India Three-Wheeler Market Size, Share, Trends and Forecast by Vehicle Type, Passenger Vehicle, Fuel Type, and Region, 2026-2034

India Three-Wheeler Market Size & Forecast 2026-2034

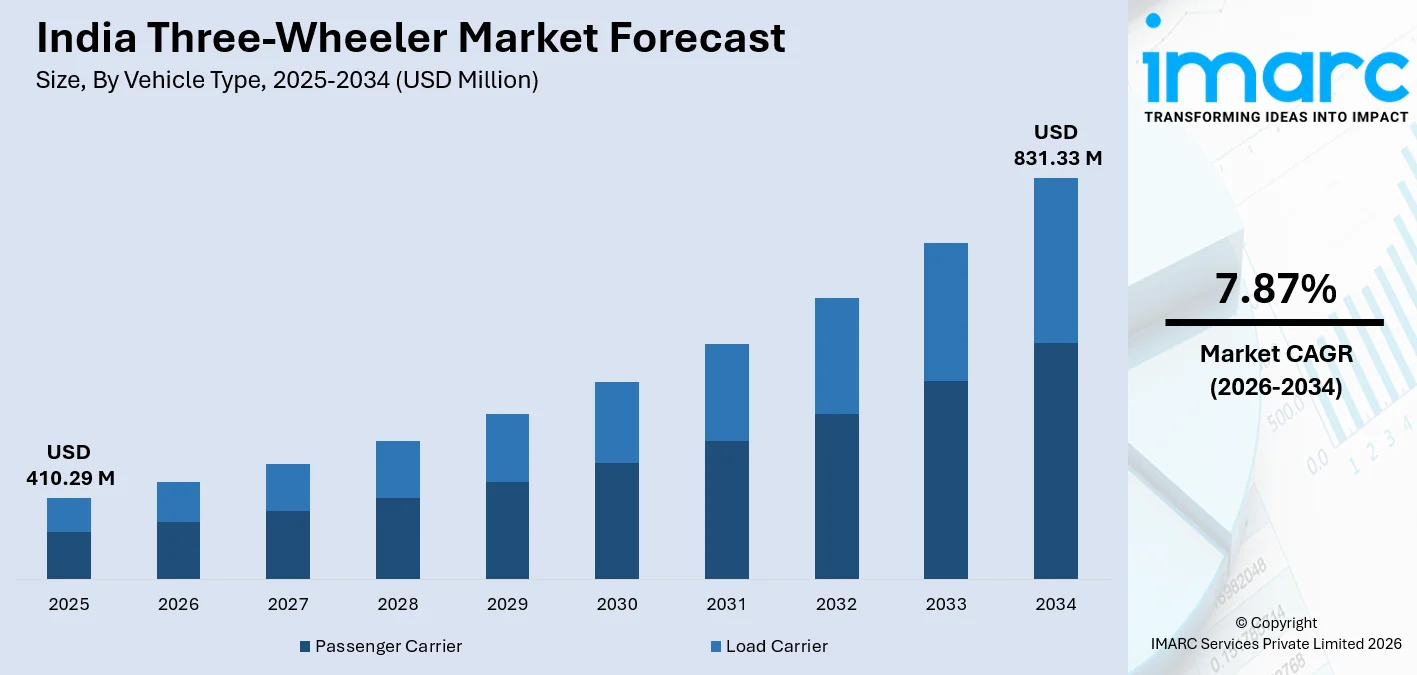

The India three-wheeler market size, valued at USD 410.29 Million in 2025, is projected to reach USD 831.33 Million by 2034, growing at a CAGR of 7.87% from 2026-2034, driven by rapid urbanization, rising last-mile mobility demand, and strong government support for electrification through the PM E-DRIVE scheme. Three-wheeler sales in India reached a record 7.41 lakh units in FY 2024–25, a 6.7% year-on-year increase surpassing the previous FY2019 peak, underscoring robust structural demand that continues to expand the India three-wheeler market share.

To get more information on this market Request Sample

India Three-Wheeler Industry Analysis - Key Insights

- Passenger Carrier owns 68.0% of vehicle type in 2025 - Auto-rickshaws remain the backbone of intra-city last-mile mobility across hundreds of towns.

