India Orthopedic Braces and Supports Market Size, Share, Trends and Forecast by Product, Type, Application, End User, and Region, 2026-2034

India Orthopedic Braces and Supports Market Summary:

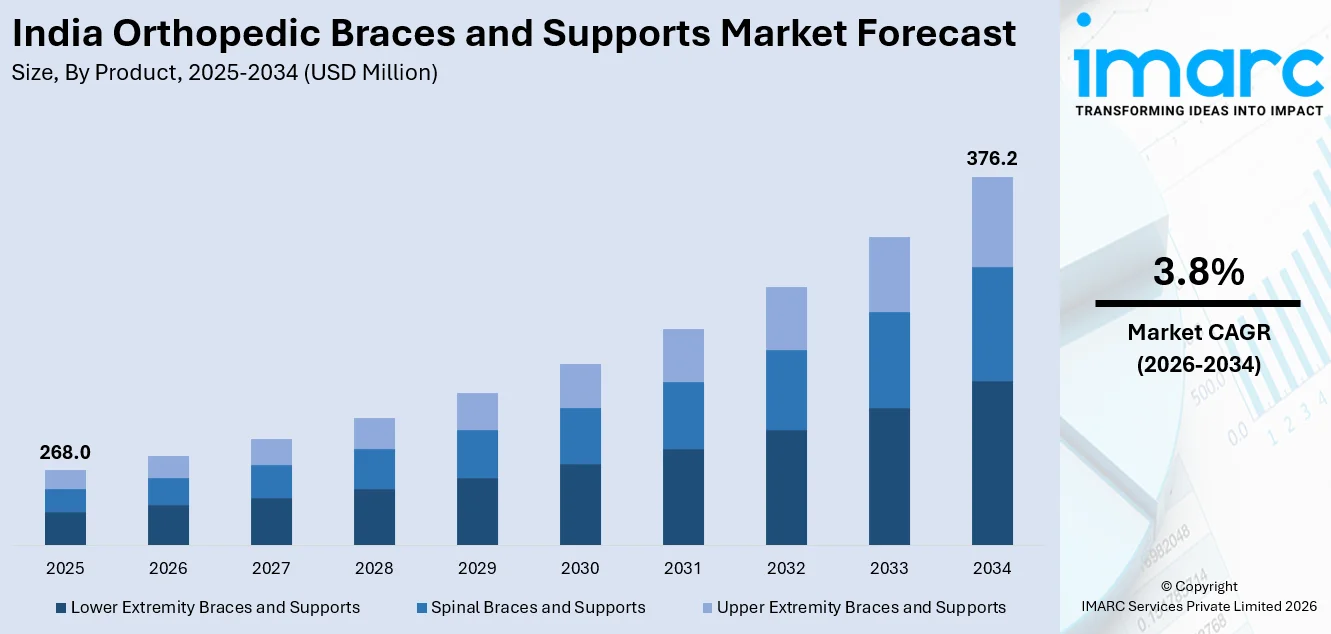

The India orthopedic braces and supports market size was valued at USD 268.0 Million in 2025 and is projected to reach USD 376.2 Million by 2034, growing at a compound annual growth rate of 3.8% from 2026-2034.

The Indian market for orthopedic braces and supports is growing steadily, thanks to the rising number of musculoskeletal disorders, sports injuries, and the geriatric population. Increasing awareness about preventive orthopedic care, improved healthcare infrastructure, and increased accessibility to orthopedic care are opening up new avenues for the adoption of orthopedic braces and supports. Advances in orthopedic brace design and materials, along with improved distribution channels, are working together to strengthen the market share of the India orthopedic braces and supports market.

Key Takeaways and Insights:

- By Product: Lower extremity braces and supports leads the market with a share of 40% 2025, driven by widespread knee and ankle injuries, high physical activity, and growing preference for non-invasive injury management across India.

- By Type: Soft and elastic braces and supports dominate the market with a share of 45% in 2025, favored for their comfort, flexibility, and wide applicability in managing mild to moderate musculoskeletal conditions.

