India Tablet Market Size, Share, Trends and Forecast by Product, Operating System, Screen Size, End User, Distribution Channel, and Region, 2026-2034

India Tablet Market Size, Share, Trends & Forecast (2026-2034)

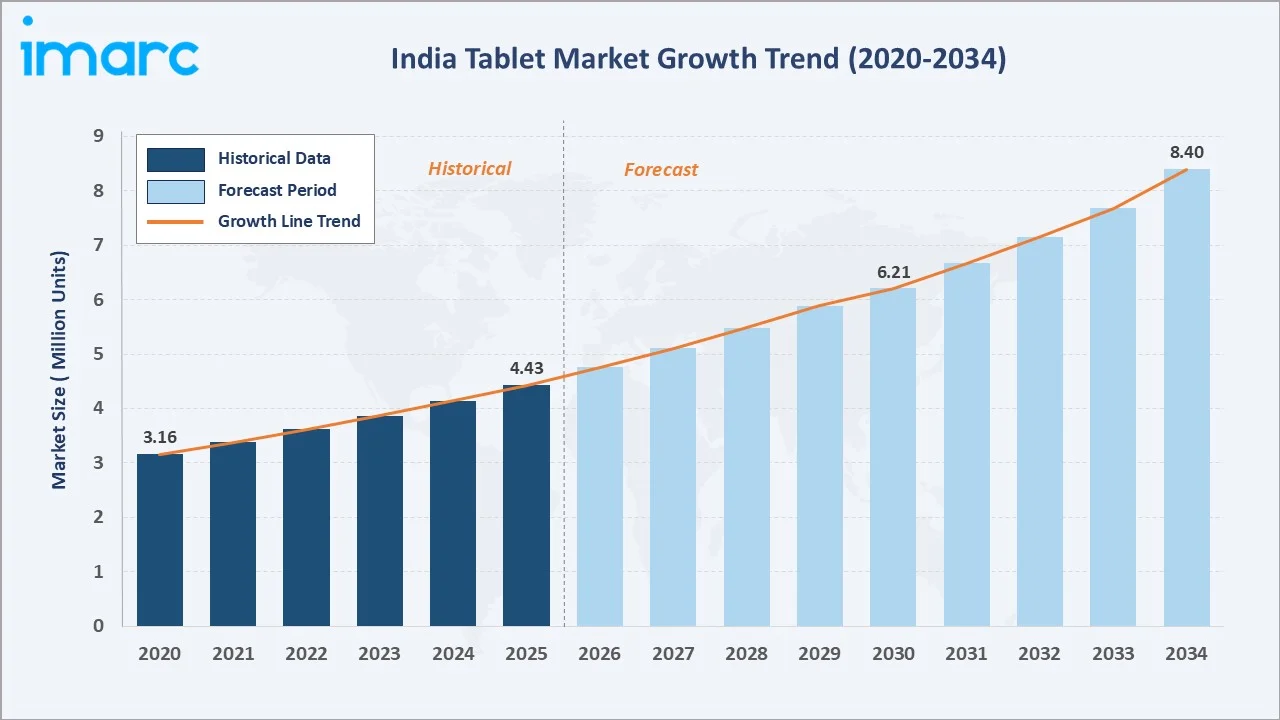

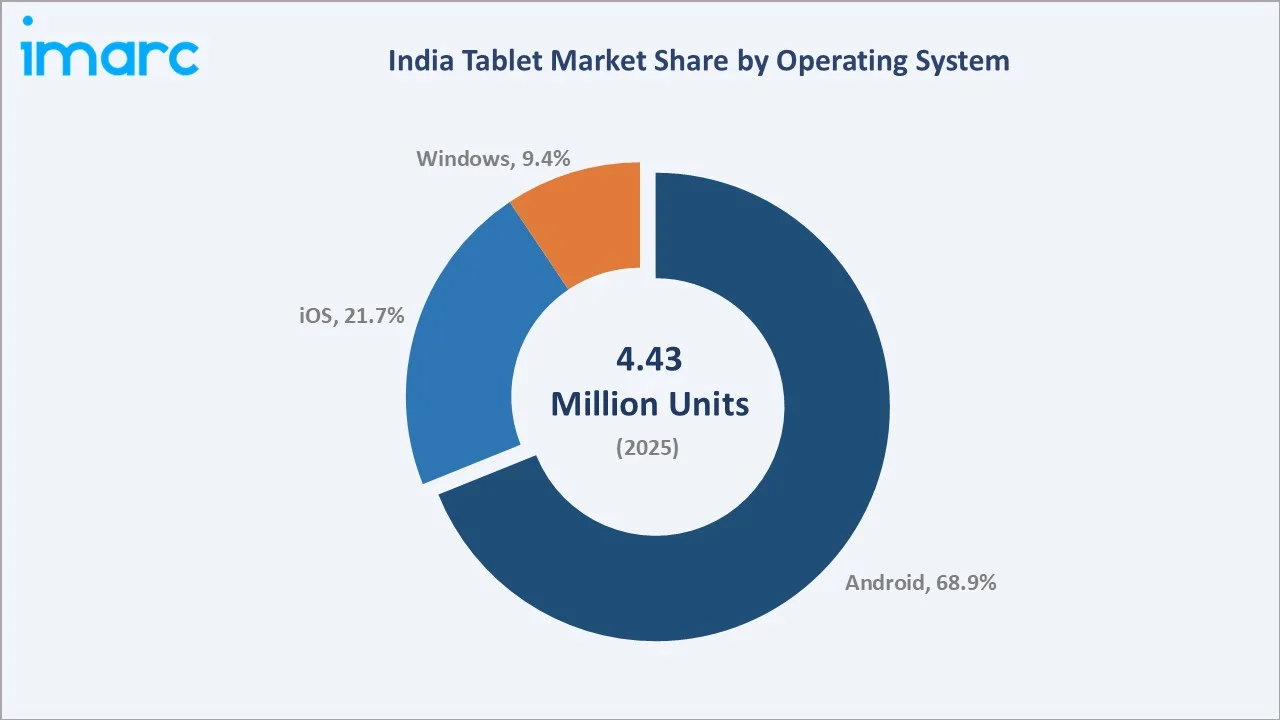

The India tablet market size reached 4.43 Million Units in 2025 and is projected to reach 8.40 Million Units by 2034, exhibiting a CAGR of 7.01% during 2026-2034. Rising internet penetration, government digital initiatives, and education-sector adoption are the primary forces driving tablet market growth.

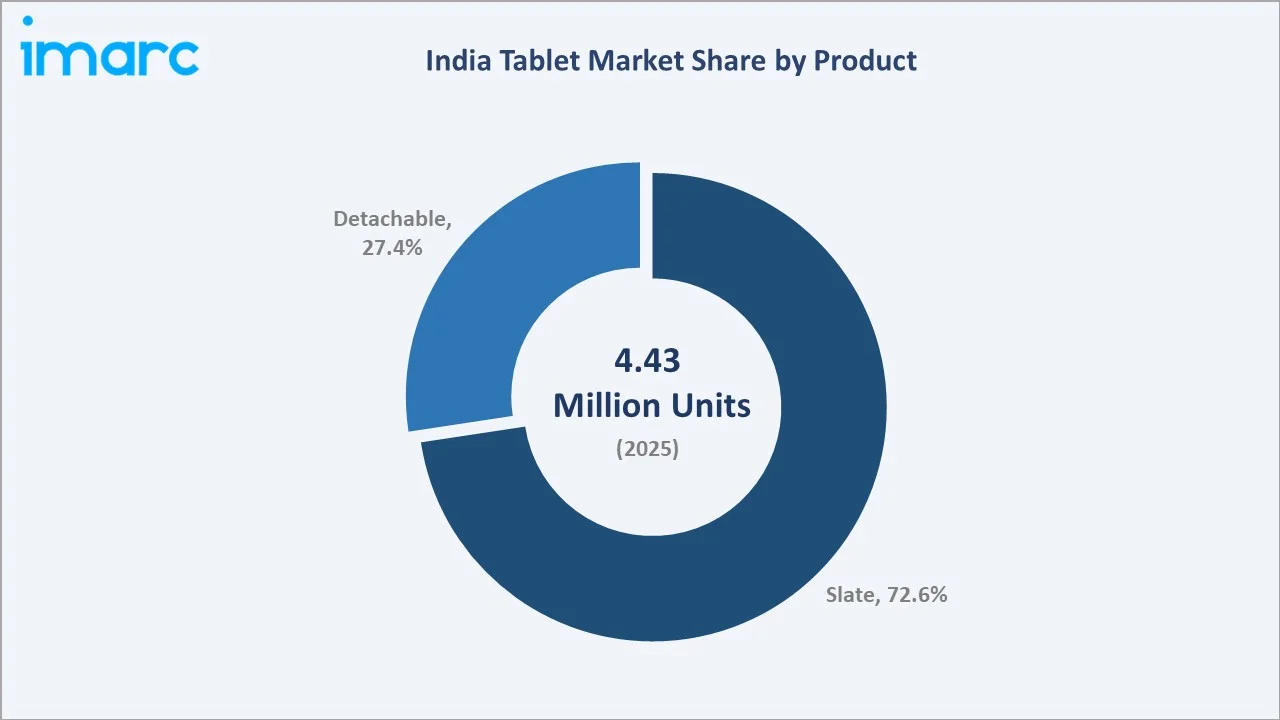

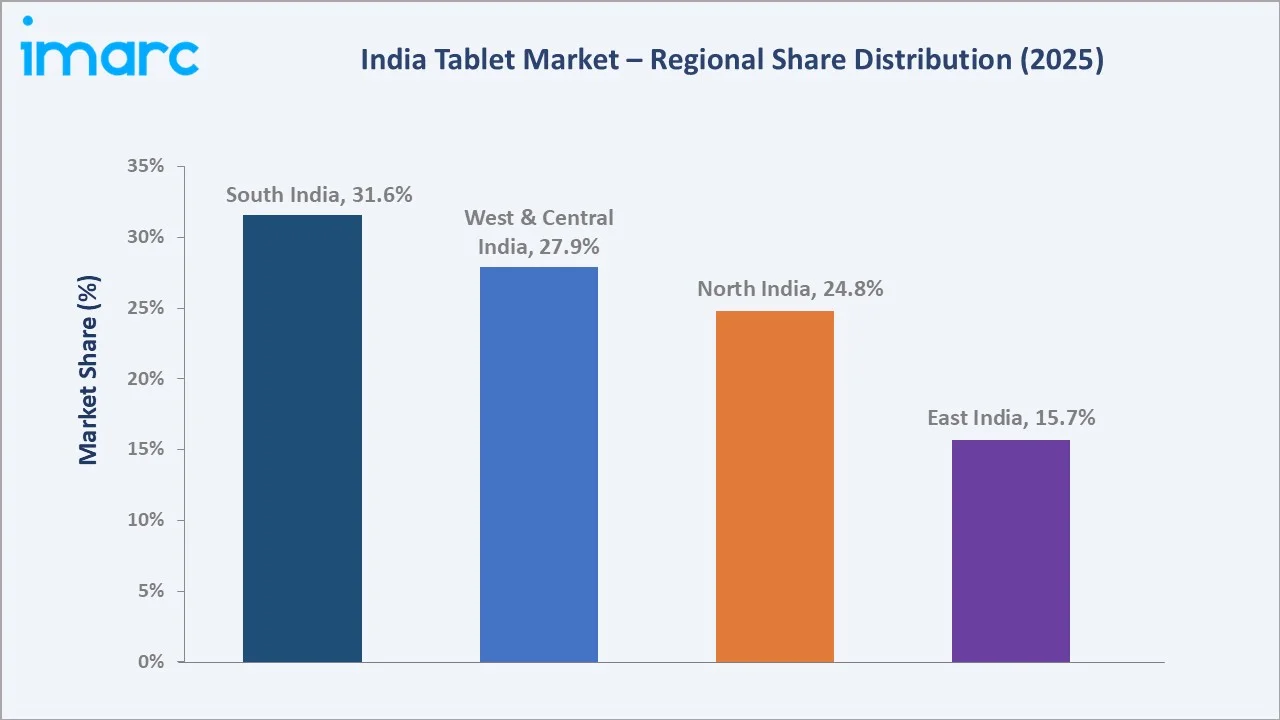

Slate tablets dominate the product mix at 72.6% in 2025, owing to affordability and broad consumer appeal across education and general use. Android leads the operating system segment at 68.9%, reflecting a diverse device ecosystem across price tiers. South India commands the largest regional share at 31.6% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

4.43 Million Units |

|

Forecast Market Size (2034) |

8.40 Million Units |

|

CAGR (2026-2034) |

7.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South India (31.6% share, 2025) |

|

Second Largest Region |

West & Central India (27.9% share, 2025) |

|

Leading Product Type |

Slate (72.6%, 2025) |

|

Leading Operating System |

Android (68.9%, 2025) |

The India tablet market growth trajectory from 2020 through 2034, with historical expansion to 4.43 Million Units in 2025, reflects consistent digitalization-driven demand, while the forecast to 8.40 Million Units captures accelerating education investment, remote-work adoption, and government digital program procurement.

To get more information on this market, Request Sample

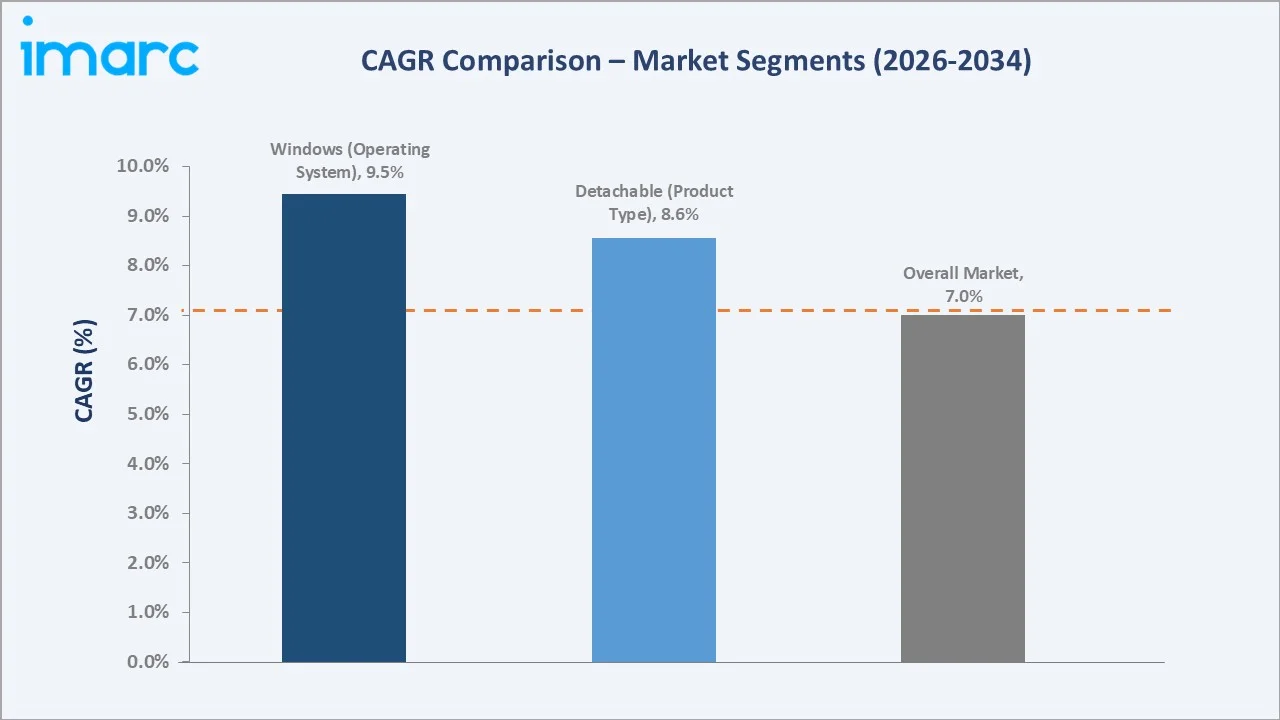

The CAGR trajectories across key product, operating system, and regional sub-segments, with Windows OS at ~9.45% CAGR and detachable tablets at ~8.55% CAGR, are the fastest-growing categories within the India tablet industry analysis through 2034.

Executive Summary

The India tablet market is on a sustained growth trajectory from 4.43 Million Units in 2025 to 8.40 Million Units by 2034. Tablets, as essential portable computing devices deployed across education, healthcare, enterprise, and consumer use cases, benefit from rising digital adoption across urban and semi-urban India.

Slate tablets dominate product share at 72.6% in 2025, owing to competitive pricing and suitability for educational and consumer use. Detachable tablets (27.4%) are growing faster at ~8.55% CAGR, driven by enterprise professionals seeking laptop-equivalent portability at a lower price point.

Android dominates operating system share at 68.9% in 2025, benefiting from the widest device variety and most competitive price points. iOS (21.7%) anchors the premium segment, while Windows (9.4%) serves enterprise and education markets, growing fastest at ~9.45% CAGR through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Slate – 72.6% share (2025) |

|

Fastest-Growing Product |

Detachable – ~8.55% CAGR (2026-2034) |

|

Leading OS |

Android – 68.9% share (2025) |

|

Fastest-Growing OS |

Windows – ~9.45% CAGR (2026-2034) |

|

Leading Region |

South India – 31.6% share (2025) |

|

Second Largest Region |

West & Central India – 27.9% share (2025) |

|

Top Companies |

SAMSUNG, Apple Inc., Lenovo, Xiaomi, OnePlus |

Key Analytical Observations Expanding on the Above Data:

- Slate Dominance: Slate tablets, at 72.6% in 2025, dominate because of their strong cost-value proposition for mass-market consumers and educational institutions procuring at scale under government programs such as PM e-VIDYA and NDEAR.

- Android Leadership: Android's 68.9% OS share in 2025 reflects India's price-sensitive market, where sub-INR 15,000 Android tablets from Samsung, Lenovo, and Xiaomi collectively drive high-volume institutional and consumer procurement.

- South India Dominance: South India's 31.6% lead in 2025 reflects concentration of IT employment, educational institutions, and state-level digital procurement programs in Karnataka, Tamil Nadu, Andhra Pradesh, and Telangana.

- Windows Growth: Windows tablets at ~9.45% CAGR through 2034 is the fastest-growing OS segment, driven by enterprise remote-work adoption, government e-governance deployments, and growing demand for 2-in-1 productivity devices in BFSI and healthcare verticals.

India Tablet Market Overview

A tablet is a portable, touchscreen computing device positioned between a smartphone and a laptop in screen size and functionality. Product configurations are defined by OS platform, display size, connectivity, processing tier, and form factor (slate or detachable with keyboard dock).

India's tablet ecosystem integrates global hardware OEMs, chipset suppliers, OS platform developers, telecom operators, e-commerce and offline retail networks, and diverse end-use sectors spanning education, healthcare, enterprise, government, and mass consumer markets.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

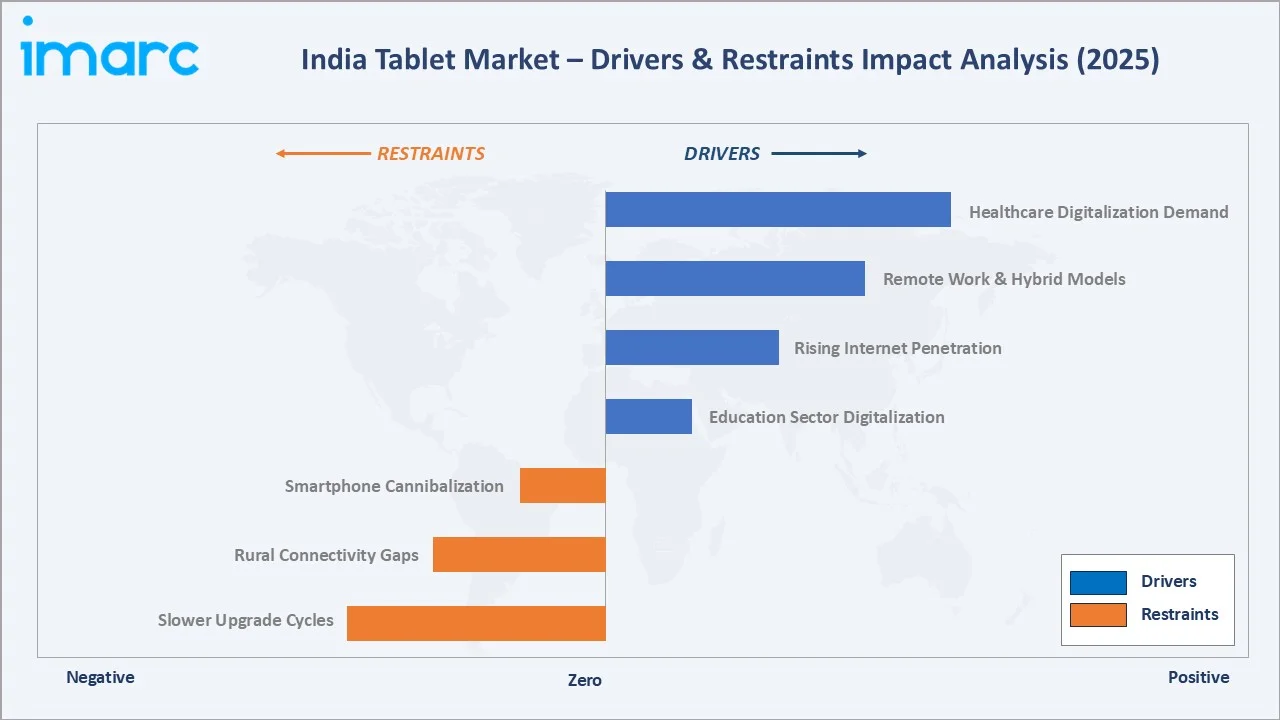

- Education Sector Digitalization: India's digital education push, anchored by the National Education Policy (NEP) 2020 and programs such as PM e-VIDYA and DIKSHA, is driving large-scale institutional tablet procurement. State governments procure tablets in bulk for school students, creating recurring volume demand.

- Rising Internet Penetration: India had over 1.2 billion internet users in 2023, and internet penetration exceeded 52% in 2024. Growing broadband and 4G/5G coverage enhances the utility of tablets for streaming, productivity, and e-commerce, fueling consumer and enterprise demand.

- Remote Work & Hybrid Models: Approximately 28% of Indian professionals use hybrid work models. Tablets serve as cost-effective portable productivity devices for remote work, video-conferencing, and field-based enterprise workflows, expanding the addressable market.

Market Restraints

- Smartphone Cannibalization: Smartphone screen sizes have expanded to 6.5–7 inches, blurring the functionality gap with entry-level tablets. The cannibalization from large-screen smartphones that offer voice calling is a persistent challenge for tablet volume growth in the mass segment.

- Rural Connectivity Gaps: Poor internet infrastructure in rural areas limits tablet adoption for digital learning and enterprise use outside Tier-1 and Tier-2 cities, constraining the addressable market expansion potential.

Market Opportunities

- Healthcare Digitalization: India's healthcare digitalization, with EHR adoption and telemedicine expansion post-COVID-19, is creating demand for ruggedized and clinical-grade tablets in hospitals and diagnostic centers, opening a high-value institutional procurement channel.

- Rising Premium Segment: Increasing disposable incomes and evolving consumer preferences are driving demand for higher-end products, with the premium category witnessing strong growth momentum and signaling a shift toward upgraded offerings beyond entry-level options; this trend reflects a broader willingness among consumers to invest in better features, performance, and brand value, while manufacturers are also expanding their premium portfolios to capture higher margins, and the sustained demand is gradually reshaping the overall market mix toward more value-driven segments.

Market Challenges

- Manufacturing Competitiveness: Samsung and Lenovo began exporting tablets to the US and European markets from India in 2025. However, competing with established Chinese manufacturers on cost remains challenging for domestic production scale-up under the PLI scheme.

- Slower Upgrade Cycles: Rapid refresh cycles in tablet technology require consumer upgrades every 2–3 years. Price sensitivity in India's mass market limits willingness to pay for spec upgrades, extending effective replacement cycles.

Emerging Market Trends

1. AI-Powered Features Elevating Tablet Utility

OEMs are embedding on-device AI into tablets for real-time translation, intelligent content recommendations, and adaptive learning. AI-driven educational tablets are gaining traction in school procurement programs, enhancing personalized learning outcomes.

2. 5G Connectivity Accelerating Enterprise Adoption

5G-enabled tablets from Samsung and Apple are gaining enterprise adoption for field sales, logistics, and healthcare applications where high-speed cellular connectivity is essential. 5G tablet shipments are growing faster than Wi-Fi-only variants.

3. Government Procurement Programs Driving Volume

State governments have announced large-scale tablet distribution programs for students and farmers. These procurement tenders create predictable high-volume demand cycles for budget Android tablet manufacturers and component suppliers.

4. Detachable Tablets Gaining Share in Enterprise Segment

Enterprise buyers are replacing laptops with detachable tablets for field workforce, point-of-sale, and boardroom applications. DeX-compatible and Windows detachables are driving the segment's above-average ~8.55% CAGR through 2034.

Industry Value Chain Analysis

The India tablet value chain spans six stages from component sourcing through end-user deployment. OEM assembly and OS integration capture the highest brand value-add, while distribution and after-sales networks determine market penetration depth across regions.

|

Stage |

Key Players / Examples |

|

Raw Material & Components |

Display panels, chipsets, batteries, cameras, memory modules |

|

OEM Manufacturing |

Original design manufacturers and brand OEMs assembling finished tablets |

|

OS & Software Integration |

Operating system providers and app ecosystem developers |

|

Quality Assurance & Testing |

Compliance, BIS certification, safety standards, OEM internal QA |

|

Distribution & Logistics |

Online platforms, offline retail, B2B direct sales, institutional tenders |

|

End User Deployment |

Education, consumer, enterprise, healthcare, government segments |

|

After-Sales & Support |

Authorised service centers, OEM warranty programs, third-party repair |

OEMs with India-local assembly capabilities benefit from PLI scheme advantages, enabling competitive pricing. Vertical integration in distribution, combining direct e-commerce with offline retail, is a key differentiator for volume market share.

Technology Landscape in the India Tablet Industry

Chipset Technology: Qualcomm Snapdragon and MediaTek Helio/Dimensity

Leading chipset providers continue to drive performance improvements and efficiency gains across devices, with premium segments benefiting from high-end processors enabling advanced features such as 5G connectivity and enhanced multitasking, while cost-effective chipset solutions remain dominant in value-focused devices, ensuring a balance between performance and affordability; this dual positioning supports broader market coverage and caters to diverse consumer segments.

Display Technology: LCD to AMOLED Transition

The transition from conventional displays to higher-quality panel technologies is gaining traction, particularly in premium devices that emphasize better visual experience, color accuracy, and contrast; at the same time, mid-sized screen formats are emerging as the preferred choice, offering an optimal balance between portability and productivity, and influencing product design and consumer purchasing decisions across segments.

Connectivity: 5G and Wi-Fi 6 Integration

5G-enabled tablets are becoming the default specification in the premium segment above INR 40,000. Wi-Fi 6 integration in mid-range devices improves throughput for video-conferencing and cloud-intensive enterprise deployments.

Software Ecosystems: Android, iPadOS, and Windows Platforms

Google's Android tablet optimization, Apple's Stage Manager multitasking on iPadOS, and Microsoft's Windows 11 ARM compatibility are each enhancing tablet-as-PC productivity use cases, supporting detachable and enterprise segment growth through 2034.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Slate |

72.6% |

2025 |

|

Operating System |

Android |

68.9% |

2025 |

|

Screen Size |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

South India |

31.6% |

2025 |

By Product

Slate tablets command a 72.6% majority share in 2025 owing to their fundamental cost-competitiveness and broad suitability for education, entertainment, and general consumer use cases. Government procurement programs targeting slate tablets for student distribution amplify volume concentration in this segment.

To access detailed market analysis, Request Sample

Detachable tablets, at 27.4% in 2025 and growing at ~8.55% CAGR, are gaining enterprise traction as 2-in-1 productivity devices. Samsung Galaxy Tab S series with DeX support and Microsoft Surface represent the primary detachable product lines driving this segment.

By Operating System

Android dominates the OS segment at 68.9% in 2025, reflecting the widest price-range coverage from entry-level to premium devices. Android's open ecosystem, Google Play Store access, and OEM customization flexibility make it the default choice across consumer and educational buyers.

iOS at 21.7% in 2025 anchors the premium segment, with the iPad 11-series contributing 69% of Apple's shipments in Q3 2025. Windows at 9.4% serves specialized enterprise and government use cases, growing fastest at ~9.45% CAGR as 2-in-1 work devices gain mainstream enterprise acceptance.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

31.6% |

IT sector concentration; educational institutions; state digital programs |

|

West & Central India |

27.9% |

Economic growth; urban consumer electronics; enterprise demand |

|

North India |

24.8% |

Large student population; central government digital initiatives |

|

East India |

15.7% |

Nascent market growth; digital literacy programs; state government schemes |

South India's 31.6% dominance in 2025 is driven by the highest concentration of IT/ITES employment, premier engineering institutions, and progressive state government digital education initiatives. Karnataka and Tamil Nadu lead in both consumer and enterprise tablet procurement.

West & Central India, at 27.9% in 2025, benefits from Maharashtra's large BFSI enterprise base and Gujarat's manufacturing community. Urban Mumbai and Pune drive premium iOS and Windows tablet demand, while Tier-2 cities fuel mid-range Android volume.

North India at 24.8% reflects a large student population in Uttar Pradesh and Delhi-NCR, supported by central and state government tablet distribution schemes. East India at 15.7% represents the fastest latent-growth region as digital literacy programs scale through 2034.

Competitive Landscape

The India tablet market is moderately concentrated at the top, with Samsung and Apple collectively commanding over 60% of shipments. The market also includes strong mid-tier competition from Lenovo, Xiaomi, OnePlus, and Acer, each targeting distinct price-performance segments.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

SAMSUNG |

Galaxy Tab S11, A11, A11+ |

Leader |

Premium & mid-range; 5G; education and enterprise |

|

Apple Inc. |

iPad Pro, iPad Air, iPad (11th Gen), iPad mini |

Leader |

Premium segment; ecosystem integration; enterprise |

|

Lenovo |

Idea Tab, Yoga Tab Plus, Idea Tab Pro |

Challenger |

Value & enterprise; Motorola-branded consumer tablets |

|

Xiaomi |

Pad 7, Pad 8 |

Challenger |

Value Android; youth segment; feature-rich mid-range |

|

OnePlus |

OnePlus Pad 4, OnePlus Pad Go 2, OnePlus Pad 3, OnePlus Pad 2 |

Emerging |

Premium Android; OxygenOS; performance positioning |

Key players include SAMSUNG, Apple Inc., Lenovo, Xiaomi, OnePlus, and others.

Key Company Profiles

Samsung

Samsung manufacturing presence in Noida provides PLI scheme benefits and supply chain agility.

- Product Portfolio: Offers Galaxy Tab S10, S11, A11, A11+

- Recent Developments: In August 2025, Samsung launched the Galaxy Tab Active5 Enterprise Edition in India, a rugged and 5G-enabled tablet specifically designed for enterprise and field workforce applications across sectors such as logistics, manufacturing, healthcare, retail, and public services.

- Strategic Focus: Samsung's strategy combines vertical integration, local manufacturing, and 5G product leadership to defend market share against Chinese rivals while expanding premium positioning in enterprise and creator segments across India.

Apple Inc.

Apple is one of top leading brand in India market. Apple's ecosystem integration across iPhone, iPad, and Mac drives strong brand loyalty among professionals and urban consumers.

- Product Portfolio: Offers iPad Pro, iPad Air, iPad (11th Gen), iPad mini

- Recent Developments: In March 2026, Apple introduced the new iPad Air powered by the M4 chip, featuring enhanced performance, increased memory, improved connectivity, and advanced AI capabilities aimed at boosting productivity, creativity, and multitasking.

- Strategic Focus: Apple focuses on ecosystem integration (iPhone–iPad–Mac continuity), Stage Manager multitasking, and M-series chip performance parity to drive iPad Pro premium positioning and enterprise adoption in India.

Lenovo

Lenovo captured a reputable market share, effectively leveraging Motorola-branded tablets to attract younger consumers while expanding enterprise deployments.

- Product Portfolio: Offers Idea Tab, Yoga Tab Plus, Idea Tab Pro

- Recent Developments: In April 2026, Lenovo launched the IdeaTab Pro Gen 2 tablet, powered by a Qualcomm processor and designed to deliver enhanced productivity, entertainment, and multitasking capabilities. The device features a large high-resolution display, AI-enabled functionalities, improved audio performance, and support for accessories aimed at students, professionals, and content consumers, while reinforcing Lenovo’s strategy of expanding its premium tablet portfolio with performance-focused and feature-rich devices for evolving consumer needs.

- Strategic Focus: Lenovo's strategy targets cross-segment coverage from budget education devices to enterprise-grade detachables, leveraging Motorola's brand equity in consumers.

Market Concentration Analysis

The India tablet market is moderately concentrated, with Samsung (~37%) and Apple (~26%) collectively commanding over 60% of shipments. Lenovo (~17%) and Xiaomi (~12%) compete in the mid and value tiers, leaving approximately 8% distributed among OnePlus, Acer, and smaller regional brands.

Consolidation at the premium tier is pronounced. Apple and Samsung have jointly increased premium segment share, with tablets above INR 20,000 surging 71% QoQ in Q3 2025. The value tier below INR 15,000 remains contested between Xiaomi, Lenovo, and Acer, with no single brand commanding dominant share.

Investment & Growth Opportunities

Fastest-Growing Segments

Detachable tablets at ~8.55% CAGR through 2034 are the highest-growth product segment, driven by enterprise productivity demand and remote-work normalization. Windows tablets at ~9.45% CAGR represent the fastest OS segment growth opportunity across BFSI and government verticals.

Emerging Markets

East India, at the lowest current penetration with 15.7% share, represents the highest latent growth opportunity as digital literacy programs, telecom infrastructure investment, and state government tablet distribution schemes scale through the forecast period to 2034.

Venture & Investment Trends

India's PLI scheme for IT hardware is attracting OEM manufacturing investment. Samsung and Lenovo exported over 1 million tablet units from India in 2025, positioning India as an emerging export manufacturing hub and creating investment opportunities in component supply chains and EMS providers.

Future Market Outlook (2026-2034)

The India tablet market is forecast to expand from 4.43 Million Units in 2025 to 8.40 Million Units by 2034 at a CAGR of 7.01%, adding approximately 3.97 Million Units in incremental annual volume over the forecast period.

Three structural forces will most significantly shape India's tablet industry through 2034: national digital education mandates scaling tablet-per-student ratios, 5G network rollout enhancing tablet utility in rural and semi-urban markets, and enterprise digital transformation replacing paper-based workflows with tablet-enabled applications.

AI integration in tablets, with on-device language models supporting regional language interfaces for Hindi, Tamil, and Bengali, will broaden the addressable market beyond English-proficient urban users, unlocking demand in Tier-3 and rural markets through 2034.

Research Methodology

Primary Research

Primary research encompassed structured interviews with India tablet industry stakeholders, including OEM commercial managers, institutional procurement officers, telecom channel partners, and e-commerce category managers. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include IDC India Quarterly Tablet Tracker, CyberMedia Research (CMR) India Tablet PC Market Reviews, Statista Digital Economy reports, Ministry of Electronics & IT (MeitY) publications, TRAI connectivity data, and trade publications including Digit, Business Standard Technology, and Economic Times Tech.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating India GDP growth rates, urbanization indices, digital literacy expansion, government program expenditure projections, and OEM shipment trend analysis. Scenario analysis accounted for macroeconomic uncertainty.

India Tablet Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Units |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Detachable, Slate |

| Operating Systems Covered | Android, iOS, Windows |

| Screen Sizes Covered | 8”, 8” and Above |

| End Users Covered | Consumer, Commercial |

| Distribution Channels Covered | Online, Offline |

| Regions Covered | South India, North India, West & Central India, East India |

| Companies Covered | SAMSUNG, Apple Inc., Lenovo, Xiaomi, OnePlus, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India tablet market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India tablet market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India tablet industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the India Tablet Market Research Report and Industry Forecast Report

The India tablet market size reached 4.43 Million Units in 2025.

The India tablet market is projected to reach 8.40 Million Units by 2034.

The India tablet market is expected to exhibit a CAGR of 7.01% during 2026-2034.

Slate tablets dominate with a 72.6% share in 2025, driven by education sector procurement and broad consumer demand for affordable portable computing devices.

Android leads with 68.9% OS share in 2025, reflecting its broad price-range coverage and open ecosystem, followed by iOS at 21.7% and Windows at 9.4%.

South India leads with 31.6% share in 2025, driven by IT sector concentration, premier educational institutions, and progressive state government digital initiatives.

The major drivers include education sector digitalization under NEP 2020, rising internet penetration, remote work adoption, and government digital programs for students and public services.

The key players in the India tablet market include SAMSUNG, Apple Inc., Lenovo, Xiaomi, OnePlus, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)