India Passenger Car Market Size, Share, Trends and Forecast by Vehicle Type, Fuel Type, Transmission Type, Price Segment, and Region, 2026-2034

India Passenger Car Market Size, Share, Trends & Forecast (2026-2034)

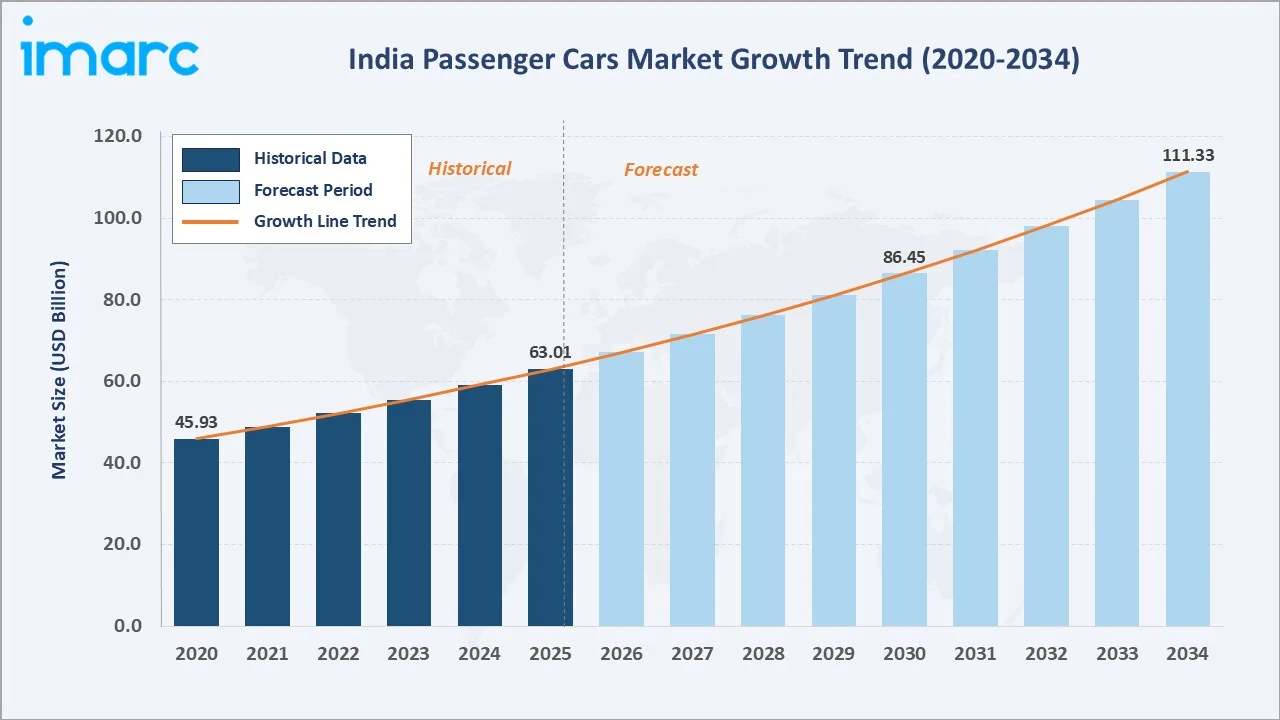

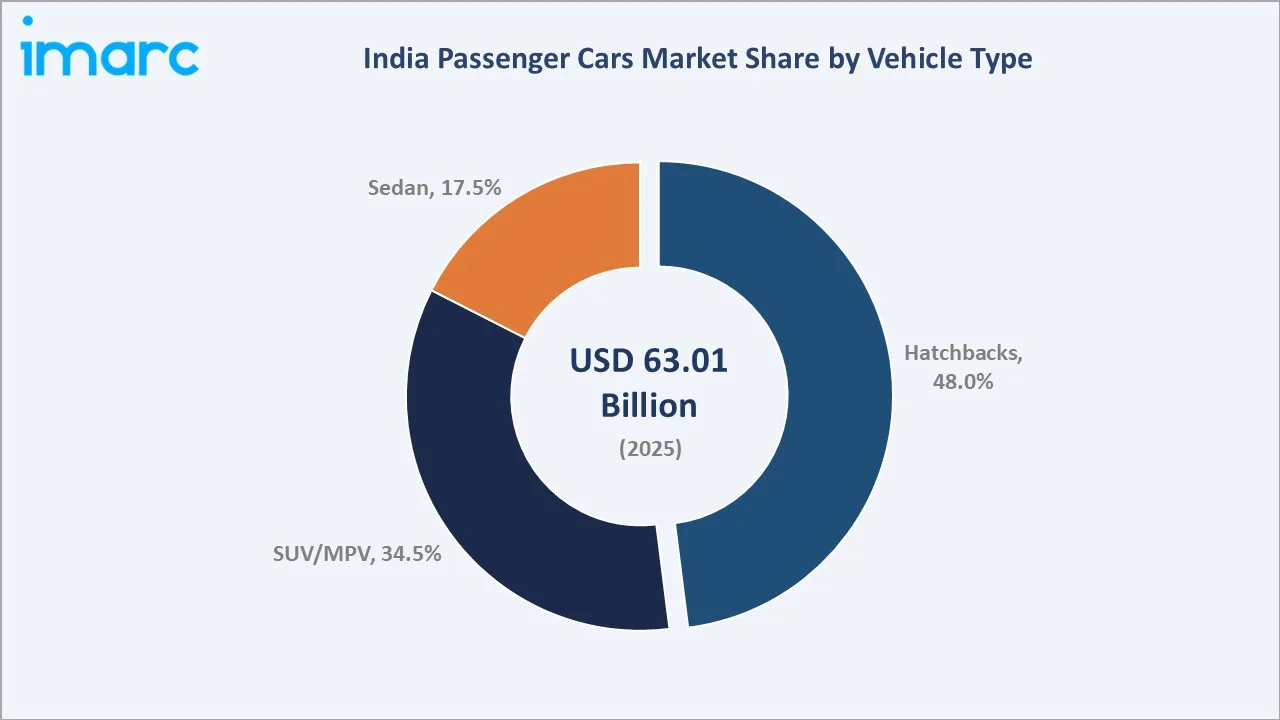

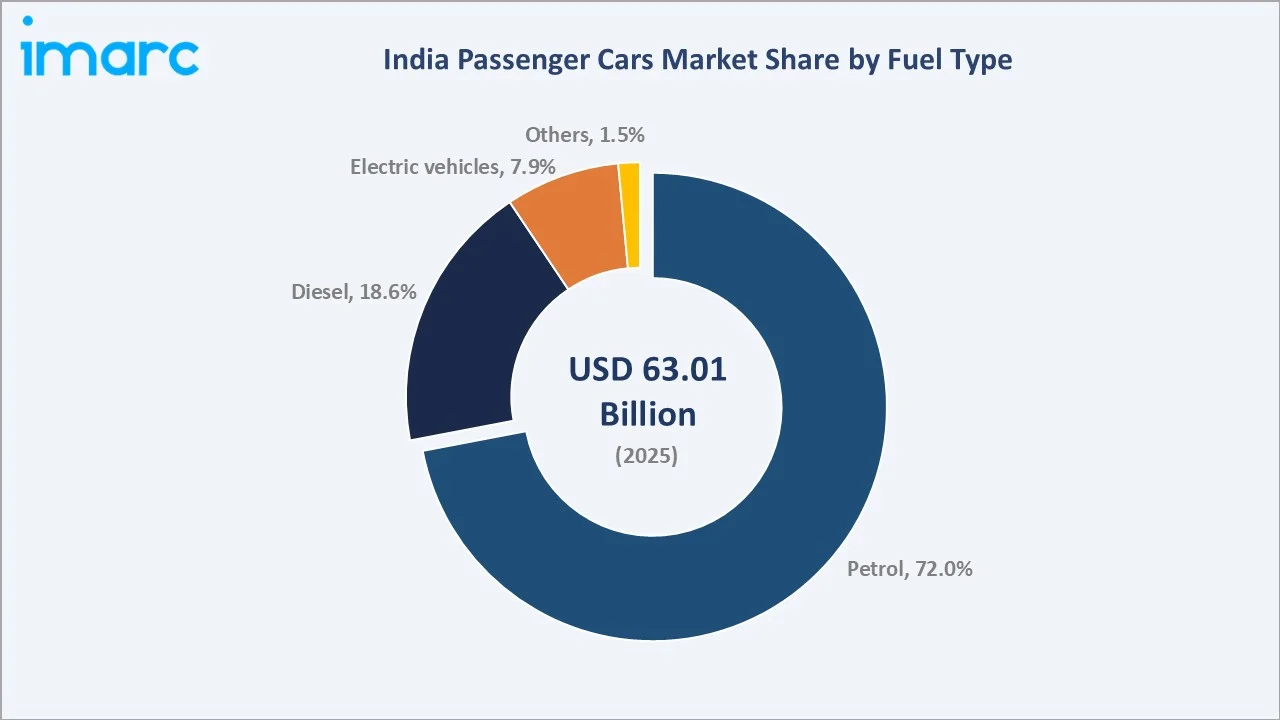

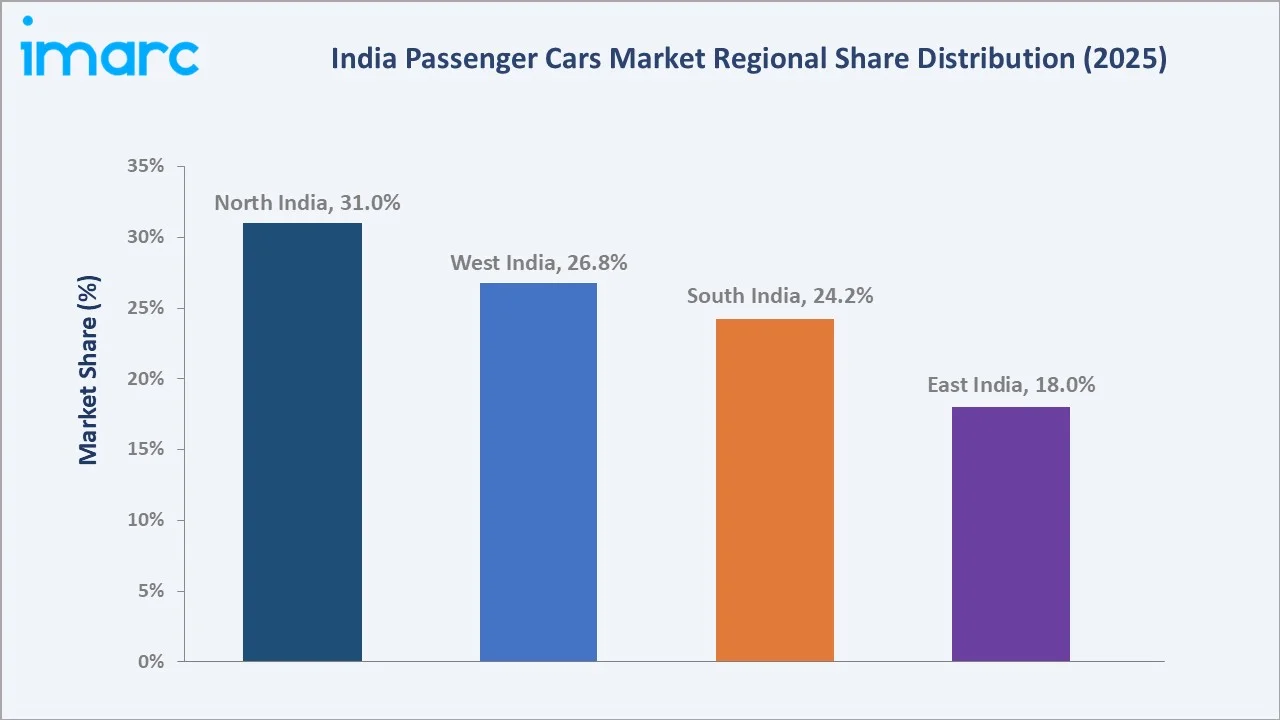

The India passenger car market size reached USD 63.01 Billion in 2025 and is projected to reach USD 111.33 Billion by 2034, exhibiting a CAGR of 6.53% during 2026-2034. The market is powered by rapid urbanization, rising disposable incomes among the expanding middle class, and government-backed schemes such as the Production-Linked Incentive (PLI) and PM E-DRIVE programs. Hatchbacks dominate vehicle-type sales at 48.0% share in 2025, while petrol engines command 72.0% of fuel-type preferences. North India leads regional demand at 31.0%, supported by Delhi-NCR's dense dealership ecosystem. Improving road infrastructure, competitive financing, and an increasingly young buyer demographic are reinforcing long-term demand for personal mobility across urban and semi-urban geographies.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 63.01 Billion |

|

Forecast Market Size (2034) |

USD 111.33 Billion |

|

CAGR (2026-2034) |

6.53% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Vehicle Type |

Hatchback (48.0%, 2025) |

|

Dominant Fuel Type |

Petrol (72.0%, 2025) |

|

Leading Region |

North India (31.0%, 2025) |

The India passenger car market expanded from USD 45.93 Billion in 2020 to USD 63.01 Billion in 2025, anchored at USD 86.45 Billion in 2030, and forecast to reach USD 111.33 Billion by 2034. This trajectory reflects India's structural shift from a cost-driven market to a feature-driven, aspirational automobile market. With over 4.5 million passenger vehicles sold annually as of 2025, a figure tracked by the Society of Indian Automobile Manufacturers (SIAM), India ranks as the third-largest automobile market globally.

To get more information on this market, Request Sample

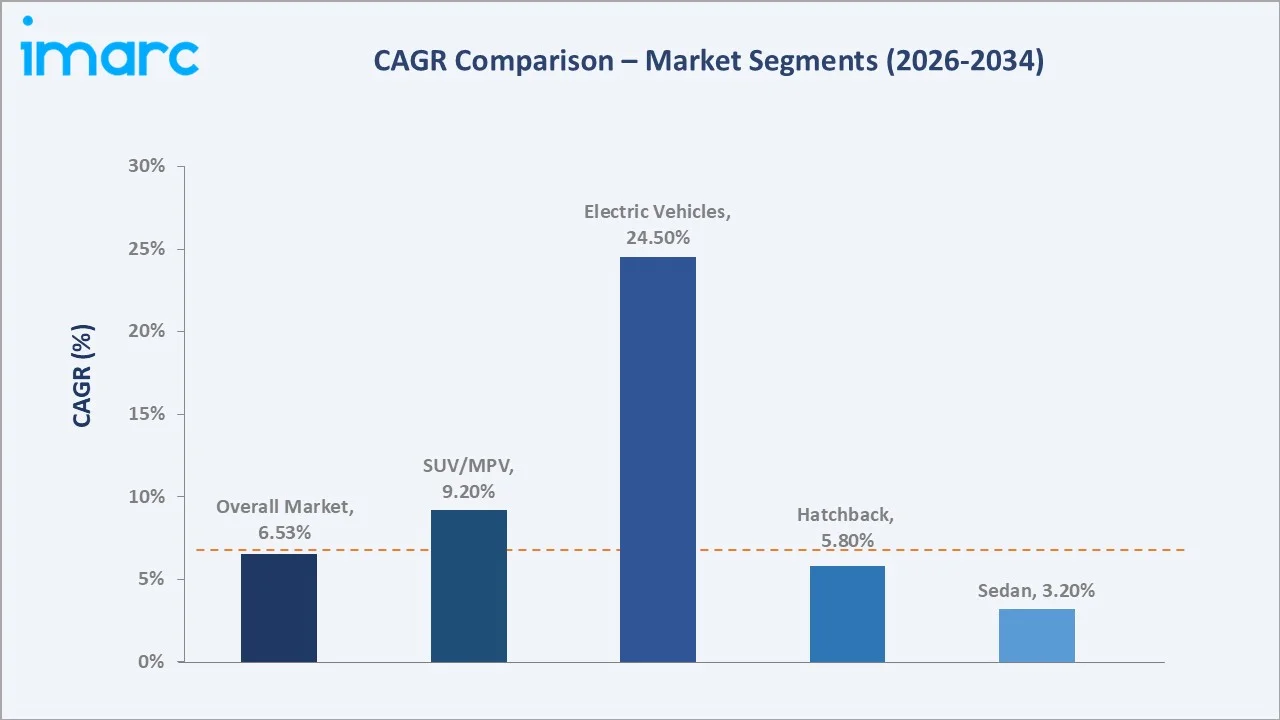

SUV and electric vehicle sub-segments are registering above-market growth rates. The EV segment, supported by PM E-DRIVE subsidies and expanding charging networks across Tier-1 cities, is projected to expand at a CAGR exceeding 24% through 2034. Meanwhile, compact SUVs, priced between INR 8-25 lakh, represent the most commercially contested arena, with every major OEM launching new models across this price band.

Executive Summary

The India passenger car market, valued at USD 63.01 Billion in 2025, is one of the fastest-expanding automobile markets among major global economies. Strong demographic tailwinds, including a median population age of approximately 28 years, rising per-capita income, and accelerating urbanization, are creating sustained first-time buyer demand. The market is projected to reach USD 111.33 Billion by 2034 at a 6.53% CAGR, driven by diverse growth vectors spanning hatchbacks, compact SUVs, and an emerging electric vehicle ecosystem.

Hatchbacks maintain their dominance at 48.0% in 2025, leveraging affordability and urban suitability. However, the SUV/MPV segment at 34.5% is the fastest-growing category, fueled by lifestyle aspirations and an expanding model portfolio across entry, mid, and premium price tiers. Petrol vehicles continue leading at 72.0% fuel type share, though diesel's share at 18.6% remains significant in commercial-use and long-distance travel applications. The electric vehicle segment at 7.9%, up from near-zero in 2020, signals a structural transition underway in India's powertrain preferences.

North India commands 31.0% of the national market, anchored by Delhi-NCR's consumption intensity and strong dealership density. West India (26.8%) benefits from Mumbai's financial market and Pune's manufacturing-proximity purchasing. South India (24.2%) reflects IT-sector wealth in Bengaluru, Hyderabad, and Chennai, while East India (18.0%) remains underpenetrated but growing above the national average, driven by Kolkata's retail development.

Key Market Insights

|

Insight |

Data |

|

Dominant Vehicle Type |

Hatchback- 48.0% share (2025) |

|

Dominant Fuel Type |

Petrol - 72.0% share (2025) |

|

Leading Region |

North India - 31.0% share (2025) |

|

Fastest Growing Segment |

Electric Vehicles (~24%+ CAGR, 2026-2034) |

|

Top Companies |

Suzuki Motor Corporation, Mahindra Group, Tata Group, and Hyundai Motor Company |

|

Market Opportunity |

EV expansion, compact SUV launches, Tier-2 city retail growth, and PM E-DRIVE incentives |

Key Analytical Observations Supporting the Above Data:

- Hatchback at 48.0% (2025): Hatchbacks dominate owing to compact footprints suited to congested urban environments. Affordable pricing between INR 4-10 lakh, high fuel efficiency, and wide after-sales service availability from OEMs reinforce this segment's leadership, particularly among first-time buyers.

- Petrol at 72.0% (2025): Petrol vehicles benefit from a well-distributed fuel infrastructure spanning over 100,000 petrol stations across India (as per Ministry of Petroleum). Lower initial vehicle costs and broad engine options across hatchback and sedan body styles support sustained dominance.

- North India at 31.0% (2025): Delhi-NCR's high vehicle penetration rate, backed by a dense network of over 1,200 authorized dealerships across the region, and strong income levels in states like Haryana and Punjab, support regional leadership.

- EV Growth: Battery electric vehicle production in India is expected to nearly triple from approximately 130,000 units in 2024 to 377,000 units in 2025, per industry estimates, positioning EVs as the single fastest-growing passenger car sub-segment through 2034.

- Market Expansion into Tier-2 Cities: Cities including Jaipur, Lucknow, Surat, and Coimbatore are recording above-national-average automobile sales growth as dealership networks expand and financing penetration improves.

India Passenger Car Market Overview

The India passenger car market encompasses the design, manufacturing, assembly, distribution, and sale of private and family-use automobiles with seating for up to eight passengers. The ecosystem spans domestic OEM assembly plants, authorized multi-brand dealerships, organized fleet operators, government-facilitated vehicle financing channels, and an expanding digital sales and servicing infrastructure. India's automobile sector contributes approximately 7% of GDP and employs over 30 million people directly and indirectly, per data from the Society of Indian Automobile Manufacturers (SIAM).

Macroeconomic influences include India's GDP growth rate projected above 7% annually through 2030, the government's Bharatmala highway expansion program improving inter-city road connectivity, and rising per-capita income that crossed USD 2,700 in 2025, all reinforcing the structural case for expanding passenger car ownership across income tiers.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Rising Disposable Income and Urban Middle-Class Expansion: Rising per-capita income and expanding urban middle-class demographics are driving first-time and upgrade car purchases. India's consumer spending is projected to grow to USD 6 trillion by 2030, as noted by multiple government economic surveys. This income growth is motivating buyers to transition from two-wheelers to entry-level hatchbacks and from budget hatchbacks to compact SUVs, creating a natural volume funnel across vehicle segments.

- Government Incentive Schemes-PLI and PM E-DRIVE Programs: The Production-Linked Incentive (PLI) scheme for automobile and auto components, with an approved outlay of INR 25,938 crore (approximately USD 3.2 billion), is accelerating domestic manufacturing capacity. PM E-DRIVE subsidies are reducing EV acquisition costs for consumers, while the Vehicle Scrappage Policy is stimulating replacement demand. The government's target of EV penetration in new car sales provides a regulatory directional push that is motivating OEM investment in electrification.

- Expanding Road Infrastructure and Connectivity: India's National Highways network expanded to approximately 1,46,145 km in 2025, per the Ministry of Road Transport and Highways. The Bharatmala Pariyojana project targeting 34,800 km of new highways is improving inter-city travel, making car ownership more practical in Tier-2 and Tier-3 cities. This infrastructure development directly expands the car market's addressable geography, supporting long-term volume growth.

- Growing Preference for SUVs and Feature-Rich Models: Consumer preference has structurally shifted toward compact SUVs offering higher ground clearance, commanding driving positions, and premium interior features. SUV/MPV sales in India's passenger vehicle market exceeded 60% of total volumes in FY2025. Manufacturers are responding with cascading model launches across price bands, sustaining premium segment momentum.

Market Restraints

- High Import Duties on CBU Vehicles: India imposes a 100% customs duty on Completely Built Unit (CBU) imported passenger vehicles priced above USD 40,000, and 60-70% on vehicles below this threshold. This significantly restricts the premium and luxury car segments' addressable market, limiting consumer access to international brands and restricting competitive pricing options for aspiring buyers.

- Underdeveloped EV Charging Infrastructure in Non-Metro Areas: While EV charging infrastructure is expanding rapidly in metro cities, Tier-2 and Tier-3 markets remain underserved. As of early 2026, India had approximately 29,000 public EV charging stations, disproportionately concentrated in Delhi, Mumbai, Bengaluru, and Chennai. This infrastructure gap restrains EV adoption in geographies that represent over 40% of new car sales, limiting the overall market's green transition velocity.

Market Opportunities

- Electric Vehicle Ecosystem Buildout: India's EV passenger car segment, with a ~7.9% market share in 2025, presents one of the largest growth runways in the Asia-Pacific region. With battery costs expected to fall below USD 100/kWh by 2027, price parity with ICE vehicles in the compact car segment is approaching. OEMs investing now in local battery supply chains, charging partnerships, and software-defined vehicle platforms will capture first-mover advantages in this rapidly expanding sub-market.

- Tier-2 and Tier-3 City Market Penetration: Approximately 65% of India's incremental passenger car demand through 2030 is projected to originate from cities outside the top 30 urban centers, per industry estimates. Declining financing rates, rising household incomes, and improving road infrastructure are making car ownership accessible in cities such as Nashik, Bhopal, Vizag, and Patna, offering significant whitespace for OEMs and dealerships.

Market Challenges

- Rising Input Costs and Semiconductor Supply Dependencies: Steel and aluminum price volatility, combined with the global semiconductor supply chain's structural vulnerability exposed during 2021-2023, continue posing margin and production planning challenges for OEMs. Semiconductor content per vehicle is rising as connected car features proliferate, increasing both cost exposure and supply-chain complexity for manufacturers operating in India's price-sensitive market.

- Consumer Price Sensitivity in a Competitive Multi-Brand Environment: India's passenger car buyer remains highly price-sensitive despite premiumization trends. Over 54% of passenger car sales fall within the economy segment priced below INR 10 lakh. Intense competition among 15+ active OEMs drives frequent discounting, pressuring profit margins and complicating value-chain economics for dealerships and component suppliers alike.

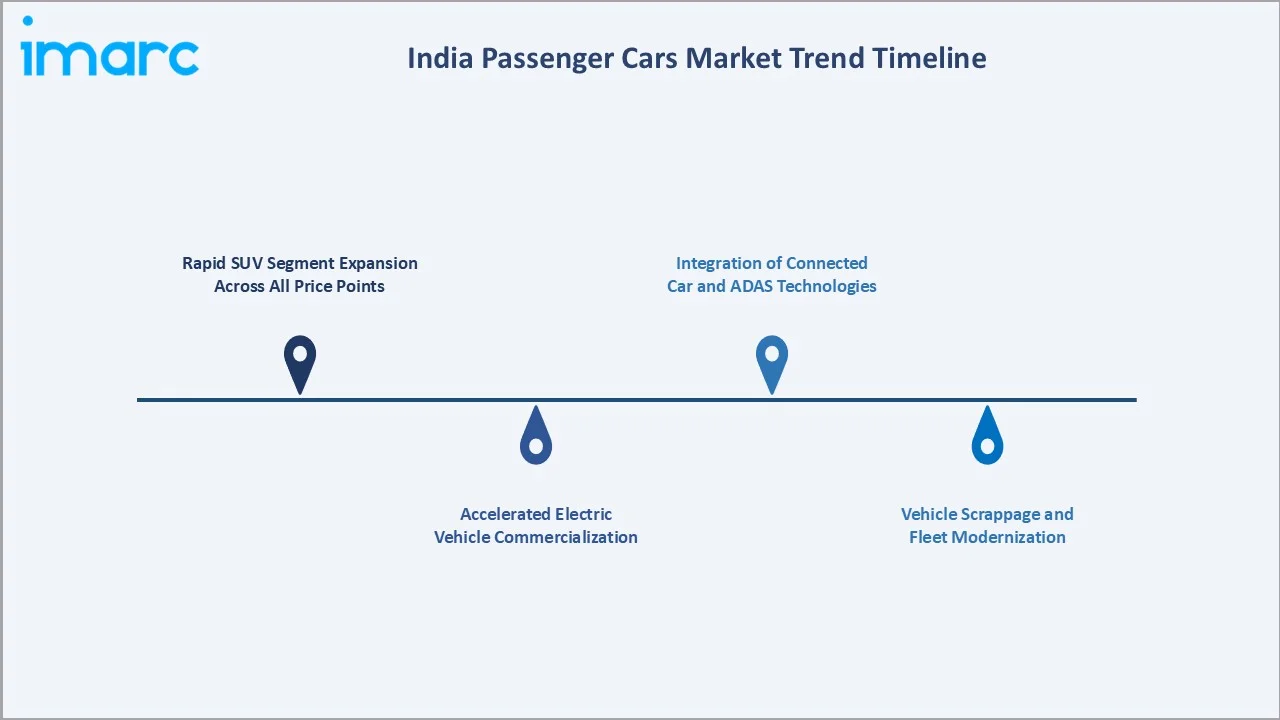

Emerging Market Trends

1. Rapid SUV Segment Expansion Across All Price Points

SUVs have evolved from a premium-only category to India's mainstream vehicle choice. Entry-level compact SUVs priced at INR 6-12 lakh are now produced by Maruti Suzuki (Brezza), Tata Motors (Punch), Mahindra (Bolero Neo), and Hyundai (Venue), ensuring that aspirational SUV ownership is accessible to a broad income base. This democratization of the SUV form factor is a defining commercial trend through 2034.

2. Accelerated Electric Vehicle Commercialization

In January 2025, Maruti Suzuki unveiled the e VITARA at the Bharat Mobility Global Expo, claiming over 500 km of range and ADAS Level 2 capabilities, marking a pivotal entry by India's largest OEM into the EV segment. Simultaneously, Mahindra's BE 6e and XEV 9e launches in November 2024 established new performance and design benchmarks. With every top OEM now committed to EV product roadmaps, EV adoption is transitioning from early-adopter phase to mainstream commercialization.

3. Integration of Connected Car and ADAS Technologies

Advanced Driver Assistance Systems (ADAS) and connected car platforms are migrating from luxury segments into mid-range vehicles priced below INR 15 lakh. Features such as automatic emergency braking, lane keep assist, and real-time navigation are becoming standard specifications. In October 2024, Qualcomm Technologies and Google announced a multi-year collaboration integrating Gen AI-enabled in-car experiences using the Snapdragon platform, directly targeting India's rapidly scaling connected car segment.

4. Vehicle Scrappage and Fleet Modernization

India's Vehicle Scrappage Policy, offering scrapping certificates providing up to 25% rebates on new vehicle purchases, is generating incremental replacement demand estimated at 4-5 million vehicles annually over the medium term. Commercial fleet operators are the immediate beneficiaries, but the policy is progressively stimulating private car replacement cycles, adding volume to both entry and mid segments.

5. Premiumization and Feature Inflation in Mid-Segment

Mid-segment buyers in India are increasingly selecting vehicles at or above the INR 10-20 lakh price band, demanding features previously reserved for premium cars. Panoramic sunroofs, ventilated seats, 360-degree cameras, and wireless charging have become competitive battleground specifications even in models priced around INR 12 lakh. This premiumization trend is expanding revenue per unit for OEMs while sustaining volume momentum.

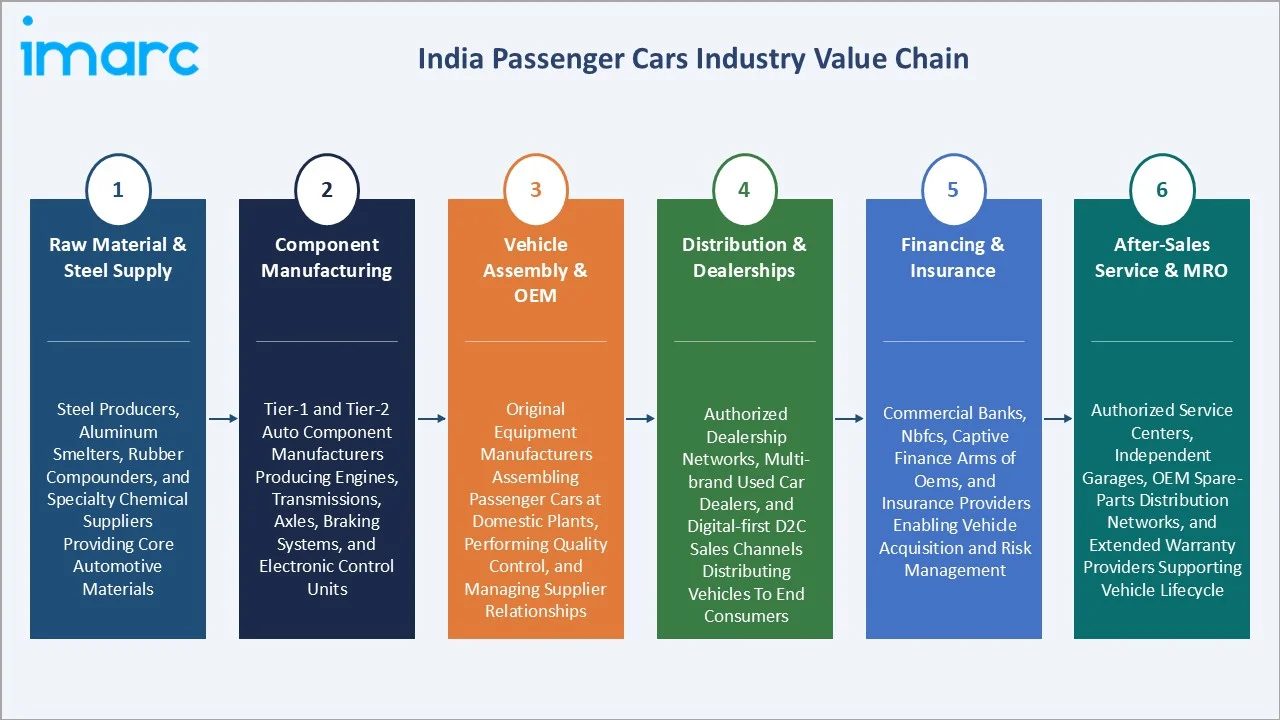

Industry Value Chain Analysis

India's passenger car value chain integrates global and domestic participants across raw material supply, precision component manufacturing, OEM assembly, authorized retail, and organized after-sales service infrastructure. The value chain's commercial structure creates a multi-tier competitive environment where domestic manufacturing cost advantages coexist with imported technology content, particularly in electronics, advanced safety systems, and battery packs for EVs.

|

Stage |

Key Participants |

|

Raw Material & Steel Supply |

Steel producers, aluminum smelters, rubber compounders, and specialty chemical suppliers providing core automotive materials |

|

Component Manufacturing |

Tier-1 and Tier-2 auto component manufacturers producing engines, transmissions, axles, braking systems, and electronic control units |

|

Vehicle Assembly & OEM |

Original Equipment Manufacturers assembling passenger cars at domestic plants, performing quality control, and managing supplier relationships |

|

Distribution & Dealerships |

Authorized dealership networks, multi-brand used car dealers, and digital-first D2C sales channels distributing vehicles to end consumers |

|

Financing & Insurance |

Commercial banks, NBFCs, captive finance arms of OEMs, and insurance providers enabling vehicle acquisition and risk management |

|

After-Sales Service & MRO |

Authorized service centers, independent garages, OEM spare-parts distribution networks, and extended warranty providers supporting vehicle lifecycle |

The distribution and dealership stage is the most commercially critical interface, where over 25,000 authorized dealer touchpoints across India determine purchase experience and brand loyalty. OEM investments in digital sales platforms and virtual showrooms are supplementing but not yet replacing the physical dealership's role in India's consultative, high-touch vehicle purchase process.

Technology Landscape in the India Passenger Car Industry

Internal Combustion Engine Evolution

Advanced ICE technology remains the backbone of India's passenger car market, with BS6 Phase 2 emission norms, effective April 2023, mandating On-Board Diagnostics and real-driving emission controls. Turbocharged petrol engines in the 1.0-1.2 litre displacement range, combined with mild-hybrid systems, are delivering 18-22 kmpl fuel efficiency in the mass-market hatchback segment, maintaining ICE vehicles' economic competitiveness against EVs.

Electric Drivetrain and Battery Technology

Battery electric vehicles in India primarily use lithium iron phosphate (LFP) and lithium nickel manganese cobalt (NMC) battery chemistries. Battery costs for Indian-market EVs have declined from approximately USD 185/kWh in 2022 to below USD 130/kWh in 2025. Tata Motors' Acti.ev platform and Mahindra's INGLO electric-origin architecture represent domestically developed EV platforms optimized for India's road conditions and consumer requirements.

Connected Car and Infotainment Technology

Connected car penetration in India's new passenger car sales exceeded 35% in 2025, driven by OEM-integrated telematics platforms. Features including embedded SIM connectivity, over-the-air software updates, remote vehicle monitoring, and AI-powered voice assistants are increasingly standard even in vehicles priced below INR 15 lakh. Qualcomm's Snapdragon Automotive platforms and Google Automotive Services are the primary technology ecosystems powering India's connected car stack.

Advanced Driver Assistance Systems (ADAS)

ADAS penetration, including Level 1 and Level 2 features, has expanded rapidly as global safety regulations influence Indian OEM standard specifications. Automated emergency braking, adaptive cruise control, lane centering, and blind-spot monitoring are now offered in vehicles across the INR 10-25 lakh mid-segment range. Bharat New Car Assessment Programme (Bharat NCAP) upgrades are accelerating safety technology adoption by making it a commercial necessity for OEMs competing on safety ratings.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

Hatchback |

48.0% |

2025 |

|

Fuel Type |

Petrol |

72.0% |

2025 |

|

Transmission Type |

Manual |

78.0% |

2025 |

|

Price Segment |

Economy |

54.0% |

2025 |

|

Region |

North India |

31.0% |

2025 |

By Vehicle Type

Hatchbacks lead the India passenger car market at 48.0% in 2025. The segment commands India's most commercially mature and volume-intensive car market category, serving urban commuters, first-time car buyers, and cost-conscious families. Compact sizing ideally suited for navigating India's dense city traffic and limited parking spaces, combined with a price range starting below INR 4 lakh, makes hatchbacks the default entry point for India's expanding motorization.

To access detailed market analysis, Request Sample

SUV/MPV at 34.5% is growing faster than any other body style, driven by consumer aspirations for commanding road presence, higher ground clearance suitable for India's diverse road surfaces, and a broader feature set at equivalent or slightly higher price points versus comparable sedans. Sedan at 17.5% has structurally declined as urban consumers prioritize either the affordability of hatchbacks or the lifestyle positioning of SUVs, leaving sedans occupying a premium-niche positioning in the corporate and executive segments.

By Fuel Type

Petrol leads fuel-type preferences at 72.0% in 2025, supported by India's expansive fuel distribution network exceeding 100,000 retail outlets as per the Ministry of Petroleum and Natural Gas. Petrol-engine vehicles offer lower upfront acquisition costs compared to diesel equivalents and benefit from a broader range of turbocharged engine options across the hatchback and entry SUV segments.

Diesel at 18.6% remains relevant in the mid-to-large SUV and commercial-use vehicle segments, where torque output, fuel efficiency on highways, and total-cost-of-ownership advantages over longer distances support demand. Electric vehicles at 7.9% represent the market's fastest-growing fuel-type segment, with penetration expected to exceed 15% by 2028 as PM E-DRIVE incentives and falling battery prices improve purchase economics. Others (CNG, LPG, hybrids) at 1.5% collectively contribute incremental volume, with CNG gaining particular traction in cities with natural gas distribution infrastructure.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

North India |

31.0% |

Driven by Delhi-NCR's high income density, strong dealership network, and Punjab's above-national-average lifestyle consumption. |

|

West India |

26.8% |

Supported by Mumbai's financial sector wealth, Pune's IT and manufacturing industry growth, and expanding e-commerce penetration. |

|

South India |

24.2% |

Reflects Bengaluru and Hyderabad's tech-sector affluence, strong preference for feature-rich and electric vehicles, and growing corporate demand. |

|

East India |

18.0% |

Rising disposable incomes in Kolkata and Bhubaneswar; growing brand awareness and dealer penetration are driving above-average growth from a lower base. |

North India's 31.0% market leadership reflects the commercial density of the Delhi-NCR automotive corridor, which houses over 1,200 authorized passenger car dealerships and benefits from India's highest concentration of corporate fleet operators. Rajasthan and Uttar Pradesh contribute significant volume from semi-urban districts where road infrastructure improvements are expanding the car's practical utility.

West India's 26.8% share is anchored by the Mumbai Metropolitan Region, India's highest per-capita consumer spending geography, and Pune's expanding IT and manufacturing workforce. Gujarat's industrial economy supports commercial SUV and MUV demand alongside personal car purchases. South India's 24.2% reflects the disproportionately high SUV and EV adoption rates in Bengaluru (Karnataka), driven by the IT sector's affluent consumer base. East India's 18.0%, while the lowest regional share, is projected to grow above the national CAGR through 2030, led by West Bengal's expanding organized retail automobile sector.

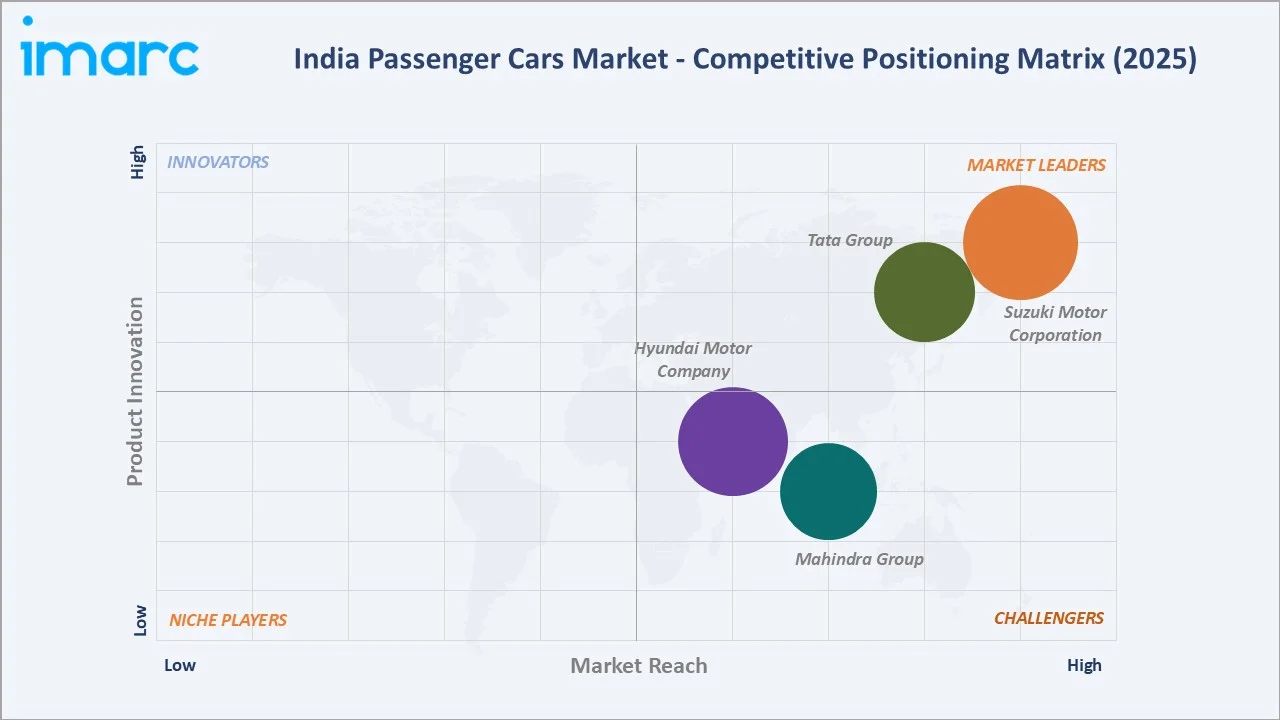

Competitive Landscape

The India passenger car competitive landscape is among the most contested globally, with 15+ active OEMs competing across body styles, fuel types, and price segments. Maruti Suzuki India retains undisputed market leadership at approximately 38.93% market share in FY2025-26, though its share has declined from 51.3% in FY2020 as Mahindra, Tata Motors, and Hyundai have grown their volumes significantly. The SUV segment's rise has disproportionately benefited domestic champions Mahindra and Tata Motors, reshaping the competitive hierarchy.

|

Company |

Key Brands / Models |

Market Position |

Core Strength |

|

Suzuki Motor Corporation |

Swift, Dzire, Baleno, Brezza, Fronx, Ertiga, Wagon R |

Market Leader |

Operates Maruti Suzuki India Limited; Distribution depth: 3,500+ dealer outlets |

|

Mahindra Group |

Scorpio-N, XUV700, Thar, BE 6e, XEV 9e, Bolero |

Strong Challenger |

Operates Mahindra & Mahindra Limited; SUV dominance and EV platform leadership |

|

Tata Group |

Nexon, Punch, Harrier, Safari, Tiago, Altroz, Curvv |

Market Leader |

Operates Tata Motors; EV portfolio scale and safety ratings |

|

Hyundai Motor Company |

Creta, i20, Venue, Verna, Alcazar, Exter |

Challenger |

Operates Hyundai Motor India Limited; Premium-feature mid-segment leadership |

Key Company Profiles

Suzuki Motor Corporation

Suzuki Motor Corporation, operates Maruti Suzuki India Limited which is India's largest passenger car manufacturer, holding approximately 39% market share in FY2025-26 with domestic sales of 18.61 lakh units, per company investor disclosures.

- Key Models: Swift, Dzire, Baleno, Brezza, Fronx, Ertiga, Wagon R, and others.

- Recent Developments: In January 2025, Maruti Suzuki unveiled its first battery electric vehicle, the e VITARA, at the Bharat Mobility Global Expo. The vehicle offers over 500 km claimed range, ADAS Level 2 features, and an OTA-updatable infotainment system.

- Strategic Focus: Maintaining volume leadership through a broad product portfolio spanning sub-INR 5 lakh to INR 25 lakh price range, while accelerating EV and strong-hybrid product integration into the portfolio to address regulatory and consumer preference shifts.

Mahindra Group

Mahindra Group operates in the automobile sector via Mahindra & Mahindra Ltd. The company has transformed from India's utility vehicle specialist to a full-spectrum SUV and EV challenger, achieving 13.25% passenger car market share in 2025 with approx. 6 lakh units sold.

- Key Models: Scorpio-N, XUV700, Thar, BE 6e, XEV 9e, Bolero, and others.

- Recent Developments: In November 2024, Mahindra launched the BE 6e and XEV 9e at a global premiere event in Chennai, introducing advanced electric origin architecture with 59 kWh and 79 kWh battery options and sophisticated ADAS Level 2+ capabilities.

- Strategic Focus: Capitalizing on India's SUV boom and positioning as the premium domestic EV brand, while expanding its XUV and Thar sub-brands as lifestyle-driven, aspirational vehicle families.

Tata Group

Tata Motors, a subsidiary of Tata Group, holds 12.68% passenger car market share in 2025, with 5.68 lakh units sold domestically. The company is India's dominant EV manufacturer, with its Nexon EV and Tiago EV collectively accounting for over 60% of India's electric passenger car sales volume.

- Key Models: Nexon, Punch, Harrier, Safari, Tiago, Altroz, Curvv, and others.

- Recent Developments: In November 2025, Tata Motors relaunched Tata Sierra with different variants- Smart, Pure, Adventure, and Accomplished, among others.

- Strategic Focus: Scaling its EV portfolio across segments, strengthening safety credentials as a brand differentiator, and leveraging synergies with Jaguar Land Rover for technology transfer.

Market Concentration Analysis

India's passenger car market exhibits a moderately concentrated competitive structure, with the top OEMs- Suzuki Motor Corporation, Mahindra Group, Tata Group, and Hyundai Motor Company, collectively accounting for approximately 80% of total FY2025-26 passenger vehicle sales. This concentration has declined from over 90% in FY2020 as new entrants (Kia, MG Motor, Skoda, VW) have established meaningful market positions in the mid-premium and compact SUV segments.

The hatchback and economy car segment remains the most concentrated, with Maruti Suzuki commanding over 60% of volumes in the sub-INR 8 lakh price band. The compact SUV segment is the most fragmented, with eight to ten active OEMs competing for share. The premium segment above INR 40 lakh is dominated by Kia (EV6, Carnival), Jeep, BMW, Mercedes-Benz, and Audi, with no single player holding above 25% of this sub-segment.

Market concentration is evolving through two forces: Maruti Suzuki's distribution scale and breadth continuing to maintain its leadership, while SUV segment fragmentation is increasing as international OEMs localize more models and domestic players expand their SUV ranges.

Investment & Growth Opportunities

Highest Growth Segments

Electric vehicles (~24%+ CAGR through 2034), compact SUVs (~9.2% CAGR), connected car technology platforms, and Tier-2 city retail network expansion (~8-10% CAGR) represent India's highest-growth investment vectors. The EV charging infrastructure buildout – estimated to require over USD 3 billion in investment to achieve India's 2030 EV penetration targets – presents adjacent investment opportunities in energy, real estate, and technology.

Emerging Investment Opportunities

Battery pack assembly and lithium-ion cell manufacturing represent the most strategically significant greenfield investment opportunity, with the government's PLI scheme for Advanced Chemistry Cell battery storage offering incentives of INR 18,100 crore (~USD 2.2 billion). Domestic battery manufacturing capacity development would reduce India's current 80%+ dependency on imported battery cells, primarily from China.

Investment Themes

- EV Charging Infrastructure: PM E-DRIVE-supported public charging station deployment requires significant capital, with government estimates suggesting 45,000+ charging stations needed in Tier-1 and Tier-2 cities by 2027 to support projected EV volumes.

- Auto Component Localization: The PLI scheme for auto components with INR 25,938 crore outlay is incentivizing domestic production of EVS drivetrains, sensors, and electronics, creating component-level investment opportunities alongside OEM-level plays.

- Digital Retail and Aftersales Platforms: OEM-branded and multi-brand digital car-buying platforms are an emerging investment theme as India's auto retail shifts toward online lead generation and remote diagnostics.

Future Market Outlook (2026-2034)

The India passenger car market is projected to grow from USD 63.01 Billion in 2025 to USD 111.33 Billion by 2034, delivering a 6.53% CAGR. The market's anchor value of USD 86.45 Billion in 2030 represents India's automobile industry at a structural inflection, transitioning from a primarily ICE-dominated volume market to a powertrain-diversified, feature-intensive, and software-defined vehicle market.

Three structural forces define India's passenger car market growth through 2034: (1) India's demographic dividend-approximately 12 million new first-time car buyers entering the addressable market annually as urban income crosses the household car-ownership threshold; (2) EV transition acceleration driven by falling battery costs, expanding charging infrastructure, and regulatory pressure from increasingly stringent CAFE (Corporate Average Fuel Economy) norms; and (3) premiumization-consumers trading up within and across vehicle segments at above-income-growth rates as lifestyle aspirations and social mobility expand.

Compact SUVs will account for over 40% of total new car sales by 2030, up from 34.5% in 2025, making it the defining segment of India's automotive growth story. Electric vehicles will reach 15-18% new car sales penetration by 2030, representing over 46.43 lakh EV units annually, creating one of Asia's largest EV markets by volume. Geographic expansion into Tier-2 and Tier-3 cities will contribute over 50% of incremental volume growth through 2034, reshaping the competitive dynamics of dealership networks and aftersales ecosystems.

Research Methodology

Primary Research

Primary research comprised structured interviews with India passenger car industry stakeholders including Senior Executives at OEM Headquarters, Dealership Principals, Fleet Purchase Managers, NBFC and Auto Finance Officers, EV Technology Engineers, and survey data from passenger car buyers across North, West, South, and East India. Respondents covered urban, semi-urban, and rural buyer profiles across income segments, encompassing first-time buyers, upgrade buyers, and fleet operators.

Secondary Research

Secondary research encompassed India passenger vehicle sales data from the Society of Indian Automobile Manufacturers (SIAM), Ministry of Road Transport and Highways annual reports, Ministry of Heavy Industries PLI scheme documentation, PM E-DRIVE implementation progress reports from the Ministry of Heavy Industries, company annual reports and investor presentations from listed OEMs, and automotive trade publications. Over 60 secondary sources were reviewed and validated.

Forecasting Models

Market revenue forecasts were developed using a bottom-up consumer income and vehicle ownership rate model: India's urban and rural household income distribution multiplied by segment-specific vehicle ownership penetration rates and average selling prices per segment, aggregated to generate total market revenue by vehicle type, fuel type, and region. CAGR convergence validation was performed against SIAM historical sales data and OEM production guidance.

India Passenger Car Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historic Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Vehicle Types Covered |

Hatchback, Sedan, SUV/MPV |

|

Fuel Types Covered |

Petrol, Diesel, Electric, Others |

|

Transmission Types Covered |

Automatic, Manual |

|

Price Segments Covered |

Economy, Mid-Range, Premium and Luxury |

|

Regions Covered |

North India, South India, East India, West India |

|

Companies Covered |

Suzuki Motor Corporation, Mahindra Group, Tata Group, Hyundai Motor Company, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Passenger Car Market Report

The India passenger car market reached USD 63.01 Billion in 2025, driven by rising incomes, urbanization, and government incentives supporting first-time buyers and EV adoption.

The India passenger car market is projected to grow at a CAGR of 6.53% during 2026-2034, reaching USD 111.33 Billion by 2034, supported by demographic growth and EV transition.

Hatchbacks lead with 48.0% market share in 2025, owing to affordability, urban suitability, and strong brand loyalty among first-time buyers in the INR 4-10 lakh price range.

Petrol leads at 72.0% in 2025, supported by extensive fuel infrastructure, lower vehicle costs, and broad consumer familiarity with petrol engines across hatchback and sedan segments.

North India leads with 31.0% market share in 2025, driven by Delhi-NCR's income density, strong dealership concentration, and Punjab's above-average lifestyle consumption.

Leading companies include Suzuki Motor Corporation, Mahindra Group, Tata Group, and Hyundai Motor Company, collectively commanding around 80% of market volume.

The India passenger car market is projected to reach USD 86.45 Billion by 2030, with compact SUVs, electric vehicles, and Tier-2 city expansion as primary growth contributors.

The India passenger car market stood at USD 45.93 Billion in 2020, before recovering and accelerating post-COVID to reach USD 63.01 Billion by 2025, reflecting strong structural demand.

PM E-DRIVE subsidies, PLI scheme for batteries, falling cell costs, expanding charging infrastructure, and new EV launches by Maruti Suzuki, Mahindra, and Tata Motors are driving EV growth.

SUV/MPV holds 34.5% market share in 2025 and is India's fastest-growing body style segment, growing at approximately 9.2% CAGR as consumer aspirations shift toward lifestyle-oriented vehicles.

Top opportunities include EV battery manufacturing, charging infrastructure buildout, Tier-2 city dealership network expansion, auto component localization under PLI, and digital retail platforms.

North India leads at 31.0% versus South India's 24.2% in 2025. South India shows faster EV and premium adoption, while North India benefits from higher volume density and corporate fleet demand.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)