India Organic Baby Skincare Market Size, Share, Trends and Forecast by Skin Type, Product Type, Distribution Channel, and Region, 2026-2034

India Organic Baby Skincare Market Size, Share, Trends & Forecast (2026-2034)

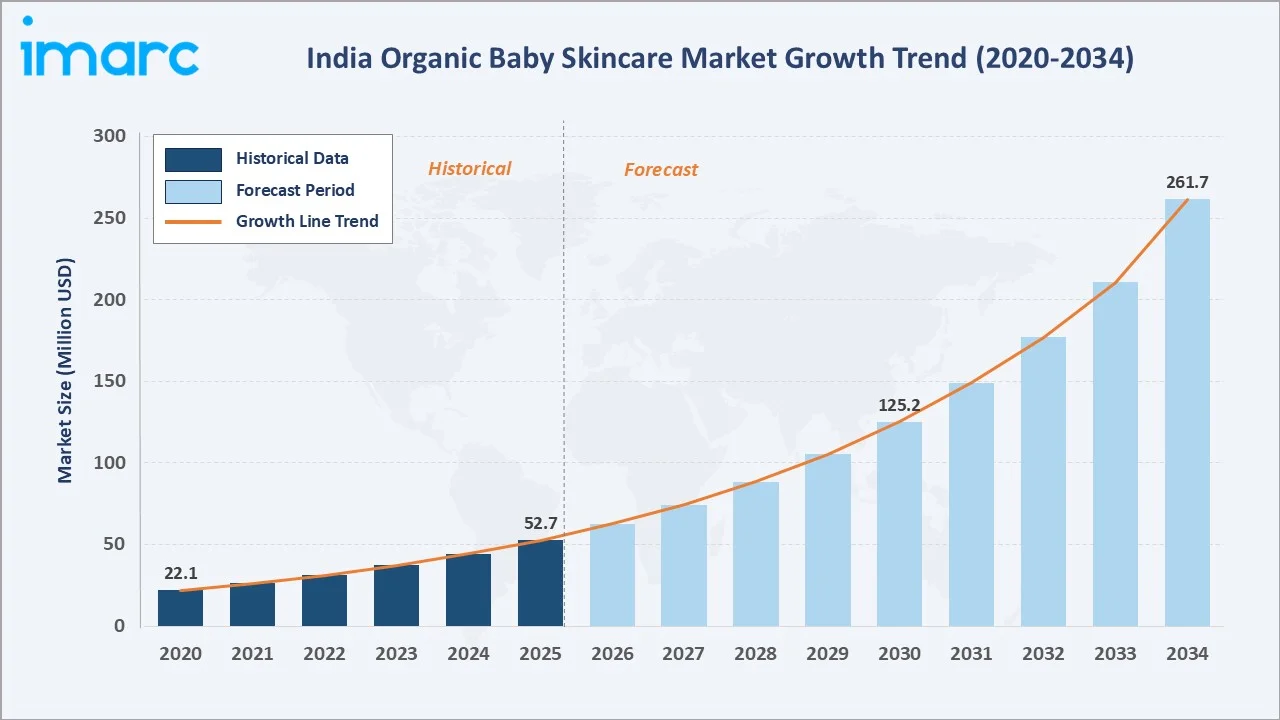

The India organic baby skincare market reached USD 52.7 Million in 2025 and is projected to reach USD 261.7 Million by 2034, growing at a CAGR of 18.91% during 2026-2034. Rising parental awareness about harmful synthetic ingredients, rapid urbanization, and growing digital influence from social media platforms are the primary growth drivers.

Dry Skin dominates at 41.6%, Hypermarkets and Supermarkets lead distribution at 34.8%, and North India holds a 33.2% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 52.7 Million |

|

Forecast Market Size (2034) |

USD 261.7 Million |

|

CAGR (2026-2034) |

18.91% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Skin Type Segment |

Dry Skin (41.6%, 2025) |

|

Leading Distribution Channel |

Hypermarkets and Supermarkets (34.8%, 2025) |

|

Leading Region |

North India (33.2%, 2025) |

The market expanded from USD 22.1 Million in 2020 to USD 52.7 Million in 2025 - more than doubling in five years - anchored at USD 125.2 Million in 2030 and forecast to reach USD 261.7 Million by 2034. The growing organic consciousness among Indian urban parents and accelerating e-commerce penetration are sustaining above-market category growth through the forecast period.

To get more information on this market, Request Sample

Dry Skin formulations dominate product mix at 41.6%, reflecting the prevalence of low-humidity climatic conditions across large Indian population centres. Hypermarkets and Supermarkets at 34.8% lead distribution through trusted retail environments, while North India commands 33.2% regional share through elevated urban consumer concentration.

Executive Summary

The India organic baby skincare market reached USD 52.7 Million in 2025, representing one of India's fastest-growing personal care categories driven by the fundamental shift among urban parents toward chemical-free, certified organic infant care formulations. The market is projected to reach USD 261.7 Million by 2034.

Dry Skin at 41.6% dominates by capturing the widest addressable infant skin type demographic. Hypermarkets and Supermarkets at 34.8% lead distribution through the highest product trial, in-store promotions, and consumer trust. North India at 33.2% leads regionally through urban density and high disposable incomes among the premium organic consumer base.

Key Market Insights

|

Insight |

Data |

|

Dominant Skin Type |

Dry Skin - 41.6% share (2025) |

|

Leading Distribution Channel |

Hypermarkets and Supermarkets - 34.8% market share (2025) |

|

Leading Region |

North India - 33.2% market share (2025) |

|

Market Opportunity |

E-commerce channel expansion; product premiumization; Ayurvedic organic formulations; Tier-2/Tier-3 city penetration |

Key Analytical Observations Supporting the Above Data:

- Dry Skin at 41.6%: The dry skin segment dominates as India's diverse climatic conditions and prevalent dry-skin infant demographics drive demand for richer organic moisturizers. Its widespread adoption in northern and central regions with low ambient humidity further strengthens segment demand.

- Hypermarkets and Supermarkets at 34.8%: This channel dominates due to broad physical product availability, trusted retail environments, in-store promotional activities, and impulse purchasing convenience. Its presence across Tier-1 and growing Tier-2 cities ensures sustained channel leadership through the forecast period.

- North India at 33.2%: The North India region dominates through the National Capital Region's high affluence concentration, dry climatic conditions driving Dry Skin formulation demand, and the presence of all major organic baby skincare brand retail touch points across Delhi, Chandigarh, and Lucknow.

India Organic Baby Skincare Market Overview

The India organic baby skincare market encompasses the design, formulation, and supply of all organic-certified skincare products for infants and toddlers across all skin types, including baby oils, lotions, soaps, powders, and petroleum jelly alternatives distributed across modern trade, pharmacy, specialty, and e-commerce channels.

The ecosystem integrates certified organic ingredient suppliers, sustainable packaging manufacturers, modern trade and e-commerce distributors, and regulatory bodies setting organic cosmetic standards. Macroeconomic factors include rising urban birth rates, increasing disposable incomes, internet penetration, and social media-driven brand awareness.

Market Dynamics

To evaluate market opportunities, Request Sample

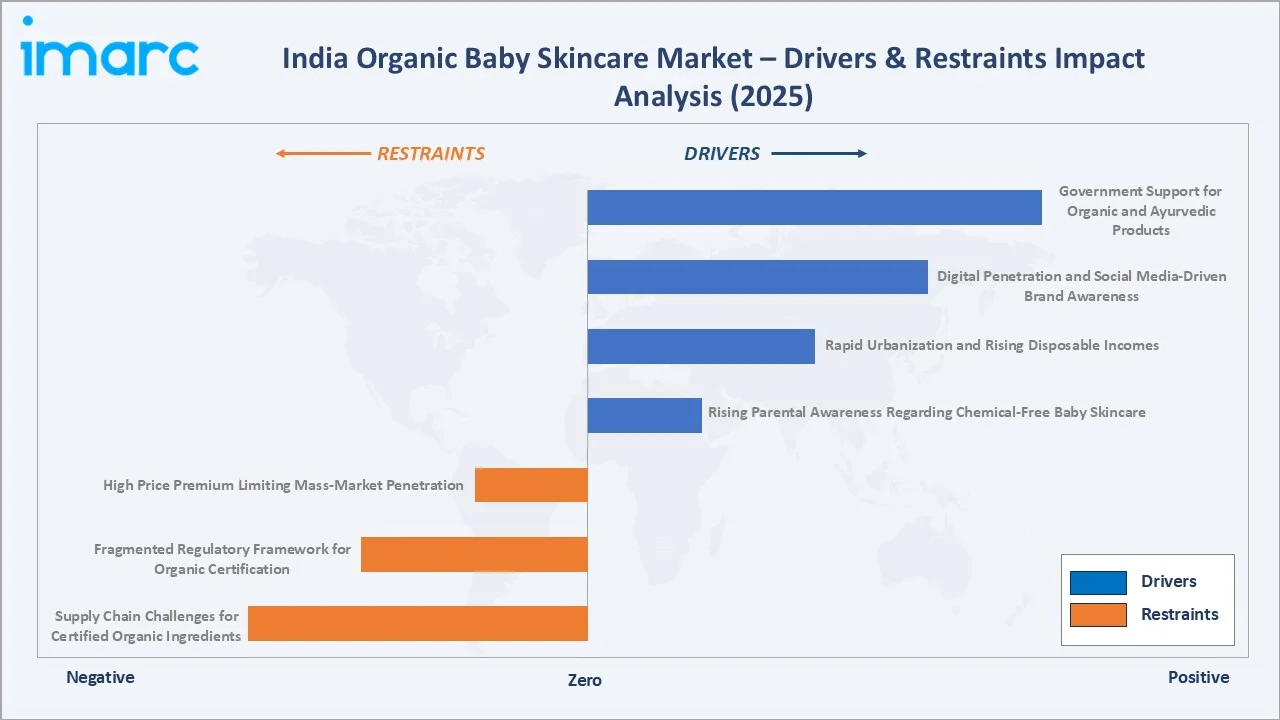

Market Drivers

- Rising Parental Awareness Regarding Chemical-Free Baby Skincare: Growing parental concern over harmful synthetic chemicals in conventional baby products is driving demand for certified organic alternatives. Parents increasingly scrutinize ingredient lists and seek products free from parabens, sulfates, and artificial fragrances, accelerating adoption of organic baby skincare across urban India.

