorithms are personalizing product feeds, optimizing dynamic pricing, and predicting consumer intent with high accuracy. AI-driven chatbots and virtual assistants are reducing customer service costs while improving resolution rates.

3. D2C Brand Proliferation and Brand-Specific Website Growth

India's D2C ecosystem has witnessed explosive growth, with thousands of brands establishing direct online channels to improve margins and build deeper consumer relationships. In March 2025, IKEA expanded its North India digital presence with online delivery across Delhi-NCR and 9 additional cities. In the same month, Shein re-entered India through a partnership with Reliance Retail, underscoring renewed confidence in India's organized online retail. Brand-specific websites are growing at ~4.8% CAGR and represent the higher-margin, loyalty-rich segment of the market.

4. Social Commerce and Live-Stream Shopping Gaining Mainstream Traction

Social media platforms including Instagram, YouTube, and emerging Indian platforms are enabling shopping directly within social feeds. Influencer-led product launches and live-stream shopping events are creating impulse purchase occasions at scale. This trend is particularly powerful in Fashion, Beauty, and Lifestyle categories, where visual content drives purchase decisions among India's 500 million social media users.

5. Cross-Border E-Commerce and International Brand Entry

India's maturing e-commerce infrastructure is attracting international brands seeking market entry without physical retail investments. In September 2024, Amazon India launched three new Fulfillment Centers, creating over 110,000 seasonal jobs. Cross-border imports in electronics, fashion, and beauty are growing rapidly, with platforms enabling international brand storefronts accessible to Indian consumers, broadening product choice and intensifying competitive dynamics.

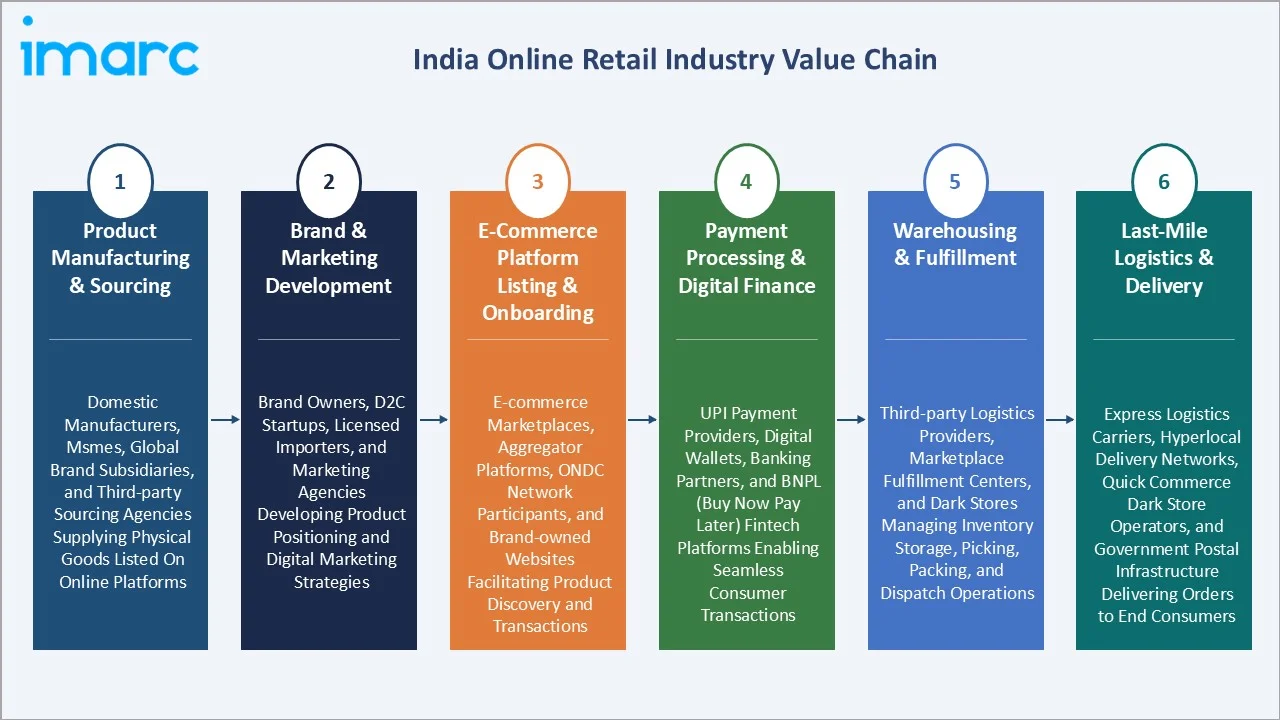

Industry Value Chain Analysis

India's online retail value chain integrates a broad network of participants - from raw material suppliers and product manufacturers to technology platforms, payment gateways, logistics providers, and end consumers. The ecosystem's commercial structure enables both domestic-first brands and globally imported products to compete for India's digitally active consumer base across highly differentiated price points.

|

Stage |

Key Participants |

|

Product Manufacturing & Sourcing |

Domestic manufacturers, MSMEs, global brand subsidiaries, and third-party sourcing agencies supplying physical goods listed on online platforms |

|

Brand & Marketing Development |

Brand owners, D2C startups, licensed importers, and marketing agencies developing product positioning and digital marketing strategies |

|

E-Commerce Platform Listing & Onboarding |

E-commerce marketplaces, aggregator platforms, ONDC network participants, and brand-owned websites facilitating product discovery and transactions |

|

Payment Processing & Digital Finance |

UPI payment providers, digital wallets, banking partners, and BNPL (Buy Now Pay Later) fintech platforms enabling seamless consumer transactions |

|

Warehousing & Fulfillment |

Third-party logistics providers, marketplace fulfillment centers, and dark stores managing inventory storage, picking, packing, and dispatch operations |

|

Last-Mile Logistics & Delivery |

Express logistics carriers, hyperlocal delivery networks, quick commerce dark store operators, and government postal infrastructure delivering orders to end consumers |

The e-commerce platform listing stage is commercially central to India's online retail value chain. Major platforms deploy advanced data analytics to optimize seller visibility, dynamic pricing, and promotional targeting. The warehousing and fulfillment stage is undergoing rapid investment expansion. The India e-commerce warehousing market reached USD 10.0 Billion in 2025 and is expected to reach USD 39.1 Billion by 2034, exhibiting a CAGR of 16.42% during 2026-2034, per IBEF data.

Technology Landscape in the India Online Retail Industry

Artificial Intelligence and Machine Learning

AI is the most commercially impactful technology in India's online retail sector. Personalized recommendation engines, deployed by Amazon India, Flipkart, and Myntra, drive incremental revenue by surfacing relevant products for each unique shopper. ML algorithms optimize dynamic pricing in real-time, adjusting to competitor price changes, demand fluctuations, and inventory positions. Generative AI shopping agents, such as DealSpy launched by CurveAi in December 2024, are enabling autonomous deal discovery, representing the leading edge of AI commerce integration.

Digital Payment Technologies and UPI Infrastructure

India's Unified Payments Interface (UPI) has become the world's most adopted real-time payment network, processing over 18.68 billion transactions in May 2025. UPI's instant settlement capability has eliminated the need for saved credit card credentials, lowering the checkout abandonment barrier. BNPL (Buy Now Pay Later) technology and EMI solutions embedded in e-commerce checkout flows are expanding purchasing power for mid-income consumers, directly increasing Average Order Values (AOV).

Augmented Reality and Virtual Try-On

AR technology is reducing purchase hesitation in high-return categories such as fashion and furniture. Myntra deploys virtual try-on features for apparel, while platforms like Pepperfry and IKEA enable AR-based room visualization for furniture purchases. Amazon India's "View in Your Room" AR feature has shown measurable impact on conversion rates in the Home category. As smartphone camera quality improves and AR processing costs decline, this technology is expected to scale across all major product categories by 2027-2028.

Logistics Technology and Supply Chain Automation

Automation in warehouses through robotic picking systems, conveyor automation, and AI-based routing is dramatically reducing order fulfillment times. In September 2024, Amazon India launched three new Fulfillment Centers, creating over 110,000 seasonal jobs. The rapid expansion of new-age logistics infrastructure, with an estimated 2.5-3 billion D2C shipments projected by 2030 (per IBEF), is driving investment in technology-enabled logistics platforms that provide real-time tracking, dynamic routing, and predictive demand signals.

Market Segmentation Analysis

The report covers the following key segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Sales Channel |

E-Commerce Marketplaces |

81.3% |

2025 |

|

Product Category |

Electronics & Appliances |

28.6% |

2025 |

|

Payment Method |

🔒 |

🔒 |

|

|

Region |

West India |

31.2% |

2025 |

By Sales Channel

E-Commerce Marketplaces lead at 81.3% in 2025. This channel dominates through its ability to aggregate supply from millions of sellers, offer competitive pricing via marketplace algorithms, and provide fulfillment reliability through invested logistics infrastructure. Platforms such as Amazon India, Flipkart, Meesho, Myntra, and Nykaa serve distinct but partially overlapping consumer segments, collectively generating the vast majority of India's digital retail GMV.

To access detailed market analysis, Request Sample

Brand-Specific Websites at 18.7% represent the higher-margin, brand-controlled retail channel. D2C brands including Boat, Mamaearth, Sugar Cosmetics, and Lenskart have built significant revenue streams through owned digital channels. International brands such as IKEA, which expanded online delivery to Delhi-NCR and 9 cities in March 2025, are choosing brand-owned websites as primary India market entry points, reinforcing the long-term commercial viability of direct-to-consumer digital channels.

By Product Category

Electronics and Appliances lead at 28.6% in 2025, driven by India's aspirational consumer class investing in smartphones, laptops, televisions, and major appliances. Festival shopping events - such as Flipkart Big Billion Days and Amazon Great Indian Festival - generate a disproportionate share of annual electronics sales. Apparel and Footwear at 24.3% holds the second-largest share. India's fashion e-commerce has been the traditional growth driver, with Myntra, AJIO, and Meesho collectively serving diverse income segments.

Food and Beverages at 18.7% is the fastest-growing category at ~7.2% CAGR. Quick commerce platforms have permanently accelerated online grocery adoption. Home and Furniture at 12.8% is supported by India's real estate activity and rising home improvement spending. Personal Care at 9.4% benefits from the D2C beauty brand revolution.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

West India |

31.2% |

Led by Mumbai's high-income urban population, Maharashtra's strong tech workforce, and Gujarat's entrepreneurial e-commerce adoption. Superior logistics infrastructure and dense digital payment penetration support the region's leadership. |

|

North India |

28.4% |

Delhi-NCR drives regional dominance through high consumer spending, premium brand affinity, and strong corporate procurement. Punjab and Haryana contribute through above-national-average consumer electronics and fashion spending. |

|

South India |

24.1% |

Bengaluru's IT sector wealth creates premium and electronics demand. Hyderabad and Chennai support fashion and personal care online retail. High digital literacy and UPI adoption rates underpin strong e-commerce fundamentals. |

|

East India |

16.3% |

Rising disposable incomes in Kolkata and Odisha's industrial belt are gradually supporting premium and mid-range online retail growth. The region grows above the overall market CAGR from a lower base, offering significant long-term upside. |

West India's 31.2% market leadership reflects Mumbai's concentration of high-net-worth households, India's highest per capita digital payment adoption in Maharashtra, and Gujarat's commerce-first culture embracing e-commerce for both B2B and B2C purchasing. North India's 28.4% reflects Delhi-NCR's luxury retail cluster, India's highest-density corporate procurement market, and strong government employee consumer base across the region.

South India's 24.1% share reflects Bengaluru's tech-savvy, high-income IT professional population creating above-average spending on electronics, apparel, and premium consumer goods. East India at 16.3% represents the market's most commercially underserved region, growing above the overall CAGR as organized e-commerce penetrates Tier-2 cities in West Bengal, Odisha, and the Northeast.

Competitive Landscape

India's online retail competitive landscape is one of the most intensely contested digital commerce battlegrounds in Asia. Major global players Amazon.com, Inc. and Walmart Inc., compete for GMV leadership, while domestic platforms, such as Reliance JioMart, and Tata Group target differentiated consumer segments with distinctive value propositions. Competition is intensifying through quick commerce, social commerce, and D2C brand growth.

|

Company |

Key Platforms / Brands |

Market Position |

Core Strength |

|

Amazon.com, Inc. |

Amazon.in, Amazon Fresh, Amazon Now |

Market Leader |

World-class fulfillment infrastructure, Prime loyalty ecosystem, AWS-backed tech capabilities, and vast international seller network |

|

Walmart Inc. |

Flipkart, Myntra, Cleartrip, Flipkart Minutes |

Market Leader |

Dominant domestic market knowledge, Flipkart Quick commerce, Myntra fashion leadership, and PhonePe payments integration |

|

Reliance Retail Ventures Limited (RRVL) |

JioMart, Ajio, Reliance Digital |

Strong Challenger |

Unparalleled physical-to-digital integration, India's largest retail network, and Jio telecom ecosystem creating captive digital consumer base |

|

Tata Group |

Tata Neu, BigBasket, Tata CLiQ, Tata 1mg |

Strong Challenger |

Grocery e-commerce pioneer with strong private label, cold-chain infrastructure, and expanding quick delivery footprint |

|

Swiggy |

Swiggy, Instamart |

Emerging Leader |

Quick commerce infrastructure across 76 cities by January 2025, with Instamart positioned to surpass core food delivery in revenue scale |

Key Company Profiles

Amazon.com, Inc.

