India Polyester Fabrics Market Size, Share, Trends and Forecast by Type, Fabric Structure, Application, End Use Industry, and Region, 2026-2034

India Polyester Fabrics Market Overview:

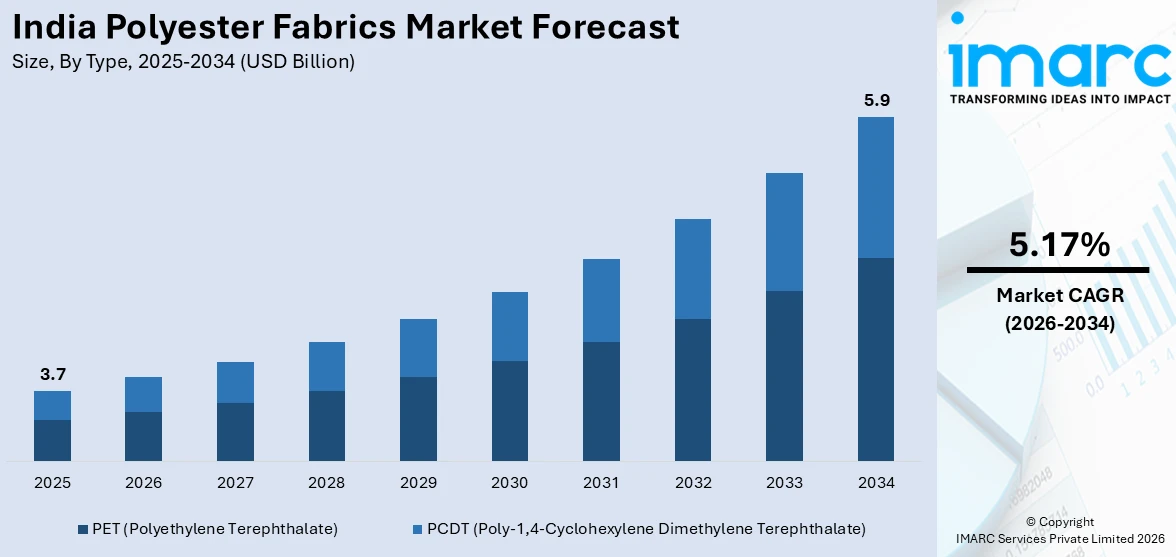

The India polyester fabrics market size reached USD 3.7 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 5.9 Billion by 2034, exhibiting a growth rate (CAGR) of 5.17% during 2026-2034. Expansion in apparel and home textile manufacturing, policy-driven synthetic fiber incentives, and integration into export supply chains, along with abundant raw material feedstock, advanced spinning systems, and sustainable dyeing technologies, are some of the factors positively impacting the market. Digital printing adoption, automated fabric inspection, and custom development capabilities are additional factors augmenting the India polyester fabrics market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3.7 Billion |

| Market Forecast in 2034 | USD 5.9 Billion |

| Market Growth Rate 2026-2034 | 5.17% |

India Polyester Fabrics Market Trends:

Expanding Apparel and Home Textile Manufacturing Base

India’s textile industry is undergoing vertical integration, with polyester fabrics playing a central role in value-added apparel and home furnishing production. As global fashion retailers increase their sourcing from Indian manufacturers, demand for synthetic blends is rising across shirts, sportswear, ethnic wear, curtains, upholstery, and bed linens. On June 7, 2024, the textile industry in India welcomed the relaxation of the mandatory Quality Control Order (QCO) for polyester fiber, filament yarn, and spun yarn. The QCO, which was originally issued in April 2021, required all users to source these products only from BIS license holders, but the relaxation now applies to imports under the advance authorization scheme, export-oriented units, and spsecial economic zones. This move is expected to benefit the textile sector by easing access to necessary materials while supporting growth and efficiency in the industry. Polyester’s affordability, wrinkle resistance, and high tensile strength make it an essential input for mass-market and export-oriented textile production. Large-scale apparel hubs such as Tiruppur, Ludhiana, and Surat are investing in automated weaving, dyeing, and finishing lines dedicated to synthetic fabrics. The government’s Production Linked Incentive (PLI) scheme for man-made fibers is further accelerating domestic capacity expansion, enabling backward integration in polyester yarn and fabric manufacturing. In addition, technical textile applications, including filtration, geotextiles, and industrial threads are generating complementary demand. With foreign brands establishing local supply chains and Indian exporters diversifying their product portfolios, fabric producers are optimizing quality, cost, and lead times to stay competitive, thereby contributing to the India polyester fabrics market growth.

To get more information on this market Request Sample

Availability of Raw Material Feedstock and Technological Advancements

The ready availability of PTA (Purified Terephthalic Acid) and MEG (Monoethylene Glycol), critical raw materials for polyester production, has enhanced India’s self-reliance in synthetic textile inputs. Major petrochemical companies such as Reliance Industries and Indian Oil Corporation continue to expand upstream capacities, ensuring cost-effective and uninterrupted feedstock supply. This domestic availability minimizes exposure to global price volatility and reduces dependency on imported raw materials, strengthening the competitiveness of downstream fabric producers. Simultaneously, innovations in filament spinning, air-jet texturizing, and dye-sublimation printing are improving the functionality and visual appeal of polyester fabrics. Mills are increasingly adopting waterless dyeing technologies, automated inspection systems, and energy-efficient looms to meet sustainability benchmarks and reduce processing costs. As per recent industry reports, India’s polyester market continues to expand, with an estimated annual consumption of 6 million tons of polyester, of which 50% is imported. The market is projected to reach USD 35 Billion by 2026, driven by demand from key sectors such as textiles, automotive, and packaging. Moreover, digital design software enabling custom fabric development for small-batch orders and quick-turn retail cycles are contributing to a positive market outlook. These operational upgrades are enhancing responsiveness to dynamic fashion trends while maintaining scalable output, positioning polyester as a high-performance fabric in both lifestyle and industrial segments.

India Polyester Fabrics Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on type, fabric structure, application, and end use industry.

Type Insights:

- PET (Polyethylene Terephthalate)

- PCDT (Poly-1,4-Cyclohexylene Dimethylene Terephthalate)

The report has provided a detailed breakup and analysis of the market based on the type. This includes PET (Polyethylene Terephthalate) and PCDT (Poly-1,4-Cyclohexylene Dimethylene Terephthalate).

Fabric Structure Insights:

- Woven Polyester Fabrics

- Non-woven Polyester Fabrics

- Knitted Polyester Fabrics

The report has provided a detailed breakup and analysis of the market based on the fabric structure. This includes woven polyester fabrics, non-woven polyester fabrics, and knitted polyester fabrics.

Application Insights:

- Apparel

- Sportswear

- Casual Wear

- Workwear

- Home Textiles

- Upholstery

- Curtains

- Bedding

- Industrial Applications

- Automotive Fabrics

- Medical Textiles

- Geotextiles

The report has provided a detailed breakup and analysis of the market based on the application. This includes apparel, sportswear, casual wear, workwear, home textiles, upholstery, curtains, bedding, industrial applications, automotive fabrics, medical textiles, and geotextiles.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

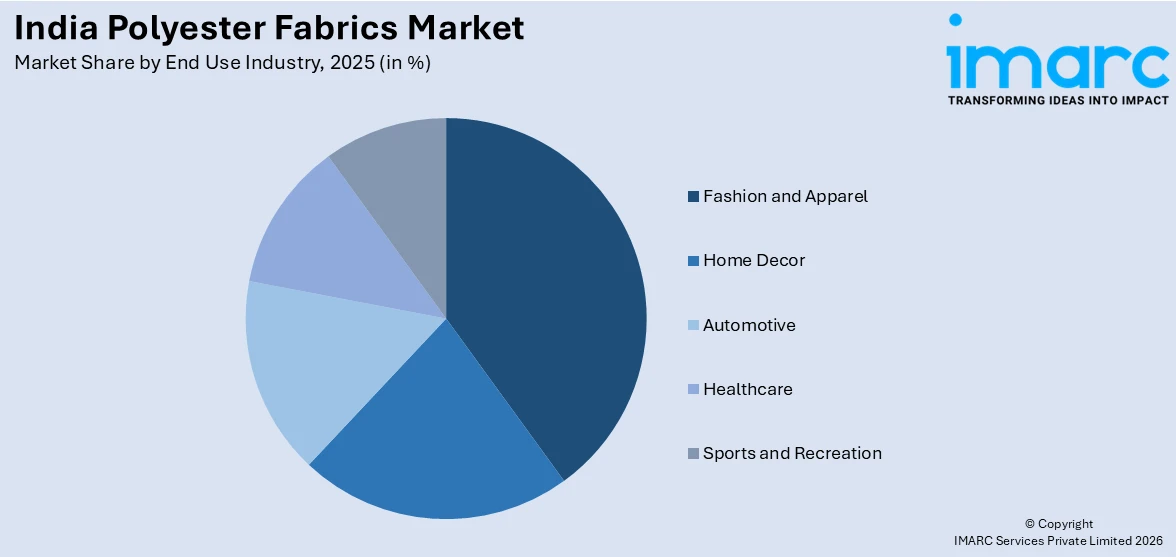

- Fashion and Apparel

- Home Decor

- Automotive

- Healthcare

- Sports and Recreation

The report has provided a detailed breakup and analysis of the market based on the end use industry. This includes fashion and apparel, home decor, automotive, healthcare, and sports and recreation.

Regional Insights:

- North India

- South India

- East India

- West India

The report has provided a comprehensive analysis of all major regional markets, which include North India, South India, East India, and West India.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

India Polyester Fabrics Market News:

- On January 20, 2025, Indian giant, Reliance Industries Limited, showcased its sustainable polyester technology, Recron®, at Heimtextil 2025 in Frankfurt, Germany, receiving a strong response from the global textile industry. The presentation of HEXaREL™ Fiberfill and Ecotherm™ textile products garnered significant interest from textile firms, winter product manufacturers, and end users, highlighting the growing demand for high-performance, sustainable fibers. The positive reception underscores the market's shift towards sustainable solutions, with increased business inquiries and potential partnerships spurred by the performance and cost-effectiveness of these innovative materials.

India Polyester Fabrics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | PET (Polyethylene Terephthalate), PCDT (Poly-1,4-Cyclohexylene Dimethylene Terephthalate) |

| Fabric Structures Covered | Woven Polyester Fabrics, Non-woven Polyester Fabrics, Knitted Polyester Fabrics |

| Applications Covered | Apparel, Sportswear, Casual Wear, Workwear, Home Textiles, Upholstery, Curtains, Bedding, Industrial Applications, Automotive Fabrics, Medical Textiles, Geotextiles |

| End Use Industries Covered | Fashion and Apparel, Home Decor, Automotive, Healthcare, Sports and Recreation |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India polyester fabrics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India polyester fabrics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India polyester fabrics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Polyester Fabrics Market Report

The polyester fabrics market in India was valued at USD 3.7 Billion in 2025.

The India polyester fabrics market is projected to exhibit a CAGR of 5.17% during 2026-2034, reaching a value of USD 5.9 Billion by 2034.

The India polyester fabrics market is driven by growing demand for versatile, durable, and cost-effective textiles across fashion, home décor, and industrial applications. Rising popularity of modern apparel trends, increasing use in technical and functional fabrics, and innovations in sustainable and high-performance polyester materials further contribute to the market’s expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)