- Rapid Urbanization and Rising Disposable Incomes: India's accelerating urbanization, with urban population expected to reach 600 million by 2031, is expanding the premium organic consumer base. Higher disposable incomes among urban middle-class families are enabling premium organic baby skincare purchases, directly fueling market revenue growth across all skin type categories.

- Digital Penetration and Social Media-Driven Brand Awareness: Aggressive brand promotion on Instagram, YouTube, and parenting communities is accelerating organic baby skincare adoption. Influencer-led content, mother-focused digital communities, and targeted digital advertising are generating awareness and trust, particularly for direct-to-consumer brands operating in India.

- Government Support for Organic and Ayurvedic Products: Government promotion of Ayurvedic and organic product segments through Aatmanirbhar Bharat and preferential certification frameworks is enabling faster market entry for domestic brands, reducing compliance costs and accelerating organic baby skincare supply-side expansion across India.

Market Restraints

- High Price Premium Limiting Mass-Market Penetration: Organic baby skincare products command a significant price premium of 30-60% over conventional alternatives, limiting adoption among price-sensitive consumers in Tier-2 and Tier-3 cities. This premium pricing creates a structural barrier to mass-market penetration and constrains addressable market expansion.

- Fragmented Regulatory Framework for Organic Certification: India's organic certification landscape for cosmetics remains fragmented, with inconsistent standards across COSMOS, USDA Organic, and domestic NPOP certifications. This regulatory ambiguity creates consumer confusion and increases compliance complexity, slowing market formalization and brand differentiation.

- Supply Chain Challenges for Certified Organic Ingredients: Sourcing consistent, certified organic botanical ingredients at scale within India remains challenging due to limited certified farmland, seasonal supply variability, and nascent organic ingredient supplier networks, increasing formulation costs and quality inconsistency risks.

Market Opportunities

- E-Commerce Channel Expansion in Tier-2 and Tier-3 Cities: India's rapidly expanding e-commerce logistics infrastructure is enabling organic baby skincare brands to reach previously underserved Tier-2 and Tier-3 city consumers, creating significant growth opportunities for both established and emerging brands through digital-first distribution models.

- Product Premiumization and Dermatologically Certified Formulations: Rising demand for clinically tested dermatologist-approved organic baby formulations is creating a premium product tier opportunity. Brands investing in dermatological certification, hypoallergenic claims, and transparent ingredient disclosure can command higher price points and stronger brand loyalty.

Market Challenges

- Counterfeit and Mislabelled Organic Products Undermining Consumer Trust: Proliferation of counterfeit or mislabelled organic baby skincare products on e-commerce platforms and unorganized retail channels is eroding consumer confidence and creating brand differentiation challenges, requiring sustained investment in consumer education and supply chain authentication.

- Intense Competition Between Global MNC Brands and Domestic Players: Intensifying competition between established MNC brands and rapidly scaling domestic brands is compressing margins and increasing marketing expenditure requirements across the India organic baby skincare competitive landscape.

Emerging Market Trends

1. Waterless and Concentrated Organic Formulations

Waterless skincare formats, including solid baby bars, concentrated balms, and anhydrous lotions, are gaining traction as eco-conscious parents seek sustainable, travel-friendly organic alternatives. These formulations reduce preservative requirements and packaging waste, aligning with premium organic brand positioning and driving innovation across the India baby skincare market.

2. Ayurvedic and Herb-Infused Organic Baby Skincare

Integration of traditional Ayurvedic ingredients such as turmeric, neem, sandalwood, and ashwagandha into organic baby skincare formulations is differentiating Indian brands from global competitors, leveraging India's deep-rooted traditional medicine heritage and resonating strongly with culturally conscious urban parents.

3. Subscription-Based and D2C E-Commerce Models

Direct-to-consumer subscription models for organic baby skincare are emerging as a high-lifetime-value channel strategy. Brands offering monthly curated organic baby skincare bundles are achieving higher customer retention rates and predictable revenue streams while bypassing traditional distribution margin structures.

4. Eco-Friendly Packaging Adoption

Recyclable, biodegradable, and refillable packaging formats are becoming a key purchase criterion for environmentally aware parents. Organic baby skincare brands adopting sustainable packaging are gaining competitive differentiation and aligning with India's expanding ESG retail compliance requirements for consumer goods companies.

Industry Value Chain Analysis

The India organic baby skincare value chain integrates certified organic ingredient sourcing, compliant formulation and manufacturing, sustainable packaging, multi-channel distribution, and post-purchase consumer engagement. The value chain's commercial architecture has been progressively consolidating toward integrated D2C formats replacing traditional multi-tier distribution structures.

|

Stage |

Key Participants |

|

Raw Material & Ingredient Sourcing |

Certified organic botanical extract suppliers, cold-pressed oil producers, natural active ingredient manufacturers, and compliant preservative system suppliers |

|

Formulation & Quality Testing |

Organic cosmetic formulators, dermatological testing laboratories, and certified contract manufacturing organizations |

|

Packaging & Labelling |

Eco-friendly packaging suppliers, BPA-free container manufacturers, recyclable material producers, and organic label compliance specialists |

|

Distribution & Retail |

Hypermarkets and supermarkets, e-commerce platforms, specialty baby stores, retail pharmacy chains, and D2C subscription platforms |

|

Consumer & Brand Engagement |

Digital parenting communities, social media influencers, brand loyalty programme managers, and quick-commerce platform partners |

The raw material and ingredient sourcing tier is the India organic baby skincare value chain's most commercially critical stage, with certified organic botanical availability creating structural supply constraints. The distribution and retail tier is experiencing the fastest transition as e-commerce and quick-commerce platforms progressively displace traditional multi-tier distribution.

Technology Landscape in the India Organic Baby Skincare Industry

Green Chemistry and Cold-Process Formulation Technology

Green chemistry formulation techniques, including cold-process emulsification and solvent-free extraction, enable stable, high-efficacy organic baby skincare products without synthetic preservatives or heat-sensitive ingredient degradation, improving product performance and clean-label compliance for premium organic baby care brands.

Microbiome-Friendly Probiotic Skincare Technology

Probiotic and postbiotic skincare technologies incorporated into premium organic baby formulations support the developing infant skin microbiome. These science-backed approaches are differentiating premium brands and attracting dermatologist endorsements, supporting higher price positioning in the India organic baby skincare market.

AI-Driven Personalization for Skin-Type Specific Formulations

Emerging AI-powered skin assessment tools enable D2C organic baby skincare brands to offer personalized product recommendations based on individual infant skin type profiles across dry, oily, and flaky skin categories. This technology-driven personalization model increases conversion rates and strengthens consumer retention for India's digital-first organic baby care brands.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Skin Type |

Dry Skin |

41.6% |

2025 |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

Hypermarkets and Supermarkets |

34.8% |

2025 |

|

Region |

North India |

33.2% |

2025 |

By Skin Type

The Dry Skin segment leads at 41.6% in 2025, encompassing the mainstream organic baby moisturizer and lotion product range - the most commercially significant and highest-revenue product category in the India organic baby skincare market.

To access detailed market analysis, Request Sample

The Oily Skin segment at 32.4% captures formulations designed for coastal and humid-climate infant consumers requiring lighter, non-comedogenic organic textures. Flaky Skin at 26.0% represents the specialized therapeutic segment requiring targeted organic treatment formulations with higher active ingredient concentrations for sensitive infant skin conditions.

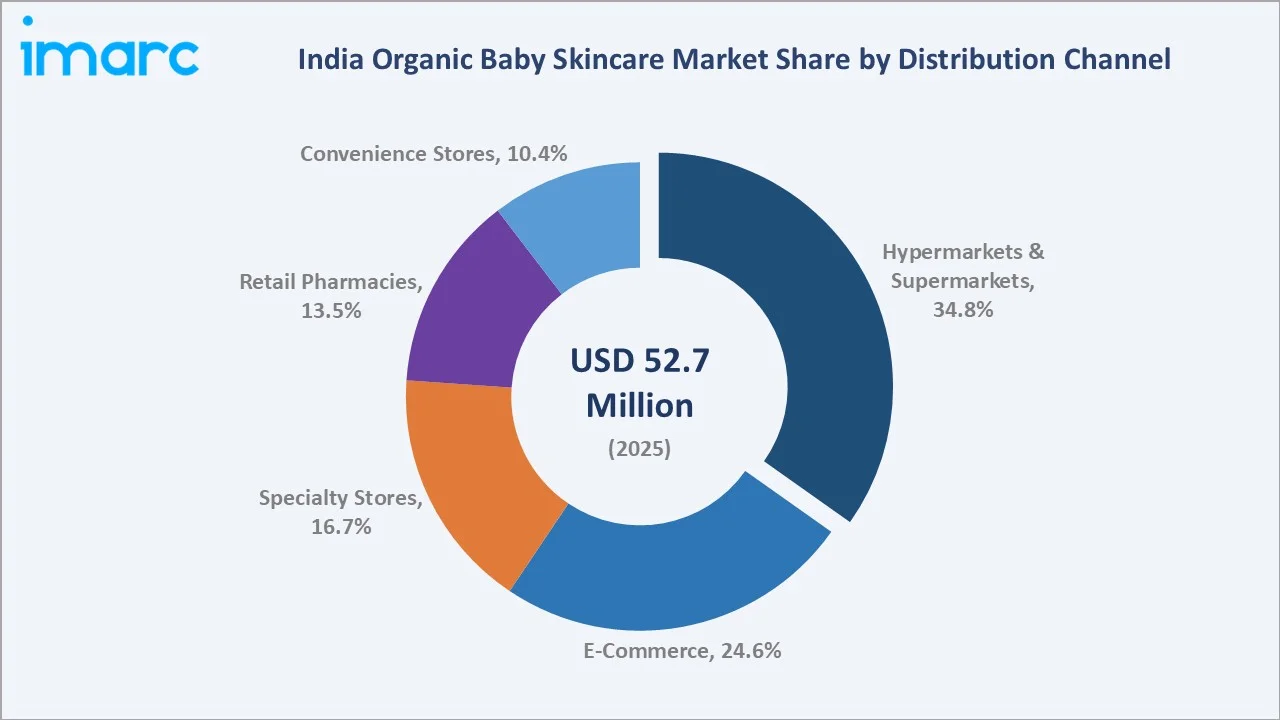

By Distribution Channel

Hypermarkets and Supermarkets lead at 34.8% through broad physical product availability, trusted brand presentation environments, and impulse purchasing opportunity for organic baby skincare products. The channel benefits from India's expanding modern trade footprint across Tier-1 and Tier-2 cities.

E-Commerce at 24.6% is the fastest-growing distribution channel, powered by India's expanding digital consumer base and D2C brand growth. Specialty Stores at 16.7% serve premium organic brand consumers seeking expert consultation, while Retail Pharmacies at 13.5% capture medically oriented purchase decisions and Convenience Stores at 10.4% address top-up purchasing.

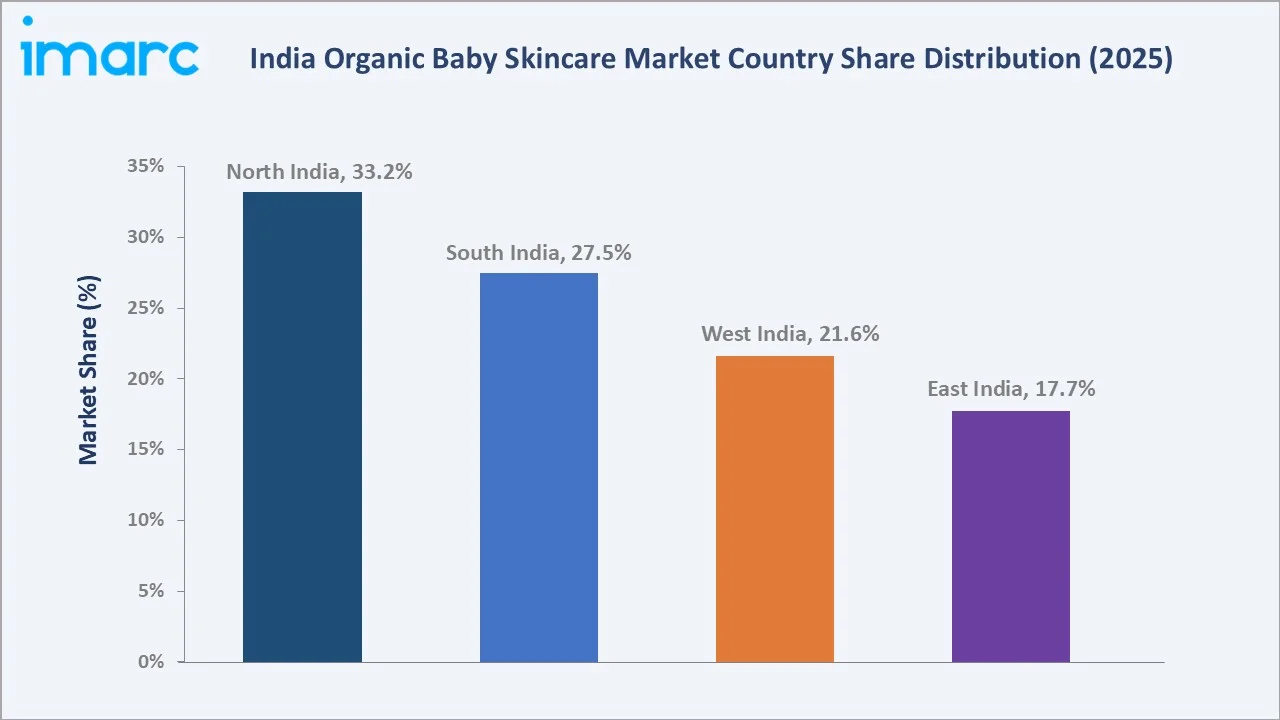

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

North India |

33.2% |

High urban density; elevated disposable incomes; dry-climate infant skin needs; strong premium brand retail presence across NCR, Chandigarh, and Lucknow |

|

South India |

27.5% |

High literacy and health awareness; strong Ayurvedic product affinity; robust specialty organic retail and pharmacy distribution across Tamil Nadu and Kerala |

|

West India |

21.6% |

Affluent urban consumer base; thriving D2C e-commerce adoption; strong modern trade retail infrastructure across Mumbai and Pune |

|

East India |

17.7% |

Rising awareness; expanding e-commerce logistics enabling organic brand penetration in previously underserved markets across Kolkata and Bhubaneswar |

North India, at 33.2%, leads through the National Capital Region's high affluence concentration, dry climatic conditions driving Dry Skin formulation demand, and the presence of all major organic baby skincare brand retail touch points. South India, at 27.5%, reflects the region's high health literacy and strong Ayurvedic product affinity.

West India, at 21.6%, benefits from Mumbai and Pune's advanced modern trade ecosystem and high D2C e-commerce adoption. East India, at 17.7%, represents the market's highest-potential under-penetrated geography as e-commerce logistics expansion opens organic product access to Tier-2 and Tier-3 eastern city consumers.

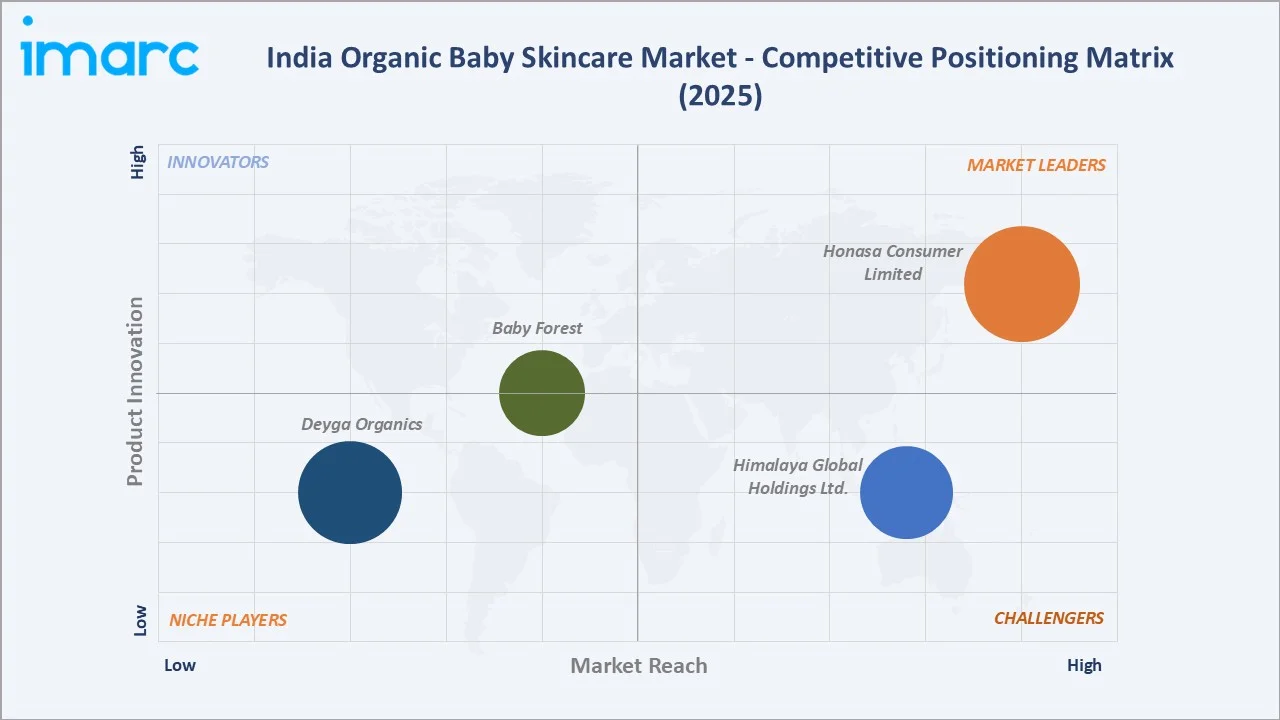

Competitive Landscape

The India organic baby skincare competitive landscape is moderately fragmented with three distinct competitive tiers: established MNC brands with wide retail distribution, domestic Ayurvedic and herbal brands with pharmacy-led reach, and emerging D2C digital-native brands competing through social media marketing and organic certification transparency.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Honasa Consumer Limited |

Mamaearth Gentle Cleansing Baby Shampoo, Baby Lotion, Baby Face Cream |

Market Leader |

Toxin-free D2C brand with strong digital presence and MadeSafe certification |

|

Deyga Organics |

Baby Body Lotion, Bath Bar, Baby Butter, Baby Powder |

Niche Player |

Ayurvedic-inspired, handcrafted organic baby care brand using indigenously grown organic ingredients with no parabens, sulfates, or harsh chemicals |

|

Himalaya Global Holdings Ltd. |

Baby Lotion, Baby Cream, Baby Soap |

Strong Challenger |

Herbal and Ayurvedic positioning with extensive pharmacy and modern trade distribution |

|

Baby Forest |

Baby Face Cream, Baby Body Lotion, Baby Body Wash |

Emerging Leader |

Ayurveda-inspired D2C brand offering chemical-free, certified formulations rooted in traditional Indian ingredients |

Key players include Honasa Consumer Limited, Deyga Organics, Himalaya Global Holdings Ltd., Baby Forest, and others.

