India Point of Care Diagnostics Market Size, Share, Trends and Forecast by Product Type, Platform, Prescription Mode, End User, and Region, 2026-2034

India Point of Care Diagnostics Market Size and Share:

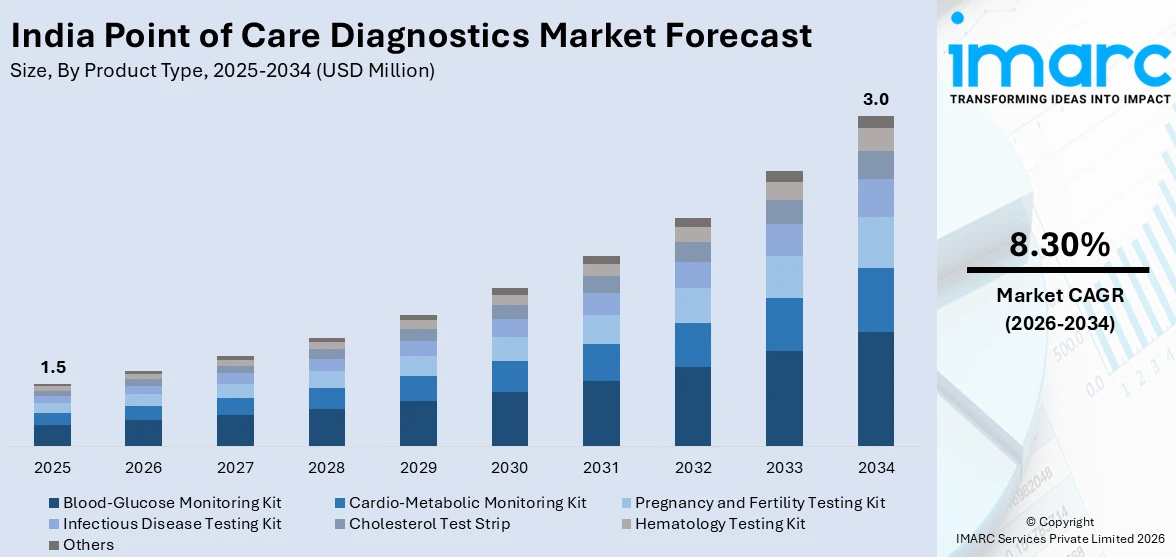

The India point of care diagnostics market size was valued at USD 1.5 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 3.0 Million by 2034, exhibiting a CAGR of 8.30% during 2026-2034. The increasing incidence of chronic diseases such as diabetes, cardiovascular diseases, and infectious diseases, coupled with the rising demand for rapid and efficient diagnostic solutions at the point of care, is contributing to the India point of care diagnostics market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034 |

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1.5 Million |

| Market Forecast in 2034 | USD 3.0 Million |

| Market Growth Rate 2026-2034 | 8.30% |

The India point of care diagnostics market is primarily driven by the growing demand for rapid and accessible diagnostic solutions, especially in remote and underserved regions. The increasing burden of infectious and chronic diseases, such as diabetes, tuberculosis, and cardiovascular disorders, has amplified the need for immediate diagnostic testing at or near the site of patient care. Rising healthcare awareness, government initiatives to strengthen rural health infrastructure, and the expansion of primary health centers are further supporting market growth. Additionally, technological advancements have enabled the development of portable, user-friendly, and cost-effective diagnostic devices that do not require sophisticated laboratory setups. The COVID-19 pandemic also accelerated adoption by highlighting the importance of decentralized and quick testing. Private sector investment and public-private partnerships continue to foster innovation and deployment across both urban and rural healthcare settings. These combined factors are actively driving India point of care diagnostics market growth.

To get more information on this market Request Sample

Mobile diagnostic programs are gaining momentum as a way to bring preventive health services directly to communities. By offering free screenings and consultations at local touchpoints, such initiatives are encouraging early detection, routine monitoring, and wider adoption of point-of-care diagnostics, particularly in urban residential clusters. For instance, in April 2025, Healthians launched its “Health on Wheels” initiative in Mumbai to improve access to diagnostics by offering free health screening camps in housing societies. Services include BP, BMI, ECG checks, and wellness consultations. The program aims to promote preventive care and regular health monitoring.

India Point of Care Diagnostics Market Trends:

Surge in Demand for Rapid Infectious Disease Detection

The growing burden of infectious diseases in India is pushing healthcare systems toward faster and more accessible diagnostic solutions. Rising case numbers have heightened the need for real-time detection at the patient site. As outbreaks continue to strain centralized lab capacities, portable and immediate testing devices are gaining preference. These tools are enabling quicker clinical decisions, especially in resource-limited or high-incidence areas. Public health authorities and private providers are increasingly prioritizing decentralized testing models to contain infections early and reduce transmission. This shift is contributing to a broader change in how diagnostics are accessed and delivered across urban and rural healthcare settings. The rising prevalence of infectious diseases, as reported by the WHO, with 151 Zika virus disease cases across Gujarat, Karnataka, and Maharashtra in 2025, has spurred the demand for rapid, on-the-spot diagnostic solutions.

Government Push Boosting On-the-Spot Diagnostic Development

Based on the India point of care diagnostics market outlook, supportive policy initiatives and investments in biotechnology are strengthening the foundation for rapid diagnostic solutions in India. With increased attention to building a self-reliant healthcare system, authorities are promoting homegrown innovations in medical diagnostics. This push is helping scale local manufacturing, improve accessibility, and reduce dependence on centralized lab infrastructure. As part of a broader focus on bio-based industries, efforts are being made to integrate portable diagnostic tools into mainstream healthcare delivery. These developments are enhancing the reach of timely disease detection, especially in underserved areas. By aligning national goals with healthcare innovation, the sector is witnessing faster adoption of point-of-care diagnostics tailored to the needs of diverse Indian populations. The Indian government has also supported this momentum, with the Ministry of Science & Technology noting a remarkable growth in India’s bioeconomy from USD 10 Billion in 2014 to nearly USD 130 Billion in 2025, with a target of USD 300 Billion in the near future.

Rising Public Health Spending Enhancing Diagnostic Accessibility

The India point of care diagnostics market forecast indicates that the steady rise in public healthcare funding is reinforcing India’s shift toward accessible diagnostic solutions. With increased allocations directed toward strengthening infrastructure and services, there is growing emphasis on early detection and decentralized testing. More financial support enables wider integration of portable diagnostic tools across government-run facilities and outreach programs. This is especially significant for rural and semi-urban areas, where access to centralized labs remains limited. The broader budgetary focus on preventive care and primary health services is driving the adoption of rapid, point-of-care testing devices. These developments reflect a clear move toward strengthening healthcare delivery models that prioritize timely diagnosis, quicker treatment initiation, and improved patient outcomes across diverse population segments. For example, the government allocated approximately INR 95,957.87 Crore to the healthcare sector for FY26, marking a 9.46% increase from the FY25 budget, as per the Observer Research Foundation.

India Point of Care Diagnostics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the India point of care diagnostics market, along with forecasts at the regional levels from 2026-2034. The market has been categorized based on product type, platform, prescription mode, and end user.

Analysis by Product Type:

- Blood-Glucose Monitoring Kit

- Cardio-Metabolic Monitoring Kit

- Pregnancy and Fertility Testing Kit

- Infectious Disease Testing Kit

- Cholesterol Test Strip

- Hematology Testing Kit

- Others

Blood-glucose monitoring kits are propelling the growth of the Indian point-of-care diagnostics market, supported by the country’s expanding diabetic population and rising demand for home-based, real-time testing solutions. Their affordability, portability, and user-friendliness make them particularly effective in reaching semi-urban and rural regions. At the same time, cardio-metabolic monitoring kits are gaining prominence as cardiovascular and metabolic conditions become increasingly common. These kits allow for quick evaluation of lipid profiles and cardiac markers, supporting early diagnosis and timely intervention. Their widespread use in outpatient services, health camps, and emergency settings reflects India’s growing emphasis on preventive and decentralized healthcare access.

Analysis by Platform:

- Lateral Flow Assays

- Dipsticks

- Microfluidics

- Molecular Diagnostics

- Immunoassays

Lateral flow assays are boosting the Indian point-of-care diagnostics market due to their rapid, low-cost, and easy-to-use format, making them ideal for widespread screening in both urban clinics and rural outreach programs. They are extensively used for detecting infectious diseases, pregnancy, and COVID-19-related testing, offering immediate results without the need for complex infrastructure. Similarly, dipsticks are gaining momentum for their role in routine urine analysis and basic diagnostics, especially in primary healthcare settings. Their affordability, minimal training requirement, and fast turnaround make them suitable for mass deployment. Together, these formats are expanding diagnostic reach, enabling timely detection and treatment, and supporting India's push toward accessible, frontline healthcare services across diverse population segments.

Analysis by Prescription Mode:

- Prescription-based Testing

- OTC Testing

Prescription-based testing is advancing the Indian point-of-care diagnostics market as physicians increasingly rely on rapid test results to guide immediate clinical decisions, especially in outpatient departments, emergency rooms, and rural clinics. These tests support faster diagnosis and treatment initiation, improving patient outcomes and reducing the burden on centralized labs. At the same time, OTC testing is gaining popularity due to growing consumer awareness, demand for self-monitoring, and availability of easy-to-use kits for conditions like diabetes, pregnancy, and infectious diseases. The rise of e-pharmacies and retail health channels has further improved accessibility. Together, these segments are expanding the market by addressing both clinical and consumer-driven diagnostic needs across India’s diverse healthcare landscape.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

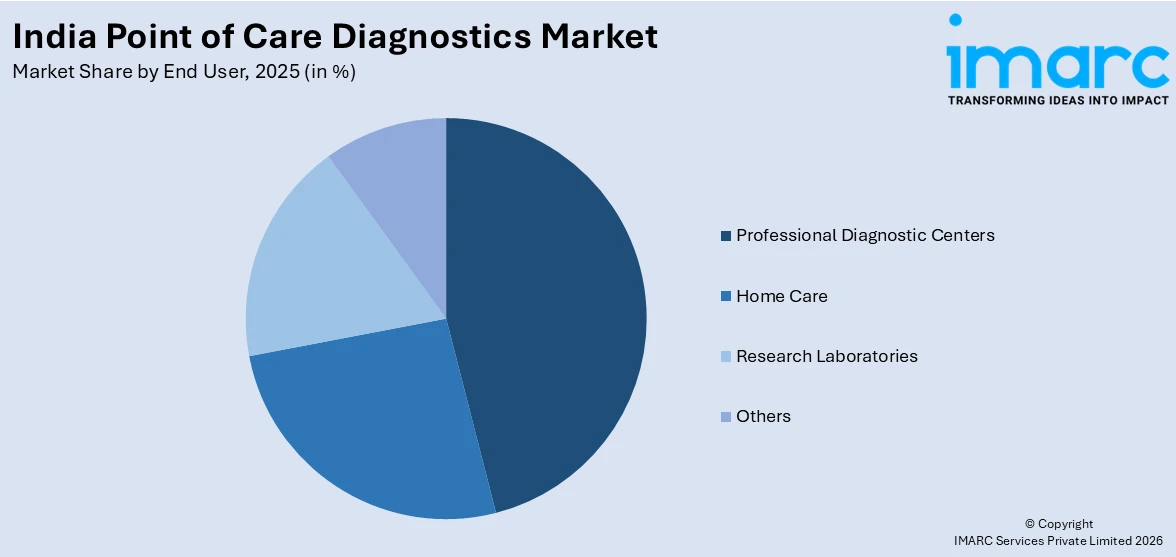

- Professional Diagnostic Centers

- Home Care

- Research Laboratories

- Others

Professional diagnostic centers are accelerating the growth of India’s point-of-care diagnostics market by integrating rapid testing solutions to deliver quick and accurate results, catering to the rising demand for same-day diagnostics. These centers are increasingly adopting point-of-care technologies to manage high patient volumes efficiently, especially in urban and semi-urban regions. Simultaneously, the home care segment is expanding due to increasing consumer preference for convenience, safety, and real-time monitoring. The rise in chronic diseases, elderly population, and telehealth services is encouraging the use of portable diagnostic kits for home use. Combined, both segments are enhancing the accessibility and responsiveness of healthcare delivery, driving demand for compact, user-friendly, and reliable point-of-care testing devices across the country.

Regional Analysis:

- North India

- West and Central India

- South India

- East and Northeast India

North India is contributing significantly to the growth of the point-of-care diagnostics market due to its dense population, rising burden of chronic and infectious diseases, and expanding network of public and private healthcare providers. States like Delhi, Uttar Pradesh, and Punjab are witnessing increased deployment of rapid testing kits in both urban hospitals and rural health centers. Meanwhile, West and Central India, including Maharashtra, Gujarat, and Madhya Pradesh, are experiencing strong uptake driven by government health initiatives, growing awareness, and rising investments in diagnostic infrastructure. These regions are also benefiting from the presence of leading diagnostic companies and innovation hubs. Together, North and West-Central India are shaping market expansion through high demand, infrastructural readiness, and targeted healthcare outreach.

Competitive Landscape:

The point of care diagnostics market in India is currently witnessing strong momentum across multiple fronts. Companies are actively engaging in product development and launching new testing solutions tailored for rapid, decentralized use. Strategic collaborations, partnerships, and licensing agreements are widespread, helping to scale distribution and integrate advanced technologies. Government support through healthcare initiatives and public-private partnerships is fostering accessibility and innovation. Research and development remain robust, with emphasis on affordability, portability, and accuracy. Among all activities, collaborations and government-led programs have emerged as the most common practices, reflecting a collective push to improve diagnostic reach and efficiency across urban and rural areas.

The report provides a comprehensive analysis of the competitive landscape in the India point of care diagnostics market with detailed profiles of all major companies.

Latest News and Developments:

- April 2025: Ambrosia launched a 24x7 real-time glucose (A-CGM) and stress monitoring service. Integrating wearable sensors, AI analytics, and remote monitoring, the service provides continuous health insights and aims to address India’s diabetes and stress burden, offering flexible rental plans and enhancing preventive care accessibility nationwide.

- April 2025: South Korea's E-Fiber Group announced that it is establishing an INR 209 Crore manufacturing unit in Ujjain's Medical Device Park to produce affordable cancer diagnosis kits. The facility will manufacture 5 million in-vitro diagnostic (IVD) kits and 10 million related products monthly. Utilizing urine samples and incorporating advanced nano-fiber and cellulose-based biopolymers, these kits aim to simplify early cancer detection.

- April 2025: T&D Diagnostics began manufacturing its Starkwert FIA diagnostic kits in India through a partnership with Noida-based Genenest. The initiative aims to boost global supply chain resilience, tap Asian markets, and establish India as a cost-effective biotech manufacturing and export hub.

- March 2025: HaystackAnalytics launched the ‘TB One’ solution at ICMR’s India Innovation Summit. This pre-sequencing kit enables genomic TB testing via Next-Generation Sequencing, offering resistance profiling for 18 drugs.

India Point of Care Diagnostics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Blood-Glucose Monitoring Kit, Cardio-Metabolic Monitoring Kit, Pregnancy and Fertility Testing Kit, Infectious Disease Testing Kit, Cholesterol Test Strip, Hematology Testing Kit, Others |

| Platforms Covered | Lateral Flow Assays, Dipsticks, Microfluidics, Molecular Diagnostics, Immunoassays |

| Prescription Modes Covered | Prescription-based Testing, OTC Testing |

| End Users Covered | Professional Diagnostic Centers, Home Care, Research Laboratories, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India point of care diagnostics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India point of care diagnostics market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India point of care diagnostics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Point of Care Diagnostics Market Report

The point of care diagnostics market in India was valued at USD 1.5 Million in 2025.

The India point of care diagnostics market is projected to exhibit a CAGR of 8.30% during 2026-2034, reaching a value of USD 3.0 Million by 2034.

Key factors driving the India point of care diagnostics market include rising demand for rapid diagnostic testing, increasing prevalence of chronic and infectious diseases, growing rural healthcare needs, government initiatives for decentralized healthcare, and technological advancements enabling portable, easy-to-use diagnostic tools suitable for resource-limited settings.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade