India Organic and Natural Pet Food Market Size, Share, Trends and Forecast by Pet Type, Product Type, Packaging Type, Distribution Channel, and Region, 2026-2034

India Organic and Natural Pet Food Market Size, Share, Trends & Forecast (2026-2034)

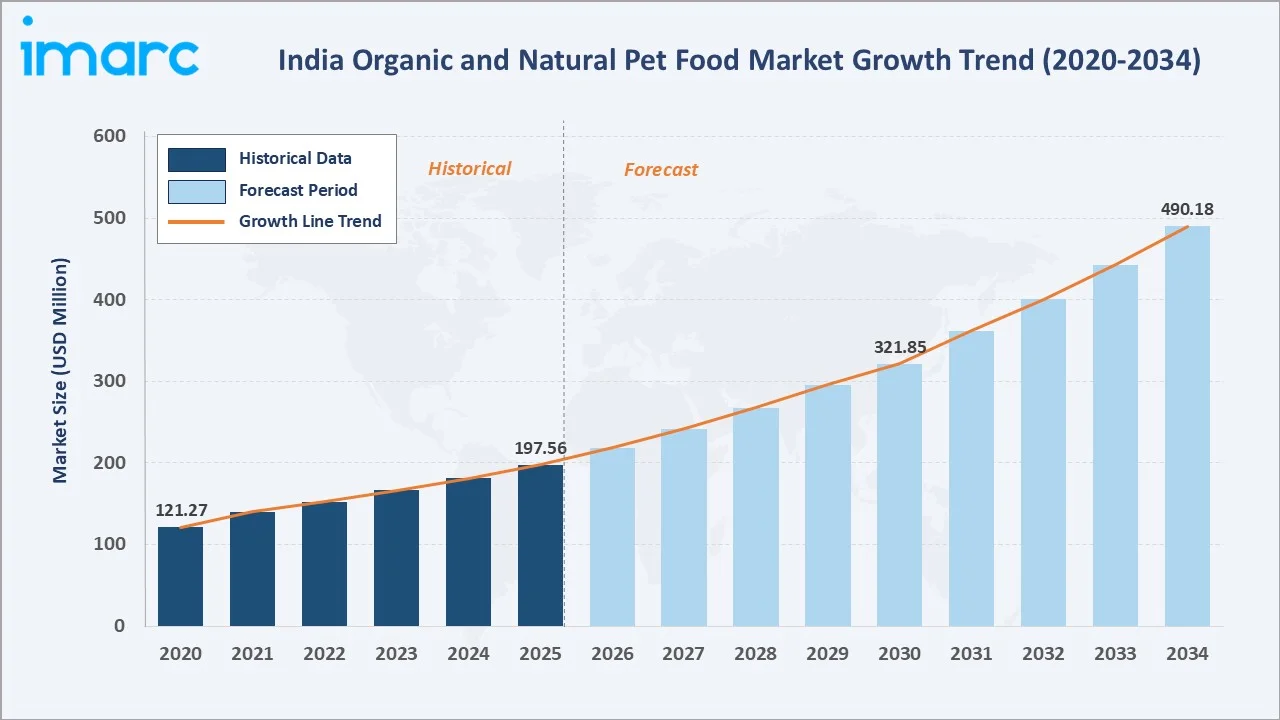

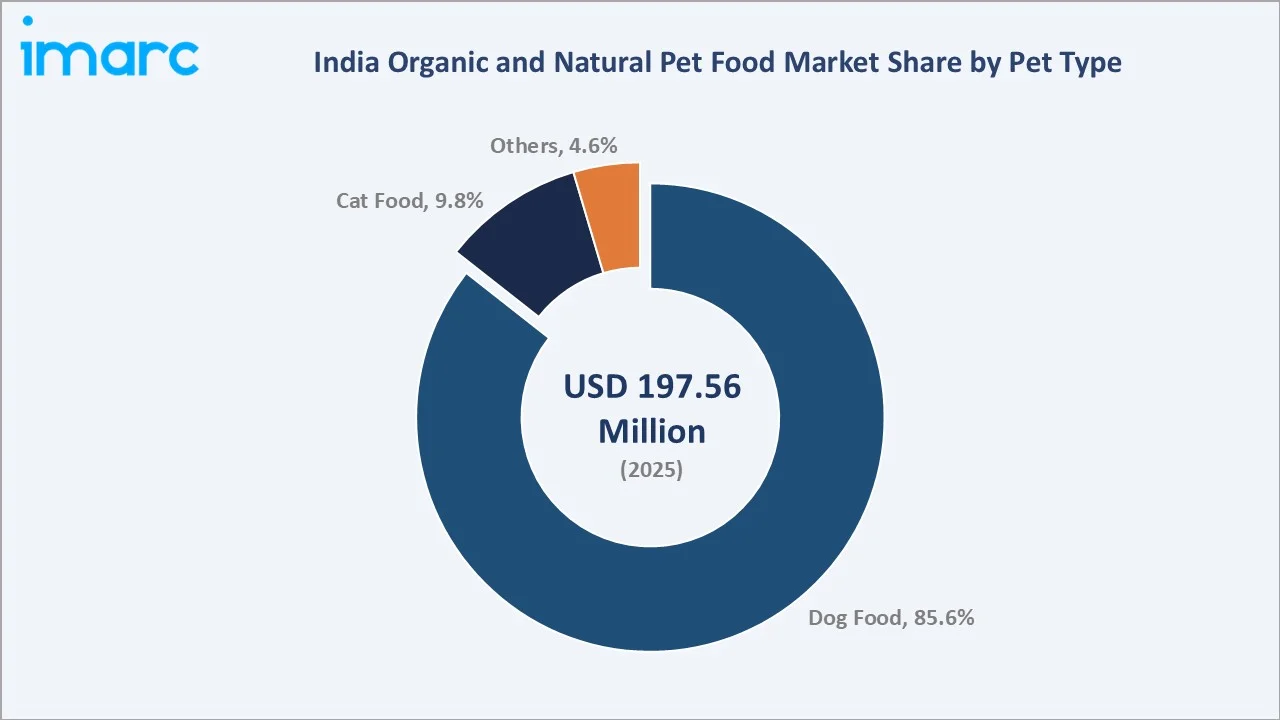

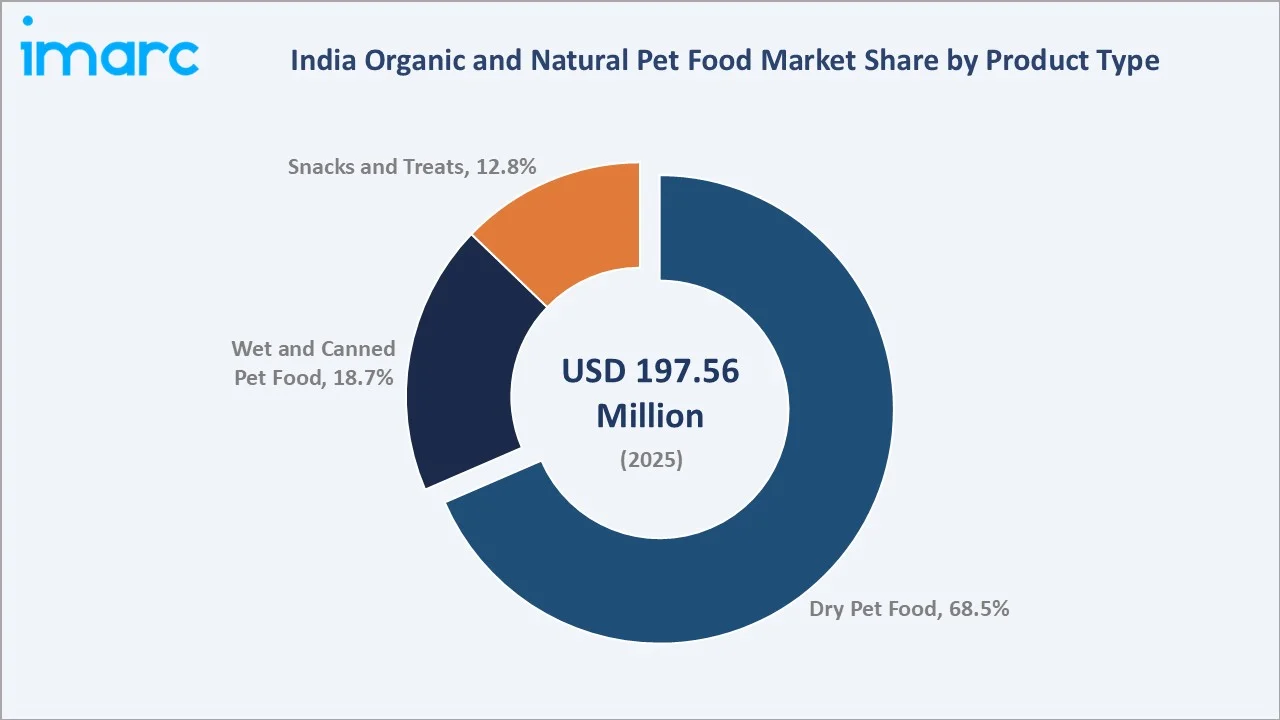

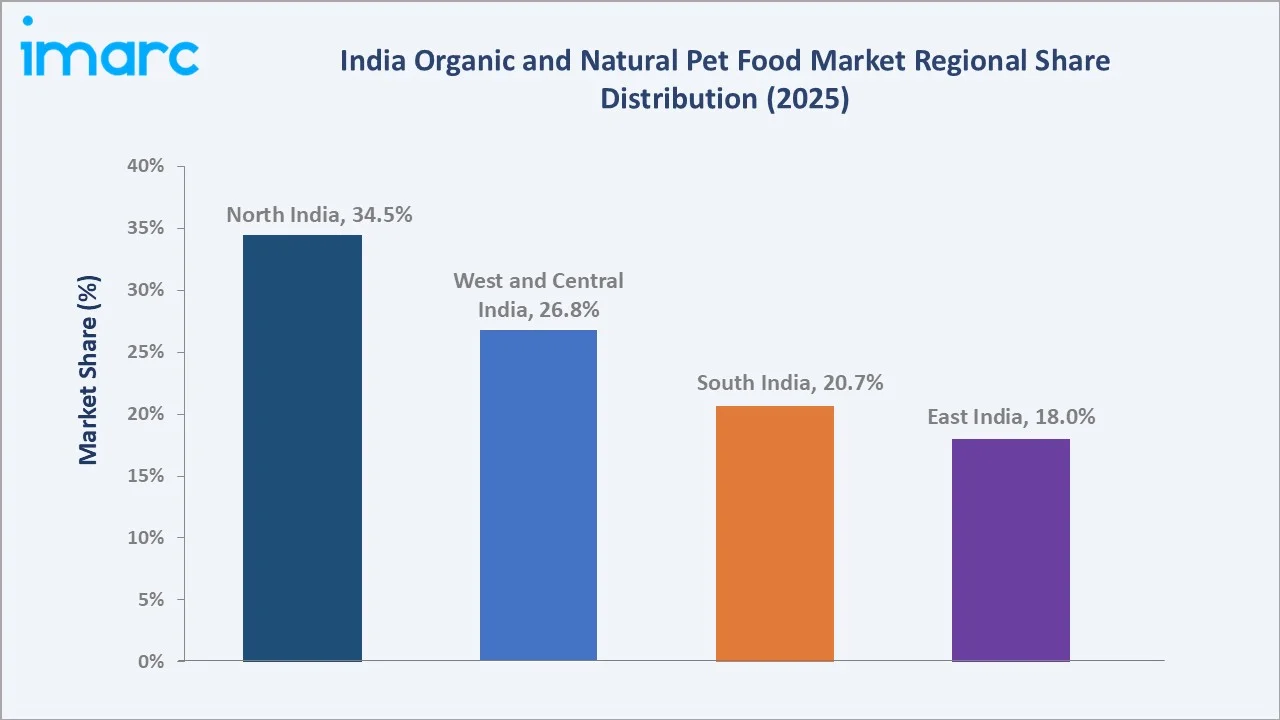

The India organic and natural pet food market size increased from USD 197.56 Million in 2025 to USD 217.82 Million in 2026 and is projected to reach USD 490.18 Million by 2034, exhibiting a CAGR of 10.25% during 2026-2034. Rising pet humanisation, premiumisation of pet diets, expanding e-commerce penetration, and growing clean-label awareness are driving market growth. Dog Food leads pet type at 85.6% in 2025, while Dry Pet Food dominates the product category at 68.5%. North India accounts for 34.5% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Base Year Market Size (2025) |

USD 197.56 Million |

|

Market Size 2026 |

USD 217.82 Million |

|

Forecast Market Size (2034) |

USD 490.18 Million |

|

CAGR (2026-2034) |

10.25% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (34.5% share, 2025) |

|

Fastest Growing Region |

South India (CAGR ~12.6%) |

|

Leading Pet Type |

Dog Food (85.6%, 2025) |

|

Leading Product Type |

Dry Pet Food (68.5%, 2025) |

The India organic and natural pet food market trajectory from 2020 through 2034 reflects a consistent historical expansion base against a sustained forecast curve, powered by rising urban pet ownership, premium product adoption, and faster D2C and online retail penetration.