Key Company Profiles

Honasa Consumer Limited

Honasa Consumer Limited operating through Honasa Consumer Limited is an India-based D2C personal care company and market leader in the organic baby skincare segment, known for its toxin-free, MadeSafe-certified baby formulations with nationwide e-commerce and modern trade distribution across 500+ Indian cities.

- Key Products: Mamaearth Gentle Cleansing Baby Shampoo, Baby Lotion, Baby Face Cream, and others.

- Strategic Focus: Expanding certified organic product portfolio for infants; deepening e-commerce and quick-commerce channel penetration; strengthening international market presence.

Himalaya Global Holdings Ltd.

Himalaya Global Holdings Ltd. Operating through Himalaya Wellness is an India-based herbal healthcare and personal care company with a strong presence in the baby skincare segment through its Ayurvedic and natural ingredient-based product range, distributed extensively across pharmacy and modern trade channels throughout India.

- Key Products: Baby Lotion, Baby Cream, Baby Soap, and others.

- Recent Developments: In April 2026, Himalaya expanded its baby care portfolio with the launch of Soothing Powder, specially developed for babies with sensitive skin. The new product is formulated with natural ingredients and is designed to help absorb excess moisture, soothe skin irritation, and keep babies comfortable while supporting gentle everyday skincare.

- Strategic Focus: Expanding certified organic Ayurvedic baby product lines; scaling pharmacy and specialty store distribution; investing in dermatological validation of herbal formulations.

Market Concentration Analysis

The India organic baby skincare market is moderately fragmented, with the top five players collectively accounting for approximately 55-65% of organized market revenue. The unorganized segment comprising regional and private-label brands accounts for an estimated 20-25% of total market volume.

Market concentration is declining over the forecast period as new D2C digital brands gain organic certification and consumer trust, while established MNC players respond through product reformulation and premiumization strategies. E-commerce democratization is the primary force reducing market concentration by enabling new entrants to build national presence without physical retail infrastructure investment.

Investment & Growth Opportunities

Highest Growth Segments

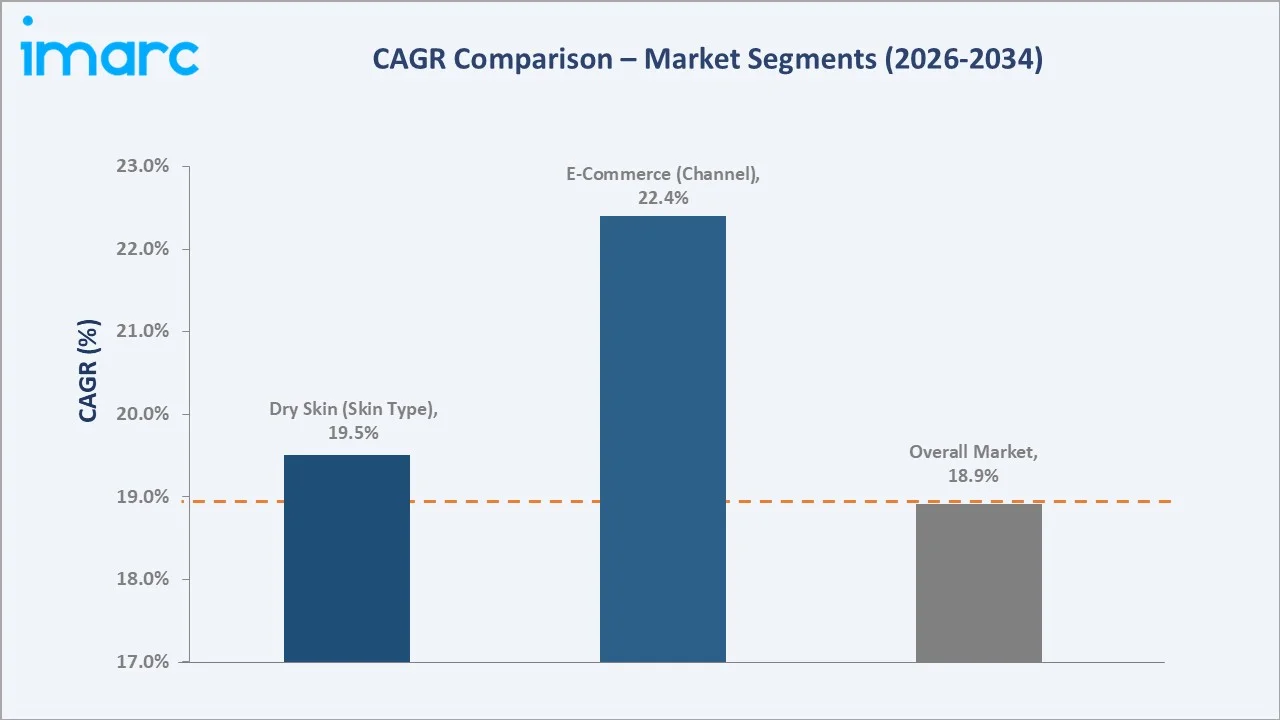

E-Commerce distribution channel (~22.4% CAGR), Flaky Skin therapeutic formulations (~18.1% CAGR), premium certified organic product lines (~20%+ CAGR), Ayurvedic herb-infused organic formulations, and Tier-2/Tier-3 city market penetration through digital-first D2C models represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Quick-commerce integration for organic baby skincare represents an emerging high-frequency repurchase channel opportunity. Brands achieving early integration with quick-commerce platforms in major metro areas can capture premium convenience-oriented parents willing to pay higher per-unit prices for immediate availability of trusted organic infant care products.

Investment Themes

- Organic certification infrastructure investment for COSMOS and USDA certification to unlock export and premium domestic pricing opportunities as consumer organic literacy and purchasing power increase across India's growing urban middle class.

- India Tier-2 and Tier-3 city e-commerce distribution expansion, capturing the world's fastest-growing urban digital consumer base with targeted organic baby skincare brand penetration through digital-first go-to-market strategies.

Future Market Outlook (2026-2034)

The India organic baby skincare market is projected to grow from USD 52.7 Million in 2025 to USD 261.7 Million by 2034, delivering an 18.91% CAGR over the forecast period. The market's anchor value of approximately USD 125.2 Million in 2030 represents an organic baby skincare industry at its most transformative commercial inflection, with e-commerce displacing traditional retail as the dominant growth channel.

Three structural forces define market growth through 2034: India's rising birth rate among urban middle-class families creating a sustained new consumer pipeline, the compounding digitalization of retail enabling national organic brand reach without physical infrastructure, and the growing body of clinical evidence supporting organic formulations for infant skin health driving sustained category premiumization.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025), including brand founders, pediatric dermatologists, retail category managers, e-commerce platform baby care leads, and certified organic ingredient suppliers across India.

Secondary Research

Secondary research encompassed company annual reports; IMARC Group proprietary databases; CDSCO regulatory publications; India e-commerce industry reports 2025; consumer panel data on baby care; Ministry of Commerce organic sector reports; and brand investor disclosures. Over 50 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using bottom-up consumer demand model: (i) addressable infant population by region; (ii) organic baby skincare adoption rate by income segment; (iii) average annual per-infant organic skincare spend by product category; (iv) distribution channel growth premium adjustments by channel type.

India Organic Baby Skincare Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Skin Type | Flaky Skin, Oily Skin, Dry Skin |

| Product Type | Baby Oil, Baby Powder, Baby Soaps, Petroleum Jelly, Baby Lotion, Others |

| Distribution Channel | Hypermarkets and Supermarkets, E-Commerce, Specialty Stores, Retail Pharmacies, Convenience Stores |

| Region Covered | North India, South India, East India, West India |

| Companies Covered | Honasa Consumer Limited, Deyga Organics, Himalaya Global Holdings Ltd., Baby Forest, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Organic Baby Skincare Market Report

The India organic baby skincare market reached USD 52.7 Million in 2025, driven by rising parental awareness of organic formulations, Dry Skin segment dominance at 41.6%, Hypermarkets and Supermarkets leading distribution at 34.8%, and North India commanding 33.2% regional share through urban affluence and dry-climate infant skin care demand.

The market grows at 18.91% CAGR during 2026-2034, reaching USD 261.7 Million by 2034. This growth reflects e-commerce expansion, urban middle-class growth, product premiumization, increasing organic certification adoption, and the compounding demand from India's growing urban infant consumer population.

Dry Skin leads at 41.6%, capturing the largest infant skin type demographic in India, particularly across northern and central regions with low-humidity climatic conditions requiring intensive organic moisturization formulations. The segment grows at approximately 19.5% CAGR through the forecast period.

Hypermarkets and Supermarkets lead at 34.8% through broad product availability and trusted retail environments. E-Commerce at 24.6% is the fastest-growing channel at approximately 22.4% CAGR, powered by India's expanding digital consumer base and D2C organic brand growth strategies.

North India leads at 33.2% through the National Capital Region's affluent urban consumer concentration, dry-climate infant skin care needs driving Dry Skin formulation demand, and premium brand retail penetration across Delhi NCR, Chandigarh, and Lucknow metropolitan areas.

Key players include Honasa Consumer Limited, Deyga Organics, Himalaya Global Holdings Ltd., Baby Forest, and others.

The market is projected to reach approximately USD 125.2 Million by 2030, driven by sustained e-commerce penetration growth, premiumization of organic product lines, Ayurvedic formulation differentiation scaling nationally, and expansion into Tier-2 and Tier-3 city markets through digital-first D2C brand models.

Top investment opportunities include E-Commerce D2C brand building for Tier-2/Tier-3 market penetration, organic certification and premium positioning for higher price-point capture, Ayurvedic and herb-infused organic formulation development leveraging India's botanical heritage, and quick-commerce integration for high-frequency metro urban repurchase channels.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)