India Sports and Energy Drinks Market Size, Share, Trends and Forecast, 2026-2034

India Sports and Energy Drinks Market Summary:

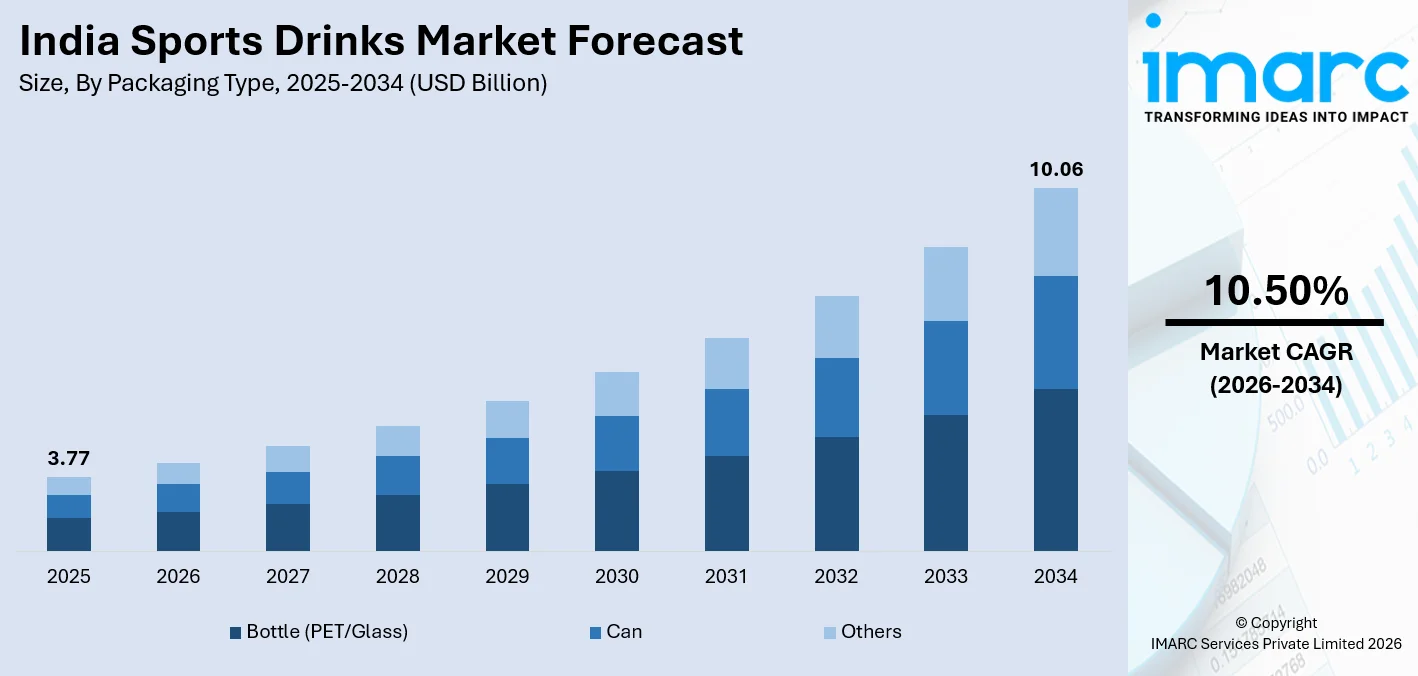

The India sports and energy drinks market size was valued at USD 3.77 Billion in 2025 and is projected to reach USD 10.06 Billion by 2034, growing at a compound annual growth rate of 10.50% from 2026-2034.

The India sports and energy drinks market is propelled by a rapidly evolving health and fitness culture, a youthful demographic base, and intensifying participation in organized sports, gym activities, and recreational fitness. Growing urbanization, rising disposable incomes, and the expanding penetration of modern retail and quick-commerce platforms are making functional beverages increasingly accessible to a wide consumer spectrum. Government initiatives have catalyzed grassroots sports engagement, while the proliferation of digital fitness content has accelerated awareness of hydration and energy supplementation.

Key Takeaways and Insights:

India Sports Drinks Market:

- By Product Type: Isotonic dominates the market with a share of 45.2% in 2025, owing to its ability to rapidly replenish fluids, electrolytes, and carbohydrates during physical exertion, making it the preferred hydration solution among recreational and competitive athletes across India.

- By Packaging Type: Bottle (PET/glass) leads the market with a share of 52.3% in 2025, driven by consumer preference for resealable, portable formats that enable convenient on-the-go hydration during workouts, outdoor sports events, and daily active routines.

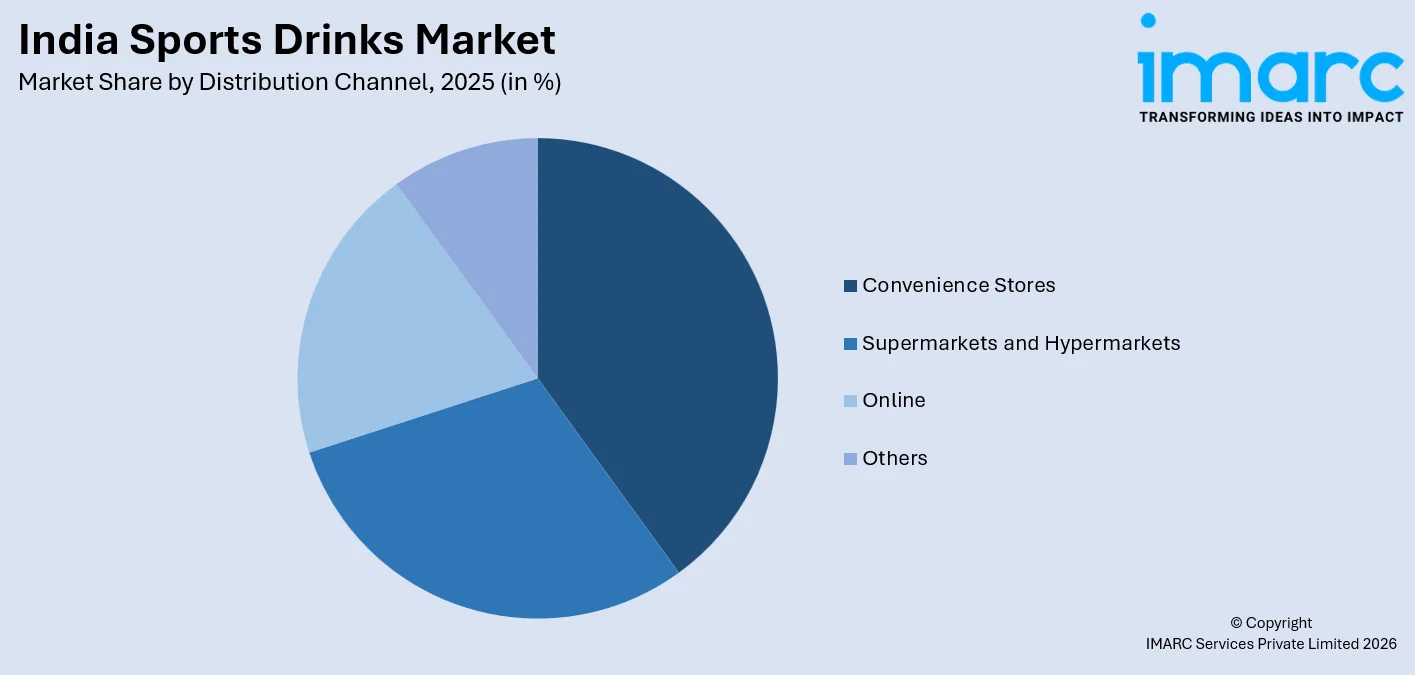

- By Distribution Channel: Convenience stores represent the largest segment with a share of 38.4% in 2025, reflecting strong impulse purchase behavior among active consumers seeking quick access to hydration beverages during commutes, gym visits, and on-the-go sporting activities.

- By Region: South India prevails the market with a share of 28.5% in 2025, due to hot climate driving hydration needs, higher urban fitness awareness, strong gym culture, better retail access, and early adoption across cities like Bengaluru, Chennai, and Hyderabad.

- Key Players: Key players in the India sports drinks market drive growth by expanding distribution networks, launching low-sugar and electrolyte-enriched formulations, and investing in sports sponsorships. Their targeted marketing efforts and strategic partnerships with fitness chains bolster brand recognition and accelerate category penetration across urban and semi-urban markets.

To get more information on this market Request Sample

India Energy Drinks Market:

- By Product: Non-alcoholic leads the market with a share of 96.0% in 2025, driven by widespread consumer preference for functional energy beverages without alcohol content, supported by mainstream retail distribution and broader demographic acceptability across all age groups.

- By Type: Non-organic prevails the market with a share of 82.0% in 2025, reflecting the high availability, affordability, and brand familiarity of conventional energy drink formulations among mass-market consumers across urban and semi-urban geographies in India.

- By Packaging Type: Bottle (PET/glass) exhibits a clear dominance in the market with a 58.0% share in 2025, owing to strong consumer preference for portable, resealable packaging formats that align with on-the-go lifestyles and India's fragmented retail distribution infrastructure.

- By Distribution Channel: Supermarkets and hypermarkets dominate the market with a share of 36.0% in 2025, providing wide product variety and promotional visibility that reinforce the channel's role as the primary purchase touchpoint for energy beverages among health-oriented modern trade shoppers.

- By Target Consumer: Adults comprise the leading segment with a share of 54.0% in 2025, driven by rising demand for energy-boosting beverages among working professionals, fitness enthusiasts, and lifestyle-oriented urban consumers seeking sustained mental and physical performance.

- By Region: West and Central India represents the largest region with a 33.0% share in 2025, supported by the high concentration of urban population centers, evolved retail infrastructure, and strong fitness culture in cities, such as Mumbai, Pune, and Ahmedabad.

- Key Players: Key players in the India energy drinks market accelerate growth through aggressive sports sponsorships, celebrity-led product launches, and competitive pricing strategies. Their investments in flavor innovation, clean-label reformulations, and digital marketing strengthen brand equity while expanding reach across metro and emerging tier-2 markets.

The India sports and energy drinks market is being driven by a combination of lifestyle shifts, demographic advantages, and evolving consumption patterns. A large young population, increasing participation in fitness activities, and growing awareness around hydration and performance are key demand catalysts. As of February 2025, India possessed the biggest youth demographic globally, with approximately 65% of its population being below 35 years old. Urbanization and rising disposable incomes are enabling consumers to experiment with premium and functional beverages, while the influence of gyms, sports culture, and social media is normalizing regular consumption. Additionally, the expansion of modern retail and e-commerce platforms is improving product accessibility across tier I and tier II cities. Aggressive marketing, celebrity endorsements, and localized product innovations, such as low-sugar, natural ingredient-based, and regionally tailored flavors, are further strengthening market penetration. The blurring line between lifestyle beverages and functional nutrition is also positioning these drinks as everyday consumption products rather than occasional use items.

India Sports and Energy Drinks Market Trends:

Rising Demand for Clean-Label and Low-Sugar Functional Beverages

Indian consumers are increasingly scrutinizing ingredient lists and gravitating towards beverages that offer functional benefits without artificial additives or excessive sugar. The FSSAI's July 2024 front-of-pack labelling mandate requiring bold disclosure of sugar, salt, and fat content has accelerated reformulation across the sports and energy drinks category. Brands are substituting synthetic sweeteners with stevia and monk fruit extracts, while launching zero-sugar hydration variants and herbal-infused energy drinks. This clean-label shift is particularly pronounced among urban millennials and Gen Z consumers who prioritize ingredient quality alongside functional performance in their beverage choices.

Expansion of Digital and Quick-Commerce Distribution Channels

The rapid expansion of quick-commerce platforms and e-commerce channels is transforming how sports and energy drinks reach Indian consumers, enabling chilled beverage delivery within minutes. India surpassed 950 Million internet users as of 2025, creating a vast digital commerce ecosystem that brands are actively leveraging through targeted social media campaigns and direct-to-consumer strategies. Social media influencer marketing, esports sponsorships, and digital advertising are enabling brands to engage younger demographics with precision. The availability of premium and niche functional beverages online is also increasing trial rates among consumers who may not encounter these products in traditional retail formats.

Government-Led Sports Infrastructure Growth Boosting Category Demand

Government investments in sports infrastructure and youth fitness programs are creating a long-term structural demand driver for sports and energy drinks across India. Inaugurated with the vision ‘From Grassroots to Glory’, the Khelo Bharat Niti 2025 aims to transform the nation's sports landscape. A key feature of the program is KIRTI (Khelo India Rising Talent Identification), which identifies talent between the ages of 9 and 18 via 174 Talent Assessment Centers. Its goal is to elevate India to among the top-10 sports nations by 2036 and the top-5 by 2047. These initiatives foster a culture of regular physical activity from grassroots levels, normalizing consumption of hydration and energy beverages among young athletes.

Market Outlook 2026-2034:

The India sports and energy drinks market is positioned for sustained and robust growth over the forecast period, underpinned by deepening health consciousness, a rapidly expanding fitness culture, and significant retail infrastructure development across urban and semi-urban geographies. The growing youth population, rising disposable incomes, and increasing sports participation are collectively amplifying demand for functional hydration and energy beverages across all demographics. The market generated a revenue of USD 3.77 Billion in 2025 and is projected to reach a revenue of USD 10.06 Billion by 2034, growing at a compound annual growth rate of 10.50% from 2026-2034. The convergence of product innovation, premiumization trends, and expanding distribution through quick-commerce and modern trade channels will continue to drive category volumes.

India Sports and Energy Drinks Market Report Segmentation:

India Sports Drinks Market:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Isotonic |

45.2% |

|

Packaging Type |

Bottle (PET/Glass) |

52.3% |

|

Distribution Channel |

Convenience Stores |

38.4% |

|

Region |

South India |

28.5% |

Product Type Insights:

- Isotonic

- Hypertonic

- Hypotonic

Isotonic dominates with a market share of 45.2% of the total India sports drinks market in 2025.

Isotonic has established a dominant position in the market, delivering an ideal combination of fluids, electrolytes, and carbohydrates that reflects the concentration of bodily fluids for quick absorption during exercise. Gym-goers, leisure athletes, and competitive sports players prefer this formulation since it works especially well during moderate-to-high intensity exercise. The primary market for isotonic products has grown because of increased engagement in football, cricket, cycling, and marathons in tier-1 and tier-2 cities. Brands are constantly improving their formulas to include natural electrolytes and flavors unique to each location.

The widespread use of isotonic sports drinks in a variety of athletic contexts, from team sports and gym sessions to endurance competitions and outdoor recreation, further supports the high preference for these beverages. In order to appeal to health-conscious millennial and Gen Z consumers, brands have broadened their isotonic portfolios to include low-sugar, natural-flavor, and fortified varieties. Increased athlete endorsements, IPL-related marketing initiatives, and sports sponsorships have enhanced isotonic product visibility and solidified their place in India's mainstream fitness discourse.

Packaging Type Insights:

- Bottle (PET/Glass)

- Can

- Others

Bottle (PET/glass) leads with a share of 52.3% of the total India sports drinks market in 2025.

Bottle (PET/glass) commands dominant preference in the India sports drinks market, due to its functional versatility, portability, and resealability, which make it ideal for active consumption during workouts, commutes, and outdoor events. The transparent nature of PET bottles enhances product visibility at the point of sale, supporting purchase confidence. Their lightweight structure, ease of handling, and suitability for on-the-go consumption further enhance user convenience across diverse consumption settings.

The suitability of bottle forms with India's dispersed retail distribution network, which includes supermarkets, convenience stores, gyms, and vending machines, contributes to their broad popularity. In order to accommodate single-serve and multi-serve consumption occasions, brands have continued to innovate in the bottle segment by developing ergonomic designs, sports cap closures, and a variety of size alternatives. Consumer and retailer trust in bottle packaging is growing as a result of the sustainability shift towards recycled PET and bio-based materials. This allows brands to balance environmental commitments with practical convenience and premium positioning in a variety of Indian urban and semi-urban markets.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Online

- Others

Convenience stores exhibit a clear dominance with a 38.4% share of the total India sports drinks market in 2025.

Convenience stores have emerged as the leading distribution channel for sports drinks in India, catering to the impulsive and time-sensitive purchasing behavior of active consumers who seek immediate hydration solutions. Their strategic placement near gyms, sports complexes, transit hubs, and educational institutions ensures high product visibility among athletes and fitness-conscious individuals. Their compact store formats and quick in-store navigation further support rapid purchase decisions, minimizing time and effort for consumers.

Extended operation hours, single-serve format availability, and chilled product access that corresponds with the impulsive buy occasions of commuters, gym patrons, and outdoor sports participants further solidify convenience stores' supremacy. Sports drink companies are increasingly able to target semi-urban consumers who were previously dependent on traditional kirana stores, because of the proliferation of convenience stores in tier-2 and tier-3 cities. While digital platforms are becoming more popular among health-conscious urban consumers for subscription-based and discovery-driven purchases, supermarkets and hypermarkets remain the anchor channel for planned purchases and bulk buying.

Regional Insights:

- North India

- West and Central India

- South India

- East India

South India comprises the largest region with a 28.5% share of the total India sports drinks market in 2025.

South India leads the sports drinks market, driven by its large urban population, well-established fitness culture, and high sports participation across states, such as Tamil Nadu, Karnataka, Telangana, and Kerala. The region's warm climate creates year-round demand for hydration beverages, while a strong tradition of cricket, kabaddi, and marathon culture underpins consumer familiarity with functional sports drinks. In 2025, Kerala recorded its 13th hottest year ever, with an annual mean land surface air temperature of 25.82°C.

The region's dominance is further supported by the high density of educational institutions, corporate campuses, and fitness centers in cities, such as Bengaluru, Chennai, and Hyderabad, which serve as key consumption hubs for sports beverages. South India's relatively higher disposable incomes, strong health awareness, and early adoption of international lifestyle trends have accelerated the premiumization of sports drinks in the region. Robust retail infrastructure and strong presence of modern trade channels further enhance product availability and brand visibility across urban and semi-urban markets.

India Energy Drinks Market:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Non-Alcoholic |

96.0% |

|

Type |

Non-Organic |

82.0% |

|

Packaging Type |

Bottle (PET/Glass) |

58.0% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

36.0% |

|

Target Consumer |

Adults |

54.0% |

|

Region |

West and Central India |

33.0% |

Product Insights:

- Alcoholic

- Non-Alcoholic

Non-alcoholic prevails with a market share of 96.0% of the total India energy drinks market in 2025.

Non-alcoholic constitutes the vast majority of the India energy drinks market, driven by broad demographic appeal, regulatory alignment, and a health-forward consumer shift away from alcohol-combined stimulant products. These beverages cater to students, working professionals, athletes, and fitness enthusiasts who seek functional cognitive and physical stimulation without the social complexities of alcoholic formulations. In January 2025, Reliance Consumer Products Limited launched RasKik Gluco Energy, a non-alcoholic energy drink containing glucose, electrolytes, and lemon juice, specifically targeting consumers requiring hydration and energy during sporting activities, underscoring the expanding appeal of accessible functional non-alcoholic beverages in India.

The non-alcoholic segment's dominance is further bolstered by the proliferation of product variants addressing diverse functional needs, including sugar-free options, herbal-infused formulations, and vitamin-enriched variants that align with India's growing clean-label movement. Distribution through mainstream channels, including supermarkets, convenience stores, and online platforms, has made non-alcoholic energy drinks a staple impulse purchase across both metro and emerging semi-urban markets. Rising disposable incomes, increasing exposure to global beverage trends, and intensified digital marketing campaigns are collectively solidifying consumer habits around non-alcoholic energy drink consumption across India.

Type Insights:

- Non-Organic

- Organic

Non-organic dominates with a share of 82.0% of the total India energy drinks market in 2025.

Non-organic maintains a commanding position in the market in India, underpinned by competitive affordability, extensive shelf presence, and established brand recognition among mass-market consumers. These formulations leverage conventional stimulant ingredients, such as synthetic caffeine, taurine, and B-vitamins, to deliver consistent energy-boosting effects. These products benefit from deep distribution across modern and traditional trade channels, ensuring consistent supply from metropolitan supermarkets to unorganized retail in semi-urban and rural geographies.

The non-organic segment's dominance is sustained by the strong consumer familiarity built through decades of category marketing, athlete endorsements, and mass media visibility. Major brands invest heavily in product range diversification, introducing new flavors, limited-edition variants, and co-branded packaging to sustain consumer engagement. The segment also benefits from well-established cold chain logistics and wide retail availability, ensuring consistent supply across diverse geographies. Pricing flexibility and frequent promotional strategies further strengthen volume sales and reinforce consumer retention across price-sensitive segments.

Packaging Type Insights:

- Bottle (PET/Glass)

- Can

- Others

Bottle (PET/glass) represents the leading segment with a 58.0% share of the total India energy drinks market in 2025.

Bottle (PET/glass) is the dominant packaging type in the India energy drinks market, propelled by its affordability, widespread retail availability, and strong compatibility with India's fragmented distribution infrastructure. Its lightweight design lowers the risk of breakage and shipping expenses, and its high-volume manufacturing capabilities allow for effective large-scale production. Additionally, the format accommodates a range of pricing ranges, enabling firms to successfully serve both mass-market and premium consumer sectors.

The preference for bottle (PET/glass) formats is reinforced by their practicality in facilitating on-the-go consumption across a range of occasions, including gym workouts, gaming sessions, office environments, and outdoor recreation. Resealable cap designs enhance usage convenience, while transparent PET material supports brand confidence at the point of sale. Manufacturers are increasingly incorporating ergonomic design elements, varied size formats, and eco-friendly rPET materials to attract environmentally conscious consumers. Continued investments in sustainable bottle infrastructure are expected to further consolidate bottle packaging dominance within the India energy drinks market.

Distribution Channel Insights:

- Supermarkets and Hypermarkets

- Convenience Stores

- Online

- Others

Supermarkets and hypermarkets comprise the leading segment with a 36.0% share of the total India energy drinks market in 2025.

Supermarkets and hypermarkets represent the primary distribution channel for energy drinks in India, delivering product visibility, promotional reach, and the convenience of bundled shopping. These outlets facilitate impulse purchases through strategic aisle placement, in-store promotions, and sampling activations. Brands leverage dedicated wellness sections and prominent in-store visibility to drive both trial and repeat purchase across the energy drinks category. Their structured retail environments and standardized merchandising practices further enhance brand discoverability and influence informed purchase decisions.

The supermarkets and hypermarkets channel benefits from its ability to accommodate wide product ranges, ensuring consumers have access to both premium international brands and affordable domestic alternatives in a single shopping visit. Organized retail chains are progressively expanding into tier-2 and tier-3 cities, extending the commercial footprint of energy drink brands into previously underpenetrated markets. Retailer loyalty programs, exclusive seasonal promotions, and co-branded fitness partnerships are strengthening the commercial ecosystem between energy drink manufacturers and modern trade operators. This channel's role in category education and consumer engagement positions it as a critical driver of sustained market expansion.

Target Consumer Insights:

- Teenagers

- Adults

- Geriatric Population

Adults hold the largest share at 54.0% of the total India energy drinks market in 2025.

Adults constitute the largest target consumer segment in the India energy drinks market, reflecting the category's strong resonance with working professionals, fitness enthusiasts, and lifestyle-oriented urban consumers seeking functional beverages to combat fatigue and sustain performance. This segment is particularly responsive to premium positioning, clean-label claims, and functional ingredient innovation. Higher disposable incomes and greater willingness to spend on convenience-oriented, performance-enhancing products further reinforce their dominant consumption share.

The adult segment's consumption of energy drinks is driven by diverse use occasions, including early-morning commutes, pre- and post-workout routines, extended work sessions, and social settings. Brands targeting this demographic are increasingly investing in premium product development, incorporating functional ingredients, such as amino acids, adaptogens, and natural caffeine sources, to differentiate within the category. Digital marketing campaigns, influencer collaborations, and sports event sponsorships have effectively elevated brand engagement among adult consumers. As lifestyle-related fatigue and work pressure intensify among India's expanding professional class, demand for functional energy beverages within the adult segment is set to remain dominant.

Regional Insights:

- North India

- West and Central India

- South India

- East India

West and Central India represents the largest region with a 33.0% share of the total India energy drinks market in 2025.

West and Central India leads the energy drinks market, anchored by the high urban density and affluent consumer base of cities, such as Mumbai, Pune, Ahmedabad, and Nagpur. The region's well-developed modern retail infrastructure and strong distribution networks enable broad product availability across organized and unorganized trade formats. Additionally, the region’s role as a commercial and media hub enhances brand visibility through aggressive marketing, events, and sponsorship activities.

The region's dominance is further reinforced by its vibrant fitness culture, growing esports community, and high penetration of quick-commerce platforms that deliver chilled energy beverages on demand. West and Central India's young demographic profile and rising disposable incomes support premiumization across beverage categories, with consumers actively seeking innovative formulations and premium formats. The concentration of corporate offices, fitness studios, and premium retail outlets in metropolitan hubs has established this region as the strategic epicenter of the market growth.

Market Dynamics:

Growth Drivers:

Why is the India Sports and Energy Drinks Market Growing?

Expanding Health, Fitness, and Sports Participation Culture

India's fitness landscape is undergoing a structural transformation, with gym memberships, marathon participation, cycling events, and recreational sports engagement growing significantly across metropolitan and tier-2 cities. In March 2026, India launched the Cycling League of India (CLI), the world's first professional franchise-based road cycling league. The project sought to establish an organized professional framework for cyclists in India, simultaneously enhancing the nation's position in international competitive cycling. This rising participation is directly increasing demand for functional beverages that support hydration, energy replenishment, and physical recovery. The normalization of fitness as a lifestyle choice among India's urban population has embedded sports and energy drinks into daily wellness routines. Fitness centers, sports academies, and wellness studios are actively stocking and endorsing functional beverages, creating a powerful retail ecosystem that reinforces category visibility. The convergence of fitness influencer culture and sports media coverage has further amplified awareness of the benefits of electrolyte and energy-enriched drinks, motivating first-time trial among consumers previously unfamiliar with the category.

Government Investments in Sports and Youth Wellness Initiatives

Government-led initiatives are creating significant structural demand tailwinds for the India sports and energy drinks market by expanding sports participation and cultivating an active youth culture. The Fit India Movement and related governmental wellness campaigns have driven institutional sports engagement and encouraged health-positive behaviors among students, young professionals, and athletes. These programs are creating a pipeline of regular sports participants who increasingly demand functional beverages as part of their athletic routines. The systematic investment in sports infrastructure is accelerating the formation of a large, habit-driven consumer base for sports and energy drinks across India's diverse geographic markets. Government-backed school and university-level competitions are further normalizing structured physical activity, reinforcing early adoption of hydration and performance-oriented beverages. Public-private partnerships (PPPs) in sports development are also enhancing market visibility for brands through sponsorships and grassroots engagement initiatives.

Rapid Retail Expansion and Quick-Commerce Penetration

The accelerated growth of modern retail, quick-commerce platforms, and e-commerce channels is dramatically expanding the availability and accessibility of sports and energy drinks across India's diverse consumer base. As per IMARC Group, the India quick-commerce market size reached USD 5.3 Billion in 2025. Quick-commerce platforms in major cities are enabling chilled beverage delivery within minutes, transforming purchase behavior for impulse-driven functional drinks. The expansion of supermarket and hypermarket chains into tier-2 and tier-3 cities is progressively extending the geographic footprint of both domestic and international sports and energy drink brands. This distribution expansion, combined with increasingly competitive pricing and promotional strategies, is enabling brands to reach previously untapped consumer segments, driving both category trial and repeat purchase across India's rapidly modernizing retail landscape.

Market Restraints:

What Challenges the India Sports and Energy Drinks Market is Facing?

Stringent Regulatory and Labelling Compliance Requirements

The India sports and energy drinks market operates under increasingly stringent regulatory oversight from the FSSAI, which mandates specific limits on caffeine content and requires bold front-of-pack disclosure of nutritional information. Compliance costs for reformulation, relabeling, and ongoing regulatory monitoring add to operational expenses for manufacturers, disproportionately affecting smaller domestic brands with limited research and development resources. Brands that fail to meet evolving compliance requirements face product recalls, market entry barriers, and reputational risks that can undermine category growth momentum.

Cold Chain Infrastructure Gaps in Emerging Markets

Adequate cold chain infrastructure remains a critical constraint for the distribution of sports and energy drinks in rural markets, where chilled product availability directly impacts consumer experience and shelf life. Maintaining the cold chain from manufacturing to retail point requires substantial investment in refrigerated transport, cold storage warehouses, and vending infrastructure, inflating distribution costs in underserved regions and constraining the overall expansion of the India sports and energy drinks market.

Intense Price Competition and High Consumer Price Sensitivity

The India sports and energy drinks market is characterized by intense price competition between established international brands and aggressively priced domestic entrants, creating significant margin pressure across the category. A large portion of India's consumer base remains highly price-sensitive, particularly in tier-2 and tier-3 cities, where premium-priced sports and energy drinks face resistance from affordable traditional alternatives, such as coconut water, lemonade, and glucose beverages. New domestic entrants offering products at low price points are disrupting category economics and forcing established brands to balance premium positioning with accessibility.

Competitive Landscape:

The India sports and energy drinks market features a dynamic competitive landscape, comprising established multinational brands, emerging domestic players, and celebrity-backed entrants. Multinational incumbents maintain strong brand equity through aggressive sports sponsorships, IPL partnerships, and premium product positioning. Domestic brands are competing effectively on price and regional distribution breadth. The competitive environment is intensifying with new international brand entries, product innovation in sugar-free and functional variants, and expanding distribution through quick-commerce and modern trade channels. Strategic collaborations with fitness influencers, sports academies, and digital platforms are further amplifying brand reach and consumer engagement. Additionally, continuous investments in localized product development and targeted marketing campaigns are enabling players to capture diverse consumer segments across urban and semi-urban markets.

Recent Developments:

- In September 2025, HELL ENERGY DRINK broadened its offerings in India by introducing its newest variant, HELL ENERGY DRINK - BLACK CHERRY. Infused with a unique flavor and supported by the esteemed quality of HELL ENERGY DRINK, HELL ENERGY DRINK BLACK CHERRY offers a refreshing and tasty variation in the energy drink market with its strong character. It is ideal for those who crave a distinct taste experience in their beverages.

India Sports and Energy Drinks Market Report Coverage:

India Sports Drinks Market:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Isotonic, Hypertonic, Hypotonic |

| Packaging Types Covered | Bottle (PET/Glass), Can, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

India Energy Drinks Market:

| Report Features | Details |

|---|---|

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Alcoholic, Non-Alcoholic |

|

Types Covered |

Non-Organic, Organic |

|

Packaging Types Covered |

Bottle (PET/Glass), Can, Others |

|

Distribution Channels Covered |

Supermarkets and Hypermarkets, Convenience Stores, Online, Others |

|

Target Consumers Covered |

Teenagers, Adults, Geriatric Population |

|

Regions Covered |

North India, West and Central India, South India, East India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10–12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Sports and Energy Drinks Market Report

The India sports and energy drinks market size was valued at USD 3.77 Billion in 2025.

The India sports and energy drinks market is expected to grow at a compound annual growth rate of 10.50% from 2026-2034 to reach USD 10.06 Billion by 2034.

Isotonic dominated the India sports drinks market with a share of 45.2%, owing to its superior fluid and electrolyte replacement efficacy during physical activity, making it the preferred hydration choice among recreational and competitive athletes across India.

Non-alcoholic dominated the India energy drinks market with a share of 96.0%, driven by broad demographic appeal, mainstream retail availability, and alignment with India's growing health-forward consumer preference for functional beverages without alcohol content.

Key factors driving the India sports and energy drinks market include rising health consciousness, expanding fitness infrastructure, government sports promotion initiatives, a growing youth population, surging disposable incomes, and the proliferation of quick-commerce and modern retail channels.

Major challenges include stringent FSSAI regulations on caffeine content and front-of-pack labelling, high price sensitivity in semi-urban markets, cold chain infrastructure gaps in tier-3 regions, intense competition from traditional beverages, and consumer concerns over sugar and artificial ingredient content.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)