India Pharmaceutical Market Size, Share, Trends and Forecast by Type, Nature, and Region, 2026-2034

India Pharmaceutical Market Size, Share, Trends & Forecast (2026-2034)

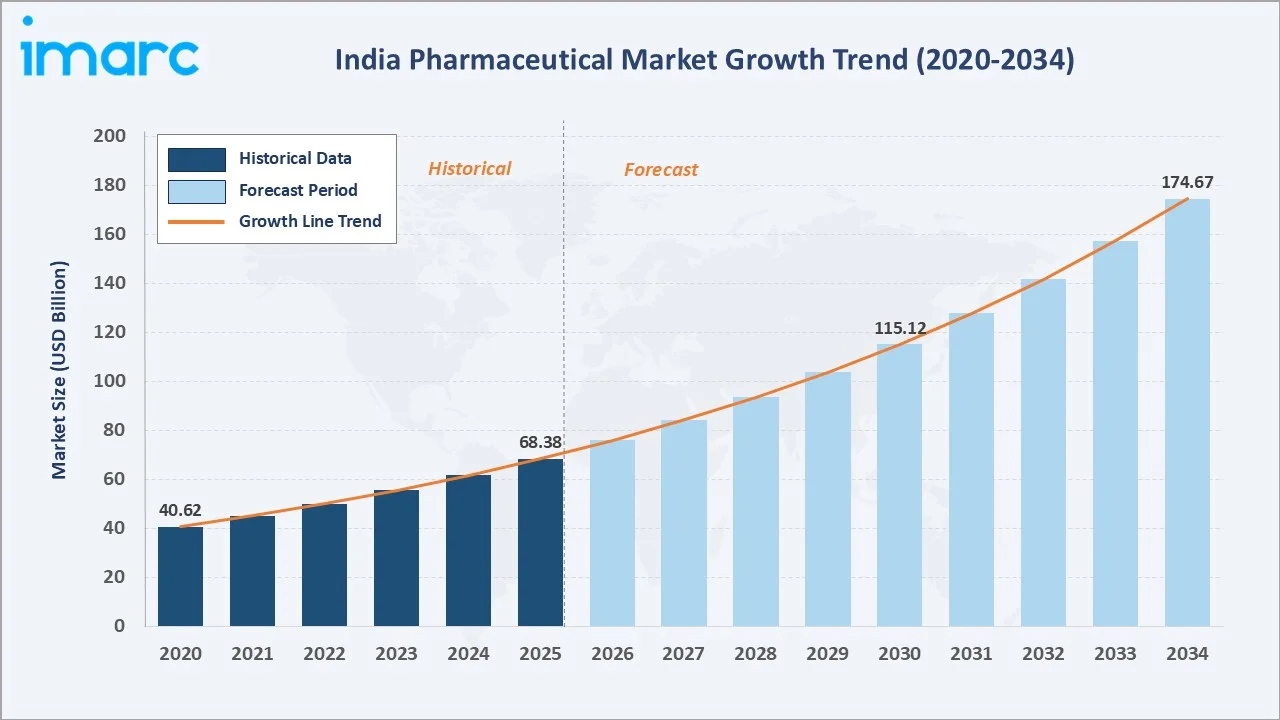

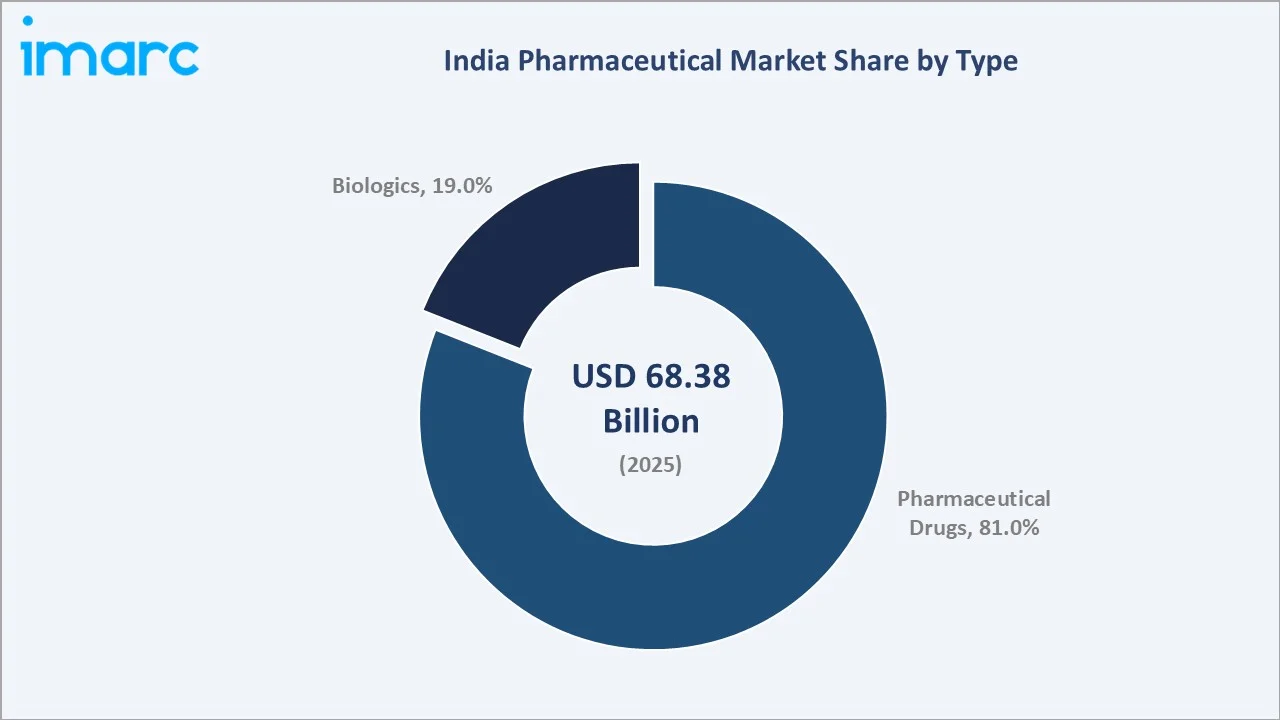

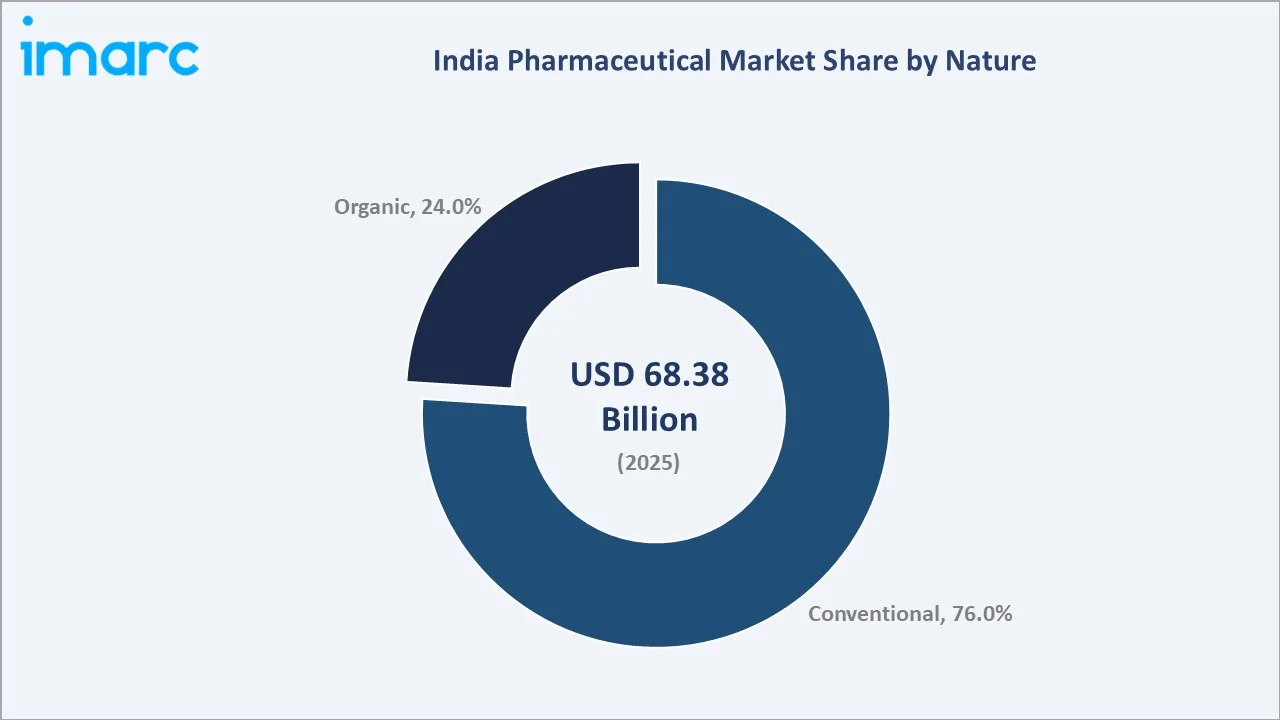

The India pharmaceutical market reached USD 68.38 Billion in 2025 and is projected to reach USD 174.67 Billion by 2034, growing at a CAGR of 10.98% during 2026-2034. India, recognized worldwide as the "Pharmacy of the World," is the global backbone of generic drug supply. Rising chronic disease prevalence, expanding health insurance coverage, strong government policy support through PLI schemes, and surging export demand are the primary growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 68.38 Billion |

|

Forecast Market Size (2034) |

USD 174.67 Billion |

|

CAGR (2026-2034) |

10.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

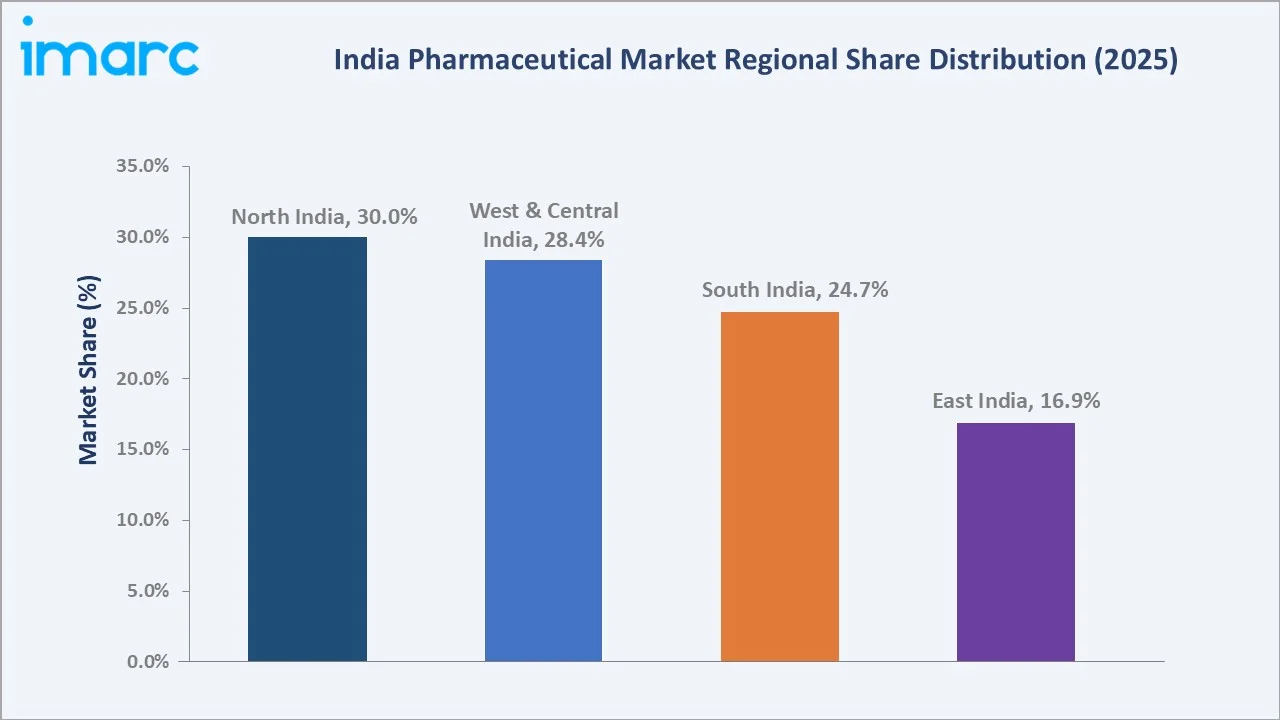

Largest Region |

North India (30.0% share, 2025) |

|

Fastest Growing Segment |

Biologics |

North India dominates, holding a 30.0% market share in 2025, owing to its concentration of pharmaceutical manufacturing hubs and strong distribution networks. Pharmaceutical drugs account for 81.0% of total market revenue. The conventional formulations segment leads with a 76.0% share. India's sector benefits from skilled research talent, cost-efficient API manufacturing, and a favorable regulatory environment supporting global exports.

To get more information on this market, Request Sample

India's pharmaceutical market is positioned for significant expansion through 2034, underpinned by rising healthcare infrastructure investment, patent cliff opportunities for generics, and strategic government initiatives promoting domestic production of active pharmaceutical ingredients. The sector's global export competitiveness further accelerates demand across regulated markets in the US, EU, and Africa.

Executive Summary

The India pharmaceutical market is on a robust growth trajectory, driven by the convergence of favorable demographics, government policy support, and accelerating biomedical innovation. The market was valued at USD 68.38 Billion in 2025 and is forecast to surpass USD 174.67 Billion by 2034, growing at a CAGR of 10.98%. This strong growth is attributable to rising healthcare awareness, expanding insurance coverage, and increasing prescription drug demand across urban and rural populations.

Pharmaceutical drugs dominate market revenue with an 81.0% share in 2025, encompassing cardiovascular, oncology, anti-infective, and metabolic disorder therapeutics. The biologics segment, representing 19.0% in 2025, is the fastest-growing category, with Indian firms such as Biocon Biologics and Dr. Reddy's Laboratories scaling biosimilar pipelines to address global demand. Conventional formulations maintain a 76.0% market share due to established manufacturing processes and extensive distribution infrastructure.

North India leads regionally with a 30.0% share in 2025, supported by major manufacturing clusters in Himachal Pradesh, Uttarakhand, and Delhi-NCR. West and Central India follow at 28.4%, anchored by Gujarat and Maharashtra's pharmaceutical corridors. Leading domestic players, including Sun Pharmaceutical Industries Ltd., Cipla, Dr. Reddy’s Laboratories Ltd., Lupin, and Aurobindo Pharma Limited, maintain global competitiveness alongside multinationals such as Pfizer, GSK, and Abbott India.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Pharmaceutical Drugs – 81.0% share (2025) |

|

Fastest Growing Segment (Type) |

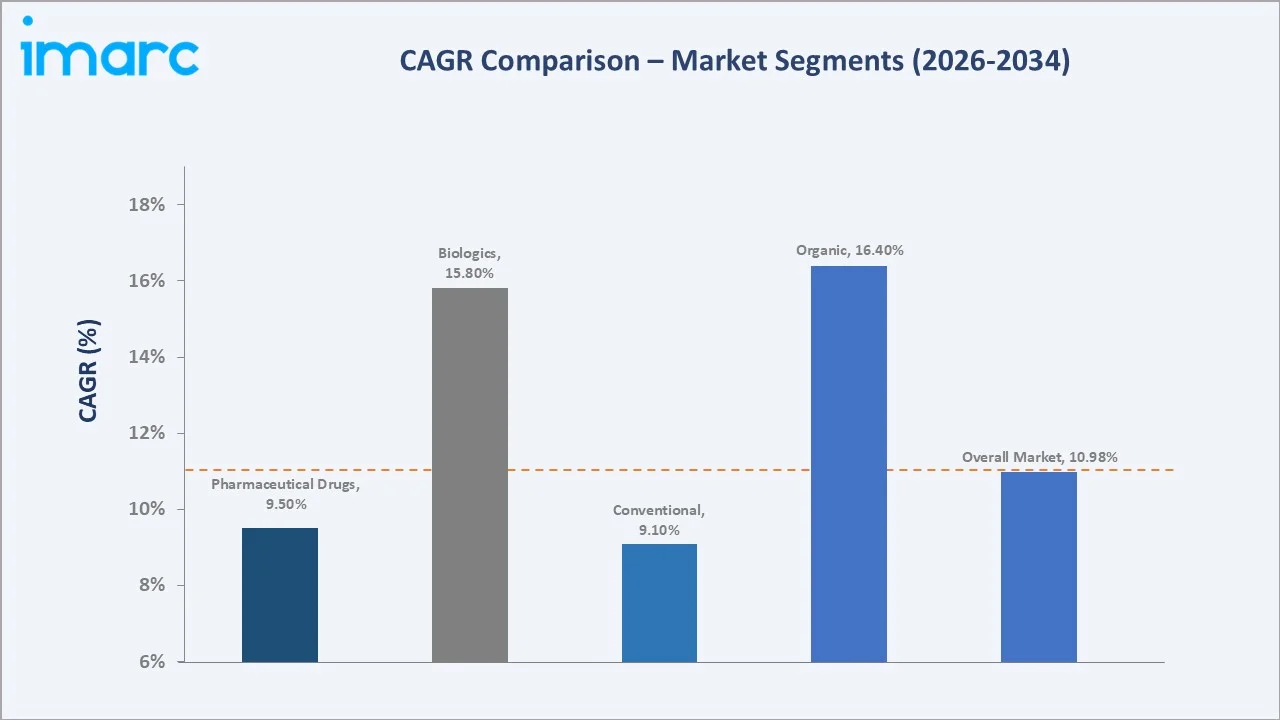

Biologics – ~15.8% CAGR (2026-2034) |

|

Largest Segment (Nature) |

Conventional – 76.0% share (2025) |

|

Leading Region |

North India – 30.0% share (2025) |

|

Fastest Growing Region |

South India (expanding biotech clusters) |

|

Top Companies |

Sun Pharmaceutical Industries Ltd., Cipla, Dr. Reddy’s Laboratories Ltd., Lupin, and Aurobindo Pharma Limited |

Key Analytical Observations Supporting the Above Data:

- Pharmaceutical drugs account for 81.0% of India's pharmaceutical market in 2025, valued at approximately USD 55.39 Billion, driven by high prescription volumes in cardiovascular, anti-infective, and metabolic therapeutic categories across tier-1 and tier-2 cities.

- Biologics represent 19.0% of the market in 2025 (approx. USD 12.99 Billion), propelled by India's emerging biosimilar leadership. Biocon Biologics alone has commercialized over 10 biosimilar molecules globally, with a focus on oncology and immunology.

- North India's 30.0% share reflects its pharmaceutical manufacturing dominance, with Himachal Pradesh and Uttarakhand together hosting over 1,400 manufacturing units that benefit from government excise exemptions and low-cost infrastructure.

- The conventional formulations segment at 76.0% continues to command the market due to physician familiarity, established supply chains, and lower cost structures versus complex biologics or novel drug delivery systems.

- In 2024–25, pharmaceutical exports reached USD 30.5 billion, marking nearly a 16-fold rise from USD 1.9 billion in 2000–01, with exports reaching 191 countries, with around 50% directed to highly regulated markets such as the United States and Europe.

India Pharmaceutical Market Overview

The Indian pharmaceutical industry ranks third globally by volume and eleventh by value, supported by over 3,000 companies and around 10,500 manufacturing units. Recognized as a leading generic drug producer, India supplies over 20% of global generic medicines by volume and manufactures about 60,000 generic brands across 60 therapeutic categories. The ecosystem spans API manufacturers, formulation producers, contract research organizations (CROs), and distributors.

Macroeconomic drivers include rising per-capita healthcare expenditure, government health schemes such as Ayushman Bharat covering over 500 million beneficiaries, and the PLI scheme boosting domestic API production. India's young demographic profile, with approximately 65% of the population below 35 years of age in 2025, creates sustained demand across primary care, OTC, and specialty pharmaceutical segments.

Market Dynamics

To evaluate market opportunities, Request Sample

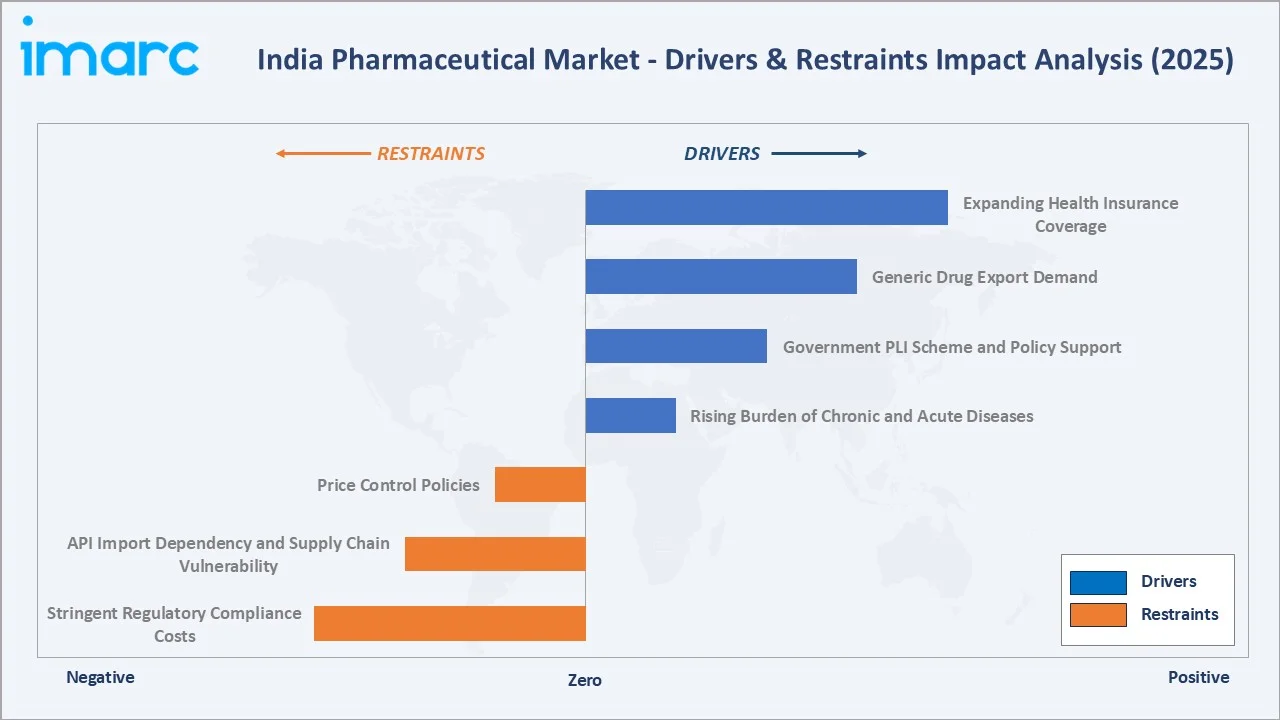

Market Drivers

- Rising Burden of Chronic and Acute Diseases: According to the ICMR–INDIAB Study, India has over 101 million diabetics (2025) and an estimated 220 million hypertension patients, creating sustained demand for cardiovascular, metabolic, and oncology drugs.

- Government PLI Scheme and Policy Support: The Government of India's Production Linked Incentive scheme for pharmaceuticals has committed INR 15,000 Crore (approx. USD 1.8 Billion) to reduce import dependence, strengthen domestic manufacturing, and attract significant investments.

- Generic Drug Export Demand: In 2024–25, pharmaceutical exports reached USD 30.5 billion, driven by patent expiry opportunities in regulated markets and the cost-efficiency advantage of Indian manufacturers.

- Expanding Health Insurance Coverage: Recent National Sample Survey data indicates a sharp rise in India’s health insurance coverage, reaching 47.4% in rural areas and 44.3% in urban regions by 2025, supported by government and private insurer expansion, increasing prescription drug consumption across previously underserved demographic segments.

Market Restraints

- Stringent Regulatory Compliance Costs: Meeting US FDA, EU EMA, and WHO GMP standards requires significant capital investment. USFDA Warning Letters and import alerts issued to Indian facilities create supply disruptions and reputational risks for mid-tier manufacturers.

- API Import Dependency and Supply Chain Vulnerability: In FY 2024–25, India imported around 200 categories of APIs, bulk drugs, and drug intermediates valued at approximately USD 4.35 billion, according to HSN-based import data, with China accounting for about 73.7% of the total. Geopolitical disruptions can trigger input cost escalation, affecting margins across the formulation value chain.

- Price Control Policies: The National Pharmaceutical Pricing Authority (NPPA) oversees 928 drugs under price control in 2025, compressing manufacturer margins particularly in the essential medicines segment and limiting profitability in mass-market formulations.

Market Opportunities

- Biosimilar and Biologics Export Pipeline: With the global biosimilar market projected to reach USD 210.4 Billion by 2034, Indian firms are positioned to capture a disproportionate share. Biocon Biologics, Dr. Reddy's, and Lupin collectively have 45+ biosimilar molecules in development pipelines targeting the US, EU, and emerging markets.

- Contract Manufacturing and CDMO Growth: India's CDMO market is projected to grow at a CAGR of 14% to 15% through 2030, as global innovators increasingly outsource manufacturing to cost-efficient Indian partners. Companies such as Divi's Laboratories and Aurobindo Pharma are expanding dedicated CDMO capacity.

- Digital Health and E-Pharmacy Expansion: E-pharmacy platforms, including PharmEasy and Truemeds (USD 85 Million Series C in 2025), are reshaping distribution. In August 2025, Zepto entered the online pharmacy segment with the launch of Zepto Pharmacy, offering 10-minute medicine delivery in select metro cities like Mumbai, Bengaluru, Delhi-NCR, and Hyderabad.

Market Challenges

- Talent Retention and R&D Competitiveness: India's pharmaceutical sector faces challenges in retaining specialized research talent to global pharma hubs and MNCs. The country's R&D expenditure as a percentage of pharmaceutical revenue remains below 5%, constraining innovation beyond generics and biosimilars.

- Counterfeit Drug Proliferation: An estimated 12-25% of drugs in Indian circulation in 2025 are substandard or counterfeit, according to WHO estimates. This undermines public trust and creates regulatory enforcement burdens that increase operating costs for legitimate manufacturers.

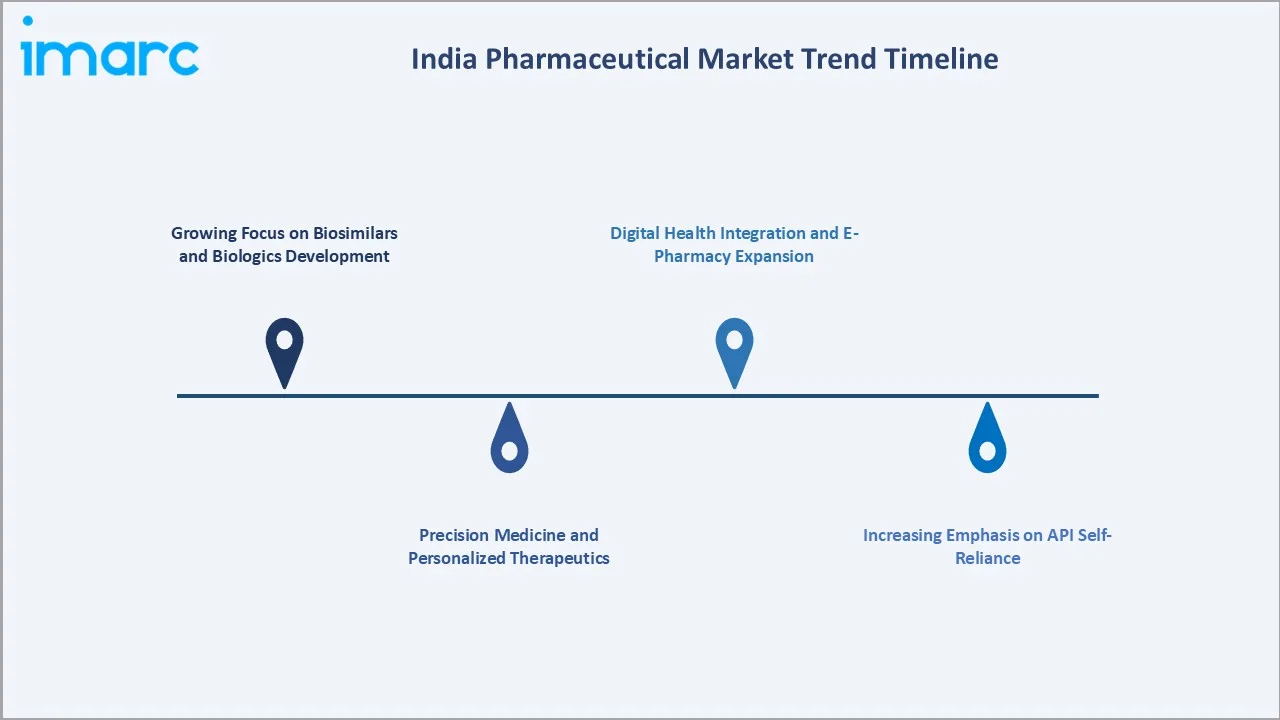

Emerging Market Trends

1. Growing Focus on Biosimilars and Biologics Development

Indian manufacturers are accelerating investment in complex biologics production. Biocon Biologics announced the expansion of its oncology biosimilar portfolio with Trastuzumab, Nivolumab, and Pembrolizumab biosimilars in 2024–2025. The biologics segment grew at approximately 18% annually between 2020 and 2025, outpacing the broader market CAGR, and is positioned to reach a 25% share by 2034.

2. Digital Health Integration and E-Pharmacy Expansion

E-pharmacy and telehealth platforms are reshaping pharmaceutical access across urban and semi-urban India. Truemeds secured USD 85 Million in Series C funding in 2025, while platforms such as Tata 1mg and PharmEasy collectively serve over 5 million registered users and 6,000 digital consultation clinics. Digital prescription systems and AI-driven adherence monitoring are creating new demand pathways for specialty and OTC pharmaceuticals.

3. Increasing Emphasis on API Self-Reliance

Under the PLI Bulk Drugs scheme, as of September 2025, manufacturing capacity has been established for 26 KSMs/APIs, generating cumulative sales of INR 2,315 crore since the scheme’s inception. This structural shift reduces India's vulnerability to API supply disruptions and enables better margin retention across the pharmaceutical value chain, with capacity expansions concentrated in Gujarat, Hyderabad, and Aurangabad clusters.

4. Precision Medicine and Personalized Therapeutics

The convergence of genomics, AI-driven drug discovery, and precision diagnostics is reshaping India's pharmaceutical innovation landscape. In pharmaceutical research, 82% of surveyed organizations in India’s pharma and life sciences sector have implemented AI on a limited scale, with plans to scale up adoption in 2024. Companies such as Sun Pharma and Dr. Reddy's are investing in specialty segment therapies for oncology and dermatology targeting personalized treatment protocols.

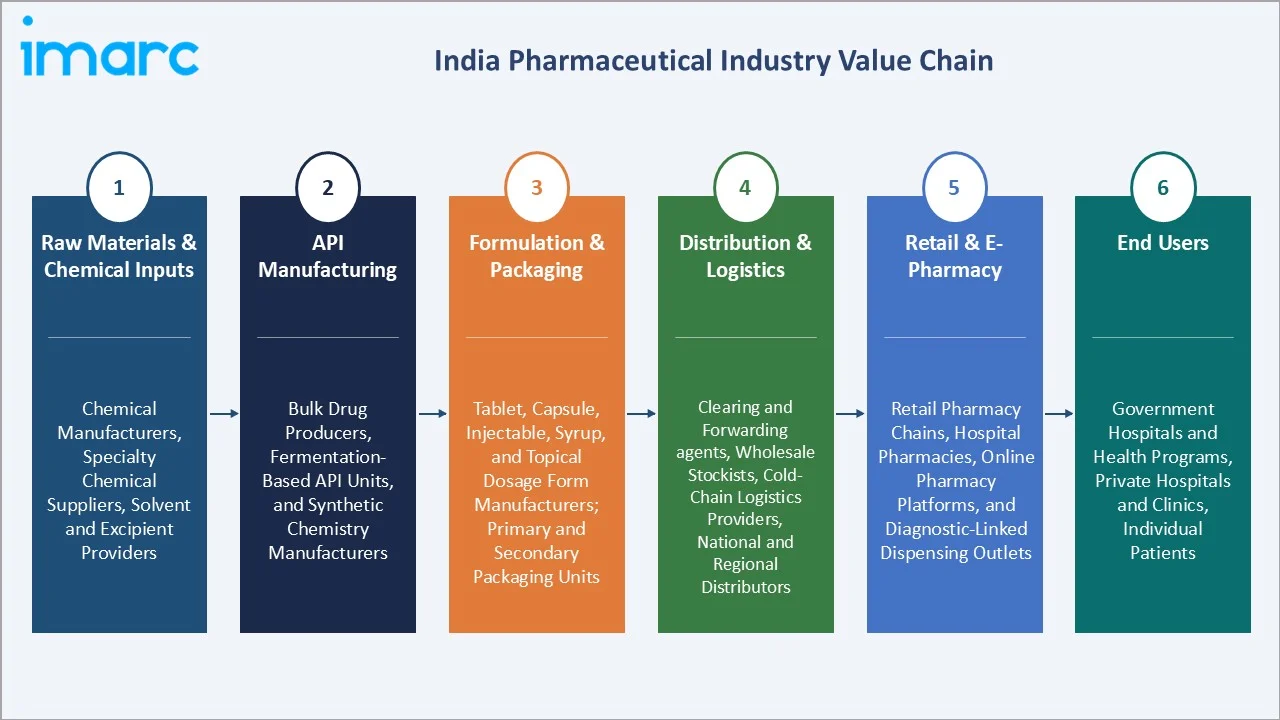

Industry Value Chain Analysis

The India pharmaceutical value chain spans raw material extraction through patient-level distribution, with each stage populated by specialized operators directly influencing product quality, cost, and regulatory compliance.

|

Stage |

Key Players / Examples |

|

Raw Materials & Chemical Inputs |

Chemical manufacturers, specialty chemical suppliers, solvent and excipient providers |

|

API Manufacturing |

Bulk drug producers, fermentation-based API units, and synthetic chemistry manufacturers |

|

Formulation & Packaging |

Tablet, capsule, injectable, syrup, and topical dosage form manufacturers; primary and secondary packaging units |

|

Distribution & Logistics |

Clearing and forwarding agents, wholesale stockists, cold-chain logistics providers, national and regional distributors |

|

Retail & E-Pharmacy |

Retail pharmacy chains, hospital pharmacies, online pharmacy platforms, and diagnostic-linked dispensing outlets |

|

End Users |

Government hospitals and health programs, private hospitals and clinics, and individual patients |

Technology Landscape in the India Pharmaceutical Industry

Biologics and Biosimilar Manufacturing Technology

Indian firms are adopting single-use bioreactor systems, perfusion cell culture technologies, and advanced downstream purification processes to scale biologics production cost-effectively. Biocon Biologics's Bengaluru facility, one of Asia's largest integrated biologics campuses, deploys 500L–2,000L bioreactor scales with mammalian cell culture platforms, producing biosimilar insulins and monoclonal antibodies for global markets.

AI-Driven Drug Discovery

Artificial intelligence platforms are accelerating molecular screening and lead optimization. In April 2024, Aurigene Pharmaceutical Services introduced Aurigene.AI, an AI- and ML-driven platform designed to accelerate drug discovery from hit identification to candidate nomination by integrating predictive, generative models and computer-aided drug design.

Advanced Drug Delivery Systems

Nano-particle drug delivery, liposomal formulations, and transdermal patch technologies are gaining commercial scale in India. Sun Pharma and Lupin are investing in specialty NDDS platforms for targeted cancer therapy, pain management, and chronic disease applications, commanding premium pricing over conventional generics and improving patient outcomes.

Digital Manufacturing and Quality Automation

Continuous manufacturing processes, real-time release testing (RTRT), and digital quality management systems (QMS) are being adopted by major Indian manufacturers to meet FDA and EMA regulatory expectations. India’s pharmaceutical manufacturing is evolving through increased process automation and digital integration, with PLC and SCADA systems enabling real-time monitoring, improved control, and operational flexibility.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Pharmaceutical Drugs | 81.0% | 2025 |

| Nature | Conventional | 76.0% | 2025 |

| Region | North India | 30.0% | 2025 |

By Type

Pharmaceutical drugs dominate the type segment with an 81.0% share in 2025. This segment encompasses small-molecule drugs across cardiovascular, anti-infective, metabolic, CNS, oncology, and respiratory therapeutic categories. Rising chronic disease burden, stronger healthcare infrastructure, and government initiatives driving domestic manufacturing underpin segment dominance.

To access detailed market analysis, Request Sample

Biologics represent 19.0% of the market, growing as the fastest expanding type segment. Indian firms have leveraged generics expertise to develop biosimilar versions of blockbuster biologics. Regulatory approvals for biosimilars in the US and EU by CDSCO-accredited Indian manufacturers continue to accelerate biosimilar revenue contribution.

By Nature

Conventional pharmaceutical formulations hold a 76.0% market share in 2025. The segment's dominance reflects established manufacturing processes, widespread physician prescribing familiarity, cost advantages, and extensive distribution network penetration across urban, semi-urban, and rural geographies.

Organic/specialty formulations account for 24.0% of the market, growing at an estimated 16.4% CAGR. This segment includes herbal-based pharmaceuticals, nutraceuticals with pharmaceutical applications, organic API-derived formulations, and natural active ingredient medicines. Rising consumer preference for natural therapeutics and government Ayush-aligned policy support are driving organic segment growth.

Regional Market Insights

North India's market leadership (30.0%, 2025) reflects its pharmaceutical manufacturing cluster concentration. Himachal Pradesh now hosts 25 contract manufacturing facilities, the highest among northern states, compared to 23 in Madhya Pradesh and 10 in Uttarakhand. The region is benefiting from excise duty exemptions, while Delhi-NCR serves as a critical distribution and corporate headquarters hub.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

30.0% |

Manufacturing clusters (HP, Uttarakhand), distribution hubs |

|

West & Central India |

28.4% |

Gujarat pharma corridor, Maharashtra biotech hubs, strong export base |

|

South India |

24.7% |

Hyderabad API cluster, Bengaluru biotech, strong R&D ecosystem |

|

East India |

16.9% |

Growing healthcare infrastructure, state health schemes, and generic demand |

South India, while third in market share at 24.7%, hosts India's most innovation-intensive pharmaceutical ecosystem. Hyderabad's Genome Valley cluster is home to over 200 biotech and pharmaceutical R&D companies, with companies such as Divi's Laboratories and Aurobindo Pharma operating FDA-approved API manufacturing at a global scale.

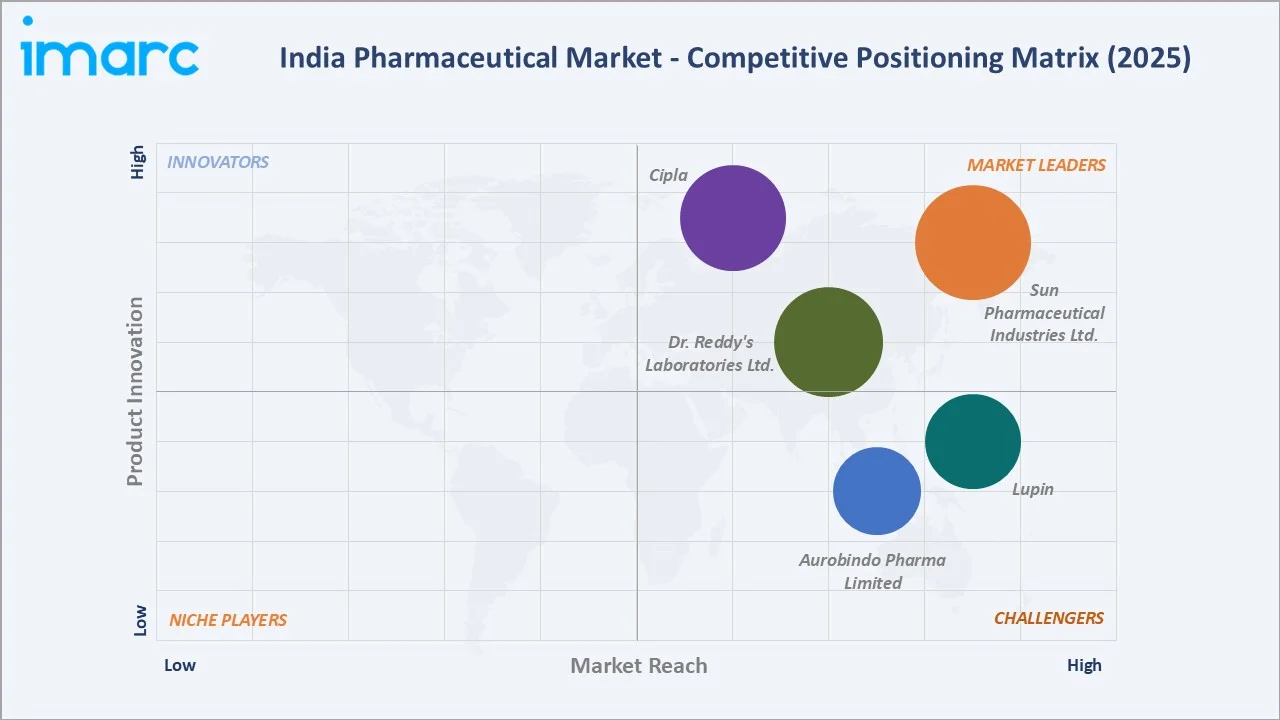

Competitive Landscape

The India pharmaceutical market exhibits a moderately fragmented competitive structure. The top five manufacturers, including Sun Pharmaceutical Industries Ltd., Cipla, Dr. Reddy’s Laboratories Ltd., Lupin, and Aurobindo Pharma Limited, collectively hold approximately 30–35% of total market revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Sun Pharmaceutical Industries Ltd. |

Sun Pharma |

Market Leader |

India's largest pharma co.; US generics and specialty leadership |

|

Cipla |

Cipla |

Market Leader |

Respiratory, ARV, and oncology generics; 80+ country exports |

|

Dr. Reddy’s Laboratories Ltd. |

Dr. Reddy's |

Market Leader |

US generics, APIs, biosimilar pipeline; PSAI division |

|

Lupin |

Lupin |

Strong Challenger |

US and Japan generics; branded formulations in India |

|

Aurobindo Pharma Limited |

Aurobindo |

Strong Challenger |

API manufacturing; US injectables and oral solids |

Multinational corporations, including Pfizer, GSK, Abbott, and Novartis, command significant shares in specialty and OTC segments, while regional manufacturers and private-label distributors account for the balance across tier-2 and tier-3 markets.

Key Company Profiles

Sun Pharmaceutical Industries Ltd.

Sun Pharmaceutical Industries, headquartered in Mumbai, is India's largest pharmaceutical company by revenue and one of the world's leading specialty generic pharmaceutical companies. The company operates in 100+ countries with a diversified portfolio spanning branded generics, specialty pharmaceuticals, and OTC products.

- Product Portfolio: Generics, branded generics, speciality, difficult-to-make technology intensive products, over-the-counter (OTC), anti-retrovirals (ARVs), Active Pharmaceutical Ingredients (APIs), and intermediates.

- Recent Developments: In March 2026, Sun Pharma launched its semaglutide injection in India under the brands Noveltreat (for weight management) and Sematrinity (for type 2 diabetes), offering multiple dose strengths and user-friendly prefilled pen devices.

- Strategic Focus: Specialty pharmaceutical leadership; increasing branded generics share in the Indian market; biosimilar pipeline development.

Cipla

Cipla, headquartered in Mumbai, is a global pharmaceutical company with a 90-year legacy in affordable medicine access. It supplies critical antiretroviral, respiratory, and oncology medicines to over 80 countries, with a strong social mission rooted in the HIV/AIDS access movement from 2001 onwards.

- Product Portfolio: Respiratory inhalers, ARVs, oncology generics, and peptide-based injectables across 50+ therapeutic categories.

- Recent Developments: In December 2025, Cipla partnered with Stempeutics Research to launch Ciplostem, a DCGI-approved stem cell therapy for knee osteoarthritis targeting Grade II and III patients, marking its entry into orthobiologic treatments.

- Strategic Focus: Branded formulations growth in India.

Lupin

Lupin, headquartered in Mumbai, is among the top 3 generic pharmaceutical companies in the US by prescription volume. The company has a strong branded formulations presence in India, particularly in cardiovascular and anti-tuberculosis therapy.

- Product Portfolio: Cardiovascular, anti-infective, CNS, and ophthalmology generics; inhalation products for COPD and asthma.

- Recent Developments: In December 2025, Lupin entered into an exclusive licensing, supply, and distribution agreement with Gan & Lee Pharmaceuticals for Bofanglutide, a novel GLP-1 receptor agonist, gaining exclusive rights to commercialize the therapy in India.

- Strategic Focus: Branded generics in India; Japan market consolidation.

Market Concentration Analysis

The India pharmaceutical market reflects moderate concentration at the manufacturer level, with the top 10 domestic companies holding approximately 35–40% of total domestic market revenue in 2025. A large base of 3,000+ manufacturers and 10,500+ registered pharmaceutical companies ensures substantial fragmentation, particularly in the branded generics and OTC segments, creating competitive pricing dynamics that benefit healthcare consumers.

Consolidation activity is gradually increasing, driven by regulatory compliance costs, quality upgrade requirements to meet USFDA and EU EMA standards, and the capital intensity of biosimilar development. Between 2020 and 2025, approximately 12 significant M&A transactions reshaped the competitive map, including Mankind Pharma's acquisition of Panacea Biotec's domestic formulation business.

Investment & Growth Opportunities

Fastest Growing Segments

Biologics and biosimilars (estimated CAGR 15.8%), organic and natural formulations (16.4% CAGR), and specialty injectables (12.1% CAGR) represent the three highest-growth investment vectors through 2034. Together, these categories address a total addressable market of approximately USD 35 Billion by 2030 within India's domestic and export combined market.

Emerging Market Expansion

India's pharmaceutical companies are aggressively expanding into Africa, Latin America, and Southeast Asia. These markets collectively represent an incremental USD 15+ Billion pharmaceutical export opportunity by 2034. Entry via technology transfer partnerships, joint ventures with local distributors, and compliance with WHO GMP standards are the preferred market entry modalities, with generics and ARVs driving initial market penetration.

Venture and Institutional Investment Trends

- Key investment themes include AI-driven drug discovery, digital health platforms, biologics manufacturing infrastructure, and India-specific rare disease therapy development.

- Private equity investment in Indian pharma exceeded USD 4.2 Billion across 2022–2025, focused on CDMO capacity expansion, specialty formulations, and biosimilar clinical development programs.

- Government production-linked incentive schemes for pharmaceuticals (INR 15,000 Crore) are generating institutional co-investment opportunities aligned with domestic manufacturing expansion objectives.

Future Market Outlook (2026-2034)

The India pharmaceutical market is positioned for sustained, broad-based growth through 2034. From a base of USD 68.38 Billion in 2025, the market is projected to reach USD 174.67 Billion by 2034, representing total incremental value creation of USD 106.29 Billion over the forecast period at a CAGR of 10.98%.

Regulatory evolution will shape competitive dynamics: the CDSCO's new drug approval reforms, India's updated biosimilar guidelines aligning with WHO standards, and the USFDA's continued regulatory scrutiny of Indian manufacturing facilities will collectively drive quality investment across the sector. Manufacturers that achieve gold-standard compliance portfolios by 2027 are positioned to capture disproportionate shares of US and EU generic procurement markets.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 140 industry participants in 2024–2025, including pharmaceutical manufacturers, API producers, regulatory consultants, hospital pharmacists, healthcare professionals, and investment analysts across India, the US, and the EU. Insights were collected through in-depth interviews and standardized questionnaires to validate market sizing and segment data.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, CDSCO regulatory filings, Ministry of Health and Family Welfare data, PHARMEXCIL export data, industry databases (Pharma Bureau, IMS Health, AIOCD AWACS), trade publications, and publicly available financial data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, disease burden data, insurance penetration rates, export market analysis, and historical market evolution. A base-case CAGR of 10.98% reflects consensus analyst estimates validated against reported manufacturer revenue growth rates from FY2020 to FY2025.

India Pharmaceutical Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Natures Covered | Organic, Conventional |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Sun Pharmaceutical Industries Ltd., Cipla, Dr. Reddy’s Laboratories Ltd., Lupin, Aurobindo Pharma Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Pharmaceutical Market Report

The India pharmaceutical market was valued at USD 68.38 Billion in 2025 and is projected to reach USD 174.67 Billion by 2034.

The market is expected to grow at a CAGR of 10.98% during 2026-2034, driven by rising healthcare demand, biosimilar sector expansion, and growing export revenues.

North India leads with a 30.0% share in 2025, supported by major pharmaceutical manufacturing clusters in Himachal Pradesh and Uttarakhand.

Pharmaceutical drugs dominate with an 81.0% share in 2025, valued at approximately USD 55.39 Billion, driven by high chronic and acute disease drug demand.

Conventional formulations hold a 76.0% share in 2025, valued at approximately USD 51.97 Billion, owing to established manufacturing and distribution networks.

Key players include Sun Pharmaceutical Industries Ltd., Cipla, Dr. Reddy’s Laboratories Ltd., Lupin, and Aurobindo Pharma Limited.

The PLI scheme committed approximately USD 1.8 Billion to incentivize domestic API manufacturing, reducing India's API import dependency from 68% in 2020 to approximately 52% in 2025.

Key challenges include USFDA regulatory compliance costs, API import dependency from China, NPPA price controls, counterfeit drug proliferation, and R&D talent retention.

Biosimilars, CDMO capacity expansion, e-pharmacy platforms, AI drug discovery, and specialty injectables represent the highest-growth investment opportunities through 2034.

Biologics held a 19.0% market share in 2025 and are growing at approximately 15.8% CAGR, driven by Indian firms scaling biosimilar pipelines for global regulated markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)