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight Snacks and Treats and Functional Nutrition as fastest growing sub-categories within the India organic pet food industry through 2034, while online channel growth at 14.5% CAGR remains the most disruptive structural shift.

Executive Summary

The India organic and natural pet food market is undergoing a fundamental transformation driven by pet humanisation, premiumisation, and digital channel disruption. Valued at USD 197.56 Million in 2025, to USD 217.82 Million in 2026 and it is forecast to reach USD 490.18 Million by 2034, at a CAGR of 10.25%. India's pet population reached nearly 32 million in 2024, with urban households accounting for a significant share of total spend, marking a structural shift where pets are treated as family members deserving clean-label nutrition equivalent to human food standards.

Dog Food commands the dominant pet type share at 85.6% in 2025, driven by India's deep dog ownership culture and breed-specific organic SKU launches. Dry Pet Food at 68.5% leads product type categories, supported by lower per-meal cost, longer shelf life, and the broadest distribution footprint.

North India dominates with a 34.5% revenue share in 2025, led by Delhi NCR's high pet density and premium retail penetration. West and Central India account for a 26.8% share in 2025 and represent the second-fastest growing region, with cities such as Mumbai, Pune, and Ahmedabad showing strong pet food spend.

Key Market Insights

|

Insight |

Data |

|

Largest Pet Type Segment |

Dog Food - 85.6% share (2025) |

|

Largest Product Segment |

Dry Pet Food - 68.5% share (2025) |

|

Leading Region |

North India - 34.5% share (2025) |

|

Second Region |

West and Central India - 26.8% share (2025) |

|

Top Companies |

Mars India, Drools Pet Food Pvt. Ltd., Nestle S.A, Earth Paws Private Limited., Vivaldis, Wiggles, Dogseechew, Supertails, and Goofy Tails Private Limited. |

Key Analytical Observations Supporting the Above Data:

- Dog Food's 85.6% dominance in 2025 reflects India's culture of dog-first pet ownership and the wide assortment of breed-specific organic SKUs across small, medium, and large breeds.

- Dry Pet Food leads at 68.5% in 2025, driven by convenience, lower per-meal cost, wider organised retail availability, and easy storage in Indian household conditions.

- North India's 34.5% regional dominance in 2025 reflects Delhi NCR's role as the country's largest urban pet hub combined with the highest premium pet food retail penetration in India.

India Organic and Natural Pet Food Market Overview

Organic and natural pet food refers to feed products formulated using ingredients free from synthetic pesticides, antibiotics, growth hormones, and artificial preservatives. The category spans dry kibble, wet meals, treats, and freeze-dried offerings, with formulations integrating organic proteins, plant-based fibres, vitamins, and functional add-ins for joint, skin, coat, and gut health benefits.

Applications span the full pet care spectrum: companion dogs, cats, small mammals, and birds. Macroeconomic enablers include rising household incomes, expanding pet ownership with pet dogs and cats in India accounting for approximately 23 million and 1.7 million respectively in 2023, and consumer expectation convergence between human food quality and pet nutrition.

