India Set-Top Box Market Size, Share, Trends and Forecast by Type, Resolution, End-User, Service Type, Distribution, and Region, 2026-2034

India Set-Top Box Market Summary:

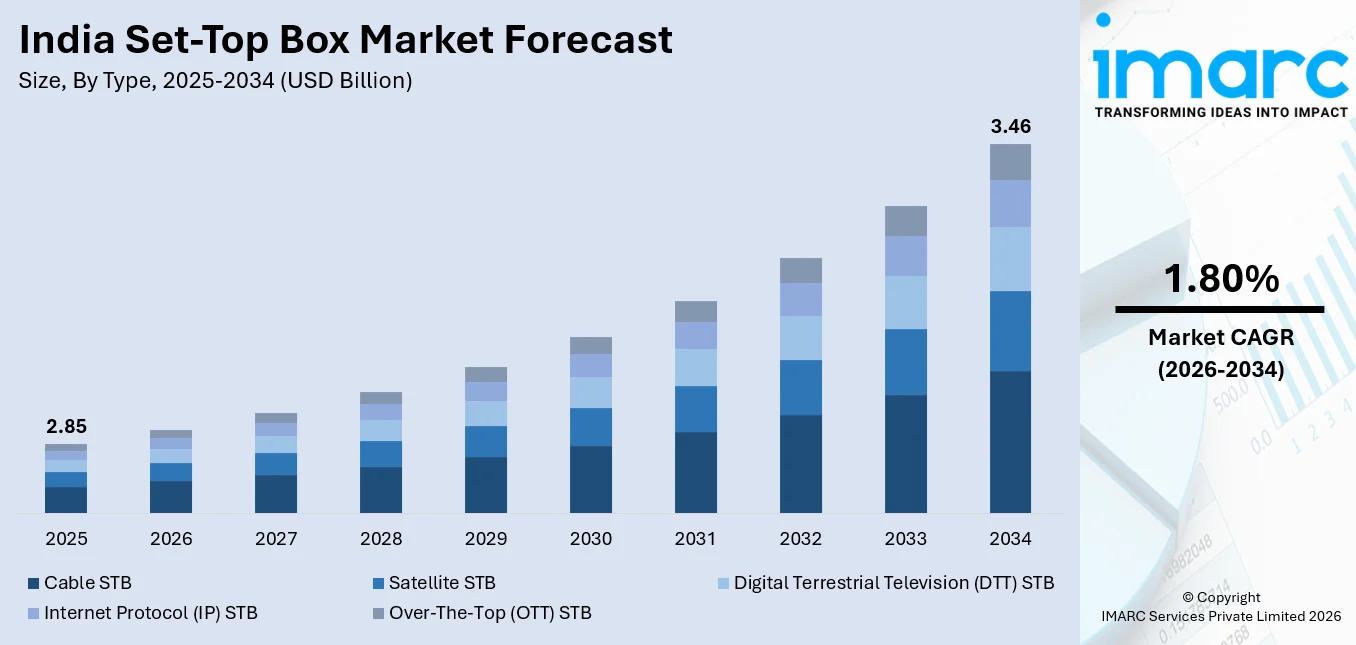

The India set-top box market size was valued at USD 2.85 Billion in 2025 and is projected to reach USD 3.46 Billion by 2034, growing at a compound annual growth rate of 1.80% from 2026-2034.

The India set-top box market is advancing as the country accelerates its transition toward digital broadcasting and integrated entertainment ecosystems. Rising consumer preference for high-definition content, expanding broadband connectivity, and the convergence of traditional television with internet-based streaming services are strengthening demand. Evolving regulatory frameworks, growing residential adoption, and the proliferation of hybrid viewing solutions continue to reshape the television distribution landscape across urban and rural regions.

Key Takeaways and Insights:

- By Type: Cable STB dominates the market with a share of 46% in 2025, owing to the extensive cable television infrastructure built through India’s phased digitization mandate and the widespread network of multi-system operators and local cable operators serving diverse consumer segments.

- By Resolution: HD (high definition) leads the market with a share of 48% in 2025, driven by growing consumer demand for superior picture quality, affordable high-definition set-top box variants, and the expansion of HD channel offerings by major broadcasters and distribution platform operators.

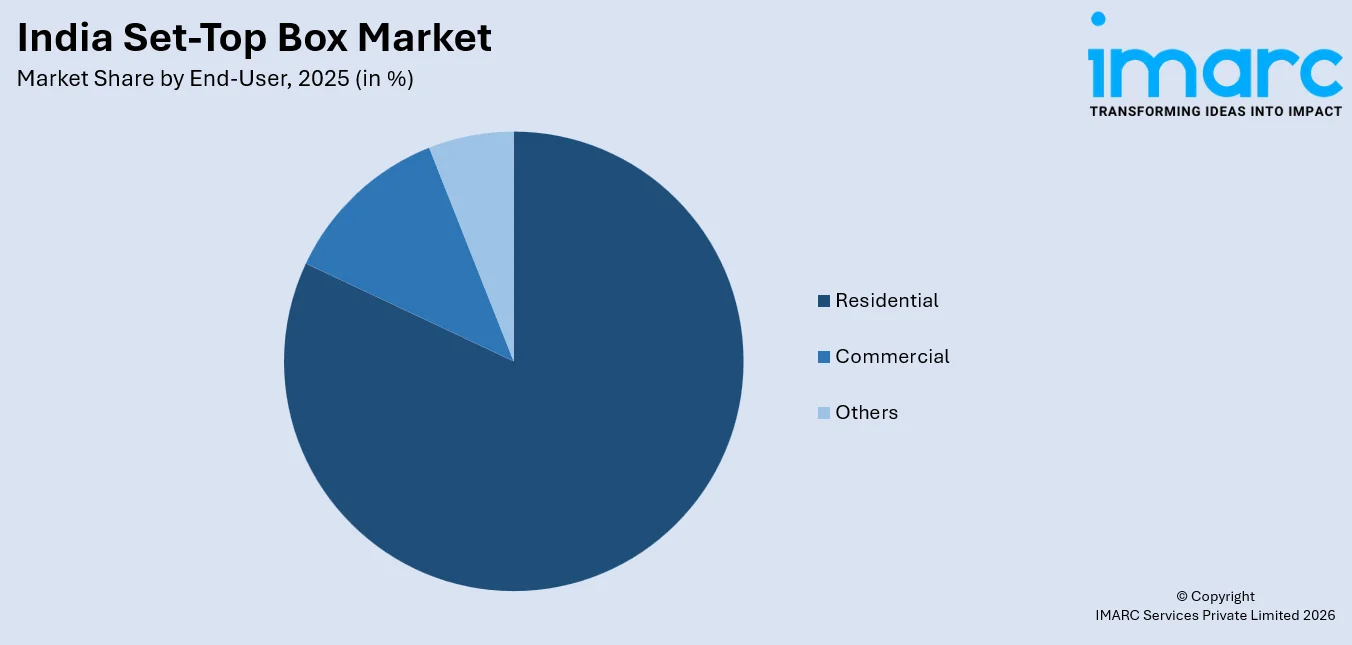

- By End-User: Residential represents the largest segment with a market share of 82% in 2025, reflecting the central role of television as a primary entertainment source in Indian households, supported by rising disposable incomes and the availability of affordable digital set-top box packages across the country.

- By Service Type: Pay TV exhibits a clear dominance in the market with 74% share in 2025, underpinned by the strong subscriber bases of direct-to-home operators and cable service providers offering curated channel bouquets, premium content, and value-added interactive services to viewers.

- By Distribution: Offline distribution is the biggest segment with 69% share in 2025, driven by the established retail networks of authorized dealers, operator-owned stores, and electronic retail chains that facilitate hands-on customer engagement, installation support, and after-sales service delivery.

- By Region: South India is the largest region with 29% share in 2025, driven by the strong penetration of cable and satellite television services across key states such as Tamil Nadu, Andhra Pradesh, Karnataka, and Kerala, supported by robust regional broadcasting ecosystems and high consumer engagement.

- Key Players: Key players are advancing the India set-top box market by developing hybrid devices that integrate satellite, cable, and streaming functionalities. Their investments in 4K-enabled hardware, voice-controlled interfaces, and partnerships with content platforms are strengthening consumer adoption and ensuring broader product availability across diverse distribution networks.

To get more information on this market Request Sample

The India set-top box market is experiencing sustained growth driven by the convergence of traditional broadcasting with digital content delivery platforms. The country’s vast television landscape, encompassing nearly 190 Million households with TV access in 2024, provides a substantial consumer base for set-top box manufacturers and distribution platform operators. The government’s phased cable television digitization mandate has accelerated the replacement of analog connections with digital addressable systems, creating consistent demand for standardized set-top box units. Simultaneously, the rapid expansion of broadband infrastructure and the growing popularity of over-the-top streaming services are encouraging operators to launch hybrid devices that combine linear television with on-demand content. Rising consumer expectations for high-definition and ultra-high-definition viewing experiences, coupled with increasing affordability of advanced set-top box variants, are broadening market penetration across both metropolitan and semi-urban geographies. The proliferation of regional content ecosystems and multilingual broadcasting further reinforces steady demand across the India set-top box market share.

India Set-Top Box Market Trends:

Integration of OTT platforms with traditional set-top boxes

India is witnessing a significant shift toward hybrid set-top boxes that merge traditional broadcast services with internet-based streaming capabilities. Operators are launching devices that provide unified access to live television channels alongside popular on-demand platforms, offering consumers seamless content navigation through a single interface. For instance, in March 2025, Bharti Airtel launched its IPTV service across 2,000 cities in India, providing access to 29 streaming applications, over 600 television channels, and high-speed broadband through a single integrated offering. This convergence of linear and digital entertainment is expected to support India set-top box market growth.

Rising adoption of high-definition and ultra-high-definition set-top boxes

Consumer demand for superior viewing quality is accelerating the transition from standard-definition to high-definition and 4K-capable set-top boxes across India. Broadcasters are expanding their HD channel offerings while manufacturers are introducing affordable UHD variants to capture growing interest in premium content experiences. The increasing penetration of large-screen smart televisions is further reinforcing consumer appetite for high-resolution content that extends to compatible set-top box hardware. Voice-enabled remote controls and AI-driven content recommendations are enhancing the appeal of next-generation devices, driving broader adoption across urban and semi-urban households.

Expansion of free-to-air satellite television services

The continuously growing reach of free-to-air satellite platforms is currently reshaping India's television distribution landscape by providing no-subscription-cost viewing options to price-sensitive households. These platforms are expanding their channel portfolios and attracting broadcasters seeking wider audience reach through advertising-supported models, particularly in rural and semi-urban regions. The increasing availability of regional language channels and entertainment content on free-to-air services is further broadening their appeal among diverse consumer segments. For instance, DD Free Dish, operated by Prasar Bharati, reaches over 45 Million households across India and continues to expand its slot capacity.

Market Outlook 2026-2034:

India’s set-top box market is poised for stable growth over the forecast period, supported by continued digital infrastructure investments, broadband expansion, and evolving consumer entertainment preferences. The ongoing transition toward hybrid and IP-based content delivery models is encouraging operators and manufacturers to develop integrated solutions that address diverse viewing requirements. The market generated a revenue of USD 2.85 Billion in 2025 and is projected to reach a revenue of USD 3.46 Billion by 2034, growing at a compound annual growth rate of 1.80% from 2026-2034. Expanding regional content ecosystems, increasing HD and UHD adoption, and growing penetration in semi-urban and rural areas are expected to sustain steady demand. Furthermore, the convergence of telecom and broadcasting services through bundled broadband and television packages is creating new revenue opportunities and strengthening the long-term outlook for set-top box deployment across the country.

India Set-Top Box Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Cable STB |

46% |

|

Resolution |

HD (High Definition) |

48% |

|

End-User |

Residential |

82% |

|

Service Type |

Pay TV |

74% |

|

Distribution |

Offline Distribution |

69% |

|

Region |

South India |

29% |

Type Insights:

- Cable STB

- Satellite STB

- Digital Terrestrial Television (DTT) STB

- Internet Protocol (IP) STB

- Over-The-Top (OTT) STB

Cable STB dominates with a market share of 46% of the total India set-top box market in 2025.

Cable set-top boxes continue to anchor India’s television distribution infrastructure, benefiting from the country’s mandatory digitization of cable networks completed across four phases. The extensive network of over 800 registered multi-system operators and thousands of local cable operators ensures widespread availability of cable STB services across metropolitan, urban, and semi-urban markets. India’s cable television subscriber base stood at approximately 60 Million as of March 2025 according to TRAI data, underscoring the enduring relevance of cable-based content delivery in the country’s broadcasting ecosystem.

The cable STB segment benefits from competitive pricing and localized content offerings that appeal to diverse linguistic and regional preferences. Operators are upgrading their infrastructure to support digital addressable systems and high-definition content delivery, enabling cable subscribers to access improved picture quality and interactive services. The ongoing modernization of cable networks through fiber-optic backbone upgrades is further strengthening the segment’s ability to compete with satellite and IPTV alternatives in delivering reliable, affordable television services to Indian households.

Resolution Insights:

- HD (High Definition)

- SD (Standard Definition)

- UHD (Ultra-High Definition)

HD (high definition) leads with a share of 48% of the total India set-top box market in 2025.

High-definition set-top boxes have become the preferred choice for Indian consumers seeking enhanced visual experiences, driven by the growing availability of HD channels across cable, satellite, and IPTV platforms. The expansion of HD content by major broadcasters, including regional language networks, has created sustained demand for compatible hardware. India’s television industry served a nationwide audience of more than 900 Million viewers by 2025 according to government data, with a significant proportion accessing content through HD-enabled devices that deliver superior picture clarity and audio quality.

The affordability of HD set-top boxes has improved substantially through competitive pricing strategies and exchange offers from leading distribution platform operators. Manufacturers are incorporating advanced features such as HDMI connectivity, electronic program guides, and recording capabilities into their HD devices, enhancing the overall viewing experience. As broadcasters continue expanding their HD channel portfolios and consumers increasingly prioritize visual quality, the HD resolution segment is expected to maintain its dominant position within India’s set-top box market.

End-User Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Others

Residential is the largest segment, accounting for 82% of the total India set-top box market in 2025.

The residential segment dominates India's set-top box market, reflecting the central role of television as the primary entertainment medium in Indian households. The country's extensive television penetration across urban, semi-urban, and rural regions ensures a substantial and growing consumer base that continues to drive consistent demand for set-top box devices. The availability of diverse channel packages covering entertainment, news, sports, and regional content ensures that households across income segments find value in maintaining active set-top box connections. Rising disposable incomes and expanding broadband accessibility are further reinforcing residential adoption across geographically diverse markets.

Indian residential consumers are increasingly upgrading from basic standard-definition set-top boxes to HD and smart variants that offer access to both linear television and streaming applications. The proliferation of hybrid set-top boxes enabling simultaneous access to broadcast channels and over-the-top platforms is particularly attractive to family-oriented households seeking consolidated entertainment solutions. Growing broadband penetration in semi-urban and rural regions, coupled with affordable entry-level pricing from operators, is expanding the residential addressable market beyond traditional metropolitan strongholds.

Service Type Insights:

- Pay TV

- Free-to-Air

Pay TV holds the largest share at 74% of the total India set-top box market in 2025.

Pay television services remain the backbone of India’s set-top box market, supported by the established subscriber bases of major direct-to-home operators and cable service providers offering curated channel bouquets and premium programming. India’s pay DTH sector maintained an active subscriber base of approximately 59.91 Million as of September 2024 according to TRAI’s performance indicator report, reflecting the continued preference among consumers for subscription-based access to exclusive entertainment, sports, and news content.

Pay TV operators are strengthening their competitive position by bundling linear television services with over-the-top application subscriptions, creating integrated value propositions that address evolving consumer expectations. The introduction of smart set-top boxes with built-in access to popular streaming platforms enables pay TV providers to offer consolidated entertainment packages that combine broadcast reliability with on-demand flexibility. Additionally, tiered pricing structures and customizable channel selection options under the prevailing tariff order framework are helping operators retain subscribers while attracting cost-conscious consumers across urban and rural markets nationwide.

Distribution Insights:

- Online Distribution

- Offline Distribution

The offline distribution exhibits a clear dominance with a 69% share of the total India set-top box market in 2025.

In India, set-top box sales are still mostly conducted through offline distribution channels, which make use of vast retail networks that include local electronics stores, operator-owned stores, authorized dealer showrooms, and multi-brand electronics outlets. Many Indian consumers, especially those in semi-urban and rural areas, still prefer the physical retail environment because it offers crucial customer touchpoints for product presentation, installation support, and technical guidance. The offline channel's position as the main middleman for set-top box deployment is further reinforced by the nation's extensive cable television distribution infrastructure, which is made up of multiple multi-system operators and local cable operators.

Customers' familiarity and comfort with in-person shopping experiences are advantageous to the offline channel, particularly for technology products that need expert installation and configuration. To guarantee smooth client onboarding and post-sale support, distribution platform operators spend in educating retail partners and setting up service centers. Even while internet channels are becoming more popular, especially in cities, the offline distribution network's capacity to reach geographically scattered markets and offer practical support keeps it at the top of the market.

Regional Insights:

- North India

- West and Central India

- South India

- East India

South India represents the leading segment with a 29% share of the total India set-top box market in 2025.

Due to the widespread use of cable and satellite television services in Tamil Nadu, Andhra Pradesh, Karnataka, Telangana, and Kerala, South India dominates the set-top box market. The region gains from a thriving regional broadcasting ecology that is based in important production centers like Hyderabad and Chennai, where Telugu and Tamil content ecosystems sustain long-term customer engagement. Large-scale cable infrastructure coverage in urban and semi-urban markets is guaranteed by South India's well-established multi-system operator networks, which are dominated by major companies with subscriber bases surpassing several million.

Set-top box devices are in high demand due to the region's high television penetration rate and strong customer preference for premium sports content and regional language programming. Due to increased literacy rates and expanding internet access, South Indian consumers have shown early adoption of high-definition and smart set-top boxes. The move to IPTV-based solutions is being made easier by the rise of fiber-to-the-home connections in southern states, making South India a major growth location for the deployment of next-generation set-top boxes.

Market Dynamics:

Growth Drivers:

Why is the India Set-Top Box Market Growing?

Expanding digital broadcasting infrastructure and government digitization mandates

The government's four-phase digitalization mandate under the Cable Television Networks (Regulation) Amendment Act has propelled India's methodical shift from analog to digital cable television, which has been a key factor in the set-top box market's growth. Every cable television household had to purchase a compliant set-top box due to the forced implementation of digital addressable systems, which generated significant demand in every region. In addition to creating a strong baseline of digital customers, this regulatory drive encouraged operators to modernize their network infrastructure in order to enable more sophisticated content delivery capabilities. By facilitating internet access in previously underserved markets, the continuous development of broadband infrastructure, especially through government-led rural connection initiatives, is bolstering the ecosystem for set-top box adoption. The adoption of IP-based set-top boxes and hybrid devices that need dependable internet access is made possible by this growing digital infrastructure, opening up new growth prospects for content service providers and set-top box manufacturers nationwide.

Growing consumer demand for high-definition and interactive entertainment experiences

The upgrade cycle from standard-definition to high-definition and ultra-high-definition set-top boxes is being driven by Indian customers' growing emphasis on greater visual and audio quality in their home entertainment setups. Households are being encouraged to purchase compatible technology due to the growth of HD and 4K material from broadcasters, as well as the growing appeal of premium sports programming and cinematic entertainment. The increasing use of large-screen televisions contributes to this trend by increasing customer demand for high-resolution viewing experiences provided by cutting-edge set-top box devices. Set-top boxes are evolving from simple signal receivers into complex entertainment centers with the addition of interactive features like voice-activated remote controls, tailored content recommendations, and electronic program guides. Devices that provide smooth switching between live broadcast channels and on-demand streaming libraries draw consumers, eliminating the need for numerous separate devices and maintaining demand in both urban and semi-urban areas.

Convergence of telecom and broadcasting services through bundled offerings

Adoption of set-top boxes is being fueled by the strategic convergence of broadcasting and telecommunications services, which is producing attractive value propositions. Large telecom companies are pitching the set-top box as the primary device for home entertainment delivery by combining broadband internet, linear television channels, and over-the-top streaming subscriptions into single packages. This strategy reduces subscription fragmentation, streamlines the content discovery process, and responds to the growing consumer preference for consolidated services available through a single platform. By converting broadband-only customers into multi-service subscribers, the bundled service model is especially successful in growing the addressable market beyond traditional pay TV subscribers. This increases demand for set-top boxes and improves customer retention through increased service stickiness. The incorporation of television services into broadband bundles is anticipated to continue to be a sustained impetus for the deployment of set-top boxes across the country as telecom companies deepen their fiber-to-the-home infrastructure and increase coverage in semi-urban and rural areas.

Market Restraints:

What Challenges the India Set-Top Box Market is Facing?

Intensifying competition from smart televisions with built-in streaming capabilities

Customers' reliance on external set-top box devices is decreasing due to the quick spread of reasonably priced smart televisions with built-in streaming services and app ecosystems. Many homes are choosing direct streaming access through built-in operating systems, avoiding the need for a separate set-top box, as manufacturers offer internet-connected TVs at ever-lower price points. Younger, digitally native customers in urban areas that favor on-demand video consumption over conventional linear television are especially affected by this substitution effect.

Declining pay television subscriber base amid cord-cutting trends

The number of subscribers to India's pay television industry is steadily declining as more people turn to digital streaming services and free-to-air programming options. A larger structural shift in content consumption patterns, especially among younger and digitally connected households, is shown in the continuous decline of the traditional pay TV subscriber base. Operators and manufacturers are under pressure to modify their business models as a result of this subscriber attrition, which lowers the need for conventional set-top box upgrades and replacements.

Regulatory complexities and evolving tariff frameworks

Manufacturers and service providers of set-top boxes face uncertainty due to the changing regulatory environment governing broadcasting prices and distribution methods. Investment decisions and product launches may be delayed by ongoing disagreements between broadcasters, distribution platform operators, and the regulatory body over channel pricing, platform carriage obligations, and free-to-air classification requirements. The adoption of new set-top box technologies may be slowed by these legislative obstacles, which also make long-term strategic planning difficult for market players.

Competitive Landscape:

Established distribution platform operators coexist with specialist hardware manufacturers and up-and-coming technology providers in the somewhat consolidated competitive landscape of the Indian set-top box market. Product innovation, price tactics, content collaborations, and distribution network reach are what fuel competition. Market players are increasingly using OTT platform integration, hybrid device capabilities, and improved user interface experiences to differentiate their products. Competitive dynamics are changing as a result of strategic partnerships between telecom companies, content aggregators, and device makers. As operators look to improve subscriber retention and draw in new clients in a changing entertainment market, investments in regional manufacturing, voice-enabled technology, and AI-powered content personalization are emerging as crucial differentiators.

India Set-Top Box Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Cable STB, Satellite STB, Digital Terrestrial Television (DTT) STB, Internet Protocol (IP) STB, Over-The-Top (OTT) STB |

| Resolutions Covered | HD (High Definition), SD (Standard Definition), UHD (Ultra-High Definition) |

| End Users Covered | Residential, Commercial, Others |

| Service Types Covered | Pay TV, Free-to-Air |

| Distributions Covered | Online Distribution, Offline Distribution |

| Regions Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Set-Top Box Market Research Report and Industry Forecast Report

The India set-top box market size was valued at USD 2.85 Billion in 2025.

The India set-top box market is expected to grow at a compound annual growth rate of 1.80% from 2026-2034 to reach USD 3.46 Billion by 2034.

Cable STB dominated the market with a share of 46%, driven by India’s extensive cable television infrastructure established through the government’s mandatory digitization program and the widespread network of multi-system operators across urban and semi-urban regions.

Key factors driving the India set-top box market include expanding digital broadcasting infrastructure, growing consumer demand for high-definition and interactive entertainment, convergence of telecom and broadcasting services, broadband expansion in semi-urban areas, and rising adoption of hybrid devices.

Major challenges include intensifying competition from smart televisions with built-in streaming capabilities, declining pay television subscriber bases amid cord-cutting trends, regulatory complexities around evolving tariff frameworks, and the growing substitution effect of affordable streaming devices.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)