India Pre-Engineered Buildings Market Size, Share, Trends and Forecast by Product, End-User, and Region, 2026-2034

India Pre-Engineered Buildings Market Size, Share, Trends & Forecast (2026-2034)

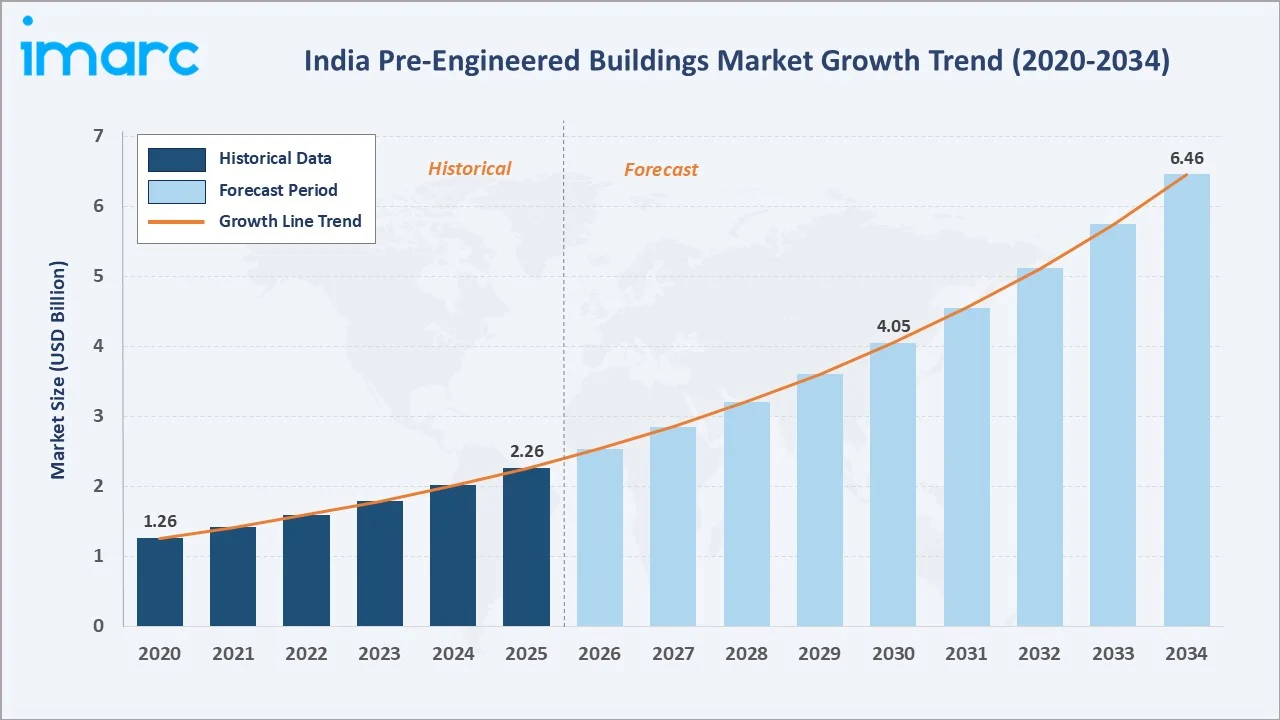

The India pre-engineered buildings (PEB) market reached USD 2.26 Billion in 2025 and is projected to reach USD 6.46 Billion by 2034, growing at a CAGR of 12.38% during 2026-2034. The market is driven by the growing demand for cost-effective, sustainable construction solutions, rapid urbanization, and the expansion of sectors like industrial, commercial, and infrastructure development. India’s ₹11,11,111 crore allocated for capital expenditure in the 2024-25 budget is driving the India pre-engineered buildings market by boosting infrastructure and industrial development, leading to higher demand for efficient and cost-effective construction solutions. Steel structure leads at 52.6% product share. The industrial sector commands 48.7% end-user share. West India leads regionally at 30.4%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.26 Billion |

|

Forecast Market Size (2034) |

USD 6.46 Billion |

|

CAGR (2026-2034) |

12.38% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

Steel Structure (52.6%, 2025) |

|

Largest End User |

Industrial Sector (48.7%, 2025) |

|

Leading Region |

West India (30.4%, 2025) |

The market expanded from USD 1.26 Billion in 2020 to USD 2.26 Billion in 2025, anchored at USD 4.05 Billion in 2030, and forecast to reach USD 6.46 Billion by 2034. PEB adoption in India accelerated as government-backed industrialization programs created unprecedented factory, warehouse, and infrastructure construction demand.

To get more information on this market, Request Sample

Steel structure grows at ~13.1% CAGR (2026-2034), driven by structural steel's inherent advantages in PEB applications. The industrial sector grows at ~13.5% CAGR as semiconductor, EV battery, pharmaceutical, and electronics manufacturing investment creates sustained factory PEB procurement.

Executive Summary

The India PEB market reached USD 2.26 Billion in 2025, positioning India as one of Asia's largest PEB markets and one of the world's fastest-growing PEB geographies by CAGR. Pre-engineered buildings are displacing conventional reinforced concrete construction across industrial, commercial, and infrastructure sectors where construction time, cost predictability, and structural performance converge as procurement criteria. The market is projected to reach USD 6.46 Billion by 2034 at 12.38% CAGR.

Steel structure at 52.6% leads the market as the defining PEB product type serving warehouses, factories, aircraft hangars, sports halls, and retail showrooms. The industrial sector at 48.7% is the primary demand driver through PLI scheme factory construction, e-commerce warehouse expansion, cold chain infrastructure, and automobile manufacturing plant greenfield and brownfield development. West India, at 30.4%, leads regionally through industrial estates.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Steel Structure - 52.6% share (2025) |

|

Largest End User |

Industrial Sector - 48.7% market share (2025) |

|

Leading Region |

West India - 30.4% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Steel structure at 52.6% anchored by clear-span large-span building requirements of industrial and warehouse sectors: India's PEB steel structure market is structurally anchored in industrial and warehouse applications where clear internal spans of 20-100 meters are required without intermediate columns.

- Industrial sector at 48.7%: India's Production Linked Incentive (PLI) scheme committed INR 1.97 Trillion. Currently, with 806 applications approved across 14 strategic sectors, it demonstrates strong industry confidence and widespread adoption.

