India Solar Tracker Market Size, Share, Trends and Forecast by Type, Tracking Type, Technology, Application, and Region, 2026-2034

India Solar Tracker Market Size, Share, Trends & Forecast (2026-2034)

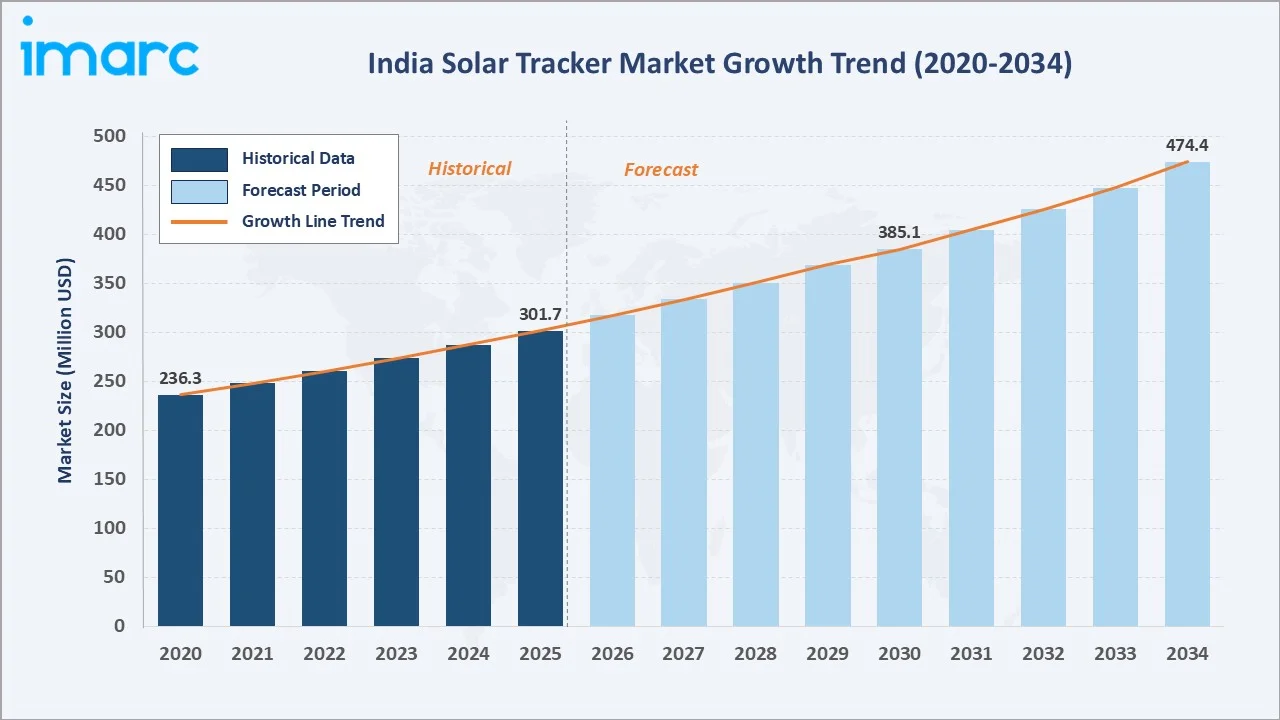

The India solar tracker market reached USD 301.7 Million in 2025 and is projected to reach USD 474.4 Million by 2034, growing at a CAGR of 5.00% during 2026-2034. The market is propelled by India’s 500 GW renewable energy target, falling solar module costs, and increasing utility-scale project deployments.

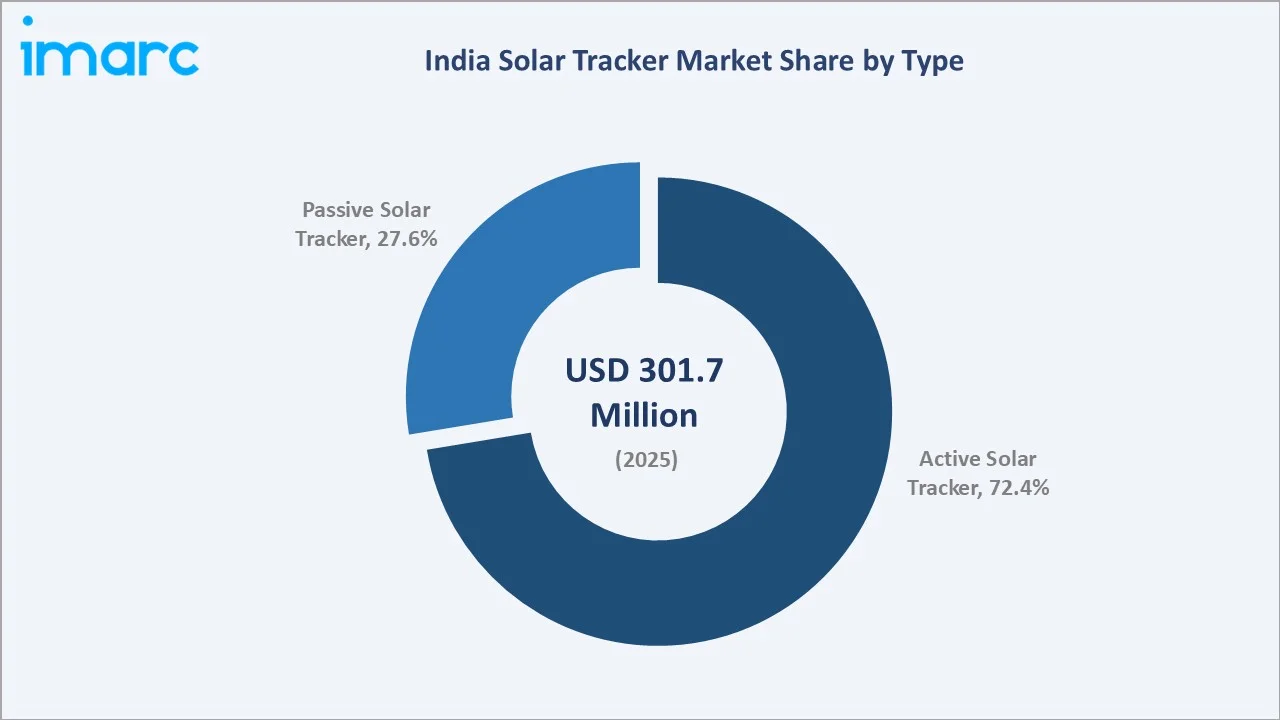

Active solar trackers dominate at 72.4% of the type segment. The utility sector leads applications at 70.4%. West & Central India commands 33.8% of the regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 301.7 Million |

|

Forecast Market Size (2034) |

USD 474.4 Million |

|

CAGR (2026-2034) |

5.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Active Solar Tracker (72.4%, 2025) |

|

Leading Application |

Utility Sector (70.4%, 2025) |

|

Leading Region |

West & Central India (33.8%, 2025) |

The market expanded from USD 236.3 Million in 2020 to USD 301.7 Million in 2025, anchored at USD 385.1 Million in 2030 and forecast to reach USD 474.4 Million by 2034. India’s national solar mission and expanding utility solar park pipeline have sustained consistent market growth, while smart tracker technology adoption is accelerating energy yield improvements across large-scale installations.

To get more information on this market, Request Sample

Active solar tracker adoption grows above the overall market CAGR as utility-scale bifacial solar projects prioritize tracked installations for maximum energy yield. The utility sector at 70.4% application share generates the strongest tracker demand, driven by India’s large solar park programme across Rajasthan, Gujarat, and Andhra Pradesh.

![]()

Executive Summary

The India solar tracker market reached USD 301.7 Million in 2025, representing a high-growth renewable energy equipment segment driven by India’s rapid solar capacity expansion. Solar trackers improve panel output versus fixed-tilt installations, making them the preferred choice for utility-scale solar projects. The market is projected to reach USD 474.4 Million by 2034.

Active solar trackers at 72.4% dominate through their sensor-driven motorized design and superior energy yield for utility and commercial projects. The utility sector at 70.4% leads driven by India’s large-scale solar park programme. West & Central India at 33.8% commands regional leadership through high solar irradiation and concentration of major solar parks.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Active Solar Tracker – 72.4% share (2025) |

|

Leading Application |

Utility Sector – 70.4% market share (2025) |

|

Leading Region |

West & Central India – 33.8% market share (2025) |

|

Market Opportunity |

Smart tracking systems; bifacial panel integration; agrivoltaic trackers; domestic manufacturing under PLI schemes |

Key Analytical Observations Supporting the Above Data:

- Active Solar Tracker at 72.4%: Active trackers dominate as their sensor-driven, motorized systems deliver superior energy yield over passive trackers, making them the preferred choice for utility-scale solar farms investing in long-term ROI maximization.

- Utility Sector at 70.4%: The utility sector leads through India’s large-scale solar park procurement, where tracker ROI is most pronounced and project scale justifies the incremental capital expenditure over fixed-tilt installations.

- West & Central India at 33.8%: This region leads through Rajasthan and Gujarat’s combination of the highest solar irradiation in India, flat terrain ideal for tracker deployment, and the concentration of India’s largest solar park clusters.

India Solar Tracker Market Overview

The India solar tracker market encompasses the design, manufacture, and supply of single-axis and dual-axis tracking systems used to orient solar photovoltaic panels toward the sun throughout the day. The ecosystem integrates tracker manufacturers, structural component suppliers, software control providers, EPC contractors, and utility-scale solar developers.

The ecosystem integrates raw material and component suppliers, tracker system manufacturers, software and control system providers, EPC project installers, and utility and commercial end users. Macroeconomic factors include India’s National Solar Mission targets, government PLI schemes for solar manufacturing, declining tracker component costs, and increasing investments in grid-scale solar infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

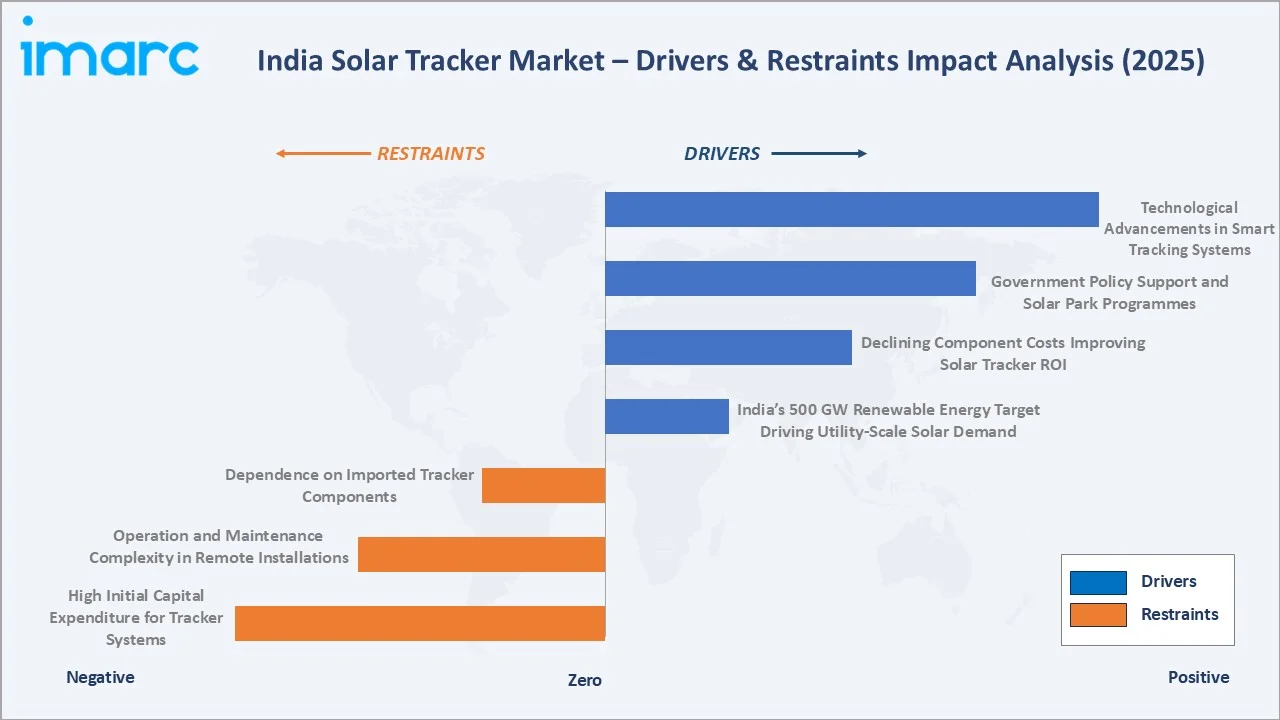

Market Drivers

- India’s 500 GW Renewable Energy Target Driving Utility-Scale Solar Demand: India’s commitment to 500 GW of renewable energy capacity by 2030 is accelerating utility-scale solar project development. Government-backed solar parks across Rajasthan, Gujarat, and Andhra Pradesh are procuring tracker systems at scale, directly driving market demand for solar trackers. This policy mandate creates a structural, long-term demand floor for tracker procurement.

- Declining Component Costs Improving Solar Tracker ROI: Falling steel, motor, and sensor costs are reducing tracker system prices, improving project-level ROI and broadening tracker adoption beyond premium utility projects into commercial installations. Lower LCOE achievable with trackers versus fixed tilt is accelerating developer preference for tracked installations across new project designs.

- Government Policy Support and Solar Park Programmes: India’s Solar Park Scheme, KUSUM programme, and PM-SURYA GHAR initiative are expanding solar capacity across utility, agricultural, and residential segments. Policy-mandated renewable procurement obligations for distribution companies are sustaining long-term solar project pipelines that directly drive tracker demand.

- Technological Advancements in Smart Tracking Systems: Integration of IoT sensors, AI-driven backtracking algorithms, and real-time remote monitoring in modern solar trackers is improving energy yield versus fixed-tilt. Advanced tracker software enabling wind to stow, bifacial optimization, and predictive maintenance is increasing investor confidence and driving tracker adoption in premium utility projects.

Market Restraints

- High Initial Capital Expenditure for Tracker Systems: Solar trackers require higher upfront investment compared to fixed-tilt mounting structures, representing a 10–15% premium on initial capital costs. This cost differential restrains tracker adoption in smaller commercial and residential installations where project economics are more sensitive to initial investment outlay.

- Operation and Maintenance Complexity in Remote Installations: Solar tracker systems involve mechanical moving parts, motors, and electronic control systems that require more intensive operation and maintenance compared to fixed-tilt installations. Remote solar park locations in Rajasthan and Gujarat face challenges in O&M workforce availability and increasing lifecycle maintenance costs.

- Dependence on Imported Tracker Components: India’s solar tracker market remains reliant on imported drive systems, sensors, and electronic control components, primarily from China and Europe. This import dependency exposes projects to global supply chain disruptions, currency fluctuation risk, and tariff-related cost increases, limiting domestic manufacturing competitiveness.

Market Opportunities

- Agrivoltaic Solar Tracker Installations: The integration of solar trackers with agricultural land use is creating a new market segment in India. Agrivoltaic trackers that allow crop cultivation beneath elevated solar panels are gaining traction in states like Maharashtra and Madhya Pradesh, supported by the KUSUM programme incentives for farmer-linked solar generation.

- Domestic Tracker Manufacturing Under PLI Scheme: India’s Production Linked Incentive scheme for solar manufacturing is encouraging domestic tracker component production. Domestic torque tube, structural steel, and control system manufacturing investment can reduce import dependency and position India as a solar tracker supply hub for South Asian markets.

Market Challenges

- Land Acquisition and Site Development Constraints: Large-scale utility solar projects requiring tracker systems face challenges in land acquisition, grid connectivity, and environmental clearances in high-solar-potential regions. Delays in project development reduce the pipeline of tracker procurement opportunities and create uncertainty in market growth projections.

- Grid Integration Challenges for Variable Solar Generation: Solar tracker systems concentrate generation in peak solar hours, creating grid integration challenges. Transmission capacity constraints and grid infrastructure limitations in tracker-dense solar regions require coordinated grid expansion investment alongside solar project development.

Emerging Market Trends

![]()

1. Integration of AI and IoT in Smart Tracker Control Systems

Modern solar trackers increasingly incorporate AI-driven algorithms and IoT-connected sensors that enable real-time backtracking optimization, wind stow automation, and predictive maintenance. Smart tracker control systems improve energy yield by dynamically adjusting panel angles based on cloud cover and diffuse irradiance data, making them a differentiating feature in utility project procurement decisions.

2. Bifacial Solar Panel Integration Driving Tracker Demand

The growing adoption of bifacial solar modules in utility-scale projects is increasing tracker demand, as bifacial panels generate significant rear-side energy from ground-reflected irradiance that is maximized through tracker tilt optimization. Bifacial tracker combinations are increasing energy yields, justifying tracker premiums in new utility project designs across India.

3. Shift Towards Larger Utility-Scale Solar Projects

India’s solar project pipeline is concentrating around large-scale 500 MW to 2,000 MW ultra-mega solar parks where tracker economics are most favorable. This consolidation toward gigawatt-scale projects is driving bulk tracker procurement, long-term supply agreements, and technology standardization across India’s utility solar sector.

4. Domestic Manufacturing Investment in Tracker Components

India’s solar manufacturing incentive programmes are stimulating domestic production of tracker structural components, including torque tubes, drive mechanisms, and mounting hardware. This is progressively reducing India’s import dependency for tracker hardware and improving project-level cost competitiveness for domestically sourced systems.

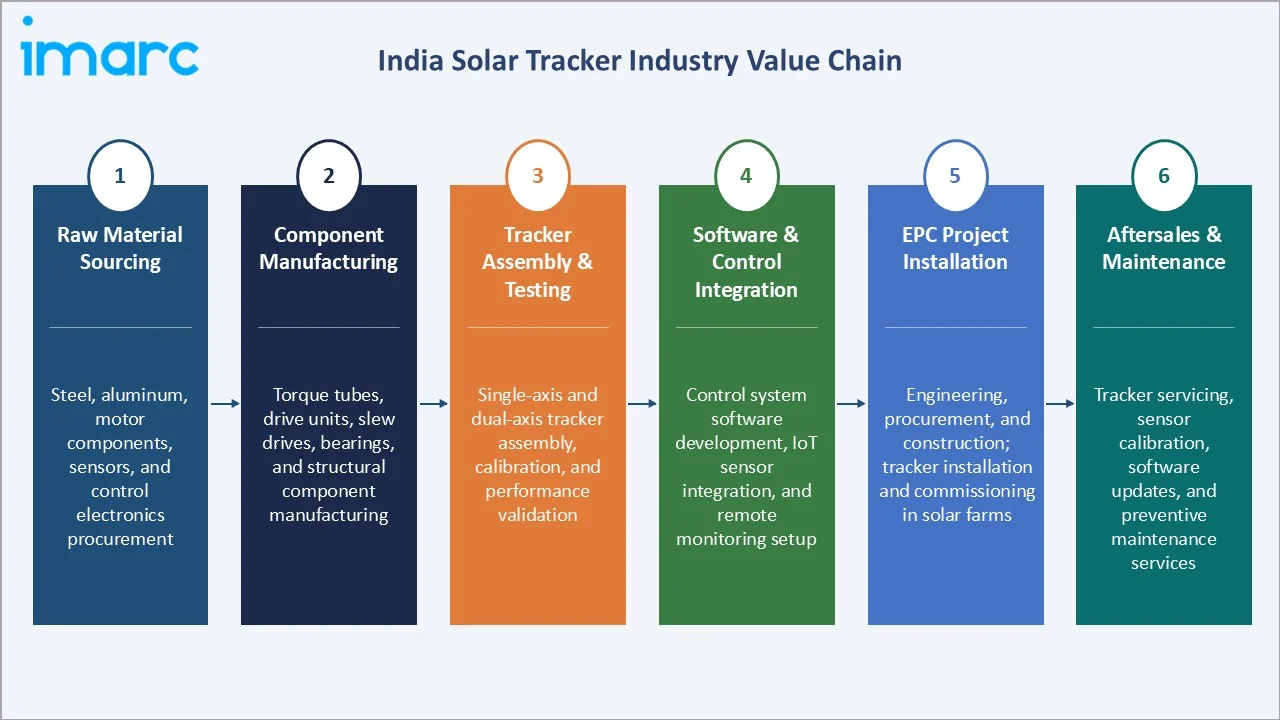

Industry Value Chain Analysis

The India solar tracker value chain integrates raw material and component sourcing, tracker assembly and performance testing, control software and IoT integration, EPC project installation, and after-sales maintenance services. The value chain spans upstream raw material suppliers through to downstream end users in utility, commercial, and residential applications.

|

Stage |

Key Activities |

|

Raw Material Sourcing |

Steel, aluminum, motor components, sensors, and control electronics procurement |

|

Component Manufacturing |

Torque tubes, drive units, slew drives, bearings, and structural component manufacturing |

|

Tracker Assembly & Testing |

Single-axis and dual-axis tracker assembly, calibration, and performance validation |

|

Software & Control Integration |

Control system software development, IoT sensor integration, and remote monitoring setup |

|

EPC Project Installation |

Engineering, procurement, and construction; tracker installation and commissioning in solar farms |

|

Aftersales & Maintenance |

Tracker servicing, sensor calibration, software updates, and preventive maintenance services |

The EPC installation tier is the value chain’s highest-employment stage, where domestic contractors execute tracker deployment across large solar parks. The control software tier is experiencing rapid technology evolution as AI-enabled smart trackers displace conventional scheduled-angle tracking systems.

Technology Landscape in the India Solar Tracker Industry

Single-Axis Tracking Technology

Single-axis tracking technology rotates solar panels along one axis – typically east to west – to follow the sun’s daily path. This technology delivers 15–25% higher energy yield versus fixed-tilt at lower cost and mechanical complexity compared to dual-axis systems, making it the dominant commercial format for utility-scale solar projects in India.

Dual-Axis Tracking Technology

Dual axis tracking technology enables solar panels to follow the sun on both horizontal and vertical axes, maximizing energy capture throughout the day and across seasons. While offering the highest energy yield potential, dual-axis systems involve greater mechanical complexity and cost, limiting their application primarily to concentrated solar power and specialized high-value installations.

Smart IoT-Enabled Control Systems

IoT-enabled smart control systems integrate real-time sensors, wireless communication, and AI-driven optimization algorithms that continuously adjust tracker angles based on actual solar irradiance data. These systems enable predictive maintenance, remote fault detection, and backtracking optimization that collectively improve energy yield and reduce O&M costs across large solar park deployments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Active Solar Tracker |

72.4% |

2025 |

|

Tracking Type |

🔒 |

🔒 |

2025 |

|

Technology |

🔒 |

🔒 |

2025 |

|

Application |

Utility Sector |

70.4% |

2025 |

|

Region |

West & Central India |

33.8% |

2025 |

By Type

The active solar tracker segment leads at 72.4% in 2025, encompassing motorized, sensor-driven systems that automatically adjust panel orientation throughout the day. Their superior energy yield, compatibility with utility-scale bifacial panels, and smart control system integration make them the dominant commercial format across India’s solar market.

To access detailed market analysis, Request Sample

Passive solar trackers at 27.6% serve cost-sensitive commercial and smaller installations. Their reliance on thermal fluid or gravity-driven mechanisms eliminates motor and sensor complexity, reducing O&M costs, but limits energy yield optimization. Passive tracker adoption is declining as active tracker costs fall and utility-scale projects increasingly specify active systems.

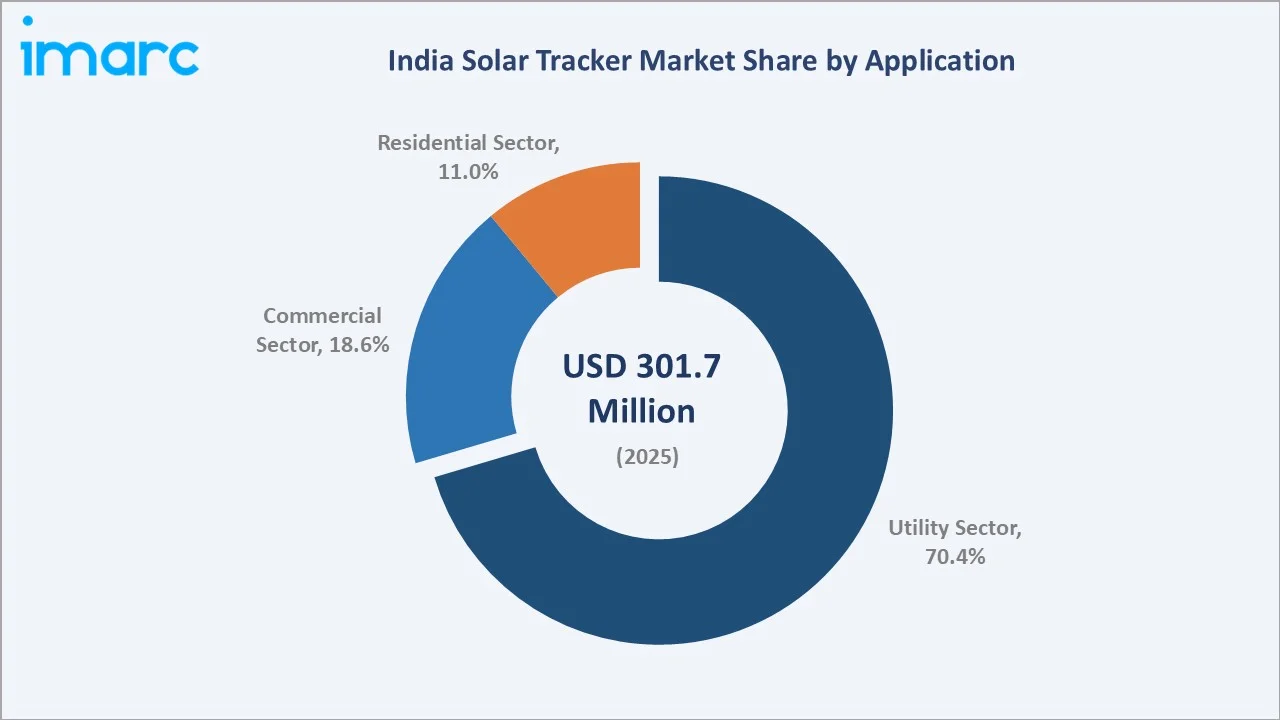

By Application

The utility sector leads at 70.4% through India’s large-scale solar park programme. Utility-scale projects above 100 MW generate the strongest tracker ROI, with energy yield improvements of 15–25% versus fixed-tilt, justifying tracker premiums across long project lifetimes. The sector continues to expand, driven by SECI auctions and state-level renewable procurement mandates.

The commercial sector at 18.6% is growing as falling tracker costs improve project economics for industrial and ground-mounted commercial solar installations above 1 MW. The residential sector at 11.0% remains limited to premium solar home systems, where tracker capital premiums are harder to justify at smaller system scales.

Regional Market Insights

|

Region |

Share (2025) |

Key Solar Tracker Market Drivers & Characteristics |

|

West & Central India |

33.8% |

Driven by Rajasthan and Gujarat’s high solar irradiation, large utility-scale solar parks, and strong government support for renewable energy capacity additions |

|

North India |

28.5% |

Fueled by desert solar zones, NTPC solar project commissions, and national solar mission targets, driving large tracker deployments |

|

South India |

22.3% |

Led by Andhra Pradesh, Karnataka, and Tamil Nadu’s growing utility solar pipeline, commercial installations, and state-level renewable targets |

|

East & Northeast India |

15.4% |

Emerging market driven by increasing renewable energy investments, state renewable targets, and expanding solar capacity in underserved regions |

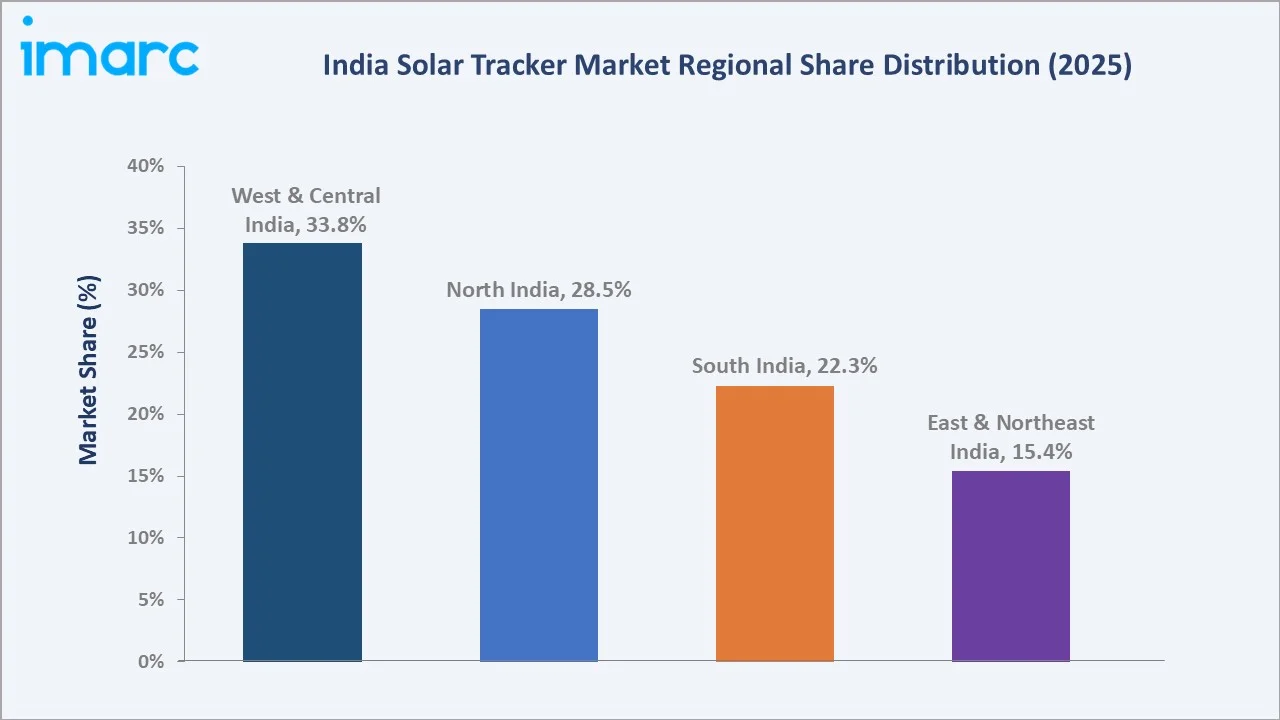

West & Central India, at 33.8%, leads through Rajasthan’s Bhadla Solar Park and Gujarat’s extensive solar park clusters. North India at 28.5% captures Rajasthan’s desert belt solar zones and NTPC-commissioned national solar mission projects.

South India, at 22.3%, reflects Andhra Pradesh, Karnataka, and Tamil Nadu’s growing utility solar pipeline and commercial tracker adoption. East & Northeast India, at 15.4%, represents the market’s emerging growth frontier as renewable energy investment expands into solar-underserved regions with increasing state renewable targets.

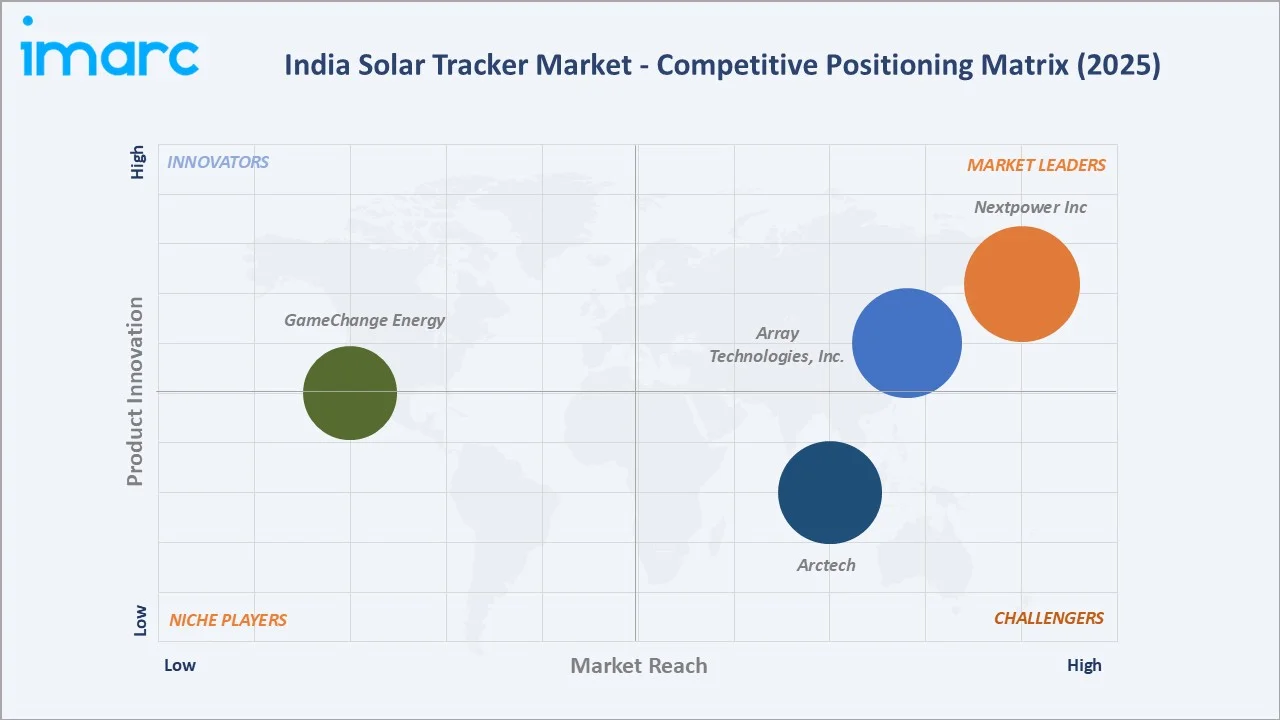

Competitive Landscape

The India solar tracker market competitive landscape is moderately concentrated with international tracker leaders and domestic players competing across utility-scale and commercial project segments. International players dominate technology supply while domestic EPC firms and manufacturers are strengthening their position under government PLI incentives and domestic content requirements.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Nextpower Inc |

NX Horizon, NX Horizon-XTR, NX Horizon Low Carbon, NX Horizon with Hail Pro |

Market Leader |

Industry-leading single-axis tracker with AI-powered independent row technology deployed across large Indian utility solar projects |

|

Array Technologies, Inc. |

DuraTrack, STI H250, OmniTrack, SkyLink Tracker System, DuraTrack Hail XP, SmarTrack |

Market Leader |

Durable, cost-effective single-axis trackers with strong utility-scale project presence and vertical supply chain integration |

|

Arctech |

SkyLine II, SkySmart II, SkyWings, SkyLight, SkyFocus |

Strong Challenger |

Advanced bifacial-optimized trackers with competitive pricing and growing India project execution capability |

|

GameChange Energy |

Genius Tracker, Genius Tracker TF |

Emerging Player |

High-wind-rated single-axis trackers with strong India market execution across Gujarat, Rajasthan, and Karnataka |

Key players include Nextpower Inc, Array Technologies, Inc., Arctech, GameChange Energy, and others.

Key Company Profiles

Nextpower Inc

Nextpower Inc is a US-based solar tracker manufacturer and a global leader in single-axis solar tracking systems, with a significant presence in India’s utility-scale solar project market through its NX Horizon smart solar tracker and integrated energy solutions.

- Key Products: NX Horizon, NX Horizon-XTR, NX Horizon Low Carbon, NX Horizon with Hail Pro

- Strategic Focus: Expanding AI-powered independent row technology that allows each tracker row to move independently, maximizing energy output in non-uniform terrain prevalent in Indian solar parks.

Array Technologies, Inc.

Array Technologies Inc. is a US-based solar tracker manufacturer known for its durable and cost-effective single-axis tracking systems, with active deployments in India’s utility-scale solar sector through large EPC partnerships and supply agreements.

- Key Products: DuraTrack, STI H250, OmniTrack, SkyLink Tracker System, DuraTrack Hail XP, SmarTrack.

- Strategic Focus: Strengthening cost-competitive tracker supply for high-volume utility solar procurement, leveraging vertical steel supply chain integration to improve structural component cost competitiveness in price-sensitive markets like India.

Market Concentration Analysis

The India solar tracker market is moderately concentrated at the utility-scale tracker supply level. The top 3 players collectively account for approximately 50–60% of India’s utility solar tracker project supply by installed capacity.

Domestic players and emerging local manufacturers account for the remainder, with domestic market share growing under domestic content regulation incentives.

Investment & Growth Opportunities

Highest Growth Segments

Utility sector tracker installations are expected to grow at an above-market CAGR, driven by smart AI-enabled tracker systems, bifacial-optimized tracker configurations, agrivoltaic tracker installations under the KUSUM programme, and domestic tracker component manufacturing under PLI schemes, representing the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Agrivoltaic solar tracker projects represent India’s highest value emerging opportunity, combining agricultural income support with solar generation. Commercial-scale tracker deployments above 5 MW are emerging as the next growth frontier as component costs decline, and commercial power purchase agreement markets mature across Indian states.

Investment Themes

- Domestic Tracker Manufacturing Investment: India’s PLI solar manufacturing scheme creates a structural investment opportunity in domestic torque tube, drive mechanism, and control electronics production. Domestic manufacturing investment reduces import dependency and improves project-level LCOE competitiveness for India-sourced tracker systems across the 2026–2034 forecast horizon.

- Smart Tracker Technology Integration: AI-driven smart solar tracker systems with IoT remote monitoring, predictive maintenance, and bifacial optimization represent a premium technology investment opportunity. Growing utility demand for smart tracker features creates a defensible technology revenue stream above commodity tracker pricing in India’s competitive market.

Future Market Outlook (2026-2034)

The India solar tracker market is projected to grow from USD 301.7 Million in 2025 to USD 474.4 Million by 2034, delivering a 5.00% CAGR. India’s solar capacity expansion targeting 500 GW by 2030 will sustain a consistent tracker project pipeline anchored by utility-scale solar park development and growing commercial solar adoption.

Three structural forces will define the growth of the India solar tracker market through 2034. India’s national solar mission creates a policy-mandated demand floor for tracker procurement largely independent of private sector cyclicality. Bifacial module adoption multiplies the per-watt tracker ROI case, reinforcing developer preference for tracked over fixed-tilt installations. Domestic manufacturing scale-up progressively reduces tracker system costs, broadening the addressable market beyond utility scale into commercial and agrivoltaic segments across high-irradiation states.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025), including solar EPC project directors, tracker system procurement managers, utility-scale solar developers, government renewable energy officials, and tracker manufacturing engineers across India’s major solar markets.

Secondary Research

Secondary research encompassed company annual reports and investor presentations; Ministry of New & Renewable Energy (MNRE) solar capacity data; Solar Energy Corporation of India (SECI) project award databases; India solar tracker market intelligence databases; international tracker supplier filings; and industry publication reports. Over 45 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using project-pipeline bottom-up model: (i) India annual utility solar project commissioning forecast by state; (ii) tracker adoption rate by project size and application segment; (iii) average tracker system revenue per MW by type; (iv) technology premium adjustment for smart versus standard tracker pricing across the forecast period.

India Solar Tracker Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Active Solar Tracker, Passive Solar Tracker |

| Tracking Types Covered |

|

| Technologies Covered | Solar Photovoltaic (PV), Concentrated Solar Power (CSP), Concentrated Photovoltaic (CPV) |

| Applications Covered | Utility Sector, Residential Sector, Commercial Sector |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Nextpower Inc, Array Technologies, Inc., Arctech, GameChange Energy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India solar tracker market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India solar tracker market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India solar tracker industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Solar Tracker Market Report

The India solar tracker market reached USD 301.7 Million in 2025, driven by active solar trackers at 72.4% type share, utility sector dominance at 70.4%, West & Central India leading at 33.8%, and India’s accelerating solar park development programme across Rajasthan, Gujarat, and Andhra Pradesh.

The India solar tracker market grows at 5.00% CAGR during 2026-2034, reaching USD 474.4 Million by 2034, supported by expanding utility solar capacity, smart tracker adoption, bifacial panel integration, and India’s national solar mission driving long-term project pipeline growth.

Active solar trackers lead at 72.4% in 2025, driven by their superior energy output and wide deployment in utility-scale solar parks. Active trackers deliver 15-25% higher energy yield versus fixed tilt, justifying their adoption premium in large solar project designs across India.

The utility sector leads at 70.4% through large-scale solar park deployments, government renewable energy targets, and high tracker ROI at utility scale. SECI-driven project auctions and state solar park programmes sustain strong long-term utility demand for solar tracker systems.

West & Central India leads at 33.8% through Rajasthan and Gujarat’s high solar irradiation, extensive land availability, and large-scale solar park development including the Bhadla Solar Park and multiple SECI-tendered projects in Rajasthan’s desert belt.

Leading companies include Nextpower Inc, Array Technologies, Inc., Arctech, GameChange Energy, and others.

The India solar tracker market is projected to reach approximately USD 385.1 Million by 2030, driven by India’s 500 GW renewable energy target, expansion of utility-scale solar parks, bifacial panel tracker integration, smart IoT-enabled tracker adoption, and domestic manufacturing scale-up.

Three priority investment opportunities: domestic tracker component manufacturing under PLI schemes, smart IoT-enabled tracker technology integration for premium utility projects, and agrivoltaic solar tracker installations under India’s KUSUM programme for farmer-linked solar generation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)