Market Dynamics

To evaluate market opportunities, Request Sample

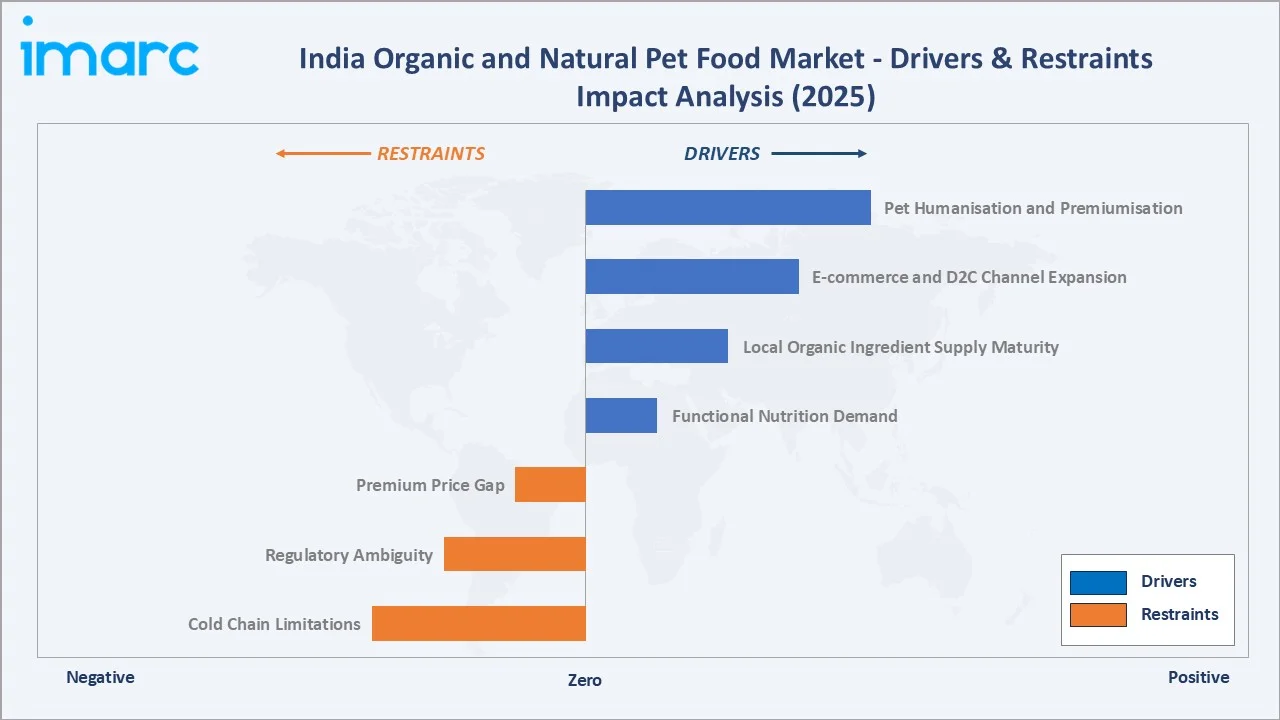

Market Drivers

- Pet Humanisation and Premiumisation: Total pet care spend in India more than doubled from USD 1.6 billion in 2019 to USD 3.6 billion in 2024, reflecting a sharp rise in per-owner expenditure on premium nutrition and wellness products.

- E-commerce and D2C Channel Expansion: Online pet food sales are rising rapidly, driven by convenience, wider availability, and growing subscription adoption.

- Local Organic Ingredient Supply Maturity: Expanding organic ingredient supply is improving availability, reducing costs, and supporting wider adoption.

- Functional Nutrition Demand: Premium and super-premium pet food segments in India grew at over 20% annually in 2024, significantly outpacing overall market growth, driven by demand for joint, digestive, and skin/coat formulations.

Market Restraints

- Premium Price Gap: Organic pet food is significantly more expensive than conventional alternatives, limiting adoption beyond metro cities. Tier 3 city penetration remains low in 2025.

- Regulatory Ambiguity: FSSAI introduced pet food regulations, but specific organic certification pathways remain fragmented, leading to consumer confusion.

- Cold Chain Limitations: Cold chain coverage outside the top cities remains limited, restricting wet and fresh-format penetration in eastern and central India.

Market Opportunities

- Tier 2 City Expansion: Metro cities account for approximately 60% of India's packaged pet food demand, leaving Tier 2 and Tier 3 cities as a largely underpenetrated growth runway.

- Functional and Therapeutic Categories: Veterinary therapeutic diets are projected to grow their share of India's total pet food revenue from 4% to 12% by 2030, underpinned by new pet insurance schemes reimbursing up to 80% of prescription diet costs.

- Subscription Commerce Models: D2C subscription delivery saw strong year-on-year growth in 2024, increasing customer lifetime value and reducing acquisition costs.

Market Challenges

- Crowded D2C Brand Landscape: Rising number of D2C brands is intensifying competition and increasing customer acquisition costs.

- Input Cost Volatility: Dependence on imported organic ingredients exposes brands to currency fluctuations and cost uncertainty.

- Awareness Gap in Non-Metro Markets: Limited pet food awareness in rural areas restricts market expansion and requires continuous consumer education.

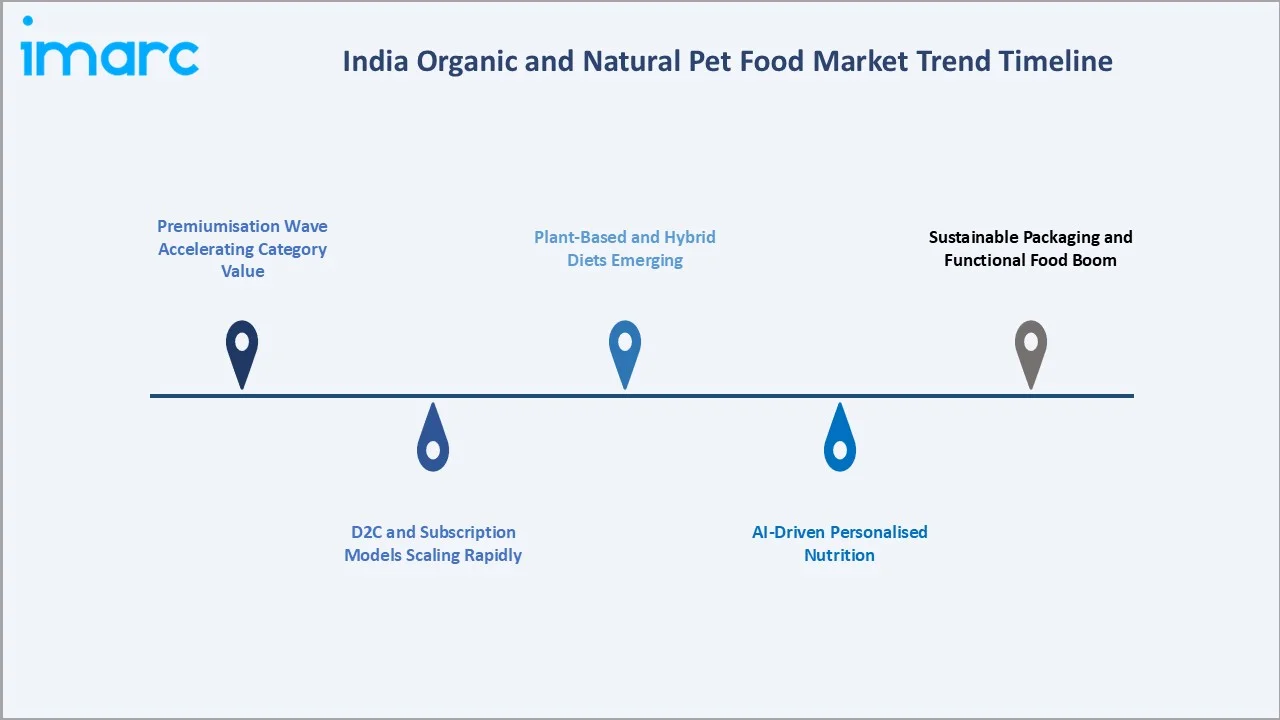

Emerging Market Trends

1. Premiumisation Wave Accelerating Category Value

India's premium and super-premium pet food segments grew over 20% annually in 2024, more than double the overall market pace. Urban pet parents increasingly equate price with safety, paying up to 3x standard kibble prices for ingredient transparency and traceability.

2. D2C and Subscription Models Scaling Rapidly

Subscription customers demonstrate significantly higher purchase frequency and basket size than transactional buyers in India, committed subscribers are spending ₹1,000–₹15,000 per month on pet food alone, reshaping unit economics for D2C brands.

3. Plant-Based and Hybrid Diets Emerging

Plant-forward formulations with insect protein or pulse blends entered India in 2023, and while adoption remains nascent, growth is accelerating rapidly among environmentally conscious millennial buyers in metros.

4. AI-Driven Personalised Nutrition

Brands like Wiggles and Henlo combine breed, age, and weight data to customise meal plans. Online channels now account for over 25% of organised pet food sales in India as of 2024, with customised diet offerings cited as a leading growth driver for D2C brands.

5. Sustainable Packaging and Functional Food Boom

Recyclable kraft pouches and compostable scoops are appearing across new launches, with a growing share of new SKUs featuring low-plastic packaging. Functional formulas have emerged as the fastest-growing sub-category, driven by rising consumer demand for health-forward nutrition.

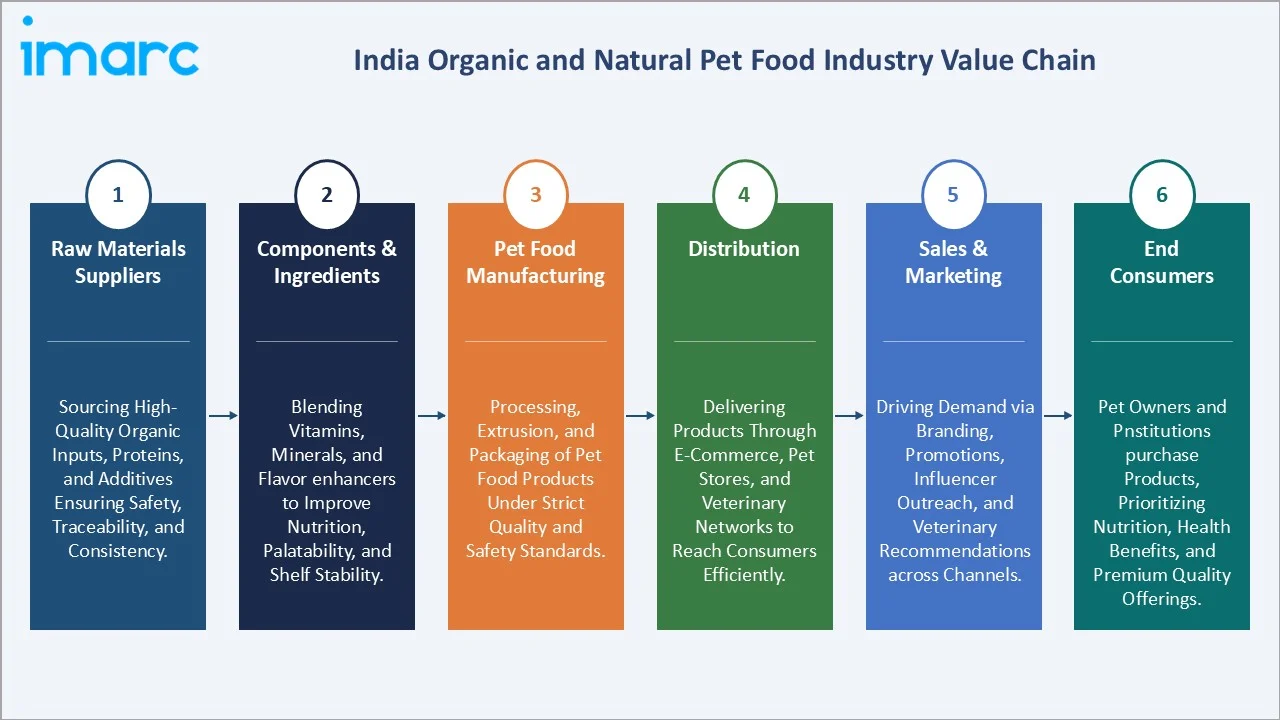

Industry Value Chain Analysis

The India organic and natural pet food value chain spans six integrated stages from organic ingredient sourcing through end-consumer delivery. Each stage presents distinct competitive dynamics and margin profiles, with brand and retail stages capturing the highest profit pools.

|

Stage |

Key Players / Examples |

|

Raw Materials Suppliers |

Sourcing high-quality organic inputs, proteins, and additives ensuring safety, traceability, and consistency. |

|

Components & Ingredients |

Blending vitamins, minerals, and flavor enhancers to improve nutrition, palatability, and shelf stability. |

|

Pet Food Manufacturing |

Processing, extrusion, and packaging of pet food products under strict quality and safety standards. |

|

Distribution |

Delivering products through e-commerce, pet stores, and veterinary networks to reach consumers efficiently. |

|

Sales & Marketing |

Driving demand via branding, promotions, influencer outreach, and veterinary recommendations across channels. |

|

End Consumers |

Pet owners and institutions purchase products, prioritizing nutrition, health benefits, and premium quality offerings. |

Manufacturers and brand owners occupy the highest strategic position in the India organic pet food value chain, integrating ingredient sourcing, formulation, and brand equity into branded products. However, this position is increasingly challenged by D2C-native brands compressing the chain by going direct to consumers.

Technology Landscape in the India Organic Pet Food Industry

Ingredient Innovation: Novel Proteins and Plant-Forward Formulations

The Indian pet food industry is exploring next-generation proteins including insect meal, single-source novel proteins (duck, venison, lamb), and pulse-based blends. Trial production volumes grew 4x between 2022 and 2025, with Drools and Henlo introducing limited-batch novel-protein SKUs in 2024-2025.

Smart Connectivity and AI-Driven Personalisation

Brands now combine veterinary records, breed databases, and at-home weight scales to power personalised subscription nutrition. Leading platforms like Supertails have served over 100,000 pet parents since 2021, with AI-driven recommendation engines and vet consultation services driving rapid digital adoption.

Manufacturing Automation and Quality Control

Automated extrusion lines and inline NIR quality sensors are increasingly being adopted across leading Indian pet food plants. This has cut production wastage and improved batch consistency for organic SKUs, where ingredient variability historically posed higher risk.

Sustainable Packaging Technology

Mono-material recyclable pouches, compostable inner liners, and refillable bulk dispensers are being trialled by Mars Petcare India and select D2C brands. India's recent Extended Producer Responsibility mandate, requiring 30% recycled PET content from 2025-26 rising to 40%.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Pet Type | Dog Food | 85.6% | 2025 |

| Product Type | Dry Pet Food | 68.5% | 2025 |

| Packaging Type | Bags | 52.8% | 2025 |

| Distribution Channel | Online Stores | 38.5% | 2025 |

| Region | North India | 34.5% | 2025 |

By Pet Type

Dog Food commands an 85.6% majority share in 2025, reflecting India's deeply rooted dog ownership culture and the broad assortment of breed-specific organic formulations across small, medium, and large breeds. The segment benefits from the largest installed pet base nationally and a strong premium SKU pipeline.

To access detailed market analysis, Request Sample

Cat Food at 9.8% in 2025 is the fastest growing pet type segment, driven by rising feline adoption in urban households where smaller living spaces make cats an increasingly popular companion animal. Lower maintenance demand, growing urban apartment living, and the rise of single-pet households in metros are accelerating cat ownership. Others (4.6%) covers small mammals, birds, and exotic pets.

By Product Type

Dry Pet Food dominates with 68.5% share in 2025, supported by lower per-meal cost, longer shelf life, easy storage, and the broadest distribution footprint across organised retail and e-commerce. Premium organic dry kibble remains the entry SKU for most pet parents transitioning from conventional feed.

Wet and Canned Pet Food at 18.7% in 2025 is gaining traction among senior pets and dental-sensitive breeds, supported by improved cold chain coverage in metros. Snacks and Treats at 12.8% is the fastest growing product, as functional treats like dental sticks, joint chews, and training rewards gain shelf space.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

34.5% |

Delhi NCR pet density, Punjab/Haryana income growth, premium retail penetration |

|

West and Central India |

26.8% |

Mumbai-Pune affluence, strong specialty store presence, robust e-commerce reach |

|

South India |

20.7% |

Bengaluru tech-millennial spend, rising cat ownership, fastest growth pace |

|

East India |

18.0% |

Kolkata urban core, growing Tier 2 demand, expanding cold chain infrastructure |

North India commands a 34.5% revenue share in 2025, anchored by Delhi NCR which represents the largest single-city pet food market in India alongside Mumbai and Bengaluru. The region benefits from the highest premium retail penetration and a robust specialty pet store network driving premiumisation.

South India holds 20.7% in 2025 and is the fastest growing region. Tech-millennial buying patterns, strong online subscription adoption, and rising cat ownership are the primary drivers. East India at 18.0% remains the smallest region but is benefiting from rapid Tier 2 expansion in Bhubaneswar, Patna, and Guwahati.

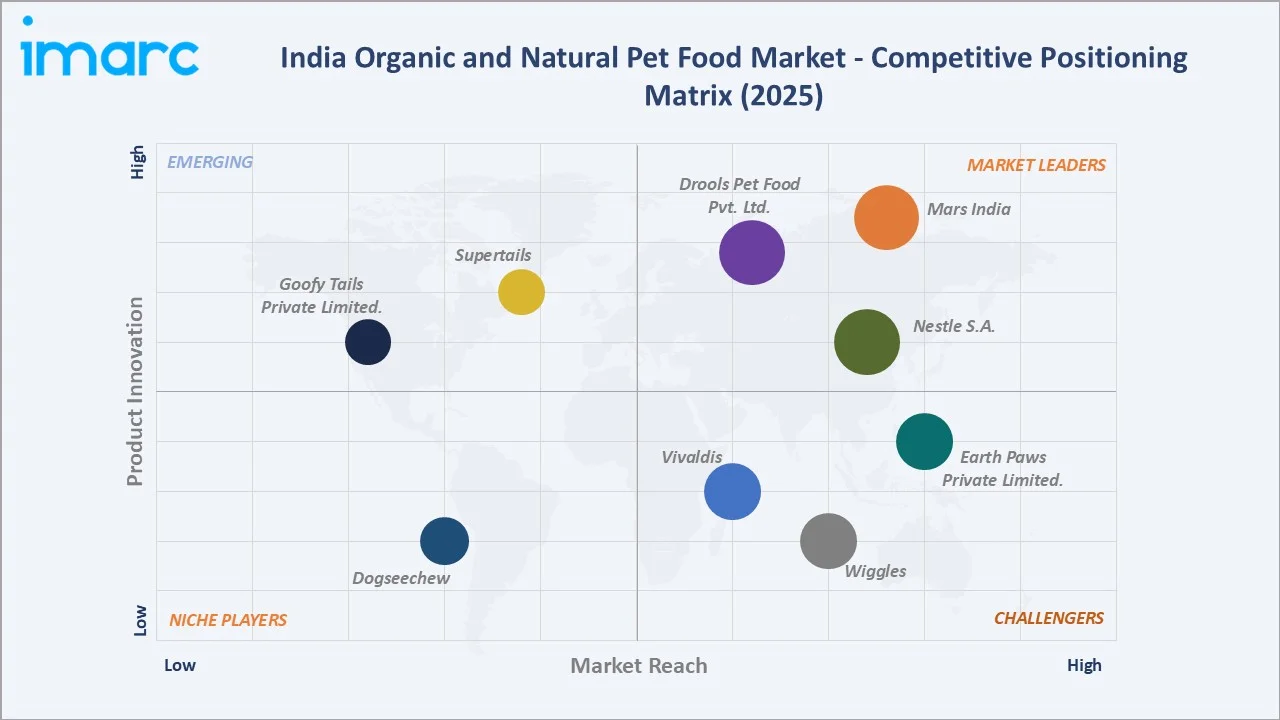

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Mars India |

Nutro |

Leader |

Largest portfolio, breed-specific nutrition, vet partnerships |

|

Drools Pet Food Pvt. Ltd. |

Drools |

Leader |

Domestic manufacturing, fastest scaling, Tier 2 distribution |

|

Nestle S.A. |

Nestle Purina |

Leader |

Global R&D depth, organised retail tie-ups, life-stage SKUs |

|

Earth Paws Private Limited. |

HUFT |

Challenger |

Vertical retail integration, 90+ stores, premium private label |

|

Vivaldis |

Bark Out Loud |

Challenger |

Vet-clinic distribution, premium imported brand portfolio |

|

Wiggles |

Wiggles |

Challenger |

AI-driven personalised nutrition, D2C subscription model |

|

Dogseechew |

Dogsee Chew |

Niche |

Yak milk treats, export-led brand, premium positioning |

|

Supertails |

Henlo |

Emerging |

D2C-native, novel protein SKUs, millennial brand voice |

|

Goofy Tails Private Limited. |

Goofy Tails |

Emerging |

Functional treats, online-first distribution, value pricing |

The India organic pet food competitive landscape is moderately concentrated. Multinational players Mars Petcare, Nestle, and domestic leader Drools collectively command an estimated 52-58% of market revenue in 2025. The remaining 42-48% is fragmented across challengers and 35+ D2C brands competing on transparency, ingredient innovation, and personalised delivery.

Key Company Profiles

Mars India

Mars Petcare India is the largest pet food company in India, operating Pedigree, Royal Canin, and Whiskas, with a manufacturing facility in Chittoor, Andhra Pradesh.

- Product Portfolio: Pedigree, Royal Canin, Whiskas, plus organic and natural extensions launched in 2024.

- Recent Developments: In 2024, Mars Petcare advanced its Hyderabad plant expansion with a second dry extruder line and boosted packing capacity, lifting total production to 65,000 tons of dry food annually. The company stated this capacity is sufficient to cover Indian market demand and cater to exports across Asia.

- Strategic Focus: Breed-specific premium nutrition, deepening veterinary channel partnerships across 6,500+ vet clinics, and building organic SKU depth within mainstream brand equity.

Drools Pet Food Pvt. Ltd.

Drools is one of India's fastest scaling domestic pet food brands with manufacturing in Bengaluru, serving India and select export markets across Asia and the Middle East.

- Product Portfolio: Dry food (puppy/adult/senior), wet food, treats, and natural variants with chicken, lamb, and fish-based formulations.

- Recent Developments: In May 2025, Drools became India's first pet food unicorn after Nestlé S.A. acquired a minority stake, valuing the company at over USD 1 billion.

- Strategic Focus: Domestic manufacturing leadership, scaling premium and natural variants, and building India's first vertically integrated pet nutrition brand with farm-to-bowl traceability.

Earth Paws Private Limited.

Heads Up For Tails operates as a vertically integrated pet retail and product brand with 90+ stores across India, covering food, accessories, grooming, and private-label organic SKUs.

- Product Portfolio: HUFT private-label organic and grain-free food, multi-brand retail, accessories, and premium grooming and pet wellness offerings.

- Recent Developments: In 2025, Earth Paws Private Limited (HUFT) entered advanced talks to raise approximately USD 25 million in Series B funding led by Apparel Group India, after earlier discussions in January 2025 to raise USD 40 million.

- Strategic Focus: Vertical retail-to-product integration, premium private-label expansion, and omnichannel customer experience.

Market Concentration Analysis

The India organic and natural pet food market exhibits moderate concentration. The top 5 companies (Mars, Drools, Nestle, HUFT, and Vivaldis) collectively account for approximately 52-58% of total market revenue in 2025, indicating leadership clarity at the top while leaving meaningful room for challengers.

The remaining 42-48% is distributed across D2C and emerging brands competing on niche positioning, premium ingredients, and digital-native marketing. Fragmentation is highest in snacks and treats, where new SKU launches grew over 60% between 2022 and 2025.

Consolidation is expected to accelerate by 2027-2028, driven by venture-funded D2C brands seeking scale through M&A and multinational players acquiring local capabilities. At least four strategic deals have been recorded in Indian pet care since 2023, signalling the structural shift underway.

Investment & Growth Opportunities

Fastest-Growing Segments

Snacks and Treats and functional nutrition sub-categories offer the strongest near-term opportunity. Pet parents are willing to pay premiums for joint, gut, and skin coat benefits, lifting category margins above the market average.

Emerging Geographic Markets

Tier 2 and Tier 3 cities including Indore, Jaipur, Coimbatore, Bhubaneswar, and Lucknow are emerging as high-growth pockets. Combined organic pet food spend in these cities rose from USD 18 Million in 2020 to over USD 41 Million in 2024, more than doubling in four years.

Venture & Private Investment Trends

Venture investment in Indian pet food and pet care startups crossed USD 95 Million in 2024, up from USD 22 Million in 2020, reflecting more than 4x growth. Subscription D2C, fresh-meal kitchen models, AI-personalised nutrition, and pet pharma have attracted the bulk of recent funding rounds.

Future Market Outlook (2026-2034)

The market forecast projects to grow from USD 292.62 Million in 2025 to USD 217.82 Million in 2026, reaching USD 197.56 Million by 2034 to USD 490.18 Million at a CAGR of 10.25%. This near 2.5x expansion is underpinned by deeper urban premium adoption, Tier 2 retail spread, and a structural shift from private kibble to branded clean-label SKUs.

Three discontinuities are most likely to reshape the market through 2034. AI-driven personalised nutrition will mature from niche to mainstream by 2028-2030. Sustainable packaging mandates will reshape SKU economics. Functional and therapeutic nutrition will move from premium niche to mainstream growth engine.

By 2034, the India organic and natural pet food industry will have transformed from a metro-only premium niche to a mainstream urban category. The competitive landscape will be shaped by three archetypes: established multinational and domestic leaders, AI-personalised D2C subscription platforms, and vet-clinic-led therapeutic specialists.

Research Methodology

Primary Research

Primary research encompassed over 60 structured interviews conducted in 2024-2025 with India pet care industry stakeholders including product directors at leading pet food brands, retail and e-commerce category managers, veterinarians, ingredient suppliers, and pet parents across six metros. Primary insights validated market sizing, segmentation, channel growth, and competitive positioning.

Secondary Research

Secondary sources include FSSAI pet food regulatory filings (2024), MCA company financial filings, IBEF and Invest India industry data, IMARC's proprietary pet care database, Nielsen retail audits, Kantar consumer panels, and trade publications including PetBiz World.

Forecasting Models

Market sizing and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth, urban household income trends, pet ownership penetration, and historical evolution patterns. Scenario analysis was performed to account for macroeconomic uncertainty.

India Organic and Natural Pet Food Market Report Coverage

|

Attribute |

Details |

|

Market Size (2025) |

USD 197.56 Million |

|

Market Forecast (2034) |

USD 490.18 Million |

|

CAGR (2026-2034) |

10.25% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation Covered |

Pet Type, Product Type, Packaging Type, Distribution Channel, Region |

|

Regional Analysis |

North India, West and Central India, South India, East India |

|

Companies Covered |

Mars India, Drools Pet Food Pvt. Ltd., Nestle S.A., Earth Paws Private Limited., Vivaldis, Wiggles, Dogseechew, Supertails, and Goofy Tails Private Limited., etc. |

|

Customisation Scope |

10% free customisation, additional customisation on request |

|

Report Format |

PDF + Excel |

Frequently Asked Questions About the India Organic and Natural Pet Food Market Report

The India organic and natural pet food market reached USD 197.56 Million in 2025, driven by pet humanisation, premiumisation, and e-commerce growth.

The market is projected to reach USD 490.18 Million by 2034, growing at a CAGR of 10.25% during 2026-2034.

Dog Food leads with an 85.6% share in 2025, supported by India's deep dog ownership culture and breed-specific organic SKUs.

Dry Pet Food dominates with 68.5% share in 2025, supported by lower per-meal cost, longer shelf life, and broad availability.

North India commands a 34.5% share in 2025, anchored by Delhi NCR pet density, premium retail penetration, and rising disposable incomes.

Key drivers include pet humanisation, e-commerce growth at 32% CAGR, local organic ingredient supply maturity, and rising functional nutrition demand.

Snacks and Treats and functional nutrition formulas grow fastest at 13-14% CAGR through 2034, driven by joint and skin health demand.

Leading companies include Mars India, Drools Pet Food Pvt. Ltd., Nestle S.A., Earth Paws Private Limited., Vivaldis, Wiggles, Dogseechew, Supertails, and Goofy Tails Private Limited.

Online channels accounted for 28% of organic pet food sales in 2025, doubling from 2021 and growing at 32% CAGR.

Premium pricing 35-60% above conventional feed, regulatory ambiguity, cold chain limitations beyond top 8 cities, and rural awareness gaps.

By 2025, 19% of new India organic pet food SKUs feature low-plastic packaging, addressing millennial sustainability preferences.

The report covers segmentation by Pet Type, Product Type, Packaging Type, Distribution Channel, and four Indian regions across 2020-2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade