India Sleepwear Market Size, Share, Trends and Forecast by Product Type, Material, Distribution Channel, End User, and Region, 2026-2034

India Sleepwear Market Summary:

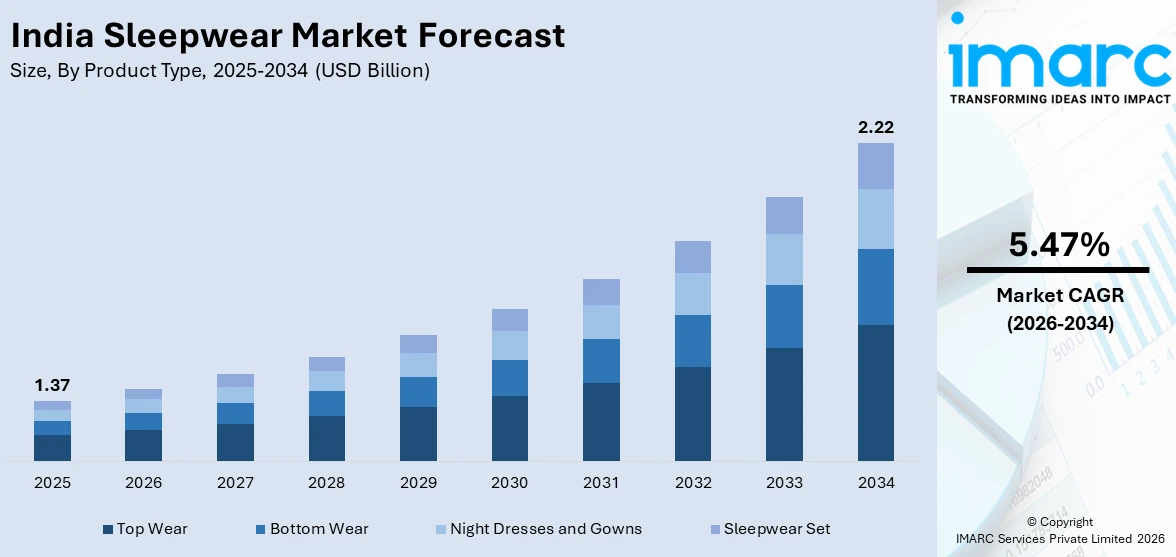

The India sleepwear market size was valued at USD 1.37 Billion in 2025 and is projected to reach USD 2.22 Billion by 2034, growing at a compound annual growth rate of 5.47% from 2026-2034.

The India sleepwear market is experiencing robust expansion driven by evolving consumer lifestyles and a growing preference for comfortable, stylish nightwear across all demographics. Increasing urbanization, rising disposable incomes, and the influence of social media on fashion choices are reshaping demand patterns. The expansion of digital retail channels and direct-to-consumer brands is further accelerating product accessibility, fueling sustained India sleepwear market share.

Key Takeaways and Insights:

- By Product Type: Top wear dominates the market with a share of 33% in 2025, owing to its versatility, affordability, and high replacement rate across demographics. Consumers increasingly prefer loose-fitting, breathable tops for sleep and casual home use, driving sustained demand.

- By Material: Cotton leads the market with a share of 60% in 2025, driven by its natural breathability, softness, and suitability for India’s tropical climate. Consumer preference for hypoallergenic and moisture-absorbing fabrics reinforces cotton’s dominance in sleepwear.

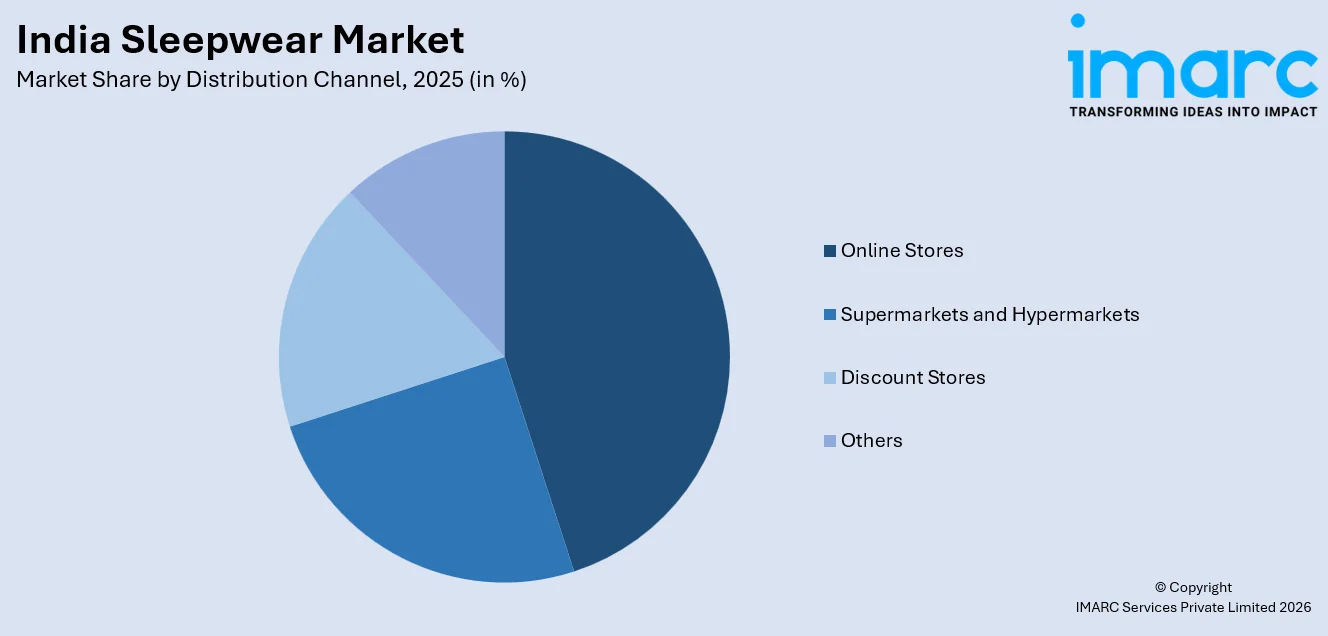

- By Distribution Channel: Online stores represent the largest segment with a market share of 42% in 2025, reflecting the rapid growth of e-commerce platforms, wider product selection, competitive pricing, and the convenience of doorstep delivery that appeals to digitally savvy consumers.

- By End User: Women hold the largest segment with a share of 49% in 2025, driven by increasing fashion consciousness, demand for stylish yet comfortable nightwear, and expanding product ranges tailored to diverse preferences across age groups.

- By Region: North India exhibits a clear dominance in the market with 30% share in 2025, driven by higher urbanization rates, concentration of metropolitan populations in Delhi-NCR and surrounding cities, and greater disposable income levels supporting premium sleepwear purchases.

- Key Players: Key players drive the India sleepwear market by expanding product portfolios, enhancing fabric innovation, strengthening omnichannel distribution networks, and leveraging digital marketing. Their investments in brand building, affordability, and partnerships with e-commerce platforms boost consumer awareness and accelerate adoption across diverse market segments.

To get more information on this market Request Sample

The India sleepwear market is advancing as consumers increasingly prioritize comfort-driven fashion, self-care routines, and versatile nightwear that transitions seamlessly between home and casual settings. The convergence of athleisure influences with traditional sleepwear is creating innovative product categories that appeal to younger demographics seeking both functionality and aesthetic appeal. The expansion of organized retail and branded sleepwear is disrupting a historically unbranded market, with established apparel companies entering the category to capture significant value. The Union Budget 2025-26 announced a five-year Cotton Productivity Mission aimed at boosting domestic cotton output and promoting extra-long staple varieties, which is expected to stabilize raw material availability and strengthen the textile supply chain supporting sleepwear manufacturing. Digital platforms and influencer-driven marketing are transforming consumer discovery and purchase patterns, enabling brands to reach tier-two and tier-three cities effectively. The growing emphasis on sleep wellness, sustainable fabrics, and personalized nightwear experiences continues to propel the India sleepwear market growth across all consumer segments nationwide.

India Sleepwear Market Trends:

Rise of Athleisure-Inspired Sleepwear Designs

The blurring lines between sleepwear, loungewear, and casual fashion is essentially revolutionizing product design in the Indian market. The new-age consumer is now demanding nightwear that can seamlessly shift from a home environment to a social setting or even a short outing. As a result, the industry is now focusing on developing nightwear that is performance-oriented and has a modern silhouette. This has also led to a change in the way the industry approaches retail, with brands now focusing on experiential retail and hybrid retail models.

Growth of Direct-to-Consumer Sleepwear Brands

The emergence of digital-first sleepwear brands is transforming the competitive landscape as new entrants leverage social media, influencer partnerships, and e-commerce platforms to build loyal customer bases. These brands focus on niche positioning, personalized offerings, and community engagement to differentiate from traditional retailers. In July 2025, Indian sleepwear brand Ammarzo announced its global expansion through online platforms, targeting premium consumers while aiming for INR 100 crore revenue by FY30, demonstrating the scalability of D2C models in the sleepwear segment.

Increasing Demand for Sustainable and Organic Sleepwear

Consumer awareness around sustainable fashion is extending into the sleepwear category, with growing demand for organic cotton, bamboo fiber, and recycled materials. Brands are responding by incorporating eco-friendly production practices and transparent sourcing into their value propositions. India’s textile market size was valued at USD 152.40 Billion in 2025 and is projected to reach USD 213.75 Billion by 2034, growing at a compound annual growth rate of 3.83% from 2026-2034, with sustainability and energy efficiency standards increasingly shaping production. Several new eco-conscious fashion startups emerged in India, signaling strong momentum toward ethical and environmentally responsible sleepwear manufacturing.

Market Outlook 2026-2034:

The India sleepwear market is poised for growth over the forecast period, driven by favorable demographic trends, increasing consumer expenditure on lifestyle products, and the rising trend of adopting branded sleepwear. The penetration of e-commerce platforms in the semi-urban and rural markets is expected to unlock substantial untapped demand in the India sleepwear market, and technological advancements in textile innovation will allow manufacturers to develop differentiated products. Strategic investments in brand development, omnichannel, and sustainable manufacturing practices are expected to improve competitive positioning in the India sleepwear market. The market generated a revenue of USD 1.37 Billion in 2025 and is projected to reach a revenue of USD 2.22 Billion by 2034, growing at a compound annual growth rate of 5.47% from 2026-2034.

India Sleepwear Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Top Wear |

33% |

|

Material |

Cotton |

60% |

|

Distribution Channel |

Online Stores |

42% |

|

End User |

Women |

49% |

|

Region |

North India |

30% |

Product Type Insights:

- Top Wear

- Bottom Wear

- Night Dresses and Gowns

- Sleepwear Set

Top wear dominates with a market share of 33% of the total India sleepwear market in 2025.

Top wear continues to lead the India sleepwear market due to the demand for light, comfortable sleep tops, T-shirts, and camisoles. The high replacement rate of top wear due to the desire to upgrade one’s sleepwear collection also helps the market. The affordability of top wear compared to complete sleepwear sets is another factor that contributes to the repeat business in the market. The increasing use of social media platforms and fashion influencers has raised the bar for sleepwear design, with graphic prints and character-based designs becoming extremely popular among the younger generation.

The top wear category is growing as consumers become more receptive to the idea of sleepwear as a dual-functional garment that can be worn both at night and during the day. This trend has led manufacturers to incorporate innovative fabric combinations and contemporary cuts that are able to fill the gap between comfort wear and streetwear. By moving away from the conventional notion of pajamas, these functional garments have been able to meet the growing demand for high-end loungewear and are thus one of the fundamental pillars of the contemporary apparel industry.

Material Insights:

- Cotton

- Wool

- Silk

- Others

Cotton leads with a share of 60% of the total India sleepwear market in 2025.

The dominance of cotton in the India sleepwear market can be attributed to its unique properties of breathability, moisture absorption, and softness, which make it the most suitable fabric for the India climate, which is largely warm and humid. The hypoallergenic nature of the cotton fiber and its ease of maintenance are additional factors that contribute to the loyalty of consumers towards the product. The fact that India is the world’s largest producer of cotton ensures a steady supply of cotton to the industry at favorable prices. The government’s Kasturi Cotton Bharat brand promotion program is also helping to create a premium image for Indian cotton.

The cotton sleepwear category is gaining popularity as consumers increasingly demand natural, chemical-free fabrics that fit the wellness and sustainability trend. Organic cotton is particularly popular with high-end consumers who are looking for sustainable sleepwear. The large production base in India gives a substantial raw material cost advantage, which is now further strengthened by a national mission to enhance cotton productivity. The mission focuses on developing high-quality, long-staple cotton through biotechnology and advanced breeding.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Online Stores

- Discount Stores

- Others

Online stores represent the largest share with 42% of the total India sleepwear market in 2025.

The online stores segment commands the largest share in the India sleepwear distribution landscape, driven by the explosive growth of e-commerce platforms that offer consumers unparalleled product variety, competitive pricing, and doorstep delivery convenience. Digital channels enable brands to reach consumers in tier-two and tier-three cities that traditionally lacked access to branded sleepwear. The proliferation of flash sales, festive discounts, and easy return policies has significantly lowered purchase barriers and encouraged first-time online buyers to explore sleepwear categories on major platforms.

The online shopping strength in the sleepwear distribution space is further accentuated by the increasing impact of social media marketing, influencer partnerships, and recommendation algorithms that help consumers discover new products. The fashion e-commerce industry in India is expected to grow at a very aggressive rate in the coming decade, thereby offering ample room for the growth of the sleepwear industry in the online shopping space. The foray of quick commerce players in the fashion delivery space is further reducing delivery times.

End User Insights:

- Men

- Women

- Kids

Women hold the largest segment with a 49% share of the total India sleepwear market in 2025.

The women’s segment maintains its leading position in the India sleepwear market, driven by increasing fashion consciousness, rising participation of women in the workforce, and expanding product innovation tailored to diverse lifestyle needs. Women consumers demonstrate higher engagement with sleepwear as a fashion category, seeking products that combine comfort with contemporary aesthetics for nighttime wear and home lounging. The growing emphasis on self-care rituals and wellness routines has further elevated demand for premium and designer nightwear among urban women.

The segment is further bolstered by the proliferation of women-focused sleepwear brands that offer specialized products including maternity nightwear, feeding-friendly designs, and inclusive sizing options. In September 2024, SD Retail Limited, specializing in sleepwear under the Sweet Dreams brand that primarily targets modern Indian women, raised INR 64.98 Crores through its IPO on NSE Emerge, with plans to expand its exclusive brand outlet network and enhance product offerings. The brand’s success underscores the substantial commercial opportunity in women’s sleepwear, where branded offerings are increasingly displacing unorganized alternatives.

Regional Insights:

- North India

- South India

- East India

- West India

North India exhibits a clear dominance in the market with a 30% share of the total India sleepwear market in 2025.

The largest market share in the India sleepwear market is held by North India, which is driven by the presence of large urban populations in Delhi-NCR, Chandigarh, Jaipur, and Lucknow. The region also has higher disposable income levels and a well-developed retail infrastructure, including both offline and online shopping platforms, which helps to create a strong demand for sleepwear products in the mid and premium segments. Seasonal changes with a clear distinction between cold winters and other seasons also help to increase the sales of sleepwear products such as flannel pajamas.

The dominance of the market is further aided by the presence of prominent fashion retail hubs and distribution channels that act as a launchpad for new entrants in the Indian sleepwear market. The consumer expenditure in tier two and tier three cities in the northern states has witnessed a substantial rise from 2022 to 2024, with greater exposure to international fashion trends through digital media driving the fashion industry in these regions. The presence of textile manufacturing clusters in the states of Punjab and Rajasthan further aids the production of sleepwear in the North India market.

Market Dynamics:

Growth Drivers:

Why is the India Sleepwear Market Growing?

Expanding E-Commerce and Digital Retail Penetration

The rapid expansion of e-commerce platforms is fundamentally transforming sleepwear distribution in India, enabling brands to access consumers across geographic and economic segments with unprecedented efficiency. Digital retail channels provide sleepwear manufacturers with cost-effective means to showcase extensive product catalogs, engage customers through personalized recommendations, and convert sales through seamless checkout experiences. The growing adoption of mobile commerce and social commerce is particularly significant, as consumers increasingly discover and purchase sleepwear through Instagram shops, influencer recommendations, and platform-native content. India’s e-commerce market size reached USD 129.72 Billion in 2025 and is projected to reach USD 651.10 Billion by 2034, growing at a compound annual growth rate of 19.63% from 2026-2034, with the fashion and apparel category accounting for a substantial share of this growth. Quick commerce platforms are further compressing delivery timelines, enabling same-day or next-day sleepwear delivery that appeals to convenience-driven urban consumers and supports impulse purchasing behavior.

Rising Disposable Incomes and Urbanization

India’s accelerating urbanization and rising household incomes are creating favorable conditions for sleepwear market expansion by elevating consumer spending capacity and shifting purchasing priorities toward lifestyle-oriented products. Urban consumers with higher disposable incomes are willing to invest in branded, comfortable, and aesthetically appealing sleepwear, moving away from traditional unbranded alternatives that historically dominated the market. The expanding middle class is driving demand across multiple price points, from value-oriented cotton basics to premium designer collections. Consumer spending in tier-two and tier-three cities across India grew between 4.5-6.5% in 2024, with increased exposure to global trends through digital platforms driving fashion consumption in these emerging markets. This geographic democratization of fashion awareness is creating new growth frontiers for sleepwear brands seeking to expand beyond traditional metropolitan strongholds.

Increasing Fashion Consciousness and Self-Care Culture

The growing cultural emphasis on self-care, wellness, and personal grooming in India is reshaping consumer attitudes toward sleepwear, elevating it from a functional necessity to a lifestyle fashion category. Social media platforms and wellness influencers are promoting the importance of quality sleep hygiene, comfortable nightwear, and intentional bedtime routines, driving consumer investment in premium sleepwear. The work-from-home trend has further blurred boundaries between workwear and homewear, increasing the daily visibility and importance of comfortable, presentable sleepwear. In September 2024, Raymond Lifestyle Ltd. launched Sleepz by Raymond, a dedicated men’s sleepwear brand targeting the largely unorganized sleepwear market, with revenue projections of INR 500-700 Crore by FY27. The entry of an established legacy brand into the sleepwear category validates the growing consumer sophistication and commercial potential of the segment, signaling a broader industry-level shift toward branded nightwear in India.

Market Restraints:

What Challenges the India Sleepwear Market is Facing?

Intense Competition from the Unorganized Sector

The India sleepwear market remains heavily dominated by unorganized local manufacturers and small-scale tailors who offer low-cost nightwear products without brand premiums. These unbranded alternatives capture significant consumer spending, particularly in semi-urban and rural areas where price sensitivity outweighs brand preference. The fragmented nature of this competition makes it challenging for organized players to build consistent market share and justify premium pricing strategies across all geographies.

Fluctuating Raw Material Costs

Volatility in cotton and synthetic fiber prices directly impacts sleepwear production economics, squeezing manufacturer margins and complicating pricing strategies. Cotton price fluctuations driven by monsoon variability, pest infestations, and global commodity cycles create uncertainty in input costs. Sleepwear manufacturers, particularly smaller enterprises, face difficulties in absorbing these cost variations without passing increases to price-sensitive consumers, potentially dampening demand in the value segment.

Overlap with Loungewear and Casualwear Categories

The increasing convergence between sleepwear, loungewear, and casual home attire creates category ambiguity that dilutes sleepwear-specific brand positioning and marketing effectiveness. Consumers frequently substitute dedicated sleepwear with athleisure or casual clothing, reducing the perceived need for specialized nightwear purchases. This overlap intensifies cross-category competition, making it challenging for sleepwear-focused brands to establish clear differentiation and justify dedicated product development investments.

Competitive Landscape:

The India sleepwear market is turning out to be more and more competitive with the entry of established apparel conglomerates and also new direct-to-consumer brands. Brands are focusing on innovation, differentiation through fabrics, and omnichannel distribution to corner market share in a largely unorganized market. Online marketing prowess and influencer partnerships have become the new key to success, allowing brands to create consumer awareness and loyalty on a large scale. Investments in exclusive brand-owned stores, e-commerce optimization, and geographic expansion into tier-two and tier-three cities are dramatically changing the landscape, with competition increasingly being driven by design innovation, sustainability, and consumer experience excellence.

Recent Developments:

- In July 2024, Clovia, a leading Indian lingerie and sleepwear brand backed by Reliance Retail, launched a new sleepwear collection featuring the iconic Garfield character. The collection emphasized comfort with 100% cotton T-shirts and oversized pajama pants while the brand continued expanding its physical retail presence across multiple Indian cities.

India Sleepwear Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Type Covered | Top Wear, Bottom Wear, Night Dresses and Gowns, Sleepwear Set |

| Materials Covered | Cotton, Wool, Silk, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Online Stores, Discount Stores, Others |

| End Users Covered | Men, Women, Kids |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Sleepwear Market Report

The India sleepwear market size was valued at USD 1.37 Billion in 2025.

The India sleepwear market is expected to grow at a compound annual growth rate of 5.47% from 2026-2034 to reach USD 2.22 Billion by 2034.

Top wear dominated the market with a share of 33%, driven by its versatility, affordability, high replacement frequency, and growing consumer preference for fashionable yet comfortable sleep tops across all demographic segments.

Key factors driving the India sleepwear market include expanding e-commerce penetration, rising disposable incomes, increasing urbanization, growing fashion consciousness, self-care culture influence, and the shift from unbranded to organized branded sleepwear products.

Major challenges include intense competition from the unorganized sector, fluctuating raw material costs, category overlap with loungewear, price sensitivity among consumers, limited brand awareness in rural markets, and inconsistent sizing standards.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)