India Small Hydropower Market Size, Share, Trends and Forecast by Capacity, Component, and Region, 2026-2034

India Small Hydropower Market Summary:

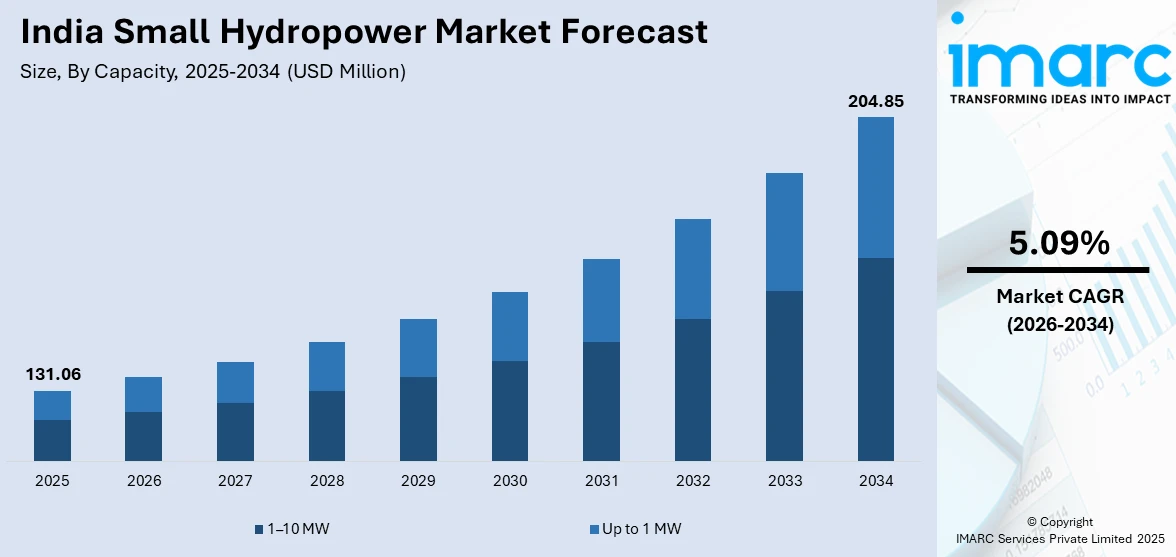

The India small hydropower market size was valued at USD 131.06 Million in 2025 and is projected to reach USD 204.85 Million by 2034, growing at a compound annual growth rate of 5.09% from 2026-2034.

The India small hydropower market is experiencing sustained expansion driven by favorable government policies, abundant water resources in hilly terrain, and the growing emphasis on decentralized renewable energy solutions. Rising electricity demand in rural and remote areas, combined with the push toward rural electrification and clean energy transition, is strengthening market adoption. Technological advancements in turbine efficiency, digital monitoring systems, and grid integration capabilities are enhancing operational performance. The strategic focus on modernizing existing plants and developing untapped potential across northern and northeastern states is positioning small hydropower as a reliable component of India's diversified energy portfolio, contributing to the India small hydropower market share.

Key Takeaways and Insights:

- By Capacity: The 1–10 MW dominates the market with a share of 58% in 2025, driven by superior cost efficiency per kilowatt, higher head utilization, and greater installed capacity potential compared to sub-1 MW installations.

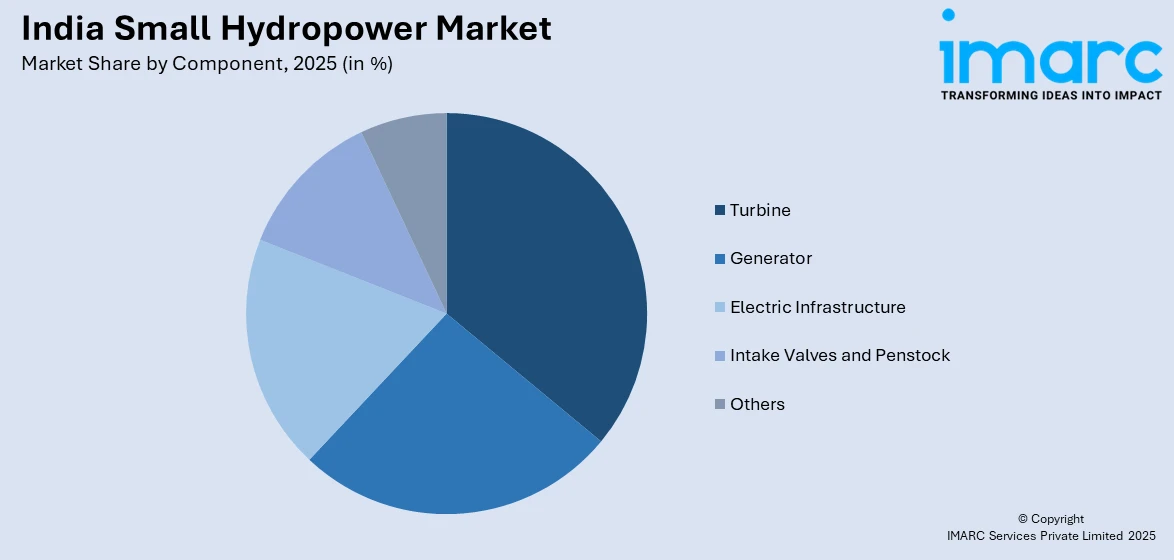

- By Component: Turbine leads the market with a share of 31% in 2025, representing the critical electromechanical equipment that converts water flow into mechanical energy for electricity generation.

- By Region: South India represents the largest segment with a market share of 35% in 2025, benefiting from favorable terrain in the Western Ghats, proactive state-level policies, and established hydropower infrastructure in Karnataka and Tamil Nadu.

- Key Players: The India small hydropower market exhibits moderate competitive intensity, with public sector undertakings and specialized equipment manufacturers competing alongside regional developers. Established players focus on indigenous technology development, modernization services, and comprehensive project execution capabilities.

To get more information on this market Request Sample

The India small hydropower market is progressing steadily as the country seeks to harness its significant untapped resource potential across numerous identified locations. Supportive government programs and policy measures are encouraging project development by improving financial viability and easing implementation challenges. These efforts are helping to promote wider adoption of small hydropower as a reliable renewable energy source, contributing to energy diversification, regional development, and long-term sustainability goals. For instance, in February 2025, the Arunachal Pradesh government reviewed its small hydropower initiatives, allocating 35 projects totaling 570.75 MW with an expected investment of INR 7,000 crore and potential creation of 7,500 jobs. The market benefits from small hydropower's inherent advantages including low environmental footprint, minimal land disruption, and suitability for decentralized power generation in remote communities. State-specific development models in regions like Himachal Pradesh, Karnataka, and the northeastern states are accelerating project deployment through streamlined approvals and localized stakeholder engagement.

India Small Hydropower Market Trends:

Shift Toward Modernization and Digital Upgradation of Existing Plants

India is placing greater emphasis on modernizing existing small hydropower facilities to improve operational efficiency and long-term reliability. Many older plants continue to operate with aging turbines and worn infrastructure, prompting developers to undertake refurbishment initiatives. These efforts typically include upgrading electromechanical equipment, optimizing water flow management, and integrating digital monitoring and control systems. Such improvements help extend asset life, enhance performance, and lower operating expenses. The growing focus on refurbishment and repowering is creating meaningful opportunities for market growth by improving the productivity and sustainability of the existing small hydropower fleet.

Integration of Climate-Resilient Infrastructure Solutions

The industry is increasingly focusing on climate-resilient infrastructure to mitigate operational challenges caused by changing hydrological conditions. Fluctuations in monsoon patterns and inconsistent river flows are encouraging developers to adopt adaptive engineering approaches such as flexible turbine designs, strengthened intake systems, and improved sediment control solutions. Greater use of hydrological modeling during the planning stage allows projects to account for multiple climate scenarios, supporting more robust plant design and stable operations. This shift toward climate-adaptive engineering is helping improve long-term reliability, reduce risk exposure, and enhance the sustainability of hydropower assets.

Emergence of State-Specific Small Hydropower Development Policies

States are developing tailored policies to encourage small hydropower development reflecting regional resource profiles and governance approaches. For instance, in August 2024, Tamil Nadu released its Small Hydel Policy permitting private entities to participate in projects ranging from 100 kW to 10 MW, offering incentives including electricity duty exemptions and stamp duty concessions. Himachal Pradesh follows a consent-based model involving local stakeholders for smooth land acquisition, while Karnataka leverages public-private partnerships for rapid capacity growth. These localized approaches are creating favorable investment environments and accelerating deployment across diverse geographic and regulatory landscapes.

Market Outlook 2026-2034:

The India small hydropower market outlook remains positive as the sector benefits from renewed government attention and infrastructure investments. The Ministry of New and Renewable Energy is preparing to revive the small hydropower scheme with a targeted capacity addition of 1.5 GW and proposed funding of INR 2,500 crore in the upcoming budget. Focus regions include Arunachal Pradesh, Himachal Pradesh, Uttarakhand, and Ladakh where abundant water resources and terrain provide optimal conditions. The market generated a revenue of USD 131.06 Million in 2025 and is projected to reach a revenue of USD 204.85 Million by 2034, growing at a compound annual growth rate of 5.09% from 2026-2034.

India Small Hydropower Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Capacity |

1–10 MW |

58% |

|

Component |

Turbine |

31% |

|

Region |

South India |

35% |

Capacity Insights:

- Up to 1 MW

- 1–10 MW

1–10 MW dominates with a market share of 58% of the total India small hydropower market in 2025.

The 1–10 MW capacity segment commands the largest market share owing to superior economics and operational advantages. Projects in this range benefit from lower investment costs per kilowatt compared to sub-1 MW installations while maintaining manageable project complexity. The segment attracts substantial private sector investment due to favorable returns and established financing mechanisms. State nodal agencies focus on this capacity range for grid-connected projects, while government support through capital subsidies for installations within 1 MW to 25 MW helps improve project feasibility and attractiveness for developers.

The segment’s strong position is supported by its adaptability to varied geographic conditions, particularly across India’s hilly and riverine regions. Medium-scale hydropower installations have demonstrated effective implementation in such terrains, offering a balanced approach to power generation. These projects combine efficient capacity utilization with manageable grid integration and adherence to environmental norms. As a result, they are increasingly favored for deployment under both public initiatives and private development strategies, making them a practical and scalable solution across northern and southern parts of the country.

Component Insights:

To get more information on this market Request Sample

- Turbine

- Generator

- Electric Infrastructure

- Intake Valves and Penstock

- Others

Turbine leads with a share of 31% of the total India small hydropower market in 2025.

Turbines represent the core electromechanical equipment in small hydropower installations, converting the kinetic energy of flowing water into mechanical power for electricity generation. The segment's market leadership reflects the critical role of turbine technology in determining plant efficiency, capacity utilization, and long-term operational performance. Domestic manufacturers have developed indigenous turbine designs suited to India's specific water resources and head conditions.

Technological advancements are driving segment growth as manufacturers introduce improved turbine configurations. For instance, in September 2024, BHEL announced a major contract to supply turbine equipment for multiple hydroelectric projects, reinforcing its position as a key supplier to India's small-to-mid-scale hydro market. International players, including are expanding localized production capabilities, introducing advanced designs such as variable-flow systems and fish-friendly turbines. These innovations support modernization initiatives and enable energy generation in previously non-viable locations with varying water flow conditions.

Regional Insights:

- North India

- South India

- East India

- West India

South India exhibits a clear dominance with a 35% share of the total India small hydropower market in 2025.

South India commands the largest regional market share, benefiting from favorable terrain across the Western Ghats, established hydropower infrastructure, and proactive state-level policies. Karnataka and Tamil Nadu lead regional development with substantial installed capacities and ongoing project pipelines. The region benefits from diversified river systems including the Bhavani, Kundah, and Moyar rivers, that provide consistent water resources for run-of-river installations.

State governments in the region are promoting small hydropower development through supportive policies and incentives that encourage private sector participation. Regional initiatives include medium- to large-scale projects that reflect significant investment in renewable infrastructure. Authorities are also exploring advanced technologies, such as AI-driven systems for load forecasting and water flow optimization, to enhance operational efficiency, improve plant performance, and maintain grid stability. These measures underscore the region’s proactive approach in combining policy support with technological innovation to drive sustainable growth in the small hydropower sector.

Market Dynamics:

Growth Drivers:

Why is the India Small Hydropower Market Growing?

Government Policy Support and Financial Incentives

Government support continues to be a key driver of India’s small hydropower market, with policies, financial incentives, and streamlined regulations encouraging project development. Subsidies and capital assistance for small- and medium-scale projects lower entry barriers, while tax benefits, reduced duties, and faster approvals enhance project feasibility. Revised guidelines simplify procedural requirements and link financial assistance to performance, further improving viability. Combined with preferential tariffs and exemptions for smaller installations, these measures reduce administrative challenges and create a favorable environment for private investment, fostering growth and expansion in the small hydropower sector.

Abundant Untapped Hydropower Potential Across Hilly Regions

India holds significant untapped small hydropower potential, estimated at approximately 21,133 MW across more than 7,133 identified sites, with less than 25% of this capacity currently utilized. A significant portion of India’s small hydropower potential is concentrated in hilly and riverine states, while several plains regions also offer considerable opportunities. This largely untapped resource base presents strong growth prospects as states focus on developing renewable energy infrastructure. Regional initiatives are increasingly allocating projects and resources to harness local hydropower potential, supporting national objectives such as energy security, rural electrification, and sustainable development. The northeastern region holds vast capacity in river basins, highlighting its strategic importance for expanding small hydropower generation across the country.

Rising Demand for Decentralized Rural Electrification Solutions

Small hydropower projects are playing an increasingly important role in meeting electricity needs in remote and rural areas where grid connectivity is limited or unreliable. These plants provide stable, dispatchable power, offering greater reliability compared with intermittent renewable sources. Beyond energy generation, small hydropower supports local development by enabling infrastructure improvements, such as roads, bridges, and transmission lines, and by creating employment opportunities that help reduce rural-to-urban migration. Its scalable design and low land impact make it well-suited for powering irrigation, water treatment, and small enterprises in agricultural and hilly regions.

Market Restraints:

What Challenges the India Small Hydropower Market is Facing?

Environmental and Social Concerns in Project Implementation

Although small hydropower developments are not as invasive as large hydro projects are, they are becoming less popular because of environmental and social issues. There may be significant environmental implications of the projects in the delicate mountainous scenery, including local ecology and river course. The non-existence of extensive environmental tests and communication of a community in certain areas raises the level of suspicion, which may cause delays, the negative reaction of the population, or the limitations of the policy, which will delay the implementation of a project.

Hydrological Variability and Climate-Related Risks

Hydropower generation and the overall project feasibility are very much affected by seasonal changes in water availability and changes in monsoon patterns. Unpredictable rainfall, weather extremities and environmental deformities like floods and landslides pose operational uncertainty, especially in mountainous and river-related areas. Also, the development of snowmelt dynamics leads to a further impact on the reliability of water flows. These risks put developers of a project in a more perilous position, make the long-term income prediction more complicated, and can undermine investor trust by making power generation less predictable and the economics of the project harder to control.

Infrastructure Constraints and Project Execution Challenges

Limited transmission infrastructure remains a major barrier to project implementation, causing delays in construction and commissioning. Remote locations often lack adequate access roads, power evacuation facilities, and a skilled local workforce, increasing project costs and timelines. Long gestation periods for development, combined with complex geological conditions in hilly terrain, make projects difficult to justify when compared to faster-deploying solar and wind alternatives.

Competitive Landscape:

The India small hydropower market shows moderate competitive intensity, with public sector entities competing alongside specialized equipment suppliers and regional project developers. The market is shaped by a mix of domestic capabilities and increasing participation from international companies through localized manufacturing, modernization services, and technology partnerships. Competition is largely centered on cost efficiency achieved through standardized and pre-engineered solutions, supported by strong after-sales service networks. Additionally, expertise in digital upgrades, turbine retrofits, and replacement programs is becoming a key differentiator, while strategic collaboration with state agencies and utilities plays an important role in securing project awards and long-term maintenance contracts.

Recent Developments:

- In May 2025, the Ministry of New and Renewable Energy issued revised guidelines for small hydro power schemes, simplifying procedures and addressing ongoing challenges faced by developers. The revised regulations mandate that projects attain a minimum of 80% of their expected generation to qualify for full Central Financial Assistance, while a 12-month grace period has been incorporated to address any unexpected delays.

- In March 2025, the 100 MW UHL-III Hydropower Project in Himachal Pradesh achieved full capacity, marking a significant milestone in the state's renewable energy expansion. The project is expected to generate 392 million units of electricity annually, bringing in an estimated INR 200 crore in revenue, with the state government providing INR 185 crore in No Default Guarantee to expedite completion.

India Small Hydropower Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Capacities Covered | Up to 1 MW, 1–10 MW |

| Components Covered | Turbine, Generator, Electric Infrastructure, Intake Valves and Penstock, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Small Hydropower Market Report

The India small hydropower market size was valued at USD 131.06 Million in 2025.

The India small hydropower market is expected to grow at a compound annual growth rate of 5.09% from 2026-2034 to reach USD 204.85 Million by 2034.

The 1–10 MW capacity dominates the market with a 58% share in 2025, driven by superior cost economics, favorable government subsidies of up to 30%, and an optimal balance between capacity utilization and project complexity for grid-connected installations.

Key factors driving the India small hydropower market include government policy support and capital subsidies from MNRE, abundant untapped potential across hilly regions, rising demand for decentralized rural electrification, and technological advancements in turbine efficiency and digital monitoring systems.

Major challenges include environmental and social concerns during project implementation, hydrological variability and climate-related risks affecting generation capacity, limited transmission infrastructure in remote areas, long project gestation periods, and shortage of skilled local workforce for plant operations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)