India Organic Farming Market Size, Share, Trends and Forecast by Crop Type, Method, and Region, 2026-2034

India Organic Farming Market Summary:

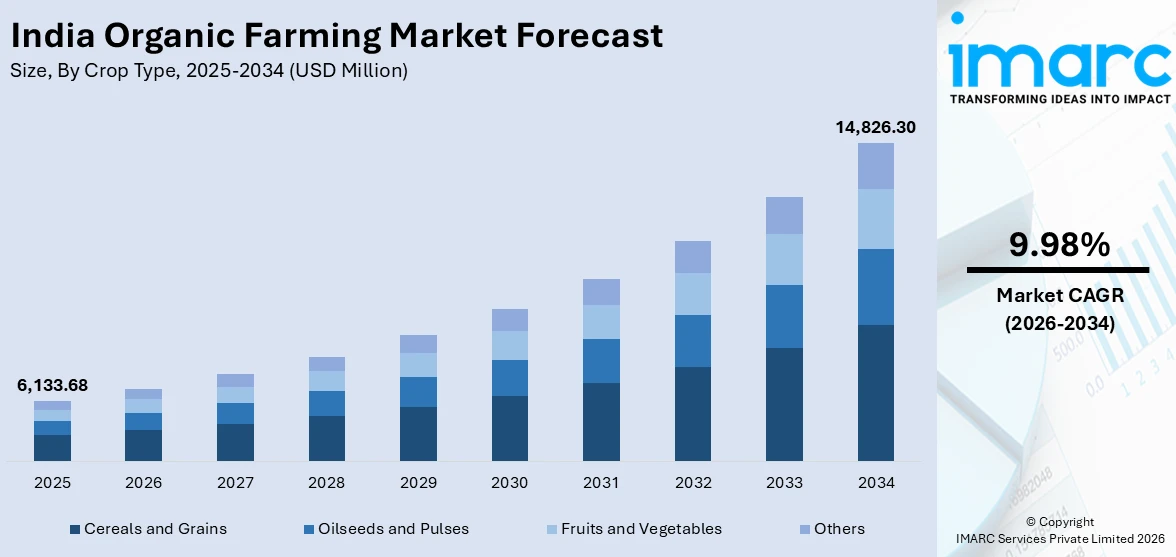

The India organic farming market size was valued at USD 6,133.68 Million in 2025 and is projected to reach USD 14,826.30 Million by 2034, growing at a compound annual growth rate of 9.98% from 2026-2034.

The India organic farming market is driven by rising consumer awareness about food safety and health, leading to higher demand for chemical-free produce across urban centers. The growing concerns about soil degradation and long-term farm productivity are encouraging a shift toward sustainable practices. Government support through subsidies, certification programs, and export incentives is strengthening farmer participation. Expanding retail networks, e-commerce platforms, and direct-to-consumer (DTC) models are improving market access. Increasing export demand for organic tea, spices, and grains is further supporting production growth.

Key Takeaways and Insights:

- By Crop Type: Cereals and grains dominate the market with a share of 32.5% in 2025, driven by strong domestic demand for staple foods, expanding export opportunities, and wider cultivation across certified organic farmland in key producing states.

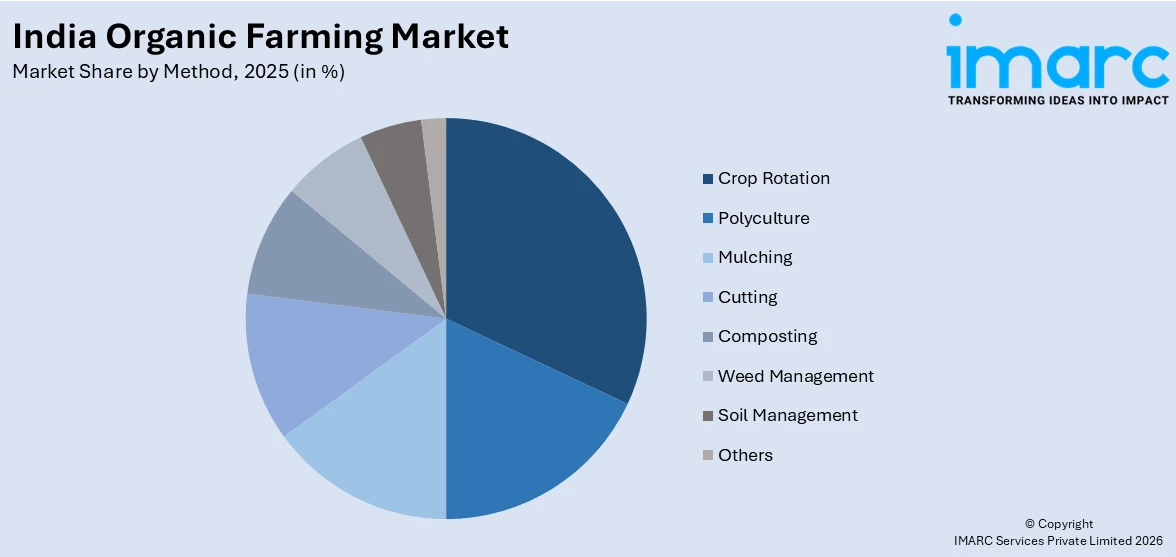

- By Method: Crop rotation leads the market with a share of 32.8% in 2025, owing to its ability to improve soil fertility, reduce pest incidence naturally, enhance yield stability, and support long term sustainable agricultural practices.

- By Region: West India represents the largest segment with a market share of 36.5% in 2025, reflecting favorable agro-climatic conditions, strong farmer participation, established organic clusters, and supportive state level initiatives promoting certification and exports.

- Key Players: The India organic farming market features a competitive landscape characterized by the presence of established agribusiness firms, farmer producer organizations, certified cooperatives, and emerging startups focused on sustainable cultivation, processing, branding, and domestic and international distribution.

To get more information on this market Request Sample

The organic farming market in India is driven by rising health awareness, the growing demand for chemical free food, supportive government policies, and expanding export opportunities. Consumers across urban centers are actively shifting toward organic staples, fruits, and packaged products, encouraging retailers and brands to widen certified offerings. Government initiatives promoting soil health, reduced chemical fertilizer usage, and crop diversification are accelerating farmer participation. Financial assistance and direct income support schemes improve the economic viability of transitioning to organic practices. For example, in 2025, Prime Minister Narendra Modi stated that India is on track to become a global hub for organic farming while inaugurating the South India Natural Farming Summit in Coimbatore. He highlighted efforts to cut chemical fertilizer use and strengthen soil health, and released over INR 18,000 Crore under the PM-KISAN scheme benefiting around nine crore farmers, reinforcing sector growth momentum.

India Organic Farming Market Trends:

Farmer-Led Branding and Vertical Integration

A crucial trend in the India organic farming market is the movement toward farmer-led branding and partial vertical integration, enabling cultivators to capture greater value beyond primary production. Organized farmer groups are increasingly participating in certification, processing, packaging, and direct marketing to reduce reliance on intermediaries and strengthen income stability. This approach improves traceability, enhances product positioning, and builds localized brand identity rooted in origin and authenticity. It also supports collective bargaining power and structured aggregation of produce. An illustration of this trend is the 2025 launch of the ‘Bithoor Organic’ brand in Kanpur, backed by nearly 4,000 farmers under the Namami Gange scheme. Supported by local Farmer Producer Organizations, the initiative markets certified wheat flour, millets, pulses, mustard oil, turmeric, and traditional snacks, strengthening direct market access and regional self-reliance.

Expansion of Advanced Biological Input Solutions

The increasing adoption of scientifically developed biofertilizers and microbial inputs is strengthening the foundation of organic cultivation in India. Farmers are gradually shifting toward biologically derived crop nutrition and soil enhancement solutions to improve productivity while maintaining compliance with organic standards. Collaboration between cooperatives and biotechnology firms is accelerating domestic production and distribution of advanced agri-biosolutions. These inputs support root development, nutrient absorption, and soil vitality, thereby reducing dependency on synthetic fertilizers. This shift reflects the growing confidence in research-backed biological technologies. In 2024, KRIBHCO introduced ‘KRIBHCO Rhizosuper’ in partnership with Novonesis, a granular biofertilizer using LCO promoter technology. With an annual capacity of up to 20,000 tons, the product aims to support crops such as rice, wheat, and pulses, expanding access to sustainable agricultural inputs nationwide.

Commercialization of Indigenous and Specialty Organic Crops

The structured promotion of indigenous and region-specific crops is emerging as a key growth driver within the organic farming market. Increased focus on preserving traditional seed varieties and cultural farming practices is aligning with rising consumer interest in nutritionally distinct and geographically unique products. Governments and local enterprises are facilitating market linkages to connect remote growers with premium buyers. This strategy enhances product differentiation and strengthens rural entrepreneurship. It also supports biodiversity conservation and sustainable land use in ecologically sensitive regions. In 2026, Arunachal Pradesh launched ‘Rakta’ rice, an organic indigenous red rice from Tawang district. Produced by Rakta Organic, the initiative highlights cultural heritage while linking high-altitude Monpa farmers to wider markets, promoting seed conservation and sustainable cultivation practices.

Market Outlook 2026-2034:

The India organic farming market is projected to demonstrate notable growth over the coming years, supported by increasing domestic consumption and rising export opportunities. Greater awareness about health, clean eating, and environmentally responsible farming practices is strengthening demand across metropolitan and tier two cities. The market generated a revenue of USD 6,133.68 Million in 2025 and is projected to reach a revenue of USD 14,826.30 Million by 2034, growing at a compound annual growth rate of 9.98% from 2026-2034. Policy initiatives promoting organic clusters and farmer training programs are improving adoption rates. Expansion of organized retail and digital grocery platforms is enhancing product availability. Growing interest from food processors and global buyers is also creating stable demand for certified organic produce.

India Organic Farming Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Crop Type |

Cereals and Grains |

32.5% |

|

Method |

Crop Rotation |

32.8% |

|

Region |

West India |

36.5% |

Crop Type Insights:

- Oilseeds and Pulses

- Cereals and Grains

- Fruits and Vegetables

- Others

The cereals and grains dominate with a market share of 32.5% of the total India organic farming market in 2025.

Cereals and grains lead the market due to their large cultivation base, steady domestic demand, and strong policy support. Staples like rice, wheat, and millets are widely grown across multiple states, making them a natural entry point for farmers shifting to organic practices. Public procurement programs and rising consumer preference for chemical free staples further strengthen their position. Export demand for organic basmati rice and specialty grains also adds momentum. Since cereals form a daily part of Indian diets, retailers and brands prioritize certified organic variants, ensuring consistent offtake and price realization for growers. This scale advantage secures sustained market leadership.

Cereals and grains also benefit from a robust existing infrastructure that minimizes risk for smallholders through established processing and storage networks. This institutional support was notably demonstrated in 2024, when Union Home Minister Amit Shah announced a strategic partnership between National Cooperative Organics Limited and Amul to distribute authenticated organic grains nationwide under the Bharat and Amul brands. By integrating such large-scale market access initiatives with the inherent yield stability of grains, the industry ensures consistent returns for Adivasi farmers while reinforcing the overall dominance of organic staples.

Method Insights:

Access the comprehensive market breakdown Request Sample

- Crop Rotation

- Polyculture

- Mulching

- Cutting

- Composting

- Weed Management

- Soil Management

- Others

The crop rotation leads with a share of 32.8% of the total India organic farming market in 2025.

Crop rotation represents the largest segment owing to its effectiveness in maintaining soil fertility and controlling pests without synthetic inputs. By alternating crops, such as cereals, pulses, and oilseeds across seasons, farmers naturally restore nutrient balance and break pest cycles. This approach reduces dependency on external organic fertilizers and biopesticides, lowering cultivation costs. It also improves soil structure and water retention, which is critical in rainfed regions. Agricultural extension programs and organic certification bodies actively promote rotation as a foundational practice. As it aligns with traditional Indian farming systems, adoption remains high across both smallholder and large organic farms nationwide.

Crop rotation also supports yield stability and long-term land productivity, making it attractive for farmers transitioning from conventional to organic systems. Rotating nitrogen fixing legumes with nutrient intensive crops enhances soil health and minimizes nutrient depletion. This method reduces weed pressure through varied planting patterns, limiting the need for mechanical intervention. Organic export buyers often prefer produce grown under structured rotation plans, as it strengthens traceability and compliance standards. State level organic missions emphasize rotation in training modules, reinforcing widespread implementation. Compared to monocropping, it lowers production risk and improves overall farm resilience, securing its leading position among organic farming methods in India.

Region Insights:

- North India

- South India

- East India

- West India

The West India exhibits a clear dominance with a 36.5% share of the total India organic farming market in 2025.

West India holds the biggest market share because of its large certified cultivation area and strong export orientation. States, such as Maharashtra, Gujarat, and Rajasthan, are actively promoting organic agriculture through state missions, farmer training programs, and cluster-based development models. The region has a diverse crop mix, including cotton, pulses, oilseeds, and cereals, supporting steady organic output. Favorable climatic conditions across semi-arid and dryland zones reduce pest pressure, making organic practices more viable. Export infrastructure at major ports like Mumbai and Kandla further strengthens trade in organic commodities, positioning West India as a key production and supply hub.

West India also benefits from well-organized farmer producer organizations and private sector participation that improve certification, aggregation, and market access. Contract farming models in organic cotton and oilseeds are encouraging structured supply chains and traceability systems. Several districts have developed dedicated organic clusters, enabling scale efficiencies and better price realization. For instance, in 2025, the Thane Municipal Corporation launched an experimental organic farming project on a 1.5-acre civic plot in Patlipada to promote sustainable urban agriculture. The initiative included cultivation of vegetables, grains, and fruit trees, along with an artificial pond, and aimed to encourage chemical-free farming and hands-on learning for city residents. These combined factors reinforce West India’s leadership in India’s organic farming market by region.

Market Dynamics:

Growth Drivers:

Why is the India Organic Farming Market Growing?

Institutional Support for Scientific Organic Crop Development

The growing involvement of agricultural universities and research institutions in structured organic crop programs is contributing to productivity improvements and commercialization. Scientific interventions focused on improved varieties, mechanized practices, and standardized cultivation methods are enhancing yield stability under organic conditions. This approach strengthens export competitiveness and supports regionally identified specialty products. Institutional programs also promote farmer training, market awareness, and quality consistency. The integration of research-driven cultivation with traditional farming knowledge is improving operational efficiency. In 2025, Bihar Agricultural University launched the Organic Makhana Cultivation Programme under its ‘Know Your Crop’ initiative, aiming to expand cultivation by 25–30%. The program included the release of Sabour Makhana-1 and emphasized organic practices, mechanization, and strengthening the GI-tagged Mithila makhana’s market potential.

Rising Health and Food Safety Awareness

The growing consumer awareness regarding the adverse effects of chemical residues in conventional produce is significantly driving the demand for organic food products in India. Urban households are increasingly prioritizing clean-label, minimally processed, and naturally cultivated food options. Concerns related to lifestyle diseases, immunity, and long-term well-being are influencing purchasing behavior across income groups. This shift in consumption patterns is encouraging retailers and food brands to expand their organic portfolios. As awareness deepens through media exposure and educational initiatives, sustained demand for certified organic fruits, vegetables, cereals, and processed foods continues to offer a favorable market outlook.

Technology-Enabled Cluster Development and Capacity Building

The formation of organized organic clusters supported by digital monitoring and structured training programs is a crucial factor impelling the market growth. Cluster-based models enable standardized certification processes, shared resources, and coordinated production planning. Integration of digital tools such as UAV-based monitoring and data systems enhances transparency, crop tracking, and compliance management. These initiatives strengthen scalability while improving farmer capabilities and traceability standards. Structured capacity-building programs also promote sustainable input usage and efficient resource management. An example is the 2025 organic agriculture project launched by NECTAR in Arunachal Pradesh under the PM-DevINE scheme. Covering 15 clusters across East and West Kameng districts, the initiative supported 1,500 farmers through PGS certification, seed banks, digital monitoring, and technology-driven organic cultivation systems.

Market Restraints:

What Challenges the India Organic Farming Market is Facing?

High Certification and Compliance Costs

Organic certification involves detailed documentation, inspections, and recurring renewal fees, increasing financial pressure on small and marginal farmers. The mandatory transition period before produce can be labeled organic limits immediate income realization. Limited awareness about certification procedures and costs further discourages farmers from adopting organic practices at scale across different regions in India.

Lower Initial Yields and Limited Technical Knowledge

Farmers shifting to organic cultivation often face reduced yields during the initial years as soil health stabilizes and natural pest control methods take effect. Insufficient access to quality organic inputs, bio-fertilizers, and expert guidance restricts productivity. Limited extension services and training programs slow knowledge transfer and hinder consistent implementation of organic farming standards.

Supply Chain and Market Access Constraints

The organic farming sector faces challenges related to fragmented supply chains, inadequate cold storage facilities, and limited processing infrastructure. These gaps affect product quality, increase post-harvest losses, and reduce profitability. Uneven market linkages and price fluctuations create uncertainty for farmers, especially in remote areas with limited access to organized retail channels.

Competitive Landscape:

Key players in the India organic farming market are focusing on expanding certified cultivation areas, strengthening farmer networks, and improving traceability systems to ensure quality and compliance with domestic and export standards. Many companies are investing in contract farming models and collaborating with farmer producer organizations to secure consistent raw material supply. They are also enhancing processing, packaging, and branding capabilities to capture premium user segments. Strategic partnerships with retail chains and e-commerce platforms are improving product reach across urban markets. Several players are promoting value-added organic products, including ready-to-cook (RTC) and packaged food items, while investing in awareness campaigns to build consumer trust and drive repeat purchases.

Recent Developments:

- September 2025: Tripura announced an organic mushroom cultivation initiative to reduce imports and move toward self-sufficiency in production. The program was launched at the Horticulture Research Complex, Nagichhara, with participation from 53 Farmer Producer Companies, aiming to integrate mushrooms into 26,000 hectares of organic farmland. The state government highlighted mushrooms as a nutrient-rich crop and positioned the initiative as a step toward sustainable agriculture and stronger rural incomes.

- August 2025: A Youth Farming Internship Programme was launched in Chennai by We The Leaders Foundation in collaboration with IIT-M Research Park to promote hands-on exposure to organic farming. The initiative allowed urban students to spend two or seven days on organic farms, learning directly from experienced farmers. The program aimed to connect modern technology and sustainable practices with traditional agricultural knowledge, encouraging youth to view farming as a viable and innovative career option.

India Organic Farming Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Crop Types Covered | Oilseeds and Pulses, Cereals and Grains, Fruits and Vegetables, Others |

| Method Covered | Crop Rotation, Polyculture, Mulching, Cutting, Composting, Weed Management, Soil Management, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Organic Farming Market Report

The India organic farming market size was valued at USD 6,133.68 Million in 2025.

The India organic farming market is expected to grow at a compound annual growth rate of 9.98% from 2026-2034 to reach USD 14,826.30 Million by 2034.

Cereals and grains dominate the market with a share of 32.5% in 2025, supported by strong domestic consumption of staple foods such as rice, wheat, and millets, rising health awareness, expanding export demand, and wider availability of certified organic acreage across major agricultural states.

Key factors driving the India organic farming market include the rising adoption of scientifically developed biofertilizers and microbial inputs, supported by partnerships between cooperatives and biotechnology firms, as seen in KRIBHCO’s 2024 launch of ‘KRIBHCO Rhizosuper’ with Novonesis to expand sustainable crop nutrition solutions nationwide.

Major challenges in the market include high certification and compliance costs, lower initial yields during transition, limited technical knowledge and access to organic inputs, along with fragmented supply chains, inadequate storage infrastructure, price volatility, and weak market linkages affecting farmer profitability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)