- West India at 30.4% through industrial estate expansion: The Maharashtra Industrial Development Corporation (MIDC) has granted approvals for over 57,745 units, with 9,147 located in western Maharashtra, and 5,774 of them have restarted production, generating continuous PEB industrial building demand.

India Pre-Engineered Buildings Market Overview

India's pre-engineered buildings market encompasses all factory-manufactured, engineered building systems delivered as kit-form assemblies for rapid on-site erection, including hot-rolled steel primary structures (primary frames, rafters, columns), cold-formed secondary members (purlins, girts, eave struts), roof and wall cladding panels (pre-coated steel, insulated sandwich panels, polycarbonate skylights), mezzanine flooring systems, and structural accessories (doors, ventilators, downspouts).

The ecosystem integrates primary steel producers, PEB manufacturers/fabricators, structural engineering design teams, EPC contractors for site foundation and PEB erection, regulatory bodies, and end-user sectors spanning industrial, commercial, infrastructure, and residential. Macroeconomic factors include rapid industrialization, government infrastructure initiatives, urbanization, and a growing focus on cost-effective, sustainable construction solutions that reduce project timelines and costs.

Market Dynamics

To evaluate market opportunities, Request Sample

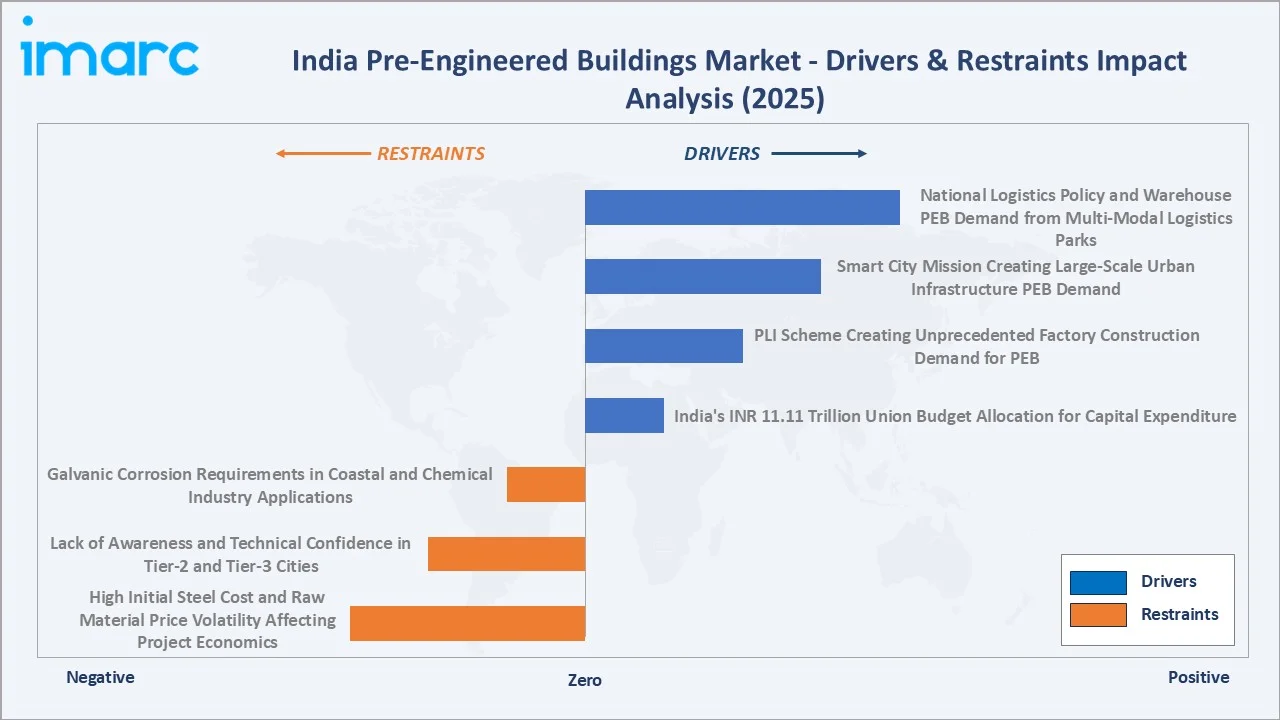

Market Drivers

- India's INR 11.11 Trillion Union Budget Allocation: Recognizing the significant economic impact of infrastructure development, Union Minister for Finance & Corporate Affairs, Smt. Nirmala Sitharaman, in Budget 2024-25, announced a provision of ₹11,11,111 crore for capital expenditure, which will account for 3.4% of the country's GDP and emphasized that the government aims to continue providing robust fiscal support for infrastructure over the next five years.

- PLI Scheme Creating PEB Demand: India's PLI scheme committed INR 1.97 Trillion across 14 key sectors. Each PLI-approved investment requires physical manufacturing space, driving unprecedented factory construction demand where PEB's faster construction timeline versus conventional RCC is commercially decisive given PLI's time-bound production targets.

- Smart City Mission: India's Smart City Mission is creating large-scale urban infrastructure PEB demand across multi-level parking structures, public market buildings, sports facilities, transit terminals, and solid waste management facilities.

Market Restraints

- High Initial Steel Cost and Raw Material Price Volatility Affecting Project Economics: India's domestic hot-rolled coil prices fluctuated, creating project cost variability between design-stage estimation and construction-stage material procurement.

- Lack of Awareness and Technical Confidence in Tier-2 and Tier-3 Cities: Despite PEB's India presence, awareness and technical confidence among developers, contractors, and local government agencies in Tier-2 and Tier-3 cities remain significantly lower than in major industrial hubs.

Market Opportunities

- National Logistics Policy and Warehouse PEB Demand from Multi-Modal Logistics Parks: India's National Logistics Policy targets reducing logistics cost by 2030, requiring high logistics infrastructure investment. This represents a structural warehouse PEB demand wave that will sustain industrial sector growth.

- India's Cold Chain Infrastructure Gap Creating Premium PEB Demand: India's cold chain capacity is critically undersupplied. The Government of India's cold chain development incentives and private investment from companies are creating premium cold chain PEB demand.

Market Challenges

- Galvanic Corrosion and Maintenance Requirements in Coastal and Chemical Industry Applications: Steel PEB structures in India's coastal industrial zones and chemical/pharmaceutical industrial estates face accelerated corrosion from marine salt air and chemical vapor exposure that requires enhanced corrosion protection systems, adding 8-15% to baseline PEB project costs.

- Regulatory Fragmentation Complicating National PEB Project Approvals: India's building plan approval system remains fragmented, with each having different structural safety certification requirements, fire NOC procedures, and occupancy certificate processes for steel buildings.

Emerging Market Trends

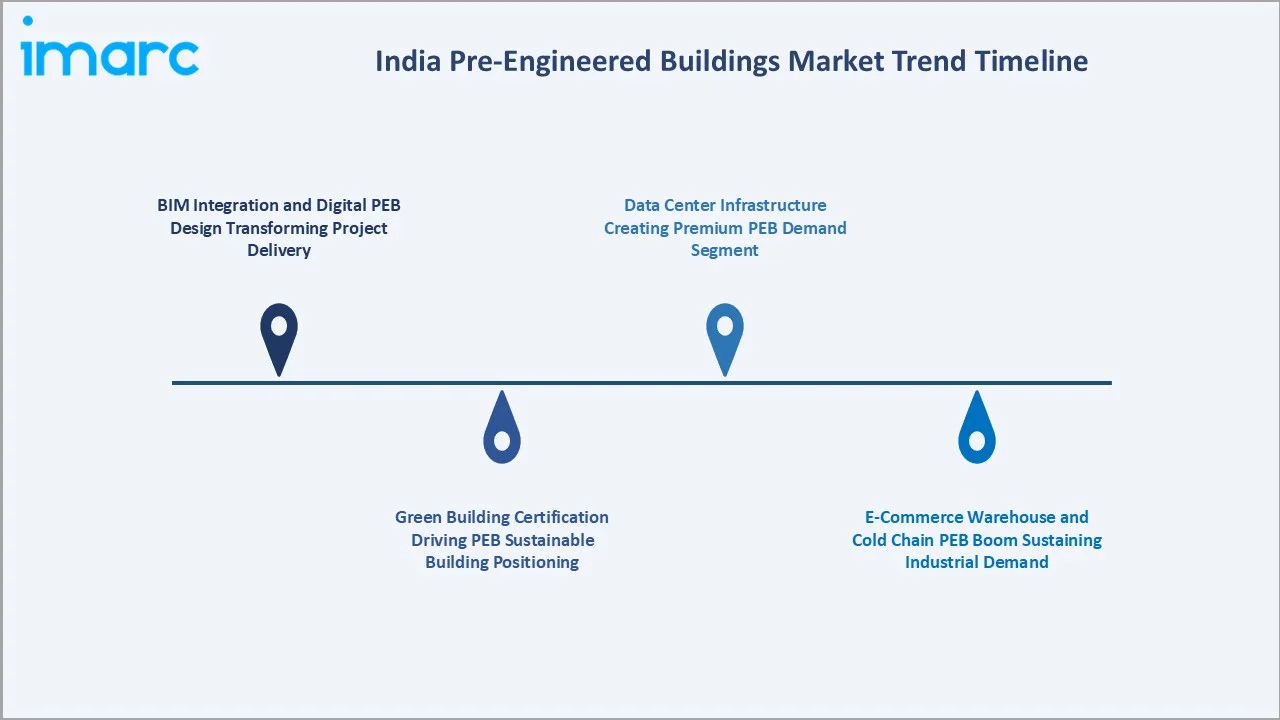

1. BIM Integration and Digital PEB Design Transforming Project Delivery

BIM (Building Information Modeling) integration and digital PEB (pre-engineered building) design are transforming project delivery by enhancing design accuracy, improving collaboration, and streamlining construction processes. These technologies allow for better visualization, faster decision-making, and more efficient resource management, leading to reduced costs, quicker project completion, and higher quality buildings. This shift is driving increased adoption of PEB solutions across various sectors.

2. Green Building Certification Driving PEB's Sustainable Building Positioning

Green building certification is driving the sustainable positioning of pre-engineered buildings (PEB) in India by encouraging the adoption of eco-friendly materials, energy-efficient designs, and reduced carbon footprints. As more PEB projects seek certification, it enhances their market appeal, attracting environmentally conscious clients and aligning with government sustainability goals, thus fostering growth in the sector.

3. E-Commerce Warehouse and Cold Chain PEB Boom Sustaining Industrial Demand

The boom in e-commerce warehouses and cold chain logistics is sustaining industrial demand in the India pre-engineered buildings (PEB) market by driving the need for efficient, scalable, and quick-to-construct facilities. PEBs offer cost-effective and customizable solutions for large storage and temperature-controlled environments, making them ideal for the growing e-commerce and food distribution sectors, thus driving continuous market expansion.

4. Data Center Infrastructure Creating Premium PEB Demand Segment

The rapid growth of data center infrastructure is creating a premium demand segment, as these facilities require highly specialized, energy-efficient, and scalable structures. PEBs provide the ideal solution for constructing data centers quickly, with customizable designs that meet the technical and operational needs of the sector, driving their increased adoption in this high-demand market.

Industry Value Chain Analysis

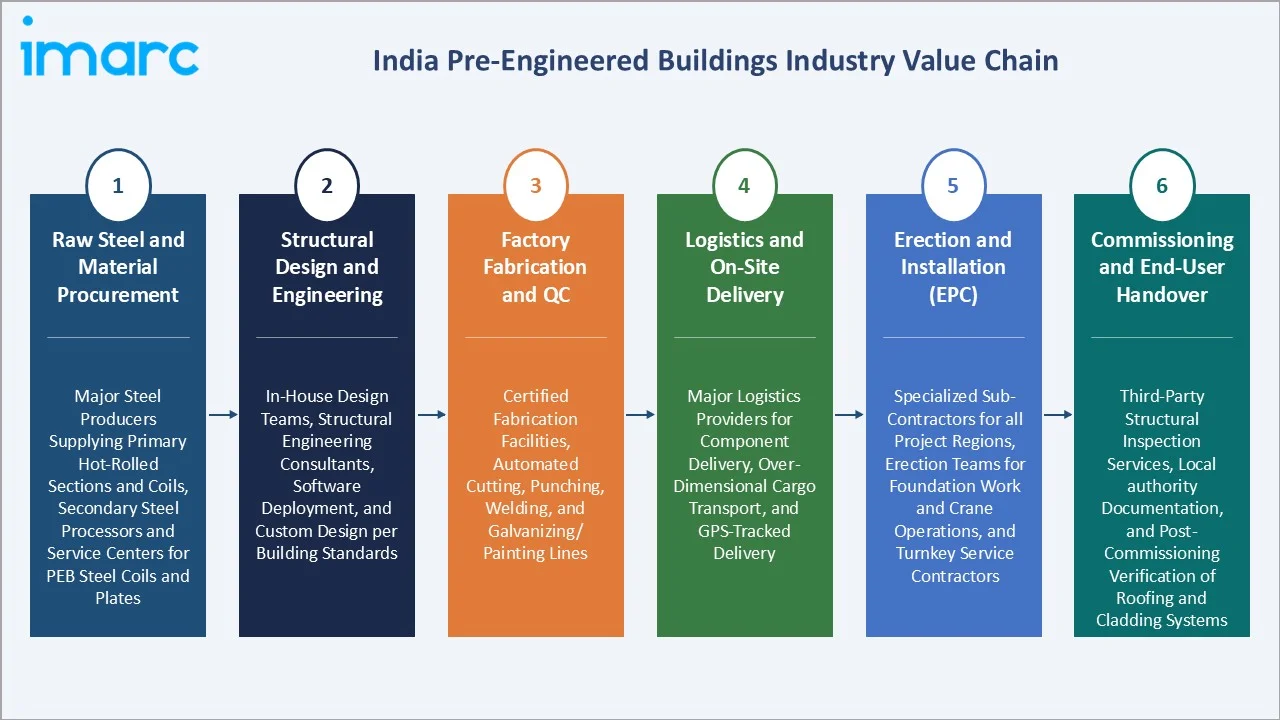

The India PEB value chain integrates primary steel procurement through structural design, computer-aided fabrication, logistics, on-site erection by specialized EPC contractors, and final commissioning to industrial, commercial, and infrastructure end users. PEB manufacturers capture 18-28% EBITDA margins on design-to-delivery projects; EPC-integrated PEB companies capture higher 22-32% margins by controlling the full value chain. Raw steel accounts for 55-65% of total PEB project cost, making steel procurement efficiency the most strategically critical margin determinant.

|

Stage |

Key Participants |

|

Raw Steel & Material Procurement |

Major steel producers supplying primary hot-rolled sections and coils, secondary steel processors and service centers for PEB steel coils and plates |

|

Structural Design & Engineering |

In-house design teams, structural engineering consultants, software deployment, and custom design per building standards |

|

Factory Fabrication & QC |

Certified fabrication facilities, automated cutting, punching, welding, and galvanizing/painting lines |

|

Logistics & On-Site Delivery |

Major logistics providers for component delivery, over-dimensional cargo transport, and GPS-tracked delivery |

|

Erection & Installation (EPC) |

Specialized sub-contractors for all project regions, erection teams for foundation work and crane operations, and turnkey service contractors |

|

Commissioning & End-User Handover |

Third-party structural inspection services, local authority documentation, and post-commissioning verification of roofing and cladding systems |

The EPC contracting tier is the value chain's most operationally complex element, coordinating foundation civil works, PEB structure delivery, erection crew deployment, roofing and cladding installation, and auxiliary systems within PEB's compressed construction timeline. PEB manufacturers with in-house erection capability maintain tighter quality control and scheduling discipline than those relying entirely on third-party EPC subcontractors, providing a competitive advantage in complex multi-span or crane-integrated industrial building projects.

Technology Landscape in the India Pre-Engineered Buildings Industry

Computer-Aided Structural Design (CASD) and Automated Fabrication

Computer-Aided Structural Design (CASD) and automated fabrication streamlining design and production processes. CASD enables precise and efficient structural design, reducing errors and optimizing resource use, while automated fabrication enhances production speed and consistency, allowing for faster, cost-effective manufacturing of PEB components. These technologies drive innovation, improve quality control, and reduce overall project timelines, positioning PEB as a competitive choice for various construction needs.

High-Strength Steel and Advanced Coating Technology

High-strength steel and advanced coating technology are enhancing the durability, strength, and longevity of structures. High-strength steel allows for the construction of lighter yet more robust buildings, reducing material costs and improving load-bearing capacity. Advanced coating technologies provide superior corrosion resistance, especially in harsh environmental conditions, ensuring that PEBs remain structurally sound over time and require minimal maintenance, thereby increasing their appeal for industrial and commercial applications.

Solar-Ready PEB Design and Green Building Integration

Solar-ready PEB design and green building integration are promoting sustainability and energy efficiency. Solar-ready designs enable easy installation of photovoltaic systems, allowing buildings to harness renewable energy and reduce operational costs. Additionally, integrating green building standards, such as energy-efficient materials and water conservation systems, ensures that PEBs meet eco-friendly building certifications, making them more attractive to environmentally conscious clients and aligning with India's growing emphasis on sustainability.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Steel Structure | 52.6% | 2025 |

| End-User | Industrial Sector | 48.7% | 2025 |

| Region | West India | 30.4% | 2025 |

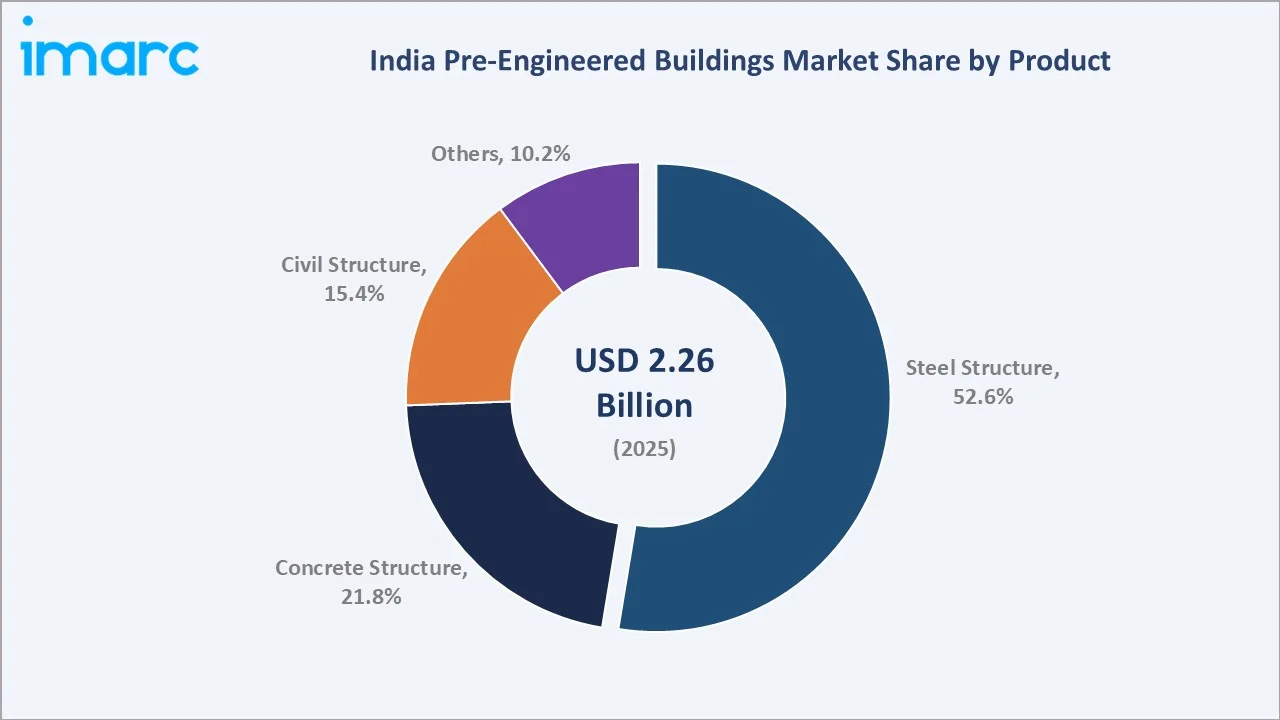

By Product

Steel structure leads at 52.6% market share (2025). This segment encompasses hot-rolled steel primary frames, cold-formed secondary members, pre-coated steel roofing and walling panels, and structural steel mezzanine systems. Steel structure's dominance reflects India's industrial and warehouse PEB market's preference for long-span clear buildings, achievable only with structural steel primary frames.

To access detailed market analysis, Request Sample

Concrete structure at 21.8% serves applications requiring higher fire resistance, seismic performance in Zone IV/V locations, or integration with conventional building codes that prefer RCC, particularly for multi-storey commercial PEB, pharmaceutical clean room facilities, and certain residential PEB. Civil structure at 15.4% covers foundation systems and ancillary civil works integral to PEB project delivery. Others at 10.2% includes insulated sandwich panels, translucent roofing sheets, ventilators, doors, and louvre systems.

By End User

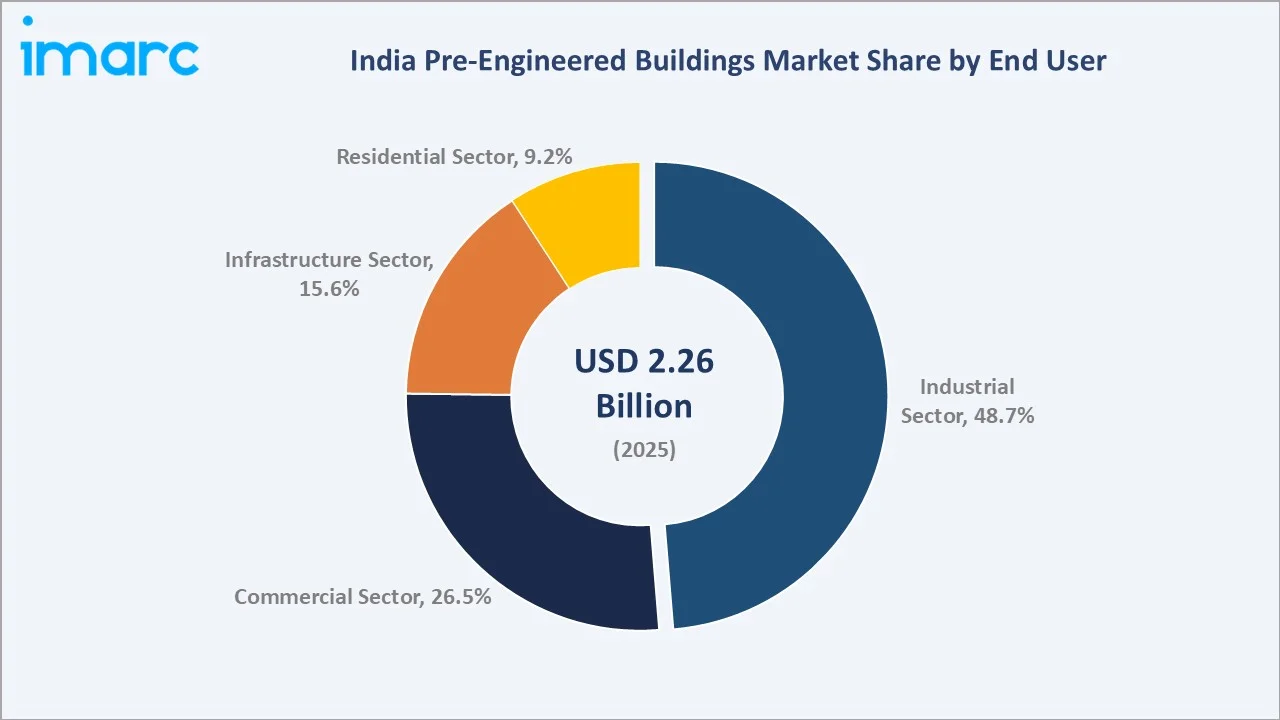

The industrial sector leads at 48.7% market share (2025). India's industrial PEB demand spans automobile manufacturing plants, e-commerce and 3PL warehouses, steel plants and heavy industry ancillaries, pharmaceutical and biotech manufacturing, food processing factories, textile and garment factories, and chemical/petrochemical facilities.

The commercial sector at 26.5% covers automobile showrooms, retail hypermarkets and shopping malls, data centers, corporate office campuses, and hospitality infrastructure. The infrastructure sector at 15.6% serves railways (goods sheds, maintenance depots), airports (terminal extensions, cargo handling), metro rail depots, sports complexes, and bridge/flyover maintenance facilities. The residential sector at 9.2% uses light-gauge steel framing for affordable housing, farmhouse construction, and modular refugee/temporary housing.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

West India |

30.4% |

Strong industrial demand from automotive, engineering, and infrastructure sectors; major investments in industrial zones and logistical hubs. |

|

South India |

27.8% |

Rapid industrial growth, especially in electronics, pharmaceuticals, and manufacturing; expansion of industrial zones and special economic zones. |

|

North India |

24.6% |

High demand driven by large-scale infrastructure projects and manufacturing growth in sectors like electronics, automotive, and logistics. |

|

East India |

17.2% |

Growth in manufacturing and logistics, driven by key industries such as steel, coal, and automotive, with increasing investments in infrastructure. |

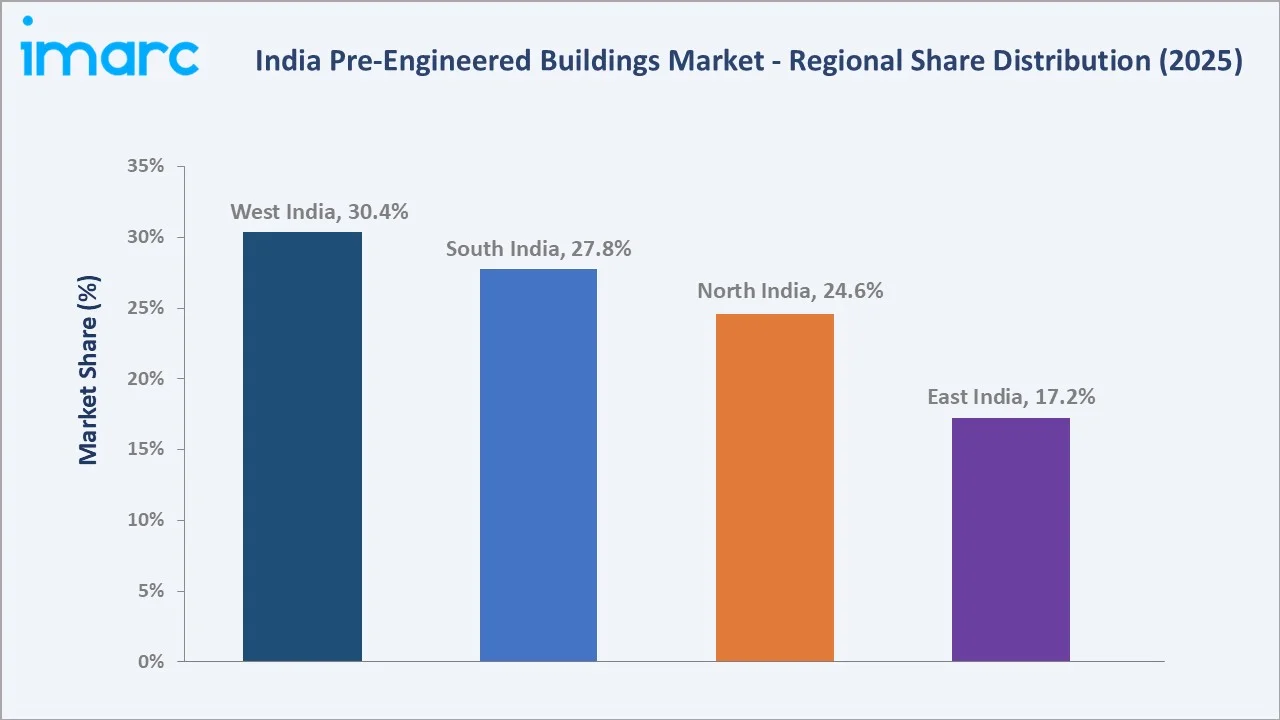

West India's 30.4% leadership represents India's most diverse PEB demand landscape, combining Maharashtra's massive MIDC industrial estate ecosystem with Gujarat's greenfield mega-industrial zones and DMIC corridor surge.

South India's 27.8% is growing fastest, driven by Tamil Nadu's electronics and EV manufacturing cluster attracting PLI investments, Karnataka's aerospace and space tech creating specialized precision industrial PEB demand, and Telangana's Hyderabad pharmaceutical and IT hardware manufacturing zones. East India at 17.2% is the highest-growth potential region, as Odisha's steel-anchored industrialization and West Bengal's logistics hub development create structural PEB demand.

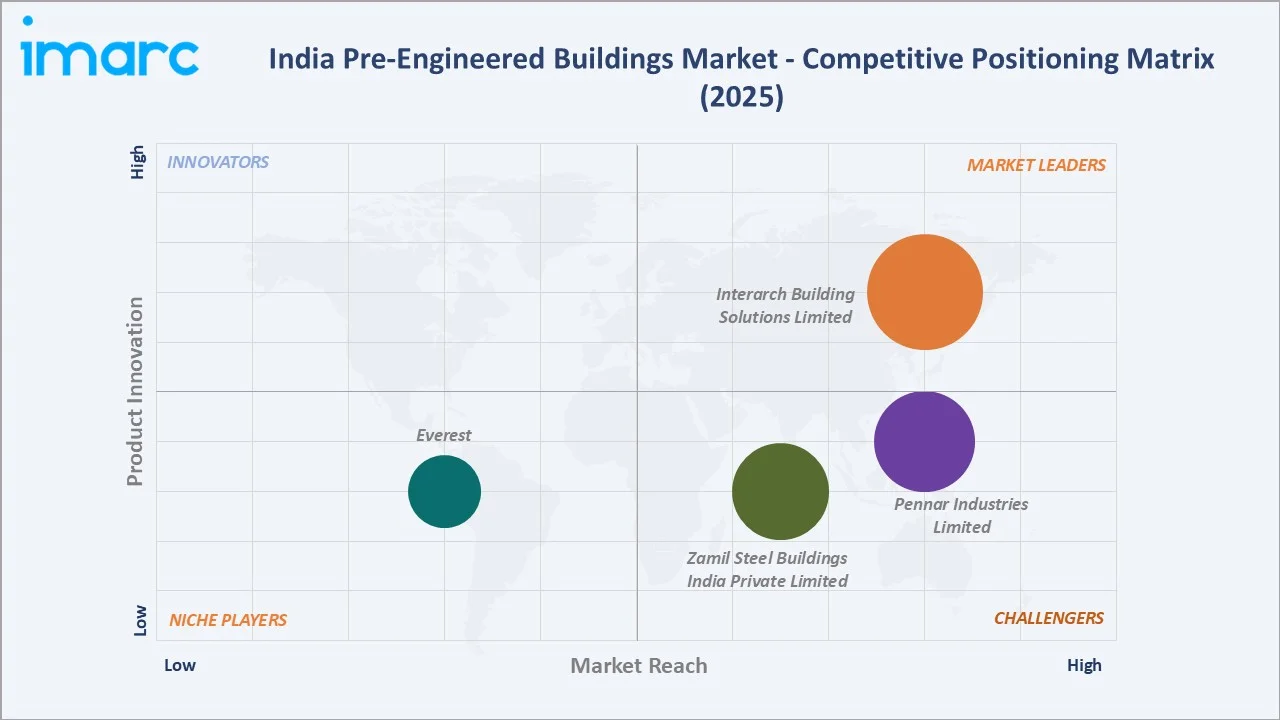

Competitive Landscape

India's PEB market exhibits moderate concentration at the organized sector level. However, the total market includes a significant unorganized segment of regional steel fabricators providing basic PEB-style structures without the engineering rigor, quality certification, or design software investment of organized sector players. The organized PEB sector accounts for approximately 60-65% of total market revenues and virtually all the premium industrial, commercial, and infrastructure PEB demand from multinational and large Indian corporate clients.

|

Company Name |

Brand / Product |

Market Position |

Core Strength |

|

Interarch Building Solutions Limited |

Interarch Pre-engineered Buildings |

Market Leader |

Interarch is one of the leading turnkey pre-engineered steel construction solution providers in India with integrated facilities for design and engineering, manufacturing, and on-site project management capabilities for installation and erection of pre-engineered steel buildings. |

|

Pennar Industries Limited |

PEBS Pennar |

Strong Challenger |

Pennar pre-engineered steel buildings are uniquely designed and fabricated to suit client requirements. |

|

Zamil Steel Buildings India Private Limited |

Zamil Steel Pre-Engineered Building |

Strong Challenger |

Zamil pre-engineered steel buildings consist of primary framing, secondary framing, structural subsystems, floor systems and other building accessories (sliding doors, roll-up doors, windows, louvers, etc.) |

|

Everest |

Everest Pre-Engineered Buildings |

Niche Player |

From warehouses to industrial PEB buildings, Everest designs, manufactures, supplies, and installs PEB buildings in a wide range of market segments. |

The competitive landscape is being reshaped by global PEB brands, deepening their India manufacturing investment in response to the PLI scheme and infrastructure-driven demand growth that is making India among the world's most attractive PEB market geographies for international players.

Key Company Profiles

Interarch Building Solutions Limited

Interarch is one of India's largest pre-engineered buildings companies by annual fabrication capacity, and represents the Indian PEB industry's most comprehensive manufacturing, design, and erection capability.

- Portfolio: Interarch Pre-engineered Buildings.

- Recent Developments: In May 2025, Interarch Building Solutions acquired 20 acres of industrial land next to its current manufacturing facility in Attivaram Village, Nellore, Andhra Pradesh. This strategic expansion will focus on the production of Pre-Engineered Heavy Steel Structures.

- Strategic Focus: South India market development through new fabrication plant planning.

Pennar Industries Limited

Pennar Industries offers a comprehensive solution for diverse building needs. Pennar’s pre-engineered steel buildings are custom-designed and fabricated to meet client-specific requirements. Adhering to international standards, these structures are made up of various components that are carefully designed to ensure compatibility with each other.

- Portfolio: PEBS Pennar

- Recent Developments: Pennar Industries surged 4.46% to Rs 181.60 after announcing plans to expand its manufacturing operations in Northern India with a new plant in Raebareli, Uttar Pradesh. The pre-engineered building (PEB) manufacturing facility, established in Q2 2024, covers 16 acres with a built-up area of 12,000 square meters.

- Strategic Focus: Expanding manufacturing capacity, enhancing product customization, and leveraging advanced technologies to meet growing demand across industrial and infrastructure sectors.

Market Concentration Analysis

The organized India PEB market is moderately concentrated, with the top 5 companies collectively commanding approximately 55-60% of organized sector PEB revenues. Including the unorganized regional steel fabricator segment, total market concentration drops to 35-40% for the top 5, reflecting the substantial presence of smaller regional PEB manufacturers serving Tier-2/3 city markets and MSME clients.

The market is experiencing gradual organized sector consolidation driven by large corporate clients preferring ISO-certified, financially stable organized sector PEB providers and Bank of Baroda, SBI, and HDFC Bank preferring organized sector PEB contractors for project loan disbursement against PEB construction milestones, creating a financial ecosystem bias toward organized sector players.

Technology investment differentiation is increasingly separating the organized PEB sector's top-tier from mid-tier players, creating a quality and reliability gap that supports premium pricing by technology-enabled manufacturers. ZAMIL Steel and Interarch operate at technology standards comparable to global PEB manufacturers, while regional players operate with conventional fabrication equipment and manual design methods, creating a sustainable competitive moat for technology-invested organized sector leaders.

Investment & Growth Opportunities

Fastest Growing Segments

Industrial sector (~13.5% CAGR), steel structure (~13.1% CAGR), data center PEB (~25%+ CAGR from small base), cold chain PEB (~18%+ CAGR), East India region (~14-15% CAGR), and residential LGSF (~18%+ CAGR) represent India's PEB market's highest-growth investment vectors through 2034. East India's emergence as India's fastest-growing PEB region represents the most geographically underserved high-growth PEB investment opportunity in the current market.

Emerging Market Opportunities

India's semiconductor and advanced electronics manufacturing boom creates premium PEB demand for cleanroom manufacturing facilities, wafer fab ancillary buildings, and test and assembly structures. Semiconductor fabs require specialized PEB solutions (vibration-controlled foundations, static-free cladding, ultra-clean air circulation integration) that command a higher price versus industrial PEB, making semiconductor facility PEB the highest-margin and fastest-growing industrial PEB sub-segment through 2034.

Investment Themes

- PEB fabrication capacity expansion in South and East India: Manufacturing plant establishment in Tamil Nadu or Telangana and Odisha or West Bengal would capture geographic market share currently served by West India-based manufacturers at a 5-8% transportation cost premium.

- Cold chain and pharmaceutical PEB specialization: India's cold chain deficit (capacity requirement 2x installed capacity) and pharmaceutical GMP manufacturing expansion create sustained premium PEB demand for insulated panel-intensive cold storage and cleanroom-compatible pharmaceutical manufacturing buildings.

Future Market Outlook (2026-2034)

The India pre-engineered buildings market is projected to grow from USD 2.26 Billion in 2025 to USD 6.46 Billion by 2034, delivering a 12.38% CAGR over the forecast period. The market's anchor value of USD 4.05 Billion in 2030 represents an India PEB industry at its structural inflection point, where PEB has transitioned from a preferred alternative to conventional RCC for large industrial buildings to becoming the dominant construction method for India's entire industrial CAPEX investment cycle, driven by PLI scheme manufacturing investment, National Logistics Policy warehousing build-out, and the data center infrastructure boom collectively creating new industrial building demand through 2030.

Three structural forces define India's PEB market growth trajectory with exceptional certainty through 2034: India's infrastructure pipeline creating mandatory infrastructure construction demand across projects where PEB's construction speed advantage makes it the preferred structural system for terminal buildings, maintenance facilities, and logistics infrastructure across highways, railways, airports, and ports; the PLI scheme's 14-sector manufacturing investment activation generating sustained greenfield factory PEB demand for semiconductor, EV, electronics, pharmaceutical, and food processing sectors that individually represent multi-billion-dollar annual PEB procurement pipelines; and East India's industrial development acceleration as Odisha, West Bengal, and Northeast states emerge from industrial underperformance with large-scale steel, aluminum, chemicals, and logistics investments that are beginning to create PEB demand concentrations.

Research Methodology

Primary Research

Primary research comprised structured interviews with 65+ industry stakeholders (2025), including VP Engineering and Business Development executives; structural engineers from BIS TC 54 (structural steel) and NBC 2016 revision committee; MIDC, GIDC, and TIDCO industrial estate officers; PLI scheme beneficiary company project heads commissioning PEB factories; EPC contractors specializing in PEB erection across North, South, and West India; and institutional buyers managing PEB warehouse procurement.

Secondary Research

Secondary research encompassed the Ministry of Steel annual report 2024-25, PECJ (Pre-Engineered Concrete Joist Council of India) industry statistics, DPIIT PLI scheme beneficiary database and disbursement data 2025, Ministry of Commerce Industrial Corridor Development Authority project status reports, CMIE (Centre for Monitoring Indian Economy) CAPEX database, MoRTH National Infrastructure Pipeline progress report, company annual reports, and building construction industry trade publications. Over 120 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up project pipeline models incorporating DPIIT PLI scheme investment commitment to floor area conversion ratios by sector, National Infrastructure Pipeline project count to PEB structural cost estimation, CMIE CAPEX database segment-specific industrial CAPEX growth projections, and organized sector PEB manufacturer capacity utilization-revenue relationship modeling. Key inputs include steel price projections, NIP project completion timeline distributions, PLI scheme disbursement schedules by sector, and regional industrial estate expansion area targets from MIDC, GIDC, TIDCO, and APIIC official five-year development plans.

India Pre-Engineered Buildings Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Concrete Structure, Steel Structure, Civil Structure, Others |

| End-Users Covered | Industrial Sector, Commercial Sector, Infrastructure Sector, Residential Sector |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Interarch Building Solutions Limited, Pennar Industries Limited, Zamil Steel Buildings India Private Limited, Everest, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India pre-engineered buildings market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India pre-engineered buildings market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India pre-engineered buildings industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Pre-Engineered Buildings Market Report

The India PEB market reached USD 2.26 Billion in 2025, driven by PLI scheme factory construction across 14 sectors, e-commerce warehouse expansion, infrastructure pipeline, National Logistics Policy, and data center infrastructure development requiring rapid-build structural systems.

The market grows at 12.38% CAGR during 2026-2034, reaching USD 6.46 Billion by 2034, driven by India's INR 11.11 Trillion infrastructure budget, PLI-driven factory demand, semiconductor and EV manufacturing, National Logistics Policy warehousing build-out, and data center infrastructure boom.

Steel structure leads at 52.6%, reflecting the dominance of hot-rolled steel primary frames for large-span industrial and warehouse applications.

The industrial sector leads at 48.7% and grows fastest at ~13.5% CAGR, driven by PLI scheme factory construction, e-commerce warehouses, cold chain infrastructure, pharmaceutical manufacturing, data centers, and automobile plant expansions requiring rapid-build construction solutions.

Leading companies include Interarch Building Solutions Limited, Pennar Industries Limited, Zamil Steel Buildings India Private Limited, and Everest, among others.

The market is projected to reach approximately USD 4.05 Billion by 2030, with Interarch scaling capacity, new South/East India manufacturing plants operational, semiconductor and data center PEB growth, and BIM adoption mandatory for organized sector projects.

India's PLI scheme committed INR 1.97 Trillion across 14 sectors with approved beneficiaries investing in manufacturing capacity. Each PLI-approved investment requires greenfield/brownfield factory construction, driving the market demand.

Key restraints include steel price volatility, limited PEB awareness in Tier-2/3 cities, and a skilled erection workforce shortage, compressing EPC contractor margins on fast-paced industrial projects.

East India's PEB acceleration is driven by the region’s steel and logistics hub development, and Northeast India's improving connectivity, unlocking previously inaccessible industrial markets, collectively creating new PEB demand concentrations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade