India Polyester Staple Fiber Market Size, Share, Trends and Forecast by Origin, Product, Application, and Region, 2026-2034

India Polyester Staple Fiber Market Summary:

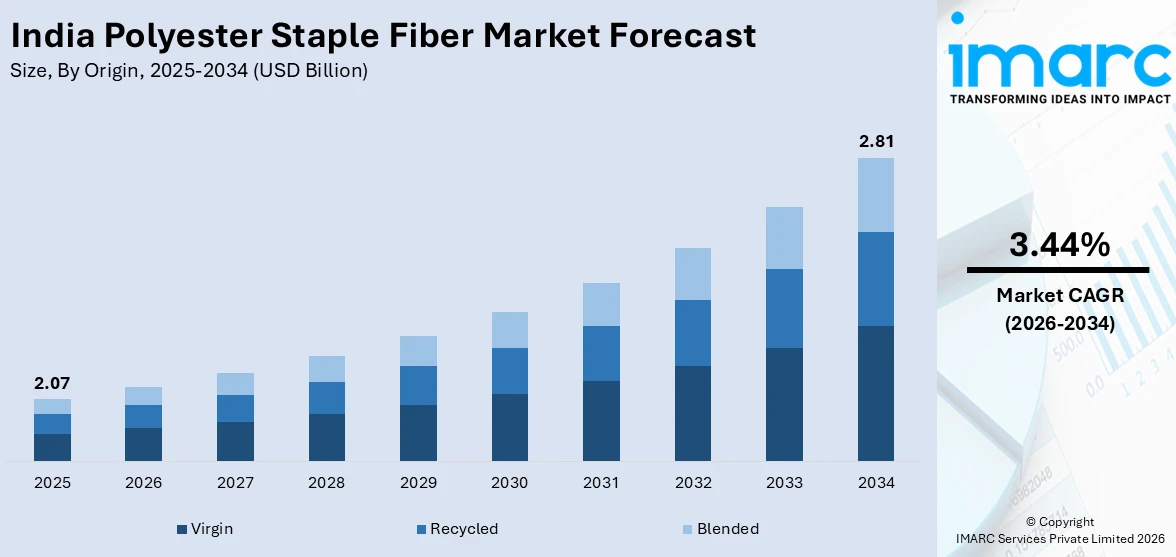

The India polyester staple fiber market size was valued at USD 2.07 Billion in 2025 and is projected to reach USD 2.81 Billion by 2034, growing at a compound annual growth rate of 3.44% from 2026-2034.

The India polyester staple fiber market is expanding steadily, underpinned by robust domestic textile manufacturing, rising consumer demand for affordable synthetic fabrics, and increasing industrial applications. Government initiatives promoting man-made fiber production and integrated textile ecosystems are further accelerating growth. Advancements in fiber processing technologies, expanding non-woven applications, and growing emphasis on sustainability through recycled polyester are reinforcing the long-term demand trajectory, strengthening the India polyester staple fiber market share.

Key Takeaways and Insights:

- By Origin: Virgin dominates the market with a share of 50% in 2025, driven by its consistent quality, uniform composition, and widespread preference across large-scale textile manufacturing and industrial applications.

- By Product: Solid leads the market with a share of 57% in 2025, owing to its superior tensile strength, abrasion resistance, and versatile suitability for spinning, blending, and non-woven fabric production.

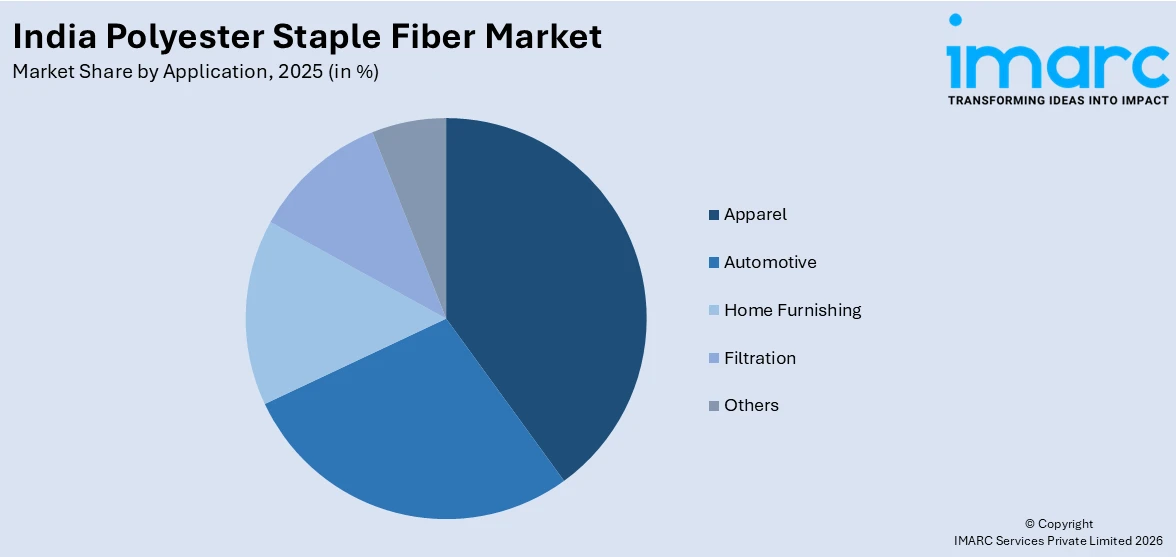

- By Application: Apparel represents the largest segment with a market share of 33% in 2025, reflecting strong consumer preference for cost-effective, durable, and easy-care polyester-blended garments across casual, formal, and activewear categories.

- Key Players: The India polyester staple fiber market features a moderately consolidated competitive landscape, with established domestic manufacturers and global integrated producers competing through capacity expansions, product diversification, sustainability-focused innovations, and strategic partnerships to capture growing demand across textile, automotive, and industrial applications.

To get more information on this market Request Sample

The India polyester staple fiber market is positioned as a critical pillar of the country's broader textile and synthetic fiber ecosystem. India ranks as the world's third-largest exporter of textiles and apparel, with polyester staple fiber serving as a foundational raw material across multiple downstream industries. The market benefits from an extensive and vertically integrated manufacturing base, particularly concentrated in clusters such as Surat in Gujarat, which accounts for approximately 60% of India's polyester cloth production. Growing urbanization, rising disposable incomes, and expanding middle-class consumption are accelerating demand for affordable polyester-based textiles. Government-led initiatives are playing a significant role in transforming the manufacturing ecosystem. Policy measures aimed at promoting domestic production of man-made fiber apparel, fabrics, and technical textiles are encouraging fresh investments and strengthening industrial capacity. Such structural support, combined with a favorable regulatory environment, is fostering long-term industry development and reinforcing steady growth across diverse application segments.

India Polyester Staple Fiber Market Trends:

Growing Adoption of Recycled Polyester Staple Fiber

Sustainability imperatives are driving a notable shift toward recycled polyester staple fiber production in India. Manufacturers are increasingly investing in technologies that convert post-consumer PET bottles and textile waste into high-quality recycled fibers, aligning with global brand commitments for higher recycled content in products. This transition is supported by India's expanding PET collection infrastructure and rising environmental awareness among consumers. Notably, Filatex India's subsidiary Texfil is establishing a INR 300 crore chemical recycling facility at Dahej, Gujarat, with a capacity of 26,750 metric tonnes per annum, targeting commissioning by September 2026, which underscores the India polyester staple fiber market growth trajectory.

Expansion of Non-Woven and Technical Textile Applications

Polyester staple fiber is witnessing accelerated adoption in non-woven and technical textile segments across India, driven by rising demand from hygiene products, filtration systems, automotive interiors, and geotextile applications. The versatility of PSF in producing durable, lightweight, and cost-effective non-woven fabrics is opening new consumption channels beyond traditional apparel. The Indian government's National Technical Textiles Mission, with an outlay of INR 1,480 crore, is specifically fostering research, innovation, and capacity building in technical textiles, creating a favorable ecosystem for expanded PSF utilization in high-value industrial segments.

Integration of Advanced Fiber Processing Technologies

Indian polyester staple fiber manufacturers are increasingly adopting advanced processing technologies to enhance fiber properties such as strength, elasticity, moisture management, and colorfastness. Innovations in dope-dyeing, conjugate spinning, and melt-direct fiber lines are enabling the production of specialty-grade PSF for performance-oriented applications. Manufacturers are also investing in automation and quality control systems to meet stringent international specifications. In addition, companies are focusing on energy-efficient production processes and sustainable raw material integration to align with evolving environmental standards. These strategic upgrades are strengthening their competitiveness in both domestic and export markets while supporting long-term value creation.

Market Outlook 2026-2034:

The India polyester staple fiber market is poised for sustained growth over the forecast period, supported by expanding textile manufacturing capacity, increasing downstream applications, and favorable government policies promoting man-made fiber production. The establishment of seven PM MITRA mega integrated textile parks across India, backed by a budgetary allocation of INR 4,445 crore, is expected to significantly enhance manufacturing scale, reduce logistics costs, and attract fresh domestic and foreign investments into the polyester value chain. The market generated a revenue of USD 2.07 Billion in 2025 and is projected to reach a revenue of USD 2.81 Billion by 2034, growing at a compound annual growth rate of 3.44% from 2026-2034.

India Polyester Staple Fiber Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Origin |

Virgin |

50% |

|

Product |

Solid |

57% |

|

Application |

Apparel |

33% |

Origin Insights:

- Virgin

- Recycled

- Blended

Virgin dominates with a market share of 50% of the total India polyester staple fiber market in 2025.

Virgin polyester staple fiber maintains its leadership position in the Indian market owing to its superior quality, consistency, reliable chemical composition, and broad applicability across diverse manufacturing requirements. Produced directly from purified terephthalic acid and monoethylene glycol, virgin PSF offers uniform fiber properties that are essential for high-volume textile production. India's well-established integrated PTA-to-fiber production chains, particularly concentrated in Gujarat and Maharashtra, provide significant cost advantages for virgin fiber manufacturing, ensuring competitive pricing for domestic spinners and weavers.

The segment continues to witness solid demand from apparel, home furnishings, and industrial textile applications, where stringent performance requirements necessitate consistent and high-quality fiber inputs. Although recycled polyester is steadily expanding its presence, many large textile producers still rely on virgin PSF for applications that demand superior durability, uniformity, and processing stability. Leading manufacturers are therefore focusing on strengthening domestic production capabilities and enhancing supply reliability, reflecting sustained confidence in the long-term relevance of virgin polyester within India’s evolving textile ecosystem.

Product Insights:

- Solid

- Hollow

Solid leads the market with a share of 57% of the total India polyester staple fiber market in 2025.

Solid polyester staple fiber holds the dominant position in the Indian market due to its versatile applicability across spinning, weaving, and non-woven fabric production. Characterized by its uniform composition and dense structural profile, solid PSF delivers excellent tensile strength, abrasion resistance, and dimensional stability, making it the preferred fiber for blending with cotton, viscose, and other natural fibers in fabric manufacturing. Its cost-effectiveness and ease of processing further reinforce its widespread adoption across the country's textile value chain.

The segment continues to gain momentum from robust demand in the apparel and home furnishing industries, where solid PSF-based fabrics are preferred for their crease resistance, long-lasting color, and durability. Major textile hubs across India depend significantly on solid PSF as a key raw material supporting large-scale fabric production. Furthermore, rising adoption of nonwoven materials in hygiene products, filtration systems, and geotextile applications is broadening the end-use landscape, thereby reinforcing steady consumption of solid polyester staple fiber throughout the country.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Automotive

- Home Furnishing

- Apparel

- Filtration

- Others

The apparel segment holds the largest share at 33% of the total India polyester staple fiber market in 2025.

The apparel segment commands the leading position in India's polyester staple fiber market, driven by the country's massive garment manufacturing capacity and rising domestic consumption of affordable, durable clothing. Polyester staple fiber offers inherent advantages for apparel production, including wrinkle resistance, color fastness, moisture-wicking properties, and ease of blending with natural fibers like cotton. The growing popularity of athleisure, sportswear, and fast fashion categories has further amplified demand for PSF-based fabrics across the Indian apparel value chain.

Numerous companies have been selected under the scheme, collectively committing substantial investments and generating strong revenue performance. The initiative has attracted broad industry participation, reflecting growing business confidence and reinforcing the program’s role in strengthening domestic manufacturing capabilities and overall sectoral growth. As of September 2025, 91 companies had been selected under the scheme, with combined investments of INR 7,731 crore and reported turnover of INR 7,290 crore, demonstrating the scheme's effectiveness in stimulating PSF-intensive manufacturing activity.

Regional Insights:

- North India

- South India

- East India

- West India

North India serves as a significant consumption center for polyester staple fiber, supported by a dense network of spinning mills and textile manufacturing units concentrated in states such as Punjab, Haryana, and Uttar Pradesh. The region benefits from proximity to major domestic markets and established logistics infrastructure facilitating raw material supply and finished goods distribution.

South India contributes meaningfully to the PSF market through its established textile manufacturing ecosystem in Tamil Nadu, Telangana, and Karnataka, with strong presence in apparel exports and technical textiles production.

East India represents a growing market for polyester staple fiber consumption, with expanding textile manufacturing activity and increasing government focus on industrial development in states such as West Bengal and Odisha.

Western India leads the regional market, supported by Gujarat’s well-established polyester manufacturing hubs. Surat serves as a key center for polyester fabric production, while Maharashtra contributes substantial manufacturing and processing capabilities, further strengthening the region’s consumption base for polyester staple fiber.

Market Dynamics:

Growth Drivers:

Why is the India Polyester Staple Fiber Market Growing?

Supportive Government Policies and Industrial Incentive Programs

The Indian government has implemented a comprehensive policy framework aimed at strengthening domestic man-made fiber manufacturing and boosting the textile sector's global competitiveness. The Production Linked Incentive scheme for textiles, with a budgetary outlay of INR 10,683 crore, is specifically targeting man-made fiber apparel, fabrics, and technical textile production. The existence of these incentives is motivating current manufacturers to seek investments in capacity building and modernization. Moreover, the PM MITRA program is also enabling the emergence of integrative textile parks in various states to consolidate the manufacturing ecosystem of the country. These parks are meant to concentrate the whole textile value chain in one place, making it more efficient, accessible to infrastructure, and integrating the supply chain. This is the polyester staple fiber market that is growing in the long run due to such policy-based measures that promote a favorable industrial environment, stimulate new investments and capacity building, and eventually enhance the growth of such a market.

Expanding Textile and Apparel Manufacturing Ecosystem

India's textile and apparel sector continues to expand rapidly, driven by rising domestic consumption, growing export opportunities, and an increasingly competitive manufacturing base. The country produces approximately 1,700 million kilograms of man-made fibers and 3,400 million kilograms of man-made filaments annually, reflecting a well-established production infrastructure. India's textile industry attracted investment commitments exceeding INR 60,000 crore in 2025, with significant contributions from both domestic and foreign investors across fibers, fabrics, apparel, and technical textiles. The expanding ecosystem of spinning mills, weaving units, processing facilities, and garment manufacturers directly translates into growing demand for polyester staple fiber as a foundational raw material, supporting sustained market expansion.

Rising Demand from Automotive and Industrial Applications

The automotive and industrial industries are becoming significant sources of demand for polyester staple fiber in India. PSF finds large applications in automotive fabrics such as seating fabrics, carpet backing, door panels, trunk liners, airbag parts, safety belts, and acoustical insulation fabrics. There is a strong and well-established manufacturing base of man-made fibers and filaments in the country, whose production infrastructure and integrated supply networks support it. This good industrial base allows uniform production, productivity, and flexibility to meet the domestic and export needs in the various textile uses. Beyond automotive, the growing adoption of PSF in construction applications for concrete reinforcement, geotextiles, and insulation materials, as well as in filtration systems and personal care products, is diversifying the demand base and strengthening overall market growth prospects.

Market Restraints:

What Challenges the India Polyester Staple Fiber Market is Facing?

Volatility in Raw Material Prices

Polyester staple fiber production is heavily dependent on petroleum-derived feedstocks, primarily purified terephthalic acid and monoethylene glycol. Fluctuations in crude oil prices and global petrochemical market dynamics directly impact raw material costs, creating uncertainty in production planning and profit margins for manufacturers. This price volatility can disrupt supply chain stability and limit the ability of producers to maintain competitive pricing for downstream customers.

Competition from Natural Fibers and Alternative Synthetics

Polyester staple fiber faces ongoing competition from cotton, viscose, and other natural and regenerated fibers, particularly in markets where consumer preference for natural-origin textiles is growing. Additionally, alternative synthetic fibers such as nylon and polypropylene compete in specific application segments. Government programs supporting cotton cultivation and processing can also redirect manufacturing focus away from synthetic fibers, constraining PSF market penetration in certain textile categories.

Environmental and Regulatory Pressures

Increasing environmental scrutiny around synthetic fiber production, microplastic pollution, and textile waste management is creating regulatory and reputational challenges for the polyester staple fiber industry. Manufacturers face rising compliance costs related to wastewater treatment, emissions control, and waste management standards. Evolving international regulations, particularly concerning microplastic shedding from synthetic textiles, may necessitate additional investments in product development and manufacturing processes to meet stricter environmental benchmarks.

Competitive Landscape:

The India polyester staple fiber market exhibits a moderately consolidated competitive structure, characterized by the presence of large-scale integrated manufacturers alongside mid-sized regional producers. Key market participants compete on the basis of production capacity, product quality, cost efficiency, sustainability credentials, and downstream integration capabilities. Companies are actively pursuing capacity expansions, technological upgrades, and investments in recycled polyester production to strengthen their market positions. Strategic acquisitions, backward integration into raw material production, and forward integration into yarn and fabric manufacturing are commonly observed strategies. The competitive landscape is further shaped by government incentive programs that are attracting new investments and encouraging both domestic and international players to expand their manufacturing footprint across India's polyester value chain.

Recent Developments:

- In December 2025, Texfil Private Limited, a subsidiary of Filatex India Limited, signed a Memorandum of Understanding with Decathlon Sports India to collaborate on the use of high-quality recycled polyester in sports apparel. The partnership focuses on integrating Ecosis™ recycled polyester chips and yarn produced through Texfil's patented textile-to-textile chemical recycling technology into Decathlon's manufacturing ecosystem.

- In October 2025, the Indian government announced major amendments to the PLI scheme for textiles, reducing the minimum investment threshold from INR 300 crore to INR 150 crore under Part 1 and from INR 100 crore to INR 50 crore under Part 2, while relaxing incremental turnover criteria from 25% to 10% to encourage wider participation from man-made fiber and technical textile manufacturers.

India Polyester Staple Fiber Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Origins Covered | Virgin, Recycled, Blended |

| Products Covered | Solid and Hollow |

| Applications Covered | Automotive, Home Furnishing, Apparel, Filtration, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Polyester Staple Fiber Market Report

The India polyester staple fiber market size was valued at USD 2.07 Billion in 2025.

The India polyester staple fiber market is expected to grow at a compound annual growth rate of 3.44% from 2026-2034 to reach USD 2.81 Billion by 2034.

Virgin polyester staple fiber, holding the largest share of 50% in 2025, remains the dominant origin segment owing to its consistent quality, uniform composition, and widespread preference across large-scale textile and industrial manufacturing applications in India.

Key factors driving the India polyester staple fiber market include supportive government incentive programs, expanding textile manufacturing capacity, rising demand from automotive and industrial applications, growing non-woven and technical textile consumption, and increasing investments in recycled polyester production.

Major challenges include volatility in petroleum-derived raw material prices, competition from natural fibers and alternative synthetics, increasing environmental and regulatory pressures around microplastic pollution, rising compliance costs, and supply chain disruptions affecting feedstock availability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)