India Plastic Caps and Closure Market Size, Share, Trends and Forecast by Product Type, Raw Material, Container Type, Technology, End Use, and Region, 2026-2034

India Plastic Caps and Closure Market Summary:

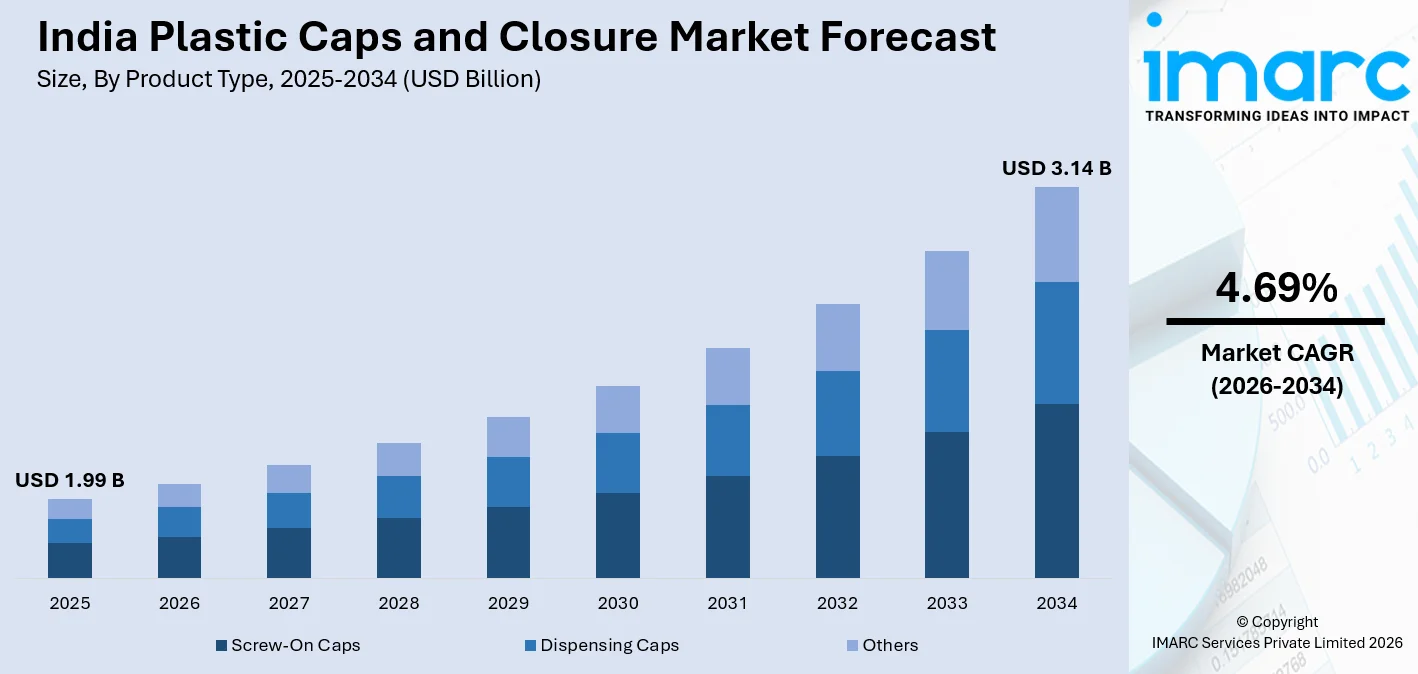

The India plastic caps and closure market size was valued at USD 1.99 Billion in 2025 and is projected to reach USD 3.14 Billion by 2034, growing at a compound annual growth rate of 4.69% from 2026-2034.

India's plastic caps and closure market is propelled by robust expansion in the packaged beverage, food processing, and pharmaceutical sectors. Growing urbanization, rising disposable incomes, and shifting consumer preferences toward hygienic and tamper-evident packaging continue to amplify demand. The increasing scale of organized retail and e-commerce distribution is accelerating the adoption of high-performance closure solutions, underpinning sustained growth in the India plastic caps and closure market share.

Key Takeaways and Insights:

- By Product Type: Screw-on caps dominate the market with a share of 58.5% in 2025, owing to their versatile performance across beverage, food, and personal care packaging applications, combined with ease of use and reliable re-sealability.

- By Raw Material: PP leads the market with a share of 42.5% in 2025, driven by its superior chemical resistance, processing versatility, and cost efficiency across a wide range of closure manufacturing applications.

- By Container Type: Plastic is the largest segment with a share of 86.5% in 2025, reflecting the widespread adoption of lightweight, shatter-resistant plastic containers across food, beverage, and household chemical industries.

- By Technology: Injection molding holds the largest share of 52.5% in 2025, attributed to its capacity for high-volume production of precision-engineered closures with consistent dimensional accuracy.

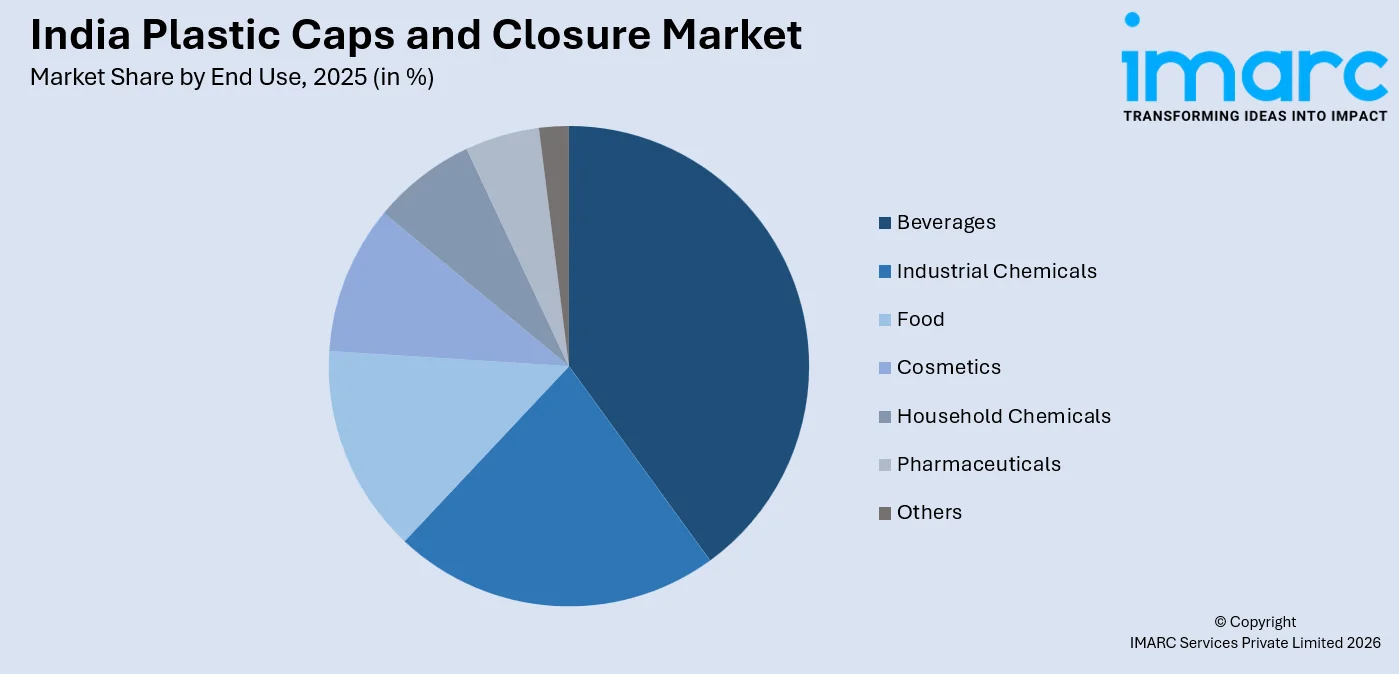

- By End Use: Beverages lead the market with a share of 39.8% in 2025, driven by India's rapidly expanding packaged water, carbonated soft drinks, and ready-to-drink beverage categories.

- By Region: North India dominates the market with a share of 32.2% in 2025, supported by a high concentration of food and beverage manufacturers, pharmaceutical plants, and robust logistics infrastructure.

- Key Players: The India plastic caps and closure market features a competitive mix of global and domestic manufacturers across diverse packaging segments. Some of the key players include, AptarGroup, Inc., Bericap Holding GmbH, Berry Global, Inc., KKD International, Vimal Plastics Pvt. Ltd., Aglo Polymers Pvt. Ltd., Sonoco Products Company, and Amcor Group GmbH.

To get more information on this market Request Sample

The India plastic caps and closure market is experiencing consistent growth, underpinned by the country's expanding consumer packaged goods sector and accelerating urbanization. As one of the world's most dynamic economies, India presents a fertile environment for packaging innovation, with demand rising across beverages, pharmaceuticals, food, and household chemicals. In August 2025, Guala Closures announced the acquisition of the metal closures division of Oricon Enterprises, strengthening its manufacturing footprint in India and expanding its portfolio of premium closure solutions for spirits and beverage packaging. The adoption of tamper-evident and child-resistant closures is increasing in response to evolving safety regulations and heightened consumer awareness around product integrity. Manufacturers are prioritizing lightweight closure designs that minimize material usage without compromising performance. The shift toward convenient, on-the-go packaging formats is further amplifying closure demand. Additionally, the rapid growth of organized retail is prompting brand owners to invest in aesthetically differentiated closures that reinforce brand identity and elevate shelf appeal.

India Plastic Caps and Closure Market Trends:

Rising Demand for Tamper-Evident and Child-Resistant Closures

The demand for tamper-evident and child-resistant closures is accelerating across India's pharmaceutical and household chemical packaging sectors. Regulatory frameworks are increasingly mandating protective packaging that prevents accidental ingestion and unauthorized access. In August 2025, Closure Systems International launched a new range of child-resistant closures designed for pharmaceutical packaging applications, aimed at enhancing consumer safety while meeting stricter regulatory compliance requirements. This trend is driving manufacturers to engineer innovative closure systems that balance safety performance with consumer convenience, resulting in multi-functional designs serving both protective and practical roles across high-risk product categories.

Expansion of India's Organized Beverage Sector

India's organized beverage industry is undergoing rapid expansion, fueled by rising disposable incomes, evolving consumption habits, and growing preference for packaged beverages across urban and semi-urban markets. This momentum is generating robust demand for high-performance plastic closures designed for leak-proof sealing and product freshness. In 2024, Varun Beverages, one of the largest franchise bottlers of PepsiCo beverages in India, announced plans to expand its production capacity with new bottling plants to meet rising demand for carbonated drinks and packaged beverages in the country. Manufacturers are adapting closure formats to accommodate the diverse packaging structures increasingly utilized by beverage producers serving varied consumer tastes.

Growing Shift Toward Sustainable Packaging Practices

Sustainability is emerging as a defining trend in India's plastic closure market as packaging converters and brand owners respond to mounting environmental concerns. The industry is gradually transitioning toward closures made from recycled and bio-based polymers, alongside efforts to reduce material weight without compromising structural integrity. In January 2026, the Ministry of Environment, Forest and Climate Change tightened India’s Extended Producer Responsibility (EPR) rules for plastic packaging, requiring producers, importers, and brand owners to meet stricter recycling obligations and comply with category-specific recycling targets for plastic waste. Extended producer responsibility frameworks and rising consumer consciousness around plastic waste are encouraging manufacturers to develop eco-compatible closure solutions aligned with circular economy principles.

Market Outlook 2026-2034:

The India plastic caps and closure market is poised for consistent growth over the forecast period, supported by continued expansion across beverages, pharmaceuticals, food, and personal care. Modernization of India's retail infrastructure and deepening distribution penetration into tier-two and tier-three cities are expected to unlock new consumption centers. Premiumization trends in food and beverage packaging, combined with regulatory emphasis on tamper-proof closures and sustainable material adoption, will catalyze ongoing market evolution. The market generated a revenue of USD 1.99 Billion in 2025 and is projected to reach a revenue of USD 3.14 Billion by 2034, growing at a compound annual growth rate of 4.69% from 2026-2034.

India Plastic Caps and Closure Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Screw-On Caps |

58.5% |

|

Raw Material |

PP |

42.5% |

|

Container Type |

Plastic |

86.5% |

|

Technology |

Injection Molding |

52.5% |

|

End Use |

Beverages |

39.8% |

|

Region |

North India |

32.2% |

Product Type Insights:

- Screw-On Caps

- Dispensing Caps

- Others

The screw-on caps dominate with a market share of 58.5% of the total India plastic caps and closure market in 2025.

Screw-on caps represent the most widely adopted closure format across India's packaging landscape, delivering consistent performance across beverages, edible oils, personal care products, and pharmaceutical liquids. Their dominance is rooted in ease of application, reliable re-sealability, and compatibility with high-speed automated filling and capping lines. The structural simplicity of screw-on designs reduces production complexity while ensuring dependable torque performance, positioning them as the preferred choice for large-scale manufacturers seeking cost efficiency without sacrificing packaging integrity.

The sustained leadership of Screw-on caps is further reinforced by continuous innovation in thread configurations, liner materials, and tamper-evident band designs. As consumer expectations around packaging convenience and product safety continue to evolve, manufacturers are integrating enhanced sealing mechanisms into screw-on formats to meet growing market demands. Their adaptability across a diverse range of neck finishes and container materials ensures that screw-on caps remain indispensable across India's food, beverage, pharmaceutical, and personal care sectors throughout the forecast period.

Raw Material Insights:

- PET

- PP

- HDPE

- LDPE

- Others

The PP leads with a share of 42.5% of the total India plastic caps and closure market in 2025.

Polypropylene is the dominant raw material in India's plastic caps and closure market, valued for its exceptional balance of chemical resistance, mechanical strength, and processing flexibility. Its compatibility with injection and compression molding processes makes it the preferred polymer for manufacturing a wide range of closure types, including screw-on, dispensing, and snap-fit designs. Its resistance to heat and moisture ensures the integrity of closures used in hot-fill beverage applications and chemically sensitive product categories such as household cleaners and industrial fluids.

The preference for polypropylene is further driven by its cost-effectiveness relative to engineering-grade alternatives and the availability of a well-established domestic supply chain across India. Its recyclability aligns with the growing industry emphasis on sustainable packaging practices, enabling manufacturers to meet both performance and environmental objectives simultaneously. As India's packaging industry continues to scale in response to expanding consumer and industrial markets, polypropylene's role as the primary closure raw material is expected to remain firmly entrenched throughout the forecast period.

Container Type Insights:

- Plastic

- Glass

- Others

The plastic dominates with a market share of 86.5% of the total India plastic caps and closure market in 2025.

Plastic containers constitute the overwhelming majority of closure applications in India, reflecting a broad preference for lightweight, shatter-resistant, and economically viable packaging formats across virtually all end-use industries. The compatibility of plastic containers with high-throughput automated packaging lines, combined with their superior cost-to-performance ratio relative to glass and metal alternatives, has cemented their market dominance. According to reports, Amcor expanded its advanced packaging capabilities in India with new investments aimed at strengthening its portfolio of lightweight plastic packaging solutions for food, beverage, and personal care products. As India's manufacturing and consumer goods sectors continue to expand, plastic containers remain the structural foundation driving consistent and diversified demand for compatibly engineered closures.

The dominance of plastic containers is amplified by their widespread deployment across beverages, household chemicals, agriculture, pharmaceuticals, and personal care categories. The extensive variety of plastic container types and neck finishes creates continuous demand for compatibly designed closures tailored to specific application requirements. Ongoing investments in plastic container manufacturing capacity across India's major industrial corridors are expected to sustain this segment's commanding market position and reinforce its integral relationship with closure manufacturing throughout the forecast period.

Technology Insights:

- Injection Molding

- Compression Molding

- Post-Mold Tamper-Evident Band

The injection molding leads with a share of 52.5% of the total India plastic caps and closure market in 2025.

Injection molding is the prevailing manufacturing technology for plastic caps and closures in India, recognized for producing high volumes of precision-engineered closures with consistent dimensional accuracy and superior surface quality. The technology accommodates a wide range of polymer types and enables the production of complex closure geometries, including multi-component designs incorporating integrated sealing liners and tamper-evident features. High output rates and minimal material wastage make injection molding the preferred choice for large-scale closure manufacturers seeking operational efficiency and product uniformity.

Continued investment in advanced injection molding equipment, including multi-cavity tooling and automated quality inspection systems, is reinforcing this segment's technological leadership. Closure manufacturers across India are increasingly adopting energy-efficient injection molding platforms that reduce cycle times and operating costs, enhancing their competitive positioning in both domestic and export markets. As demand for precision-engineered plastic closures continues to grow across diverse end-use industries, injection molding will remain the primary production methodology underpinning India's closure manufacturing ecosystem throughout the forecast period.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Beverages

- Industrial Chemicals

- Food

- Cosmetics

- Household Chemicals

- Pharmaceuticals

- Others

The beverages dominate with a market share of 39.8% of the total India plastic caps and closure market in 2025.

The beverages segment is the largest driver of plastic closure demand in India, encompassing packaged drinking water, carbonated soft drinks, fruit juices, energy drinks, and ready-to-drink beverages. The rapid expansion of India's bottled beverage industry, fueled by urbanization, a large and youthful consumer demographic, and growing health consciousness, has generated sustained demand for reliable, tamper-evident, and aesthetically appealing closures. Closure formats must withstand carbonation pressure and maintain airtight sealing throughout the supply chain, creating ongoing demand for technologically optimized designs.

The beverage sector's growing emphasis on product differentiation through packaging has elevated closures as critical branding tools. Brand owners are investing in custom-colored, shaped, and embossed closures that enhance on-shelf visibility and communicate premium product positioning. As India's organized beverage market continues to penetrate smaller towns and rural markets, the requirement for durable, cost-effective, and scalable closure formats will continue to drive sustained expansion of this leading end-use segment throughout the forecast period.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India exhibits a clear dominance with a 32.2% share of the total India plastic caps and closure market in 2025.

North India's commanding position in the plastic caps and closure market reflects the region's dense concentration of food and beverage manufacturing facilities, pharmaceutical plants, and fast-moving consumer goods operations. States such as Uttar Pradesh, Punjab, and Haryana host large-scale packaging operations serving both domestic and export markets. The region benefits from well-developed logistics infrastructure and proximity to major polymer raw material suppliers, enabling efficient production and broad distribution of plastic closures across diverse industry verticals.

The region's market strength is further supported by a large and growing urban consumer base that is driving accelerating demand for packaged food, beverages, and personal care products. Strong retail penetration, an expanding organized grocery sector, and the presence of numerous national and regional brand owners actively investing in packaging upgrades collectively reinforce North India's dominance. These structural advantages are expected to sustain the region's leadership position across the forecast period as consumption continues to deepen.

Market Dynamics:

Growth Drivers:

Why is the India Plastic Caps and Closure Market Growing?

Rapid Expansion of India's Packaged Beverage Industry

India's packaged beverage industry is undergoing transformative growth driven by accelerating urbanization, rising health consciousness, and a growing preference for hygienic and convenient packaged formats. The proliferation of bottled water, fruit juices, energy drinks, and ready-to-drink beverages has created an expansive and continuously growing base of closure demand. According to reports, Bisleri International announced the expansion of its packaged drinking water portfolio with the launch of the Vedica Himalayan Sparkling Water in new bottle formats to cater to premium beverage consumers in India. The adoption of modern retail formats and deepening organized supply chain penetration are multiplying consumption touchpoints, creating a sustained pipeline of demand for high-performance plastic closures tailored to India's diverse and rapidly evolving beverage product portfolio.

Growth of India's Pharmaceutical Packaging Sector

India's pharmaceutical industry, one of the largest globally by production volume, generates substantial and growing demand for specialized plastic closures that meet stringent safety and quality standards. The strong growth trajectory of pharmaceutical packaging further reflects this demand, with the India pharmaceutical packaging market valued at USD 1,907.15 million in 2024 and projected to reach USD 3,447.8 million by 2033. Rising prevalence of chronic diseases, expanding healthcare access, and increasing self-medication trends are driving robust growth in pharmaceutical product volumes, necessitating a corresponding expansion in compliant and technically advanced packaging solutions. Child-resistant and senior-friendly closure designs are gaining prominence as regulatory authorities enforce packaging safety mandates across prescription and over-the-counter drug categories. The expansion of contract manufacturing organizations and pharmaceutical export activity is further amplifying the breadth and scale of closure requirements across India's pharmaceutical packaging value chain.

Rising Investment in India's Food Processing Infrastructure

India's food processing sector is attracting significant public and private investment aimed at reducing post-harvest losses, improving food safety standards, and extending the shelf life of value-added products. Government policy support and incentive schemes for food processing are catalyzing capacity expansion across dairy, snacks, condiments, and ready-to-eat meals. For instance, the Government of India continues to promote the sector through the Pradhan Mantri Kisan SAMPADA Yojana, which provides financial assistance for food processing infrastructure, cold chains, and agro-processing clusters to strengthen value-added food production and reduce wastage. This growth is creating robust demand for hermetically sealed packaging equipped with functional plastic closures that preserve product freshness and prevent contamination. As processed and packaged food products capture a larger share of Indian consumer expenditure, demand for innovative and hygienic closure formats compatible with modern food packaging processes will continue to strengthen materially.

Market Restraints:

What Challenges the India Plastic Caps and Closure Market is Facing?

Volatility in Polymer Raw Material Prices

The plastic caps and closure industry's dependence on petroleum-derived polymers makes it highly susceptible to fluctuations in crude oil prices and upstream petrochemical supply conditions. Price volatility in raw materials creates margin pressures for closure manufacturers, particularly smaller producers with limited ability to absorb or pass through input cost increases. This unpredictability complicates production cost management, procurement planning, and long-term pricing strategies, disrupting stable operations across the value chain and deterring investment in capacity expansion.

Stringent Environmental Regulations on Single-Use Plastics

Growing regulatory scrutiny of single-use plastics at national and state levels in India is creating compliance complexity for plastic closure manufacturers. Regulations targeting single-use plastic items are prompting packaging buyers to explore alternative materials, potentially limiting addressable market opportunities for conventional plastic closures. Manufacturers are required to make material and design investments to meet evolving Extended Producer Responsibility mandates and sustainability criteria imposed by brand owners and institutional procurement policies, adding to operational costs.

Intense Price Competition and Market Fragmentation

India's plastic caps and closure market is characterized by a large number of small and medium-scale manufacturers competing primarily on price, resulting in structural margin compression across the industry. Low barriers to entry for basic closure formats attract frequent new entrants, intensifying competitive pressure on established players. Differentiation through product innovation and quality consistency requires sustained capital investment that many domestic manufacturers find challenging, creating persistent tension between competitive pricing imperatives and the pursuit of quality improvement and technical advancement objectives.

Competitive Landscape:

The India plastic caps and closure market features a dynamic and evolving competitive environment encompassing global packaging conglomerates alongside agile domestic manufacturers. International players bring advanced technical capabilities, extensive product portfolios, and significant research and development resources that enable them to address the growing demand for specialized and premium closure formats. Domestic manufacturers compete effectively in high-volume, price-sensitive segments by leveraging proximity to customers, lower operating costs, and established distribution networks. The competitive landscape is further shaped by the progressive adoption of automation and precision manufacturing technologies, raising quality benchmarks industry-wide. Strategic focus on product customization, lightweight design, material innovation, and sustainable closure solutions is emerging as a key differentiator among leading participants seeking to strengthen their positioning. Growing collaboration between packaging manufacturers and brand owners to develop co-engineered closure solutions tailored to specific application requirements is a notable feature of the competitive dynamic in this market.

Some of the key players include:

- AptarGroup, Inc.

- Bericap Holding GmbH

- Berry Global, Inc.

- KKD International

- Vimal Plastics Pvt. Ltd.

- Aglo Polymers Pvt. Ltd.

- Sonoco Products Company

- Amcor Group GmbH

Recent Developments:

- In November 2025, Nipra Industries introduced new pry-off crown caps at the drinktec India 2025 exhibition in Mumbai, marking the company’s expansion into advanced beverage closure solutions. The caps are designed for glass beverage bottles and aim to improve sealing performance and manufacturing efficiency for breweries and beverage brands in India’s growing packaging market.

India Plastic Caps and Closure Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types End Use | Screw-On Caps, Dispensing Caps, Others |

| Raw Materials End Use | PET, PP, HDPE, LDPE, Others |

| Container Types End Use | Plastic, Glass, Others |

| Technologies End Use | Injection Molding , Compression Molding, Post-Mold Tamper-Evident Band |

| End Uses End Use | Beverages, Industrial Chemicals, Food, Cosmetics, Household Chemicals, Pharmaceuticals, Others |

| Regions End Use | North India, West and Central India, South India, East India |

| Companies Covered | AptarGroup, Inc., Bericap Holding GmbH, Berry Global, Inc., KKD International, Vimal Plastics Pvt. Ltd., Aglo Polymers Pvt. Ltd., Sonoco Products Company, Amcor Group GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Plastic Caps and Closure Market Report

The India plastic caps and closure market size was valued at USD 1.99 Billion in 2025.

The India plastic caps and closure market is expected to grow at a compound annual growth rate of 4.69% from 2026-2034 to reach USD 3.14 Billion by 2034.

Screw-On Caps held the largest share of the market, owing to their versatile application across beverage, food, pharmaceutical, and personal care packaging, combined with ease of use and reliable sealing performance.

Key factors driving the India plastic caps and closure market include rapid expansion of the packaged beverage industry, growth of the pharmaceutical packaging sector, rising investment in food processing infrastructure, urbanization, and growing consumer preference for hygienic and tamper-evident packaging solutions.

Major challenges include volatility in polymer raw material prices, stringent and evolving environmental regulations on single-use plastics, intense price competition in a fragmented market structure, compliance with Extended Producer Responsibility mandates, and margin pressures on small and medium-scale manufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)