India Semiconductor Market Size, Share, Trends and Forecast by Components, Material Used, End User, and Region, 2026-2034

India Semiconductor Market Size, Share, Trends & Forecast (2026-2034)

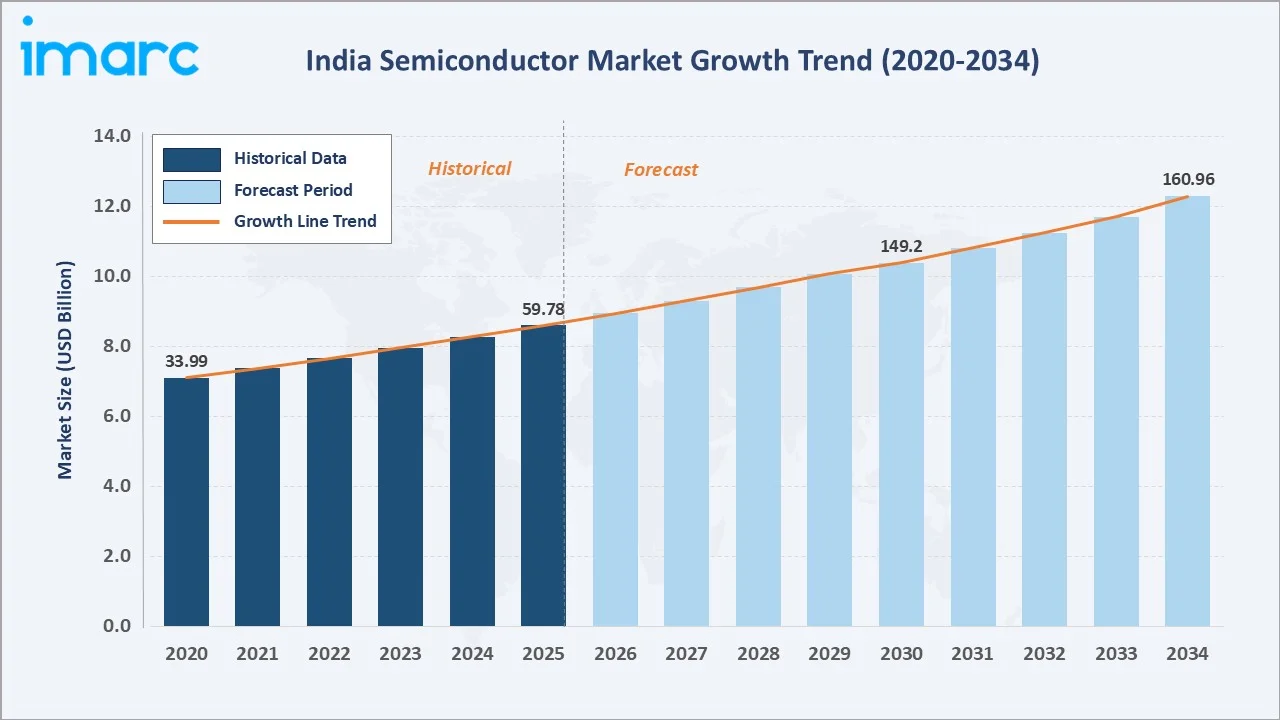

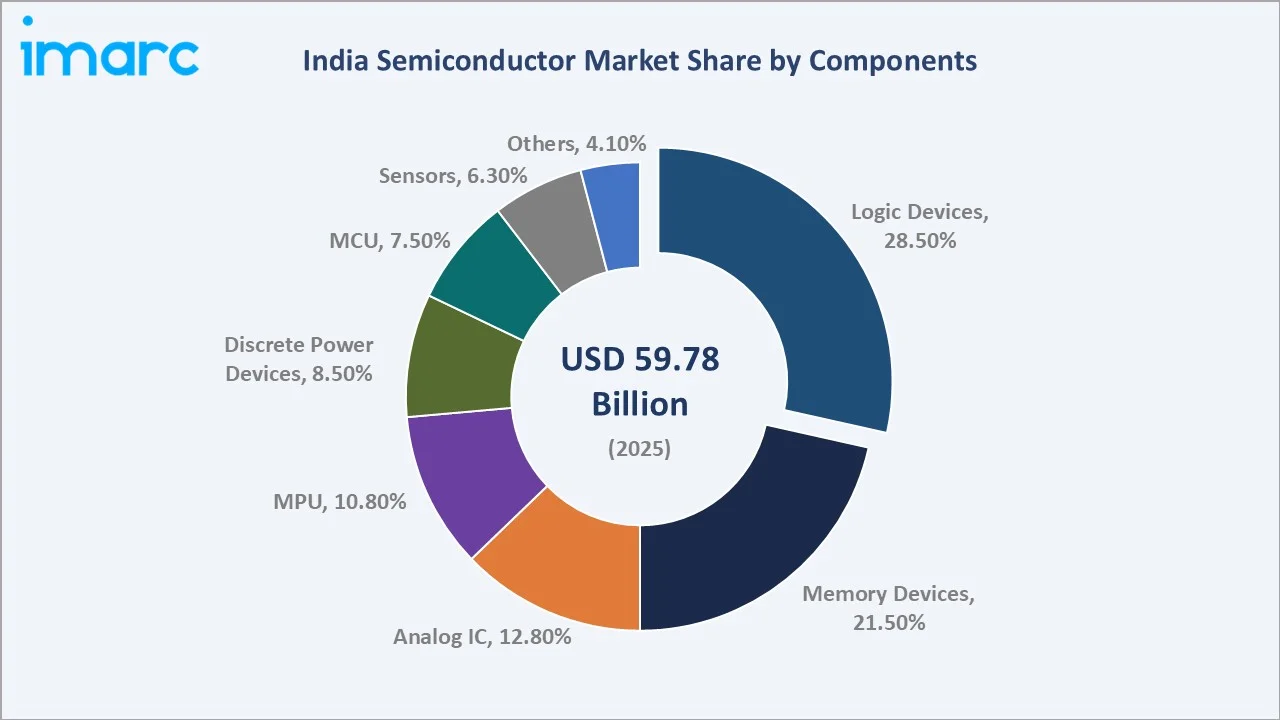

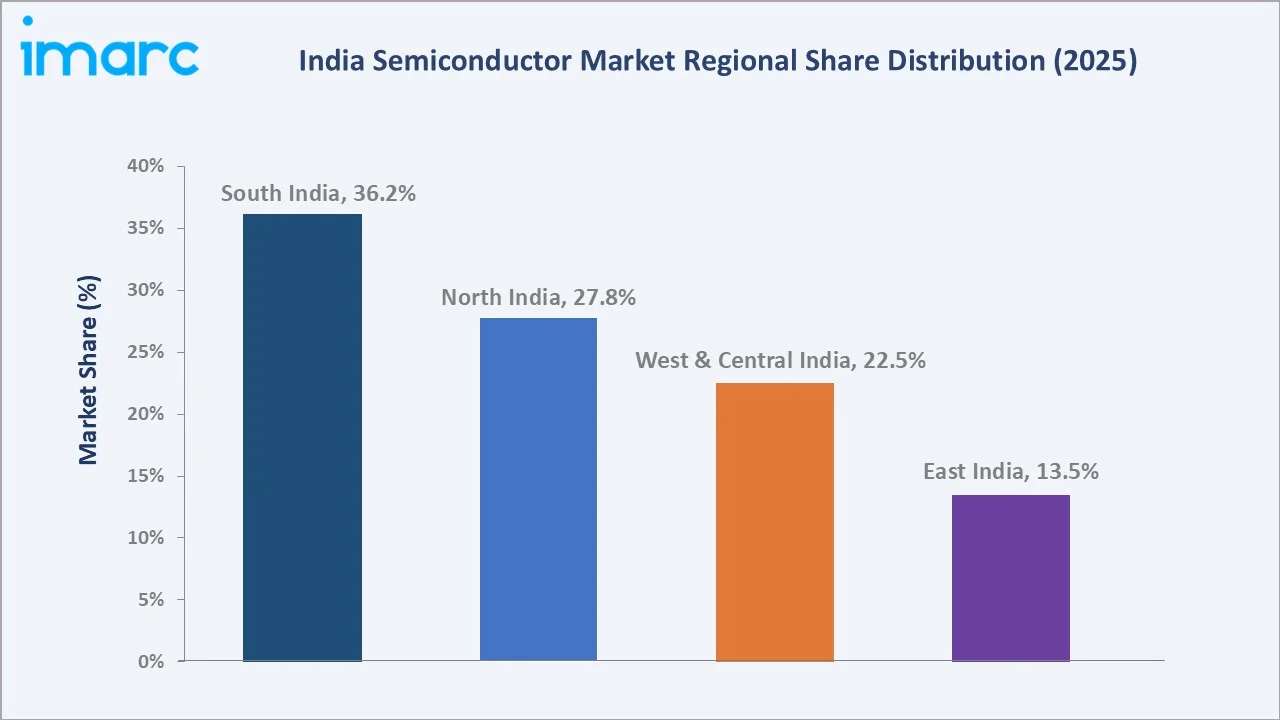

The India semiconductor market was valued at USD 59.78 Billion in 2025 and is projected to reach USD 180.20 Billion by 2034, exhibiting a CAGR of 11.95% during the forecast period (2026-2034). Robust government-backed initiatives such as the Production Linked Incentive (PLI) and Design Linked Incentive (DLI) schemes, combined with surging demand from 5G, electric vehicles (EVs), artificial intelligence (AI), and the Internet of Things (IoT), are collectively fueling the India semiconductor market growth. Consumer electronics leads end-user demand at 30.4% of total market share (2025), closely followed by the automotive sector at 16.2%. From a components perspective, logic devices dominate at 28.5%. South India remains the largest regional contributor, accounting for 36.2% of domestic revenues in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 59.78 Billion |

|

Forecast Market Size (2026-2034) |

USD 180.20 Billion |

|

CAGR (2026-2034) |

11.95% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Component Segment |

Logic Devices (28.5% share, 2025) |

|

Largest End-User Segment |

Consumer Electronics (30.4% share, 2025) |

|

Dominant Region |

South India (36.2% share, 2025) |

|

Fastest Growing Region |

West & Central India |

The India semiconductor market growth trajectory from 2020 through 2034, contrasting the historical base with the strong forward-looking expansion driven by domestic manufacturing policy and rising electronics demand.

To get more information on this market, Request Sample

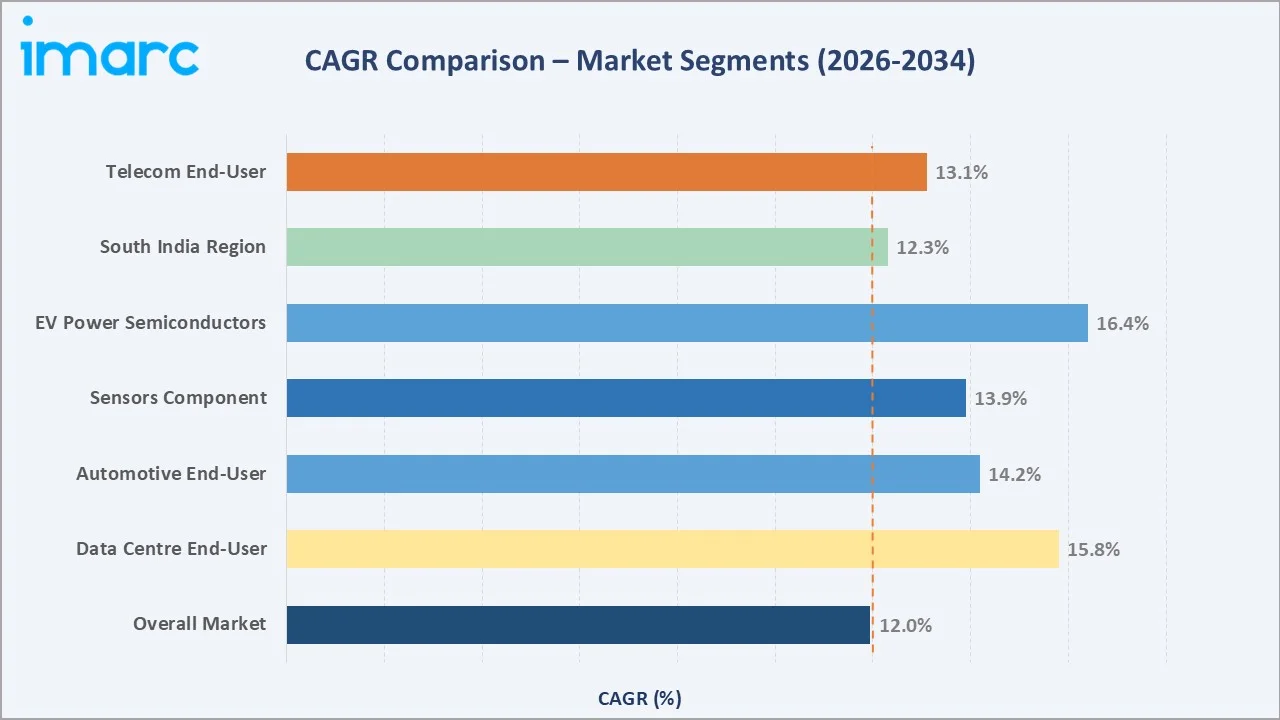

The CAGR comparison across key segments of the India semiconductor industry, revealing Silicon Carbide and automotive-linked components as standout high-growth categories through 2034.

Executive Summary

The market, valued at USD 59.78 Billion in 2025, is forecast to more than triple to USD 180.20 Billion by 2034, advancing at a robust CAGR of 11.95% across the 2026-2034 forecast period. Government initiatives including the PLI scheme for Large Scale Electronics Manufacturing, backed by incentives of INR 76,000 Crore are laying the groundwork for a full-stack domestic semiconductor ecosystem.

Key growth drivers include the rapid rollout of 5G networks, with India expects over 500 million 5G subscribers by 2030, accelerating EV adoption with India’s goal of a 30% electric vehicle penetration by 2030, and a massive digital infrastructure build-out. Among component categories, memory devices lead at 21.5% of market share (2025), followed by logic devices (18.3%) and analog ICs (12.8%). On the end-user side, consumer electronics commands the largest share at 30.4%, while the automotive segment, at 16.2%, represents the fastest-converging growth vector given India's EV ambitions.

Geographically, South India dominates with a 36.2% revenue share (2025), underpinned by Bengaluru's world-class semiconductor design ecosystem and Hyderabad's rapidly expanding R&D infrastructure. North India (27.8%) is consolidating through projects like the HCL-Foxconn OSAT facility in Jewar (Union Cabinet approves ₹3,706 crore), which is positioned as the fastest-growing region through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Component Segment |

Logic Devices - 28.5% share (2025) |

|

Largest End User Segment |

Consumer Electronics - 30.4% share (2025) |

|

Leading Region |

South India - 36.2% revenue share (2025) |

|

Fastest Growing Region |

West & Central India |

|

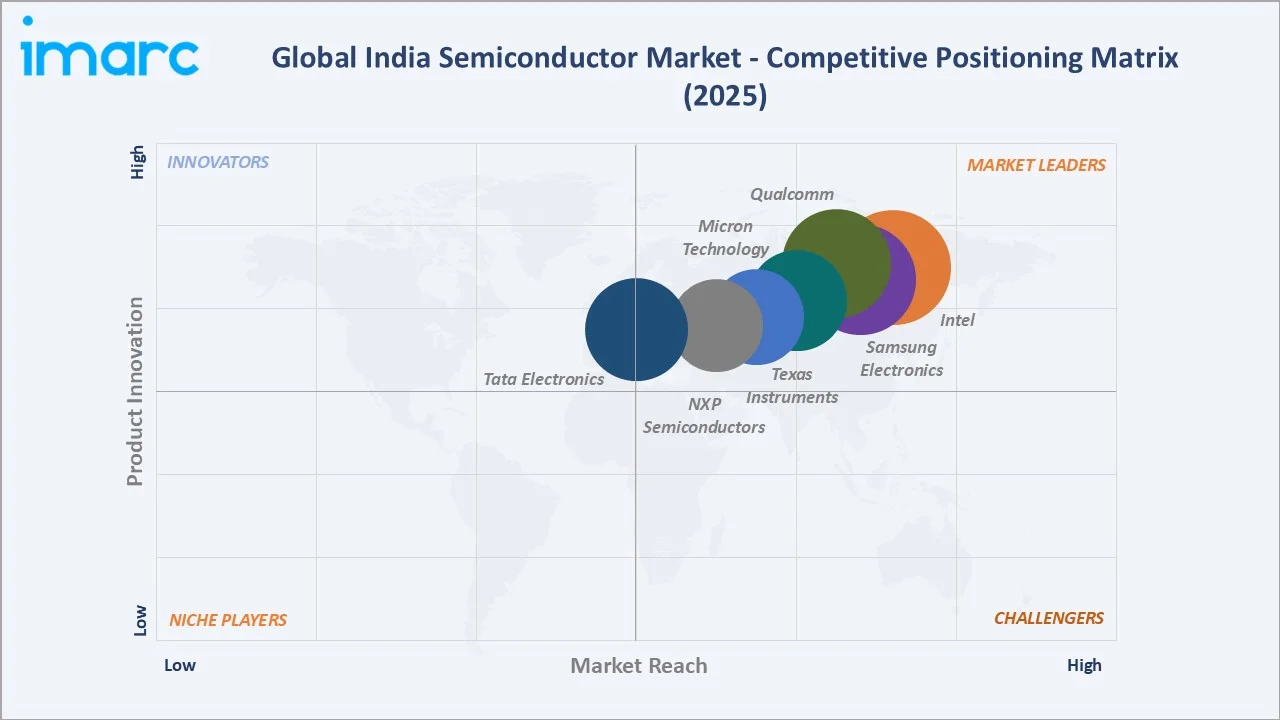

Top Companies |

Intel, Samsung, Qualcomm, Micron Technology, Texas Instruments, Tata Electronics |

|

Market Opportunity |

1st Made-in-India chips expected by 2026; USD 177 Bn addressable market by 2034 |

Key Analytical Observations Supporting the Above Data:

- Logic devices dominate components with a 28.5% share (2025), driven by application processors, SoCs, and FPGAs constitute the highest-value semiconductor content in India's largest consumption market, and smartphone upgrades across India's 600 million+ internet users.

- Consumer Electronics is the largest end-user segment at 30.4% (2025). India's smartphone market, remains one of the top three globally, underpinning sustained semiconductor consumption.

- South India is the revenue powerhouse at 36.2% (2025), anchored by Bengaluru's chip design professionals and Hyderabad's growing OSAT and design center ecosystem.

India Semiconductor Market Overview

The India semiconductor value chain currently spans three primary tiers: chip design, assembly, test, mark and pack (ATMP) facilities (now operational at Jewar), and nascent wafer fabrication capacity (Tata-PSMC Dholera fab under construction, 2025).

The India semiconductor market growth is supported by macroeconomic tailwinds: a GDP growth rate of ~6.5% (FY2025), a growing middle class of 350 million consumers, and a 5G subscriber base projected to exceed 500 million by 2030. India's digital economy, targeted at USD 1 Trillion by 2028, creates persistent demand for high-performance chips across every industry vertical. The India semiconductor market forecast is strongly positive, driven by import substitution, rising domestic manufacturing capacity, and surging semiconductor content per vehicle as EV adoption accelerates.

Market Dynamics

To evaluate market opportunities, Request Sample

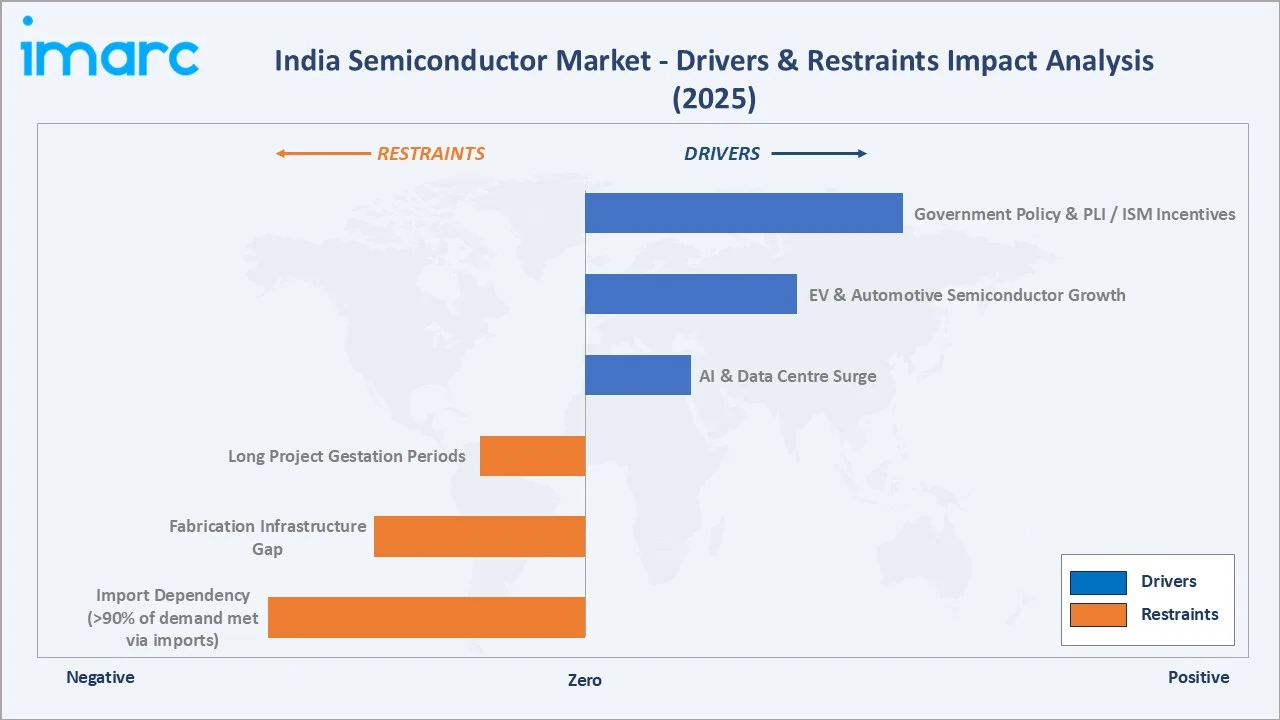

Market Drivers

- Government Policy & PLI / ISM Incentives: The India Semiconductor Mission substantial financial investment of ₹76,000 crore (around $10 billion), and combined production-linked incentive (PLI) program worth ₹760 billion have radically improved project economics, lowering capital costs by up to 50% for qualified fab projects.

- EV & Automotive Semiconductor Growth: India set an ambitious target to elevate EV sales to 30% of private cars, 70% of commercial vehicles, 40% of buses, and 80% of two- and three-wheelers by 2030, translating to approximately 80 million EVs on Indian roads. Each EV contains 3-5x the semiconductor content of a conventional ICE vehicle, with ADAS, battery management, and powertrain control systems each demanding specialized chips.

- AI & Data Centre Surge: Hyperscaler investments in India data centres exceeded USD 30 Billion in announced commitments as of early 2026. AI training and inference workloads drive demand for high-bandwidth memory and advanced logic devices, two of the top-three component segments by share.

These drivers collectively create a self-reinforcing demand cycle. Policy incentives de-risk greenfield manufacturing investments, which attract global technology partners, which accelerate technology transfer and domestic capability building, ultimately strengthening India semiconductor market trends toward self-sufficiency by 2034.

Market Restraints

- Import Dependency (>90% of demand met via imports): India currently imports over 90% of its semiconductor requirements, primarily from Taiwan, South Korea, and China. Geopolitical disruptions, shipping bottlenecks, or export control escalations represent significant supply continuity risks.

- Fabrication Infrastructure Gap: Domestic fabless startups are compelled to tape out at TSMC or Samsung foundries overseas, sustaining import dependency and limiting the value captured domestically in the semiconductor value chain.

- Long Project Gestation Periods: Greenfield semiconductor fabs require 3-5 years from approval to production readiness. Tata Electronics' Dholera facility is expected to achieve production volumes only in 2027-28, delaying near-term supply impact.

Market Opportunities

- OSAT Expansion & Semiconductor Packaging: India's lower cost structure, engineering talent pool, and strategic geographic position create compelling economics for OSAT (Outsourced Semiconductor Assembly and Test) expansion. Micron’s $2.75 billion ATMP facility in Sanand.

- Semiconductor Design Services Export: India's with over 85,000 semiconductor design engineers, represents a globally significant talent base. Export revenues from chip design services, with further upside as AI-assisted EDA tools improve design productivity.

Market Challenges

- Ultrapure Water & Specialized Infrastructure: Semiconductor manufacturing demands ultrapure water supply, vibration-free environments, and ultra-stable power grids. Infrastructure bottlenecks in key regions persist, requiring dedicated investment in feeders, desalination plants, and clean utility supply chains.

- Talent Shortage in Advanced Manufacturing: While India possesses world-class chip design talent, the country faces a critical shortage of process engineers, equipment technicians, and yield specialists required for front-end wafer fabrication, roles that are not interchangeable with design skills.

Emerging Market Trends

1. Domestic Fab Manufacturing Milestone (2024–2027)

India's transition from a design-only ecosystem to an integrated manufacturing base represents the most transformational trend in the India semiconductor market outlook. In February 2026, Micron Technology's opening of its semiconductor assembly and test facility in Sanand, Gujarat, India for advanced DRAM and NAND wafers. Tata Electronics, in partnership with PSMC, is constructing a USD 11 Billion, in Dholera targeting 50,000 wafer starts per month at mature nodes (28nm).

2. AI-Driven Demand for Specialized Semiconductors

The proliferation of AI and machine learning across Indian industries, from healthcare diagnostics to fintech fraud detection and autonomous vehicles, is reshaping the composition of semiconductor demand. Qualcomm and NVIDIA have both formed strategic partnerships in 2025 to develop AI-optimized server CPUs, with India's design centers playing a key role in architectural IP development.

3. Automotive & EV Semiconductor Surge

India's EV production, targeting 30% EV penetration by 2030, requires advanced power management ICs, microcontrollers, and ADAS sensor chips. NXP Semiconductors, Texas Instruments, and Infineon Technologies are aggressively expanding India-based R&D to address this growing market, with NXP committing USD 1 Billion+ in India R&D expansion.

4. Wide-Bandgap & Compound Semiconductor Adoption

Silicon Carbide (SiC) and Gallium Nitride (GaN) semiconductors are gaining rapid traction in India's power electronics and EV charging infrastructure. The Material Used segment in this report spans SiC, Gallium Manganese Arsenide, Copper Indium Gallium Selenide, and Molybdenum Disulfide, each targeting specialized high-power, high-frequency applications. SiCSem Pvt. Ltd. (Bhubaneswar, Odisha) operates a compound semiconductor fab focused on SiC wafers, with government DLI incentives accelerating investment in wide-bandgap IP development.

5. 5G-Enabled Smart Manufacturing & IoT Integration

India's '5G-enabled smart factory' initiative is driving semiconductor content growth in industrial applications (16.7% of demand, 2025). The government’s goal to achieve $150 billion through components manufacturing and imports of the total $500 billion electronics manufacturing target by 2030, is creating a virtuous cycle of industrial semiconductor demand growth through 2034.

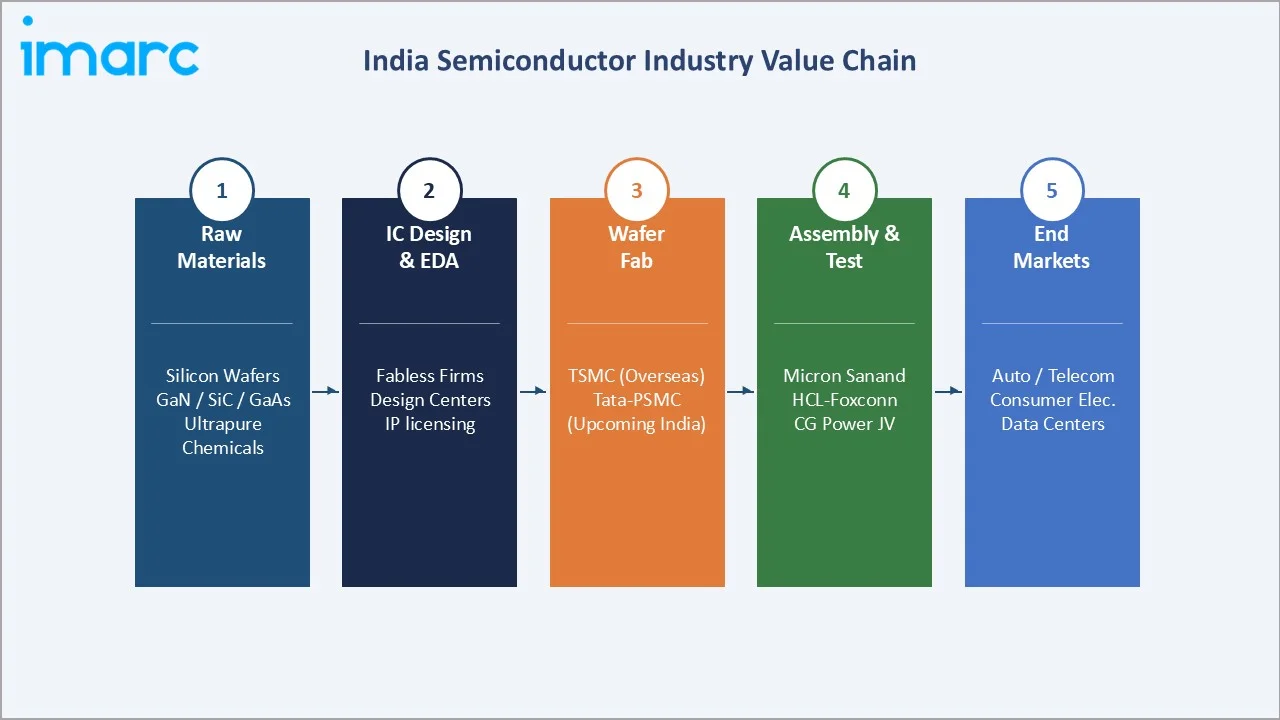

Industry Value Chain Analysis

The India semiconductor value chain encompasses five interconnected stages. Each stage presents distinct investment opportunities, risk profiles, and value-capture potential as the country builds toward an integrated domestic semiconductor ecosystem.

|

Stage |

Key Activities |

Key Players / Examples |

|

Raw Materials |

Silicon wafer supply, SiC/GaN/GaAs substrates, specialty chemicals (ultrapure gases, photoresists) |

Global suppliers (Shin-Etsu, SUMCO); SiCSem (India, SiC wafers) |

|

IC Design & EDA |

Chip architecture, RTL design, physical layout, IP licensing, EDA software tools |

Intel, Qualcomm, AMD, Texas Instruments (design centers); Mindgrove Technologies, Saankhya Labs (startups) |

|

Wafer Fabrication |

Photolithography, deposition, etching, doping – front-end manufacturing |

Tata Electronics-PSMC (Dholera, upcoming); SCL Mohali (legacy); TSMC, Samsung (overseas) |

|

Assembly, Test & Packaging (ATMP) |

Die bonding, wire bonding, encapsulation, electrical testing, final marking and packing |

Micron Technology (Sanand); HCL-Foxconn JV (Jewar); Renesas-Stars (Sanand); CG Power JV |

|

Distribution & OEMs |

Component distribution, PCB assembly, electronics manufacturing services (EMS) |

Dixon Technologies, Kaynes Technology, Syrma SGS, MosChip Technologies, Bharat Electronics |

|

End Users |

Consumer electronics OEMs, automotive OEMs, telecom operators, data centre operators, defence contractors |

Samsung, Apple (India mfg); Tata Motors, Mahindra (EV); Jio, Airtel (5G); ISRO, DRDO (defence) |

The value chain analysis reveals that India is strongest in design and ATMP segments, while wafer fabrication remains nascent as of 2025. Policy-backed fab projects are expected to bridge the fabrication gap by 2027-2028, creating a more complete domestic chain.

Technology Landscape in the India Semiconductor Industry

Advanced Packaging & ATMP Technology

Micron's Sanand ATMP facility, representing a USD 2.75 Billion investment, leverages advanced packaging technologies including multi-chip modules and stacked DRAM configurations. These packaging innovations are critical for meeting the bandwidth and power-efficiency requirements of AI accelerators and mobile SoCs, segments driving India semiconductor market growth.

Wide-Bandgap Semiconductor Materials

The Material Used segmentation of this report spans Silicon Carbide (SiC), Gallium Manganese Arsenide (GaMnAs), Copper Indium Gallium Selenide (CIGS), Molybdenum Disulfide (MoS2), and others. GaN-on-Si power transistors are being deployed in 5G base station amplifiers and fast-charging adapters. India's DLI scheme provides up to 50% design cost reimbursement for wide-bandgap IP, directly incentivizing domestic R&D investment in these materials.

AI-Optimized & Edge Computing Chips

Qualcomm and NVIDIA's 2025 partnership to co-develop AI server CPUs, with significant India R&D contributions, underscores the country's growing role in next-generation chip architecture. AMD's USD 400 Million investment in its Bengaluru design center (the company's largest global design campus, 500,000 sq ft, opened November 2023) focuses on 3D stacking and AI chip technologies. Edge AI chips, essential for ADAS, industrial robots, and smart city sensors, represent a high-growth intersection of India's sensor and MCU segments.

5G RF & Connectivity Semiconductor Innovation

Intel's design centers in Hyderabad and Bengaluru employ 13,000 engineers developing AI-integrated data center processors and IoT application chips. The telecommunications end-user segment, at 14.8% of total demand (2025), is expected to maintain above-market growth as 5G base station density increases through 2028.

Smart Sensors & MEMS Technology

MEMS (Micro-Electro-Mechanical Systems) and smart sensors are among the fastest-growing component categories, projected at ~14.5% CAGR through 2034. Automotive ADAS applications require radar, lidar, and ultrasonic sensor chips; industrial IoT applications demand pressure, temperature, and proximity sensors.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Components |

Logic Devices |

28.5% |

2025 |

|

Material Used |

Silicon Carbide |

34.2% |

2025 |

|

End User |

Consumer Electronics |

30.4% |

2025 |

|

Region |

South India |

36.2% |

2025 |

By Components

To access detailed market analysis, Request Sample

Logic devices dominate at 28.5% in 2025, driven by India's massive smartphone consumption, growing PC and tablet market, and explosive data centre GPU procurement. Memory Devices at 21.5% in 2025. India's rapidly expanding data centre ecosystem, hyperscaler commitments exceeding USD 30 Billion as of early 2026, drives DRAM and NAND flash demand at scale. Smartphone penetration with 155 million units shipped in 2024 sustains consumer-side memory consumption. Micron Technology's Sanand ATMP facility, represents a critical domestic supply node for this segment. India's cloud computing market creates sustained institutional demand for memory at multiple tiers.

By End User

Consumer Electronics is the dominant end-user segment at 30.4% in 2025. India is the world's second-largest smartphone market by shipments, with 155 million units in 2024. PLI incentives for mobile manufacturing are reinforcing domestic electronics production, with India's electronics output reaching INR 11.3 Lakh Crore in FY2025 in exports.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory / Policy Impact |

Major Companies |

|

South India |

36.2% |

Bengaluru chip design hub; Hyderabad OSAT & R&D; AMD 500K sq ft campus (2023) |

State EV policies; IT/ITeS incentives; Karnataka Semiconductor Policy |

Intel, AMD, Qualcomm, Micron, Texas Instruments |

|

North India |

27.8% |

HCL-Foxconn Jewar OSAT (INR 37 Bn); SCL Mohali modernization (INR 45 Bn); Delhi NCR design centers |

ISM flagship investments; UP Semiconductor Policy 2023; Haryana auto OEM proximity |

Intel, Qualcomm, MediaTek (design centers); HCL, Foxconn (OSAT) |

|

West & Central India |

22.5% |

Tata-PSMC Dholera Fab (USD 11 Bn); Micron Sanand ATMP (USD 2.75 Bn); CG Power Sanand JV |

Gujarat Semiconductor Policy; Dholera SIR incentives; 50% cost reduction via PLI |

Tata Electronics, Micron Technology, Renesas-Stars, CG Power |

|

East India |

13.5% |

SiCSem SiC fab (Bhubaneswar); 3D Glass Solutions-Intel packaging facility; ASIP Technologies-APACT JV (95M units/yr) |

Odisha Industrial Policy; Andhra Pradesh semiconductor corridor plans |

BEL, SiCSem, ASIP Technologies, 3D Glass Solutions |

South India dominates India's semiconductor ecosystem, capturing 36.2% of revenues in 2025. Bengaluru, home to semiconductor design professionals and design centers for Intel, AMD, Qualcomm, Micron, Texas Instruments, and Broadcom, is Asia's largest chip design hub outside Taiwan and South Korea.

West & Central India is positioned as the fastest-growing region, anchored by two landmark projects: Tata Electronics' USD 11 Billion Dholera fab (targeting 50,000 wafer starts per month) and Micron Technology's USD 2.75 Billion Sanand ATMP facility. Gujarat's Dholera Special Investment Region provides dedicated power, water, and transportation infrastructure specifically designed for semiconductor manufacturing requirements.

Competitive Landscape

The India semiconductor market is moderately fragmented, with global technology leaders maintaining dominant design and supply positions while domestic manufacturers build manufacturing capacity.

|

Company Name |

Brand / Product Line |

Market Position |

Core India Strength |

|

Intel Corporation |

Intel Core / Xeon / Gaudi |

Market Leader |

13,000+ India employees; AI chips, data center processors, IoT design centers in Hyderabad & Bengaluru |

|

Samsung Electronics |

Exynos / Galaxy Memory |

Market Leader |

DRAM/NAND supply, smartphone SoC design; key supplier to India's consumer electronics sector |

|

Qualcomm Incorporated |

Snapdragon / FastConnect |

Market Leader |

Mobile chipsets for India's 155M+ smartphone shipments/yr; 5G modem chips; design centers in Hyderabad & Bengaluru |

|

Micron Technology |

Crucial / BallistiX Memory |

Strong Challenger |

USD 2.75 Bn Sanand ATMP facility (2023 groundbreaking); 4,000+ India R&D engineers; DRAM + NAND packaging |

|

Texas Instruments |

TI Analog / Embedded Processing |

Strong Challenger |

Analog ICs for automotive & industrial; 18,000+ India engineers; design centers across Bengaluru, Hyderabad, Noida |

|

Tata Electronics (Tata Group) |

Tata Semiconductor / PSMC |

Emerging Domestic Leader |

USD 11 Bn Dholera fab (with PSMC); Assam assembly: 18 Bn chip units/yr; partnership with BEL for defense semis |

|

Bharat Electronics Ltd (BEL) |

BEL Defence Electronics |

Domestic Champion |

Aerospace & defence electronics; 2025 JV with Tata Electronics for MCU and SoC solutions; INR 6.81 Lakh Cr MoD budget |

|

NXP Semiconductors |

NXP S32 / i.MX / Kinetis |

Challenger |

Automotive & IoT chips; USD 1 Bn+ India R&D expansion (Sept 2024); 2,500+ engineers across Noida, Bengaluru, Hyderabad, Pune |

The top players Intel, Samsung Electronics, Qualcomm, Micron Technology, and Texas Instruments, collectively capture an estimated 55–60% of the India market's component value in 2025.

Key Company Profiles

Intel Corporation

Intel Corporation is one of the world's foremost semiconductor companies, with over 13,000 employees across design facilities in Hyderabad and Bengaluru in India.

- Product Portfolio: Core, Xeon, and Gaudi processors.

- Recent Developments: Intel's 3D Glass Solutions partnership in Odisha (2025) targets advanced semiconductor packaging with 50 million unit annual capacity; continued expansion of the Hyderabad development center with new AI research labs.

- Strategic Focus: AI chip design leadership; advanced packaging innovation; India as a global design and verification hub; reducing dependency on single-node manufacturing via IDM 2.0 strategy.

Qualcomm Incorporated

Qualcomm is the world's dominant mobile chipset supplier, with Snapdragon SoCs powering the majority of India's 155 million+ annual smartphone shipments.

- Product Portfolio: Snapdragon mobile series, Snapdragon X series, Dragonwing IQ Series, Dragonwing Q series

- Recent Developments: NVIDIA-Qualcomm partnership for AI server CPU development; expanded 5G modem chipset supply for Jio and Airtel network equipment.

- Strategic Focus: 5G and AI edge semiconductor leadership; expanding automotive ADAS chipset portfolio; India as a top-tier global design center for AI IP.

Micron Technology

Micron Technology is a global leader in DRAM, NAND flash memory, and storage solutions. Its USD 2.75 Billion ATMP facility in Sanand, Gujarat, with groundbreaking in 2023 and first packaged memory shipped in late 2024 is India's most operationally significant semiconductor manufacturing milestone.

- Product Portfolio: DRAM (DDR5, LPDDR5); NAND flash; SSDs (Crucial, Micron Pro); HBM (High-Bandwidth Memory) for AI accelerators.

- Recent Developments: First packaged DRAM shipped from Sanand facility, India's first commercial ATMP production milestone; Phase 2 expansion planning underway.

- Strategic Focus: Scaling India ATMP capacity; expanding HBM supply for AI data centres; positioning India as a resilient alternative to East Asian supply chains.

Market Concentration Analysis

The India semiconductor market displays a moderately concentrated structure at the supply level, with the top five global players, Intel, Samsung Electronics, Qualcomm, Micron Technology, and Texas Instruments, collectively accounting for an estimated 55–60% of component value consumed in India in 2025. This concentration is notably higher in specific sub-segments: in mobile SoCs, Qualcomm and MediaTek together command over 85% of India's smartphone chipset market.

The value chain is more fragmented downstream. The OSAT and EMS tiers include dozens of operators including Micron, HCL-Foxconn, Renesas-Stars, Dixon Technologies, Syrma SGS, Kaynes Technology, and MosChip Technologies. This diversity reflects India's strength in electronics assembly and testing over pure chip manufacturing.

Consolidation trends are accelerating. The Tata Electronics-BEL strategic alliance (2025) signals domestic consolidation to compete with global integrated device manufacturers. Government policy deliberately favors vertically integrated ecosystem development, ISM incentives are structured to encourage partnerships between foreign technology leaders and Indian manufacturing companies, creating joint ventures that concentrate supply chain control within Indian-anchored entities.

Investment & Growth Opportunities

Fastest Growing Segments

The three highest-growth investment vectors in the India semiconductor market through 2034 are: Sensors (~14.5% CAGR), driven by EV ADAS, industrial IoT, and healthcare monitoring; MCU segment (~13.8% CAGR), underpinned by EV motor controllers, smart appliances, and 5G edge devices; and Discrete Power Devices (~8.5% CAGR), benefiting from India's renewable energy build-out and EV power electronics. These three segments collectively represent a total addressable market exceeding USD 60 Billion by 2034.

Emerging Markets & Geographic Opportunity

West & Central India presents the most compelling near-term investment opportunity, with Gujarat alone secured ₹1.24 lakh crore in semiconductor investments. The Dholera Special Investment Region provides plug-and-play infrastructure for fab operations, dedicated power feeders (2GW allocated), ultrapure water systems, and seamless logistics connectivity.

Venture Investment Trends

- Government-Backed Capital: Union Budget 2025–26 allocated INR 70 Billion for semiconductors with a 56% hike in the fab scheme outlay.

- Private Equity & Strategic Investment: NXP announced USD 1 Billion+ in India R&D expansion (September 2024).

- OSAT Greenfield Expansion: India's lower manufacturing cost structure makes it highly attractive for OSAT capacity expansion. Near-term revenue traction is expected from ATMP facilities within a 2–3 year project gestation vs. 5+ years for full fabs, offering superior capital efficiency for investors prioritizing earlier cash flow.

Future Market Outlook (2026-2034)

The India semiconductor market is poised for transformative, broad-based growth through 2034, anchored by domestic manufacturing scale-up, deepening digital economy penetration, and accelerating EV and AI adoption.

Technological disruptions AI-driven chip design automation, 3D stacking packaging technology, wide-bandgap semiconductor commercialization, and chiplet-based heterogeneous integration will reshape the competitive landscape through 2034. India's design engineering base is well-positioned to capture high-value IP in these frontier areas.

Structurally, the India semiconductor industry of 2034 will look fundamentally different from 2025, transitioning from a design-and-import model to a vertically integrated, domestically anchored semiconductor ecosystem capable of serving both the world's largest growth markets and global OEM supply chains.

Research Methodology

Primary Research

Primary research for this report included structured interviews and in-depth discussions conducted with over 120 industry participants in 2024-2025, comprising semiconductor design executives, fab project managers, OSAT facility heads, procurement specialists, government policy officials, technology distributors, and end-user electronics OEMs across India's major semiconductor clusters in Bengaluru, Hyderabad, Pune, Delhi NCR, and Ahmedabad.

Secondary Research

Secondary research encompassed a comprehensive review of government policy documents (India Semiconductor Mission guidelines, PLI scheme annexures, Union Budget 2025–26 allocations), company annual reports and investor presentations, regulatory filings with SEBI and MCA, trade publications (Electronics For You, IEEE Spectrum, Semiconductor Digest), industry databases, and publicly available investment announcements. Over 280 secondary sources were reviewed, cross-referenced, and triangulated for data consistency.

Forecasting Models

Market size estimations and the India semiconductor market forecast were derived using a combination of bottom-up and top-down approaches. The bottom-up model aggregated segment-level demand projections (components × end-user verticals × regions) using bill-of-materials (BOM) semiconductor content analysis per device category. The top-down model cross-validated against India's GDP growth trajectory, electronics production output, and PLI-driven manufacturing investment timelines. Scenario analysis (base, optimistic, and conservative cases) was performed incorporating geopolitical risk variables, fab ramp timeline uncertainty, and EV adoption pace sensitivity.

India Semiconductor Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Memory Devices, Logic Devices, Analog IC, MPU, Discrete Power Devices, MCU, Sensors, Others |

| Material Useds Covered | Silicon Carbide, Gallium Manganese Arsenide, Copper Indium Gallium Selenide, Molybdenum Disulfide, Others |

| End Users Covered | Automotive, Industrial, Data Centre, Telecommunication, Consumer Electronics, Aerospace and Defense, Healthcare, Others |

| Regions Covered | South India, West and Central India, North India, East India |

| Companies Covered | Intel Corporation, Samsung Electronics, Qualcomm Incorporated, Micron Technology, Texas Instruments, Tata Electronics (Tata Group), Bharat Electronics Ltd (BEL), NXP Semiconductors |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India semiconductor market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India semiconductor market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India semiconductor industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Semiconductor Market Report

The India semiconductor market was valued at USD 59.78 Billion in 2025 and is projected to reach USD 180.20 Billion by 2034.

The India semiconductor market is expected to grow at a CAGR of 11.95% during the forecast period 2026-2034, reflecting robust demand across all end-user verticals.

South India is the dominant region, accounting for 36.2% of revenues in 2025, anchored by Bengaluru's world-class chip design ecosystem and Hyderabad's expanding OSAT infrastructure.

Logic devices dominate component demand at 28.5% of total market share in 2025.

Key drivers include the USD 10+ Billion India Semiconductor Mission, 5G network rollout, EV proliferation, AI-driven data center investments exceeding USD 30 Billion in commitments, and a 155 million unit smartphone market. Government PLI incentives reduce greenfield fab capital costs by up to 50%.

The India semiconductor market is projected to reach USD 180.20 Billion by 2034. First Made-in-India chips are expected in 2026, with India targeting 20% domestic supply sufficiency by 2030 supported by Tata Electronics' Dholera fab and multiple OSAT facilities.

Consumer electronics lead with 30.4% of end-user demand in 2025, followed by Automotive at 16.2% and Industrial at 14.8%. The automotive segment shows the highest growth potential given India's EV transition.

Leading companies include Intel Corporation, Samsung Electronics, Qualcomm, Micron Technology, Texas Instruments, Tata Electronics, Bharat Electronics Limited (BEL), NXP Semiconductors, AMD, Broadcom, and Infineon Technologies.

South India leads at 36.2% share (2025); North India holds 27.8%; West & Central India accounts for 22.5% and is the fastest growing; East India holds 13.5% with emerging fab and OSAT projects underway in Odisha and Andhra Pradesh.

Key trends include domestic fab manufacturing scale-up (Tata-PSMC Dholera fab), AI-driven demand for specialized logic and memory chips, EV-led automotive semiconductor surge, wide-bandgap material adoption (SiC, GaN), and 5G-enabled smart manufacturing driving sensor and MCU growth.

The India Semiconductor Mission (USD 10+ Bn), PLI scheme (INR 760 Bn combined with DLI), Union Budget 2025 eliminating customs duties on lithography tools, and the Make in India / Digital India programs collectively provide the world's most comprehensive government support package for a developing semiconductor ecosystem.

Top investment opportunities include OSAT greenfield facilities (2-3 year gestation vs 5+ years for fabs), SiC/GaN power semiconductor IP development (DLI covers 50% of design costs), semiconductor design services export (projected USD 20 Billion+ by 2025), and automotive/EV chip design targeting India's EV market growing at 50%+ CAGR through 2030.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade