India School Market Size, Share, Trends and Forecast by Level of Education, Ownership, Board of Affiliation, Fee Structure, and Region 2026-2034

India School Market Size, Share, Trends & Forecast (2026-2034)

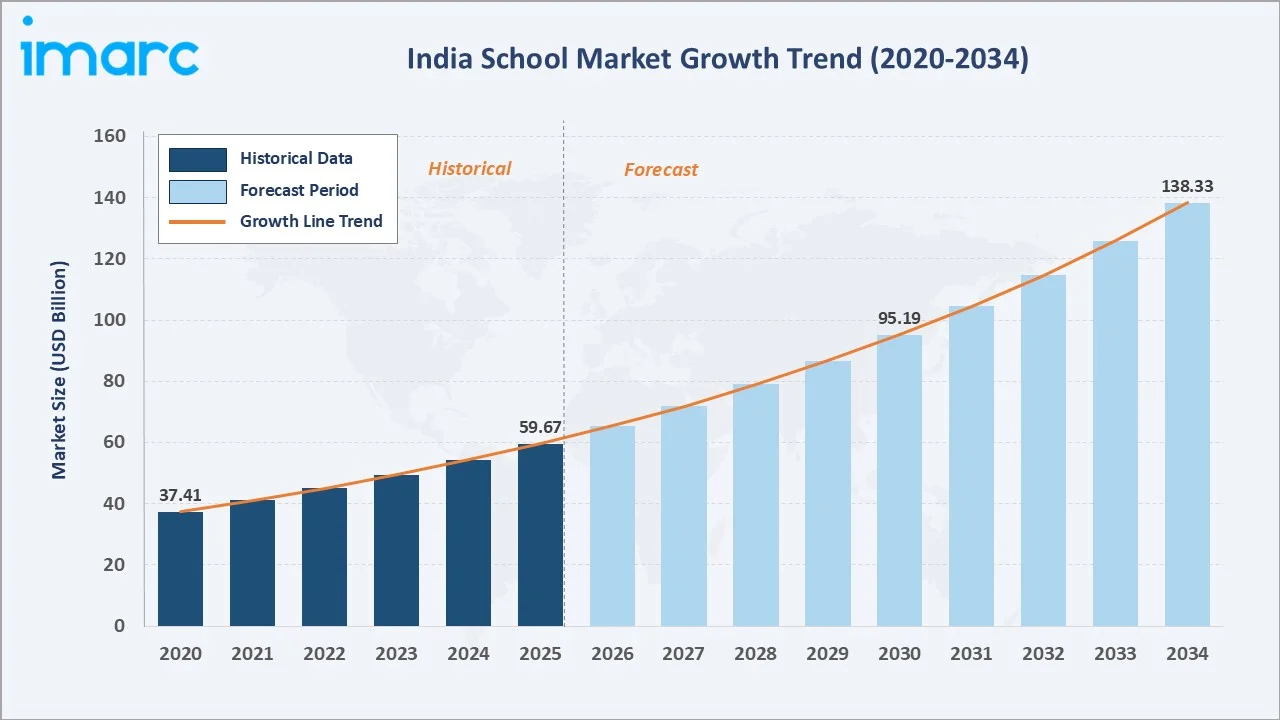

The India school market size reached USD 59.67 Billion in 2025 and is projected to reach USD 138.33 Billion by 2034, growing at a CAGR of 9.79% during 2026-2034. The market is driven by demographic expansion, education policy reforms under NEP 2020, rising household income, government digital infrastructure investment, and sustained public spending on school access and quality improvement.

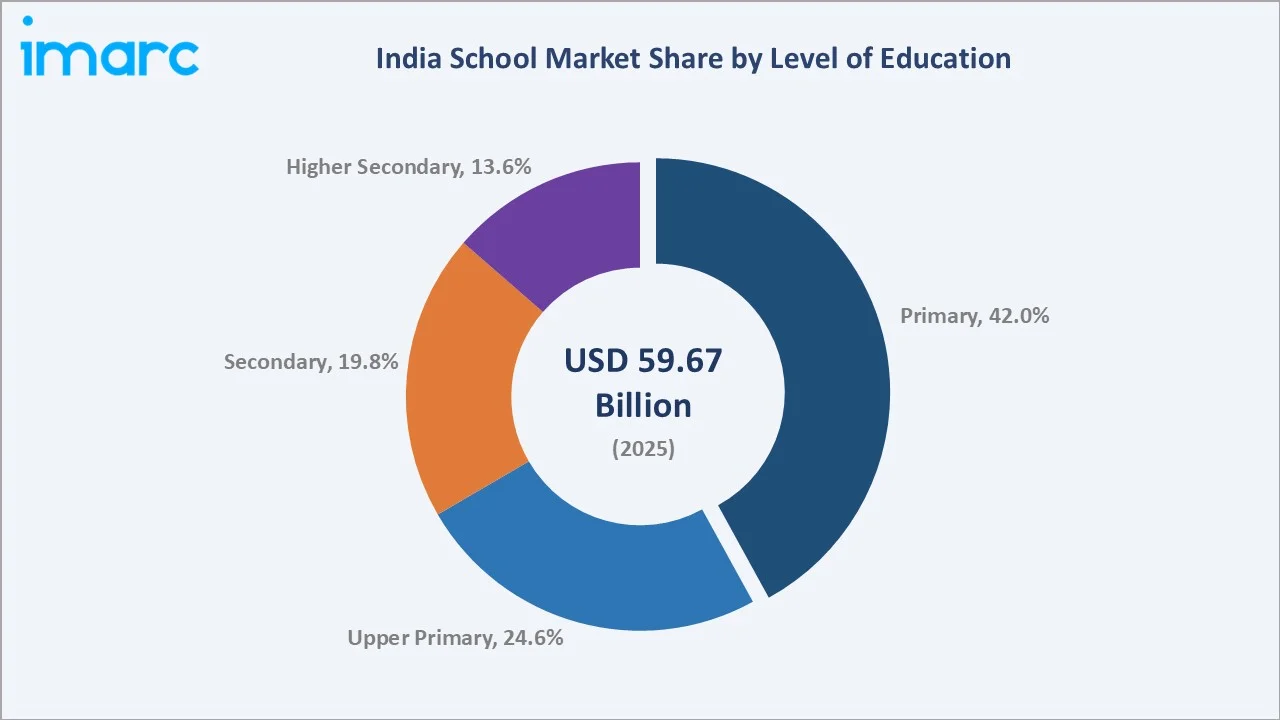

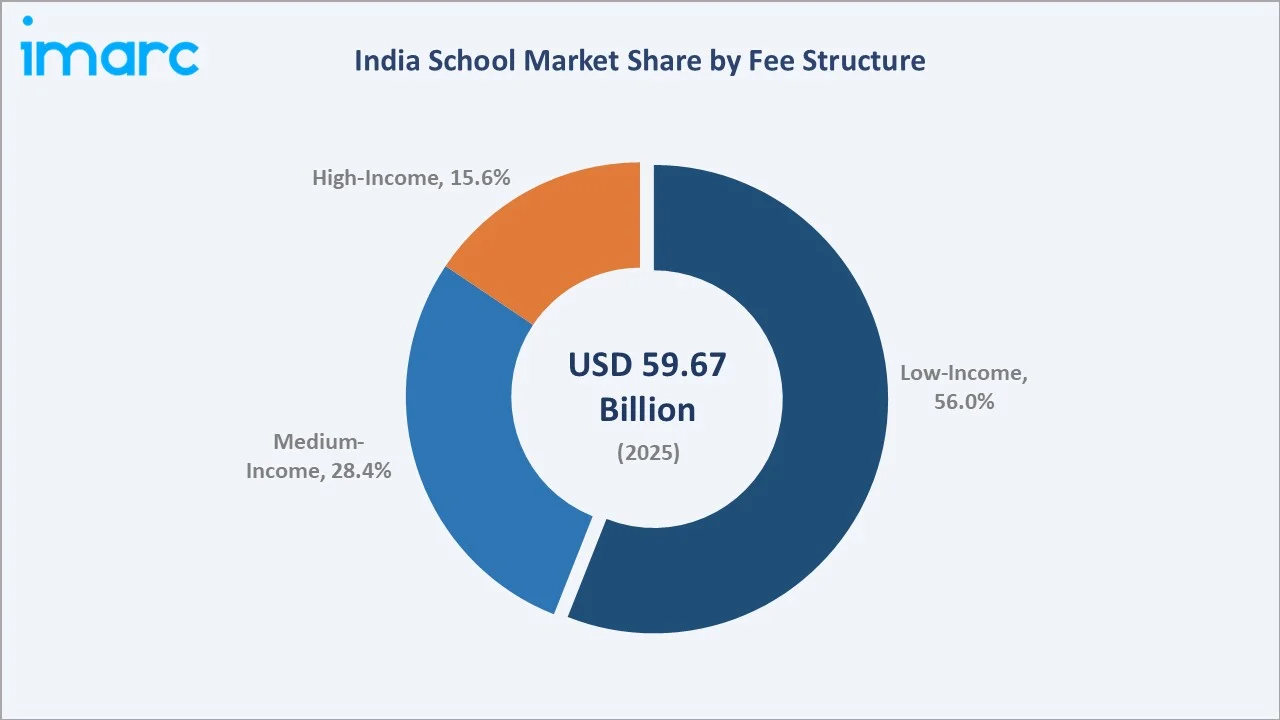

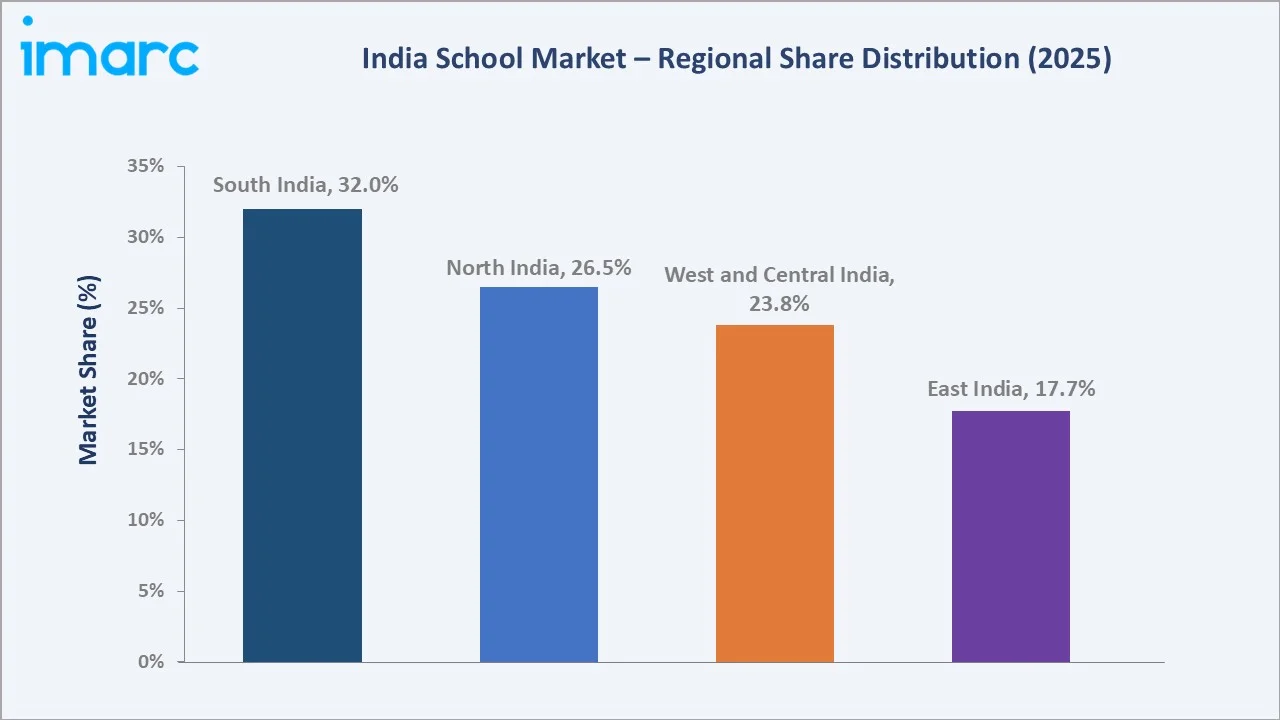

The Primary segment dominates at 42.0%. Low-income fee structure leads at 56.0%. South India commands 32.0% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 59.67 Billion |

|

Forecast Market Size (2034) |

USD 138.33 Billion |

|

CAGR (2026-2034) |

9.79% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Level of Education |

Primary (42.0%, 2025) |

|

Dominant Fee Structure |

Low-Income (56.0%, 2025) |

|

Leading Region |

South India (32.0%, 2025) |

The market expanded from USD 37.41 Billion in 2020 to USD 59.67 Billion in 2025, anchored at USD 95.19 Billion in 2030 and forecast to reach USD 138.33 Billion by 2034. Rising parental aspirations, NEP 2020 reforms, and digital infrastructure upgrades are sustaining above-average growth through the forecast period.

To get more information on this market, Request Sample

The Primary level at 42.0% and Low-income fee structure at 56.0% reflect the market's fundamental structure as a predominantly government-operated system. The High-income fee structure segment grows fastest at approximately 12–14% CAGR as urbanization and income growth expand the addressable premium school market.

Executive Summary

The India school market reached USD 59.67 Billion in 2025, driven by the country's vast student population, policy-driven universal access mandates, and growing private sector participation in premium and technology-enabled education delivery. The market is projected to reach USD 138.33 Billion by 2034.

The Primary segment at 42.0% dominates by capturing the largest enrollment base, supported by the Right to Education Act and government midday meal schemes. Low-income fee structure at 56.0% leads through free and subsidized government school provision.

South India at 32.0% leads nationally through higher literacy rates, proactive state governments, and superior school infrastructure.

Key Market Insights

|

Insight |

Data |

|

Dominant Level of Education |

Primary – 42.0% share (2025) |

|

Dominant Fee Structure |

Low-Income – 56.0% market share (2025) |

|

Leading Region |

South India – 32.0% market share (2025) |

|

Market Opportunity |

NEP 2020 implementation; digital classrooms; private school chain expansion; international board schools; EdTech integration |

Key Analytical Observations Supporting The Above Data:

- Primary at 42.0%: The Primary segment dominates as India's largest enrollment tier, reinforced by compulsory education mandates, government midday meal programs, and Samagra Shiksha infrastructure support, creating the foundation for sustained school market revenue growth.

- Low-Income at 56.0%: Government schools serving economically weaker households represent most of the India's school market, supported by free tuition, uniforms, textbooks, and meals, sustaining mass enrollment across rural and semi-urban geographies.

- South India at 32.0%: South Indian states – Tamil Nadu, Karnataka, Kerala, Andhra Pradesh, and Telangana – lead through higher literacy rates, well-developed private school ecosystems, proactive state education policies, and greater household spending on quality schooling.

India School Market Overview

The India school market encompasses all formal K-12 education institutions including government, government-aided, and private unaided schools across primary, upper primary, secondary, and higher secondary levels affiliated with CBSE, CISCE, and state boards across all 28 states and 8 union territories.

The ecosystem integrates government ministries, state education departments, school management committees, curriculum developers, educational publishers, EdTech providers, infrastructure developers, teacher training institutes, and examination boards. Macroeconomic factors include demographic growth, urbanization, disposable income rise, and public education spending.

Market Dynamics

To evaluate market opportunities, Request Sample

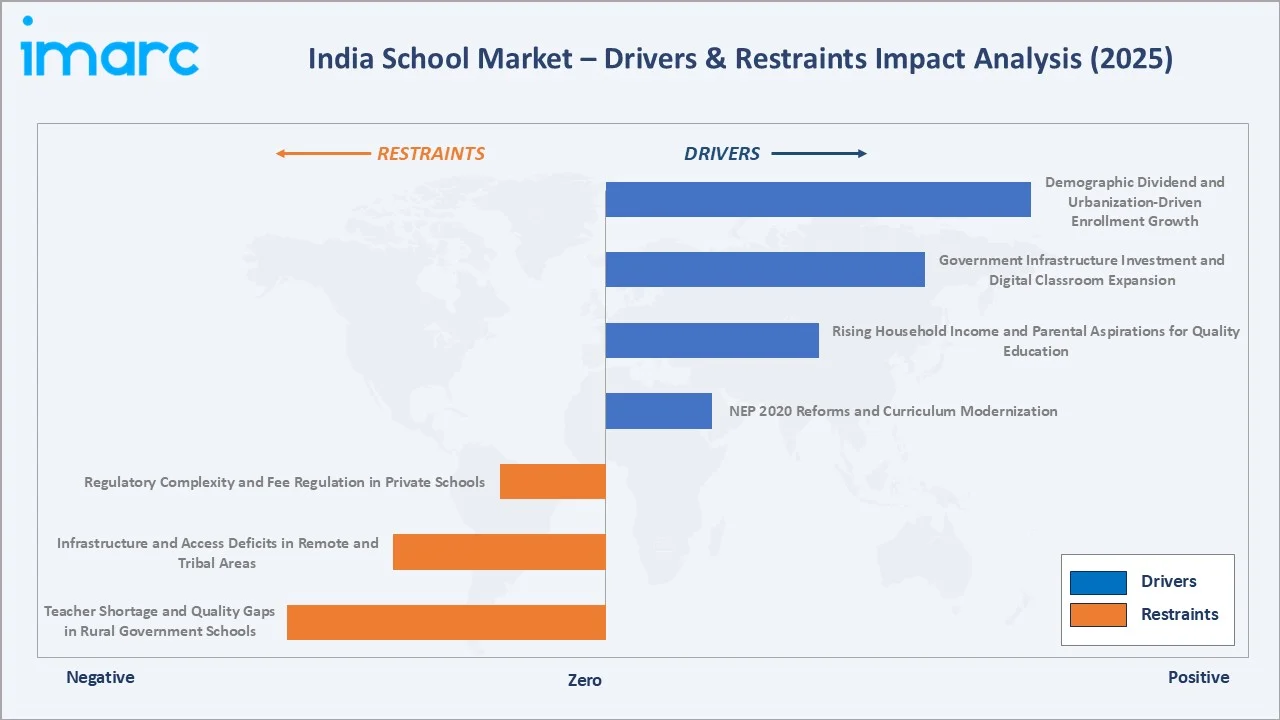

Market Drivers

- NEP 2020 Reforms and Curriculum Modernization: National Education Policy 2020 is driving comprehensive curriculum transformation, foundational literacy-numeracy focus, and pedagogical innovation across India's school system. Restructuring the school system from the 10+2 format to a 5+3+3+4 structure is increasing enrollment at the foundational and preparatory stages, boosting overall school market participation and spending by government and private operators.

- Rising Household Income and Parental Aspirations for Quality Education: Growing middle-class incomes are raising household education spending as parents increasingly prioritize quality schooling with strong academic outcomes. Families are transitioning children from government to private schools, increasing enrollment in CBSE-affiliated and international schools, and investing in supplementary private tuition, collectively expanding the India school market revenue base.

- Government Infrastructure Investment and Digital Classroom Expansion: Sustained public investment in school construction, smart classrooms, broadband connectivity under BharatNet, and PM e-VIDYA is upgrading school infrastructure quality. Digital classroom programs including installation of smart boards and interactive learning tools are improving retention, improving learning outcomes, and increasing the perceived value of formal schooling nationally.

- Demographic Dividend and Urbanization-Driven Enrollment Growth: India's large youth population aged 6–17 years numbering approximately 250 million students sustains structurally high school enrollment demand. Accelerating urbanization is concentrating school-age populations in cities and tier-2 towns, supporting private school expansion and increasing per-student revenue as urban families exhibit higher willingness to pay for premium schooling.

Market Restraints

- Teacher Shortage and Quality Gaps in Rural Government Schools: Acute shortfall of trained and qualified teachers in rural government schools undermines education quality and parental confidence in public education. Poor student-teacher ratios, absenteeism, and inadequate subject expertise at the secondary level particularly constrain quality delivery, limiting market formalization and fee-paying enrollment growth in underserved geographies.

- Infrastructure and Access Deficits in Remote and Tribal Areas: Inadequate school infrastructure in remote, hilly, and tribal areas including lack of secondary and higher secondary schools within accessible distance increases dropout rates and restricts market expansion. Transportation barriers limited female enrollment, and low economic capacity of households reduce addressable private school market potential in these areas.

- Regulatory Complexity and Fee Regulation in Private Schools: Fee regulation laws enacted by multiple state governments restrict private school operators from freely adjusting tuition to recover infrastructure and quality investment costs. Regulatory unpredictability and compliance burdens increase operational costs and deter institutional investment in school network expansion, limiting private sector market growth capacity.

Market Opportunities

- International Curriculum School Expansion: Rising demand from upper-middle-class and expatriate families for IB, Cambridge (IGCSE/A-Level), and British curriculum schools is creating significant investment opportunities in metropolitan and tier-1 cities. Premium residential school campuses offering global curricula with boarding facilities command high fee realizations, supporting above-market revenue growth for developers and education operators.

- EdTech Integration and Hybrid Learning Models: Integration of EdTech platforms within school infrastructure for adaptive learning, AI-based personalized content, and digital assessment is creating new revenue streams for schools and technology providers. Hybrid learning partnerships between schools and technology companies are expanding reach and quality, particularly in tier-2 and tier-3 cities.

Market Challenges

- High Private School Attrition During Economic Downturns: Private school enrollment is vulnerable to household income shocks that shift families back to government schools during economic slowdowns, creating revenue volatility for fee-dependent private school operators. Maintaining enrollment during periods of income stress represents a structural challenge for low- and mid-tier private schools without government funding support.

- Digital Divide Limiting EdTech-Augmented School Delivery: Persistent digital infrastructure gaps between urban and rural schools limit equitable adoption of technology-augmented learning. Students in low-connectivity regions are unable to benefit from digital classroom investments, creating a two-tier education quality system that constrains the overall market's quality standardization and premium repositioning potential.

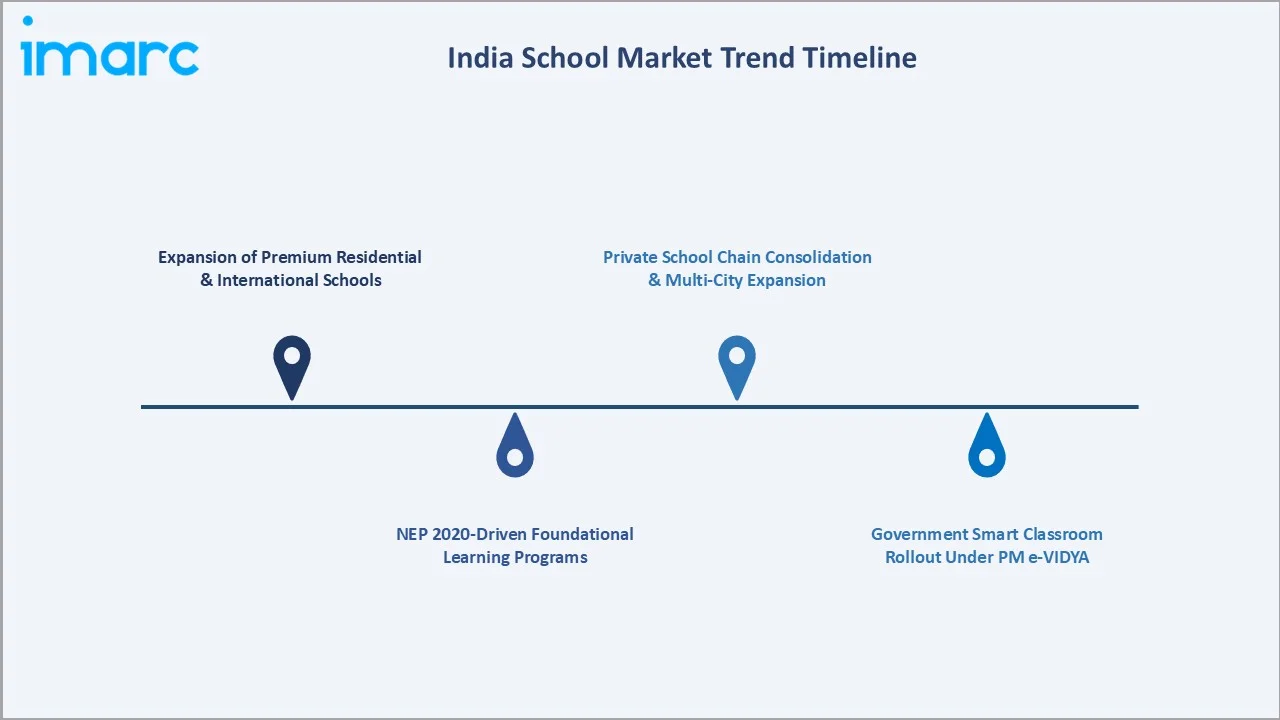

Emerging Market Trends

1. Expansion of Premium Residential and International Schools

Growing demand from aspirational families and NRI households for world-class residential schooling is driving investment in premium campus infrastructure across tier-1 and tier-2 cities. Institutions offering IB or Cambridge curricula with boarding, sports, and arts facilities are expanding rapidly, supported by institutional investors and education-focused private equity funding.

2. NEP 2020-Driven Foundational Learning Programs

National Education Policy 2020 mandates are accelerating adoption of play-based and activity-driven foundational learning programs for ages 3–8 years. Government and private schools are redesigning early childhood curriculum, creating demand for specialized teachers, learning materials, and assessment tools.

3. Government Smart Classroom Rollout Under PM e-VIDYA

The increasing adoption of smart classrooms, digital boards, and internet-enabled learning infrastructure through central and state-led education initiatives is accelerating the modernization of school education across India. Ongoing investments in digital teaching tools and classroom technology are enhancing access to interactive learning, supporting curriculum delivery, and strengthening the implementation of digital education across government schools.

4. Private School Chain Consolidation and Multi-City Expansion

Organized private school chains are consolidating fragmented private school markets through multi-city expansion and brand standardization. Franchise and partnership models allow rapid geographic scaling, improving operational efficiency and enabling brand-conscious parents to access standardized quality at accessible fee points. The top private school chains are targeting tier-2 cities where rising incomes and limited quality schooling options create strong enrollment demand.

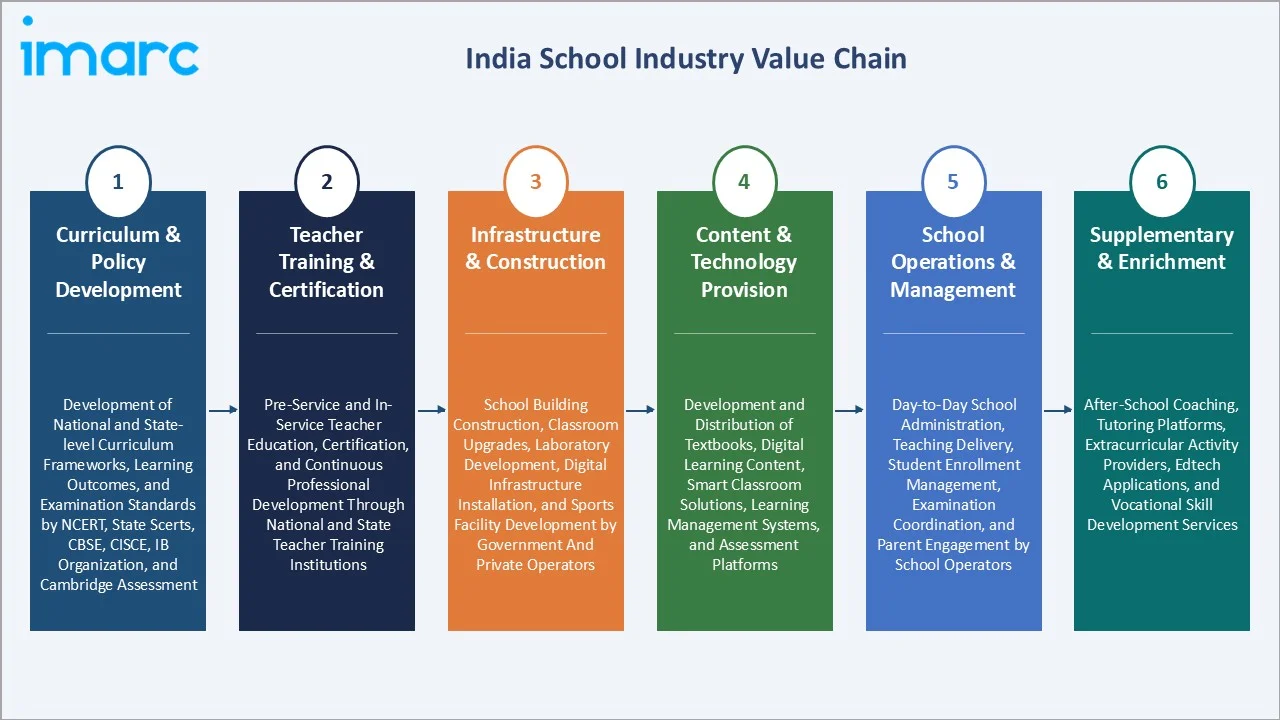

Industry Value Chain Analysis

The India school education value chain integrates curriculum development, teacher training, school infrastructure construction, content publishing, school operations management, supplementary education, and examination administration, with EdTech platforms increasingly embedded across multiple stages.

|

Stage |

Key Activities |

|

Curriculum & Policy Development |

Development of national and state-level curriculum frameworks, learning outcomes, and examination standards by NCERT, state SCERTs, CBSE, CISCE, IB Organization, and Cambridge Assessment |

|

Teacher Training & Certification |

Pre-service and in-service teacher education, certification, and continuous professional development through national and state teacher training institutions |

|

Infrastructure & Construction |

School building construction, classroom upgrades, laboratory development, digital infrastructure installation, and sports facility development by government and private operators |

|

Content & Technology Provision |

Development and distribution of textbooks, digital learning content, smart classroom solutions, learning management systems, and assessment platforms |

|

School Operations & Management |

Day-to-day school administration, teaching delivery, student enrollment management, examination coordination, and parent engagement by school operators |

|

Supplementary & Enrichment Services |

After-school coaching, tutoring platforms, extracurricular activity providers, EdTech applications, and vocational skill development services |

The curriculum and policy development tier is the India school value chain's most strategically significant stage as NCERT and state SCERTs define learning outcomes for most enrolled students. The content and technology tier is experiencing the most rapid transformation as EdTech platforms displace traditional textbook-only instruction across both government and private school segments.

Technology Landscape in the India School Industry

Smart Classroom and Interactive Whiteboard Technology

Smart classroom technologies including interactive whiteboards, digital projectors, and connected tablets are being deployed across government and private schools under national programs. These tools improve lesson interactivity, enable multimedia content delivery, and support differentiated instruction, raising school quality perception and student engagement at scale across metropolitan and tier-2 city schools.

Adaptive Learning and AI-Powered EdTech Platforms

AI-driven adaptive learning platforms are personalizing instruction by analyzing student performance data and dynamically adjusting content difficulty. Integration of these platforms within school curricula supports teachers, identifies learning gaps early, and improves academic outcomes. Schools partnering with EdTech companies are differentiating on technology-augmented teaching quality, particularly at the secondary and higher secondary levels.

Learning Management Systems and Digital Assessment

Cloud-based Learning Management Systems and digital assessment tools are replacing paper-based testing and manual record-keeping across private schools and progressive government schools. These platforms enable continuous formative assessment, automated progress reporting, and parent communication, improving operational efficiency and education quality transparency for fee-paying school customers across India.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Level of Education |

Primary |

42.0% |

2025 |

|

Ownership |

Government |

63.0% |

2025 |

|

Board of Affiliation |

State Government Boards |

62.0% |

2025 |

|

Fee Structure |

Low-Income |

56.0% |

2025 |

|

Region |

South India |

32.0% |

2025 |

By Level of Education

The Primary segment leads at 42.0% in 2025, representing the largest and most universally enrolled education tier in India, anchored by the Right to Education Act mandating free and compulsory education for ages 6–14 and sustained government funding under Samagra Shiksha.

To access detailed market analysis, Request Sample

Upper Primary at 24.6% reflects high enrollment maintained through midday meal programs and government scholarship schemes. Secondary at 19.8% and Higher Secondary at 13.6% show lower shares due to dropout rates linked to economic constraints, representing high-growth opportunity segments as retention improves under NEP 2020 foundational and preparatory stage reforms.

By Fee Structure

The Low-income fee structure leads at 56.0% in 2025, driven by India's extensive government school network providing free or nominally priced education to economically weaker sections, reflecting the market's fundamental structure as a predominantly public education system serving most Indian students.

Medium-income at 28.4% captures the growing private school segment serving aspirational middle-class households seeking CBSE or state-board education at accessible fee levels. High-income at 15.6% reflects premium private, international, and residential school enrolment, the fastest-growing fee tier as urbanization and income growth expands the addressable premium market.

Regional Market Insights

|

Region |

Share (2025) |

Key School Market Drivers & Characteristics |

|

South India |

32.0% |

High literacy rates, proactive state education policies, strong private school ecosystem, and greater household spending on quality schooling drive market leadership |

|

North India |

26.5% |

Large student population across Uttar Pradesh, Delhi, and Rajasthan; rapid private school growth; CBSE dominance; and rising middle-class enrollment drive the market |

|

West and Central India |

23.8% |

Maharashtra and Gujarat drive premium school demand through corporate education investment and urban middle-class income growth |

|

East India |

17.7% |

Growing enrollment base in West Bengal and Odisha; increasing government investment under Samagra Shiksha; lower but improving private school penetration |

South India, at 32.0%, leads through Tamil Nadu, Karnataka, Kerala, Andhra Pradesh, and Telangana's combined strengths in school infrastructure, higher enrollment completion rates at secondary level, and above-average private school density. North India, at 26.5%, reflects the large student population across Uttar Pradesh, Delhi, and Rajasthan, with rapid private school expansion in tier-2 cities.

West and Central India, at 23.8%, is driven by Maharashtra and Gujarat's urban premium private school market and corporate school operator investment. East India, at 17.7%, represents an emerging growth region as government investment under Samagra Shiksha and improving access to secondary schools narrows historical infrastructure gaps and increases private school penetration.

Competitive Landscape

The India school market competitive landscape is highly fragmented, with government-operated institutions holding majority enrollment share and a growing organized private sector led by school chains, international franchise operators, and technology-augmented private school networks competing across metropolitan, tier-1, and tier-2 cities.

|

Company Name |

Key Offerings |

Market Position |

Core Strength |

|

K12 Techno Services Pvt. Ltd. |

K-12 CBSE schools, activity-based learning curriculum |

Market Leader |

India's largest private K-12 school chain by campus count with experiential learning curriculum |

|

VIBGYOR Group of Schools |

VIBGYOR High, VIBGYOR Rise |

Strong Challenger |

Premium CBSE school chain focused on holistic development and metro city locations with strong co-curricular differentiation |

|

Ryan Group |

K-12 CBSE and ICSE schools |

Established Player |

One of India's oldest private school groups with multi-city footprint and strong brand recognition across multiple states |

|

Pathways Schools |

IB continuum schools, PYP/MYP/DP |

Emerging Player |

Premium international curriculum school chain serving India's upper-income and expatriate segment with IB continuum delivery |

Key players include K12 Techno Services Pvt. Ltd., VIBGYOR Group of Schools, Ryan Group, Pathways Schools, and others.

Key Company Profiles

K12 Techno Services Pvt. Ltd.

K12 Techno Services Pvt. Ltd. working through Orchids-The International School is an India-based K-12 private school chain operating one of India's largest networks of CBSE and ICSE-affiliated schools, with a focus on activity-based, experiential learning and holistic student development across metropolitan and tier-2 cities.

- Key Products: K-12 CBSE schools, activity-based learning curriculum

- Strategic Focus: Scaling multi-city franchise model, integrating adaptive learning technology, and expanding into tier-2 and tier-3 cities to capture India's growing private school demand from aspirational middle-class families.

VIBGYOR Group of Schools

VIBGYOR Group of Schools is an India-based premium CBSE, ICSE/ISC school operator with campuses concentrated in metropolitan cities including Mumbai, Bengaluru, Pune, and others, focused on delivering holistic education with strong co-curricular emphasis.

- Key Products: VIBGYOR High, VIBGYOR Rise

- Strategic Focus: Premium holistic school positioning in top metropolitan cities, co-curricular differentiation, and phased adoption of NEP 2020 foundational learning frameworks across all campuses.

Market Concentration Analysis

The India school market is highly fragmented at the national level, with government-operated institutions accounting for approximately 60–65% of total enrolment and revenue, and no single private operator controlling more than 1–2% of the national market. The top 10 organized private school chains collectively account for an estimated 3–5% of total private school market revenue. Market concentration is increasing gradually over the forecast period as private equity-backed school chains expand through franchise models, but the sheer scale of India's school system limits the pace of consolidation through 2034.

Investment & Growth Opportunities

Highest Growth Segments

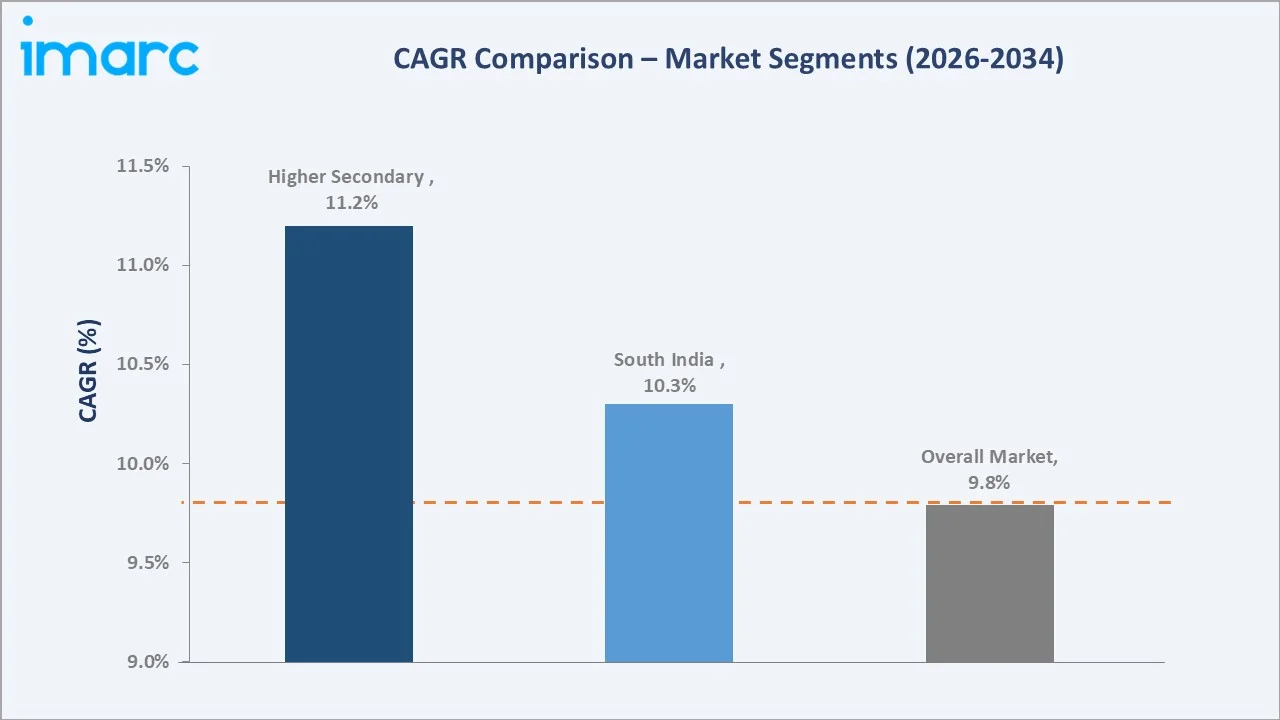

High-income fee structure (~12–14% CAGR), international curriculum schools (~15–18% CAGR from small base), EdTech-integrated private schools (~13% CAGR), premium residential schools (~15% CAGR), Higher Secondary segment (~11% CAGR as retention improves under NEP 2020), and South and West India private school market expansion represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

International board school expansion (IB, Cambridge, British) represents the India school market's highest per-student revenue emerging opportunity. IB and Cambridge school fee structures of USD 5,000–20,000 per year generate 5–15x the fee revenue of standard CBSE schools, with European and British school operators actively seeking Indian franchise or joint venture partnerships for campus development in major cities.

Investment Themes

- Private equity school chain roll-up targeting India's fragmented mid-market private CBSE school segment, acquiring single-school operators in growing tier-2 cities and standardizing curriculum, brand, and technology to capture India's aspirational middle-class education spending.

- EdTech-school hybrid model investment, developing AI-adaptive learning-integrated school networks for the mass-market fee segment, combining physical campus delivery with digital personalization to improve academic outcomes at scale and differentiate from traditional school operators.

Future Market Outlook (2026-2034)

The India school market is projected to grow from USD 59.67 Billion in 2025 to USD 138.33 Billion by 2034, delivering a 9.79% CAGR over the forecast period. NEP 2020 implementation will reshape curriculum delivery, foundational learning, and vocational integration, driving quality investment by both government and private operators. South India's school market lead is expected to sustain through the forecast, while North India narrows the gap through rapid private school growth in Uttar Pradesh and Rajasthan.

Three structural forces define India school market growth through 2034 with high confidence. Universal secondary education access improvement reduces dropout rates and increases market revenue per enrolled student. Private school chain consolidation creates above-market revenue growth for organized operators capturing fragmented single-school market share. International curriculum adoption by aspirational middle-class households creates a premium fee tier expanding faster than overall market CAGR, driving revenue mix upgrade across the India school market through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including school principals; state education department officials; private school chain operators; EdTech platform executives; curriculum developers; and parent focus groups across major Indian metros and tier-2 cities.

Secondary Research

Secondary research encompassed Ministry of Education UDISE+ database; NCERT annual reports; state government education department publications; CBSE and CISCE enrollment statistics; World Bank India education reports; ASER rural education surveys; private equity education sector investment reports 2025; India school market analysis 2024–2025. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using enrollment-based bottom-up model: (i) total school-age population forecast by level of education; (ii) estimated enrollment ratio by level; (iii) estimated average fee per enrolled student by fee tier; (iv) government expenditure per student multiplied by government school enrollment; (v) private school fee revenue model combining enrollment, fee level, and school type distribution.

India School Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Levels of Education Covered | Primary, Upper Primary, Secondary, Higher Secondary |

| Ownership Covered | Government, Local Body, Private Aided, Private Unaided |

| Board of Affiliation Covered | Central Board of Secondary Education, Council for the Indian School Certificate Examinations, State Government Boards, Others |

| Fee Structure Covered | Low-Income, Medium-Income, High-Income |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | K12 Techno Services Pvt. Ltd., VIBGYOR Group of Schools, Ryan Group, Pathways Schools, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India School Market Report

The India school market reached USD 59.67 Billion in 2025, driven by the Primary segment's dominance at 42.0%, Low-income fee structure at 56.0%, South India's regional leadership at 32.0%, and sustained government and private investment in school quality and infrastructure.

The India school market grows at 9.79% CAGR during 2026-2034, reaching USD 138.33 Billion by 2034, reflecting NEP 2020-driven quality investment, private school expansion, and increasing household education spending.

Primary level leads at 42.0%, supported by compulsory education mandates, government funding, and the largest student enrollment base nationwide, sustained by Right to Education Act provisions and Samagra Shiksha infrastructure investment.

Low-income fee structure leads at 56.0% through India's extensive government school network providing free or subsidized education to most enrolled students, reflecting the market's predominantly public education structure.

South India leads at 32.0% through high literacy rates, strong private school ecosystems, proactive state education policies, and above-average household education spending across Tamil Nadu, Karnataka, Kerala, Andhra Pradesh, and Telangana.

Leading companies include K12 Techno Services Pvt. Ltd., VIBGYOR Group of Schools, Ryan Group, Pathways Schools, and others.

The India school market is projected to reach approximately USD 95.19 Billion by 2030, driven by NEP 2020 implementation, private school expansion, digital infrastructure upgrades, and continued enrollment growth at secondary and higher secondary levels.

Three priority investment opportunities: premium international curriculum school development, private equity-backed mid-market CBSE school chain consolidation in tier-2 cities, and EdTech-integrated hybrid school models combining physical delivery with AI-adaptive personalization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)