Amazon.com, Inc., which operates Amazon India, is the market's largest e-commerce platform by infrastructure scale, offering a vast product assortment across all categories through Amazon.in.

- Key Platform: Amazon.in, Amazon Fresh, Amazon Now

- Recent Developments: In May 2026, Amazon Now, a quick commerce brand under Amazon.in, announced the expansion across 100 Indian cities including Pune, Hyderabad, Chennai, Kolkata, Jaipur, etc.

- Strategic Focus: Expanding Prime membership penetration, strengthening quick delivery capabilities, growing Amazon Business B2B segment, and deepening payment ecosystem integration through Amazon Pay.

Walmart Inc.

Flipkart, acquired by Walmart, is India's largest home-grown e-commerce platform and a dominant player in electronics, fashion, and home categories. Flipkart's subsidiary Myntra leads India's fashion e-commerce segment.

- Key Brands: Flipkart, Myntra, Cleartrip, Flipkart Minutes, and others.

- Recent Developments: In June 2025, Flipkart Commerce Cloud (FCC) was awarded the AI Initiative of the Year -India category win at the Retail Asia Awards 2025 for its artificial intelligence (AI)-driven Retail Media solution.

- Strategic Focus: Fashion category leadership through Myntra, PhonePe payments ecosystem integration, international brand partnerships, and expanding private label through Flipkart Fashion brands.

Market Concentration Analysis

India's online retail market is moderately concentrated at the marketplace layer, with the top three players - Amazon India, Flipkart, and Reliance JioMart - commanding an estimated 55-65% of total platform GMV in 2025. The market exhibits a dual concentration structure: high platform concentration at the marketplace level but high fragmentation at the seller and brand level, with over 7 lakh+ sellers active on the ONDC network alone as of early 2025.

Market concentration is evolving through two forces. Consolidation is occurring among major platforms investing in ecosystem expansion, while fragmentation increases in niche categories through the growth of category-specialist platforms. The D2C movement is reducing marketplace dependency for premium brands, creating structural diversification in India's online retail revenue distribution.

The quick commerce sub-segment shows higher concentration, with Blinkit, Swiggy Instamart, and Zepto collectively commanding 85-90% of the instant delivery market by GMV in 2025. This concentrated structure is expected to moderate as new quick commerce players enter Tier-2 city markets with differentiated category focus.

Investment & Growth Opportunities

Highest Growth Segments

Food and Beverages quick commerce (~7.2% CAGR through 2034) represents the segment with the strongest organic growth momentum. The segment benefits from habitual repeat purchase behavior, high purchase frequency, and India's growing urban convenience culture. Apparel and Footwear grows at ~6.3% CAGR, supported by India's young demographic and rising fashion consciousness. Electronics and Appliances (~5.5% CAGR) benefits from India's smartphone upgrade cycle and rising home appliance penetration.

Emerging Investment Opportunities

- Tier-2 and Tier-3 City E-Commerce Infrastructure: Logistics and dark store infrastructure in smaller cities offers high-return investment potential. Tier-3 cities increased e-commerce market share from 34.2% in 2021 to 41.5% in 2022, indicating structural demand growth ahead of supply. Warehousing and fulfillment center investments in these geographies are underpinned by growing e-commerce GMV with limited existing infrastructure competition.

- Social Commerce and Influencer-Commerce Platforms: India's 500 million social media users and content creator economy present a compelling opportunity for platforms enabling direct social-to-commerce conversion. Influencer-led product launches and live-stream shopping are creating impulse purchase occasions across fashion, beauty, and lifestyle categories.

- D2C Brand Scaling and Private Label Development: India's D2C ecosystem is estimated to grow to USD 110 Billion by 2026, supported by affordable digital marketing, social media reach, and accessible logistics infrastructure. Investment in brand incubation, private label development, and D2C technology stacks represents a high-conviction opportunity in India's evolving retail landscape.

Investment Themes

Three strategic investment themes define India online retail's highest-conviction opportunities through 2034: First, supply chain and logistics infrastructure expansion supporting India's 2.5 billion projected D2C shipments by 2030. Second, AI and personalization technology investments improving customer lifetime value across all platform types. Third, regulatory tailwind positioning through ONDC participation, enabling platforms to expand into government-facilitated seller and buyer networks at scale.

Future Market Outlook (2026-2034)

The India online retail market is projected to grow from USD 217.16 Billion in 2025 to USD 366.42 Billion by 2034, delivering a 5.81% CAGR through the forecast period. The anchor value of USD 287.95 Billion in 2030 represents a structural inflection point where India's digital consumer base is expected to exceed 500 million active online shoppers. Three structural forces will define India's online retail expansion through 2034.

First, India's income growth will create the world's largest new middle-class consumer cohort entering the e-commerce market between 2025 and 2034. India is projected to become the world's third-largest consumer economy by 2030, with consumer spending expected to grow to USD 6 trillion from USD 2.4 trillion in 2022. Second, technological disruption through AI, AR, voice commerce, and autonomous delivery will reduce friction in the consumer purchase journey. Third, ONDC's network expansion - targeting democratized e-commerce access for India's unorganized seller base - will structurally expand the addressable market by enabling micro-sellers to access pan-India digital commerce infrastructure.

Quick commerce will transition from urban-only to Tier-2 city deployment by 2026-2027, fundamentally reshaping grocery and daily essentials retail. Cross-border e-commerce will grow as India's improving logistics infrastructure enables faster international deliveries.

Research Methodology

Primary Research

Primary research comprised structured interviews with India online retail industry stakeholders, including e-commerce platform executives, category managers, logistics operators, payment gateway directors, D2C brand founders, and consumer survey data from online shoppers across North, South, West, and East India, spanning Tier-1, Tier-2, and Tier-3 city demographics.

Secondary Research

Secondary research encompassed Press Information Bureau (PIB) government publications, DPIIT policy documents, India Brand Equity Foundation (IBEF) industry reports, company annual reports, RBI payment system data, ONDC network disclosures, NASSCOM digital economy reports, investor presentations, and industry publications. Over 60 secondary sources were reviewed and cross-referenced.

Forecasting Models

Market revenue forecasts were developed using a consumer adoption diffusion model: India's internet user base growth trajectory multiplied by e-commerce conversion rates and Average Order Values per income segment, creating total market GMV by channel aggregation. Government initiative multipliers (ONDC, UPI adoption curves) were applied across relevant segments to reflect structural policy-driven demand acceleration.

India Online Retail Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Categories Covered | Food and Beverages, Personal Care, Apparel and Footwear, Electronics and Appliances, Home and Furniture, Others |

| Payment Methods Covered | Cash on Delivery (COD), Digital Payments, EMI and Buy Now Pay Later (BNPL) |

| Sales Channels Covered | E-Commerce Marketplaces, Brand-Specific Websites |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Amazon.com, Inc., Walmart Inc., Reliance Retail Ventures Limited (RRVL), Tata Group, Swiggy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India online retail market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India online retail market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India online retail industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Online Retail Market Report

The India online retail market reached USD 217.16 Billion in 2025, driven by rising internet penetration, digital payment adoption, expanding logistics infrastructure, and government initiatives such as ONDC and UPI.

The India online retail market is projected to grow at a CAGR of 5.81% during 2026-2034, driven by expanding digital consumer base, income growth, AI-powered shopping experiences, and quick commerce penetration.

E-Commerce Marketplaces lead at 81.3% in 2025, driven by Amazon India, Flipkart, and JioMart, offering vast product assortments and competitive pricing through established logistics infrastructure.

Electronics and Appliances leads at 28.6% in 2025, supported by India's smartphone upgrade cycle, rising consumer electronics aspiration, and festival-season demand events driving disproportionate category sales.

West India leads at 31.2% in 2025, driven by Mumbai's high-income consumer base, Maharashtra's digital payment leadership, and Gujarat's commerce-oriented consumer culture embracing e-commerce for business and personal purchases.

Food and Beverages is the fastest-growing category at ~7.2% CAGR, driven by quick commerce platforms Swiggy Instamart, Blinkit, and Zepto transforming India's grocery purchasing habits across urban demographics.

Leading companies include Amazon.com., Inc., Walmart Inc., Reliance Retail Ventures Limited (RRVL), Tata Group, and Swiggy, among others.

The India online retail market is projected to reach USD 287.95 Billion by 2030, supported by India's growing 500 million+ online shopper base, quick commerce expansion, and AI-driven personalization improving conversion rates.

Top opportunities include Tier-2 city logistics and dark store infrastructure, quick commerce platform expansion, D2C brand scaling through digital channels, social commerce technology, and AI-powered personalization platforms.

The India online retail market reached USD 163.77 Billion in 2020, growing from the base period. The market expanded substantially during 2020-2025 at a healthy CAGR, driven by COVID-19 accelerating digital commerce adoption.

Brand-specific websites hold 18.7% market share in 2025, growing at ~4.8% CAGR as D2C brands including boAt, Mamaearth, Sugar Cosmetics, and international brands like IKEA expand direct digital retail channels.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade