India Pumped Hydro Storage Market Size, Share, Trends and Forecast by Type, Sources, and Region, 2026-2034

India Pumped Hydro Storage Market Summary:

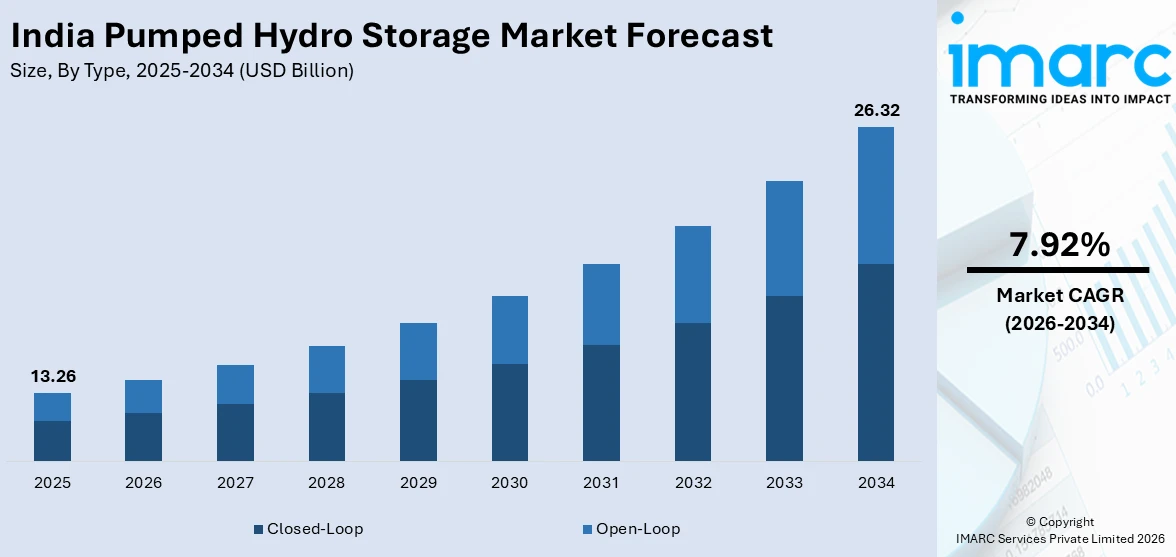

The India pumped hydro storage market size was valued at USD 13.26 Billion in 2025 and is projected to reach USD 26.32 Billion by 2034, growing at a compound annual growth rate of 7.92% from 2026-2034.

The India pumped hydro storage market is expanding rapidly, as the nation prioritizes large-scale, long-duration energy storage to support its growing renewable energy capacity. Favorable government policies, streamlined regulatory approvals, and increasing private sector participation are driving project development across multiple states. Rising demand for grid flexibility, peak load management, and clean energy integration is further strengthening the market share.

Key Takeaways and Insights:

- By Type: Closed-loop dominates the market with a share of 56% in 2025, owing to its minimal environmental disruption, independence from natural river systems, and faster regulatory approvals that accelerate project commissioning timelines across Indian states.

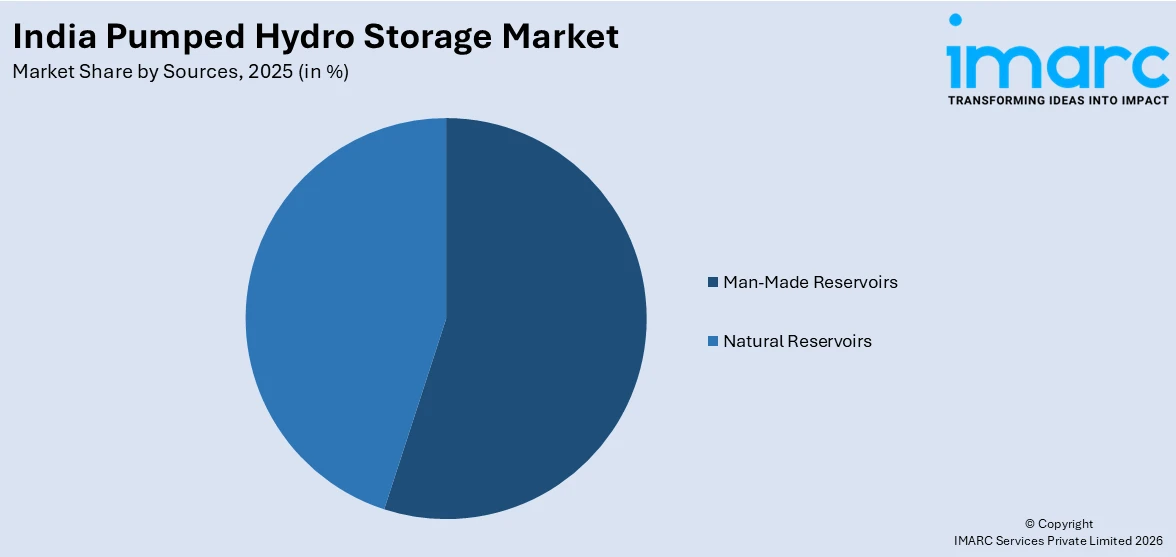

- By Sources: Man-made reservoirs lead the market with a share of 52% in 2025. This dominance is driven by the flexibility of constructing purpose-built reservoirs at optimal elevations, enabling efficient energy storage and release cycles without dependence on existing natural water bodies.

- Key Players: Key players drive the India pumped hydro storage market by developing large-scale projects, investing in advanced variable-speed turbine technologies, forming strategic partnerships with state governments, and expanding project pipelines to strengthen grid reliability and accelerate the nation's clean energy transition.

To get more information on this market Request Sample

The India pumped hydro storage market is undergoing a transformative expansion, driven by the nation's ambitious renewable energy targets and the urgent need for grid-scale energy storage solutions. As India's non-fossil fuel installed capacity has increased, the demand for reliable storage infrastructure has intensified significantly. In November 2025, the installed capacity of non-fossil power reached 262.74 GW, accounting for 51.5% of the nation's total installed energy capacity (509.64 GW). Private sector involvement has surged, with major energy companies securing development rights across states with favorable terrain and water resources. The government's streamlined approval processes, coupled with policy incentives, such as waiver of interstate transmission charges and inclusion under energy storage obligations, are creating a robust ecosystem for sustained market growth.

India Pumped Hydro Storage Market Trends:

Shift Towards Off-Stream Closed-Loop Configurations

The India pumped hydro storage market is witnessing a decisive shift towards off-stream closed-loop systems that operate independently of natural river flows and minimize ecological disruption. In August 2025, the Ministry of Power issued a notification exempting off-stream closed-loop projects from Central Electricity Authority (CEA) concurrence requirements, regardless of project expenditure, significantly accelerating development timelines and reducing regulatory complexity for developers across the country. This policy move is boosting private investment by improving project certainty and site flexibility.

Adoption of Variable-Speed Pumped Storage Technology

Modern variable-speed pumped storage technology is gaining traction, as operators seek enhanced grid flexibility and faster response times to load fluctuations. This technology enables rapid transitions between turbine and pump operations, providing superior power control compared to conventional fixed-speed units. In June 2025, GE Vernova commissioned the first 250 MW variable-speed pumped storage unit at the Tehri Hydropower Complex in Uttarakhand, marking India's first deployment of this advanced technology. The complex is set to reach 2.4 GW of total generating capacity upon full completion, representing a significant market growth milestone.

State-Level Policy Frameworks Accelerating Development

Multiple Indian states are formulating dedicated pumped hydro storage policies to attract investment and streamline project execution. These state-level frameworks complement national guidelines by offering site identification, competitive bidding mechanisms, and expedited clearance processes tailored to local conditions. In March 2025, the Madhya Pradesh government introduced a plan to develop and carry out pump hydro storage projects in the state, positioning the state as a leading hub for clean energy storage development and renewable energy integration.

Market Outlook 2026-2034:

The India pumped hydro storage market outlook remains highly promising, supported by the government’s clear national roadmap and long-term commitment to expanding pumped storage capacity. The country's commitment to achieving its net-zero emissions goals and integrating an expanding share of variable renewable energy sources is expected to sustain robust investment inflows into pumped storage infrastructure. The market generated a revenue of USD 13.26 Billion in 2025 and is projected to reach a revenue of USD 26.32 Billion by 2034, growing at a compound annual growth rate of 7.92% from 2026-2034. The rapid expansion of off-stream closed-loop projects, combined with increasing private sector participation from major energy developers, is expected to transform India's energy storage landscape.

India Pumped Hydro Storage Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Closed-Loop |

56% |

|

Sources |

Man-Made Reservoirs |

52% |

Type Insights:

- Open-Loop

- Closed-Loop

Closed-loop dominates with a market share of 56% of the total India pumped hydro storage market in 2025.

Closed-loop has emerged as the preferred configuration in India because it operates independently of the natural river ecosystems and has a far smaller environmental impact. These systems do not require constant water inflow from rivers or streams since they use two separate reservoirs that recycle water in a closed cycle. In India, developers and state authorities are increasingly choosing layouts that reduce land acquisition problems and ecological concerns.

Closed-loop systems have been highly favored by the regulatory environment, which sets them apart from traditional hydropower projects with their simplified approval processes. Compared to river-based solutions, closed-loop topologies usually have shorter construction timelines and less complicated regulations. In hilly and plateau areas, especially in Maharashtra, Andhra Pradesh, Gujarat, Karnataka, and Uttar Pradesh, developers and state utilities have been proposing these systems more frequently. The growth potential of closed-loop pumped hydro storage across India's varied terrains is further enhanced by the capacity to repurpose depleted mines and existing reservoirs.

Sources Insights:

Access the comprehensive market breakdown Request Sample

- Natural Reservoirs

- Man-Made Reservoirs

Man-made reservoirs lead with a share of 52% of the total India pumped hydro storage market in 2025.

Man-made reservoirs have become the predominant source for pumped hydro storage installations in India, offering developers the flexibility to construct purpose-built facilities at optimal locations with suitable elevation differences. In September 2024, the Indian government expanded its financial assistance for hydropower projects, allocating INR 12,461 Crore for the fiscal years 2024-2025 to 2031-32. All pumped storage projects, including captive/merchant pumped storage projects, will be eligible for this program. Unlike natural reservoirs, man-made structures can be engineered to precise specifications, ensuring efficient water storage and energy conversion cycles.

The development of man-made reservoirs enables project deployment in regions lacking suitable natural water bodies, significantly expanding the geographic scope of pumped hydro storage across India. These engineered reservoirs facilitate closed-loop system designs that minimize river ecosystem disruption while providing reliable water availability for continuous pump-turbine operations. State governments are actively identifying and allocating sites for man-made reservoir construction, with dedicated policies streamlining land allocation and environmental approvals. The ability to integrate man-made reservoirs with existing infrastructure and mine rehabilitation programs further strengthens their appeal for large-scale energy storage deployment.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India represents a significant region in the pumped hydro storage market, leveraging its mountainous terrain and established hydropower infrastructure. The region's favorable topography and existing dam networks continue to attract substantial investment for both on-river and off-river pumped storage development.

West and Central India is emerging as a key hub for pumped hydro storage development, supported by favorable policies, strong institutional backing, and increasing private sector interest. Maharashtra is playing a pivotal role due to its supportive regulatory environment and proactive approach to long-duration energy storage, while Madhya Pradesh’s dedicated pumped hydro storage policy is further accelerating regional development momentum.

South India holds substantial pumped hydro storage potential, driven by progressive clean energy policies and extensive site identification efforts. Andhra Pradesh is leading regional development through its integrated clean energy framework, which promotes the deployment of large-scale storage solutions alongside renewable power generation. Karnataka and Tamil Nadu are also advancing pumped hydro initiatives, strengthening the region’s contribution to grid stability and renewable energy integration.

East India is steadily accelerating pumped hydro storage development, with Odisha and Bihar taking the lead through targeted state-level initiatives. Policy-driven project approvals and growing developer participation are positioning pumped hydro storage as a critical enabler of power system flexibility, supporting the region’s transition towards higher shares of renewable energy.

Market Dynamics:

Growth Drivers:

Why is the India Pumped Hydro Storage Market Growing?

Ambitious Renewable Energy Integration Targets Necessitating Large-Scale Storage

India's accelerating deployment of solar and wind power generation capacity has created an urgent need for large-scale, long-duration energy storage to manage grid intermittency and ensure reliable power supply during non-solar hours. As per IMARC Group, the India solar energy market size was valued at USD 30,032.78 Million in 2025 and is projected to attain USD 5,38,913.68 Million by 2034. Pumped hydro storage serves as the most established and cost-effective solution for grid-scale energy storage, offering unmatched reliability and scalability for long-duration applications. As India continues to expand its renewable energy portfolio towards ambitious clean energy targets, pumped storage infrastructure is increasingly recognized as indispensable for maintaining grid frequency stability, managing peak demand fluctuations, and enabling the seamless integration of variable renewable energy generation into the national electricity grid.

Proactive Government Policies and Streamlined Regulatory Frameworks

The Indian government has introduced a comprehensive suite of policy measures and regulatory reforms specifically designed to accelerate pumped hydro storage development. The Ministry of Power issued guidelines in April 2023 promoting competitive bidding, concessional land rates, and waiver of interstate transmission charges for pumped storage projects. These measures have been further strengthened by the inclusion of pumped hydro storage under Energy Storage Obligation targets requiring utilities to source an increasing proportion of renewable energy through storage systems. The Central Electricity Authority has dramatically reduced project approval timelines through portal-based transparent processing and streamlined detailed project report formats. Additionally, the government has simplified environmental clearance procedures by creating a separate category for standalone pumped storage projects, distinguishing them from conventional hydroelectric projects and reducing compliance burdens for developers seeking rapid project execution.

Surging Private Sector Investments and Capacity Commitments

The India pumped hydro storage market is experiencing unprecedented private sector participation, with major energy corporations committing substantial capital to develop large-scale projects across multiple states. Three leading private developers, Greenko, Adani, and JSW alone are set to deliver nearly two-thirds of India's planned 51 GW pumped storage capacity by 2032, representing a more than tenfold expansion from the current installed base. This massive private investment is complemented by public sector initiatives, with entities such as NHPC and state power corporations actively developing additional projects across diverse geographies. The strong investor interest is driven by favorable internal rates of return, the long operational lifespan of pumped storage plants, and the growing recognition of these projects as essential grid infrastructure. Companies are actively securing development agreements with state governments, establishing memoranda of understanding for site access, and deploying advanced engineering capabilities to fast-track project commissioning timelines and capture early-mover advantages in this rapidly expanding sector.

Market Restraints:

What Challenges the India Pumped Hydro Storage Market is Facing?

Complex Land Acquisition and Environmental Clearance Processes

Land acquisition remains one of the most significant hurdles for pumped hydro storage deployment in India. Projects are frequently located in or near sensitive forested areas, necessitating extensive resettlement and rehabilitation of local communities. Environmental and forest clearance processes, despite reforms, continue to involve multiple regulatory agencies and can create substantial delays. The requirement to construct two reservoirs at different elevations intensifies land-related conflicts and opposition from affected communities and environmental groups.

High Upfront Capital Requirements

Pumped hydro storage projects face a major challenge due to their high upfront capital requirements, as significant investment is needed well before revenue generation begins. These projects involve substantial civil works, advanced electromechanical equipment, and detailed geological and engineering studies, which increase initial costs. As a result, participation is largely limited to well-capitalized developers, while financing and risk perception remain key hurdles.

Geographic and Geological Site Constraints

Pumped hydro storage requires specific topographical conditions, including adequate elevation differences between reservoirs and geologically stable terrain. Suitable sites are concentrated in hilly and mountainous regions, limiting deployment flexibility compared to battery energy storage systems that can be installed virtually anywhere. Many identified sites face challenges related to water availability during non-monsoon periods, seismic sensitivity, and accessibility constraints that increase construction costs and project complexity.

Competitive Landscape:

The India pumped hydro storage market is characterized by intensifying competition among both private and public sector entities as they race to secure project development rights across high-potential states. Companies are focusing on establishing strategic partnerships with state governments, investing in advanced turbine technologies, and expanding their project pipelines to capture a significant share of the planned capacity additions. Competition is further shaped by the ability to secure environmental clearances efficiently, demonstrate financial viability through competitive bidding, and commission projects within targeted timelines. Collaborations between domestic developers and international technology providers are fostering innovation in variable-speed systems and engineering solutions, enhancing operational efficiency and project bankability.

Recent Developments:

- In April 2025, Avaada Group signed a memorandum of understanding with Maharashtra's Water Resources Department to develop two pumped storage projects with a combined capacity of 3,650 MW. The 2400 MW Pawana Falyan and 1200 MW Sirsala projects represented a cumulative investment of INR 15,100 Crores and are expected to create more than 3,800 direct employment opportunities.

India Pumped Hydro Storage Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Open-Loop, Closed-Loop |

| Sources Covered | Natural Reservoirs, Man-Made Reservoirs |

| Regions Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Pumped Hydro Storage Market Research Report and Industry Forecast Report

The India pumped hydro storage market size was valued at USD 13.26 Billion in 2025.

The India pumped hydro storage market is expected to grow at a compound annual growth rate of 7.92% from 2026-2034 to reach USD 26.32 Billion by 2034.

Closed-loop dominated the market with a share of 56%, driven by its minimal environmental impact, independence from natural river systems, faster regulatory approvals, and growing preference among developers for off-stream configurations.

Key factors driving the India pumped hydro storage market include ambitious renewable energy integration targets, proactive government policy reforms, streamlined regulatory approvals, surging private sector investment, rising grid stability requirements, and expanding state-level development frameworks.

Major challenges include complex land acquisition processes, environmental clearance delays, high upfront capital requirements, long project gestation periods, geographic site constraints, water availability concerns, and limited specialized workforce for pumped storage engineering.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)