India Private Banking Market Size, Share, Trends and Forecast by Banking Sector, Application, and Region, 2026-2034

India Private Banking Market Summary:

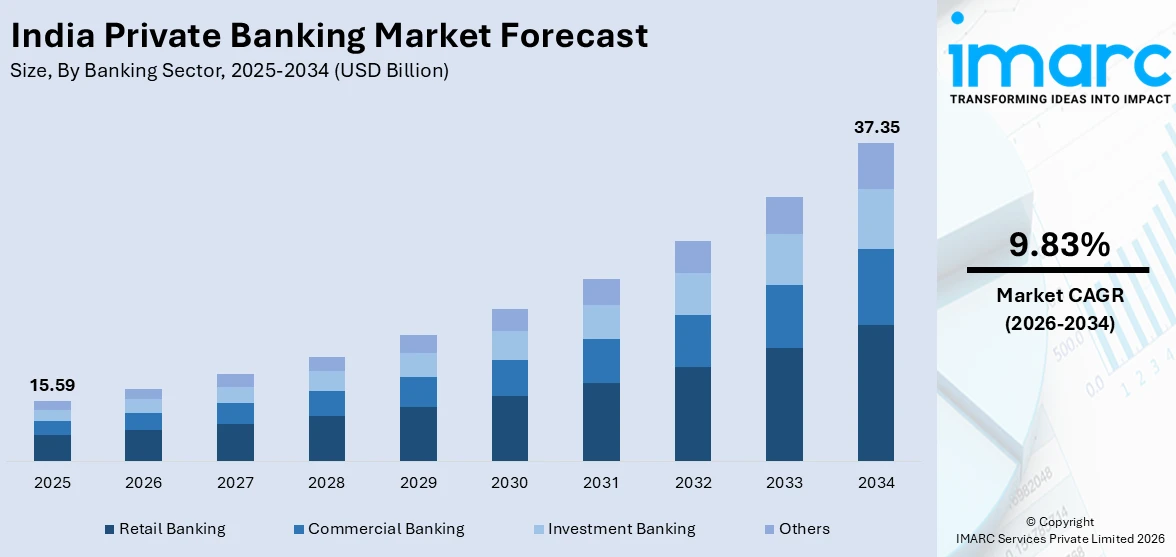

The India private banking market size was valued at USD 15.59 Billion in 2025 and is projected to reach USD 37.35 Billion by 2034, growing at a compound annual growth rate of 9.83% from 2026-2034.

The India private banking market is expanding steadily, as affluent households seek more personalized advice, broader investment access, and integrated banking relationships. Demand is being supported by rising entrepreneurial wealth, stronger interest in succession planning, wider adoption of digital wealth interfaces, and growing preference for tailored portfolios that combine preservation, liquidity, and long-term capital appreciation. Increasing financial awareness among high-net-worth individuals is further strengthening demand for specialized wealth management services.

Key Takeaways and Insights:

- By Banking Sector: Retail banking dominates the market with a share of 46.2% in 2025, owing to its wide customer reach, strong relationship-banking model, and ability to cross-sell wealth advisory, deposits, lending, and investment solutions through established premium banking ecosystems tailored for affluent clients.

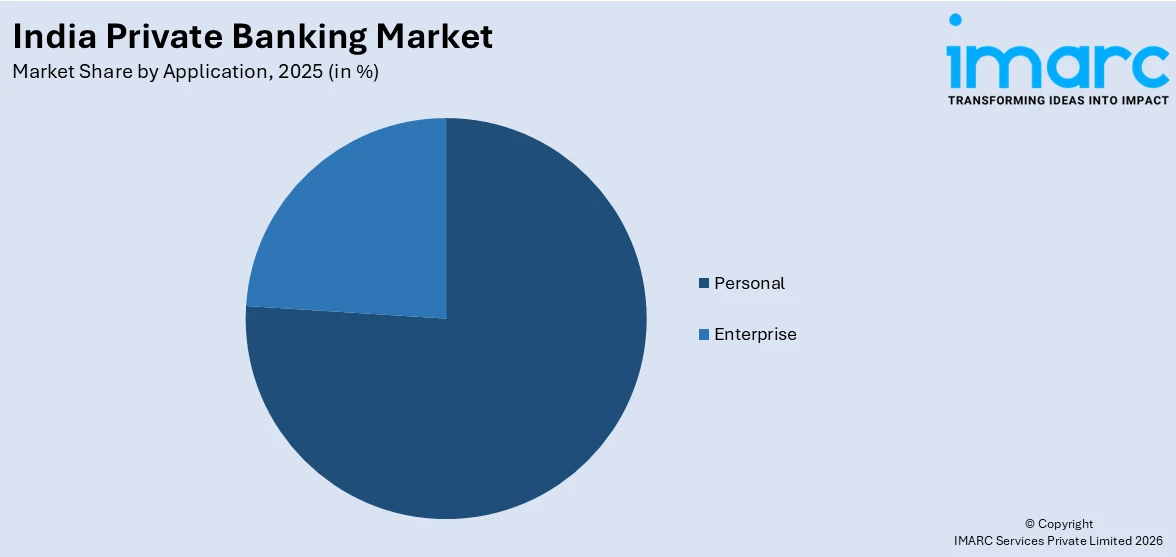

- By Application: Personal leads the market with a share of 76.2% in 2025, driven by rising demand for customized portfolio construction, estate planning, tax-efficient allocation, and advisory-led banking services among high-net-worth individuals seeking convenience, discretion, and a single point of financial relationship management.

- By Region: West India represents the largest region with 30.3% share in 2025, supported by the concentration of financial centers, family-owned businesses, startup wealth creation, and mature advisory networks that continue to attract high-value clients looking for premium banking and investment support.

- Key Players: Key players drive the India private banking market by enhancing digital advisory platforms, deepening relationship-led service models, expanding family office and succession solutions, and broadening access to diversified products across fixed income, equities, alternatives, credit, and global investment opportunities for affluent customers.

To get more information on this market Request Sample

The India private banking market is supported by structural shifts in wealth creation and financial behavior. A growing base of entrepreneurs, promoters, professionals, and business families is increasing demand for sophisticated advisory-led banking relationships that go beyond deposits and lending. As of December 31, 2023, the Department for Promotion of Industry and Internal Trade (DPIIT) identified 1,17,254 startups. Clients are seeking curated asset allocation, legacy planning, philanthropic advisory, and access to a wider range of domestic and international investment opportunities. At the same time, private banks are modernizing service delivery through digital onboarding, portfolio dashboards, remote advisory, and data-led personalization. The market is also benefiting from rising financial awareness among younger affluent clients who expect convenience, transparency, and faster execution across channels. As wealth becomes more diversified across listed equities, private markets, fixed income, real estate, and structured solutions, private banking providers are positioning themselves as long-term partners focused on preservation, growth, and intergenerational continuity.

India Private Banking Market Trends:

Rise of Hybrid Advisory and Digital Wealth Interfaces

Private banking in India is moving towards a hybrid service model that combines relationship-manager-led advice with digital access to portfolios, research, reporting, and transaction execution. Affluent clients increasingly expect seamless switching between branch engagement, remote consultation, and app-based monitoring. This shift is helping banks improve responsiveness and deepen engagement while giving clients quicker access to reviews, recommendations, and product discovery without sacrificing the personal trust that remains central to premium banking relationships.

Greater Demand for Holistic Wealth and Succession Planning

Indian clients are showing stronger interest in solutions that connect investment returns with broader financial goals, such as succession, family governance, philanthropy, liquidity planning, and risk protection. Private banking relationships are gradually expanding from product-led conversations to full-balance-sheet advice. This trend is especially visible among business owners and multi-generational families who want support in structuring assets across entities, beneficiaries, and timelines while preserving control, privacy, and long-term continuity.

Broader Appetite for Diversified and Alternative Allocation

Client portfolios in India are gradually becoming more diversified, as private banking customers look beyond traditional savings products and public-market exposure. Interest is rising in global assets, private credit, structured offerings, curated thematic strategies, and professionally managed alternatives that can improve balance across risk and return objectives. This trend is encouraging providers to strengthen advisory depth, product due diligence, and suitability frameworks so that affluent investors can access wider opportunities with more disciplined portfolio construction.

Market Outlook 2026-2034:

The India private banking market is expected to maintain healthy growth over the forecast period, as wealth creation broadens across entrepreneurship, professional services, technology, manufacturing, and family-owned businesses. Demand is likely to remain firm for customized advisory, estate planning, portfolio diversification, and digitally enabled relationship management. The market generated a revenue of USD 15.59 Billion in 2025 and is projected to reach a revenue of USD 37.35 Billion by 2034, growing at a compound annual growth rate of 9.83% from 2026-2034. Banks are expected to expand premium offerings through stronger research, improved data-led personalization, wider product access, and deeper regional penetration across affluent urban clusters. The long-term outlook is also supported by increasing participation from younger wealthy clients who value speed, transparency, and integrated financial planning.

India Private Banking Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Banking Sector |

Retail Banking |

46.2% |

|

Application |

Personal |

76.2% |

|

Region |

West India |

30.3% |

Banking Sector Insights:

- Retail Banking

- Commercial Banking

- Investment Banking

- Others

Retail banking dominates with a market share of 46.2% of the total India private banking market in 2025.

Retail banking holds the largest share in the India private banking market because it gives banks a natural entry point into affluent relationships through premium savings, deposits, cards, mortgages, and day-to-day transaction services. These relationships often mature into broader advisory mandates as customers accumulate wealth and look for investment planning, credit structuring, and portfolio support within a trusted banking ecosystem. The segment also benefits from strong service familiarity, broad branch access, and deeper customer data that helps banks tailor solutions with greater relevance and continuity.

The strength of retail-led private banking is especially visible in premium banking programs built around dedicated relationship managers, curated investment offerings, and bundled lifestyle or liquidity services. Affluent customers often prefer one institution that can manage payments, deposits, financing, and wealth allocation under a single umbrella rather than spreading activity across multiple providers. The segment expansion is supported by the continued broadening of premium relationship-led propositions by major private banks in India, which increasingly use digital dashboards and curated advisory to convert high-value retail clients into long-term wealth customers.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Personal

- Enterprise

Personal leads the market with a share of 76.2% of the total India private banking market in 2025.

Personal accounts for the largest share of the India private banking market because the core demand base comes from affluent individuals and families seeking tailored advice for wealth preservation, growth, and succession. These clients value confidential engagement, dedicated portfolio reviews, tax-aware allocation, and seamless access to liquidity alongside investment opportunities. Personal private banking also benefits from emotional trust and long-standing banker relationships, which remain important when clients are making decisions around inheritance, family needs, and changing risk preferences over time.

This leadership is also reinforced by the rising number of founders, senior professionals, and business owners who need advisories that reflect both their personal and business-linked financial realities. Their requirements often include estate structuring, family governance discussions, philanthropy planning, and curated exposure to domestic and offshore products. A useful market illustration is the growing visibility of family office-style service layers and bespoke advisory propositions across India’s premium banking landscape, showing how individual client relationships continue to anchor the market far more strongly than enterprise-led use cases.

Regional Insights:

- North India

- South India

- East India

- West India

West India represents the leading region with a 30.3% share of the total India private banking market in 2025.

West India leads the market, as it combines the country’s deepest financial infrastructure with a large concentration of wealthy entrepreneurs, legacy business families, financial professionals, and startup-linked wealth creators. Mumbai remains the anchor for the region, serving as India’s most important banking and capital-markets center, while Pune and other urban clusters add further demand through manufacturing, technology, and services-led affluence. In December 2024, Barclays Bank moved its corporate and investment banking offices in Mumbai, along with its private bank, to Raheja Altimus in Worli, Mumbai. The newly constructed building covers 65,000 square feet and includes contemporary amenities aimed at fostering collaboration and development.

The regional advantage is strengthened by the proximity of clients to decision-makers, wealth specialists, and capital-market institutions that support faster execution and more customized service. West India also tends to generate steady inflows from promoter wealth, treasury allocations, and intergenerational asset management, which suits private banking expansion. A practical illustration is the continued concentration of premium wealth events, relationship hubs, and product partnerships in Mumbai, reflecting how West India remains the natural center for high-value banking, advisory, and long-term wealth planning in the country.

Market Dynamics:

Growth Drivers:

Why is the India Private Banking Market Growing?

Expansion of Affluent and Entrepreneurial Wealth Base

India private banking is growing because the country is producing a broader and more geographically distributed affluent population. Wealth is no longer limited to a narrow pool of legacy business families. It is also being created by founders, senior professionals, exporters, investors, and owners of mid-sized companies across technology, healthcare, manufacturing, consumer businesses, and financial services. As these clients accumulate surplus capital, they begin to require more than standard banking products. They look for tailored advisory around diversification, liquidity, tax efficiency, structured credit, and succession. Private banks are well positioned to capture this shift because they can combine trust-led relationship management with access to investment products, lending, and treasury support. The broadening wealth base also supports expansion outside traditional elite circles, allowing banks to serve a larger upper-affluent and emerging high-net-worth segment. This demand pipeline is creating sustained momentum for premium banking propositions focused on preserving capital, growing assets, and managing complex personal financial decisions across life stages.

Increasing Preference for Integrated Financial Advice

Another major growth driver is the shift in client preference from isolated product purchases towards integrated financial advice. Affluent customers increasingly want a single banking relationship that can connect deposits, payments, lending, investments, risk management, and legacy planning into one coordinated service experience. This is especially relevant for clients with diversified asset bases, business linkages, cross-border interests, or intergenerational responsibilities. Private banking meets this need by offering customized portfolio reviews, periodic rebalancing guidance, access to specialists, and a more consultative approach to wealth decisions. The value of this model becomes stronger when markets are uncertain or when clients need help balancing yield, liquidity, and risk. Banks are using these needs to deepen engagement through dedicated relationship teams, research-backed recommendations, and advisory-led service journeys. As customer expectations rise for personalization and convenience, the integrated private banking model is becoming more compelling than fragmented arrangements spread across separate brokers, lenders, and transactional banking relationships.

Growing Global Investor Confidence

Increasing global investor confidence in the India private banking sector is emerging as a notable trend, reflecting the country’s strengthening financial ecosystem and long-term economic prospects. In 2025, foreign investors pumped over USD 6 Billion into the India private banking industry via a series of significant transactions, indicating a revived global trust in the nation’s financial framework. International investors increasingly view private banks as well-governed, growth-oriented institutions capable of capturing rising credit demand and expanding wealth management opportunities. The sector benefits from improving asset quality, stronger regulatory oversight, and continued progress in digital banking capabilities. As India’s economy expands and entrepreneurial wealth increases, private banks are positioned to play a larger role in financing businesses, supporting investments, and managing affluent client relationships. Foreign investors are therefore showing greater willingness to participate in the sector through strategic investments and capital partnerships. Their involvement also supports the modernization of banking infrastructure, encourages adoption of global best practices, and strengthens capital buffers.

Market Restraints:

What Challenges the India Private Banking Market is Facing?

Regulatory and Suitability Complexity

Private banking providers operate in a tightly supervised financial environment where product suitability, transparency, documentation, and risk communication carry growing importance. As affluent clients gain access to broader investment choices, banks must maintain strong governance around advice quality, disclosures, and portfolio fit. This can slow product rollout and raise compliance burden, especially when solutions involve multiple jurisdictions, structured instruments, or bespoke allocations.

Talent and Relationship Manager Dependence

The market remains heavily dependent on experienced relationship managers who can build trust, understand family dynamics, and translate complex financial needs into practical advisory. Recruiting and retaining such talent is difficult, particularly as institutions compete for seasoned bankers with strong client books. Service continuity can weaken when key managers leave, creating retention risk and making scale harder to achieve in newer cities or emerging affluent segments.

Client Caution During Market Volatility

Affluent clients often become more selective during periods of market uncertainty, which can slow fresh allocations and delay movement into new products. Risk aversion may push customers toward liquidity, deposits, or familiar instruments even when banks are trying to encourage diversified long-term planning. This can reduce advisory momentum, lengthen decision cycles, and make revenue visibility less stable for providers whose premium offerings depend on active portfolio deployment.

Competitive Landscape:

The India private banking market is moderately concentrated and highly relationship-driven, with competition centered on service quality, advisory depth, product breadth, digital convenience, and the ability to retain high-value clients over long periods. Providers compete by strengthening premium banking propositions, improving research-backed guidance, and creating a more integrated model that combines investments, lending, transaction banking, and legacy planning. Market participants are also focusing on regional expansion into affluent urban clusters, stronger family office-style capabilities, and more personalized engagement using analytics-enabled service tools. Differentiation increasingly depends on the ability to balance discretion, responsiveness, and portfolio sophistication while maintaining strong compliance and suitability standards. As client expectations rise, competitive advantage is shifting towards institutions that can deliver both trusted human relationships and seamless digital access across the full wealth journey.

Recent Developments:

- In December 2025, Axis Bank Ltd. revealed plans to recruit 50 private bankers and intended to introduce multiple funds in India’s low-tax finance hub, as part of a wider initiative to leverage the booming rise of the nation’s affluent demographic. The bank also intended to introduce several funds in early 2026 from Gujarat International Finance Tec-City, known as GIFT City.

India Private Banking Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Banking Sectors Covered | Retail Banking, Commercial Banking, Investment Banking, Others |

| Applications Covered | Personal, Enterprise |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Private Banking Market Report

The India private banking market size was valued at USD 15.59 Billion in 2025.

The India private banking market is expected to grow at a compound annual growth rate of 9.83% from 2026-2034 to reach USD 37.35 Billion by 2034.

Retail banking dominated the market with a share of 46.2%, supported by strong customer relationships, premium banking access, and its ability to bundle deposits, lending, and investment advisory within one trusted banking ecosystem.

Key factors driving the India private banking market include the expansion of affluent wealth, rising demand for integrated advisory, increasing portfolio diversification needs, and stronger digital delivery of premium banking services across major urban centers.

Major challenges include regulatory and suitability complexity, dependence on experienced relationship managers, and cautious client allocation behavior during periods of market volatility and uncertain investment sentiment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)