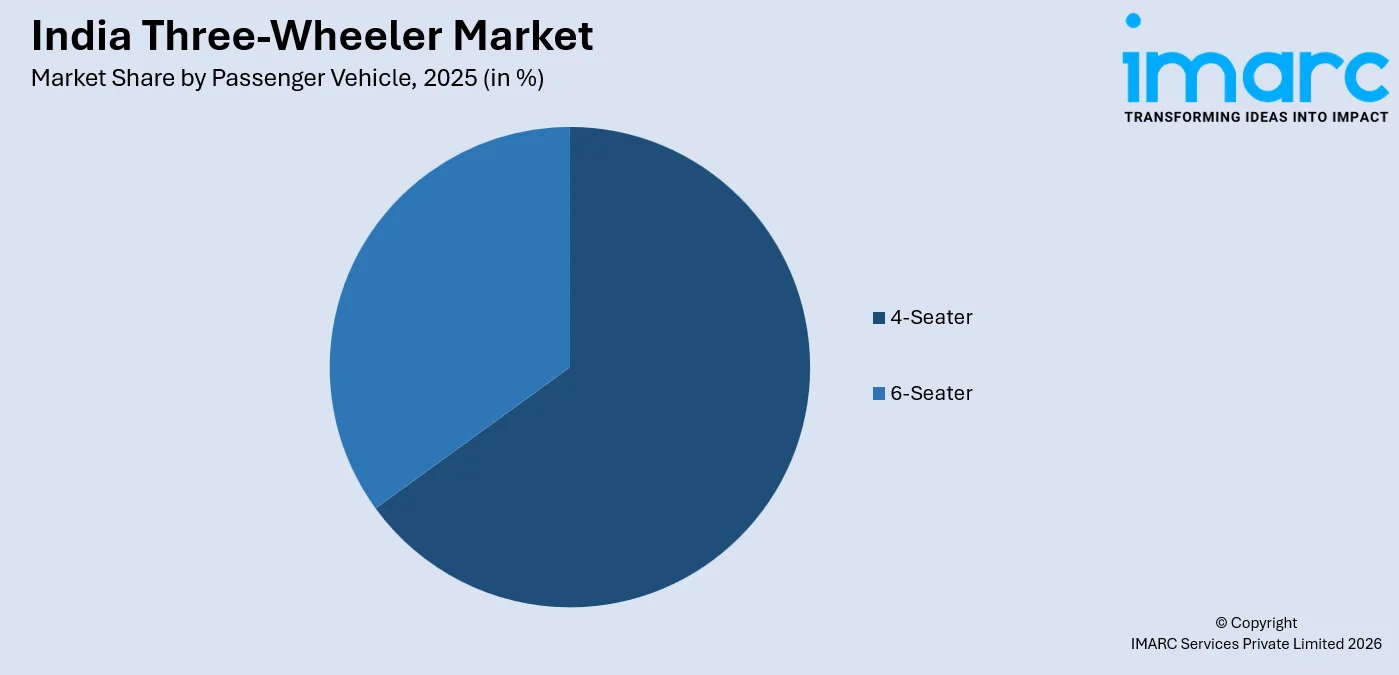

- 4-Seater commands 65.0% of passenger vehicle in 2025 - the standard auto-rickshaw configuration dominates overwhelmingly. The 6-seater maxicab variant is a niche, primarily concentrated in a handful of southern and eastern states.

- Petrol/CNG holds 55.0% of fuel type in 2025 - CNG remains the default in major northern cities where gas infrastructure is mature. Yet the gap with the electric sub-segment is narrowing faster than in any prior period.

- North India leads regionally at 32.0% in 2025 - a meaningful lead over other zones, anchored by UP's massive e-rickshaw base and Delhi-NCR's dense CNG auto fleet. Policy density in this region is structurally higher than anywhere else.

India Three-Wheeler Market Trends and Dynamic 2026

Market Trends

Electrification is accelerating into mainstream volumes

India's three-wheeler electrification has moved decisively past early-adopter boundaries. 53.61% of new three-wheeler vehicles sold were electric in 2024. The PM E-DRIVE scheme's ₹857 crore L5 allocation was exhausted three months ahead of its March 2026 deadline, signalling demand that outpaced government projections.

Passenger carrier sub-segment posting consecutive record quarters

SIAM data shows that passenger carrier three-wheelers grew in Q2 2025–26 posted the highest-ever Q2 passenger carrier volumes at 2.29 lakh units with 9.8% growth. Fleet aggregators and ride-hailing platforms are scaling commercial deployments, strengthening the demand base that drives India three-wheeler market trends across urban and peri-urban corridors.

Export momentum building as 'Made in India' gains global traction

Three-wheeler export sales are 46,013 units in November 2025, compared to 23,439 units in November 2024, with 96.3% YoY. India's growing manufacturing competitiveness and an expanding export footprint are broadening revenue pools for Indian OEMs.

- Last-Mile Fleet Digitisation: Aggregators integrating telematics, battery-state monitoring, and pay-per-km contracts are reshaping commercial deployment models for electric three-wheelers.

- Battery-Swap Ecosystem Growth: Fixed-route operators in tier-2 cities are adopting swappable battery architectures to eliminate downtime and reduce upfront vehicle cost.

- Multi-Fuel Architecture Strategies: Leading OEMs are maintaining parallel CNG and electric portfolios, targeting different customer economics across tier-1 and tier-3 geographies.

- Platform Consolidation Among OEMs: Companies like Atul Auto have merged their EV divisions with parent entities to sharpen balance sheet focus and unify go-to-market strategy.

Growth Drivers

Rapid urbanisation and persistent demand for shared mobility

India's urban population continues to swell, amplifying first- and last-mile transit gaps that auto-rickshaws are uniquely positioned to fill. Three-wheelers account for 10–20% of daily motorised trips across Indian cities. This structural role in urban transport networks sustains baseline demand and drives India three-wheeler market growth even through macroeconomic volatility.

Supportive government policy and production-linked incentives

The PM E-DRIVE scheme allocated ₹10,900 crore nationally to accelerate EV deployment across categories. For three-wheelers, 2,54,676 L5 units were supported by November 2025, and this number rose to 2,85,931 units by December 2025 against a target of 2,88,809 units, demonstrating policy effectiveness.

Lower operating costs of electric powertrains versus ICE variants

Electric three-wheelers offer per-kilometre running costs of ₹0.50–0.70 against ₹3–4 for petrol or ICE vehicles. In April 2025, the government also hiked excise duty on petrol and diesel by ₹2 per litre each, further widening the cost gap. For owner-drivers operating on thin margins in tier-2 and tier-3 towns, this operational economics case becomes a primary purchase trigger.

- Rising E-Commerce and Last-Mile Delivery Demand: Surge in quick-commerce and D2C shipments is expanding the goods-carrier three-wheeler segment, drawing investment from logistics majors.

- Expanding CNG Infrastructure in Tier-2 Cities: City Gas Distribution network additions across states like UP, Rajasthan, and Madhya Pradesh are sustaining demand for CNG-powered passenger carriers.

- Income Tax Reforms and Improved Financing Access: The Union Budget 2025–26 personal income tax revisions and back-to-back RBI rate cuts are improving loan affordability for three-wheeler buyers.

- Tourism and Hospitality Sector Recovery: Growth in domestic tourism is increasing demand for passenger three-wheelers in heritage towns, pilgrimage hubs, and hill station precincts across India.

Market Restraints

Fragmented regulatory landscape across states: Three-wheeler permit systems, fare regulations, and EV incentive structures differ substantially across India's states and union territories, creating compliance complexity and uneven market access. This patchwork regulatory environment increases operational costs for fleet operators expanding into new geographies.

High upfront cost of electric three-wheelers relative to income levels: Despite falling component costs, the acquisition price of electric three-wheelers remains out of reach for a significant portion of prospective owner-drivers without adequate financing support. Credit availability in semi-urban and rural markets remains constrained, limiting adoption among the most price-sensitive buyer segments.

Infrastructure gaps in charging and battery servicing: Charging and battery-swapping infrastructure remains concentrated in tier-1 cities, leaving tier-2, tier-3, and rural areas underserved. For drivers in these areas, range anxiety and access to quality servicing continue to delay transitions from conventional fuel variants to electric alternatives.

India Three-Wheeler Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Vehicle Type | Passenger Carrier | 68.0% | 2025 |

| Passenger Vehicle | 4-Seater | 65.0% | 2025 |

| Fuel Type | Petrol/CNG | 55.0% | 2025 |

| Region | North India | 32.0% | 2025 |

Vehicle Type Insights

Passenger Carrier - 68.0% Market Share (2025) | Leading Vehicle Type

Passenger carriers dominate the India three-wheeler market by a wide margin, reflecting the country's enduring dependence on auto-rickshaws for urban and peri-urban shared transport. SIAM data confirms passenger carrier three-wheelers recorded 30.43% year-on-year growth to 60,881 units in January 2026, continuing a multi-quarter streak of record-setting performance that underlines the segment's structural importance.

|

Segment Breakdown Passenger Carrier (68.0%) · Load Carrier |

Passenger Vehicle Insights

Access the comprehensive market breakdown Request Sample

4-Seater - 65.0% Market Share (2025) | Leading Passenger Vehicle

The 4-seater configuration, the classic three-wheeled auto-rickshaw accommodating up to three passengers, dominates the passenger vehicle segment. Its dominance is structurally entrenched in urban permit frameworks, which typically cap capacity at this level for intra-city auto routes. Bajaj Auto's RE and Maxima C models, among the best-selling variants, are engineered specifically around this seating standard.

|

Segment Breakdown 4-Seater (65.0%) · 6-Seater |

Fuel Type Insights

Petrol/CNG - 55.0% Market Share (2025) | Leading Fuel Type

Petrol and CNG-powered three-wheelers collectively hold the leading fuel type share, sustained by India's mature CNG distribution infrastructure in major cities. Delhi alone operates one of the world's largest CNG vehicle fleets, with over one lakh auto-rickshaws mandated to run on CNG under longstanding Supreme Court directives. Bajaj Auto's multi-fuel strategy, maintaining CNG product lines while simultaneously launching electric variants, reflects OEM confidence that this segment retains material volume in the near term.

|

Segment Breakdown Petrol/CNG (55.0%) · Diesel · Electric |

Regional Insights

North India – 32.0% Market Share (2025) | Leading Region

North India leads all regions in three-wheeler demand, anchored by the twin pillars of Uttar Pradesh's massive e-rickshaw base and Delhi-NCR's regulated CNG auto fleet. Uttar Pradesh contributed 38% of national electric three-wheeler sales in 2024, recording 2,66,106 units. This concentration reflects the region's high per-capita dependence on shared three-wheeled transport, dense urban-rural fringe activity, and a maturing dealership network, factors that collectively shape the India three-wheeler market outlook for the region.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

32.0%

|

|

Key States

|

Delhi, Uttar Pradesh, Haryana, Punjab, Rajasthan, Uttarakhand, Himachal Pradesh |

|

Major Growth Drivers

|

Dense urban population, mature CNG infrastructure, strong state-level EV incentives, last-mile metro connectivity demand |

|

Outlook

|

Sustained regional leader with accelerating EV shift |

|

Regional Breakdown North India (32.0%) · South India · East India · West India |

South India:

South India is the second-largest regional market, driven by strong tourism infrastructure in Kerala and Karnataka, as well as dense auto-rickshaw usage in Bengaluru and Hyderabad. In September 2025, TVS Motor signed an MoU with ALT Mobility to deploy up to 3,000 electric three-wheelers in FY26, a partnership anchored by TVS's manufacturing base in Hosur, Tamil Nadu.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Tamil Nadu, Karnataka, Kerala, Andhra Pradesh, Telangana |

|

Major Growth Drivers

|

Tourism-driven passenger demand, IT corridor last-mile connectivity, EV manufacturing proximity |

|

Outlook

|

Strong EV uptake supported by OEM proximity |

East India:

East India, encompassing Bihar, West Bengal, Jharkhand, and Odisha, is a significant growth market for electric three-wheelers driven by dense rural-urban fringe populations and very high daily dependence on affordable shared transit. Bihar registered 89,683 electric three-wheeler units and a 13% share in 2024, the second-highest among states nationally, underscoring this region's importance to overall market volumes.

|

Metric

|

Details

|

|---|---|

|

Key States

|

West Bengal, Bihar, Jharkhand, Odisha |

|

Major Growth Drivers

|

High rural-urban transit dependence, growing organised EV market, e-rickshaw proliferation |

|

Outlook

|

High-volume e-rickshaw and passenger carrier growth |

West India:

Maharashtra and Gujarat are the primary demand centres in West India, with Pune and Aurangabad hosting major three-wheeler manufacturing clusters for Bajaj Auto and Piaggio. Maharashtra offers road-tax waivers and purchase rebates that stack with central PM E-DRIVE benefits, making electric three-wheelers particularly price-competitive at the point of sale.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Maharashtra, Gujarat, Goa |

|

Major Growth Drivers

|

Manufacturing cluster proximity, state EV incentives, metro last-mile demand |

|

Outlook

|

Premium and EV variant growth driven by urban demand |

Market Outlook 2026-2034

What is the future outlook of the India three-wheeler market?

The India three-wheeler market is expected to sustain steady revenue growth through 2034.

Sustained urbanisation, ongoing income growth among India's working population, and deepening EV penetration across fuel-type segments will collectively underpin market expansion. The transition from CNG to electric powertrains is expected to accelerate as state policies align with central EV roadmaps, newer battery architectures lower acquisition costs further, and fleet operators increasingly favour electric variants for superior operating economics. Export demand from Africa and the MENA regions will amplify OEM revenue growth beyond India's domestic volumes, positioning the market for a strong and balanced India three-wheeler market forecast through the end of the decade.

India Three-Wheeler Market - Leading Key Players

The India three-wheeler market is led by a concentrated group of established OEMs that collectively account for the large majority of domestic sales and exports. These players compete across ICE, CNG, and electric sub-segments, deploying multi-fuel architectures, dealership network expansion, and government-incentive-eligible product lines to consolidate share in a rapidly evolving competitive landscape.

| Company | Leading Brands | Highlights |

|---|---|---|

| Bajaj Auto Limited | RE, Maxima C, Maxima Z, GoGo, WEGO, Riki | World's largest three-wheeler manufacturer, 44,980 units sold in January 2026 (+13.9% YoY). |

| Piaggio Vehicles Private Limited | Ape Xtra LDX, Ape Xtra Bada 700, Ape Xtra 600 | Investing in new weight-optimised three-wheeler architecture for both EV and ICE models, expanding domestic network to 250-300 touchpoints by the end of FY26, exporting to Africa and Sri Lanka |

| Mahindra Last Mile Mobility Limited | Treo, Zor Grand, E-Alfa Cargo, UDO Electric Auto | Holds 37.6% YTD FY26 L5 EV segment share, 8,227 units sold in January 2026 |

Some of the key market players in India three-wheeler market are TVS Motor Company Limited, Atul Auto Limited, Dilli Electric Auto, Saera Electric Auto, etc.

Latest Development & News

- In February 2026, Bajaj Auto launched the WEGO P9018, positioning it as India's largest electric three-wheeler with a 296 km certified range. The vehicle features an upgraded Battery Management System and enhanced regenerative braking, targeting urban, semi-urban, and rural markets that require large-capacity three-wheelers with extended range capabilities.

- In January 2026, Atul Auto Limited announced that its Board of Directors approved the acquisition of the L5 electric three-wheeler vehicle business from Atul Greentech Private Limited (AGPL). The deal, valued at Rs 3,526 lakh (around Rs 35.26 crore), will be carried out through a slump sale on a going-concern basis.

- In September 2025, TVS Motor Company signed a Memorandum of Understanding with ALT Mobility to lease up to 3,000 electric passenger and cargo three-wheelers in FY26 under pay-per-kilometre contracts that bundle insurance and maintenance. The asset-light model is designed to accelerate electric fleet adoption among operators who cannot afford outright EV purchases.

India Three-Wheeler Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Passenger Carrier, Load Carrier |

| Passenger Vehicles Covered | 4-Seater, 6-Seater |

| Fuel Types Covered | Petrol/CNG, Diesel, Electric |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India three-wheeler market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India three-wheeler market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India three-wheeler industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Three-Wheeler Market Report

The India three-wheeler market was valued at USD 410.29 Million in 2025.

The India three-wheeler market is anticipated to reach a value of USD 831.33 Million by 2034.

Passenger carrier dominates the market with a share of 68.0%, reflecting India's high dependence on auto-rickshaws for intra-city last-mile passenger transport across hundreds of urban and peri-urban centres nationwide.

4-seater commands the market with a share of 65.0%, driven by permit frameworks in major cities that restrict intra-city commercial auto operations to this standard configuration, making it the default choice for most operators and fleet buyers.

Petrol/CNG leads the market with 55.0%, CNG remains the default in major northern cities where gas infrastructure is mature. Yet the gap with the electric sub-segment is narrowing faster than in any prior period.

North India currently leads the India three-wheeler market, accounting for a share of 32.0%. The region benefits from the highest density of shared transit dependence, an advanced CNG infrastructure, strong state-level EV incentive programmes, and a growing base of electric three-wheeler fleet operators.

Some of the major players in the India three-wheeler market include Bajaj Auto Limited, Piaggio Vehicles Private Limited, Mahindra Last Mile Mobility Limited, TVS Motor Company Limited, Atul Auto Limited, etc.

Key trends include rapid adoption of electric powertrain architectures driven by improving battery economics, growing deployment of fleet-as-a-service and battery-swap models, expanding export volumes to Africa and ASEAN markets, and increasing telematics integration enabling real-time fleet management for commercial operators.

Key growth drivers include India's accelerating urbanisation that widens last-mile transit demand, per-kilometre cost advantages of electric variants over petrol and CNG alternatives, expanding CNG city gas distribution networks in tier-2 cities, and rising e-commerce volumes that are creating sustained demand for goods-carrier three-wheelers.

Key challenges include fragmented state-level permit and regulatory frameworks that increase compliance costs for fleet operators, the high upfront acquisition price of electric three-wheelers limiting rural buyer access, insufficient charging and battery-swapping infrastructure in tier-3 and rural areas, and supply chain volatility in battery-grade lithium and cobalt components that can elevate manufacturing costs for EV-focused OEMs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)