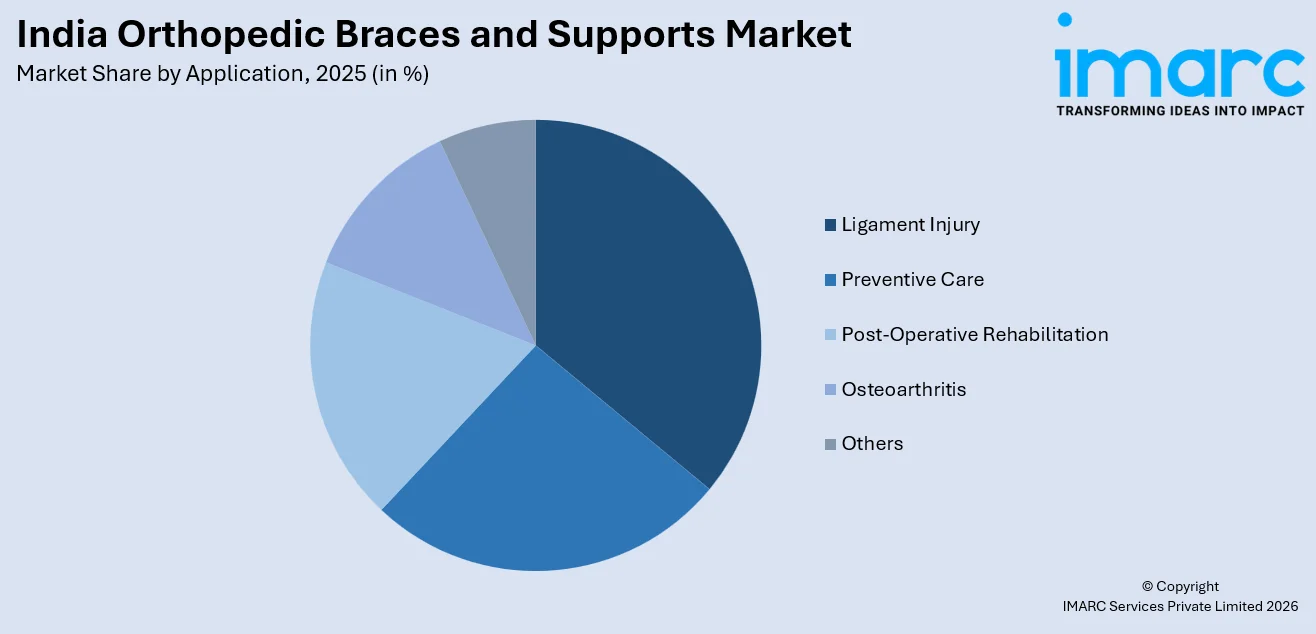

- By Application: Ligament injury holds the largest share of 33% in 2025, driven by India's rising sports participation, growing incidence of knee and ankle ligament tears, and increased physician-recommended bracing for rehabilitation.

- By End User: Hospitals and surgical centers dominate the market with a share of 45% in 2025, reflecting their central role in orthopedic care, post-operative support, and comprehensive patient management in India.

- Key Players: The India orthopedic braces and supports market is moderately competitive, with domestic and international manufacturers expanding portfolios, investing in product innovation, and strengthening distribution networks across healthcare channels.

To get more information on this market Request Sample

The India orthopedic braces and supports market is undergoing robust expansion as the country experiences a significant rise in musculoskeletal disorders, ligament injuries, and post-surgical rehabilitation needs. Rapid urbanization, shifting lifestyles, and increased participation in sports and physical activities have elevated the incidence of joint and bone-related conditions among the population. In December 2025, Bengaluru‑based startup Lumov, which designs and manufactures orthopedic recovery and rehabilitation products, raised USD 1.2 million (about ₹10 crore) in a seed funding round led by Incubate Fund Asia and several institutional investors to scale its orthoses and post‑surgical support offerings. Simultaneously, India's healthcare infrastructure has witnessed substantial development, including the expansion of specialized orthopedic hospitals and clinics in Tier 1 and Tier 2 cities. Growing health awareness among patients, combined with increasing physician adoption of evidence-based bracing protocols, is driving demand for both preventive and therapeutic orthopedic supports. Government healthcare initiatives promoting universal coverage are further widening patient access, while rising disposable incomes support spending on premium bracing solutions.

India Orthopedic Braces and Supports Market Trends:

Rising Adoption of Preventive Orthopedic Care

Rising adoption of preventive orthopedic care is reshaping market demand across India. Athletes, fitness enthusiasts, and working professionals are increasingly using braces proactively to protect joints and reduce injury risk before conditions worsen. In September 2025, global medical technology company Stryker announced a major expansion of its research and development operations in India with a new 140,000 sq ft facility in Bengaluru, strengthening its innovation footprint and accelerating development of advanced orthopedic and surgical technologies in the country. Expanding sports medicine awareness, growing digital health engagement, and physician-led patient education campaigns are catalyzing this preventive mindset, steadily boosting demand for lightweight, comfortable, and functionally versatile orthopedic support products nationwide.

Integration of Advanced and Smart Materials

Advanced material integration is transforming orthopedic brace design in India. Breathable, moisture-wicking fabrics and lightweight composites are progressively replacing conventional rigid materials, significantly enhancing wearer comfort and compliance during rehabilitation. In September 2025, global orthopedics brand ORTONYX® launched a new collection of 3D‑knitted orthopedic braces that combine breathable, medical‑grade materials with enhanced comfort and support across back, shoulder, wrist, and knee products, highlighting industry momentum toward innovative, patient‑centric materials. Emerging smart textiles embedded with sensors capable of monitoring joint alignment and tracking recovery progress are driving product innovation, opening new clinical applications and supporting sustained India orthopedic braces and supports market growth across therapeutic and preventive segments.

Expanding E-Commerce and OTC Distribution Channels

Digital commerce platforms are transforming how orthopedic braces and supports reach consumers across India. Online marketplaces and specialized healthcare e-commerce portals have significantly expanded access beyond traditional hospitals and pharmacies. Rising internet penetration, improved logistics networks, and reliable last-mile delivery are enabling faster and more convenient product availability nationwide. Additionally, detailed product descriptions, customer reviews, and comparison tools empower patients to make informed purchasing decisions independently. This digital shift is accelerating adoption and extending market penetration into semi-urban and rural areas that previously lacked consistent access to orthopedic support products and specialized medical retail infrastructure.

Market Outlook 2026-2034:

The India orthopedic braces & supports market is expected to register a positive growth trajectory over the forecast period. The increasing geriatric population with joint degeneration disorders, in addition to the high incidence of sports and occupational injuries, is expected to drive the market. The government's initiatives in the expansion of the healthcare sector, as well as increased investments by private hospitals, are expected to increase access to orthopedic care. Advances in orthopedic braces, such as smart braces, are expected to create new market opportunities, while e-commerce is expected to increase market penetration in semi-urban and rural areas. The market generated a revenue of USD 268.0 Million in 2025 and is projected to reach a revenue of USD 376.2 Million by 2034, growing at a compound annual growth rate of 3.8% from 2026-2034.

India Orthopedic Braces and Supports Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Product | Lower Extremity Braces and Supports | 40% |

| Type | Soft and Elastic Braces and Supports | 45% |

| Application | Ligament Injury | 33% |

| End User | Hospitals and Surgical Centers | 45% |

Product Insights:

- Lower Extremity Braces and Supports

- Spinal Braces and Supports

- Upper Extremity Braces and Supports

The lower extremity braces and supports dominates with a market share of 40% of the total India orthopedic braces and supports market in 2025.

Lower extremity braces and supports encompass a broad range of products designed to stabilize, protect, and rehabilitate the knee, ankle, and foot. These solutions address conditions including ligament tears, joint sprains, fractures, and degenerative disorders that are among the most commonly reported orthopedic complaints across India. Their widespread clinical prescription and growing consumer familiarity make them the most dominant product category in the market.

The rising number of sports participation, road accident cases, and physical strain at the workplace are creating a steady demand for lower extremity bracing solutions. These products are recommended by doctors as a conservative management approach, thus reducing the need for surgical solutions. The presence of lower extremity braces in hospitals, orthopedic clinics, pharmacies, and online stores also makes them easily accessible, thus ensuring the leading position of this segment in the entire orthopedic solution structure in India.

Type Insights:

- Soft and Elastic Braces and Supports

- Hinged Braces and Supports

- Hard and Rigid Braces and Supports

The soft and elastic braces and supports leads with a share of 45% of the total India orthopedic braces and supports market in 2025.

Soft and elastic braces and supports are designed to provide compression, warmth, and mild stabilization for a wide spectrum of musculoskeletal conditions. Their flexible, breathable construction enables comfortable extended wear, making them highly suitable for both active rehabilitation and daily injury management. In March 2025, BOSEGROW Medical unveiled a next‑generation line of smart orthopedic supports, including IoT‑enabled knee and ankle braces that sync with mobile apps for real‑time rehabilitation monitoring, highlighting innovation in comfort‑focused, flexible orthopedic solutions. Patient preference for non-restrictive orthopedic solutions, combined with ease of self-application, has established this type as the most widely adopted across clinical and over-the-counter settings in India.

The versatility of soft and elastic braces across multiple body regions, including the knee, ankle, wrist, and back, further amplifies their adoption. These products are accessible at varying price points, making them appropriate for a broad socioeconomic consumer base. Growing health awareness encouraging early intervention and preventive bracing use is additionally reinforcing demand, positioning soft and elastic braces as the preferred entry-level and therapeutic orthopedic support solution across India.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Ligament Injury

- Preventive Care

- Post-Operative Rehabilitation

- Osteoarthritis

- Others

The ligament injury dominates with a market share of 33% of the total India orthopedic braces and supports market in 2025.

Ligament injuries affecting the knee, ankle, and other joints are among the most prevalent orthopedic conditions encountered in India's clinical settings. High levels of sports participation, physically demanding occupational activities, and road traffic accidents contribute significantly to the frequency of anterior cruciate, medial collateral, and ankle ligament damage. Orthopedic braces designed for ligament injury management provide essential stabilization, pain relief, and controlled mobility restoration during recovery, making them indispensable within rehabilitation protocols.

Physician awareness of evidence-based bracing guidelines for ligament conditions has grown considerably, driving consistent prescription rates across hospitals, orthopedic clinics, and sports medicine centers. Patients increasingly prefer bracing as a conservative treatment pathway that avoids or delays surgical intervention. Rising public awareness of rehabilitation best practices, supported by expanding sports medicine services and physiotherapy integration, continues to strengthen demand within this application category throughout India's orthopedic care landscape.

End User Insights:

- Orthopedic Clinics

- Hospitals and Surgical Centers

- Over-the-Counter (OTC) Platforms

- Others

The hospitals and surgical centers leads with a share of 45% of the total India orthopedic braces and supports market in 2025.

Hospitals and surgical centers serve as primary institutional touchpoints for orthopedic diagnosis, treatment, and post-operative recovery across India. Their comprehensive clinical capabilities, including specialist orthopedic departments, advanced diagnostic facilities, and structured rehabilitation programs, position them as high-volume prescribers of orthopedic bracing solutions. Patients undergoing joint surgeries, fracture management, and complex musculoskeletal treatments routinely receive braces as part of standardized post-operative care protocols within these settings.

The expanding network of multi-specialty and dedicated orthopedic hospitals across metropolitan, Tier 1, and increasingly Tier 2 cities is broadening the institutional reach of this end-user segment. Government-backed hospital infrastructure development and rising private healthcare investments are enhancing patient capacity and specialist availability. As surgical volumes for joint replacements, ligament reconstructions, and spinal procedures continue to grow, hospitals and surgical centers will remain the most significant channel driving orthopedic braces and supports consumption across India.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India represents a leading regional contributor to the orthopedic braces and supports market, supported by high population density, a significant burden of musculoskeletal and sports-related conditions, and well-developed healthcare infrastructure across key states. The concentration of multi-specialty hospitals, orthopedic clinics, and expanding sports medicine facilities in major urban centers continues to drive consistent demand for orthopedic bracing products throughout the region.

West and Central India benefit from a robust and expanding urban healthcare ecosystem, with a strong concentration of private multi-specialty hospitals and orthopedic specialty centers actively driving product demand. Rising sports participation, growing health awareness among working-age populations, and increasing adoption of preventive orthopedic care are collectively strengthening the market presence of braces and supports across this economically significant and densely populated region.

South India is experiencing growing demand for orthopedic braces and supports, underpinned by high sports participation rates, an increasing aging population, and a well-established network of private hospitals and orthopedic specialty centers. States with advanced healthcare ecosystems and strong medical tourism infrastructure are driving clinical adoption of bracing solutions, while expanding health awareness among consumers is further reinforcing demand across both therapeutic and preventive orthopedic care segments.

East India represents an emerging and increasingly promising region within the orthopedic braces and supports market. Rising healthcare investments, growing government focus on improving medical infrastructure, and increasing patient awareness of orthopedic conditions are progressively expanding market access. Urban centers are witnessing steady growth in orthopedic clinic and hospital establishments, creating favorable conditions for broader adoption of bracing and support products across the region's diverse patient population.

Market Dynamics:

Growth Drivers:

Why is the India Orthopedic Braces and Supports Market Growing?

Rising Burden of Musculoskeletal Disorders and Sports Injuries

India is experiencing a growing prevalence of musculoskeletal disorders driven by a combination of demographic, lifestyle, and environmental factors. An expanding middle-aged and aging population is increasingly affected by joint degeneration, osteoarthritis, and chronic back pain, conditions that necessitate long-term orthopedic support. Recent data show that roughly one‑sixth of the Indian population suffers from musculoskeletal pain, with tens of millions affected by osteoarthritis and related conditions, underscoring the substantial healthcare burden these disorders pose. At the same time, a youthful population with high rates of participation in sports, fitness activities, and outdoor recreational pursuits is contributing to rising incidences of ligament tears, fractures, and joint sprains. Urbanization and sedentary occupational patterns are also exacerbating musculoskeletal vulnerabilities. Orthopedic braces and supports serve as critical tools in managing these conditions conservatively, reducing dependence on surgical intervention. Growing awareness of non-invasive treatment pathways is prompting clinicians and patients alike to favor bracing solutions, driving consistent market demand.

Expanding Healthcare Infrastructure and Government Initiatives

India's healthcare landscape has undergone substantial transformation, supported by both government-led initiatives and increased private sector investment in medical infrastructure. The expansion of specialized orthopedic hospitals and rehabilitation centers across metropolitan and Tier 1 cities has markedly improved patient access to orthopedic diagnosis and treatment. To strengthen the domestic medical device ecosystem, which includes essential products like orthopedic braces and supports, the Government of India launched a ₹500 crore MedTech scheme in 2024 to enhance manufacturing infrastructure, support clinical studies, and develop shared R&D facilities, aimed at reducing import dependence and boosting self‑reliance in medical technology. Government healthcare programs targeting universal health coverage, improved medical device regulation, and support for domestic manufacturing have collectively created a more enabling environment for orthopedic product adoption. Greater penetration of health insurance coverage is reducing financial barriers for patients requiring orthopedic bracing. Additionally, national health missions promoting primary healthcare access in semi-urban and rural areas are broadening the prospective consumer base.

Increasing Geriatric Population and Osteoarthritis Prevalence

India's demographic profile is shifting toward an older population, with a rising proportion of individuals experiencing age-related musculoskeletal conditions. Osteoarthritis, spondylitis, osteoporosis, and other degenerative bone and joint disorders are becoming increasingly prevalent, creating long-term demand for orthopedic bracing products that can provide pain relief, stabilization, and mobility support. In August 2025, prominent Indian orthopedic manufacturer Tynor Orthotics entered discussions to sell a majority stake valuing the company at ₹3,500–4,000 crore, reflecting strong investor confidence in the growing orthopedic care and support segment in India. Geriatric patients often require extended periods of orthopedic support and are more likely to rely on braces for both daily mobility assistance and post-rehabilitation management. Physicians are increasingly prescribing orthopedic braces as conservative management tools for age-related conditions, positioning them as cost-effective alternatives to surgery. This demographic trend is expected to remain a powerful and sustained driver of market demand throughout the forecast period.

Market Restraints:

What Challenges the India Orthopedic Braces and Supports Market is Facing?

Limited Awareness in Rural and Semi-Urban Regions

Despite urban growth, significant awareness gaps regarding orthopedic braces and their therapeutic benefits persist in rural and semi-urban India. Many patients in these regions remain uninformed about available products or rely on traditional remedies rather than modern orthopedic solutions. The absence of specialist healthcare providers in remote areas further limits access to appropriate diagnosis and brace prescriptions, slowing market penetration into these geographically dispersed populations.

Affordability and Price Sensitivity Among Consumers

A substantial segment of India's population remains highly price-sensitive, particularly in lower-income and rural demographics. Premium or advanced orthopedic braces with superior materials and smart features often carry costs that are beyond the financial reach of many patients. Limited health insurance coverage for medical devices further compounds affordability barriers. This price sensitivity constrains broader adoption of higher-value bracing products and restricts market growth potential across economically weaker segments.

Counterfeit and Low-Quality Product Proliferation

The orthopedic braces and supports market in India faces challenges from the widespread availability of substandard and counterfeit products distributed through informal and unorganized retail channels. These inferior products often fail to meet therapeutic standards, potentially causing harm or providing inadequate support to patients. The prevalence of such products erodes consumer confidence, undermines brand credibility, and creates pricing pressure for legitimate manufacturers committed to quality and safety standards.

Competitive Landscape:

The India orthopedic braces and supports market features a moderately competitive landscape comprising multinational medical device corporations, established domestic manufacturers, and an expanding base of regional and emerging players. Market participants are focused on differentiated product development strategies, including the introduction of braces with advanced materials, ergonomic designs, and smart monitoring capabilities. Distribution networks are being continuously strengthened to improve product availability across clinical, retail, and e-commerce channels, enabling broader market penetration. Research and development investments are increasingly directed toward patient-centric innovations such as customizable, lightweight, and breathable bracing systems suited to India's diverse climatic and lifestyle conditions. Strategic collaborations between healthcare institutions and device suppliers are enhancing product visibility and clinical adoption rates. The growing role of online marketplaces is intensifying competition among brands seeking to capture the direct-to-consumer segment, further driving product quality improvements and competitive pricing strategies across all market tiers.

Recent Developments:

- In January 2026, Leeford Healthcare announced a ₹200 crore investment to expand its orthopaedic & mobility aids division, launching a nationwide campaign, “Fit Raho, Hit Raho”, featuring Tiger Shroff. The company plans to introduce ~20 new products, including lumbar belts, knee supports, cervical collars, and posture correctors, by FY 2026‑27, growing its portfolio to ~50 and focusing on prevention, rehabilitation, and sports wellness.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Lower Extremity Braces and Supports, Spinal Braces and Supports, Upper Extremity Braces and Supports |

| Types Covered | Soft and Elastic Braces and Supports, Hinged Braces and Supports, Hard and Rigid Braces and Supports |

| Applications Covered | Ligament Injury, Preventive Care, Post-Operative Rehabilitation, Osteoarthritis, Others |

| End Users Covered | Orthopedic Clinics, Hospitals and Surgical Centers, Over-the-Counter (OTC) Platforms, Others |

| Regions Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Orthopedic Braces and Supports Market Report

The India orthopedic braces and supports market size was valued at USD 268.0 Million in 2025.

The India orthopedic braces and supports market is expected to grow at a compound annual growth rate of 3.8% from 2026-2034 to reach USD 376.2 Million by 2034.

Lower extremity braces and supports held the largest product share at 40%, owing to the high prevalence of knee and ankle injuries across India's sports-active and aging population, combined with widespread physician prescriptions for conservative bracing management.

Key factors driving the India orthopedic braces and supports market include rising musculoskeletal disorder prevalence, expanding geriatric population, growing sports injury incidence, improving healthcare infrastructure, government health initiatives, and increasing awareness of preventive orthopedic care.

Major challenges include limited product awareness in rural areas, price sensitivity among lower-income consumers, proliferation of counterfeit products, uneven healthcare infrastructure development, and constrained insurance reimbursement for orthopedic medical devices.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)