India Solar PV Module Market Size, Share, Trends and Forecast by Technology, Product Type, Connectivity, Mounting, End Use, and Region, 2026-2034

India Solar PV Module Market Summary:

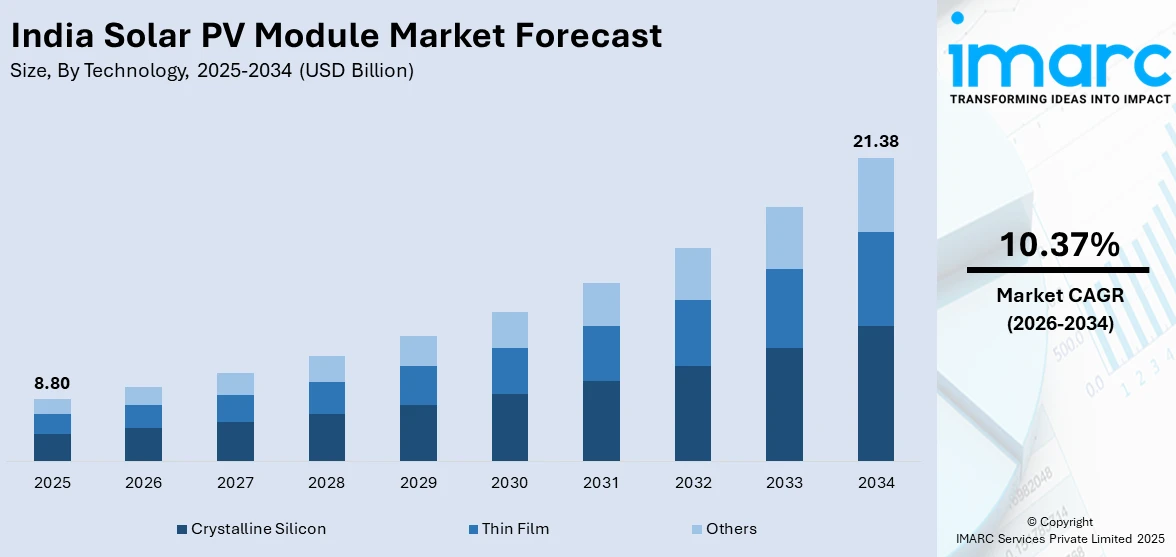

The India solar PV module market size was valued at USD 8.80 Billion in 2025 and is projected to reach USD 21.38 Billion by 2034, growing at a compound annual growth rate of 10.37% from 2026-2034.

The market is driven by the favorable government policies that encourage the use of renewable energy sources, such as the ambitious solar capacity addition plans under the national solar mission. The growing demand for electricity, awareness about the environment, and the need for sustainable energy solutions are also driving the market. In addition, the advancements in module efficiency, declining production costs, and the availability of local manufacturing capacity are also driving the market.

Key Takeaways and Insights:

- By Technology: Crystalline silicon dominates the market with a share of 77% in 2025, driven by superior energy conversion efficiency, proven long-term reliability, and cost-effectiveness in utility-scale applications.

- By Product Type: Monocrystalline leads the market with a share of 55% in 2025, owing to amplified efficiency rates, improved performance in confined spaces, and reduced manufacturing costs.

- By Connectivity: On-grid represents the largest segment with a market share of 84% in 2025, driven by established electricity infrastructure, net metering incentives, and lower system costs.

- By Mounting: Ground mounted dominates the market with a share of 65% in 2025, owing to the proliferation of utility-scale projects, availability of land in solar parks, and ease of maintenance.

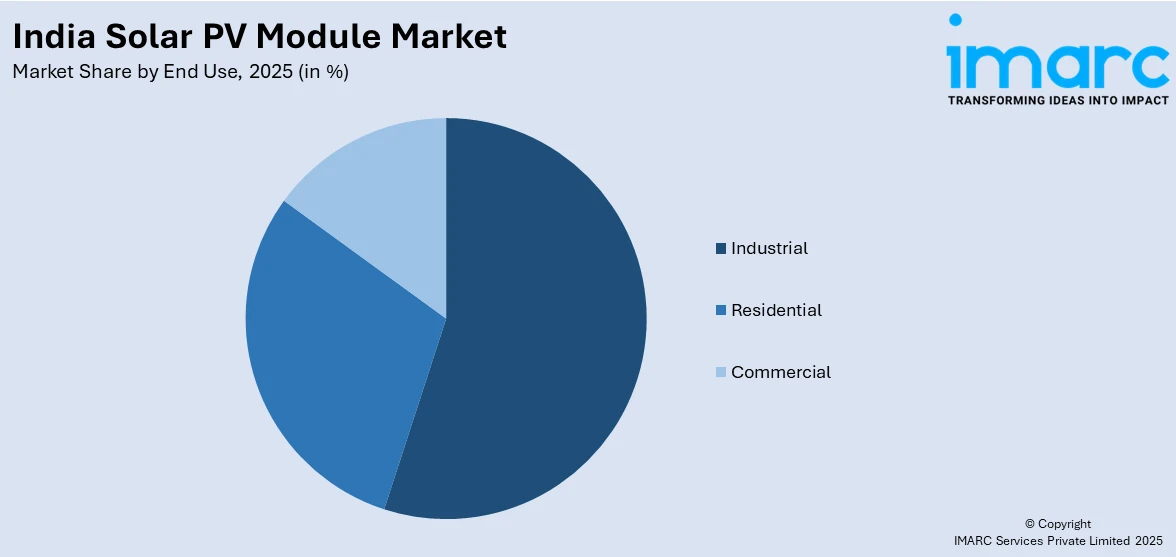

- By End Use: Industrial represents the largest segment with a market share of 38% in 2025, driven by high energy consumption requirements, corporate sustainability commitments, and favorable open-access policies.

- By Region: South India leads the market with a share of 32% in 2025, driven by favorable solar irradiance levels, progressive state policies, and concentration of manufacturing establishments.

- Key Players: The India solar PV module market exhibits a competitive landscape with both domestic manufacturers and international players vying for market position. Market participants are focusing on capacity expansion, technology upgrades, and backward integration across the value chain.

To get more information on this market Request Sample

The India solar PV module market is experiencing transformative growth driven by the government's ambitious renewable energy targets and supportive policy framework. The push for domestic manufacturing self-reliance has catalyzed significant capacity expansion, with manufacturers investing heavily in advanced technologies including TOPCon and bifacial modules. According to reports, in 2025, Waaree Energies led the market with approximately 1.4 GW of solar module shipments in India, the highest volume among all suppliers. Moreover, rising electricity tariffs and increasing industrial energy consumption are accelerating adoption across commercial and industrial segments. The establishment of large-scale solar parks and progressive state-level policies are facilitating ground-mounted installations, while rooftop solar programs are expanding residential adoption. Growing environmental awareness and corporate sustainability goals are further propelling demand. The favorable regulatory environment, including production-linked incentives and quality assurance frameworks, is strengthening the domestic manufacturing ecosystem and reducing import dependence, positioning India as a key player in the global solar manufacturing landscape.

India Solar PV Module Market Trends:

Transition Toward Advanced High-Efficiency Module Technologies

The India solar PV module market is witnessing a significant shift toward next-generation technologies as manufacturers and developers seek improved energy output and performance. Advanced cell architectures including TOPCon and heterojunction technologies are gaining prominence, offering enhanced efficiency compared to conventional PERC cells. In September 2025, Mercom reported India added 44.2 GW solar module and 7.5 GW cell capacity in H1 2025, led by 39.9 GW TOPCon and first-time 1.2 GW HJT additions. Furthermore, this transition is driven by the need to maximize power generation from limited land resources and optimize levelized cost of energy.

Accelerated Domestic Manufacturing and Backward Integration

The market is experiencing rapid expansion in domestic manufacturing capabilities as India pursues energy self-reliance and reduced import dependence. Module manufacturers are increasingly pursuing backward integration into cell, wafer, and ingot production to strengthen supply chain resilience and improve cost competitiveness. In 2025, the government reported that the Production-Linked Incentive scheme had enabled 18.5 GW of solar module, 9.7 GW of cell, and 2.2 GW of ingot-wafer capacity by June 2025, reinforcing policy support for integrated manufacturing. This vertical integration trend is supported by government incentives and policy frameworks that encourage localized value chain development.

Rising Adoption of Bifacial and Large-Format Modules

The India solar PV module market is observing growing preference for bifacial modules and large-format configurations across utility-scale and commercial installations. Bifacial modules capture reflected sunlight from both sides, enhancing energy yield particularly in ground-mounted applications with reflective surfaces. In December 2025, ADM Solar Power supplied 200 MW of bifacial PV modules for large utility‑scale projects in Gujarat and Maharashtra, reflecting growing adoption of bifacial technology in India’s ground‑mounted solar installations. Simultaneously, the industry is transitioning toward larger wafer sizes and higher wattage modules that reduce balance-of-system costs and improve installation efficiency.

Market Outlook 2026-2034:

The India solar PV module market is set to experience steady growth during the forecast period, owing to the increasing demand for energy and the government's unrelenting efforts to promote the use of renewable energy sources. The market's revenue growth will be fueled by the government's support, reducing prices of solar PV modules, and advancements in technology that improve the efficiency of energy conversion. This will be accompanied by increased investments in solar energy parks and rooftop solar installations. The market generated a revenue of USD 8.80 Billion in 2025 and is projected to reach a revenue of USD 21.38 Billion by 2034, growing at a compound annual growth rate of 10.37% from 2026-2034.

India Solar PV Module Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Technology |

Crystalline Silicon |

77% |

|

Product Type |

Monocrystalline |

55% |

|

Connectivity |

On-Grid |

84% |

|

Mounting |

Ground Mounted |

65% |

|

End Use |

Industrial |

38% |

|

Region |

South India |

32% |

Technology Insights:

- Thin Film

- Crystalline Silicon

- Others

Crystalline silicon dominates with a market share of 77% of the total India solar PV module market in 2025.

Crystalline silicon technology continues to command the India solar PV module market owing to its proven reliability, superior energy conversion efficiency, and well-established manufacturing ecosystem. This technology offers excellent long-term performance stability, making it the preferred choice for utility-scale installations and commercial projects requiring predictable energy output over extended operational lifespans. The mature supply chain infrastructure and continuous efficiency improvements through advanced cell architectures further reinforce its market leadership position across all application segments.

The widespread adoption of crystalline silicon modules is supported by declining production costs driven by economies of scale and manufacturing process optimizations. Domestic manufacturers have invested significantly in expanding crystalline silicon production capacity to meet growing demand from government-backed projects and private sector installations. The technology's compatibility with existing infrastructure and installation practices, combined with readily available technical expertise, ensures continued preference among developers seeking reliable and cost-effective solar solutions throughout India.

Product Type Insights:

- Monocrystalline

- Polycrystalline

- Cadmium Telluride

- Amorphous Silicon

- Others

Monocrystalline leads with a share of 55% of the total India solar PV module market in 2025.

Monocrystalline have emerged as the dominant product type in the India solar PV module market, driven by their superior efficiency rates and enhanced performance characteristics. According to reports, in 2024, monocrystalline modules accounted for 59.7% of India’s solar PV module production capacity, making them the largest technology segment in the country’s manufacturing ecosystem. These modules deliver higher power output per unit area, making them particularly attractive for installations with space constraints, including rooftop applications and land-limited commercial facilities.

The preference for monocrystalline is further supported by their improved performance under high-temperature conditions prevalent across much of India. Better temperature coefficients ensure more consistent energy generation during peak summer months when electricity demand is highest. Additionally, declining price differentials compared to polycrystalline alternatives, combined with longer warranty periods and superior aesthetic appeal, are driving increasing adoption. The technology's reliability and enhanced durability make it the preferred choice for long-term solar investments.

Connectivity Insights:

- On-Grid

- Off-Grid

On-grid exhibits a clear dominance with 84% share of the total India solar PV module market in 2025.

On-grid commands the India market, driven by favorable net metering policies that enable consumers to offset electricity bills by exporting excess generation to the grid. In October 2025, the Ministry of Power directed all Indian states to waive separate net-metering agreements and associated charges under the PM Surya Ghar scheme, simplifying rooftop solar adoption nationwide. This connectivity type eliminates the need for expensive battery storage systems, significantly reducing initial investment costs and improving project economics.

The dominance of on-grid is further strengthened by government initiatives that give higher priority to the expansion of grid-connected solar capacity to achieve the country's renewable energy targets. Utility-scale solar farms and commercial systems are mostly designed with on-grid topologies to generate maximum income from power sales agreements with the distribution utilities. The policy environment that promotes open-access agreements further encourages industrial consumers to opt for on-grid solar solutions.

Mounting Insights:

- Ground Mounted

- Roof-Top

Ground mounted leads with a market share of 65% of the total India solar PV module market in 2025.

Ground mounted dominate the India solar PV module market, driven by the proliferation of utility-scale solar parks and mega-projects across states with favorable solar irradiance and land availability. As per sources, in 2025, India added 16.14 GW of ground-mounted solar capacity from April to September, representing the majority of utility-scale installations and highlighting ongoing dominance of large-scale projects. These installations benefit from optimal panel orientation and tilt angles that maximize energy generation throughout the year.

The solar park development scheme launched by the government has also contributed to the increased development of ground-mounted solar projects, as it provides ready-to-use infrastructure such as land, transmission connectivity, and government approvals. The regions of Rajasthan, Gujarat, Karnataka, and Andhra Pradesh have emerged as the biggest hubs for the development of ground-mounted solar projects on a large scale. The economies of scale created in ground-mounted solar projects have made it possible to get competitive tariffs through reverse auctions.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Industrial

Industrial exhibits a clear dominance with a 38% share of the total India solar PV module market in 2025.

The industrial leads the India solar PV module market, driven by high electricity consumption patterns and escalating grid tariffs that create compelling economic rationale for solar adoption. Manufacturing facilities, processing plants, and heavy industries are increasingly deploying solar installations to reduce operational costs and achieve corporate sustainability objectives. Open-access regulations enabling direct power procurement from solar generators have particularly benefited industrial consumers seeking energy cost optimization while meeting renewable purchase obligations mandated by regulatory authorities.

Industrial have the advantage of focused energy demand during daylight hours, thereby ensuring maximum use of the produced solar energy without the need for storage solutions. Industrial consumers have suitable rooftop space or land adjacent to their operations for the installation of large-scale solar power systems. Renewable purchase obligations, which require industrial consumers to purchase their electricity from renewable energy sources, are thus promoting rapid adoption of solar power systems in India.

Regional Insights:

- North India

- South India

- East India

- West India

South India dominates with a market share of 32% of the total India solar PV module market in 2025.

South India leads the regional landscape, driven by favorable solar irradiance levels, progressive state policies, and early-mover advantage in solar capacity development. States including Karnataka, Tamil Nadu, Andhra Pradesh, and Telangana have established robust solar ecosystems with supportive regulatory frameworks, streamlined approval processes, and attractive incentive structures. The concentration of manufacturing industries and commercial establishments in the region creates substantial demand for captive solar installations serving diverse end-use applications across multiple sectors.

The region's leadership position is reinforced by significant investments in solar parks and transmission infrastructure that facilitate large-scale project development. Well-developed banking and financial services ecosystems ensure adequate project financing availability, while the presence of experienced EPC contractors and technical workforce supports efficient project execution. South India's track record of successful solar implementations continues to attract investments from both domestic and international developers, solidifying its position as the leading regional market.

Market Dynamics:

Growth Drivers:

Why is the India Solar PV Module Market Growing?

Government Policy Support and Ambitious Renewable Energy Targets

The India solar PV module market is experiencing robust growth propelled by comprehensive government policy support and ambitious renewable energy targets aimed at achieving substantial non-fossil fuel capacity. The government's commitment is demonstrated through multiple programs including the National Solar Mission, solar park development initiatives, and rooftop solar schemes that collectively create sustained demand for modules across all market segments. In December 2025, around 23.9 Lakh households have adopted rooftop solar systems under the PM Surya Ghar scheme, collectively generating around 7 GW of clean electricity. Moreover, supportive regulatory frameworks including renewable purchase obligations, net metering provisions, and open-access regulations incentivize solar adoption among residential, commercial, and industrial consumers.

Declining Module Costs and Improved Project Economics

Continuous reduction in solar PV module prices is significantly enhancing project economics and accelerating market growth across India. Manufacturing efficiencies, economies of scale, and technological advancements have contributed to substantial cost reductions over recent years, making solar energy increasingly competitive with conventional power sources. In September 2025, ReNew Energy reduced its solar module and cell prices following India’s GST cut from 12 percent to 5 percent, boosting affordability for utility‑scale and rooftop solar projects. Moreover, lower module costs translate into reduced tariffs discovered through competitive auctions, making solar power attractive for distribution companies and bulk consumers. The improved economics are particularly driving adoption among industrial and commercial consumers seeking to reduce electricity expenses while achieving sustainability objectives.

Rising Electricity Demand and Energy Security Concerns

India's escalating electricity demand, driven by economic growth, urbanization, and industrial expansion, is creating significant opportunities for solar PV module deployment. The need to augment power generation capacity to meet growing requirements positions solar energy as a critical component of India's energy mix. Additionally, concerns regarding energy security and reducing dependence on imported fossil fuels are strengthening the case for domestic solar capacity expansion. Solar installations utilizing locally manufactured modules contribute to both energy independence and economic self-reliance.

Market Restraints:

What Challenges the India Solar PV Module Market is Facing?

Grid Integration and Transmission Infrastructure Limitations

The solar PV module market in India is constrained by the lack of adequate transmission infrastructure in areas with strong solar resources. The evacuation capacity constraints at substations and transmission infrastructure lead to curtailment risks for solar power plants, thereby affecting investor confidence and project feasibility. The lengthy process of establishing transmission corridors often trails the addition of solar capacity, resulting in mismatches between solar generation and evacuation capacities.

Land Acquisition Challenges and Regulatory Delays

Land acquisition for ground-mounted solar installations presents significant challenges, including high costs, lengthy procedures, and potential disputes over ownership and usage rights. Agricultural land conversion restrictions and competing land uses create constraints in securing suitable project sites. Additionally, delays in obtaining various regulatory approvals and clearances extend project development timelines, impacting cost projections and contractual commitments.

Import Dependence for Critical Upstream Components

Despite significant progress in domestic module manufacturing, the India solar PV module market remains dependent on imports for critical upstream components including cells, wafers, and polysilicon. This dependence exposes the market to supply chain disruptions, currency fluctuations, and geopolitical uncertainties affecting component availability and pricing. Building domestic capacity for upstream manufacturing requires substantial investments and technology transfer.

Competitive Landscape:

The India solar PV module market exhibits a competitive landscape characterized by the presence of established domestic manufacturers alongside international players seeking market access. Competition is intensifying as manufacturers expand production capacities and pursue backward integration to strengthen competitive positioning. Market participants are differentiating through technology leadership, product efficiency improvements, warranty terms, and after-sales service capabilities. The regulatory framework favoring domestically manufactured modules is reshaping competitive dynamics, creating opportunities for local players while necessitating strategic adaptations by international competitors. Quality certifications, compliance with approved manufacturer lists, and demonstrated track record in executing large-scale projects serve as key competitive parameters.

Recent Developments:

- In December 2025, Emmvee inaugurated a 2.5 GW solar module manufacturing line at its Sulibele facility in Bengaluru, raising its total module capacity to 10.3 GW. The company reported a 193% year-over-year revenue increase in the first half of fiscal 2026, attributed to higher module volumes and operational efficiencies. Construction of a proposed 6 GW integrated solar cell and module facility has also commenced.

India Solar PV Module Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Thin Film, Crystalline Silicon, Others |

| Product Types Covered | Monocrystalline, Polycrystalline, Cadmium Telluride, Amorphous Silicon, Others |

| Connectivities Covered | On-Grid, Off-Grid |

| Mountings Covered | Ground Mounted, Roof-Top |

| End Uses Covered | Residential, Commercial, Industrial |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Solar PV Module Market Report

The India solar PV module market size was valued at USD 8.80 Billion in 2025.

The India solar PV module market is expected to grow at a compound annual growth rate of 10.37% from 2026-2034 to reach USD 21.38 Billion by 2034.

Crystalline silicon held the largest India solar PV module market share, driven by superior energy conversion efficiency, proven long-term reliability, well-established manufacturing infrastructure, and cost-effectiveness for utility-scale applications.

Key factors driving the India solar PV module market include supportive government policies, ambitious renewable energy targets, declining module costs, rising electricity demand, energy security concerns, expanding domestic manufacturing, and growing corporate sustainability commitments.

Major challenges include grid integration constraints, transmission infrastructure limitations, land acquisition difficulties, regulatory approval delays, import dependence for upstream components, skilled workforce shortages, financing accessibility for smaller developers, and supply chain vulnerabilities affecting project execution.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)